Cases

TDL Group Co. v. Canada, 2016 FCA 67

The ultimate parent of the taxpayer's group ("Wendy's International") lent Cdn.$234 million to a US subsidiary ("Delcan") at 7% interest, which...

Swirsky v. Canada, 2014 DTC 5037 [at at 6723], 2014 FCA 36, aff'g 2013 TCC 73, 2013 DTC 1078 [at 431]

{kind=link}

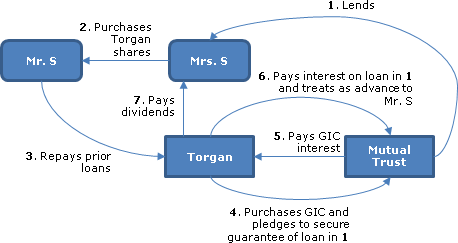

The taxpayer transferred shares in a family real estate development company ("Torgan") to his wife ("Ms. Swirsky") on three occasions in 1991,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Purpose/Intention | no objectively reasonable income-producing purpose | 85 |

| Tax Topics - General Concepts - Onus | applying GAAR at confirmation stage doesn't shift onus | 73 |

Collins v. Canada, 2010 DTC 5028 [at at 6625], 2010 FCA 12

The taxpayers owed approximately $2.7 million on mortgage loans including substantial amounts of interest that previously had been agreed to be...

Scragg v. Canada, 2009 DTC 6024, 2009 FCA 180

Before finding that the taxpayer had failed to discharge the onus on him to establish that money borrowed by him had been used by him to invest in...

Novopharm Ltd. v. Canada, 2003 DTC 5195, 2003 FCA 112

A profitable Canadian corporation ("Novopharm") acquired losses approximating $20 million of an arm's-length corporation ("Lossco") through a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 390 |

Stewart v. Canada, 2002 DTC 6969, 2002 SCC 46, [2002] 2 S.C.R. 645

After finding that rental condominium properties of the taxpayer represented a source of income and that the interest expense on related...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Business | "business" has its broad common law definition | 95 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Personal or Living Expenses | 12 | |

| Tax Topics - Income Tax Act - Section 3 - Paragraph 3(a) - Business Source/Reasonable Expectation of Profit | no reasonable expectation of profit test if no personal element | 353 |

| Tax Topics - Statutory Interpretation - Deference to Parliament/ No judicial legislation | avoid judicial rule-making | 80 |

Dansereau v. The Queen, 2001 DTC 5642, 2001 FCA 305

The taxpayer, who was a teacher by profession, owned eight rent-producing property of which seven had to be sold, following a recession, with the...

Canada v. Milewski, 2000 DTC 6559 (FCA)

The taxpayer financed virtually all of his investment in a limited partnership carrying on the business of renting apartments with borrowed money...

Chase Manhattan Bank of Canada v. Canada, 2000 DTC 6018 (FCA)

A subsidiary ("Leasing") of the appellant (the "Bank") had been financed with loan capital received by the Bank, which subsequently had been...

Shell Canada Ltd. v. Canada, 99 DTC 5669, [1999] 3 S.C.R. 622, [1999] 4 CTC 313

The taxpayer borrowed NZ$150 million from three non-resident banks by issuing five-year debentures bearing interest at 15.40%. A comparable...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Substance | legal relationships prevail over economic realities | 201 |

| Tax Topics - General Concepts - Tax Avoidance | taxpayers entitled to rely on structure of their transactions | 170 |

| Tax Topics - Income Tax Act - Section 67 | s. 67 does not apply where provisions, having their own internal limiting clauses, apply | 96 |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Foreign Exchange | FX hedging gain was capital gain as hedged borrowing was on capital account | 225 |

| Tax Topics - Statutory Interpretation - Specific v. General Provisions | general reasonableness provision should not be applied to interest which has its specific s. 20(1)(c) reasonableness limitation | 96 |

Singleton v. R., 99 DTC 5362, [1999] 3 CTC 446 (FCA), aff'd supra.

The taxpayer, who was a partner in a small law firm, withdrew $300,000 from his capital account in order to help fund the purchase of a home....

Hudson Bay Mining & Smelting Co. v. R., 99 DTC 5269, [1999] 3 CTC 76 (FCA)

The taxpayer repurchased some of its outstanding debentures through brokers. The price negotiations with the vendor focussed on the price...

Ludmer v. Ministre Du Revenu National, 99 DTC 5153, [1999] 3 CTC 601 (FCA), rev'd supra

A group of Canadian investors, including the taxpayers, invested in the shares of two Panamanian corporations (collectively, "Justinian") whose...

Elmridge Country Club Inc. v. The Queen, 99 DTC 5127 (FCA)

The taxpayer, which was a country club that was found to be subject to tax on interest from the investment of surplus funds pursuant to s. 149(5),...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 149 - Subsection 149(5) | 45 |

Laliberté v. R., 98 DTC 6604, [1999] 2 CTC 178 (FCA)

The taxpayer's husband borrowed $20,000, on the security of a mortgage on a rental property, to pay legal costs in connection with a civil suit...

The Queen v. Sherway Centre Ltd., 98 DTC 6121 (FCA)

A twenty-year bond financing that was secured on a shopping centre owned by the taxpayer provided for the payment, in addition to interest at a...

Parthenon Investments Ltd. v. Canada (National Revenue), 97 DTC 5343 (FCA)

The taxpayer was not entitled to deduct interest on a promissory note that it had delivered in payment of a dividend to its parent corporation and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Canadian-Controlled Private Corporation | control means ultimate control | 141 |

74712 Alberta Ltd. v. Minister of National Revenue, 97 DTC 5126, [1997] 2 CTC 30 (FCA)

The taxpayer guaranteed a loan which the CIBC made to its parent corporation ("Trennd"), for on-lending to various corporations within the group...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Purpose/Intention | 57 |

Brill v. The Queen, 96 DTC 6572, [1997] 1 CTC 2 (FCA)

Interest that accrued between January 1, 1987 and the date of judicial sale of a property whose purchase had been financed with borrowed money,...

Tennant v. M.N.R., 96 DTC 6121, [1996] 1 S.C.R. 305

The taxpayer used the proceeds of a $1 million bank loan to subscribe for common shares of an arm's length corporation ("Realwest"). After his...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Reciprocity | 66 |

Riddell v. The Queen, 95 DTC 5526, [1995] 2 CTC 362 (FCTD)

A corporation paid the interest on a loan that had refinanced a loan received by its individual shareholder in order to finance a purchase by him...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Interpretation Bulletins, etc. | 112 |

Farn v. The Queen, 95 DTC 5426, [1995] 1 CTC 152, [1995] DTC 5455 (FCTD)

Interest on mortgages owing by the taxpayers in their 1987 taxation years was found to be non-deductible given that they had defaulted on the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 79 | 120 | |

| Tax Topics - Other Legislation/Constitution - Federal - Official Languages Act - Section 13 | 32 |

Canassurance, Compagnie d'Assurance-Vie Inc. v. The Queen, 94 DTC 6186, [1994] 2 CTC 37 (FCA)

The taxpayer, which was a mutual life insurance company without share capital, received subscriptions to its reserve fund from the Quebec Hospital...

The Queen v. Mandryk, 92 DTC 6329, [1992] 1 CTC 317 (FCA)

Interest paid by the taxpayer on loans which were used to make advances to an insolvent corporation was non-deductible. In response to a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Loss v. Loss | guarantee made qua shareholder | 104 |

Edward Bowes v. Minister of National Revenue, 91 D.T.C 5310, [1991] 1 CTC 68 (FCTD)

The taxpayer was unable to establish that interest on money which initially had been borrowed to acquire a personal residence later was used to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Evidence | 52 |

Livingston International Inc. v. The Queen, 91 DTC 5066, [1991] 1 CTC 155 (FCTD), aff'd 92 DTC 6197 (FCA)

The taxpayer borrowed money from its parent in order to redeem high-low preference shares which had been issued on the amalgamation of the two...

