Articles

Elie Roth, Tim Youdan, Chris Anderson, Kim Brown, "Taxation of Trusts Resident in Canada", Chapter 3 of Canadian Taxation of Trusts, (Canadian Tax Foundation), 2016.

Under-the-will requirement where varied (p. 173)

It is the CRAs view that a trust is not created under a taxpayer's will when the trust is created...

Subsection 248(2) - Tax payable

Cases

R. v. Simmons, 84 DTC 6171 (Nfld. Prov. Ct.)

"[O]n the point raised by Mr. Sopinka that the charges were premature ... I will follow the Myers case (R. v. Myers and Inter Publishing Co. Ltd.,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 244 - Subsection 244(4) | 37 |

Subsection 248(3) - Property subject to certain Quebec institutions and arrangements

Cases

Canada v. Construction Bérou Inc., 99 D.T.C 5869 (FCA)

Létourneau J.A. found (at p. 5872) that s. 248(3) "is intended to treat beneficial ownership of property in the same way as various forms of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 13 - Subsection 13(21) - Undepreciated Capital Cost - A | lessee had acquired the 3 incidents of ownership | 236 |

| Tax Topics - Statutory Interpretation - Provincial Law | 61 |

Administrative Policy

7 October 2020 APFF Roundtable Q. 5, 2020-0852171C6 F - Usufruct of a principal residence

A housing unit is subject to a usufruct created by the Quebec will of Mr. X, with Mr. X’s surviving spouse (Ms. X) being the usufructuary, and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Principal Residence - Paragraph (c.1) | a deemed s. 248(3) testamentary usufruct trust might access the principal residence exemption on the spousal usufructuary’s death or on her surrendering her interest | 409 |

| Tax Topics - Income Tax Act - Section 107 - Subsection 107(4) | application of s. 107(4) to termination of deemed s. 248(3)(a) spousal trust | 472 |

| Tax Topics - Income Tax Act - Section 70 - Subsection 70(6) - Paragraph 70(6)(b) - Subparagraph 70(6)(b)(ii) | s. 70(6)(b)(ii) not satisfied where residence of deceased passes to a usufruct for his surviving spouse for a fixed term of years | 218 |

13 April 2015 External T.I. 2012-0449141E5 F - Usufruct

A corporation sold the usufruct respecting a property to an arm’s length third party for use as a secondary residence, while retaining the bare...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(2) | 75(2) applies to termination of usufruct | 174 |

| Tax Topics - Income Tax Act - Section 107 - Subsection 107(2.1) | 107(2.1) application to termination of usufruct created for valuable consideration | 126 |

22 May 2014 External T.I. 2014-0519811E5 F - Droit d'usage au Québec pré-1991

Before going on to find that the usufructuary of duplex unit (acquired before 1991) was entitled to claim the principal residence exemption on a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Principal Residence | usufructuary of duplex unit (with her right acquired pre-1991) entitled to claim principal residence exemption on post-1991 disposition | 167 |

| Tax Topics - General Concepts - Ownership | usufructuary of duplex unit was de facto owner thereof | 71 |

5 October 2012 APFF Roundtable, 2012-0451281C6 F - Usufruit étranger

Respecting the creation of a usufruct under the French Civil Code, CRA stated:

Where a usufruct is not governed by the laws of Quebec, subsection...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | whether the formation of a usufruct under overseas law triggers a disposition turns on such law | 135 |

17 August 2010 External T.I. 2010-0367371E5 F - Fin d'un usufruit - résidence principale

An individual purchased a housing unit for which he established a usufruct in favour of his parents. At all relevant times, the individual owned...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Principal Residence - Paragraph (a.1) | usufructuary parents were specified beneficiaries based on their inhabiting the housing unit | 287 |

| Tax Topics - Income Tax Act - Section 107 - Subsection 107(2.01) | deemed s. 248(3) trust that dissolved when the usufructuary parents renounced their, makes a s. 107(2.01) or (2.001) to apply principal residence exemption to dissolution gain | 287 |

27 May 2009 Internal T.I. 2009-0310751I7 F - Usufruit d'un immeuble avant 1991

In 1985, an individual sold a building to his children on which he had reserved for himself, under the deed of sale, the right of usufruct or...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Principal Residence | usufructuary under usufruct created prior to 1991 was beneficial owner on his death in 2007 for principal residence exemption purposes | 48 |

13 September 2007 External T.I. 2006-0214631E5 F - Déboursé pour usufruit ou droit d'usage

A taxpayer sold, to an arm’s length farm corporation, the usufruct or right of use for the use of land together with the buildings thereon for a...

13 July 2004 External T.I. 2004-0058141E5 F - Transfert du droit aux revenus provenant d'un bien

Monsieur and Madam will transfer, to their jointly-owned corporation, the right to receive the income from a rental property for a specified...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) | rollover not available to assignment of the rents from a rental property to a corporation for shares since the transferee was a deemed trust under s. 248(3) | 68 |

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(2) | s. 75(2) applicable to assignment of the rents from a rental property to a corporation giving rise to a deemed trust under s. 248(3) | 93 |

1 August 2003 Internal T.I. 2003-0009697 F - Usufruit et amortissement

In 1990, an individual died and bequeathed the usufruct of an immovable to a friend. CCRA noted that if the required transitional election had...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 1102 - Subsection 1102(1) - Paragraph 1102(1)(c) | bare owner not entitled to claim CCA on property even if s. 248(3) does not apply | 65 |

28 June 2001 External T.I. 2001-0069865 F - CRÉDIT-BAIL

In connection with finding that cancelled IT-233R and Construction Bérou should not be followed in considering a taxpayer to have acquired...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 13 - Subsection 13(21) - Undepreciated Capital Cost - A | Construction Bérou should not be followed in finding that a lessee can be the tax owner of the leased property | 50 |

10 May 2001 External T.I. 2001-0066095 F - CREDIT-BAIL

In the course of indicating that it would not follow the interpretation given to s, 248(3) in Construction Bérou, CCRA stated:

The Federal Court...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 13 - Subsection 13(21) - Undepreciated Capital Cost - A | following Shell, CCRA will only recharacterize a lease where the true legal relationship is not of a lease | 134 |

8 March 2001 External T.I. 2000-0048405 F - Usufruit sur immeuble en France

CCRA indicated that the bare owner who created a usufruct under French law respecting an immovable in France would not be taxed on the rental...

23 June 1999 External T.I. 9830985 F - USUFRUIT VS FIDUCIE AU CONJOINT AVANT 72

The taxpayers' will provided for the testator’s assets to go to a surviving spouse for life, but stipulated that, as regards 2/3 of the assets,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 108 - Subsection 108(1) - Pre-1972 Spousal Trust | encroachment on the capital that occurred when spouse remarried disqualified the trust from being a "pre-1972 spousal trust" | 100 |

Paragraph 248(3)(a)

Administrative Policy

20 April 2017 External T.I. 2016-0672501E5 F - Usufruct and Use of capital of a trust by a spouse

The will of the Quebec deceased bequeathed the usufruct of rental property to his spouse and the bare ownership to his adult child, thereby giving...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 70 - Subsection 70(6) - Paragraph 70(6)(b) - Subparagraph 70(6)(b)(ii) | right of the bare owner of property, subject to a usufruct in favour of a surviving spouse, to dispose of his bare ownership does not preclude a spousal trust | 151 |

11 March 2013 External T.I. 2012-0432201E5 F - Payment of tax by an institute

An individual bequeaths property by way of substitution to the individual’s surviving spouse, with the property remaining on the spouse’s...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 108 - Subsection 108(1) - Testamentary Trust - Paragraph (d) | spousal beneficiary of substitution by testament does not taint the resulting deemed testamentary trust by paying the trust taxes | 283 |

12 January 2012 External T.I. 2011-0421791E5 F - Usufruit de terres boisées acquises avant 1987

Father, a retired person, who acquired woodlands from his father before 1987 gifts the bare ownership of the woodlands to his Child, while...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110.6 - Subsection 110.6(1.3) - Paragraph 110.6(1.3)(c) | property acquired before 18 June 1987 will qualify if s. 110.6(1.3)(c)(i) or (ii) satisfied | 240 |

11 April 2005 External T.I. 2004-0091721E5 F - Usufruit d'un bien immeuble situé en France

A resident of Canada gifted to his daughter, also resident in Canada, the bare ownership of an income property located in France, while retaining...

