Subsection 95(1) - Definitions for this subdivision

Controlled Foreign Affiliate

Administrative Policy

2016 Ruling 2015-0571441R3 - Dutch Cooperative - 93.2 & 95(2)(c)

Forco 1 is held through three stacked Canadian partnerships (the bottom one, “CanGP 3”) by two taxable Canadian corporations (Canco 1D and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(c) | rollover is available on joint drop-down of shares of a Dutch private limited liability company into a Dutch cooperative in consideration for respective credits to the membership accounts | 502 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Corporation | Dutch cooperative whose articles limited member liability was a corp | 263 |

| Tax Topics - Income Tax Act - Section 93.2 - Subsection 93.2(2) | membership interest in Dutch cooperative ruled to be shares | 92 |

| Tax Topics - Income Tax Act - Section 85.1 - Subsection 85.1(3) | joint contribution of shares of FA to Netherlands co-op in consideration for credits to their respective membership accounts deemed to be for share consideration | 57 |

28 August 2003 Internal T.I. 2003-0019767 F - Investissement dans une société étrangère

All the shares of Foreignco, which made investments in stock market shares, were held by Mr. A (apparently, non-resident). Mr. B (apparently,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 17 - Subsection 17(1) | redeemable convertible rights of a Canco investor in Foreignco had not been redeemed, so that they were not debt for s. 17 purposes and Foreignco was not a CFA | 141 |

| Tax Topics - Income Tax Act - Section 94.1 - Subsection 94.1(1) | inferred satisfaction of main reason test where all stock market investment income and gains were reinvested free of local tax | 377 |

22 July 2003 Internal T.I. 2003-0018027 F - Fondation du Liechtenstein

Mr. X formed a foundation (a “sifting”) under the laws of Liechtenstein, of which he was the life beneficiary, and his wife and children were...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Corporation | Liechtenstein sifting was a corporation rather than trust | 60 |

| Tax Topics - Income Tax Act - Section 94 - Subsection 94(3) | Liechtenstein siftung was corporation, not trust | 79 |

93 C.M.T.C - Q.1

It is not necessary to establish that the persons resident in Canada are acting in concert to control the affiliate. The threshold in s....

Paragraph (b)

Administrative Policy

20 June 2023 STEP Roundtable Q. 7, 2023-0959581C6 - Deemed Resident Trust and the Resident Portion

49% of the shares of a non-resident corporation owned by a non-resident trust which has made a valid s. 94(3)(f) election were included in the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 94 - Subsection 94(1) - Resident Portion | illustration of the resident portion rules for a s. 94 trust that inter alia has lent to a resident beneficiary or earns FAPI | 492 |

| Tax Topics - Income Tax Act - Section 94 - Subsection 94(2) - Paragraph 94(2)(a) | contribution to NR trust where beneficiary pays expenses of trust property | 103 |

| Tax Topics - Income Tax Act - Section 94 - Subsection 94(2) - Paragraph 94(2)(g) - Subparagraph 94(2)(g)(iv) | application where a s. 94 trust lent to a resident beneficiary, and when loan repaid | 177 |

Excluded Property

Administrative Policy

27 March 2018 Internal T.I. 2015-0592551I7 - Excluded property status of partnership interest

Canadian-resident Parent wholly-owned Canco2 and Canco1. Two wholly-owned controlled foreign affiliates of Canco2 (“NR1” and “NR2”)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5908 - Subsection 5908(10) | partnership interests no longer were excluded property on dissolution given prior disposition of s. 95(2)(a)(ii) loans/potential qualification of partnership interest under para. (c) ignored | 297 |

| Tax Topics - Income Tax Regulations - Regulation 5903 - Subsection 5903(5) - Paragraph 5903(5)(b) | foreign affiliate parent cannot carry back FAPLs generated by wound-up foreign affiliate | 389 |

| Tax Topics - Income Tax Act - Section 96 | Icelandic Sameignarfelag was partnership | 198 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(f.14) | once partnership interests were no longer excluded property, the components of their ACB calculation was to be translated at the rates when those components first arose | 254 |

| Tax Topics - Income Tax Act - Section 98 - Subsection 98(2) | partnership interest disposition occurred no sooner than final distribution date | 79 |

2015 Ruling 2014-0536661R3 - Disposition of property by a foreign partnership

CRA ruled that a distribution of the assets of a mine held by the partnership did not give rise to foreign accrual property income provided that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Accrual Property Income | reliance on excluded property exclusion on dissolution of Foreign LP as a result of the wind-up of its FA partners | 421 |

6 March 2015 Internal T.I. 2014-0549761I7 - Internally generated goodwill & excluded property

Is internally generated goodwill considered in determining whether shares of a foreign affiliate ("FA2") of a corporation resident in Canada...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 149 - Subsection 149(10) | unpurchased goodwill is taken into account | 96 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Small Business Corporation | unpurchased goodwill is taken into account | 105 |

15 January 2015 External T.I. 2014-0546581E5 - Partnership interest excluded property

{kind=link}

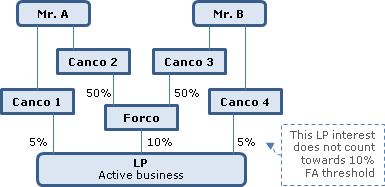

Mr. B wholly-owns Canco 3 and Canco 4, and Mr. A, who is unrelated, wholly-owns Canco 1 and Canco 2. Canco 2 and Canco 3 each holds 50% of Forco,...