Haro Pacific Enterprises Ltd. v. The Queen, 90 DTC 6583, [1990] 2 CTC 493 (FCTD)

Amounts styled as "interest" which were paid pursuant to a promissory note which provided that the interest was to be paid "at such times and such...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 97 - Subsection 97(2) | capital distribution part of consideration for land contribution | 149 |

The Queen v. Attaie, 90 DTC 6413 (FCA)

The taxpayer took out a mortgage loan to help finance the acquisition of a Toronto house. The Minister allowed the deduction of interest for the...

Kalthoff v. The Queen, 90 DTC 6378, [1990] 1 CTC 336 (FCTD), aff'd 92 DTC 6001 (FCA)

On March 26, 1980 the taxpayer entered into an agreement for the purchase of land for a purchase price of $525,000. The agreement provided that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(e) | 37 |

The Queen v. MerBan Capital Corp. Ltd., 89 DTC 5404, [1989] 2 CTC 246 (FCA)

The taxpayer, which was engaged in the business of merchant banking, incorporated a subsidiary ("MKH") which in turn incorporated another...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Personality | 107 | |

| Tax Topics - General Concepts - Separate Existence | 112 | |

| Tax Topics - Income Tax Act - Section 167 - Subsection 167(5) | 52 | |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) | 34 | |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Financing Expenditures | guarantee fees of merchant banker paid respecting bank loans made to subsidiaries with investments were capital expenditures | 207 |

| Tax Topics - Income Tax Act - Section 180 - Subsection 180(3) | 30 | |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(e) | 157 |

The Queen v. Malik, 89 DTC 5141, [1989] 1 CTC 316 (FCTD)

Interest on loans which remained outstanding after the taxpayer sold a rental property at a loss was found, following Emerson, to be non-deductible.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 8 - Subsection 8(1) - Paragraph 8(1)(f) | 95 |

Holotnak v. The Queen, 87 DTC 5443, [1987] 2 CTC 217 (FCTD), aff'd 89 DTC 5527 (FCA)

The direct use of the proceeds of a loan secured by the taxpayer's rental property was the purchase of his residence, and the interest accordingly...

Bowater Canadian Ltd. v. The Queen, 87 DTC 5287, [1987] 2 CTC 47 (FCA)

After a company (Bulkley") in which the taxpayer and another corporation ("Bathurst") had substantial loan and share investments began...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Loans and Financing Charges | 236 |

Bronfman Trust v. The Queen, [1987] 1 S.C.R. 32, 87 DTC 5059, [1987] 1 CTC 117

Interest on money borrowed by trustees in order to make discretionary capital allocations to beneficiaries was non-deductible. Although the...

Emerson v. The Queen, 86 DTC 6184, [1986] 1 CTC 422 (FCA)

The taxpayer sought to deduct interest charged on borrowed money that was used to repay a previous loan that had financed the purchase of shares....

Toolsie v. The Queen, 86 DTC 6117, [1986] 1 CTC 216 (FCTD)

The taxpayer was found to have borrowed $37,500 to acquire his residence, with the loan being secured by mortgages on two rental properties. The...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Real Estate | lawyer with history of transacting in properties | 67 |

The Queen v. Terra Mining & Exploration Ltd. (N.P.L.), 84 DTC 6185, [1984] CTC 176 (FCTD)

The parenthetical expression refers to the method regularly followed by the taxpayer for financial statement purposes. Thus, where the taxpayer...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Accounting Principles | 68 | |

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(c) | 62 | |

| Tax Topics - Statutory Interpretation - Scheme | 36 |

Alberta and Southern Gas Co. Ltd. v. The Queen, 76 DTC 6362, [1976] CTC 639 (FCTD), aff'd 77 DTC 5244 [1977] CTC 388 (FCA), aff'd 78 DTC 6566, [1978] CTC 780, [1979] 1 S.C.R. 36

The taxpayer borrowed $4 million (apparently at a commercial rate of interest) from its banker and paid that sum to Amoco in consideration of...

R. v. Balmoral Holdings Ltd., 75 DTC 5296, [1975] C.T.C. 397, [1975] C.T.C. 397 #2 (FCTD)

The taxpayer, one of whose objects was to provide management services to controlled corporations and which was prohibited by its objects from...

Sternthal v. The Queen, 74 DTC 6646, [1974] CTC 851 (FCTD)

The taxpayer, who had a large excess of assets over liabilities, borrowed $246,800 from three private companies in which he had investments and on...

Byke Estate v. The Queen, 74 DTC 6585, [1974] CTC 763 (FCTD)

A company purchased by the taxpayers paid interest on money borrowed by the taxpayers to acquire its shares. The taxpayers were not permitted to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | 102 |

MNR v. Yonge-Eglinton Building Ltd., 74 DTC 6180, [1974] CTC 209 (FCA)

In connection with the interim construction of a building, the taxpayer agreed to pay interest on the borrowed money at a rate of 9% plus 1% of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(e) | 177 |

Matheson v. The Queen, 74 DTC 6176, [1974] CTC 186 (FCTD)

Interest paid by the taxpayer on a bank loan the proceeds of which had been used to refinance an interest-free loan to a controlled company...

Lakeview Gardens Corp. v. MNR, 73 DTC 5437, [1973] CTC 586 (FCTD)

In 1954 the taxpayer borrowed money to acquire land inventory, and in 1962 acquired shares (generating exempt dividend income). The Minister was...

MNR v. Mid-West Abrasive Co. of Canada Ltd., 73 DTC 5429, [1973] CTC 548 (FCTD)

The taxpayer during its 1960 and 1961 taxation years borrowed $210,000 from its U.S. parent. The promissory notes stated "interest will be paid if...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | indefinite payment arrangements for interest | 76 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 76 |

McLaws v. Minister of National Revenue, 72 DTC 6149, [1972] CTC 165, [1974] S.C.R. 887

The taxpayer provided his personal guarantee to the bank when it was threatening to call the loans it had made to a corporation owned by the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Loss v. Loss | 104 |

Trans-Prairie Pipelines Ltd. v. MNR, 70 DTC 6351, [1970] CTC 537 (Ex Ct)

When the taxpayer started business in 1954 it raised the capital required for its business by issuing common shares for $140,006 and preferred...

D.W.S. Corp. v. MNR, 68 DTC 5045, [1968] CTC 65 (Ex Ct), briefly aff'd 69 DTC 5203 (SCC)

The taxpayer (a distilling company) borrowed $3,485,000 from a U.S. subsidiary at 6% interest and on-lent those funds to another subsidiary...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Foreign Exchange | FX loss on USD trade payables incurred in the course of trading was deductible | 142 |

Société Coopérative Agricole du Canton de Granby v. The Minister of National Revenue, 61 DTC 1205, [1961] CTC 326, [1961] S.C.R. 671

In finding that a purported issuance of preference shares was in fact a loan, with the result that the interest thereon was deductible, Cartwright...

Canada Safeway Ltd. V. Minister of National Revenue, 57 DTC 1239, [1957] CTC 335, [1957] S.C.R. 717

The taxpayer, which carried on a retail chain grocery business, used the proceeds of a debenture issue to purchase the shares of a sister company...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Financing Expenditures | interest expense generally on capital account | 59 |

Interior Breweries Ltd. v. MNR, 55 DTC 1090, [1955] CTC 143 (Ex Ct)

The taxpayer used money which it had borrowed under temporary bridge financing from a bank to acquire the shares of other brewing...

Stock Exchange Building Corp. Ltd. v. Minister of National Revenue, [1955] S.C.R. 235, 55 DTC 1014, [1955] CTC 5

The taxpayer realized $90 for each $100 bond issued by it in 1929 and invested the net proceeds in an office building. The taxpayer was only...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Financing Expenditures | compound interest payable on capital account | 42 |

Minister of National Revenue v. McCool, 49 DTC 700, [1949] CTC 395, [1950] S.C.R. 80

An individual transferred the assets of his business to the taxpayer in consideration for the assumption of his business liabilities, the issuance...

Montreal Coke and Manufacturing Co. v. MNR, [1944] A.C. 126, [1944] CTC 94, [1944] UKPC 11 (P.C.)