Paragraph 248(3)(c)

Administrative Policy

5 January 2007 External T.I. 2005-0133321E5 F - Validité d'un REER

A Quebec RRSP formed before 2010 was still valid following the Bank Nova Scotia v. Thibault, 2004 S.C.C. 29 decision, notwithstanding that it was...

Paragraph 248(3)(e)

Administrative Policy

15 December 2003 External T.I. 2003-0182855 - Fiducie pour Loi au Quebec

Regarding the satisfaction by an individual that a transfer of property to a self-benefit trust established under Quebec law for that individual...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 73 - Subsection 73(1.02) - Paragraph 73(1.02)(b) - Subparagraph 73(1.02)(b)(ii) | no change in beneficial ownership on transfer of property to self-benefit Quebec trust | 171 |

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(2) | policy is for s. 75(2) application not to result in double taxation | 118 |

| Tax Topics - General Concepts - Ownership | sole beneficiary of Quebec trust is the beneficial owner of its property | 273 |

4 April 2002 External T.I. 2001-0103735 F - Fiducie exclusive au conjoint et ass.-vie

A spousal trust for the widow (Ms. A) of Mr. A held shares of Opco which, in turn, was the owner and beneficiary of a policy that became payable...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110.6 - Subsection 110.6(14) - Paragraph 110.6(14)(g) | s. 110.6(14)(g) inapplicable to shares held by spousal trust on the spouse’s death | 90 |

| Tax Topics - Income Tax Act - Section 110.6 - Subsection 110.6(15) - Paragraph 110.6(15)(a) | the spouse beneficiary of a Quebec spousal trust owns the shares owned by that trust | 199 |

| Tax Topics - Income Tax Act - Section 70 - Subsection 70(5.3) | s. 70(5.3) applicable to s. 104(4)(a)(i) disposition | 75 |

Subsection 248(4) - Interest in real property

See Also

Re Redmond et al. and Rothschild, [1971] 1 O.R. 436 (Ont. CA)

At the relevant time, the predecessor version of s. 50(2)(b) (i.e., s. 26(1)(b)) of the Planning Act (Ontario), which prohibited an unauthorized...

Administrative Policy

16 March 2015 Internal T.I. 2013-0479861I7 - Section 116 & forfeited deposits on real property

A non-resident vendor received a deposit under an agreement for sale of B.C. real property, which will be forfeited to it due to failure of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 116 - Subsection 116(5) | forfeited sale deposit was proceeds of security interest rather than of tcp | 264 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition - Paragraph (b) | forfeited sale deposit was proceeds | 79 |

13 September 2012 CICA Compliance Roundtable, 2012-0453021C6 - Taxable Canadian Property

Respecting a question as to whether shares of an unlisted corporation would be taxable Canadian property if during the preceding 60 months "most...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Taxable Canadian Property - Paragraph (d) | mortgages not tcp | 164 |

2001 Ruling 2001-0083883 - QUALIFIED INVST RRSP RRIF RESP DPSP

A mortgage bond secured by a leasehold interest in land would constitute a mortgage secured by real property situated in Canada in light of s....

18 January 1993 External T.I. 5-921718

A three-year second mortgage loan, bearing interest at 11% per annum, made by a non-resident to a Canadian partnership provided that on maturity...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Taxpayer | 103 |

December 1990 TI 1990-240

In light of s. 248(4), leasehold improvements to a leasehold interest would, if rented, be considered to give rise to income from real property...

15 January 1987 TI 7-1282

Although s. 248(4) deem leases (in this case grazing leases on Crown lands) to be interest in real property, the definition of qualified farm...

Subsection 248(5) - Substituted property

Cases

Canada v. Sommerer, 2012 DTC 5126, 2012 FCA 207

In determining whether s. 75(2) should apply to the taxpayer, Sharlow J.A. stated (at para. 46):

This provision must be read together with...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(1) | Austrian foundation likely not a trust | 181 |

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(2) | does not apply to FMV purchases | 236 |

| Tax Topics - Treaties - Income Tax Conventions | treaty applies to economic double taxation | 356 |

| Tax Topics - Treaties - Income Tax Conventions - Article 13 | attributed gain not included | 415 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | s. 75(2) should not be applied to attribute the same gain to 2 taxpayers | 115 |

See Also

St-Pierre c. La Reine, 2008 DTC 3730, 2007 TCC 90

The taxpayer transferred shares of a corporation ("3101") to a management company controlled by him and the management company disposed of a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 74.2 - Subsection 74.2(1) | 118 |

Administrative Policy

15 June 2021 STEP Roundtable Q. 5, 2021-0883001C6 - Income Attribution from AET

How would s. 75(2) apply where proceeds or income of property of an alter ego trust that had been contributed by the settlor was reinvested?

CRA...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(2) | "second generation income" is not subject to s. 75(2) attribution | 453 |

| Tax Topics - Income Tax Act - Section 82 - Subsection 82(2) | application of s. 82(2) where s. 75(2) applies to dividend income allocated by a partnership | 125 |

22 June 2016 Internal T.I. 2016-0632821I7 F - 93(2.01) & Capital Contribution

Canco contributed (for no share consideration) its shares of a non-resident Finco subsidiary (Luxco2 – which previously had paid exempt...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 93 - Subsection 93(2.01) | a contribution of FA1 shares to FA2 causes the FA2 shares to be substituted property for s. 93(2.01) purposes | 195 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(a) - Subparagraph 95(2)(a)(ii) - Clause 95(2)(a)(ii)(B) | inter-affiliate loan generating deemed active business funded out of an interest-free loan from Canco | 105 |

25 September 2013 Internal T.I. 2013-0476311I7 F - 93(2), 93(2.01) - Share substituted

In the course of reviewing the facts summarized under s. 93(2.01), CRA stated (TaxInterpretations translation):

Subsection 248(5) provides rules...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 93 - Subsection 93(2.01) | concept of substituted share in s. 93(2.01) is subject to the exchanged-for limitation in s. 248(5)(a) | 1304 |

10 May 2013 Internal T.I. 2012-0464901I7 - 93(2), 93(2.01) - Share substituted

Canco owns all the shares of Forco1, which it transfers to Forco2 for a promissory note payable in U.S. dollars, and then transfers the note to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 93 - Subsection 93(2.01) | 72 |

15 February 2006 External T.I. 2005-0126831E5 F - 120.4(1) - définition : montant exclu

In finding that income from shares acquired by a minor child from money received as a consequence of the death of a parent was not excluded under...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 120.4 - Subsection 120.4(1) - Excluded Amount - Paragraph (a) | para. (a) exclusion does not apply to substituted property | 128 |

6 April 1992 T.I. 920265 (March 1993 Access Letter, p. 71 ¶C56-218; Tax Window, No. 18, p. 1, ¶1852)

Where, in 1978, a taxpayer transferred property to his spouse who, in turn, transferred the property to a holding company for preferred shares and...