1 September 2009 External T.I. 2006-0168571E5 - Excluded property

Canco's wholly-owned subsidiary Forhold 2 has a 30% interest as general partner in LP1 which has a 15% LP interest in LP2 which, in turn, has 75%...

21 September 2007 External T.I. 2007-0251651E5 - Excluded property

A Canadian resident individual owns 100% of a corporation ("FA") resident in the Netherlands which, in turn, has an interest in a partnership, all...

1 November 2000 External T.I. 1999-0009725 - Foreign affiliates meaning of group

A foreign affiliate ("Holdco") owns all the shares of a second foreign affiliate ("Subco A") which, in turn, owns all the shares of a third...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(a) - Subparagraph 95(2)(a)(ii) - Clause 95(2)(a)(ii)(D) | 101 |

6 January 1999 External T.I. 9829785 - FOREIGN AFFILIATE-ACTIVE BUSINESS INCOME

Where a foreign subsidiary of Canco deposits a sum with a foreign bank to secure its guarantee of a loan made by the foreign bank to another...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(a) - Subparagraph 95(2)(a)(ii) - Clause 95(2)(a)(ii)(B) | 70 |

10 March 1998 External T.I. 9804895 - definition of excluded property

Where a grandchild foreign factoring subsidiary acquires substantially all its trade receivables from a foreign subsidiary of the taxpayer that...

22 December 1997 External T.I. 9709775 - DEFINITION OF EXCLUDED PROPERTY

Intangible property that is capital property and that is used by a controlled foreign affiliate principally in producing deemed active business...

18 June 1996 External T.I. 9523595 - EXCLUDED PROPERTY STATUS - PARTNERSHIP STRUCTURES

Example A

Canco owns 100% of Forhold, which has a 90% interest in a partnership (P1), whose only assets are 25% of the shares of a foreign...

Articles

Paul Barnicke, Melanie Huynh, "FA's LP Interest: Excluded Property?", (2015) vol. 23, no. 4 Canadian Tax Highlights, 4-5

Alternative result in 2014-0546581E5 if additional partnership interest held by related Cdn corp through an FA (p. 5)

Shawn D. Porter, David Bunn, "Excluded Property and Foreign Rollovers: Interpretive Issues in the Partnership Context", International Tax Planning (Federated Press), 2010, p.1060

Potential bases for overcoming non-excluded property (“EP”) finding in 2006-0168571E5 re absence of related partnerships concept (p....

Paragraph (a)

Administrative Policy

8 October 2010 Roundtable, 2010-0373531C6 F - Qualification de bien exclu - 95(1)

In a scenario where an FA earns active business income and income other than active business income, how can it be determined whether a licence it...

Articles

Tina Korovilas, Drew Morier, "Non-Corporate Vehicles in the Foreign Affiliate Context", 2018 Conference Report (Canadian Tax Foundation), 20:1 – 114

Potential qualification of partnership interest under EP – para. (a) if (e) unavailable (p. 20:55)

- CRIC 1 owns 50 percent of the shares of an...

Paragraph (b)

Articles

Raj Juneja, Pierre Bourgeois, "International Tax Issues That Get in the Way of Doing Business", 2019 Conference Report (Canadian Tax Foundation), 36:1 – 42

Circularity element in determining excluded property status where material upstream loans

- Where an acquisition target is a holding company that...

Paragraph (c)

Articles

Tina Korovilas, Drew Morier, "Non-Corporate Vehicles in the Foreign Affiliate Context", 2018 Conference Report (Canadian Tax Foundation), 20:1 – 114

Initial concern re s. 95(1) – EP – para. (c) that property of the partnership could not qualify (pp. 20:56-59)

When the EP definition was...

Paragraph (e)

Articles

Tina Korovilas, Drew Morier, "Non-Corporate Vehicles in the Foreign Affiliate Context", 2018 Conference Report (Canadian Tax Foundation), 20:1 – 114

Narrowness of the postamble to the excluded property (EP) definition (p. 20:53)

[A]lthough the partnership postamble applies for the purposes of...