In connection with the retirement of old bonds and the issuance of replacement bonds, the taxpayer had to pay interest on both the old bonds and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Loans and Financing Charges | 79 | |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Financing Expenditures | refinancing fees not incurred in the course of earning income | 163 |

See Also

Gervais Auto Inc. v. Agence du revenu du Québec, 2021 QCCA 459

The taxpayer financed its inventory of used automobiles held for resale through unsecured loans of $2 million (for a total of $6 million) from its...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Onus | Court of Appeal free to re-weigh the evidence once the failure of the trial judge to apply onus correctly was established | 318 |

| Tax Topics - Income Tax Act - Section 67 | interest rate fell within a reasonable range | 263 |

Gervais Auto Inc. v. Agence du revenu du Québec, 2019 QCCQ 5894, rev'd 2021 QCCA 459

The taxpayer financed its inventory of used automobiles held for resale through unsecured loans from its shareholders, who were the three...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 67 | taxpayer could not displace ARQ assessment of interest on basis of low point in interest-rate range provided by taxpayer's expert | 208 |

Plains Midstream Canada ULC v. Canada, 2019 FCA 57

As part of a complex set of transactions, a predecessor of the taxpayer agreed to assume a $225M loan that was due in perhaps 43-years’ time and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 16 - Subsection 16(1) | s. 16(1) can only apply to a debtor if it equally applies to the creditor | 398 |

Solar Power Network Inc. v. ClearFlow Energy Finance Corp., 2018 ONCA 727

The typical loan agreement for a loan (a “Loan”) by ClearFlow to Solar Power Network (“SPN”) provided for a base interest rate of 12% p.a....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Financial Service - Paragraph (f) | additional discount fee, but not admin fee, was interest rather than fee | 226 |

Solar Power Network Inc. v. ClearFlow Energy Finance Corp., 2018 ONSC 7286, rev'd 2018 ONCA 727

The typical loan agreement for a loan (a “Loan”) by the respondent (“ClearFlow”) to the applicant (“SPN”) provided for a base interest...

R. v. Golini, 2016 TCC 174

A family corporation (“Ontario”) used proceeds of a daylight loan to redeem shares of Holdco, which used those proceeds to purchase a life...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | a loan to a shareholder with recourse limited to an asset pledged by the corporation was a shareholder benefit | 589 |

| Tax Topics - General Concepts - Sham | sham doctrine did not apply to a "minor pretence" | 338 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | use of corporate asset to create PUC was abuse of s. 84(1) | 250 |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(1) | policy of 84(1) | 219 |

ENMAX Energy Corp. v. Alberta, 2016 ABQB 334, rev'd 2018 ABCA 147

Enmax Energy Corporation (“EEC”) was a wholly owned subsidiary of Enmax Corporation (“EC”), which in turn was wholly-owned by the City of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 67 | Gabco test implies a range | 122 |

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) | arm's length comparables for intercompany interest rate not dispositive | 308 |

Re Nortel Networks Corporation, 2015 ONCA 681

Nortel proceedings under the Companies’ Creditors Arrangement Act (Canada) and Chapter 11 of the U.S. Bankruptcy Code had been on-going since...

The TDL Group Co. v. The Queen, 2015 DTC 1098 [at at 567], 2015 TCC 60, rev'd supra.

The ultimate parent of the taxpayer's group ("Wendy's International") made a US$147,654,000 loan to a US subsidiary ("Delcan") at 7% interest,...

McLarty v. The Queen, 2014 DTC 1162 [at at 3556], 2014 TCC 30

On December 31, 1993, the taxpayer and other parties to a joint venture acquired rights to exploit seismic data in consideration for $975,000 cash...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Agency | participations contrary to agreement were disregarded | 111 |

| Tax Topics - General Concepts - Illegality | participations contrary to agreement were disregarded | 113 |

| Tax Topics - General Concepts - Sham | sham cannot apply to just part of transaction | 145 |

| Tax Topics - General Concepts - Tax Avoidance | sham cannot apply to just part of transaction | 145 |

| Tax Topics - Income Tax Act - Section 67 | leveraged purchase of seismic data at arm's length was presumptively reasonable | 296 |

Doulis v. The Queen, 2014 DTC 1054 [at at 2933], 2014 TCC 26 (Informal Procedure)

Lamarre J dismissed the taxpayer's arguments that he should be able to deduct interest on tax arrears as a business expense. Such deductions were...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(t) | tax arrears interest is not a business expense | 86 |

| Tax Topics - Income Tax Act - Section 9 - Interest Income | tax arrears interest is not a business expense | 86 |

Garber v. The Queen, 2014 DTC 1045 [at at 2812], 2014 TCC 1

The taxpayers bought units in limited partnerships, each of which was to acquire a large yacht to be used for catered vacation charters. The...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 13 - Subsection 13(21) - Depreciable Property | title not held by GP on behalf of partnership | 122 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Income-Producing Purpose | expenses mere window-dressing | 135 |

| Tax Topics - Income Tax Act - Section 3 - Paragraph 3(a) - Business Source/Reasonable Expectation of Profit | fraudulent scheme not a source | 240 |

| Tax Topics - Income Tax Act - Section 96 | GP had fraudulent intention | 241 |

| Tax Topics - Income Tax Regulations - Regulation 1102 - Subsection 1102(1) - Paragraph 1102(1)(c) | asset was mere window-dressing | 146 |

A.P. Toldo Holding Corporation v. The Queen, 2014 DTC 1042 [at at 2787], 2013 TCC 416

The taxpayer was a holding company for various direct and indirect subsidiaries which carried on an operating business. To resolve a shareholder...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Financing Expenditures | no retained earnings or stated capital | 200 |

Collins v. The Queen, 2009 DTC 286, 2009 TCC 56, rev'd supra

The taxpayers owed approximately $2.7 million on mortgage loans including substantial amounts of interest that previously had been agreed to be...

Estate of Mary Rizak c/o George Jehn v. The Queen, 2008 DTC 4460, 2008 TCC 434 (Informal Procedure)

The taxpayer was unable to deduct interest on an alleged deferred obligation to subscribe for further shares in a company in which it had made an...

Tesainer v. The Queen, 2008 DTC 2807, 2008 TCC 101, rev'd 2009 FCA 33

Interest on money borrowed by the taxpayers to invest in a real estate partnership was found, in reliance on the decision in Moufarrège v. Quebec...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(2) - Paragraph 53(2)(c) - Subparagraph 53(2)(c)(v) | 49 |

Lipson v. The Queen, 2006 DTC 2687, 2006 TCC 148, aff'd supra.

The taxpayer's wife ("Jordanna") borrowed $562,500 from the Bank of Montreal to fund the purchase of shares of a family company from the taxpayer...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 235 |

Crown Forest Industries Ltd. v. The Queen, 2006 DTC 2321, 2006 TCC 47

The taxpayer, which consistently had filed for income tax purposes using the cash basis for computing its deductible interest, was permitted to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Stare Decisis | 110 |

Moufarrège v. Quebec (Deputy Minister of Revenue), 2005 DTC 5605, [2005] 2 S.C.R. 598, 2005 SCC 53

Interest on loans incurred to purchase real property and shares of a company was not deductible under s. 160(a) of the Taxation Act (Quebec)...

International Colin Energy Corp. v. The Queen, 2002 DTC 2185, 2002 CanLII 47015 (TCC)

The taxpayer paid a fee to a financial advisor, calculated as 0.7% of the market value of its equity and of the amount of its long-term debt net...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Income-Producing Purpose | finding an acquirer to maximize shareholder value | 168 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Shareholder Assistance | advisor fees incurred to maximize shareholder value did not create a capital structure, and were deductible | 141 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(e) | 183 |

Hill v. The Queen, 2002 DTC 1749 (TCC)

Under a non-recourse loan owing by the taxpayer and other tenants of an office building to the non-resident landlord, 90% of the cash flow was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Payment & Receipt | funds to support cheques | 143 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | no Crown explanation of different treatment of simple interest | 241 |

722540 Ontario Inc. v. The Queen, 2002 DTC 1307 (TCC)

A profitable Canadian corporation ("Novopharm") acquired losses approximating $20 million of an arm's-length corporation ("Lossco") through a...

Canada v. Confederation Life Insurance Co., [2001] OJ No. 2610 (Ont SCJ)

Two financial institutions purchased commercial paper in the form of discount notes which had a maturity date subsequent to the date of a...