15 January 1992 T.I. (Tax Window, No. 15, p. 12, ¶1700)

Where a minor son received shares from his father on a rollover basis pursuant to former s. 73(5), realizes an exempt capital gain on a later...

Paragraph 248(5)(a)

Paragraph 248(5)(b)

Administrative Policy

2023 Ruling 2020-0862441R3 - Charitable donation by Estate

S. 118.1(5.1)(b) requires that in order for a gift to be deemed to be one made by the deceased rather than the estate, it must be a gift of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(5.1) - Paragraph 118.1(5.1)(b) | cash extracted from an estate subsidiary can be rendered substituted property for s. 118.1(5.1)(b) purposes by having such cash paid as redemption proceeds | 536 |

13 January 2005 External T.I. 2004-0101701E5 F - Bien substitué

In finding that the provisions of s. 7(1.1) would not apply to shares received as a stock dividend on shares that had been acquired on the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Interpretation/Definition Provisions | deeming provision only engaged when the referenced term is used | 64 |

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(1.1) | s. 248(5)(b) inapplicable to s. 7(1.1) | 35 |

23 September 2004 External T.I. 2004-0088801E5 F - Stop-Loss Provisions -- Grandfathering

Grandfathering regarding the stop-loss rule in s. 112(3.2), which turned on the shares being considered to have been held by an individual...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 112 - Subsection 112(3.2) | s. 248(5)(b) did not deem stock dividend shares to be the same shares as those on which the dividend was paid for transitional relief purposes | 174 |

Subsection 248(6) - “Class” of shares issued in series

See Also

Bowater Canadian Ltd. v. R.L. Crain Inc. (1987), 62 OR (2d) 752 (C.A.)

The articles of amalgamation of the corporation provided for common shares, and for "special common shares" which were entitled to ten votes per...

Administrative Policy

7 October 2020 APFF Roundtable Q. 7, 2020-0852191C6 F - Capital dividend and series of shares

In finding that capital dividends potentially could be paid on one series of a class and not the other, CRA stated:

Under subsection 248(6), where...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 83 - Subsection 83(2) | capital dividends can be paid on one series and not the other | 235 |

| Tax Topics - Income Tax Act - Section 83 - Subsection 83(2.1) | s. 83(2.1) “should be considered” where one of the main purposes of a reorganization is to stream capital dividends | 141 |

Subsection 248(7) - Receipt of things mailed

Cases

Lauzon v. Canada (Revenue Agency), 2021 FC 431

The taxpayer alleged that he had not received cheques for refunds claimed in his returns for his 2005 and 2006 taxation years, which CRA’s...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Unjust Enrichment | rejection of an unjust enrichment claim by a taxpayer claiming he had not received refund cheques | 334 |

See Also

Canada v. Schafer, 2000 DTC 6542 (FCA)

A notice of assessment that the trial judge found the respondent had never received was deemed by s. 334(1) of the ETA to have been received by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 301 - Subsection 301(1.1) | 52 | |

| Tax Topics - Excise Tax Act - Section 334 - Subsection 334(1) | 95 | |

| Tax Topics - Statutory Interpretation - Interpretation/Definition Provisions | "deems" is irrebuttable | 68 |

| Tax Topics - Statutory Interpretation - Resolving Ambiguity | 57 |

Sameden Oil of Canada, Inc. v. Provincial Treasurer of Alberta (1993), 102 DLR (4th) 125 (Alta. C.A.)

The taxpayer mailed his 1988 corporate tax return by registered mail from the United States on June 30, 1989, and the return was received by the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Interpretation Act - Subsection 45(2) | 88 |

Rolling v. Willann Investments Ltd. (1989), 63 DLR (4th) 760 (Ont CA)

An offer was considered to have been "delivered" to a person ("Willann") when it was faxed to Willann:

"Where technological advances had been made...

Administrative Policy

May 2019 CPA Alberta CRA Roundtable, General Session – Q.4

After referring to s. 248(7), the questioner asked when a return is considered delivered to CRA by Canada Post’s Expedited Parcel service. CRA...

Paragraph 248(7)(a)

See Also

Morgan v. The King, 2025 TCC 36 (Informal Procedure)

For the purposes of applying ETA s. 334(1) (similar to ITA s. 248(7)(a)), Yuan J refused to accept a CRA administrative presumption that an...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Regulations - New Harmonized Value-Added Tax System Regulations, No. 2 - Section 46 - Subsection 46(6) - Paragraph 46(6)(a) | evidence of taxpayer’s accountant accepted as to when she mailed the rebate application | 365 |

| Tax Topics - Excise Tax Act - Section 334 - Subsection 334(1) | application was mailed about a month before it was stamped as received by the CRA mailroom | 259 |

| Tax Topics - Excise Tax Act - Section 256 - Subsection 256(2) | substantial completion of home renovation occurred on municipal inspection approval | 196 |

Subsection 248(8) - Occurrences as a consequence of death

Articles

Elie Roth, Tim Youdan, Chris Anderson, Kim Brown, "Taxation of Trusts Resident in Canada", Chapter 3 of Canadian Taxation of Trusts, (Canadian Tax Foundation), 2016.

Effect of disclaimer or release (pp. 177-8)

Under the common law, a disclaimer means a refusal to accept a gift or other transfer of property....

Paragraph 248(8)(a)

See Also

Bueti v. The Queen, 2015 DTC 1213 [at at 1374], 2015 TCC 265

Owen J made a factual finding that a particular property (a house in the estate of the taxpayer's father) was purchased for cash consideration by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Ownership | residuary beneficiary had no ownership of estate property | 118 |

| Tax Topics - Income Tax Act - Section 70 - Subsection 70(5) | residuary beneficiary did not acquire as a consequence of death | 250 |

Husel Estate v. The Queen, 94 DTC 1765, [1995] 1 CTC 2298 (TCC)

Kempo TCJ. found (at p. 1769) that s. 248(8)(a) was added "to obviate the denial of a rollover in situations where an individual, qua beneficiary,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 70 - Subsection 70(6) | 51 |

Administrative Policy

7 October 2020 APFF Financial Strategies and Instruments Roundtable Q. 5, 2020-0851601C6 F - TFSA Exempt Contribution - Spousal Trust

The TFSA rules contemplate that the surviving spouse of a deceased TFSA holder can make an “exempt contribution” of the payment to him or her...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 207.01 - Subsection 207.01(1) - Exempt Contribution - Paragraph (b) | bequest of TFSA to spousal trust which, in turn, distributed the TFSA proceeds per the will to the surviving spouse would qualify as an indirect transfer as a consequence of death | 500 |

6 June 2017 External T.I. 2015-0617331E5 F - TFSA - Exempt Contribution

CRA indicated, similarly to 2016-0679751E5 F, that in light inter alia of s. 248(8)(a), a payment could be considered to be made to a surviving...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 207.01 - Subsection 207.01(1) - Exempt Contribution - Paragraph (b) | payment of family-law debt out of TFSA to surviving spouse would occur as a consequence of the deceased’s death | 316 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(23.1) - Paragraph 248(23.1)(a) | payment of family-law obligation of deceased to surviving spouse out of deceased's TFSA could qualify | 84 |

11 May 2017 External T.I. 2016-0679751E5 F - TFSA - Exempt Contribution

The definition of “survivor payment” in s. 207.01(1) - exempt contribution – para. (b) references a payment to the survivor directly or...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 207.01 - Subsection 207.01(1) - Exempt Contribution - Paragraph (b) | a “survivor payment” can be made out of the deceased’s TFSA even where this occurs in the executor’s discretion | 208 |

