Subsection 105(1) - Benefits under trust

Cases

Cooper v. The Queen, 88 DTC 6525, [1989] 1 CTC 66 (FCTD)

The taxpayer, who was a residuary beneficiary and executor of his mother's estate, was held not to have received a benefit by virtue of an...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Illegality | income tax consequences attaching to illegal loan | 77 |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | interest-free loan | 114 |

See Also

Stevenson v. Wishart, [1987] BTC 283 (CA)

Substantial but regular payments of capital of a trust to pay the nursing-home expenses of the beneficiary were not income in her hands. "If, in...

Administrative Policy

5 May 2026 Roundtable, 2026-1089321C6 - 2026 CALU – Q.3 – Trusts and Life Insurance

A discretionary Ontario trust (the “Trust”) owns a life insurance policy insuring the life of Mrs. A, for which the Trust pays the insurance...

27 October 2020 CTF Roundtable Q. 7, 2020-0861041C6 - CTF Question 7 - Subsection 105(1)

Does the CRA position on the use of personal-use property (e.g., homes, cottages, boats and cars) by an individual beneficiary also apply to a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 73 - Subsection 73(1.01) - Paragraph 73(1.01)(c) | use by the children of the cottage held in an alter ego or joint spousal trust is not permitted | 217 |

18 April 2019 External T.I. 2017-0716451E5 F - Deduction in computing income of a trust

A discretionary family trust realized a taxable capital gain of $200,000, as well as a rental loss from a building of $100,000, with no other...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(6) - Paragraph 104(6)(b) | s. 104(6)(b) deduction cannot exceed net income | 189 |

8 June 2018 Internal T.I. 2017-0683021I7 - Assignment of capital interest in a trust

As a discretionary irrevocable personal family trust, which had non-resident beneficiaries (Y and Y’s spouse (Z)), was approaching the 21-year...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(13) | purported drop-down of trust interests to an excluded beneficiary resulted in s. 104(13) inclusions to transferors | 343 |

| Tax Topics - Income Tax Act - Section 107 - Subsection 107(5) | purported drop down of trust interests by non-resident beneficiaries to ULC was ineffective so that s. 107(2.1) applied to subsequent purported asset distribution to ULC | 192 |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | potential application of s. 56(2) to income distribution to non-qualifying transferee of trust interest | 203 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(25) - Paragraph 248(25)(a) | para. (a) refers to beneficiary in ordinary sense - and does not include assignee | 62 |

1 November 2016 Internal T.I. 2016-0663971I7 - 104(6)(b), whether amount became payable

A family trust paid income to the minor children in breach of a prohibition in the trust deed against making distributions to designated...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(24) | income that is paid to a minor beneficiary in contravention of the trust deed is non-deductible under s. 104(6) | 190 |

| Tax Topics - General Concepts - Illegality | distribution contrary to trust deed not considered to be payable | 137 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(6) | prohibited distribution from trust | 76 |

16 June 2014 STEP Roundtable, 2014-0523061C6 - Trust audit issues

In the course of commenting on common audit issues for trusts, CRA stated:

In one audit that we dealt with, the taxpayer had been the sole...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(21) | capital gain distributed to different beneficiary | 137 |

| Tax Topics - Income Tax Act - Section 112 - Subsection 112(3.2) | taxpayer stuck with two-transaction form | 155 |

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(1) - Total Charitable Gifts | executors lacked power to make gift | 92 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Legal and other Professional Fees | legal and accounting expenses | 45 |

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(2) | settlor taking back undervalued freeze shares | 76 |

10 July 2013 Internal T.I. 2013-0475501I7 F - Amounts returned to trustee/beneficiary

Father and Y were the trustees of a Quebec family trust, whose beneficiaries included father and his three children. Distributions made by the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(13) | family trust income distributed to children but repaid as reimbursement to father for family expenses was income to him, not them | 221 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(24) | distributions to children immediately paid to father | 184 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(6) | distributions to children immediately paid to father were deductible even though received by children as his agents | 179 |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(4) | payment of distributed family trust income by children to father did not engage s. 56(4) as it was only potential income to him | 175 |