Foreign Accrual Property Income

Cases

Loblaw Financial Holdings Inc. v. Canada, 2020 FCA 79, aff'd 2021 SCC 51

After noting (at para. 48) that "the exclusions [in the s. 95(1) investment business definition] generally further the fundamental purpose of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Investment Business - Paragraph (a) | a Barbados bank sub conducted its business of investing in short-term debt principally with arm’s length persons | 602 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Business | receipt of equity funds from parent was not part of Barbados bank’s business | 188 |

| Tax Topics - Statutory Interpretation - Redundancy/ reading in words/ speaking in vain | error to apply an unexpressed intention | 172 |

| Tax Topics - Statutory Interpretation - Drafting Style | no additional requirements should be inferred in legislation drafted with “mind-numbing detail” | 172 |

| Tax Topics - General Concepts - Separate Existence | subsidiary did not manage its funds on behalf of parent | 161 |

See Also

A.G. Canada v. Le Groupe Jean Coutu (PJC) Inc., 2015 QCCA 838, aff'd 2016 SCC 55

The taxpayer implemented a plan, to neutralize the effect of FX fluctuations on its investment in a U.S. sub, that overlooked FAPI considerations...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Rectification & Rescission | transactions achieved purpose of neutralizing FX fluctuations and were not intended to avoid FAPI | 256 |

Rostland Corp. v. The Queen, [1995] 2 CTC 2276, 96 DTC 1973 (TCC)

Two indirect wholly-owned foreign subsidiaries of the taxpayer ("Texas" and "BV") held non-recourse promissory notes of an arm's length...

Canada Trustco Mortgage Co. v. MNR, 91 DTC 1312, [1991] 2 CTC 2728 (TCC)

The taxpayer's Netherlands subsidiary, whose income was derived from Canadian mortgages which it had purchased from, and were administered by, its...

Alexander Cole Ltd. v. MNR, 90 DTC 1894, [1990] 2 CTC 2437 (TCC)

A wholly-owned U.S. subsidiary of the taxpayer, which had been engaged (through U.S. limited partnerships) in commercial real estate projects,...

King George Hotels Ltd. v. The Queen, 81 DTC 5082, [1981] CTC 87 (FCA)

It was "stressed that whether a business is an active or inactive one is ... [a question] of fact dependent on the circumstances of each case ......

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 129 - Subsection 129(4) - Canadian Investment Income | 54 |

Administrative Policy

2015 Ruling 2014-0536661R3 - Disposition of property by a foreign partnership

{kind=link}

Current structure

Canco wholly owns Foreign Holdco, which wholly owns Foreign Subco1, the owner and operator of Mine 1 in Country X. Foreign...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Excluded Property | still dormant mine as excluded property | 65 |

30 August 2004 External T.I. 2003-000135

A grandchild foreign subsidiary of Canco ("FA2") is wound-up into an immediate foreign subsidiary of Canco ("FA1") at a time that a note owing by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | 148 | |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(g.1) | 37 |

26 March 2004 External T.I. 2003-0047061E5 - Foreign currency and FAPI

Where a foreign affiliate earns foreign accrual property income (rental income) of U.S.$50,000 throughout a year, the average exchange rate for...

27 November 1998 External T.I. 9822835 - FOREIGN AFFILIATES - FOREIGN ACCRUAL TAX

Where U.S. taxes are paid by U.S. C.-corp. (which is a foreign affiliate of the Canadian taxpayer) in respect of the investment business of a U.S....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Accrual Tax | US tax paid by USco on income of LLC not FAT unless income distributed to USco | 291 |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Underlying Foreign Tax - A - Subparagraph (iii) | tax paid by C-Corp CFA regarding its share of LLC income is not added to its UFT until that income is dividended to it | 143 |

17 January 1991 T.I. (Tax Window, Prelim. No. 3, p. 2, ¶1094)

The interest income of a controlled foreign affiliate on a foreign currency deposit denominated in a currency which was depreciating rapidly...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(2) | 42 |

85 C.R. - Q.15

After the Burri decision, whether income of a foreign affiliate is active business income or property income will continue to be determined by the...

Articles

Joint Committee, "Guidance on International Income Tax Issues raised by the COVID-19", 11 June 2020 Joint Committee Submission

COVID 19 relief suggested re FAPI issues

The Guidance on international income tax issues raised by the COVID-19 crisis addresses whether COVID...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Exempt Earnings - Paragraph (d) | 115 | |

| Tax Topics - Treaties - Income Tax Conventions - Article 5 | 93 | |

| Tax Topics - Income Tax Act - Section 153 - Subsection 153(6) | Impact of COVID travel restrictions on day count tests for qualifying non-resident employee status | 67 |

Mark Coleman, Daniel A. Bellefontaine, "Forgiveness, Foreign Affiliates and FAPI: a Framework", Resource Sector Taxation (Federated Press), Vol. X, No. 1, 2015, p.694

Application of forgiven amount only to reduce losses (p. 697)

[O]ne of the main distinctions between the FAPI debt forgiveness regime and the...

Mitchell Sherman, Kenneth Saddington, "100 1 Damnations!", Corporate Finance, Volume XVIII, No. 3, 2012, p. 2126, at 2129

"Now that the provision [s. 100(1)] applies to dispositions to non-residents, with which a CFA is almost certain to transact, FAPI implications...