10 June 2016 STEP Roundtable Q. 10, 2016-0645781C6 - US Revocable Living Trusts

A U.S. resident (the “grantor”) settles a “revocable living trust” with property including taxable Canadian property. The grantor: is the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(1) | U.S. revocable living trust is not a bare trust | 171 |

| Tax Topics - Income Tax Act - Section 70 - Subsection 70(5) | transfer to remainder beneficiary of a U.S. revocable living trust on death does not occur as a consequence of death | 126 |

16 December 2014 External T.I. 2014-0539841E5 F - Testamentary Trust

Would a trust created by will in favour of the child of the deceased (the "Child Trust") cease to qualify as a testamentary trust in the year of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 108 - Subsection 108(1) - Testamentary Trust | transfer from one testamentary trust to another pursuant to a will direction treated as a non-tainting contribution from the deceased | 152 |

12 June 2012 STEP CRA Roundtable, 2012-0442931C6 - 2012 STEP Question 8

In the situation where the estate trustees are instructed under the Will to set up a number of trusts from the residue of the estate, CRA...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 108 - Subsection 108(1) - Testamentary Trust | 42 |

11 January 2012 STEP Roundtable, 2011-0402291C6 - Subsection 248(8)-Intestacy-Transfer of Property

Where a taxpayer dies intestate, then provided the property of the deceased is distributed to the beneficiaries in accordance with the shares...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 60 - Paragraph 60(l) | 108 | |

| Tax Topics - Income Tax Act - Section 70 - Subsection 70(6) | non pro rata allocations to beneficiaries | 124 |

20 October 2009 External T.I. 2009-0328441E5 F - Fiducie testamentaire

Under the terms of a deceased person's will, all property is bequeathed in equal shares to the deceased’s children. The heirs, in order to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(2) | s. 75(2) would apply if heirs form a trust to provide for their sister out of the residue, with the remainder to them on her death | 173 |

6 October 2006 Roundtable, 2006-0197151C6 F - Acquisition selon convention entre actionnaires

A shareholders' agreement gives children the right to acquire the shares of a farm corporation for $1 after their father's death. If the children...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 70 - Subsection 70(9.2) | children’s exercise of a right in a shareholders’ agreement to acquire farmco shares that is triggered on their father’s death would not be a consequence of his death | 97 |

5 May 1995 External T.I. 9500985 - ASSUMPTION OF LIABILITIES

A transfer of shares of a private corporation made to the surviving spouse after her agreement to assume liabilities of the estate and provide...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 70 - Subsection 70(6) | 68 |

17 August 1994 External T.I. 9410535 - TRUSTS - "AS A CONSEQUENCE OF THE TAXPAYER'S DEATH"

A discretion accorded by the will to the executors to determine the particular assets to be distributed to the spouse or spousal trust of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 70 - Subsection 70(6) | 41 |

Articles

Hoffstein, Lee, "Restructuring the Will and the Testamentary Trust: Methods, Underlying Legal Principles and Tax Considerations", Estates and Trust Journal, Volume 13, 1993, p. 42.

Paragraph 248(8)(b)

Cases

Biderman v. The Queen, 2000 DTC 6149, 2001 FCA 269 (FCA)

The taxpayer, who had tax debts on his death, made an "informal" disclaimer of his beneficial interest under the estate of his wife five days...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | conduct subsequent to death inconsistent with disclaimer | 150 |

See Also

Lewski v Commissioner of Taxation, [2017] FCAFC 145

The Commissioner of Taxation denied a claimed loss carryforward of a trust which had declared a distribution of all its income for a particular...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Incurring of Expense | obligation to pay purchase price was incurred on agreement date rather than subsequent closing | 430 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(24) | an alternate resolution that the taxpayer was not entitled to an income distribution if Revenue denied a trust deduction made her entitlement contingent and non-includible | 374 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(13) | a trust income declaration that was subject to a tax contingency did not result in an income inclusion to the beneficiary | 149 |

| Tax Topics - General Concepts - Agency | knowledge of agent imputed to principal | 217 |

Ginsburg v. MNR, 92 DTC 1774, [1992] 2 CTC 2152 (TCC)

The taxpayer was entitled under the will of her late husband to all the income from the residue of his estate under a spousal trust, and received ...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(24) | income payable even before amount ascertained | 242 |

Sembaliuk v. Sembaliuk (1984), 43 R.F.L. (2d) 425 (Alta. C.A.)

"[A] disclaimer, being an avoidance of a gift, is not a conveyance of the property comprised in that gift."

Montreal Trust Co. v. Matthews, [1979] 3 WWR 621 (BCSC)

"A disclaimer can be made by deed, writing, under hand only or even as a result of contract, as any document is admissible so that evidence of...

Administrative Policy

11 October 2019 APFF Financial Strategies and Instruments Roundtable Q. 6, 2019-0813451C6 F - TFSA - Bequest and disclaimer

Although an individual made a specific bequest under his will of his TFSA to his adult daughter, she executed a written renunciation of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 207.01 - Subsection 207.01(1) - Exempt Contribution - Paragraph (b) | transfer of TFSA to surviving spouse because of daughter’s renunciation occurred as a consequence of the deceased’s death | 222 |

10 May 2006 External T.I. 2005-0162591E5 F - Renonciation à une succession: REER

Mr. A, who died intestate holding an unmatured RRSP and other assets, left his spouse ("Mrs. A") and two children as heirs. If the children...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 146 - Subsection 146(8.1) | renunciation by two children for the benefit of the other heir did not give rise to a transfer as a consequence of death | 183 |

10 April 1997 External T.I. 9706185 - "AS A CONSEQUENCE OF DEATH"

Where children surrender (as defined in s. 248(9)) their interest in an RRSP and the surviving spouse (their mother) thereby acquires an interest...

9 March 1992 T.I. (Tax Window, No. 17, p. 9, ¶1788)

Discussion of factors relevant to determining whether a transfer of rights under a will by a beneficiary is a true disclaimer, release or surrender.

8 March 1991 T.I. (Tax Window, No. 1, p. 21, ¶1152)

An election under the Family Law Act (Ontario) by a surviving spouse is a disclaimer for purposes of s. 248(8)(b), with the result that the...

22 February 1990 T.I. (July 1990 Access Letter, ¶1348)

IT-385R, para. 6, continues to reflect RC's position where a taxpayer renounces any part of his income interest in a trust subsequent to having...

Articles

Elie Roth, Tim Youdan, Chris Anderson, Kim Brown, "Taxation of Beneficiaries Resident in Canada", Chapter 4 of Canadian Taxation of Trusts (Canadian Tax Foundation), 2016.

Requirements for valid disclaimer of income interest (p. 340)

A taxpayer who executes a valid disclaimer of an income interest in a trust is...

