Subsection 118.1(1) - Definitions

Right to Receive Production

Articles

R. Ashton, "Leasing: Recent Developments", 1997 Corporate Management Tax Conference Report, c. 11.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 16.1 - Subsection 16.1(1) | 0 | |

| Tax Topics - Income Tax Act - Section 181 - Subsection 181(3) | 0 |

Total Charitable Gifts

Cases

Van der Steen v. Canada, 2020 FCA 168

The taxpayer, a lawyer, withdrew $100,000 from his RRSP and “contributed” an amount exceeding the withdrawal amount (and well in excess of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Onus | taxpayer failed to meet onus of establishing donative intent | 191 |

Morrison v. Canada, 2020 FCA 93

The taxpayers in a charitable gift program for the donation by them of entitlements to pharmaceuticals (acquired in a distant land) to a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Onus | onus of proof rested at all times with the taxpayer | 271 |

Markou v. Canada, 2019 FCA 299

The taxpayers, who resided in Quebec or Ontario, participated in the same leveraged donation program as had been found to not entitle the taxpayer...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Stare Decisis | consent judgments had no precedential value | 136 |

French v. Canada, 2016 FCA 64

In his 2000 to 2002 taxation years, the taxpayer made gifts to a registered charity that were funded from personal funds and from loans tied to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Interpretation Act - Section 8.1 | Parliament may have intended what constitutes a gift outside Quebec to be partly informed by the Civil Code | 173 |

Canada v. Castro, 2015 DTC 5113 [at at 6266], 2015 FCA 225, rev'g sub nom. David v. The Queen, 2014 DTC 1111 [at 3236], 2014 TCC 117

The taxpayers received charitable receipts for 10 times the amount of contributions, paid in cash, made by them to a registered charity. Woods J...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(2) | inflated charitable receipt was invalid | 193 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(32) | inflated charitable receipt not an "advantage" | 124 |

| Tax Topics - Income Tax Regulations - Regulation 3501 | inflated charitable receipt was invalid | 193 |

| Tax Topics - Statutory Interpretation - Interpretation Act - Section 16 | Regs read in context of enabling legislation | 82 |

| Tax Topics - Statutory Interpretation - Interpretation Act - Section 32 | inflated charitable receipt not an "advantage" | 124 |

Canada v. Berg, 2014 DTC 5028 [at at 6664], 2014 FCA 25, rev'g infra

The taxpayer purchased timeshare units for cash equaling their fair market value and issued bogus promissory notes for nine times the units' fair...

Kossow v. Canada, 2014 DTC 5017 [at at 6622], 2013 FCA 283

The taxpayer participated in an avoidance scheme similar to the one in Maréchaux, in which she made donations, financed as to 80% by a...

Maréchaux v. Canada, 2010 DTC 5174 [at at 7315], 2010 FCA 287, aff'g 2009 DTC 1379 [at 2095], 2009 TCC 587

The taxpayer agreed in December 2001 to make a $100,000 donation to a charitable foundation, comprising $20,000 of his own funds and $80,000 from...

Slobodrian v. Canada (Minister of National Revenue), 2006 DTC 5625, 2005 FCA 336

The Court followed its earlier decision in Slobodrian v. Queen, 2003 DTC 5632, 2003 FCA 350 in finding (at p. 5626) that "the mere supply of...

Canada v. Doubinin, 2005 DTC 5624, 2005 FCA 298

A finding of the Tax Court Judge that the taxpayer had not made a gift of $6,887 to a registered charity with an expectation that he would be...

Canada (Attorney General) v. Nash, 2005 DTC 5696, 2005 FCA 386

A company ("CVI") operated a program through which it sold groups of limited edition prints to individuals, arranged for appraisal and located...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Other | purchase price of prints established their FMV as contrasted to speculative retail value | 316 |

Slobodrian v. Canada (Minister of National Revenue), 2003 DTC 5632, 2003 FCA 350

A retired physics professor who agreed to carry out research activities without remuneration pursuant to a contract between Public Works Canada on...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Property | statutory definition of "property" is not broader than its ordinary meaning | 57 |

Woolner v. Canada (Attorney General), 99 DTC 5722 (FCA)

Contributions made by the taxpayers to the First Mennonite Church that were designated as contributions to be applied to a student mutual aid...

The Queen v. Friedberg, 92 DTC 6031, [1992] 1 CTC 1 (FCA)

The taxpayer purchased for $12,000 an antique textile collection which had been identified and brought to his attention by an employee of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Substance | 117 | |

| Tax Topics - General Concepts - Tax Avoidance | subjective intention does not alter transactions | 156 |

The Queen v. Burns, 88 DTC 6101, [1988] 1 CTC 201 (FCTD), aff'd 90 DTC 6335 (FCA)

The taxpayer whose daughter was a member of a Canadian Ski Association training squad, was not entitled to deduct payments made by him to the...

The Queen v. McBurney, 85 DTC 5433, [1985] 2 CTC 214 (FCA)

In order for a transfer of property to be a "gift", the property generally must be transferred voluntarily and not as the result of a legal...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 165 - Subsection 165(3) | 52 |

The Queen v. Zandstra, 74 DTC 6416, [1974] CTC 503 (FCTD)

The taxpayer, whose two children were attending at the Canadian Christian School at Jarvis, Ontario (which was a registered charity) paid $590 to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 177 - Subparagraph 177(b)(iv) | 162 |

See Also

Tudora v. The Queen, 2020 TCC 11 (Informal Procedure)

The taxpayer participated in the same “Global Learning” charitable tax credit arrangement as had been considered in Mariano and under which he...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Judicial Comity | principle of judicial comity applicable to previous Tax Court decision on the same donation program | 221 |

Miller v. The Queen, 2019 TCC 204 (Informal Procedure)

The taxpayer, who held a PhD, purchased Courseware from Global Learning Systems Inc. (“GLS”) in 2003 for $7,000 and immediately donated it to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Other | software was to be valued at its purchase price | 88 |

Kaul v. The Queen, 2019 TCC 17

The taxpayers bought sets of artists’ prints (each set consisting of 11 prints) at a purchase price that might be 7 or 10 times the vendor’s...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Other | art work was donated at a FMV equal to its cost rather than appraised value | 420 |

Morrison v. The Queen, 2018 TCC 220, aff'd sub nom. Eisbrenner v. Canada, 2020 FCA 93

One of the taxpayers (Morrison) participated in a charitable gift program (the “CGI Program”) under which he purchased pharmaceuticals for a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Onus | taxpayers had the burden of disproving the Minister’s assumptions about their gift tax shelter about which they knew virtually nothing | 438 |

| Tax Topics - General Concepts - Fair Market Value - Other | Ontario list price of generic pharmaceuticals substantially exceeded their FMV in the international market | 211 |

Markou v. The Queen, 2018 TCC 66, aff'd on selected grounds 2019 FCA 299

The taxpayers, who resided in Quebec or Ontario, participated in the same leveraged donation program as had been found to not entitle the taxpayer...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(30) | donative intent no longer is required for split gifts | 296 |

Murji v. The Queen, 2018 TCC 7 (Informal Procedure)