Gordon Funt, Joel A. Nitikman, "FAPI and Debt Forgiveness - Now You See It, Now You Don't", CCH Tax Topics, No. 1724, 24 March 2005.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | 0 | |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(g.1) | 0 |

Melanie Huynh, Eric Lockwood, "Foreign Accrual Property Income: A Practical Perspective", International Tax Planning, 2000 Canadian Tax Journal, Vol. 48, No. 3, p. 752.

A

Administrative Policy

5 June 2018 External T.I. 2017-0738081E5 - Interest exp of foreign affiliate holding company

The sole activities of FA1, a wholly-owned foreign affiliate of Canco, are to use money borrowed from an arm’s length bank to buy all the shares...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(f) | Canco may choose not to deduct interest expense of a CFA so as not to generate a FAPL | 406 |

31 July 2014 Internal T.I. 2014-0536581I7 - Foreign affiliate fresh start rules

An grandchild FA subsidiary of the taxpayer (FA2), which carried on both an investment business, generated royalties from licensing its IP (which...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Leasing Obligation | licensed IP | 68 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(a) - Subparagraph 95(2)(a)(ii) - Clause 95(2)(a)(ii)(B) | licensed IP | 101 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(k) | fresh start rule applies even where the indirectly acquired subsidiary (FA2) carried on a passive IP licensing operation in the preceding year | 637 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(f.1) | deductions taken for whole year before carve-out under para. (f.1) | 164 |

Paragraph (b)

Administrative Policy

5 October 2017 Internal T.I. 2015-0614021I7 - 214(16) deemed dividend

A portion of the interest paid by CanCo to ForCo, which is a controlled foreign affiliate of the Canadian parent of CanCo, is not deductible...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 214 - Subsection 214(16) | Interest that is denied under the thin cap rules and recharacterized as dividends is still interest for FAPI and LRIP/GRIP purposes | 202 |

27 June 2008 External T.I. 2007-0247551E5 - FAPI and Part XIII Tax

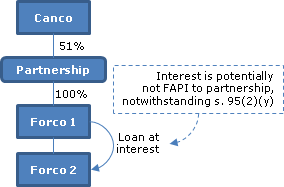

Two wholly-owned U.S.-resident subsidiaries of Canco (CFA1 and CFA2) carry on a U.S. active business through a U.S. general partnership (FP)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 96 | DRUPA partnership | 38 |

| Tax Topics - Income Tax Regulations - Regulation 5900 - Subsection 5900(3) | partnership between 2 CFAs was a Cdn-resident person for s. 91(5) purposes | 68 |

| Tax Topics - Income Tax Act - Section 92 - Subsection 92(1) - Paragraph 92(1)(a) | double ACB recognition of FAPI at partnership level and at level of Canco shareholder of CFA partners | 230 |

| Tax Topics - Income Tax Act - Section 91 - Subsection 91(5) | s. 91(5) deduction eliminated net FAPI inclusion to CFA members of foreign partnership receiving foreign dividends from partnership subsidiary | 107 |

Articles

Ian Bradley, Seth Lim, "The Updated Hybrid Mismatch Rules", International Tax Highlights (Canadian Tax Foundation and IFA Canada), Vol. 3, No. 1, February 2024. p. 2

Double taxation under A(b) (p. 3)

- The inclusion in foreign accrual property income (FAPI) of a foreign affiliate (FA) by virtue of A(b) of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 227 - Subsection 227(6.3) | 168 |

Paragraph (c)

Administrative Policy

2025 Ruling 2024-1030121R3 - FA Inversion

Under a sandwich structure, a Canadian Opco (Cansub) was wholly-owned by Foreign Parentco, which in turn was held by both Canadian shareholders...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.1 - Subsection 212.1(1.1) - Paragraph 212.1(1.1)(a) | application to dividend-in-kind of Cansub by foreign parent to new Cdn holdco for foreign parent shareholders | 543 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Accrual Property Income - B | para. (k) – proceeds of disposition exclusion for a s. 212.1(1.1) deemed dividend received by the FA on paying a dividend-in-kind of its Cansub to its Cdn Holdco | 245 |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Exempt Surplus - A - Subparagraph (v) | A(v) inclusion in exempt surplus for a s. 212.1(1.1) deemed dividend received by the FA (with exempt surplus) on paying a dividend-in-kind of its Cansub to its Cdn Holdco | 233 |