Paragraph 248(8)(c)

Administrative Policy

S6-F2-C1 - Disposition of an Income Interest in a Trust

1.14 When subsection 248(8) applies, the more restrictive requirements of the definition of release or surrender found in subsection 248(9) must...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 106 - Subsection 106(1) | 195 | |

| Tax Topics - Income Tax Act - Section 106 - Subsection 106(2) | 644 | |

| Tax Topics - Income Tax Act - Section 108 - Subsection 108(7) | 150 |

Subsection 248(9)

Disclaimer

Administrative Policy

16 December 2008 External T.I. 2008-0279741E5 F - Renonciation au capital d'une fiducie

An individual transfers shares to a trust of which he is the trustee, and he, his wife and children are the capital and income beneficiary. In...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(2) | settlor’s valid renunciation of capital interest (but not income interest) prior to trustees’ exercise of discretion to distribute a capital gain would avoid application of s. 75(2)(a)(i) | 199 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition - Paragraph (i) | non-disposition distribution of non-taxable portion of trust capital gains avoids a gain under s. 107(2.1) | 375 |

| Tax Topics - Income Tax Act - Section 54 - Proceeds of Disposition | settlor’s renunciation of capital interest (but not income interest) prior to trustees’ exercise of discretion to distribute a capital gain would generate nil proceeds and not engage s. 56(2) or (4) | 194 |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(b) | s. 69(1) does not apply to a renunciation of trust capital interest since no disposition "to" any person | 44 |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | s. 56(2) inapplicable to renunciation of capital interest in a trust | 45 |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(4) | s. 56(4) inapplicable to disclaimer of capital interest in a trust | 43 |

Subsection 248(9.1)

Administrative Policy

Folio S6-F4-C1, "Testamentary Spouse or Common-law Partner Trusts," 3 February 2022

Does not apply if no court order

1.15 Paragraph 248(9.1)(b) applies to a trust established by a court order, in relation to the taxpayer’s...

23 September 1998 External T.I. 9800555 F - FIDUCIE SUCCESSIVE - FIDUCIE TESTAMENTAIRE

An individual's will provided for the bequeathing of his property to a spousal trust and that, upon the death of the surviving spouse, the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 108 - Subsection 108(1) - Testamentary Trust | remainder trusts required by the will to be established for the children after the termination of the testamentary spousal trust were deemed to be testamentary trusts by s. 248(9.1) | 59 |

Subsection 248(10) - Series of transactions

Cases

Madison Pacific Properties Inc. v. Canada, 2025 FCA 20

Under a “restart” plan, the appellant changed its name, spun out its existing mining assets so that it was a shell with only tax losses, and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | Deans Knight applied to corporate restart plan | 154 |

Deans Knight Income Corp. v. Canada, 2023 SCC 16

In the course of a general discussion, Rowe J stated (at para. 55):

A series of transactions also includes “related transactions or events . . ....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | a transaction where a Lossco became subject to control rights similar to de jure control abused the rationale of s. 111(5) | 526 |

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(5) | rationale of s. 111(5) addresses where there is a change in the identity of those behind a corporation | 416 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | lender to distressed corporation may have de facto control | 118 |

EYEBALL NETWORKS INC. v. HER MAJESTY THE QUEEN, 2021 FCA 17

Pursuant to a conventional s. 55(3)(a) spin-off transaction, a company (“Oldco”) spun off one of its two businesses to a “Newco,” also...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | s. 160 did not apply to s. 55(3)(a) where each step involved a value-for-value exchange (including the cross-share redemptions) | 565 |

| Tax Topics - General Concepts - Effective Date | price adjustment clause eliminated any possible value discrepancy between the FMV of the transferred property and the consideration therefor | 118 |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(9) | a shareholder whose shares have been redeemed has provided valuable consideration therefor by surrendering its shares | 136 |

| Tax Topics - General Concepts - Fair Market Value - Other | note supported only by pref, then note, of a sister had full FMV | 132 |

Louie v. Canada, 2019 FCA 255

From May 15 to October 17, 2009, the taxpayer directed 71 “swaps” under which TSX-listed shares were transferred between her self-directed...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 207.01 - Subsection 207.01(1) - Advantage - Paragraph (b) - Subparagraph (b)(i) | advantages generated in Year 1 from swap transactions continued to produce indirect advantages thereafter | 547 |

| Tax Topics - Income Tax Act - Section 207.06 - Subsection 207.06(2) | concerns about future value increases are intended to be addressed by relief provisions | 384 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | taxpayer was directing mind in transactions involving an arm’s length trustee | 137 |

2763478 Canada Inc. v. Canada, 2018 FCA 209

An individual did not sell his shares of an operating company (Groupe AST) directly to a third-party purchaser, but instead transferred them on a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | not each transaction in series effecting an estate freeze had that objective | 417 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | value shift transactions that permitted the absorption of a real gain by a paper loss abused the basic capital gains regime | 317 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(6) | individual allegedly suffering double taxation re s. 245(2) denial of capital loss of his corporation failed to apply under s. 245(6) within 180 days | 327 |

Groupe Honco Inc. v. Canada, 2014 DTC 5006, 2013 FCA 128, aff'g 2013 DTC 1032 [at 149], 2012 TCC 305, infra

On January 13, 1999, a newly-incorporated corporation ("New Supervac") was leased the assets of an unrelated corporation ("Old Supervac"), coupled...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 83 - Subsection 83(2.1) | two or three main purposes | 73 |

Copthorne Holdings Ltd. v. Canada, 2012 DTC 5006 [at at 6536], 2011 SCC 63, [2011] 3 S.C.R. 721

The taxpayer's shareholders circumvented the rule in s. 87(3), which required that the paid-up capital ("PUC") of a subsidiary corporation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Stare Decisis | high threshold for reversing not met | 193 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(1) - Tax Benefit | tax benefit illuminated by comparison to reasonable and simpler alternative | 425 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | policy of s. 87(3) is to avoid preservation of PUC on parent and sub amalgamation | 372 |

| Tax Topics - Statutory Interpretation - Expressio Unius est Exclusio Alterius | implied exclusion principle | 109 |

Toronto-Dominion Bank v. Canada, 2011 DTC 5125 [at at 6061], 2011 FCA 221, [2011] 6 CTC 19

A transitional provision in the Act provided that the old s. 55(1) would apply to a transaction if it were "part of a series of transactions,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Transitional Provisions and Policies | 163 | |

| Tax Topics - Income Tax Act - Section 112 - Subsection 112(3) | 174 | |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(9) | 117 | |

| Tax Topics - Statutory Interpretation - Ordinary Meaning | clear wording | 80 |

Lipson v. Canada, 2007 DTC 5172, 2007 FCA 113, aff'd 2009 DTC 5015 [at 5528], 2009 SCC 1

The taxpayer's wife ("Jordanna") borrowed $562,500 from the Bank of Montreal under an interest-bearing demand promissory note in order to purchase...

Canada Trustco Mortgage Co. v. Canada, 2005 SCC 54, [2005] 2 S.C.R. 601, 2005 DTC 5523

In the course of a general discussion of the expression "series of transactions" apearing in ss. 245(2) and (3), the Court noted (at para. 26)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(1) - Tax Benefit | tax benefit if taxable income reduction or on basis of comparison to alternative | 132 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | policy of CCA provisions relied on cost irrespective of risk mitigation | 211 |

| Tax Topics - Statutory Interpretation - Certainty | interpretive approach should be consistent with tax law being certain, predictable and fair, | 131 |

| Tax Topics - Statutory Interpretation - Ordinary Meaning | primacy to ordinary meaning if unequivocal | 96 |

Canada v. Canadian Utilities Ltd., 2004 DTC 6475, 2004 FCA 234

Normal course dividends paid by two public corporations (“CU” and “CUH”) which gave rise to a Part IV tax refund were considered part of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2) | independent purpose for ordinary-course dividends did not exclude them from series | 230 |

OSFC Holdings Ltd. v. Canada, 2001 DTC 5471, 2001 FCA 260

Rothstein JA found that transactions that had the effect of transferring properties with accrued losses to a partnership were a “common law”...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | significant disparity between tax benefit and commercial return from transaction | 263 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | policy against corporate loss trading | 229 |

| Tax Topics - Statutory Interpretation - Interpretation Bulletins, etc. | 70 | |

| Tax Topics - Statutory Interpretation - Interpretation/Definition Provisions | deeming v. definition provisions | 46 |

See Also

Total Energy Services Inc., 2024 TCC 12

In September, 2007, most of the equity of an insolvent public corporation (“Biomerge”) in CCAA proceedings was acquired by the company...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | an acquisition of an insolvent public company with losses by a SIFT trust was an abuse of s. 111(5) | 367 |