Sudbrack v. The Queen, 2000 DTC 2521 (TCC)

Bowman A.C.J. affirmed a reassessment of the Minister which denied 15% of the interest on a loan used to renovate a tourist guest home based on...

Dansereau v. The Queen, 2000 DTC 1559 (TCC) (Informal Procedure)

A number of properties of the taxpayer were sold by the mortgagees under power of sale for less than the amounts owing. The mortgagees required...

Meggitt v. The Queen, 2000 DTC 1448 (TCC) (Informal Procedure)

The taxpayer argued that by borrowing to purchase her home, she was able to retain a rental property. In rejecting this argument and finding that...

Gagnon v. R., 99 DTC 845, [1999] 4 CTC 2426 (TCC)

Bowman TCJ. indicated (at p. 849) that the fact that interest payments were made on money borrowed through non-recourse loans that were secured by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Income-Producing Purpose | 80 | |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(m) | software receipt amortized | 39 |

| Tax Topics - Income Tax Act - Section 67 | 70 |

C.R.B. Logging Co. v. R, 99 DTC 840, [1999] 2 CTC 2279 (TCC), aff'd , 2000 DTC 6547, Docket: A-242-99 (FCA)

The taxpayer borrowed approximately $1.9 million from a Canadian bank and used the proceeds to subscribe for preferred shares of a company...

Lewisporte Holdings Ltd. v. R., [1999] 1 CTC 2056, 99 DTC 253, 1998 CanLII 185

After a bank crystallized two floating debentures for debts owing by a land development company and its parent, the taxpayer used borrowed money...

Chisholm v. The Queen, 99 DTC 150, [1999] 1 CTC 2498 (TCC)

The taxpayer gifted a portion of his common shares of a family small business corporation to a trust for his children utilizing the rollover...

Aitchison v. The Queen, 98 DTC 1956, [1995] 2 CTC 2558 (TCC)

The taxpayer borrowed money in order to acquire shares of a private mortgage investment corporation which, some years later, redeemed the shares,...

Canadian Pacific Ltd. v. The Queen, docket 95-3534-IT-G (TCC)

Although he would have decided the appeal on a different basis if not bound by authority, Bonner TCJ. applied the finding in the Shell Canada case...

Mohammad v. R., 97 DTC 5503, [1997] 3 C.T.C. 321 (FCA)

After finding that it was not proper of the Tax Court Judge to apply s. 67 to disallow a portion of the interest expense incurred by the taxpayer...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Reasonable Expectation of Profit | must be a realistic plan to reduce overleverage | 158 |

| Tax Topics - Income Tax Act - Section 3 - Paragraph 3(a) - Business Source/Reasonable Expectation of Profit | 160 | |

| Tax Topics - Income Tax Act - Section 67 | s. 67 does not embed a reasonable expectation of profit requirement | 104 |

Integrated Wood Research Inc. v. R., 98 DTC 1258, [1998] 1 CTC 2681 (TCC)

Before going on to find that interest accrued by the taxpayer was an expenditure for purposes of ss.194 and 37, Bonner TCJ. stated (at p....

Robitaille v. R., [1997] 3 C.T.C. 3031, 97 DTC 1286

During a three-day period in 1985 the taxpayer, who was a partner in a law firm, withdrew $100,000 from his capital account, purchased a private...

Barbican Properties Inc. v. The Queen, 97 DTC 122, [1996] 2 CTC 2615 (TCC), briefly aff'd 97 DTC 5008 (FCA)

The taxpayer financed the purchase of "distressed" properties from the Royal Bank through non-recourse loans received from the Royal Bank which...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(e) | 138 |

WP Graphics Inc. v. The Queen, [1996] TCJ. No. 146 (TCC)

The taxpayer borrowed money in order to pay a dividend to a recent corporate purchaser of its shares which, in turn, used those monies to pay the...

Canwest Broadcasting Ltd. v. The Queen, 96 DTC 1375, [1995] 2 CTC 2780 (TCC)

The taxpayer accessed the non-capital losses of a group of arm's length corporations in financial difficulty ("FCPL") by engaging in a series of...

Redclay Holdings Ltd. v. The Queen, 96 DTC 1207, [1996] 2 CTC 2347 (TCC)

Part of the consideration given by the taxpayer for the purchase by it of a partnership interest was the assumption by it of a portion of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 78 - Subsection 78(1) | 83 |

Joy v. The Queen, 96 DTC 2026 (TCC)

The pleadings of the taxpayer, which referred to the retroactivity of the December 21, 1991 draft legislation on interest to 1972 and "submitted...

Vander Nurseries Inc. v. The Queen, 95 DTC 91, [1994] 2 CTC 2347 (TCC)

The taxpayer was found to have advanced money to an associated corporation as an interest-free loan rather than as proceeds for the redemption of...

Plawiuk v. The Queen, 94 DTC 1050 (TCC)

In 1987, the taxpayer borrowed a substantial sum from a supplier of a Canadian company ("Seven-Up") to acquire 100 common shares of Seven-Up under...

Mutual Life Assurance Co. of Canada v. 837690 Ontario Ltd. (1993), 36 RPR (2d) 159 (Ont Ct J (GD))

The plaintiff held a mortgage which, in addition to providing for blended payments of principal and interest, also provided for the payment after...

Spectron Computer Corp. v. MNR, 93 DTC 1473, [1993] 2 CTC 3148 (TCC)

In finding that interest costs incurred by the taxpayer to finance the payroll cost of its R & D personnel were described in s. 20(1)(c), Kempo,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 2902 | 184 | |

| Tax Topics - Statutory Interpretation - Resolving Ambiguity | 112 |

Mark Resources Inc. v. The Queen, 93 DTC 1004, [1993] 2 CTC 2259 (TCC)

In order to utilize the losses of its U.S. subsidiary, the taxpayer borrowed funds in Canada from an arm's length bank and made a capital...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | 106 |

Lessard v. MNR, 93 DTC 680, [1993] 1 CTC 2176 (TCC)

The taxpayer was given the opportunity to purchase 10.25% of the shares of a private company ("Choisy") for which he worked. He accomplished this...

Morscher v. MNR, 92 DTC 2214, [1992] 2 CTC 2534 (TCC)

The taxpayer, who carried on a commercial litigation practice in partnership with another lawyer, was denied the deduction of interest which...

Glass v. MNR, 92 DTC 1759 (TCC)

The taxpayer borrowed money at prime plus 1/2% to acquire a mortgage in default which, after negotiation with the controlling shareholders of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(2) - Paragraph 40(2)(g) - Subparagraph 40(2)(g)(ii) | 86 | |

| Tax Topics - Income Tax Act - Section 54 - Adjusted Cost Base | sum paid to discontinue an injunction was part of cost of mortgage | 104 |

Goulard v. MNR, 92 DTC 1244, [1992] 1 CTC 2396 (TCC)

In a number of instances the taxpayer incorporated a real estate principal business corporation, arranged long-term construction bank financing...

Brown v. The Queen, 92 DTC 1105, [1992] 1 CTC 2152 (TCC)

Interest on money borrowed by the taxpayer to honour his personal guarantee of his corporation's indebtedness was non-deductible. "Paying off a...

Sutherland v. The Queen, 91 DTC 5318, [1991] 1 CTC 495 (FCTD)

Unpaid management fees owing to the taxpayer by a company in which he had an interest were found not to be a loan by him to the company in the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(p) - Subparagraph 20(1)(p)(i) | unpaid fees not loans | 71 |

| Tax Topics - Income Tax Act - Section 5 - Subsection 5(1) | 103 |

Ronald Michael Kornelow v. Minister of National Revenue, 91 DTC 431, [1991] 1 CTC 2403 (TCC)

Interest on money which the taxpayer had borrowed in order to invest in a corporation was non-deductible given that the corporation had been...

Tor-Guelph Holdings Limited v. Minister of National Revenue and 309901 Ontario Limited v. Minister of National Revenue, 91 DTC 355, [1991] 1 CTC 2252 (TCC)

The partners of a partnership were denied the deduction of interest on money borrowed in order to make an interest-free advance to a corporation...

Gruyich Services Inc. (formerly Gru-Reco Limited) v. Minister of National Revenue, 91 DTC 159, [1991] 1 CTC 2139 (TCC)

Notwithstanding a comingling of funds, the taxpayer was able to establish that only a portion of borrowed money was used to pay dividends, and...