The promotional materials of Strategic Gifting Group (“Strategic,” or “SGG”) contemplated that participants would make a cash donation to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 3501 - Subsection 3501(1) - Paragraph 3501(1)(h) | the cash portion of a donation made to a charity was reduced by the fees paid by it to the tax shelter promoter | 234 |

| Tax Topics - Income Tax Act - Section 237.1 - Subsection 237.1(1) - Tax Shelter | charitable gifting arrangements with high promised credits was a tax shelter | 180 |

Fonds de solidarité des travailleurs du Québec (F.T.Q) v. The Queen, 2018 TCC 3, aff'd on s. 18(1)(a) grounds 2019 FCA 36

The corporate taxpayer agreed with the City of Chandler that it would no longer use any loan repayment proceeds received by it from a City-owned...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110.1 - Subsection 110.1(1) - Paragraph 110.1(1)(a) | consideration for "gift" was elimination of obligation to invest the funds | 523 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Income-Producing Purpose | purpose of payment was to extricate from a regional economic-development obligation rather than to enhance business reputation | 224 |

Cassan v. The Queen, 2017 TCC 174

In December 2009, the taxpayers participated in a program that had both an investment and gifting component. The investment program entailed each...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 143.2 - Subsection 143.2(12) | although borrowing by taxpayers had a term of 9.3 years, they had a reasonable expectation of refinancing with the promoter’s assistance | 478 |

| Tax Topics - Income Tax Act - Section 143.2 - Subsection 143.2(7) - Paragraph 143.2(7)(a) | loans were not bona fide in that not handled with commerciality | 701 |

| Tax Topics - Income Tax Regulations - Regulation 7000 - Subsection 7000(2) - Paragraph 7000(2)(d) | no requirement to accrue interest on index-linked note in a year when the return thereon was not determinable | 605 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) - Subparagraph 20(1)(c)(i) | interest on loan to acquire LP units was deductible as there was a prospect of gross income being allocated by LP in 19 years’ time | 619 |

| Tax Topics - Statutory Interpretation - Realization Principle | amount should not be recognized until ascertainable | 73 |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(c) | gratuitous transfer is gift irresepctive of absence of benevolent intent | 56 |

Mariano v. The Queen, 2015 DTC 1209 [at at 1331], 2015 TCC 244

The taxpayers were participants in leveraged donation transactions, which were intended to result in a step-up of the adjusted cost base of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Other | courseware licences valued at modest initial cost, given relevant wholesale market and depressive effect of huge volumes purchased | 303 |

| Tax Topics - General Concepts - Ownership | no acquisition of unascertained property | 76 |

| Tax Topics - General Concepts - Sham | taxpayer involvement in deceit unnecessary | 375 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(1) | void for lack of certainty of objects | 224 |

| Tax Topics - Income Tax Act - Section 107 - Subsection 107(2) | delegation of power of appointment to promoter not authorized | 238 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(35) | attempted use of initial gift to step-up ACB under s. 69(1)(c) | 262 |

French v. The Queen, 2015 TCC 35

The taxpayer participated in the same donation scheme as in Kossow. The taxpayer, who was not a Quebec resident, sought to apply the Quebec civil...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Interpretation Act - Section 8.1 | tax results in common and civil law need not be uniform | 143 |

Webb v. The Queen, 2004 TCC 619 (Informal Procedure)

The taxpayer made a donation equal to his annual income to a charity (whose registration was revoked shortly thereafter). Bowie J found there was...

Johnson v. The Queen, 2014 DTC 1097 [at at 3185], 2014 TCC 84 (Informal Procedure)

The taxpayer claimed donations, equal to approximately half of his salary, allegedly made to a registered charity ("CFCD") in three consecutive...

David v. The Queen, 2014 DTC 1111 [at at 3236], 2014 TCC 117 (Informal Procedure)

The taxpayers or their spouses donated cash and, in some instances, household goods to a registered charity. The Minister assumed that the...

Carson v. The Queen, 2014 DTC 1006 [at at 2520], 2013 TCC 353 (Informal Procedure)

The taxpayer and his wife allowed a charity to use two rooms of their house for free (an office and a storage room), and claimed charitable...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Property | donated space must constitute an enforceable right in order to be property | 123 |

Hall v. The Queen, 2013 DTC 1241 [at at 1313], 2013 TCC 314 (Informal Procedure)

Pizzitelli J found that there was no discrimination in denying the taxpayer charitable credits for donations made to the International Association...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Other Legislation/Constitution - Charter (Constitution Act, 1982) - Subsection 15(1) | no charitable registration, no discrimination | 47 |

Bandi v. The Queen, 2013 DTC 1192 [at at 1032], 2013 TCC 230 (Informal Procedure)

The taxpayer participated in a donation scheme in which participants supposedly would acquire office software licences for a bulk rate and donate...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 237.1 - Subsection 237.1(6) | 276 |

Berg v. The Queen, 2013 DTC 1018 [at at 93], 2012 TCC 406, rev'd supra

The taxpayer purchased timeshare units for cash (as to 1/9 of the consideration) and promissory notes (as to the balance), and then donated the...

Grossett v. The Queen, 2012 DTC 1185 [at at 3465], 2012 TCC 179 (Informal Procedure)

The taxpayers relied on charitable receipts which showed donations amounting to approximately 25% of their annual income, and which had been...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4) - Paragraph 152(4)(a) - Subparagraph 152(4)(a)(i) | implausibly large charitable receipts | 59 |

Coleman v. The Queen, 2010 DTC 1096 [at at 3000], 2010 TCC 109, aff'd 2011 DTC 5040 [at 5651], 2011 FCA 82

The corporate taxpayer was indirectly controlled by the individual taxpayer. The two taxpayers contributed funds to a charitable organization...

Russell v. The Queen, 2009 TCC 548, 2009 DTC 1371 (Informal Procedure)

C. Miller, J. followed the Nash decision in finding that quantities of art purchased by the taxpayers and immediately donated to charities had a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Other | 140 |

Benquesus v. The Queen, 2006 DTC 2747, 2006 TCC 193

It was found that the taxpayer's father, in transferring funds to a charitable foundation, had thereby made a transfer to his children of loans...

Klotz v. The Queen, 2004 DTC 2236, 2004 TCC 147, aff'd 2005 DTC 5279, 2005 FCA 158

The taxpayer purchased prints from a promoter at approximately $300 per print (which the promoter contemporaneously had purchased for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 163 - Subsection 163(2) | 38 | |

| Tax Topics - Income Tax Act - Section 54 - Personal-Use Property | 113 | |

| Tax Topics - Statutory Interpretation - Interpretation/Definition Provisions | "includes" is expansive | 61 |

Nadeau v. The Queen, 2003 DTC 18 (TCC)

Employees of a college who wished to have a computer at home would make a payment to a charitable foundation associated with the college, with the...

Dutil v. The Queen, 95 DTC 281 (TCC)

After confirming the Minister's reassessment that had been made on the basis that a painting donated by the taxpayer to a gallery have been...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 163 - Subsection 163(2) | 158 |

Administrative Policy

2 April 2024 External T.I. 2024-1005231E5 - Directed gifts - official tax receipts

Regarding a situation where a municipality that is a qualified donee issued a press release in which it solicited donations that were...

7 May 2024 CALU Roundtable Q. 4, 2024-1007061C6 - Shared Ownership & Charitable Gift

After referring to the position in IT-244R3 that a gift by an individual of a life insurance policy to a registered charity is considered to be a...