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(5) | s. 256(7)(c.1) merely clarified that the acquisition of a public company lossco by a SIFT trust was an abuse of s. 111(5) | 326 |

Agence du revenu du Québec v. Custeau, 2020 QCCA 1496

When a family small business corporation (the “Corporation”) was in financial difficulty, a Quebec regional development fund and affiliated...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | no avoidance transaction where subsequent utilization of PUC created with PUC-averaging was not contemplated | 404 |

3295036 Canada Inc. v. Agence du revenu du Québec, 2020 QCCA 1435

In October 1996, a Quebec-taxpayer company (“329”) acquired public company shares from its parent, on two separate days, in “Quebec...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4) | subsequent years could be reassessed to deny the carryforward of a capital loss reported in a statute-barred year | 216 |

The Trustees of the Morrison 2002 Maintenance Trust & Ors v Revenue and Customs, [2019] EWCA Civ 93

A scheme for the avoidance by three trusts (the “Scottish Trusts”) of capital gains tax on the sale of a bloc representing approximately 2% of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Tax Avoidance | 250 |

3295036 Canada Inc. v. Agence du revenu du Québec, 2018 QCCQ 8100, aff'd 2020 QCCA 1435

On two days in October 1996, the parent company (“Marjad”) of the taxpayer (“3295036”) transferred shares of two public companies, whose...

Louie v. The Queen, 2018 TCC 225, rev'd in part on "advantage" issue (for subsequent years) 2019 FCA 255

From May 15 to October 17, 2009, the taxpayer directed 71 “swaps” under which TSX-listed shares were transferred between her self-directed...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 207.05 - Subsection 207.05(3) | holder rather than trustee liable for advantage tax | 148 |

| Tax Topics - Income Tax Act - Section 207.01 - Subsection 207.01(1) - Advantage - Paragraph (b) - Subparagraph (b)(i) | temporal limitation placed on the advantages considered to arise from TFSA swap transactions | 643 |

| Tax Topics - General Concepts - Fair Market Value - Shares | use of price range for share valuation was inappropriate where there was a second-by-second market | 185 |

Cameco Corporation v. The Queen, 2018 TCC 195, aff'd 2020 FCA 112

Owen J found (at para. 704) that the concept of a “series” under s. 247(2) should be interpreted narrowly, stating:

To allow for a meaningful...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) | having a Swiss/Lux subsidiary enter into long-term purchase contracts at a somewhat fixed price with third parties and the taxpayer did not engage s. 247(2) | 708 |

| Tax Topics - General Concepts - Sham | transactions that were not factually misrepresented were not a sham | 254 |

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(1) - Transaction | meaning of "arrangement" and "event" | 153 |

Loblaw Financial Holdings Inc. v. The Queen, 2018 TCC 182, rev'd on s. 95(1) - investment business - (a) (arm's length conduct) grounds 2020 FCA 79, in turn aff'd 2021 SCC 51

An issue addressed obiter by C Miller J was whether the renewal by the Barbados subsidiary (GBL) of the taxpayer of its international banking...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 165 - Subsection 165(1.11) | requirement met where Crown knew the nature and quantum of the dispute | 269 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Bank | CFA qualified as a foreign bank since it was licensed under Barbados law as an international bank | 123 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Investment Business - Paragraph (a) | Barbados-licensed international bank, which used Loblaw funding to invest responsively to Loblaw considerations, conducted an offside non-arm’s length business | 429 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Investment Business - Paragraph (c) | employee equivalents was reduced by employee time described in s. 95(2)(b) | 290 |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Foreign Exchange | short-term debt securities were inventory because they were the raw material for generating swap income | 130 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4.01) - Paragraph 152(4.01)(a) - Subparagraph 152(4.01)(a)(ii) | GAAR is generally a separate matter rather than being subsumed in the allegedly-misused substantive provision | 208 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | application of GAAR required the occurrence of an avoidance transaction (or series) in non-statute-barred years and the relevant previous year’s avoidance transaction did not occur as part of the series | 512 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | use of Barbados sub to engage in proprietary trading for Canadian parent misused the foreign bank exemption, whose purpose was promoting international competitiveness | 336 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(l) | purpose of s. 95(2)(l) exception was to permit non-resident subsidiaries of Canadian banks and dealers to compete internationally | 190 |

Oxford Properties Group Inc. v. The Queen, 2016 TCC 204, rev'd 2018 FCA 30

A corporation (“BPC”), which was mostly owned by a Canadian pension fund (“OMERS”), obtained the agreement of a predecessor of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | no abuse in using 88(1)(d) bump to avoid s. 100 after 3-year s. 69(11) period | 557 |

| Tax Topics - Income Tax Act - Section 97 - Subsection 97(2) | purpose not to tax underlying recapture on subsequent LP unit sale | 431 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(d) | purpose: to push down ACB of shares of sub to qualifying non-depreciable property | 489 |

| Tax Topics - Statutory Interpretation - Interpretation Act - Subsection 45(2) | subsequent amendment shed light on scope of previous version | 107 |

| Tax Topics - Income Tax Act - Section 100 - Subsection 100(1) | S. 100 operates only on outside basis gain | 290 |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(11) | Parliament provided safe harbour for sales after 3 years | 204 |

| Tax Topics - Income Tax Act - Section 98 - Subsection 98(3) - Paragraph 98(3)(c) | purpose: to preserve high outside basis through push down | 293 |

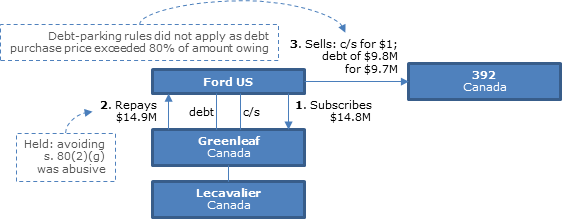

Pièces automobiles Lecavalier Inc. v. The Queen, 2014 DTC 1126, 2013 TCC 310

{kind=link}

A Canadian subsidiary ("Greenleaf") of Ford U.S. paid down to $9,750,000 (including accrued interest) a debt of $24,369,439 (plus accrued...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Evidence | Canadian tax accountant's testimony on US tax consequences accorded little weight | 152 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | debt-paydown transactions were avoidance transactions | 268 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | avoidance of debt forgiveness rules was abusive | 277 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(2) - Paragraph 80(2)(g) | using cash share subscriptions to convert debt to share equity abused s. 80(2)(g) | 190 |

MIL (Investments) S A v. The Queen, 2006 DTC 3307, 2006 TCC 460, aff'd 2007 FCA 236

In March 1993 an individual ("Boulle") transferred his shares of a Canadian public junior exploration company ("DFR") to the taxpayer, which was a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | 355 | |

| Tax Topics - Statutory Interpretation - Retroactivity/Retrospectivity | 91 | |

| Tax Topics - Treaties - Income Tax Conventions | 148 |

Canutilities Holdings Ltd. v. The Queen, 2003 DTC 1029 (TCC), rev'd in part 2004 DTC 6475, 2004 FCA 234

Normal course dividends paid by the taxpayers were not paid in contemplation of transactions in which their common shares of a public company were...

