Subsection 107.4(1) - Qualifying disposition

Administrative Policy

2024 Ruling 2023-0962031R3 - mutual fund reorganization

Background

Five mutual fund trusts with different investment mandates (the “Reorganizing Funds” and each, Fund1, Fund2, etc.) were invested...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 132.2 - Subsection 132.2(1) - Qualifying Exchange | s. 132.2 merger of 5 funds into 1 new aggregator fund | 460 |

2021 Ruling 2021-0894161R3 - Qualifying Disposition - REIT spinout

Background

The REIT is an open unit trust whose units are redeemable by their holders and which qualifies as a mutual fund trust and real estate...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(2) | REIT spin-off transaction to new REIT likely accomplished through sideways transfer described in s. 107.4(2) | 164 |

| Tax Topics - Income Tax Act - Section 132 - Subsection 132(6) - Paragraph 132(6)(b) | indemnity given in connection with REIT spin-off transaction was on-side s. 132(6)(b) | 101 |

2018 Ruling 2018-0778961R3 - Partial transfer to new funds

Background

In connection with an arm’s length acquisition transaction, apparently of the business of managing (exchange-listed mutual fund...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(2.1) | use of s. 107.4(2.1) in transfer of portion of MFT to a new MFT | 223 |

2017 Ruling 2016-0625301R3 - Merger of two related segregated fund trusts

Background

The Taxpayer, an insurance company, established two segregated funds (Fund 1 and 2), which used portions of the premiums paid by Fund 1...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 138.1 - Subsection 138.1(1) - Paragraph 138.1(1)(a) | reallocation by insurer of securities held for one segregated fund to being held for the second segregated fund effected their transfer to the second fund viewed as a deemed trust | 125 |

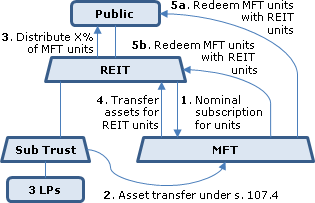

2013 Ruling 2013-0492731R3 - qualifying disposition -mutual fund trust

{kind=link}

Current structure

The Fund is an open-end mutual fund trust, whose units trade on an exchange. It owns all the units of Sub Trust (a resident...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 132 - Subsection 132(6) | MFT's trustee not to be a director of a sub | 119 |

| Tax Topics - Income Tax Act - Section 132.2 - Subsection 132.2(1) - Qualifying Exchange | elimination of REIT subtrust through s. 107.4 transfer to new "in house" MFT and s. 132.2 merger of MFT into REIT | 97 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | no disposition on MFT units consolidation back to the previous number, occurring outside a Plan of Arrangement | 107 |

2013 Ruling 2013-0488351R3 - Conversion of a MFC to a MFT

{kind=link}

The same (mutual fund corporation) taxpayer as for 2013 Ruling 2011-0395091R3 (immediately below) obtained essentially the same rulings for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 132.2 - Subsection 132.2(1) - Qualifying Exchange | conversion of MFC to MFT and subtrust elimination | 178 |

| Tax Topics - Income Tax Act - Section 21 - Subsection 21(1) | election of GP to capitalize loss before elimination of subtrust | 204 |

2013 Ruling 2011-0395091R3 - MFC to MFT Conversion

Background

Taxpayer, which is a listed mutual fund corporation, wishes to convert to a mutual fund trust (so that following the conversions...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 132.2 - Subsection 132.2(1) - Qualifying Exchange | 1059 | |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | deductible interest on internal assumption (no release) | 159 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition - Paragraph (f) | consolidation of 4 subtrusts into 1 using (f) | 178 |

17 October 2012 Ruling 2011-0428321R3 - qualifying disposition -mutual fund trust

Various mutual fund trusts (the "Funds") have several classes of outstanding units.

The sole difference among the various classes of Units is the...

Paragraph 107.4(1)(a)

Administrative Policy

9 April 2020 External T.I. 2014-0527261E5 F - Beneficial ownership discretionary power of trustees

An individual resident in Canada settles and contributes capital property to a trust governed by the Civil Code of Québec (the "C.C.Q.") under...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(1) - Paragraph 107.4(1)(i) | discretion of trustees to retain capital or income rather than distribute to the sole current beneficiary precluded s. 73(1.01)(c)(ii) application and satisfied s. 107/4(1)(i) | 291 |

| Tax Topics - General Concepts - Ownership | discretion of trustee to accumulate rather than distribute income to sole beneficiary did not detract from beneficial ownership | 269 |

| Tax Topics - Income Tax Act - Section 73 - Subsection 73(1.01) - Paragraph 73(1.01)(c) - Subparagraph 73(1.01)(c)(ii) | "right to receive" all the income not satisfied where trustees' discretion to accumulate income | 233 |

2018 Ruling 2018-0752811R3 - Transfer of Debt as Qualifying Disposition

Current Structure

The units of the REIT (a real estate investment trust) are stapled to those of Finance Trust (a portfolio investment entity and...