B

Administrative Policy

2025 Ruling 2024-1030121R3 - FA Inversion

Under a sandwich structure, a Canadian Opco (Cansub) was wholly-owned by Foreign Parentco, which in turn was held by both Canadian shareholders...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.1 - Subsection 212.1(1.1) - Paragraph 212.1(1.1)(a) | application to dividend-in-kind of Cansub by foreign parent to new Cdn holdco for foreign parent shareholders | 543 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Accrual Property Income - A - Paragraph (c) | A(c) exclusion for a s. 212.1(1.1) deemed dividend received by the FA on paying a dividend-in-kind of its Cansub to its Cdn Holdco | 245 |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Exempt Surplus - A - Subparagraph (v) | A(v) inclusion in exempt surplus for a s. 212.1(1.1) deemed dividend received by the FA (with exempt surplus) on paying a dividend-in-kind of its Cansub to its Cdn Holdco | 233 |

C

Administrative Policy

23 August 2023 Internal T.I. 2021-0882371I7 - Dividend payment and 94.1(1)(g)

A wholly-owned non-resident subsidiary (“CFA”) of Canco owned 50% of the common shares of a non-resident corporation (“FA”) which were...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 94.1 - Subsection 94.1(1) - Paragraph 94.1(1)(g) | there is no reduction under s. 94.1(1)(g) for dividends paid by the CFA/ consolidation provided of FAPI – C and s. 94.1(1)(g) language | 317 |

Foreign Accrual Tax

Administrative Policy

28 May 2025 IFA Roundtable Q. 5, 2025-1063771C6 - Computation of FAT

If a foreign affiliate (FA) carries on a business in a foreign county and pays tax to that country on income which the ITA segregates into income...

2022 Ruling 2020-0859851R3 - Foreign accrual tax and underlying foreign tax

Transactions

Canco (a Canadian-resident subsidiary of a Canadian public company) wholly-owns a US corporation (FA1), which owns some of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1.03) | application of the underlying foreign tax rules to the investment of a CFA in a US private REIT through tiered US partnerships based on equity percentage in that REIT | 420 |

11 June 2013 STEP Roundtable, 2013-0480321C6 - 2013 STEP Question 6 US LLCs - FAPI, FAT and FTCs

Is the US tax paid by a Canadian-resident taxpayer on the income (which also is foreign accrual property income) of an LLC which is owned by it...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 113 - Subsection 113(1) - Paragraph 113(1)(c) | 176 | |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(12) | deduction for US tax on LLC income which also is FAPI | 161 |

5 September 2013 External T.I. 2011-0431031E5 - Guatemala's taxes

A Guatemalan-resdent foreign affiliate paid tax on gross revenue at a rate (for 2013) of 5% up to a low threshold (approx. Cdn. $3,925) and 6%...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 126 - Subsection 126(7) - Business-Income Tax | 130 | |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Earnings | tax imposed on revenue rather than income | 118 |

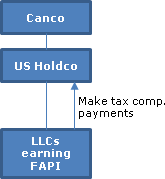

8 April 2004 Internal T.I. 2003-0037291I7 - US LLC and Regulation 5907(1.3)

{kind=link}

A wholly-owned US C-corp subsidiary (US Holdco) of a taxable Canadian corporation wholly-owned two LLCs, which earned only foreign accrual...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Dividend | 82 | |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1.3) | 260 |

15 December 1998 External T.I. 9819355 - FOREIGN AFFILIATES - FOREIGN ACCRUAL TAX

Usco (100% owned by Canco) realized FAPI on the gain from the disposition in Year 1, of a partnership in which it has a 50% interest, of a rental...

27 November 1998 External T.I. 9822835 - FOREIGN AFFILIATES - FOREIGN ACCRUAL TAX

USco1 paid US tax on its share of property income of US LLC (which is a partnership for Code purposes) for 1997. Its Canadian shareholder (Canco)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Accrual Property Income | 121 | |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Underlying Foreign Tax - A - Subparagraph (iii) | tax paid by C-Corp CFA regarding its share of LLC income is not added to its UFT until that income is dividended to it | 143 |

29 October 1997 External T.I. 9719055 - FOREIGN ACCRUAL TAX

What is the "foreign accrual tax applicable" in the following scenario?

|

Income of Affiliate |

Year 1 |

Year 2 |

Year 3 |

Total |

|

Fapi... |

5 June 1996 External T.I. 9618035 - INCOME OR PROFITS TAX FOR FOREIGN AFFILIATE RULES

"'Income or profits tax' for the purpose of the definition 'foreign accrual tax' ... may include Canadian income tax paid by a foreign affiliate...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Paragraph 5907(1)(l) | 31 |

3 September 1991 External T.I. 5-911182

The Department’s view was that the limit on the amount of FAT that can be claimed in respect of a taxable capital gain included in FAPI is the...

3 September 1991 External T.I. 9111825 F - Foreign Pension Arrangements

In 1990, FA disposed of capital property giving rise to a $10,000 capital gain for ITA purposes and a gain for Code purposes of $20,000). After...

84 C.R. - Q.57

A "personal holding company" special tax is a tax on retained earnings of a particular foreign affiliate and is not "income or profits tax".