6 August 2013 External T.I. 2012-0469481E5 F - Benefit under trust

An estate sold personal-use real estate to one of its beneficiaries for a price less than the property's fair market value, so that s. 69(1)(b)(i)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 52 - Subsection 52(1) | benefit on estate sale to beneficiary at under-value added to property's ACB | 133 |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(b) | taxable benefit added to acb | 133 |

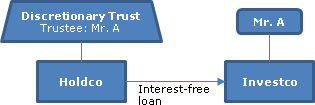

12 December 2012 Internal T.I. 2012-0464411I7 - Indirect Benefit

{kind=link}

A taxable Canadian corporation (Holdco) which is wholly-owned by a trust of which Mr. A is the sole trustee and is a discretionary beneficiary,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(e) | fee re distribution borrowing | 159 |

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) | 297 |

4 December 2012 External T.I. 2012-0470951E5 F - Technical News no. 11

Is ITTN No. 11 as to the use of personal-use property belonging to a trust is still valid? In so confirming, CRA stated:

[E]ven if the CRA...

5 July 2012 Internal T.I. 2010-0388551I7 F - Fiducie - retour de sommes

A family trust whose beneficiaries included Father, Mother, two sons (Son A and Son B) and the wife of Son A (Daughter-in-law A) but not the wife...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(2) | s. 75(2) does not apply to an estate freeze as the corp does not own its treasury shares issued to the trust | 164 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(13) | capital gain distributed by family trust to children and purportedly lent by them to their parents (also beneficiaries) was instead included in the parents’ income under s. 104(13) | 419 |

| Tax Topics - Income Tax Act - Section 110.6 - Subsection 110.6(6) | Foisy test of mental element accepted | 238 |

20 March 2007 External T.I. 2006-0173711E5 F - Paiement des impôts d'une fiducie

Mr. A is one of the two trustees for an inter vivos trust for his minor children that provides for the distribution of all income to the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) | s. 246(1) does not apply where trustee pays trust taxes | 134 |

| Tax Topics - Income Tax Act - Section 74.1 - Subsection 74.1(2) | attribution may apply where father pays income tax liability of trust for his children | 107 |

19 October 2006 Internal T.I. 2006-0173261I7 F - Avantage conféré par une fiducie

A non-income producing property of a trust, such as a cottage or boat, is used by a beneficiary, a person related to a beneficiary or by a person...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 105 - Subsection 105(2) | no s. 105(2) benefit if no trust income, and benefit to beneficiary would generate a s. 104(6) deduction | 95 |

| Tax Topics - Income Tax Act - Section 54 - Principal Residence - Paragraph (c.1) - Subparagraph (c.1)(iii) | corporation as contingent beneficiary of cottage trust precludes use of principal residence exemption | 200 |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | no s. 15(1) benefit if trust confers benefit directly on shareholder of a corporate beneficiary | 148 |

17 December 2003 Internal T.I. 2003-0047727 F - Right of Use-Deemed Trust

An individual (“Sister”), who had been experiencing financial difficulties, disposed of her home, part of which she had been renting out, to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 105 - Subsection 105(2) | potential s. 105(2) benefit where Opco pays all of the expenses on its property to a portion of which the sister of Opco’s indirect controlling shareholder has a right of (personal) use | 236 |

2 July 2003 External T.I. 2002-0180015 F - Usufruit d'un immeuble

Mr. X disposes of his principal residence and the underlying land to a corporation (whose shareholders are his son and an arm’s length person)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(b) - Subparagraph 69(1)(b)(i) | application of s. 69(1)(b)(i) on transfer of individual’s property to a corporation with him having the usufruct | 126 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | transferor to a deemed s. 248(3) trust who receives a usufruct does not deal at arm’s length with the trust | 266 |

8 April 2003 Internal T.I. 2003-0004827 F - Avantage conféré par une fiducie-par. 105(1)

An individual leased an immovable to a wholly-owned corporation. On his death, there was a legacy of the immovable to a spousal trust. The TSO...

1999 Ruling 9911853 - INCOME DISTRIBUTION REINVESTMENT PLAN

Proposed transactions

The trustees of a listed REIT will implement a distribution reinvestment plan (the "Plan") under which Canadian-resident...