2017 Ruling 2017-0720591R3 - Re-org of a stapled commercial trust structure

Current Structure

The units of the REIT (a real estate investment trust) are stapled to those of Finance Trust (a portfolio investment entity and...

14 March 2012 External T.I. 2011-0423291E5 F - Fiducie pour soi-même sans limite d'âge

Two spouses (Mr. X and Ms. X) and their two adult children wish to contribute their jointly owned shares of Holdco to a newly-settled protective...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 73 - Subsection 73(1.01) - Paragraph 73(1.01)(c) - Subparagraph 73(1.01)(c)(ii) | joint protective trust would not satisfy s. 73(1.01)(c)(ii) | 180 |

| Tax Topics - Income Tax Act - Section 73 - Subsection 73(1.01) - Paragraph 73(1.01)(c) - Subparagraph 73(1.01)(c)(iii) - Clause 73(1.01)(c)(iii)(A) | two spouses separate from their children can create a joint spousal or common-law partner trust | 156 |

| Tax Topics - Income Tax Act - Section 108 - Subsection 108(1) - Testamentary Trust | tainting effect of joint spousal or common-law partner trust on subsequent testamentary trust | 211 |

2004 Ruling 2003-0053981R3 - XXXXXXXXXX

Proposed transactions

- The Fund, which is an exchange-traded mutual fund trust, will for nominal consideration subscribe for one Trust Unit of a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | elimination of MFT corporate sub through creation of MFC and 132.2 merger | 160 |

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(1) - Paragraph 107.4(1)(h) | immediate refinancing of drop-down subsidiary trust of MFT did not offend policy of para. (h) | 234 |

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(3) - Paragraph 107.4(3)(m) | units must be received on drop-down of LP to new subtrust (thereby ousting s. 107.4(2)(a)), in order to receive outside basis under s. 107.4(3)(m) | 241 |

22 April 2002 External T.I. 2002-0117135 F - Appl. de 107.4(1)a) à une fiducie du CcQ

Would s. 107.4(1)(a) be satisfied where a transferor transfers ownership of property to a Quebec trust of which he is the sole beneficiary? CCRA...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107 - Subsection 107(4.1) | s. 107(2.1) applicable to distribution by personal trust of property to beneficiary other than the settlor | 46 |

Articles

Geraint Thomas, Alastair Hudson, "Chapter 7: The Nature of a Beneficiary’s Interest", The Law of Trusts,” Oxford University Press, 2004

Under some trusts the beneficiary has rights in rem against the trust property (p. 173)

7.01 The debate on the nature of a beneficiary's interest...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Ownership | 1015 |

Paragraph 107.4(1)(h)

Administrative Policy

2004 Ruling 2003-0053981R3 - XXXXXXXXXX

A publicly-trade mutual fund trust (the "Fund") eliminated a corporate subsidiary ("Holdings") by incorporating a subsidiary ("MFC") with a modest...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(1) - Paragraph 107.4(1)(a) | qualifying drop-down of partnership units to subsidiary unit trust where s. 107.4(2)(a) was ousted due to units issuance | 246 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | elimination of MFT corporate sub through creation of MFC and 132.2 merger | 160 |

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(3) - Paragraph 107.4(3)(m) | units must be received on drop-down of LP to new subtrust (thereby ousting s. 107.4(2)(a)), in order to receive outside basis under s. 107.4(3)(m) | 241 |

Paragraph 107.4(1)(i)

Administrative Policy

9 April 2020 External T.I. 2014-0527261E5 F - Beneficial ownership discretionary power of trustees

An individual resident in Canada settles and contributes capital property to a Quebec trust under which the settlor is one of the two trustees and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(1) - Paragraph 107.4(1)(a) | discretion of trustees to retain capital or income rather than distribute to the sole current beneficiary does not preclude the latter being the beneficial owner | 277 |

| Tax Topics - General Concepts - Ownership | discretion of trustee to accumulate rather than distribute income to sole beneficiary did not detract from beneficial ownership | 269 |

| Tax Topics - Income Tax Act - Section 73 - Subsection 73(1.01) - Paragraph 73(1.01)(c) - Subparagraph 73(1.01)(c)(ii) | "right to receive" all the income not satisfied where trustees' discretion to accumulate income | 233 |

Subsection 107.4(2) - Application of paragraph (1)(a)

Administrative Policy

2021 Ruling 2021-0894161R3 - Qualifying Disposition - REIT spinout

CRA ruled on a transactions for the spin-off by an existing REIT of a portion of its operations (the “Segment”) to a newly formed REIT.