Dockman v. MNR, 90 DTC 1804, [1990] 2 CTC 2229 (TCC)

The taxpayer was entitled to deduct interest on a $40,000 bank loan which he on-lent to his brother for the period of time that there was a...

Wilson v. MNR, 90 DTC 1744, [1990] 2 CTC 2325 (TCC)

Under a divorce settlement, the taxpayer's wife otherwise would have been entitled to shares of a company ("Taja") and other income-producing...

Lee v. MNR, 89 DTC 443 (TCC)

Only 1/8 of the interest on a vendor take-back mortgage used to finance the taxpayer's acquisition of a motel, 15.38% of the total available...

Scott v. MNR, 89 DTC 218, [1989] 1 CTC 2305 (TCC)

The taxpayer was not entitled to deduct interest on borrowed money which he had on-lent on a non-interest bearing basis to two corporations of...

Bowes & Cocks Ltd. v. MNR, 89 DTC 341, [1989] 2 CTC 2043 (TCC)

The taxpayer used borrowed money to acquire additional shares of its subsidiary, which the taxpayer immediately wound-up in the process of which a...

Wilson v. MNR, 88 DTC 1418, [1988] 2 CTC 2053 (TCC)

Christie A.C.J. stated (p. 1419) that "the fact that repayment of money that is borrowed is secured by a mortgage on the borrower's personal...

Marine Management Ltd. v. Dep. Cmmer. of Inland Rev. (Fiji), [1986] BTC 184 (PC)

It was held that borrowed money was paid by the taxpayer for the purchase of shares of a company rather than for the acquisition of a management...

Gilmour v. The Queen, 81 DTC 5322, [1981] CTC 401 (FCTD)

A corporation issued 3% and 3.5% debentures at discounts which resulted in effecte rates of 4.765 and 5.02% at a time whnen the prime rate of teh...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | 147 |

Re Balaji Apartments Ltd. and Manufacturers Life Insurance Co. (1979), 100 DLR (3d) 695 (Ont HC)

A mortgage provided for blended payments of principal and interest at 8.5%, and provided that "it is further covenanted and agreed" that until the...

Re Euro Hotel (Belgravia) Ltd. (1975), 51 TC 293 (Ch D)

The taxpayer, which was entitled to a long lease of land in consideration of developing the land, assigned its ultimate rights to the lands to a...

Attorney General (Ontario) v. Barfried Enterprises, [1963] S.C.R. 570

The pith and substance of The Unconscionable Transactions Relief Act (Ontario), which permitted a court to re-open a money-lending transaction...

C.I.R. v. Pullman Car Co., Ltd. (1954), 35 TC 221 (Ch D)

In 1938, the taxpayer, which was in financial difficulty, replaced 70% of its preference shares by income stock which stipulated for the payment...

Bennett and White Construction Co. v. Minister of National Revenue, 49 DTC 514, [1949] CTC 1, [1949] S.C.R. 287, [1949-1950] DTC 514

In finding that annual amounts described in various resolutions of the taxpayer as "interest" in fact were guarantee payments, Locke J. stated (p....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Financing Expenditures | guarantee fees paid on construction financing were on capital account | 82 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) | 91 |

Inland Revenue Commissioners v. Rowntree & Co. Ltd., [1948] 1 All ER 482 (CA)

The taxpayer drew sight bills on an acceptance house which, after accepting the bills, discounted them in the market as agent for the taxpayer and...

Reference as to the Validity of Section 6 of the Farm Security Act, 1944 of Saskatchewan, [1947] S.C.R. 394, aff'd [1949] AC 110

Section 6 of the Farm Security Act 1944 (Saskatchewan) provided that in the event of a crop failure, the principal of a mortgage on a farm would...

Dupuis Frères Ltd. v. Minister of Customs and Excise (1927), 1 DTC 104 (Ex Ct)

A holder of preferred shares of the taxpayer was entitled to fixed dividends and to have the shares redeemed 15 years after the date of their...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(11) - Investment Contract | 170 |

A. W. Walker & Co. v. C.I.R. (1920), 12 TC 297 (KBD)

A partnership borrowed £4,000 from the executors of an estate pursuant to a loan agreement which provided that the consideration for the loan...

Administrative Policy

2020 Ruling 2020-0854741R3 - Subordinated Notes without Maturity

CRA ruled that “interest” paid by a resident corporation (Aco) on subordinated notes would not be subject to Part XIII tax based on the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(b) | interest that could be cancelled in issuer's discretion was interest for Pt. XIII purposes | 337 |

2018 Ruling 2017-0732001R3 - XXXXXXXXXX

A public company (ACo) will issue unsecured subordinated Notes, whose terms will be conventional except that:

- ACo may in its discretion elect by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(b) | “interest” that could be cancelled at cost of foregoing dividends was interest | 339 |

1 June 2016 External T.I. 2015-0601211E5 - Mortgage loan from RRSP to make a shareholder loan

An individual, who is an RRSP annuitant, borrows the “Mortgage Loan” from the RRSP, with a principal residence mortgage granted in favour of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 4900 - Subsection 4900(1) - Paragraph 4900(1)(j.1) | use of qualified mortgage loan proceeds of no import | 184 |

| Tax Topics - Income Tax Act - Section 207.01 - Subsection 207.01(1) - Advantage - Paragraph (a) | 4900(1)(j.1) insurance requirements generally arm's length/potential advantage on default | 247 |

| Tax Topics - Income Tax Act - Section 207.01 - Subsection 207.01(1) - Registered Plan Strip | 4900(1)(j.1) mortgage loan unlikely to be acquired at less than FMV | 225 |

29 January 2016 Internal T.I. 2015-0621401I7 - interest deductibility and share repurchases

Canco, a listed corporation, repurchased for cancellation (the “Repurchases”) significant numbers of its Common Shares on the open market...

24 August 2015 External T.I. 2015-0589841E5 - Financial instrument as a debt obligation

Unsecured notes of Canco carry a fixed rate of interest, have a term of up to 60 years and upon the occurrence of default by reason of Canco's...

9 October 2015 APFF Roundtable Q. 11, 2015-0595771C6 F - Deductibility of interest in a leveraged buyout

When asked about interest deductibility where, in the context of a leveraged buy-out, the Bank lends to Target under a secured loan bearing...

9 October 2015 APFF Financial Strategies and Instruments Roundtable Q. 3, 2015-0588951C6 F - Deductibility of interest – ss. 20.1(1)

The sole shareholder of a CCPC uses borrowed funds to make an interest-free advance to the CCPC, and the CCPC then makes a proposal under the BIA,...

11 September 2015 Internal T.I. 2015-0586301I7 - Premiums received on re-opening of debt

The Taxpayer, a corporation whose business was not that of borrowing or lending money re-opened (i.e., extended the maturity of) notes on a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 14 - Subsection 14(5) - Cumulative Eligible Capital - Variable E | premium received on note re-opening subject to eligible capital amount treatment if not otherwise taxable | 162 |

25 May 2015 External T.I. 2014-0563351E5 - Mandatory conversions and interest deductibility

Notes of a Canadian corporation ("Canco") with an investment grade rating would carry a fixed rate of interest, be denominated in Canadian...

2014 Ruling 2014-0523691R3 - Non-Viable Contingent Capital

Aco, a public corporation, will issue (at no discount or only a shallow discount) the "Notes" which: will rank equally with its other unsecured...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3) - Participating debt interest | non-viable contingent capital sub debt of bank respected as non-participating interest debt | 138 |

20 January 2015 Internal T.I. 2014-0551121I7 F - Interest deductibility

Canco 2, 3 and 4 were wholly-owned by Canco 1. Cancos 3 and 4 used the proceeds of loans from Canco 2 in 2010 for an income-producing purpose. In...

S3-F6-C1 - Interest Deductibility

1.1 "Interest". "Interest" accrues daily, is calculated on principal and is compensation for its use.

1.2-1.4 Participating interest. Subject to...