21 January 1999 External T.I. 9829465 F - DIMINUTION LOYER CONTRE PRET SANS INTERET

Regarding the scope of s. 105(1), the Department stated:

[I]f a trust confers any benefit on a taxpayer, the provisions of subsection 105(1) could...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) - Subparagraph 20(1)(c)(i) | tenant can deduct interest on interest-free loan made to landlord where this was a barter exchange for free rent | 80 |

| Tax Topics - Income Tax Act - Section 9 - Computation of Profit | barter exchange of free rent for interest-free loan | 101 |

Income Tax Technical News, No. 11, September 30, 1997, "U.S. Spin-Offs (Divestitures) - Dividends in Kind"

26 August 1997 Internal T.I. 9707317 - AMOUNTS PAYABLE TO MINOR BENEFICIARIES AND TAXABLE BENEFITS FROM A TRUST

A beneficiary generally will not be assessed a taxable benefit for her rent-free use of personal-use property owned by the trust.

9 January 1997 External T.I. 9637535 - CAPITAL INTEREST DISTRIBUTION

S.105(1) does not apply to a distribution of property to which s. 107(2) is applicable.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107 - Subsection 107(2) | 16 |

31 March 1993 T.I. (Tax Window, No. 29, p. 23, ¶2459)

The favourable administrative position applying to personal-use property of an individual that is held by a trust will also apply where a house is...

19 June 1992 Interpretation 9218430 (January - February 1993 Access Letter, p. 25, ¶C104-038)

RC is not prepared to extend the decision in Cooper to benefits arising otherwise than in respect of an interest-free loan emanating from a...

91 C.R. - Q10

RC will apply the Cooper decision in similar situations.

90 C.R. - Q24

An interest-free loan made by a trust to a beneficiary does not result in a taxable benefit. S.105(1) is not restricted to non-arm's length...

89 C.R. - Q31

The use of a trust's real property by a beneficiary constitutes a benefit. However, in the case of property that would be personal use property of...

88 C.R. - Q69

Where property such as a cottage is held on trust for the use of individuals, RC generally will not seek to assess a benefit where the trust is...

87 C.R. - Q82

S.105(1) benefits should be reported on a T3 supplementary. Appropriate methods should be used to value a benefit.

85 C.R. - Q27

Where an income beneficiary (i.e., a beneficiary with no right to enforce any payment of the capital) receives an interest-free loan. RC will...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Interpretation Bulletins, etc. | 14 |

80 C.R. - Q45

S.105 will be applicable in most cases to a non-interest bearing loan made by an estate or trust to a beneficiary.

Articles

Elie Roth, Tim Youdan, Chris Anderson, Kim Brown, "Taxation of Trusts Resident in Canada", Chapter 3 of Canadian Taxation of Trusts, (Canadian Tax Foundation), 2016.

Whether a benefit to parent when trust pays for child’s necessities (p. 206)

An ancillary question is whether the payment is treated as a...

Subsection 105(2)

Administrative Policy

19 October 2006 Internal T.I. 2006-0173261I7 F - Avantage conféré par une fiducie

A non-income producing property of a trust, such as a cottage or boat, is used by a beneficiary, a person related to a beneficiary or by a person...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Principal Residence - Paragraph (c.1) - Subparagraph (c.1)(iii) | corporation as contingent beneficiary of cottage trust precludes use of principal residence exemption | 200 |

| Tax Topics - Income Tax Act - Section 105 - Subsection 105(1) | tolerance re use of trust personal use property by beneficiary or related person does not extend to unrelated person, but no benefit re payment of interest expense | 379 |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | no s. 15(1) benefit if trust confers benefit directly on shareholder of a corporate beneficiary | 148 |

17 December 2003 Internal T.I. 2003-0047727 F - Right of Use-Deemed Trust

An individual (“Sister”), who had been experiencing financial difficulties, disposed of her home, part of which she had been renting out, to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 105 - Subsection 105(1) | no s. 105(1) benefit from personal use of personal-use property of a trust | 312 |

Articles

Elie Roth, Tim Youdan, Chris Anderson, Kim Brown, "Taxation of Beneficiaries Resident in Canada", Chapter 4 of Canadian Taxation of Trusts (Canadian Tax Foundation), 2016.

Personal-use property of the trust (p. 358)

[T]he CRA has adopted the administrative position that when property owned by a trust was or would...