10 March 2023 External T.I. 2022-0943881E5 - Charitable Remainder Trusts

In somewhat general terms, the numerical limit in the s. 118.1 definition of ”total gifts” as to the amount of an individual’s total...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(1) - Total Gifts - Paragraph (a) - Subparagraph (a)(iii) - Variable B | an individual’s taxable capital gain on settling a charitable remainder trust increases the individual’s total gifts limit by 75%, not 100%, thereof | 176 |

1 February 2023 External T.I. 2022-0945221E5 - Directed gift to a municipality

Regarding the receipt of funds by a qualified donee that is a municipality from a registered charity where such funds would then be directed to a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 149.1 - Subsection 149.1(1) - Qualifying Disbursement | a directed gift is not a gift | 146 |

7 June 2019 STEP Roundtable Q. 2, 2019-0798491C6 - Alter ego trust and donations

An alter ego trust realizes a taxable capital gain under s. 104(4) on a portfolio of listed shares on the death of the settlor (which generated a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(1) - Total Charitable Gifts - Paragraph (c) - Subparagraph (c)(ii) - Clause (c)(ii)(C) | gifts made by alter ego trust during 3 years following settlor's death | 122 |

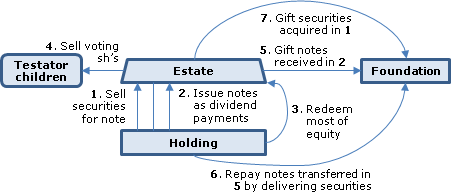

2017 Ruling 2016-0628181R3 - Donation of shares to private foundation

The estate of B gifts her shares of a portfolio holding company (“Holdco”) to a private foundation, with Holdco thereafter using its liquid...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(13) - Paragraph 118.1(13)(c) | gift of NQS in portfolio company cured when company wound-up into charity | 210 |

| Tax Topics - Income Tax Act - Section 129 - Subsection 129(1.2) | s. 129(1.2) denies a dividend refund on the wind-up of a private company bequeathed (but not gifted) to a private foundation | 264 |

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(15) | gift of shares (NQS) of portfolio company retroactively deemed to be made in terminal year once company wound up into charity | 100 |

2016 Ruling 2016-0634031R3 - Donation to a municipality

Background

The Municipality (which is a qualified donee) passed a resolution supporting a cause, and has been given full party status with...

S7-F1-C1 - Split-receipting and Deemed Fair Market Value

Meaning of "gift"

1.2 Under the common law, “a gift is a voluntary transfer of property owned by a donor to a donee, in return for which no...

21 January 2016 Roundtable, 2016-0624851C6 F - Spousal sharing of charitable gifts made by will

For deaths occurring after 2015, will it be possible to include donations made by the estate of an individual in donations made by the surviving...

2015 Ruling 2014-0532201R3 - Corporate reorganization

A privately-held Canadian corporate group uses its shareholdings in a public company to maximize the benefit from a corporate contribution to a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 38 - Paragraph 38(a.1) | donation of pubco shares to foundation and immediate cash sale to affiliate | 521 |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(3) | cancellation of upstream shareholding on s. 88(1) wind-up | 65 |

30 September 2015 External T.I. 2015-0590501E5 F - Spousal sharing

An individual and his spouse each make a charitable gift of $10,000 in a year, and they wish to allocate $17,000 to the individual as his gift,...

12 February 2015 External T.I. 2014-0550771E5 F - Allocation à des bénévoles - chantier particulier

A registered charity sends volunteers on missions to developing countries and pays them an allowance of $X per day. After finding that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 3 - Paragraph 3(a) - Business Source/Reasonable Expectation of Profit | modest compensation to volunteers qua independent contractors not income | 106 |

| Tax Topics - Income Tax Act - Section 5 - Subsection 5(1) | quite unrepresentative remuneration: exempt | 106 |

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(6) | mission work under 2 years in LDCs | 109 |

16 June 2014 STEP Roundtable, 2014-0523061C6 - Trust audit issues

In the course of commenting on common audit issues for trusts, CRA stated:

Compliance issues are often encountered [respecting]…gifts by will....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(21) | capital gain distributed to different beneficiary | 137 |

| Tax Topics - Income Tax Act - Section 105 - Subsection 105(1) | benefit conferred when trust shares redeemed at undervalue | 196 |

| Tax Topics - Income Tax Act - Section 112 - Subsection 112(3.2) | taxpayer stuck with two-transaction form | 155 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Legal and other Professional Fees | legal and accounting expenses | 45 |

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(2) | settlor taking back undervalued freeze shares | 76 |

22 May 2014 External T.I. 2014-0526131E5 - Donation of a fossil

Would the value of the custody of a fossil transferred to a qualified donee can be considered a charitable gift" CRA stated tht this was a legal...

27 January 2014 Internal T.I. 2012-0472161I7 - Gifts by Will

///?page_id=909#2012-0472161I7">s. 107(2)]: The Deceased had three wills in respect of defined components of her estate, including a second will...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107 - Subsection 107(2) | gifts v. distributions made to charities | 163 |

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(5) | gifts. v. distributions made to charities | 64 |

P113 – "Gifts and Income Tax" 2013

Fair market value (FMV)—This is usually the highest dollar value you can get for your property in an open and unrestricted market, between a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Other | 42 |

2012 Ruling 2012-0466731R3 - Donation of flow-through shares

Donors (mostly Canadian-resident individuals) as well as non-donors use cash to subscribe for flow-through shares of a listed Canadian resource...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 6202.1 - Subsection 6202.1(1) | 252 |

16 April 2013 External T.I. 2013-0477981E5 F - Interpretation of Gift

A Quebec collective agreement requires each employee to annually pay a specified amount to a pre-established registered charity whose mission...

15 June 2012 External T.I. 2012-0434761E5 F - Dons liés à une police d'assurance-vie

Regarding gifts to registered charities by means of a life insurance policy of which the donor is the policyholder and the insured, CRA stated:

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(31) | donated life insurance policy to be valued on ordinary principles | 142 |

| Tax Topics - General Concepts - Fair Market Value - Other | 7 factors to be considered in valuing a donated life insurance policy | 112 |

28 November 2010 CTF Roundtable, 2010-0389111C6 - Leveraged Donation Arrangements

CRA will generally not consider advance ruling requests for leveraged donation schemes such as the one considered in Maréchaux. CRA listed...

CPC-012 Out-of-pocket expenses December 3, 1997 (Revised April 28, 2009)

Right of expense reimbursement can be gifted back to the charity

2. A charity can reimburse a volunteer for the expenses incurred on behalf of the...

29 May 2006 Internal T.I. 2006-0171931I7 F - Medical expense tax credit - XXXXXXXXXX

The taxpayer, who had been incurring medical expenses for his disabled child, made a donation to a charity, which subsequently paid the fees for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.2 - Subsection 118.2(2) - Paragraph 118.2(2)(a) | “donation” to clinic recharacterized as an eligible medical expense | 69 |

15 March 2005 Internal T.I. 2004-0108721I7 F - Don d'une licence

A software developer donated a non-exclusive licence for an unlimited period to a charity that intends to use the software for its charitable...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Property | excepting WIP, definition of property is no broader than term’s ordinary meaning | 75 |

23 February 2004 External T.I. 2003-0050641E5 F - Fiducie

In confirming its position that a taxpayer can make a charitable donation of a residual interest in the capital of a trust to a public charitable...