Articles

Michael Black, "Cross-Border Consolidation and the Foreign Affiliate Rules", Canadian Tax Journal (2017) 65:1, 173-89

CCCTB proposal in European Commission draft EU directive package of October 2016 (pp.175-6)

[I]ncluded in that package is a proposal to revamp the...

Mark Coleman, Daniel A. Bellefontaine, "Forgiveness, Foreign Affiliates and FAPI: a Framework", Resource Sector Taxation (Federated Press), Vol. X, No. 1, 2015, p.694

Whether foreign tax on forgiven amount can be FAT (p. 699)

[T]he definition of FAT requires that the relevant foreign income tax reasonably be...

Mark Coleman, "Treaty Shopping and Back-to-Back Loan Rules", Power Point Presentation for 28 May 2015 IFA Conference in Calgary.

{kind=link}

Non-Treaty Co makes a non-interest-bearing loan to its parent (Treaty Co) to fund an interest-bearing loan to the Canadian-resident parent of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.1) - Paragraph 212(3.1)(c) | 240 | |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.1) - Paragraph 212(3.1)(d) | 90 |

Michael G. Bronstetter, Douglas R. Christie, "The Fickle Finger of FAT: An Analysis of Foeign Accrual Tax", Canadian Tax Journal, (2003) Vol 51, No. 3, p. 1317

[I]t can be difficult to envision how any foreign tax could be appliable to an amount incuded as a taxpayer's share of FAPI pursuant to subsection...

Foreign Affiliate

Administrative Policy

3 November 2021 CTF Roundtable Q. 14, 2021-0911951C6 - Failure to properly file a T1135

The T1135 form and related disclosure stated that specified foreign property “does not include … a share of the capital stock or indebtedness...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 233.3 - Subsection 233.3(1) - Specified Foreign Property - Paragraph (k) | CRA will entertain penalty and interest waiver where taxpayer was misled by Form as to the narrowness of FA exclusion | 208 |

18 February 2013 External T.I. 2012-0467121E5 - Associated corporations, Debt Forgiveness

Husband and Wife own 51% and 49% of the shares of a non-resident corporation (ForeignCo) and 49% and 51% of the shares of CanadaCo. The two...

15 July 2011 Internal T.I. 2010-0388621I7 - Entity Classification - Liechtenstein Anstalt

A Liechtenstein anstalt did not issue shares within the meaning of s. 248(1), as there was only one beneficiary. However, a division of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Corporation | anstalt a corp | 98 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Share | division of capital not necessary for "shares" | 136 |

2004 Ruling 2004-0103111R3 - Foreign affiliates; indirect payment

Ruling that a U.S. LLC would be considered a corporation, that the ownership interest of a member would be considered shares, and that...

27 June 1994 External T.I. 9406005 - CORPORATE STATUS OF A DELAWARE LLC (4093-U5-100-4)

If a Delaware limited liability company is treated as a partnership rather than a corporation for purposes of the Internal Revenue Code, with the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Corporation | 29 | |

| Tax Topics - Income Tax Act - Section 250 - Subsection 250(5) | 96 | |

| Tax Topics - Treaties - Income Tax Conventions - Article 4 | 67 |

16 December 1993 T.I. (C.T.O. "6363-1 Foreign Affiliate Deemed Active Business Income")

A Wyoming limited liability corporation that indirectly was owned 50% by each of two Canadian corporations dealing at arm's length with each other...

93 C.M.TC - Q. 12

The limited liability companies for the two states that RC has reviewed (Wyoming and Florida) are considered to be corporations rather than...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Corporation | 25 |

December 1992 B.C. Tax Executives Institute Round Table, Q.14 (October 1993 Access Letter, p. 482)

A foreign corporation is a foreign affiliate of a partnership of corporations, and not of the corporate partners.

88 C.R. - Q.11

A corporation resident in a listed country all of whose shares are "owned" by a partnership is not a foreign affiliate of a 30% partner, because...

Finance

5 October 2001 Comfort Letter 20011005B

Proposed amendment to deem for purposes of s. 95(2)(a) a non-resident corporation to be a foreign affiliate of a particular corporation resident...

Foreign Bank

See Also

Loblaw Financial Holdings Inc. v. The Queen, 2018 TCC 182, rev'd on s. 95(1) - investment business - (a) (arm's length conduct) grounds 2020 FCA 79, in turn aff'd 2021 SCC 51