2 December 2014 CTF Roundtable, Q2(a)

In a loss consolidation arrangement, "Lossco," which has non-capital losses, lends money to Profitco at a reasonable stated rate of interest and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(1) - Paragraph 111(1)(a) | positive spread/independent servicing source in loss consolidations | 171 |

10 October 2014 APFF Roundtable, 2014-0538261C6 F - Disposition of capital interest/personal trust

In order to settle the capital interest in a discretionary family trust of a beneficiary who is related to the trustees, that beneficiary agrees...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107 - Subsection 107(2) | issuance of note by trust is not distribution of trust property | 81 |

| Tax Topics - Income Tax Act - Section 108 - Subsection 108(1) - Cost Amount | note issuance is not trust property distribution to a beneficiary | 217 |

9 April 2014 Internal T.I. 2014-0519231I7 - Debt forgiveness and guarantees

Forco, a wholly-owned subsidiary of Canco, borrowed under a secured "Borrowing" from a lending syndicate, with Canco providing a guarantee"...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) - Commercial Debt Obligation | guarantee obligation not a commercial debt obligation | 153 |

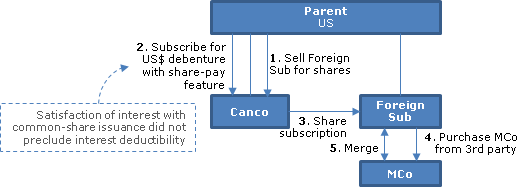

12 February 2014 Internal T.I. 2012-0443391I7 - cross-border loans and deductibility of interest

{kind=link}

Canco purchased common shares of Foreign Sub (a subsidiary of Parentco) from its foreign parent (Parentco) in consideration for treasury shares....

2013 Ruling 2013-0490341R3 - No-type of property spin-off butterfly

{kind=link}

Preliminary/butterfly reorg

The shareholders of Old Pubco (a Canadian public corporation dealing at arm's length with each shareholder) will...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | s. 55(3.02) public spin-off of CFAs to new sister TC with post butterfly FX loan by TC to DC; new public corp inserted above DC before b/f | 449 |

2013 Ruling 2011-0395091R3 - MFC to MFT Conversion

underline;">: Background. Taxpayer, which is a listed mutual fund corporation, wishes to convert to a mutual fund trust (so that following the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(1) | 210 | |

| Tax Topics - Income Tax Act - Section 132.2 - Subsection 132.2(1) - Qualifying Exchange | 1059 | |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition - Paragraph (f) | consolidation of 4 subtrusts into 1 using (f) | 178 |

3 June 2013 Internal T.I. 2012-0468131I7 - Participating debt interest

The Canadian taxpayer issued Contracts to its wholly-owning non-resident parent ("ForParent") as consideration for its purchase from ForParent of...

27 February 2013 External T.I. 2013-0477601E5 - Interest Deductibility on Restructured Borrowings

When asked us for clarification as to why in The Queen v. Singleton, 2001 SCC 61, the interest deduction was allowed whereas in the Lipson v. The...

12 June 2012 June STEP Roundtable, 2012-0449811C6 - Application of 20(1)(c) if 75(2) applies

An individual (the "Borrower") uses borrowed money to purchase an income producing property and later settles this property on an inter vivos...

2012 Ruling 2011-0431101R3 - Cross-border spin-off butterfly

On a butterfly reorganization, the non-resident parent of the distributing corporation (DC) exchange its common shares of DC for new common shares...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | cross-border b/f as part of double Code s. 355 spin-off | 1540 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Permitted Exchange | 429 | |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.1) - Paragraph 55(3.1)(b) - Subparagraph 55(3.1)(b)(i) | 604 |

13 August 2012 Internal T.I. 2012-0453481I7 - Accumulated Profits

A subsidiary of Canco ("Subco") declared a dividend payable to Canco immediately following a time at which it accumulated profits ("AP") were $X,...

15 August 2012 External T.I. 2012-0446741E5 - Interest Deductibility

An individual who is the shareholder of a corporation borrows money from a financial institution to acquire preferred shares of the corporation...

12 March 2012 Internal T.I. 2011-0398721I7 - Interest expense deduction

Two creditors provided financing for the purchase and development of land and building held by nominee corporations, with the beneficial ownership...

2011 Ruling 2011-0411821R3 - Interest deductibility and loss carry backs

a limited partnership ("BForLP") owns substantially all of the membership interests in a (presumably Netherlands) holding cooperative which owns...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(2.11) | 227 |

29 October 2010 Internal T.I. 2010-0357241I7 - Exchangeable Debenture

In response to a query as to the deductibility of interest on a note which was exchangeable into "Underlying Shares," CRA indicated that interest...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(f) | 242 |

27 May 2009 External T.I. 2008-0296731E5 F - Rachat d'actions: 20(1)c)

A corporation finances the purchase for cancellation (“redemption”) of shares in its capital for $1,000 with $500 borrowed from a financial...

5 June 2008 TI 2007 - 025221 [partial sale/partial disappearing source]

In indicating that there would be partial loss of interest deductibility on money borrowed in order to acquire mutual fund units, where a portion...

14 May 2005 Internal T.I. 2008-0304841I7 - Interest deductibility

"CanOpco" is a 100% subsidiary of "NRHoldco,” a US based corporation, which filed for protection under Chapter 11 of the U.S. Bankruptcy Code....

2008 IFA Round Table, Q. 10.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18.2 - Subsection 18.2(3) | 0 |

15 November 2007 External T.I. 2007-0254941E5 - Interest Deductibility - Second Loan

Where a taxpayer borrows money in order to acquire shares of a corporation and then borrows under a second loan to pay the interest under the...

2007 Ruling 2007-0245281R3 - windup of income trust on sale of assets:3rd party

A corporation ("Bidco") assumes the third-party debt of an income fund (the "Fund") whose units it has acquired as consideration for the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(21) | trustees making filings on behalf of terminated fund | 48 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(6) | realization and distribution of target MFT gain | 101 |

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(3.3) | capital loss on redemption of trust units following distribution of most of its assets including as capital gains distribution | 110 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 90 | |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 90 | |

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(2) - Paragraph 53(2)(h) - Subparagraph 53(2)(h)(i.1) | no ACB reduction for capital gains distribution by unit trust to bidco | 86 |

29 June 2006 Internal T.I. 2006-0190791I7 F - Dépense d'intérêts - obligation légale

Parentco made advances to its Subsidiary. In a year subsequent to the advances the Subsidiary recorded a journal entry to adjust its retained...

Income Tax Technical News, No. 34, 27 April 2006 under "Delaware Revised Uniform Partnership Act"

[W]here a corporation has borrowed to repurchase shares, the deductibility of the interest is related to the amount of the debt required to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Transitional Provisions and Policies | 0 | |

| Tax Topics - Income Tax Act - Section 132 - Subsection 132(6) | majority of subsidiary board not to be MFT trustees/guarantees re non-wholly owned subs scrutinized | 105 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2) | 7 | |

| Tax Topics - Income Tax Act - Section 96 | Delaware LPs with separate personality are not corps | 21 |

| Tax Topics - Treaties - Income Tax Conventions - Article 5 | 17 | |

| Tax Topics - Income Tax Act - Section 132 - Subsection 132(6) - Paragraph 132(6)(b) - Subparagraph 132(6)(b)(i) | guarantee must be highly integrated with trust’s core investment undertaking/limited overlap with subsidiaries' boards | 434 |

IT-533 "Interest Deductibility and Related Issues" 31 October 2003

Exceptions to the direct use test - borrowed money used by a corporation to redeem shares, return capital or pay dividends

23. Interest expense...

2005 Ruling 2005-0130541R3 - Participating Interest

Interest deduction rulings given with respect to debt on which there is base interest, plus additional interest equal to the lesser of the taxable...

3 May 2005 CALU Roundtable Q. 5, 2005-0116661C6 - Interest deductibility on second loan - Gifford

Where a taxpayer borrows money to use in its business and in order to pay interest on this loan the taxpayer borrows money under a second loan,...

8 October 2004 APFF Roundtable Q. 30, 2004-0086981C6 F - Déduction des intérêts - détermination du capital

Respecting a question as to how CRA would view the capital of preferred shares that are redeemed with the proceeds of borrowed money, where the...