3 December 2003 External T.I. 2003-001859

A person allowing a charity to use office space at no charge would not be viewed as a transfer of property (i.e., a divesting of property by the...

11 September 2003 External T.I. 2003-0029145 F - CREDIT D'IMPOT POUR DON

CCRA noted that Article 1608 of the Civil Code defined a gift as:

Gift is a contract by which a person, the donor, transfers ownership of property...

CPC-017 Gift of Services 29 March 2000

Contributions of services v. repayment to charity of payment for services or expenses

2. Contributions of services, that is, of time, skills or...

19 December 2000 Internal T.I. 2000-0054467 F - VALEUR DU DON D'UNE POLICE D'ASSURANCE

In rejecting the proposition that the present value of the insured sum for a life insurance policy (rather than its cash surrender value) to be...

15 October 1999 External T.I. 9921125 F - CRÉATION D'UN LOGO -DON

An official donation receipt could not be issued to an artist for the free graphic design of a logo requested by a charity since the creation of...

24 September 1996 External T.I. 9627705 - DONATIONS/TUITION FEES

Unlike teaching or other training, religious training is not viewed as consideration for purposes of the definition of a gift.

13 August 1996 External T.I. 9600615 - TRUE GIFT

"It is the Department's practice to view donations subject to a general direction from the donor as acceptable, provided that no benefit accrues...

4 January 1996 External T.I. 9524775 - Donation of Residual Interest

"The gift of an 'object' (within the meaning of 'total cultural gifts' in subsection 118.1(1) and the disposition of an 'object' (within...

6 July 1995 External T.I. 9503565 - 118.1(1)

"A right to use property (e.g., a helicopter or equipment) for a period of time could be considered a property and a donation of a right to use a...

5 October 1994 External T.I. 9421645 - GIFT OF EQUITABLE INTEREST IN A TRUST

Listing of the four requirements that must be met in order for a transfer of property to qualify as a gift.

In valuing an equitable interest in a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Other | 13 |

21 September 1994 External T.I. 5-94149

Although a gift to a pooled fund remainder interest charitable trust could be considered to be a gift to a charity of an equitable interest in the...

13 September 1994 External T.I. 9422275 - CHARITABLE DONATIONS - SPLIT RECEIPTING

"Although gifts directed to a person designated by a donor are not eligible for an income tax receipt, donations made to a Canadian municipality...

8 August 1994 External T.I. 9415135 - REIMBURSEMENT OF EXPENSES AS CHARITABLE DONATIONS

The payment by an individual of expenses that she has incurred in performing services for the benefit of the charity does not constitute a gift to...

25 July 1994 External T.I. 9418505 - CHARITABLE DONATIONS - KOSHER FOOD PRODUCTS

A purchase of kosher-approved products from various retailers does not meet any of the conditions for a charitable gift, i.e., the voluntary...

7 June 1994 External T.I. 9405745 - GIFTS OF LIFE INSURANCE POLICIES TO CHARITIES

In response to a question whether a life insurance policy will qualify as a charitable donation where a taxpayer names more than one charity as...

19 January 1994 Internal T.I. 9326897 F - Annuities Purchased From Charitable Organizations

Providing a donor makes an irrevocable contribution directly to a registered charity in return for life annuity, it does not matter what steps the...

16 February 1994 Institute of Chartered Accountants of Nova Scotia Roundtable Q. 7, 9401450 - ANNUITIES PURCHASED FROM CHARITABLE ORGANIZATIONS

Where a registered charity has solicited individual contributions of capital to the charity in exchange for immediate guaranteed payments to the...

12 January 1993 T.I. 922833 (November 1993 Access Letter, p. 506, ¶C117-208; Tax Window, No. 28, p. 28, ¶2368)

A gift (i.e., a voluntary transfer of property without consideration and without conditions) is considered to occur where an individual has paid...

14 July 1992 External T.I. 5-921248

A taxpayer will be permitted a credit, on the purchase of an annuity from a charitable organization, based on the difference between the purchase...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 60 - Paragraph 60(a) | 19 |

24 March 1992 T.I. (March 1993 Access Letter, p. 76, ¶C109-126; Tax Window, No. 18, p. 24, ¶1827)

The irrevocable gift of a covenant which runs with land and is binding on the landowner and his successors in title can qualify as a gift.

12 March 1992 T.I. and 13 March 1992 Memorandum (Tax Window, No. 17, p. 10, ¶1802)

In order for an Indian band council to be recognized as a municipality, the council, at a minimum, must have enacted one valid by-law under...

9 October 1991 T.I. (C.T.O. Fax Service Doc. No. 233; Tax Window, No. 11, p. 18, ¶1514)

In the case where a "donation" is made to a Canadian municipality with a request that the municipality pass the money on to a community group with...

September 1991 T.I. 1991-92 [FMV excludes GST]

If a corporation or individual donated a work of art to a public cultural institution, does the tax receipt reflect the fair market value plus the...

26 August 1991 T.I. (Tax Window, No. 8, p. 20, ¶1413)

A surviving spouse may claim a tax credit in the year of death in respect of a gift bequeathed by the will of the deceased spouse, to the extent...

10 April 1991 Memorandum (Tax Window, No. 2, p. 24, ¶1191)

A charitable organization may issue an official receipt for a gift of future breeding rights.

25 February 1991 T.I. (Tax Window, Prelim. No. 3, p. 28, ¶1125)

Where the annuity payment on an annuity purchased from a charitable organization varies with fluctuations in the interest rate, it is impossible...

88 C.R. - F.Q.2

A premium paid prior to the transfer of a life insurance policy to a charity is not deductible as a charitable donation.

81 C.R. - Q. 38

A taxpayer who transfers property to a trust of which a charity is the capital beneficiary has not thereby made a gift to a charity.

IT-86R "Vow of Perpetual Poverty".

Where an individual agrees that a salary to which he is legally entitled will be paid to a religious institution and he, in return, will receive...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110 - Subsection 110(2) | 0 |

IT-226R "Gift to a Charity of a Residual Interest in Real Property or an Equitable Interest in a Trust".

Articles

Blake Bromley, "Flaunting and Flouting The Law of Gift: Canada Customs and Revenue Agency's Philanthrophobia", Estates Trusts and Pensions Journal, Vol. 21 No. 3, June 2002, p. 177.

Ghosh, Robson, "Charity and Consideration", British Tax Review, 1993, No. 6, p. 496: Discussion of the concept of no consideration.

Paragraph (c)

Administrative Policy

25 August 2021 External T.I. 2020-0866131E5 - Gifts by Will

Will a bequest made by will to a U.S. organization qualify for a charitable donation credit on the individual’s final return?