The Minster assessed the taxpayer on the basis that its Barbados subsidiary (GBL) had realized $473 million of foreign accrual property income...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 165 - Subsection 165(1.11) | requirement met where Crown knew the nature and quantum of the dispute | 269 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Investment Business - Paragraph (a) | Barbados-licensed international bank, which used Loblaw funding to invest responsively to Loblaw considerations, conducted an offside non-arm’s length business | 429 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Investment Business - Paragraph (c) | employee equivalents was reduced by employee time described in s. 95(2)(b) | 290 |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Foreign Exchange | short-term debt securities were inventory because they were the raw material for generating swap income | 130 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4.01) - Paragraph 152(4.01)(a) - Subparagraph 152(4.01)(a)(ii) | GAAR is generally a separate matter rather than being subsumed in the allegedly-misused substantive provision | 208 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | application of GAAR required the occurrence of an avoidance transaction (or series) in non-statute-barred years and the relevant previous year’s avoidance transaction did not occur as part of the series | 512 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | hiring of employees 15-years previously to engage foreign bank exception to investment business definition was not part of same series as renewal of foreign bank licence | 228 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | use of Barbados sub to engage in proprietary trading for Canadian parent misused the foreign bank exemption, whose purpose was promoting international competitiveness | 336 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(l) | purpose of s. 95(2)(l) exception was to permit non-resident subsidiaries of Canadian banks and dealers to compete internationally | 190 |

CIT Group Securities (Canada) Inc. v. The Queen, 2016 TCC 163, 2017 TCC 86

The question of whether an indirect Barbados subsidiary (“CCG”) of a Canadian company in the CIT group was earning property income and, thus,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(l) - Subparagraph 95(2)(l)(iii) | regulated Barbados subsidiary which invested in corporate debt qualified under the s. 95(2)(l) exclusion for foreign banks | 767 |

| Tax Topics - General Concepts - Evidence | hearsay evidence could support expert opinion | 122 |

Income from Property

Articles

John Lorito, Trevor O'Brien, "International Finance – Cash Pooling Arrangements", 2014 Conference Report, (Canadian Tax Foundation), 20:1-33

Cash risked in active business (p.20:24-25)

Interest earned by a foreign affiliate on cash/deposits risked in the active business of the foreign...

Powrie, "The Potential for Realizing Foreign Accrual Property Income in Structuring Foreign Exploration and Development Ventures", International Tax Planning, Vol. VI, No. 1, p. 379

Includes a discussion of the distinction between income from an adventure or concern in the nature of trade, and income from an active business.

Investment Business

See Also

R&C Commrs v. Lockyer & Anor (for Pawson Estate), [2013] UKUT 050 (Tax and Chancery Chamber)

The deceased taxpayer and her three children held equal interests in a bungalow ("Fairhaven"), which they rented out as a holiday property. The...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Specified Investment Business | actively-manged holiday property an investment | 407 |

Indema Ltd. v. The Queen, 92 DTC 6244, [1992] 1 CTC 309 (FCTD)

The taxpayer was incorporated in 1972 in order to act as a distributor, but four years later its objects were extended and in 1978 it agreed to...

Administrative Policy

2009 Ruling 2009-0308961R3 - Principal Purpose of Business

A CFA ("CFA1") which has been developing IP, manufacturing products for distribution by affiliates and employing more than five-full time...

14 December 2008 Internal T.I. 2008-0299161I7 - five employees

When asked whether it would apply the finding in 489599 B.C. Ltd. v. The Queen, 2008 TCC 332, that the requirement for "more than five full time...

5 April 2001 External T.I. 2000-0058445 F - Entreprise de gestion et REATB

A U.S. corporation with fewer than five employees derives all of its income as management fees from managing the rental real estate (e.g.,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(b) | s. 95(2)(b) application to provision of services to rental partnerships | 113 |

26 October 2000 Internal T.I. 2000-004438

A controlled foreign affiliate of the taxpayer ("USCo") has several wholly-owned subsidiaries (Landcos) resident in the United States each of...

24 August 1999 External T.I. 9701345 - FOREIGN AFFILIATES - DEEMED ACTIVE INCOME

Mr X, a Canadian-resident individual, owns all of FA1 which, in turn owns 100% of FA2. FAl carries on a US business of acquiring and developing...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(a) - Subparagraph 95(2)(a)(i) | one development project held though subsidiary | 197 |

1 December 1997 Tax Executives Institute Roundtable Q. IX 8M17870F

A bank as part of its investment banking activities purchases LP interests in limited partnerships that actively trade non-Candian debt and equity...

13 November 1997 External T.I. 9722535 - FOREIGN AFFILIATES - INVESTMENT BUSINESS

In a situation where a foreign affiliate develops resource property and derives profits from the disposition of such resource properties once...

10 November 1997 External T.I. 9711175 - FOREIGN AFFILIATES - INVESTMENT BUSINESS

An International Business Corporation incorporated in Barbados whose business consisted solely of marketing and the collection of receivables...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(11.2) | 59 |

10 November 1997 External T.I. 9722265 - FOREIGN AFFILIATES - INVESTMENT BUSINESS

If a commissionaire through whom a foreign affiliate did business was merely an agent, the foreign affiliate would be considered to be doing...

22 September 1997 External T.I. 9641615 - INVESTMENT BUSINESS-TRADING IN COMMODITIES BY FA

Regarding a foreign affiliate of a Canadian corporation that was in the business of buying and selling natural gas and that hedged uncovered...