Les Placements E&R Simard Inc. v. The Queen, 97 DTC 1328 (TCC)

On September 10, 1988, the taxpayer transferred its assets to a subsidiary ("Alimentation 1988") in consideration for a demand promissory note and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Safe-Income Determination Time | subsequent redemption of preferred shares was not assimilated to the series in which they were issued one or more year previously, given different objectives for each and lack of interdependence | 175 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2) | 111 |

Craven v. White, [1988] BTC 268 (HL)

Lord Jauncey stated:

"If it were appropriate to prepare a formula defining 'composite transaction' in the light of the passages in the speeches in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Tax Avoidance | 203 |

Administrative Policy

2025 Ruling 2023-0990951R3 - Safe Income Determination Time Monthly Dividends

It was proposed that, rather than continuing to distribute PUC to its Canadian parent (Partner A) as before, a Canadian corporation (Partner B)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Safe-Income Determination Time | series of monthly dividends distributing interest income was not a “series” for SIDT purposes | 538 |

| Tax Topics - Treaties - Income Tax Conventions - Article 4 | reference to 2-step approach to avoiding IV(7)(a) anti-hybrid rule in Canada-US treaty | 89 |

2023 Ruling 2022-0958601R3 - Post Butterfly Transactions

CRA ruled on whether subsequent sale and redemption transactions involving shares that had been distributed on the third of three successive...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.1) - Paragraph 55(3.1)(c) | post-butterfly sales of distributed shares by TC (or redemption in hands of DC of retained shares) were independent of the butterfly and did not engage s. 55(3.1)(c) (or (d)) | 602 |

2024 Ruling 2023-0989121R3 F - Internal reorganization - 55(3)(a) and 55(3.01)(g)

Before Opco (whose shares were held by three unrelated individuals, Messrs. A, B and C) was to effect a real-estate spin-off to a new sister...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.01) - Paragraph 55(3.01)(g) | transfer of real estate to separate Realtyco beneath a newly-formed Holdco | 605 |

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(2) | 2 unrelated individuals were the settlors for each other’s family trust | 162 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) - Subparagraph 55(3)(a)(ii) | s. 55(3.01)(g) applied to the transfer (fresh after an estate freeze) by unrelated shareholders of Opco to a new Holdco, with an Opco realty spin-off to a new Realtyco sister | 274 |

7 October 2022 APFF Roundtable Q. 14, 2022-0942191C6 F - Safe-income determination time

A purchaser incorporated a Buyco to acquire the assets of the vendor corporation and then, a few weeks later, the net asset proceeds on the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Safe-Income Determination Time | incorporation of Buyco may trigger safe-income determination time | 383 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(b) | no need for CRA flexibility regarding safe income issues arising from early formation of a Buyco | 307 |

May 2019 CPA Alberta CRA Roundtable, ITA Session – Q.7

What factors would CRA typically review to assess whether certain transactions are part of the same series; and how important is it that...

2018 Ruling 2017-0683941R3 - Split-up transactions

Mother along with an arm’s length business associate (“Investor”) wanted to use some of the assets of the family business corporation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) - Subparagraph 55(3)(a)(ii) | split-up to resolve business differences between daughter and mother, with relevant significant investment of arm's length investor in further transferee company | 758 |

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(1) - Paragraph 186(1)(b) | year-end established in middle of cross-redemptions to avoid circularity | 220 |

29 October 2013 External T.I. 2013-0489771E5 F - Internal Reorganization - 55(3)(a)

Three brothers held Corporation A as to 1/3 each and their mother’s estate held all of Corporation B. Following the distribution of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.2) - Paragraph 55(3.2)(d) | s. 55(3.2)(d) application to estate distribution of corporation to 3 sibling beneficiaries does not deem them to be related to each other | 248 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) - Subparagraph 55(3)(a)(v) | relief under s. s. 256(7)(a)(i)(C) or (D) is relevant to s. 55(3.1)(b)(ii), but not to ss. 55(3)(a)(i) to (v) | 227 |

24 October 2012 Internal T.I. 2012-0456711I7 F - Inadmissibilité à la déduction pour GC

Mr. A effected an estate freeze by converting his Class "AA" shares of Opco into Class "F" Opco shares. S. 51(2) has been applied to determine the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110.6 - Subsection 110.6(7) - Paragraph 110.6(7)(b) | potential application of s. 110.6(7)(b) where s. 51(2) applied | 268 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4.2) | no retroactive adjustment of capital gains exemption where claimed before the normal reassessment period | 192 |

7 June 2001 External T.I. 2001-0079505 F - Gel suivi d'un rachat des actions priv.

A freeze transaction entailed all of the (1,000) Class A Opco common shares held by Holdco with a FMV of $10 million being exchanged under s. 51...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(c) | safe income of common shares converted to pref under s. 51 was transferred to the pref/ non-cumulative pref dividends do not reduce safe income until declared | 311 |

17 November 2000 External T.I. 1999-0008585 - Winding-up

"A particular transaction will be part of a series of transactions if that transaction is logically and reasonably connected to another...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(c) - Subparagraph 88(1)(c)(vi) | 55 |

23 August 1991 T.I. (Tax Window, No. 8, p. 21, ¶1409)

A preliminary transaction will form part of a series of transactions that includes subsequent transactions if at the time of the preliminary...

9 May 1990 Meeting (October 1990 Access Letter, ¶1474)

"If at the time of the 'butterfly' reorganization the shareholders had formed the intention to sell their shares, and their shares are eventually...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1.1) | 41 | |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 22 |

3 November 89 T.I. (April 90 Access Letter, ¶1172)

"A preliminary transaction will form part of the series of transactions or events determined with reference to subsection 248(10) if, at the time...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) | 153 |

Articles

Doron Barkai, Alexander Demner, "Dealing with New Subsection 55(2): Issues and Strategies", 2016 Conference Report (Canadian Tax Foundation), 6:1–56

Avoidance of exclusion if Pt. IV refund not received as part of the series (pp. 6:27-29)

[A]ny dividend paid from Holdco to the shareholder needs...

Justice Marshall Rothstein, "An Overview of the Supreme Court of Canada", Bulletin for International Taxation (IBFD), January/February 2016, p. 20.

Resort to foreign judgments (p. 25)

An example concerns the interpretation of a "series of transactions" under a general anti-avoidance rule...

Benjamin Alarie, Julia Lockhart, "The Importance of Family Resemblance: Series of Transactions After Copthorne", Canadian Tax Journal (2014) 62:1, 273-99.

Extension of common-law series (pp. 76-77)

… Kandev et al. argue that the purpose of subsection 248(10) is merely to bring into the Act the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) | 96 |

Marc Ton-That, Vance Sider, "Understanding Section 55 and Butterfly Reorganizations", 2nd Edition, CCH, 1999

Alleviation of already narrow concept of series (commencing with negotiations) through introduction of SIDT definition (pp. 34-35)

- Prior to the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Safe-Income Determination Time | 437 |

David M. Williamson, Michael H. Manly, "Subsection 69(11) - Unexpected Problems from Inappropriate Positions", Corporate Structures and Groups, Vol. V, No. 4, 1999, p. 285.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(11) | 0 |

Ted Harris, "An Update of Revenue Canada’s Approach to the Butterfly Reorganization", Report of Proceedings of the Forty-Third Tax Conference, 1991 Conference Report (Toronto: Canadian Tax Foundation, 1992), 14:1-15, at 14:10.

Pre-butterfly transaction whose structure or timing is affected by considerations relating to the butterfly is in contemplation thereof (p....

Michael Hiltz, "Section 245 of the Income Tax Act", Report of Proceedings of the Fortieth Tax Conference, 1988 Conference Report (Toronto: Canadian Tax Foundation, 1989), 7:1-9 at 7:6.

A preliminary transaction will be assimilated to a subsequent series if the taxpayer intended to carry out such series, although identity of...