After noting...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 21 | organization exempt under IRC s. 501(c)(3) qualifies under Art. XXI(7) of the Canada-US Convention | 324 |

Subparagraph (c)(i)

Clause (c)(i)(A)

Administrative Policy

5 September 2024 External T.I. 2024-1022711E5 - Donations by a Spouse

A single individual (the “Donor”) made a gift to a qualified donee in 2017, then married in 2019. The Donor claimed donation tax credits for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4.2) | s. 152(4.2) can be utilized where the individual was not aware of, or missed claiming a deduction or a credit | 199 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(6) - Paragraph 251(6)(b) | spousal status tested at the time that spouse used her husband’s unclaimed donations | 51 |

23 January 2024 External T.I. 2023-1000021E5 - Total charitable gifts for a particular year

Can a taxpayer who makes a gift of $400 to a qualified donee in the 2023 taxation year claim a portion of the gift (e.g., $200) in the 2023...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(2.1) | claims made on a FIFO basis | 78 |

6 October 2017 APFF Financial Strategies and Instruments Roundtable Q. 9, 2017-0705231C6 F - Gift of a Life Insurance Policy and Subrogated Own

The will of Mr. Donor provided for a gift of his life insurance policy on the life of his daughter (which was originally intended to be...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 148 - Subsection 148(7) - Paragraph 148(7)(a) | gain by estate on gift of policy based on cash surrender value | 175 |

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(1) - Total Charitable Gifts - Paragraph (c) - Subparagraph (c)(i) - Clause (c)(i)(C) | claim in terminal return for charitable gift made by estate under individual’s will | 430 |

Clause (c)(i)(C)

Administrative Policy

2 December 2020 External T.I. 2017-0734261E5 - Charitable Remainder Trusts

The terms of a charitable remainder trust (“CRT”), created by the will of the deceased taxpayer to hold property of the deceased received by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(5.1) - Paragraph 118.1(5.1)(b) | will-directed formation by a GRE of a charitable remainder trust cannot benefit the deceased’s terminal return under s. 118.1(5.1)(b) | 297 |

8 May 2018 CALU Roundtable Q. 4, 2018-0745851C6 - Timing of donations from an estate

CRA has stated that a donation tax credit can be claimed on the deceased taxpayer’s final return so long as the registered charity receives a...

24 July 2017 External T.I. 2017-0698191E5 - Gift of securities by executors of a will

S. 118.1(5.1)(b) applies to most gifts made by a graduated rate estate of property that was acquired by it on and as a consequence of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(5) - Paragraph 118.1(5)(b) | an estate gift of sales proceeds of s. 70(5) property can be carried back to the terminal return | 173 |

| Tax Topics - Income Tax Act - Section 38 - Paragraph 38(a.1) - Subparagraph 38(a.1)(ii) | s. 38(a.1)(ii) zeroes post-death appreciation on estate-donated shares | 229 |

6 October 2017 APFF Financial Strategies and Instruments Roundtable Q. 9, 2017-0705231C6 F - Gift of a Life Insurance Policy and Subrogated Own

The will of Mr. Donor provided for a gift of his life insurance policy on the life of his daughter (which was originally intended to be...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 148 - Subsection 148(7) - Paragraph 148(7)(a) | gain by estate on gift of policy based on cash surrender value | 175 |

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(1) - Total Charitable Gifts - Paragraph (c) - Subparagraph (c)(i) - Clause (c)(i)(A) | no guidance on whether designating a charity as a contingent policyholder generates a charitable credit | 211 |

Subparagraph (c)(ii)

Administrative Policy

7 October 2016 APFF Financial Strategies and Instruments Roundtable Q. 8, 2016-0651731C6 F - Gift by a Former Graduated Rate Estate

The condition in s. (c)(ii)(B) of the “total charitable gifts” definition that the trust be a graduated rate estate (GRE) must be tested in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(5.1) | qualification of gift made in Year 5 of former GRE | 107 |

29 November 2016 CTF Roundtable Q. 6, 2016-0669661C6 - 84.1 and the Poulin/Turgeon Case

Under clause (c)(ii)(A) of the definition of total charitable gifts in subsection 118.1(1), can a graduated rate estate, which has made a gift,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | touchstones for accommodation party | 184 |

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) | Poulin is consistent with CRA's previous statements on employee buycos | 148 |

Clause (c)(ii)(B)

Administrative Policy

19 April 2017 External T.I. 2016-0625841E5 F - Gift of equitable interest in a trust

In order for a charitable gift by a graduated rate estate gift to be included in the total charitable donations of the estate (or the deceased)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(5.1) | s. 118.1(5.1) does not apply where a GRE donates a capital interest in a charitable residual trust created by will | 257 |

Clause (c)(ii)(C)

Administrative Policy

27 January 2020 External T.I. 2019-0799641E5 - Gift by Life Interest Trust

As a result of the death of the beneficiary of a (life-interest) trust described in s. 104(4)(a)(ii.1), the trust’s taxation year ended on the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(1) - Total Gifts - Paragraph (a) - Subparagraph (a)(iii) | a life interest trust’s “total gifts” for the death-date year could include the eligible amount of the gift of capital property made in the (immediate) post-death year | 308 |

7 June 2019 STEP Roundtable Q. 2, 2019-0798491C6 - Alter ego trust and donations

The residual beneficiaries of an alter ego trust are a class of registered charities as determined by the trustees, the trustees make payments...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(1) - Total Charitable Gifts | payments made to registered charity beneficiaries of a trust can be charitable gifts if the payments made are in the discretion of the trustees | 327 |

Total Crown Gifts

Administrative Policy

ATR-63, 20 April 1995 "Donations to Agents of the Crown"

In the absence of a specific provision to this effect in an organization's enabling legislation, RC required an opinion from the Deputy Attorney...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110.1 - Subsection 110.1(1) - Paragraph 110.1(1)(b) | 100 |

20 January 1995 External T.I. 9500415 - GIFTS TO CROWN AGENTS

Given that s. 53 of the College and Institute Act, R.S.B.C. 1979, c. 53 provided that an institution was for all its purposes an agent of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110.1 - Subsection 110.1(1) - Paragraph 110.1(1)(b) | 58 |

16 December 1992 Income Tax Severed Letter 923559A F - Crown Gifts to Agent of Her Majesty

A gift to a foundation established under the University Foundation Act (Ontario) qualifies as a gift to an agent of the provincial Crown.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110.1 - Subsection 110.1(1) - Paragraph 110.1(1)(b) | 25 |

Total Cultural Gifts

Cases

Canada v. Malette, 2004 DTC 6415, 2004 FCA 187

It was agreed that the fair market value of 981 individual works of art by a Canadian artist named Harold Feist that the taxpayer donated to the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Other | 57 |

Administrative Policy

S4-F14-C1 - Artists and Writers

General discussion

1.84 … A certified cultural property is a property of outstanding significance to Canada, pursuant to paragraph 29(3)(b) of...

1 March 2001 External T.I. 2001-0071175 F - Don de biens culturels - copropriété

CCRA indicated that a gift of an undivided interest in cultural property to a designated institution, which became the sole owner of the property...

1 February 2001 External T.I. 2000-0049655 F - Transfert entre conjoints de crédit d'impôt

Regarding whether an individual who has donated cultural property could transfer the donation credit to their spouse, CCRA confirmed that a gift...

Paragraph (a)

Administrative Policy

11 May 2004 External T.I. 2004-0069521E5 F - Don de biens culturels

After noting the view in IT-407R4, para. 13, that “a gift of an interest in an object (including a residual interest) is not viewed as the gift...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(32) | s. 248(32) inapplicable where contract of sale rather than deed of gift | 133 |

Total Ecological Gifts

Administrative Policy

4 March 2014 External T.I. 2013-0513251E5 - Ecogifts

Under the Nova Scotia policy of no net loss of wetlands, a consultant may assume a wetland restoration or creation obligation in consideration for...

5 February 1997 External T.I. 9633455 - CONDITIONAL DONATION - WHETHER A GIFT?

The grant of an easement in fulfilment of a pre-condition to subdivision approval would not qualify as a gift.