14 January 2005 Internal T.I. 2004-009814

The interest on debt previously owing by the taxpayer's shareholder that the taxpayer assumed in consideration for the forgiveness of a...

17 December 2004 External T.I. 2004-0084881E5 - Deductibility of interest on assumed debt

Respecting a question whether the assumption by a trust of another person's indebtedness (a loan payable by a corporation to "Finco") as part of...

2004 Ruling 2004-007680

//www.bci.ca/">www.bci.ca): Non-capital losses of BCI are transferred to its affiliate, Bell Canada, pursuant to transactions under which a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(x) | contributions of capital | 205 |

2004 Ruling 2004-0061951R3 - Interest deductibility

A Canadian holding company ("MCo") for a foreign parent is no longer able to earn sufficient income to service its long-term debt, whereas its...

16 October 2003 External T.I. 2003-0038315 F - CONVENTION DE RETRAITE

An RCA trust created for the benefit of a managing shareholder and to which the employer contributed $100,000 lends the amount of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Retirement Compensation Arrangement | loan back to employer may negate RCA status | 98 |

10 October 2003 Roundtable, 2003-0035685 F - DEDUCTION INTERETS MONTANT RAISON

What factors would the CCRA consider in determining whether the amount of interest payable under a particular loan agreement exceeds a "reasonable...

7 May 2003 External T.I. 2003-0184005 - ACCUMULATED PROFITS CONSOLIDATED

Given that the determination of accumulated profits must respect the legal relationships that exist, accumulated profits should be determined on a...

14 May 2003 Internal T.I. 2003-0181477 F - DEDUCTIBILITE DES INTERETS

Regarding the deductibility of interest where a loan had an above-market rate of interest and a premium was received on its issuance, the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) - Subparagraph 20(1)(c)(i) | taxpayer discretion re attributing use of commingled funds does not apply where tracing is possible | 222 |

2003 Ruling 2003-0032993 - AMALGAMATION INTEREST EXPENSE

Dco incurs a promissory note in acquiring all the common shares of Eco with Eco then amalgamating with a subsidiary (Rco). Cco, the parent of Dco...

10 March 2003 Internal T.I. 2002-0172187 F - DEDUCTIBILITE DES INTERET

A debenture issued by a corporation provided for the payment of base interest plus the payment of an “additional interest” on maturity that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) - Subparagraph 20(1)(c)(i) | interest on debenture issued in payment of interest, was non-deductible | 118 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(f) | premium (termed additional interest”) was payable even if no early repayment, and qualified under s. 20(1)(f) | 200 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Legal and other Professional Fees | legal fees re repaying debt were non-deductible | 21 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Dividend | premium payable on debenture repayment based in part on the quantum of debtor’s equity was not a dividend | 242 |

2001 Ruling 2001-0097283 - double d's with U.S. parent

XCo (a Canadian corporation that for U.S. purposes is regarded as being a branch of its U.S.-resident parent ("NR Subco")) uses borrowed money to...

4 January 2001 External T.I. 2000-0055475 - REDUCTION OF STATED CAPITAL

In the case of a share redemption,

"a corporation may borrow to the extent that the stated capital of those shares and the accumulated profits or...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | 139 |

26 May 2003 External T.I. 2003-001242

On the sale of a home, the taxpayer is required by the lender to repay a loan that had financed mutual fund investments out of the sale proceeds,...

15 May 2003 External T.I. 2003-00626

Where a taxpayer satisfied the purchase price for an income-producing property by assuming a debt owing by the vendor to a third party and, at a...

13 May 2003 External T.I. 2003-0000825 - INTEREST DEDUCTIBILITY

Where an investor purchases a unit of a real estate investment trust for $10, receives a cash distribution of $0.80 and the REIT's income for tax...

30 April 2003 External T.I. 2002-0156045 - Debt assumed as part/distribution from trust

Where a trust distributes shares of a Canadian corporation to a beneficiary on the condition that the beneficiary assume indebtedness owing by the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107 - Subsection 107(2) | 55 | |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Personal Trust | 50 |

25 March 2003 External T.I. 2002-0176945 - INTEREST DEDUCTION DIVIDENDS

In the situation where dividends, whose ultimate aggregate amount eventually exceeded the corporation's accumulated profit, were funded out of a...

2003 Ruling 2002-0177363 - Loss Utilization in a Related Group

"It is no longer necessary for the dividend rate on the preferred shares to be greater than the interest rate on the loan (a so-called 'positive'...

18 December 2002 Internal T.I. 2002-0161747 - INTEREST EQUITY ACCOUNTING

Equity accounting may not be used to determine accumulated profits for the purpose of establishing interest deductibility on the payment of...

16 July 2002 External T.I. 2002-0142475 - INTEREST DEDUCTIBILITY INCOME TRUST

Where an individual borrows $10,000 at 4% interest and invests it in an income trust and receives, in the first year $1,400, of which $500 is...

15 May 2002 External T.I. 2001-0103605 F - Prêt par un Associé à une Société

Is the interest on a loan made to a partnership by a partner deductible under s. 20(1)(c)? CCRA responded:

Whether a partner of a partnership has...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 96 - Subsection 96(1) - Paragraph 96(1)(g) | if a loan made by a partner is at law a loan rather than a partnership contribution, the interest thereon will be treated as interest rather than profit allocation | 166 |

2002 Ruling 2002-0160913 - INTEREST

A foreign corporation ("ForeignCo") acquires a Canadian company ("Opco"): a wholly-owned newly-incorporated subsidiary of ForeignCo ("Holdco")...

Income Tax Technical News, No. 18, 16 June 2000

Discussion of the extension of the "ultimate purpose test" in Byram, 99 DTC 5117 (FCA) to s. 20(1)(c).

31 May 2001 Internal T.I. 2000-0062337 - prepaid forward sales contract - bifurcation

An agreement provided for the immediate receipt of a cash payment by the purchaser (a trust) from the vendor and obliged the vendor (a company in...

25 May 2001 External T.I. 2001-0067415 F - CONSOLIDATION DE PERTES

Regarding loss consolidation transactions, CCRA stated:

For a transaction to be commercially reasonable, the amount of borrowings and investments...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(1) - Paragraph 111(1)(a) | CCRA loss consolidation policy is available where Profitco’s income is FAPI/ requirements re transactions being commercially reasonable | 169 |

29 January 2001 External T.I. 2000-0063185 - Interest deductibility

In response to a question on the deductibility of interest on borrowed money used for the purpose of investing in common shares of a technology...

4 January 2001 External T.I. 2000-0057915 - BORROWED MONEY TO REDUCE STATED CAPITAL

"Where there has been an accounting write-down in assets and a corresponding shareholder's deficit for accounting purposes but there is no...

4 January 2001 External T.I. 2000-0055475 - REDUCTION OF STATED CAPITAL

"Accumulated profits or retained earnings, for the purpose of determining eligible borrowing, do not include appraisal surpluses or profits...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | 122 |

6 December 2000 External T.I. 2000-0056275 - LEVERAGED BUYOUTS

The finding in the CRB Logging case that the closed nature of the income flow made it virtually impossible for CRB to receive dividends that did...

29 November 2000 Internal T.I. 2000-0051367 - INTEREST ON REDEMPTION OF SHARES

Prejudgment and post judgment interest that was paid by a corporation in respect of the lapse of time between the departure of a shareholder and...

24 October 2000 Internal T.I. 2000-0048177 - DEDUCTIBILITY OF INTEREST ON ASSUMED DEBT

Where a corporation redeems its preferred shares and, as consideration, assumes a bank loan that the shareholder had previously incurred to...

29 March 2000 External T.I. 2000-0008315 - INTEREST

Where a target corporation borrowed money from a bank in order to make an interest-free loan to a holding company for management that would be...

22 March 2000 External T.I. 2000-0002705 - INTEREST DEDUCTIBILITY - INTEREST FREE LOAN

Interest on money borrowed to make an interest-free loan to a subsidiary would not be deductible because the subsidiary was not resident in Canada.

23 February 2000 External T.I. 2000-0000205 - INTEREST DEDUCTIBILITY

"In a situation where a taxpayer purchases a property from another taxpayer and assumes that taxpayer's mortgage liability in respect of the...