Thivierge, "Emerging Income Tax Issues", 1993 Conference Report, c. 4

J. Tiley, "Series of Transactions", 1988 Conference Report, c.8.

Subsection 248(16) - Goods and services tax — input tax credit and rebate

See Also

Touchette v. The King, 2025 CCI 195

Gagnon J confirmed, as to the majority of the expenses concerned, CRA assessments which denied the deduction by a corporation (“9134”) of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1.3) | s. 15(1.3) inapplicable to GST on expenses paid by a corporation for its shareholder’s benefit | 90 |

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(x) - Subparagraph 12(1)(x)(vi) | ITCs claimed on denied expenses were not income by virtue of s. 12(1)(x)(vi) since the associated GST had not been treated as an expense | 273 |

Administrative Policy

2 November 2021 External T.I. 2021-0898151E5 - GST/HST Quick Method of Accounting

Regarding the income tax effect of using the Quick Method of Accounting for the GST/HST on purchases (the “Quick Method”), CRA first noted...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(x) | use of the GST/HST Quick Method generally results in s. 12(1)(x) inclusions, but also increases expense deductions | 126 |

2 April 2014 External T.I. 2012-0473151E5 F - Limitation du coût de location d'un véhicule

Are amounts of recovered GST and QST respecting the lease of a vehicle to be considered “reimbursements” under element E in ss. 67.3(c) and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 67.3 | GST ITCs included under element E of formula | 176 |

27 November 2014 External T.I. 2013-0503861E5 F - Application du paragraphe 248(16)

Where a building drop-down under s. 85(1) generates an ITC to the transferor under ETA s. 193, such ITC does not reduce the UCC of the property...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) - Paragraph 85(1)(e) | ETA s. 193 ITC generated on drop-down does not reduce UCC at that time | 193 |

27 November 2003 Internal T.I. 2002-0180587 F - Mauvaise créance et taxes de vente

The accounts receivable of a taxpayer include GST and QST that is collectible by it on those sales. Before indicating that the write-off of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(p) - Subparagraph 20(1)(p)(i) | no bad debt deduction for write off of GST/QST | 158 |

| Tax Topics - Excise Tax Act - Section 224 | remittance of tax by supplier results in subrogation of the Crown’s claim for the tax | 215 |

5 December 2002 Internal T.I. 2002-0155187 F - DEPENSES PERSONNELLES

A taxpayer incurred what it viewed as a currently deductible expense of $100,000 and paid GST and QST thereon of $7,000 and $8,000, for which it...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(hh) | repayment of ITRs would result in deduction under s. 20(1)(hh)(i) or (ii) depending on whether or not an s. 12(2.2) election had been made | 232 |

3 January 1992 T.I. (Tax Window, No. 15, p. 24, ¶1683)

A cash-basis taxpayer will be considered to have received a GST input tax credit in the period for which the refund is claimed on the GST return.

19 August 1991 Memorandum (Tax Window, No. 8, p. 12, ¶1395)

A GST input tax credit is considered to be received or credited in the reporting period in which the claim was made rather than the reporting...

22 March 1991 T.I. (Tax Window, No. 1, p. 7, ¶1164)

A GST rebate which is claimed by a partner of a partnership at the end of the 1991 calendar year in respect of expenses incurred by him personally...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Income-Producing Purpose | 23 |

Paragraph 248(16)(a)

Subparagraph 248(16)(a)(i)

Administrative Policy

30 March 2011 External T.I. 2010-0390591E5 F - Cotisation spéciale

In the course of discussing the deductibility of an assessment made of the taxpayer by the other co-owners of a commercial condo complex to cover...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Payment & Receipt | amounts paid by set-off are both paid even though no movement of funds | 274 |

| Tax Topics - Income Tax Act - Section 9 - Timing | amounts assessed against the taxpayer by co-owners not deductible until expended on or in the business | 219 |

Subsection 248(18) - Goods and services tax — repayment of input tax credit

Administrative Policy

19 August 1991 Memorandum 911368(E)

Where the taxpayer was assessed in July 1993 to deny an input tax credit, appealed successfully to the Tax Court but with the Minister then...

Subsection 248(20) - Partition of property

Administrative Policy

9 June 2015 External T.I. 2014-0554381E5 F - Copropriété par indivision - partage de biens

Mr A held land used by him in farming in co-ownership with his brother. Following a partition and cessation of farming, Mr A became the sole owner...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110.6 - Subsection 110.6(1.3) | partition did not reset original date of acquisition of property in co-ownership | 147 |

1 September 2010 External T.I. 2009-0338641E5 - Partition of property

In course of a general discussion CRA stated:

Subsection 248(20) of the Act applies where the fair market value of the separate piece of property...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(21) | one property if two legal lots (not necessarily contiguous) acquired under one deed | 230 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(21) - Paragraph 248(21)(c)) | single property requirement can be satisfied by consolidating then partitioning | 76 |

25 September 2000 External T.I. 2000-0038595 - PARTITION OF PROPERTY

"In a situation where more than one property is acquired under one deed, such properties would be considered to be one property for purposes of...

28 October 2002 External T.I. 2002-0134785 F - Partitioning of Shares

A partnership, holding investments in inter alia public companies was dissolved such that each CCPC received a pro rata undivided interest in each...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(21) | s. 248(21) could apply to partitioning a share if the corporation could issue fractional shares on the partition satisfying the FMV test, and similarly for partitioning MFT units (viewed as a single property) | 301 |

| Tax Topics - Income Tax Act - Section 98 - Subsection 98(3) | partners not permitted to receive divided interest in shares on s. 98(3) wind-up | 116 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Property | interest in trust is a single property even if held as units | 90 |

18 September 2001 External T.I. 2001-0100485 F - PARTAGE D'ACTION DETENUE EN INDIVISION

CCRA indicated that S. 248(21) could apply if, following the s. 98(3) wind-up of a partnership holding shares, there was a legally effective...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(21) | no need to issue fractional share certificates on partition of shares held in co-ownership for s. 248(21) to apply/ no disposition on subsequent global certificate issuance | 147 |

12 January 2000 Internal T.I. 9918467 F - CORRECTION PARTAGE VS. SOULTE

A rental property partnership between two brothers (A and B) was wound-up pursuant to s. 98(3) so as to convert ownership to a 50-50 co-ownership,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(x) - Subparagraph 12(1)(x)(iv) | compensation for excess mortgage payments (including principal amortization) previously made on partitioned property was s. 12(1)(x)(iv) income | 310 |

30 November 1995 Ruling 9618173 - PARTITION OF SHARES IN A PARTNERSHIP

A partnership holding publicly-traded shares and limited partnership units was to be wound-up under s. 98(3), with the shares and units (while...

27 April 1998 Internal T.I. 9804567 - PARTITION OF A MILK QUOTA

The partition of a jointly owned non-real estate asset, such as a milk quota, could be accomplished under either s. 248(20) or (21) of the Act...

23 December 1992 T.I. (Tax Window, No. 27, p. 20, ¶2341) [partition of non-adjacent properties]

If non-adjacent parcels of land are acquired at one time and under one deed, they will be considered as property that can be partitioned under s....

24 February 1992 Memorandum (Tax Window, No. 13, p. 17, ¶1622)

Where an undivided interest in partnership property is distributed to each partner in accordance with s. 98(3), any partition of property which is...

23 October 1991 T.I. (Tax Window, No. 12, p. 18, ¶1552)

Where a co-owner exchanges an undivided interest in a property for an undivided interest in each subdivided parcel, followed by an exchange of the...

Articles

A. J Oakley, "Chapter 8: Co-ownership", A Manual of the Law Of Real Property by Robert Megarry, 8th Ed., Sweet & Maxwell, 2002

Partition at common law (p. 327)

Joint tenants and tenants in common have always been able to make a voluntary partition of the land concerned if...

Subsection 248(21) - Subdivision of property

Administrative Policy

2019 Ruling 2018-0787181R3 - Minority owners and Partition of Property

Background