Total Gifts

Administrative Policy

25 October 1994 Internal T.I. 9423177 - DEDUCTION CHARITABLE DONATIONS

Pursuant to s. 70(2), a deceased taxpayer is considered to be another person whose only income for the year is the value of rights or things as...

Paragraph (a)

Subparagraph (a)(iii)

Administrative Policy

27 January 2020 External T.I. 2019-0799641E5 - Gift by Life Interest Trust

As a result of the death of the beneficiary of a (life-interest) trust described in s. 104(4)(a)(ii.1), the trust’s taxation year ended on the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(1) - Total Charitable Gifts - Paragraph (c) - Subparagraph (c)(ii) - Clause (c)(ii)(C) | a life interest trust’s “total gifts” made for the death-date year could be included in the eligible gifts made in the (immediate) post-death year | 223 |

Variable B

Administrative Policy

10 March 2023 External T.I. 2022-0943881E5 - Charitable Remainder Trusts

An individual settles a charitable remainder trusts (CRT) with capital property and gifts an equitable interest in the CRT to a qualified donee...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(1) - Total Charitable Gifts | gift of remainder interest in CRT is not a gift of the capital property with which the CRT was settled | 173 |

Subsection 118.1(2) - Proof of gift

Cases

Canada v. Castro, 2015 DTC 5113 [at at 6266], 2015 FCA 225, rev'g sub nom. David v. The Queen, 2014 DTC 1111 [at 3236], 2014 TCC 117

The taxpayers received charitable receipts for 10 times the amount of contributions, paid in cash, made by them to a registered charity. Woods J...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(1) - Total Charitable Gifts | inflated charitable receipt not a "benefit" vitiating a gift (donative intent issue not properly raised) | 175 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(32) | inflated charitable receipt not an "advantage" | 124 |

| Tax Topics - Income Tax Regulations - Regulation 3501 | inflated charitable receipt was invalid | 193 |

| Tax Topics - Statutory Interpretation - Interpretation Act - Section 16 | Regs read in context of enabling legislation | 82 |

| Tax Topics - Statutory Interpretation - Interpretation Act - Section 32 | inflated charitable receipt not an "advantage" | 124 |

See Also

Guobadia v. The Queen, 2016 TCC 182 (Informal Procedure)

The taxpayer was disallowed her claims for several charitable donations for the 2007 and 2008 taxation years for which she may have actually given...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 3501 | receipts invalid for showing inflated amounts | 328 |

Shahbazi v. The Queen, 2016 TCC 129 (Informal Procedure)

The taxpayer made two in–kind charitable donations of large amounts of household goods in 2006 and 2007 for which he was issued receipts for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 3501 | property description mandatory | 76 |

Slobodrian v. The Queen, 2003 DTC 1252 (TCC)

A retired professor who provided his services free of charge for a research project performed for the Department of Public Works was not entitled...

O'Brien Estate v. MNR, 91 DTC 1349 (TCC)

No receipt from a charity was required for a bequest to the charity of the residue of the testator's estate upon the death of the life tenant....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(5) | 81 |

Administrative Policy

10 February 1993 T.I. (Tax Window, No. 28, p. 20, ¶2419)

Where an individual has made an anonymous gift through an agent, she will not be able to comply with the requirements of Regulations 3501 that the...

21 October 1992 T.I. 922450 (September 1993 Access Letter, p. 420, ¶C117-201)

A charitable organization can issue a receipt for the inter vivos gift to it of an equitable interest in a trust, as described in IT-226R,...

IT-110R2 "Deductible Gifts and Official Donation Receipts"

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110.1 - Subsection 110.1(1) - Paragraph 110.1(1)(a) | 0 | |

| Tax Topics - Income Tax Regulations - Regulation 3501 | 0 |

25 October 89 T.I. (March 1990 Access Letter, ¶1150)

The total charitable gifts made in the year can be utilized before the utilization of cultural gifts from preceding taxation years, and there is...

Subsection 118.1(2.1)

Administrative Policy

23 January 2024 External T.I. 2023-1000021E5 - Total charitable gifts for a particular year

CRA confirmed that an individual can choose (under s. 118.1(1) - "total charitable gifts" – (c)(i)(A)) not to claim a charitable donation in a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(1) - Total Charitable Gifts - Paragraph (c) - Subparagraph (c)(i) - Clause (c)(i)(A) | an individual can carry forward unclaimed charitable donations | 201 |

Subsection 118.1(3) - Deduction by individuals for gifts

Administrative Policy

24 September 2003 External T.I. 2003-0028145 F - DON FAIT PAR UN PARTICULIER NON-RESIDENT

In essentially confirming that a non-resident individual making a gift in one year when the individual has no source of income in Canada can then...

Subsection 118.1(4) - Gift in year of death

Administrative Policy

31 May 1995 Internal T.I. 9504917 - GIFT BY WILL

Where an executor of an estate or a trustee has a right to encroach on the capital of the estate or trust, no tax credit in respect of a donation...

Subsection 118.1(5) - Gift by will

See Also

Turcotte v. ARQ, 2015 QCCA 396

An estate which, under the Quebec equivalent of s. 118.1(5), had claimed a charitable credit in the terminal return of the deceased for a gift...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(6) | no s. 104(6) deduction for testamentary gift distributed to charity and deducted under s. 118.1(5) | 320 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | estate could not claim both a credit in deceased’s return and deduction under s. 104(6) for donation to charity | 91 |

O'Brien Estate v. MNR, 91 DTC 1349 (TCC)

The testator in his will provided for the payment of any or all of the income of the trust fund to his nephew for life without any power to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(2) | 152 |

Administrative Policy

30 August 1999 APFF Roundtable Q. 11, 9920980 F - LEGS À UNE FONDATION

When provision is made in a will for a gift to a private foundation, but the private foundation must be established by the estate—for example,...

2 January 2014 Internal T.I. 2013-0490141I7 - Charitable Donations

{kind=link}

The Will of the "Deceased" provided that half the residue of the Estate was to be transferred to the "Foundation," a registered charity. The...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(13) | s. 118.1(5) applied where gift of subsidiary notes satisfied with subsidiary property | 192 |

27 January 2014 Internal T.I. 2012-0472161I7 - Gifts by Will

The Deceased had three wills in respect of defined components of her estate, including a second will in respect of the "Secondary Estate." CRA...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107 - Subsection 107(2) | gifts v. distributions made to charities | 163 |

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(1) - Total Charitable Gifts | gifts. v. distributions made to charities | 211 |

11 October 2013 APFF Roundtable, 2013-0492791C6 F - Gift by will

The executors named in a will, who are different than the directors of a corporation of which the testator was the shareholder, are directed in...

14 June 2012 External T.I. 2011-0430131E5 - Subsection 118.1(5) - Gift by Will

Respecting an inquiry as to the situation where a charity does not receive the property donated under the deceased's will (a specified percentage...

8 October 2010 Roundtable, 2010-0370491C6 F - Don d'actions

Could a gift of shares qualify as a gift by will where the will directs that shares with an unrealized capital gain shall be donated to a...

21 March 2007 External T.I. 2005-0142121E5 F - Don au décès d'un contribuable

Mr. X and Mrs. X are married under the community of property regime. If Mrs. X survives Mr. X and renounces the community, Mr. X's will would...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(18) | gift of shares to a charity is not of non-qualifying securities if immediately after the ownership transfer, the estate now deals at arm's length with the corporation | 172 |

25 November 2005 External T.I. 2005-0139611E5 - Gift of Art by Will

A will indicated that pieces of art in the estate that the spouse did not select within one year of death would be donated to the charity. Because...