1999 Ruling 9931713 - PARTNERSHIP REORGANIZATION

Interest on debts used by a partnership to acquire fixed assets would still be deductible by the partnership after a transfer of those assets to a...

1999 APFF Round Table, Q. 2 (No. 9M19190)

Where a Canadian public corporation borrows money in order to acquire units of a corporation that is an LLC, the interest will be deductible...

5 October 1999 External T.I. 9924775 - INNOVATIVE INSTRUMENTS INTEREST DEDUCTIBILITY

Interest would not be deductible on a debenture with a mandatory conversion feature that permitted the borrower to repay holders with less than...

16 September 1999 External T.I. 9916715 - INTEREST DEDUCTIBILITY - IT 315\

A corporation (the "Target") borrows money to lend to an unrelated corporation which uses those funds to purchase shares of the Target from a...

Income Tax Technical News, No. 16, 8 March 1999

"We think the Sherway decision helps distinguish between those financial arrangements where the participation payments are intended to be...

27 January 1999 Internal T.I. 9830747 - INTEREST EXPENSE TO REDUCE CAPITAL

RC's policy that interest is deductible to the extent that the borrowing is not in excess of the paid-up capital reduction which the borrowing...

14 October 1998 External T.I. 9732475 - INTEREST DEDUCTIBILITY

Where a corporate taxpayer borrows $10 million from a bank at 6%, and uses the borrowed funds to buy a business asset which, later, is sold giving...

May 1998 Advanced Life Underwriting Round Table, Q. 4, No. 9807000

"The fact that paragraph 149(1)(q.1) exempts an RCA from being taxed under Part I of the Act on its taxable income does not, in and by itself,...

1998 APFF Congress, Q. 19

A corporation X wishes to buy back the shares of one of its shareholders (corporation Y), and corporation B wishes to acquires shares of...

30 November 1997 Ruling 9732433 F - UTILISATION DE PERTES LOSS UTILIZATION

Consideration of the reasonableness of an interest rate (8.7%) before giving favourable rulings on an arrangement respecting the deductibility of...

8 December 1997 External T.I. 9730565 - INTEREST EXPENSE DEDUCTION

The position in Question 5 of the 1996 Corporate Management Tax Conference Round Table would also extend to a public corporation.

17 July 1997 External T.I. 9718765 - INTEREST DEDUCTIBILITY - BORROWING TO MAKE DISTRIBUTION

"Interest on money borrowed by a corporation to repay capital on the redemption, acquisition or cancellation of a share is generally deductible...

14 July 1997 External T.I. 9716025 - INTEREST DEDUCTION - NON-RESIDENT

Because interest paid in respect of a partnership interest is not deductible at the partnership level, interest payable by a non-resident...

1997 Tax Executives Institute Round Table, Q. VIII, No. 9729670

In the Barbican situation (where interest is not deductible on an accrual basis because it is contingent in amount), the interest also would not...

13 November 1996 External T.I. 9636395 - RESP INTEREST ON MONEY BORROWED TO CONTRIBUTE

When a contributor has an unrestricted right to receive all educational assistance payments available under the terms of an RESP, the contributor...

29 October 1996 External T.I. 9626325 - BOND OPTIONS

Where a corporation has issued an option giving the holder the right to acquire interest-bearing bonds of the issuer at a future date for an...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(x) | option premium | 32 |

8 October 1996 Memorandum 962852 (C.T.O. "Interest Deductibility")

Non-arm's length transactions that had the effect of converting equity into debt were required to comply with RC's position on accumulated profits...

5 January 1996 CTF Roundtable Q. 31, 9523976 - GROSS-UP PAYMENTS

Where a gross-up on interest paid to a non-resident meets the legal definition of interest, it will be deductible by the taxpayer under s....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Payment & Receipt | 56 | |

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(c) | 56 | |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) | 74 |

30 November 1995 Ruling 9638023 - XXXXXXXXXX

An interest deduction was available on a loan received in order to retire existing corporate indebtedness where the obligation to pay interest was...

1996 Corporate Management Tax Conference Round Table, Q. 7

Until RC completes its review of the subject, interest on excess debt assumed by a transferee corporation in an s. 85(1) rollover transaction will...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) - Paragraph 85(1)(b) | 49 |

1996 Corporate Management Tax Conference Round Table, Q. 5

Interest on a promissory note owing by a corporation to its shareholders will be deductible to the same extent that interest would have been...

1996 Corporate Management Tax Conference Round Table, Q. 1

Affirmation of administrative positions set out in former IT-80.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20.2 - Subsection 20.2(1) | 56 |

30 November 1995 Ruling 9608123 - LOSS CONSOLIDATION

Interest on a loan from a subsidiary to a parent that was funded by a common share subscription by the parent, will be deductible to the parent...

28 July 1995 External T.I. 9519555 - IT-315

"The policy expressed in IT-315 is applicable not only to interest on funds borrowed by a taxpayer to finance a share acquisition ... but also to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(a) - Revising Claims | 65 |

17 July 1995 External T.I. 9429715 - DISAPPEARING SOURCE RULES

"Where money is borrowed to permit withdrawals by the partner, the interest on such loans would not be deductible since the borrowed money is not...

May 1995 Tax Executive Institute Round Table, Q. 16 (C.T.O. "Interest Deductibility - Preferred Shares")

Where the interest on a loan is received by a corporation to acquire preferred shares exceeds the dividends return on the preferred shares, the...

2 February 1995 Internal T.I. 9430557 - INTEREST ON MONEY BORROWED TO PAY INTEREST

Interest on money borrowed to pay interest is deductible "provided the reason for the predicament in which the individual finds himself is bona...

Income Tax Regulation News, Release No. 3, 30 January, 1995 under "Interest-Bearing Note issued in Consideration for the Redemption or Repurchase of Shares"

Interest payable on a promissory note issued as consideration for the redemption or purchase for cancellation of a corporation's capital stock is...

Income Tax Regulation News, Release No. 3, 30 January, 1995 under "Use of a Partner's Assets by a Partnership"

Where a property is acquired by a partner for the purpose of making it available to the partnership to be used in carrying on the business of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 97 - Subsection 97(1) | 38 | |

| Tax Topics - Income Tax Regulations - Regulation 1102 - Subsection 1102(1) - Paragraph 1102(1)(c) | 72 |

9 September 1994 Internal T.I. 9421957 - DEDUCTIBILITY OF DEEP DISCOUNTS AS INTEREST AND IT-114

A shallow original-issue discount on a debenture would be subject to the application of ss.18(1)(f) and 20(1)(f), and would not be viewed as...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Exempt Receipts/Business | 29 | |

| Tax Topics - Income Tax Act - Section 9 - Expense Reimbursement | 29 |

6 September 1994 External T.I. 9419955 - INTEREST DEDUCTIBILITY

In response to a query as to whether interest would be deductible on borrowed money that is used to acquire a mutual fund investment which...

3 June 1994 Internal T.I. 9405427 - DEDUCTIBILITY OF INTEREST UNDER 20(1)(C)

Consideration of interest deductibility in a situation where a loan is used to purchase preferred shares which are exchanged for common shares of...

Revenue Canada Round Table TEI, 16 May 1994, Q. 14 9410430

Where a debt obligation of Co. A owing to an arm's length creditor ("Co. B") bearing an above-market rate of interest is irrevocably assumed by...

1994 A.P.F.F. Round Table, Q. 32

Where a corporation redeems its shares in consideration for issuing an interest-bearing note, interest on the note will not be deductible under...

1993 A.P.F.F. Round Table, Q.3

Where an individual has borrowed $100,000 to acquire common shares for that amount and the shares then appreciate in value to $500,000, there will...

93 C.R. - Q. 8 (File 932812)

Interest payable on funds borrowed to purchase newly-issued preferred shares that provide for dividends on the board's discretion and that are...

29 July 1993 Internal T.I. 9320007 F - Investment By Way of Contributed Surplus

"The deduction of interest should not be denied to a Canadian corporation that borrows funds to invest in a subsidiary, by way of contributed...

28 June 1993 T.I. (Tax Window, No. 32, p. 19, ¶2619)

Where there is a repayment of a portion of debt which has partly been used for an income-producing purpose and partly to acquire non-income...