In...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(1) | use of s. 107.4(1) to effect the spin-off by a REIT of a portion of its operations to a new REIT | 1191 |

| Tax Topics - Income Tax Act - Section 132 - Subsection 132(6) - Paragraph 132(6)(b) | indemnity given in connection with REIT spin-off transaction was on-side s. 132(6)(b) | 101 |

Paragraph 107.4(2)(a)

Administrative Policy

2017 Ruling 2016-0660321R3 - Reorg of REIT to simplify multi-tier structure

Overview

A Canadian REIT (the “Fund”) holds the units and notes of a subsidiary unit trust (“Sub-Trust”), whose principal asset is most of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 132.2 - Subsection 132.2(1) - Qualifying Exchange | use of the s.132.2 merger and a renunciation of most of the units otherwise issuable on the merger in order to eliminate a REIT corporate subsidiary held through an LP and a sub-trust | 1006 |

| Tax Topics - Income Tax Act - Section 98 - Subsection 98(3) | drop down of LP 1 into LP 2 followed by immediate s. 98(3) wind-up of LP 1 into LP 2 and GP of LP1, followed by immediate taxable sale by GP to LP 2 | 146 |

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) | no taxable benefit where wholly-owned partnership renounces the right to receive units of its “parent” REIT | 325 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | no disposition of partnership interests or property on conversion of general to limited partnership or adding right of renunciation of a MFT unitholder | 165 |

| Tax Topics - Income Tax Act - Section 132.2 - Subsection 132.2(3) - Paragraph 132.2(3)(g) - Subaragraph 132.2(3)(g)(vi) - Clause 132.2(3)(g)(vi)(C) - Subclause 132.2(3)(g)(vi)(C)(I) | renunciation by subsidiary partnership of transferee MFT of units that otherwise would be issuable on the redemption of its incestuous holding in transferor MFC | 245 |

2003 Ruling 2003-000498C - Qualifying disposition from trust to Sub

Current structure

The Fund, which is an exchange-listed mutual fund trust, holds shares and debt (the Corporation Shares and the Corporation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(3) - Paragraph 107.4(3)(m) | no increase to ACB of subtrust units where dropdown to the subtrust for no consideration | 55 |

Subsection 107.4(2.1)

Administrative Policy

2018 Ruling 2018-0778961R3 - Partial transfer to new funds

In connection with an arm’s length acquisition transaction, apparently of the business of managing exchange-listed mutual fund trusts, holders...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(1) | use of s. 107.4 transfers to split up ETFs | 599 |

Subsection 107.4(3) - Tax consequences of qualifying dispositions

Administrative Policy

20 March 2013 External T.I. 2013-0474861E5 - Subparagraph 107.4(3)(a)(i) election

There is currently no prescribed form available for the subparagraph 107.4(3)(a)(i) election. In place of a prescribed form, the transferor trust...

7 December 2000 External T.I. 2000-0032685 - QUALIFIED DISPOSITION SEGREGATED FUNDS

If a policyholder does not realize any disposition of an interest in a segregated fund contract (viewed as analogous to a capital interest in a...

Paragraph 107.4(3)(m)

Administrative Policy

2004 Ruling 2003-0053981R3 - XXXXXXXXXX

The Fund, which is an exchange-traded mutual fund trust, will for nominal consideration subscribe for one Trust Unit of a unit trust (the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(1) - Paragraph 107.4(1)(a) | qualifying drop-down of partnership units to subsidiary unit trust where s. 107.4(2)(a) was ousted due to units issuance | 246 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | elimination of MFT corporate sub through creation of MFC and 132.2 merger | 160 |

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(1) - Paragraph 107.4(1)(h) | immediate refinancing of drop-down subsidiary trust of MFT did not offend policy of para. (h) | 234 |

2003 Ruling 2003-000498C - Qualifying disposition from trust to Sub

On a transfer by a mutual fund trust (the "Fund") of shares and notes of a subsidiary to a subsidiary trust (the "Trust") of the Fund for no...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(2) - Paragraph 107.4(2)(a) | s. 107.4(2)(a) applies where drop-down by MFT of corporate sub to sub trust for no consideration | 245 |

Subsection 107.4(4)

Administrative Policy

17 March 2003 External T.I. 2002-0130685 F - Limite inférieure - JVM Participation

In response to 10 conceptual questions regarding s. 107.4(4), CCRA noted inter alia:

- “the primary purpose of subsection 107.4(4) was to provide...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 108 - Subsection 108(1) - Trust - Paragraph (g) | meaning of vested indefeasibly | 56 |