4 April 2003 External T.I. 2002-0176305 F - DON PAR TESTAMENT

CCRA indicated that s. 118.1(5) applied where a will provided for a gift to a private foundation that was to be established after the testator's...

9 August 2000 External T.I. 2000-0029185 - ESTATE DESIGNATES CHARITY AS BENEFICIARY?

If, under the terms of a will, a guaranteed annuity had been donated to a charitable organization, the deceased would be entitled to a...

11 October 1994 External T.I. 9416675 - GIFT OF LIFE INSURANCE POLICY

"Subsection 118.1(5) of the Act does not apply in respect of the death benefit paid on a life insurance policy to a registered charity where the...

9 July 1992 External T.I. 5-921172

The payment of proceeds of a life insurance policy pursuant to a designation of a beneficiary in a document other than a will would not constitute...

20 December 1989 Memorandum (May 1990 Access Letter, ¶1229)

Where a taxpayer purchases an annuity of which its registered charity is the beneficiary on his death, or where a registered charity is named as...

16 October 89 T.I. (March 1990 Access Letter, ¶1150)

Where Mr. A in his Will provides a life interest to his surviving wife (who is not permitted to encroach), with the residue of the estate on her...

Articles

D. Bruce Ball, Brenda R. Dietrich, "Bequests and Estate Planning", Personal Tax Planning, 1999 Canadian Tax Journal, Vol. 47, No. 4, p. 995.

Paragraph 118.1(5)(a)

Subparagraph 118.1(5)(a)(iii)

Administrative Policy

16 December 2011 External T.I. 2011-0412502E5 F - Remboursement - frais de scolarité

An employer paid the tuition fees of one of its employees at a master's program. However, the employee was required to reimburse the employer...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.6 - Subsection 118.6(1) - Qualifying Educational Program | no benefit denying credit if employee is subsequently required to reimburse employer for employer-paid tuition | 142 |

Paragraph 118.1(5)(b)

Administrative Policy

7 October 2022 APFF Financial Strategies and Instruments Roundtable Q. 9, 2022-0940951C6 F - FRB créée par testament après 2015

CRA confirmed that where an individual has by will made a gift to a qualified donee of the capital interest in a charitable remainder trust...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(5.1) | a gift by will of a capital interest in a charitable remainder trust can be claimed only by the GRE, not the deceased | 338 |

24 July 2017 External T.I. 2017-0698191E5 - Gift of securities by executors of a will

Following the death of the deceased in 2016, the executors of his estate (a graduated rate estate) sell mutual fund units (whose adjusted cost...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(1) - Total Charitable Gifts - Paragraph (c) - Subparagraph (c)(i) - Clause (c)(i)(C) | estate gift of cash proceeds of s. 70(5) securities can be carried back to terminal return | 131 |

| Tax Topics - Income Tax Act - Section 38 - Paragraph 38(a.1) - Subparagraph 38(a.1)(ii) | s. 38(a.1)(ii) zeroes post-death appreciation on estate-donated shares | 229 |

Subsection 118.1(5.1) - Direct designation — insurance proceeds

Administrative Policy

7 October 2022 APFF Financial Strategies and Instruments Roundtable Q. 9, 2022-0940951C6 F - FRB créée par testament après 2015

CRA confirmed that where an individual has by will made a gift to a qualified donee of the capital interest in a charitable remainder trust...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(5) - Paragraph 118.1(5)(b) | gift of capital interest in charitable remainder trust is considered to be made by GRE when such interest vests in the charity | 314 |

19 April 2017 External T.I. 2016-0625841E5 F - Gift of equitable interest in a trust

A graduated rate estate ("GRE") donated a capital interest, in a charitable residual trust created by will, to a qualified donee. Is it eligible...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(1) - Total Charitable Gifts - Paragraph (c) - Subparagraph (c)(ii) - Clause (c)(ii)(B) | (c)(ii)(A) rather than (c)(ii)(B) applies where a GRE charitably donates a capital interest in a charitable residual trust created by will | 173 |

8 February 2017 External T.I. 2017-0684481E5 - Status as a graduated rate estate

The estate of Mr. X, who died on January 15, 2016, and which makes a charitable donation on February 15, 2017, meets all of the requirements to be...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Graduated Rate Estate | gift can be made qua GRE before paras. (c) and (d) satisfied | 46 |

7 October 2016 APFF Financial Strategies and Instruments Roundtable Q. 8, 2016-0651731C6 F - Gift by a Former Graduated Rate Estate

Where an estate which otherwise would still be a graduated rate estate but for the passage of 36 months from the date of death makes a charitable...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(1) - Total Charitable Gifts - Paragraph (c) - Subparagraph (c)(ii) | gifts made in Year 5 by a but-for GRE can only be claimed before death or in Years 5 to 10 | 389 |

10 June 2016 STEP Roundtable Q. 1, 2016-0634871C6 - GREs and Testamentary Trusts

A deceased taxpayer’s will provides that the division of the estate assets into a spousal and children’s trust. As donations now must be made...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Graduated Rate Estate | division of an estate into testamentary trusts may accelerate (perhaps back to inception) the demise of the estate as a GRE | 449 |

| Tax Topics - Income Tax Act - Section 108 - Subsection 108(1) - Testamentary Trust - Paragraph (b) | trusts on estate residue arise on death | 90 |

18 June 2015 STEP Roundtable Q. 11, 2015-0578551C6 - 2015 STEPQ11-Subsection 118.1(5.1)-sub property

Amended s. 118.1(5.1) require that a donation be a gift of "property that was acquired by the estate on and as a consequence of the death" or...

Articles

Jessica Fabbro, "Dying to Donate – Determining Charitable Donation Tax Credits on Death after 2015", Tax Topics, Wolters Kluwer, Number 2249, April 16, 2015

Allocation of gifts on death (p.2)

The amended Legislation will no longer deem all charitable gifts to have been made by the deceased immediately...

Paragraph 118.1(5.1)(b)

Administrative Policy

2023 Ruling 2020-0862441R3 - Charitable donation by Estate

Background

At the time of the proposed transactions, the Estate of the deceased held the common shares of Aco, which the Estate had acquired...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(5) - Paragraph 248(5)(b) | cash received as redemption proceeds for pref paid as stock dividend on shares was substituted property | 253 |

2 December 2020 External T.I. 2017-0734261E5 - Charitable Remainder Trusts

A terms of a charitable remainder trust (“CRT”), created by the will of a deceased taxpayer to hold property received by the graduated rate...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(1) - Total Charitable Gifts - Paragraph (c) - Subparagraph (c)(i) - Clause (c)(i)(C) | rule inapplicable to testamentary creation of charitable remainder trust | 260 |

Subsection 118.1(6) - Gifts of capital property

Administrative Policy

28 June 1993 T.I. (Tax Window, No. 32, p. 11, ¶2605)

The election under s. 118.1(6) is available in respect of the gift of an equitable interest in a trust.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(21) | 54 |

15 January 1991 T.I. (Tax Window, Prelim. No. 3, p. 5, ¶1093)

The election is not available to a spousal trust under which the trust property is to be distributed to registered charities after the death of...

20 October 89 T.I. (March 1990 Access Letter, ¶1151)

Mr. X dies leaving assets in a spousal trust with power to the trustees to encroach on capital and with the direction that the residue of the...

IT-297R2 "Gifts in Kind to Charity and Others"

Articles

Elie Roth, Tim Youdan, Chris Anderson, Kim Brown, "Taxation of Trusts Resident in Canada", Chapter 3 of Canadian Taxation of Trusts, (Canadian Tax Foundation), 2016.

Immediate reduction of capital gain/deferred credit (pp. 197-8)

A subsection 118.1(6) election can be made in respect of a gift of non-qualifying...

Subsection 118.1(7.1) - Gifts of cultural property

Administrative Policy

S4-F14-C1 - Artists and Writers

Review of requirements for s. 118.1(7.1) deduction

1.88 As discussed in ¶1.82, an individual who is a visual artist carrying on an artistic...

Articles

Innes, "Gifts of Cultural Property by Artists", Estates and Trust Journal, Volume 12, No. 3, March 1993.

Subsection 118.1(8)

Administrative Policy

T4068 Guide for the Partnership Information Return (T5013 Forms)

Partnership donations treated as made by the partners

Chapter 8 – T5013 schedules …

T5013 SCH 1, Net Income (Loss) for Income Tax Purposes ...

Subsection 118.1(11)

Cases

YELLOW POINT LODGE LTD. v. HER MAJESTY THE QUEEN, 2020 FCA 195

A taxpayer, who donated an interest in ecologically sensitive land to two qualified donees in 2008, unsuccessfully argued that the gift was not...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110.1 - Subsection 110.1(1) - Paragraph 110.1(1)(d) - Subparagraph 110.1(1)(d)(iii) | ecological gift was made in the year its ownership was transferred rather than subsequently when the certification conditions under s. 110.1(1)(d)(ii) were met | 310 |

| Tax Topics - Statutory Interpretation - French and English Version | "peut" (may) in French version accorded with a sense of the English version's "shall" | 80 |

Subsection 118.1(13) - Non-qualifying securities

Administrative Policy

2 January 2014 Internal T.I. 2013-0490141I7 - Charitable Donations

A testator bequeathed half the residue of his estate to a charitable foundation. The executors apparently satisfied this bequest, in part, by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(5) | s. 118.1(5) applied where discretion in gift mechanics | 615 |

15 July 2013 External T.I. 2013-0486701E5 - Gift by will of a non-qualifying security

There is a gift by will of a non-qualifying security ("NQS") to a qualified donee where the legal representative of the deceased individual makes...

Articles

Wolfe D. Goodman, "Commentary on Some Revenue Canada Rulings Regarding Charitable Gifts", Goodman on Estate Planning, Vol. VIII, No. 4, p. 642.

Paragraph 118.1(13)(c)

See Also

Odette (Estate) v. The Queen, 2021 TCC 65

The appellant estate donated shares of a private company (Edmette), which were non-qualifying securities, to a private foundation with which it...

Administrative Policy

7 October 2021 APFF Roundtable Q. 14, 2021-0901041C6 F - Meaning of Any consideration received by Donee

Under s. 118.1(13)(c), where a qualified donee that disposes of non-qualifying securities (“NQS”) that were gifted to it, the amount of the...

2017 Ruling 2016-0628181R3 - Donation of shares to private foundation

Background

At the date of death of B (who had survived her husband A) she held common shares of Holdco and a testamentary spousal trust held the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 129 - Subsection 129(1.2) | s. 129(1.2) denies a dividend refund on the wind-up of a private company bequeathed (but not gifted) to a private foundation | 264 |

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(1) - Total Charitable Gifts | residue paid under terms of spousal trust to charitable beneficiary was not a gift | 139 |

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(15) | gift of shares (NQS) of portfolio company retroactively deemed to be made in terminal year once company wound up into charity | 100 |

Subsection 118.1(15)

Administrative Policy

2017 Ruling 2016-0628181R3 - Donation of shares to private foundation

The estate of B gifts her shares of a portfolio holding company (“Holdco”) to a private foundation, with Holdco thereafter using its liquid...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(13) - Paragraph 118.1(13)(c) | gift of NQS in portfolio company cured when company wound-up into charity | 210 |

| Tax Topics - Income Tax Act - Section 129 - Subsection 129(1.2) | s. 129(1.2) denies a dividend refund on the wind-up of a private company bequeathed (but not gifted) to a private foundation | 264 |

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(1) - Total Charitable Gifts | residue paid under terms of spousal trust to charitable beneficiary was not a gift | 139 |

Subsection 118.1(16)

Administrative Policy

7 October 2019 Internal T.I. 2019-0801871I7 - Loanbacks

In the first situation, a corporation makes a gift to a private foundation and within the following 60 months, the foundation makes...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110.1 - Subsection 110.1(6) | there can be multiple counting of loans for purposes of reducing a gift amount under ss. 118.1(16) and 110.1(6) | 135 |

Subsection 118.1(17)

Administrative Policy

18 July 2022 Internal T.I. 2021-0921671I7 - Loanbacks and the application of 118.1(17)

A corporation (the donor) made charitable gifts in 2007, as well as in 2015 to 2017, to a registered charity (a private foundation)....

11 May 2009 External T.I. 2009-0307941E5 - Back to Back Loans provisions

2009-0307941E5 dealt with two donors (not dealing with each other at arm’s length) who each made a cash gift to the same donee, and with one of...

Finance

6 October 2017 APFF Financial Strategies and Instruments Roundtable, Q.15

2009-0307941E5 dealt with two donors (not dealing with each other at arm’s length) who each made a cash gift to the same donee, and with one of...

Subsection 118.1(18) - Non-qualifying security defined

Administrative Policy

21 March 2007 External T.I. 2005-0142121E5 F - Don au décès d'un contribuable

Mr. X and Mrs. X are married under the community of property regime and Mr. X is the sole shareholder of Realty Co. If Mr. X survives Mrs. X, all...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(5) | bequest of shares to spousal trust, with the shares then directed to a registered charity on the spouse’s is treated as a gift of an equitable trust interest by the deceased | 246 |

May 1998 Conference for Advance Life Underwriting Round Table, Q. 13, No. 9807000

The provisions of ss.118.1(18)(a) and (b) will not be applicable where father, who owns all the shares of Holdco together with a promissory note...

May 1998 Conference for Advance Life Underwriting Round Table, Q. 12, No. 9807000

A remainder interest in a charitable reminder trust is not a security described in any of paragraphs (a) to (c) in the definition of...

Subsection 118.1(19) - Excepted gift

Administrative Policy

19 June 2015 STEP Roundtable, Q. 12

Given that s. 118.1(5)(a) provides that a testamentary gift made to a public foundation is deemed to be made by the estate, will such a gift of...

Subsection 118.1(26)

Administrative Policy

31 March 2017 External T.I. 2016-0630351E5 - Return of a gift

In 1981, the taxpayer gifted a whole life insurance policy to a charitable foundation that raises funds for a specific college on condition that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 149.1 - Subsection 149.1(1) - Charitable Foundation | gift potentially could be returned by charity pursuant to a condition subsequent | 169 |

| Tax Topics - Income Tax Act - Section 110.1 - Subsection 110.1(15) | return of gift made 35 years previously by charity | 286 |