26 July 1995 T.I. 950977 (C.T.O. "6363-1 Meaning of the Term "Regulated")

Where a foreign affiliate is licensed under the Barbadian Off-Shore Banking Act to carry on business activities defined under that Act as...

14 July 1995 External T.I. 9509775 - 6363-1 FOREIGN AFFILIATES - INVESTMENT BUSINESS

The fact that a foreign affiliate receives funding to carry on its income earning activity by way of debt or equity from a related party would...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Paragraph 95(2)(a) (historical) | 103 |

28 June 1995 External T.I. 9505615 - 6363-1 FOREIGN AFFILIATES - INVESTMENT BUSINESS

In response to the question as to whether a particular foreign affiliate is able to include the services provided to it by its own employees in...

6 December 1995 No. 9530400

CRA repeated the position set out in 6363-1 immediately below that:

a part-time employee who is employed in the active conduct of the affiliate's...

1995 International Fiscal Association Conference, Q. 3 6363-1

In response to a question as to how Revenue Canada assesess whether a foreign affiliate employs more than five employees full time in the active...

1995 Tax Executives Institute Round Table, Q. 13 No. 9530400

When an employee is employed directly by Company A under a 80% part-time employment contract and is also employed directly by Company B under a...

31 October 1995 External T.I. 9526255 - FOREIGN AFFILIATES - EMPLOYEE EQUIVALENCY TEST

Two foreign affiliates (Aco and Bco) each carries on the business of real estate development and employ individuals in the active conduct of that...

Articles

Franco-Nevada Press Release, "Franco-Nevada Reaches Settlement on Canadian Tax Disputes", 11 September 2025 Press Release of Franco-Nevada Corporation

Franco-Nevada has settled its appeal of CRA reassessments of its 2013 to 2019 taxation years in respect of its Barbados and Mexican subsidiaries...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) | Franco-Nevada settles its transfer-pricing dispute on the basis of no FAPI from steaming agreements, and 30% mark-up for its management charges, re its Barbados and Mexican subsidiaries | 239 |

Tasso Lagios, Arda Minassian, "Foreign Accrual Property Income: Pitfalls for the Unwary", 1999 Conference Report, c. 3.

Jack Bernstein, "Canadian Taxation of Technology: Part II", Tax Profile, Vol. 5, No. 15, November 1997, p. 169

Discussion of utilization of international licensing companies.

Ahmed, "The Investment Business Definition", Canadian Current Tax, Vol. 6, No. 8, May 1996, p. 71.

Paragraph (a)

Cases

Canada v. Loblaw Financial Holdings Inc., 2021 SCC 51, [2021] 3 S.C.R. 687

The taxpayer, an indirect wholly-owned subsidiary of the Loblaw public company, wholly-owned a Barbados subsidiary (Glenhuron), that was licensed...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Business | “business conducted,” as contrasted to “business,” did not include the raising of capital | 229 |

| Tax Topics - General Concepts - Foreign Law | meaning of banking business under Barbados law was not persuasive | 234 |

| Tax Topics - Statutory Interpretation - Certainty | full effect should be given to Parliament’s precise and unequivocal words to produce certainty | 88 |

| Tax Topics - Statutory Interpretation - Speaking in vain | Parliament does not speak in vain | 72 |

| Tax Topics - Income Tax Act - Section 91 - Subsection 91(1) | two policies balanced in FAPI regime | 79 |

| Tax Topics - Statutory Interpretation - Expressio Unius est Exclusio Alterius | specific addition of a competition requirement in another provision implied that there was no such requirement here | 152 |

Loblaw Financial Holdings Inc. v. Canada, 2020 FCA 79, aff'd 2021 SCC 51

The taxpayer, an indirect wholly-owned subsidiary of the Loblaw public company, wholly-owned a Barbados subsidiary (Glenhuron), that was licensed...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Business | receipt of equity funds from parent was not part of Barbados bank’s business | 188 |

| Tax Topics - Statutory Interpretation - Redundancy/ reading in words/ speaking in vain | error to apply an unexpressed intention | 172 |

| Tax Topics - Statutory Interpretation - Drafting Style | no additional requirements should be inferred in legislation drafted with “mind-numbing detail” | 172 |

| Tax Topics - General Concepts - Separate Existence | subsidiary did not manage its funds on behalf of parent | 161 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Accrual Property Income | fundamental purpose of FAPI is to capture passive income | 164 |

See Also

Loblaw Financial Holdings Inc. v. The Queen, 2018 TCC 182, rev'd on s. 95(1) - investment business - (a) (arm's length conduct) grounds 2020 FCA 79, in turn aff'd 2021 SCC 51

The taxpayer, which was an indirect wholly-owned subsidiary of Loblaw Companies Limited (a Canadian public company) wholly-owned a Barbados...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 165 - Subsection 165(1.11) | requirement met where Crown knew the nature and quantum of the dispute | 269 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Bank | CFA qualified as a foreign bank since it was licensed under Barbados law as an international bank | 123 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Investment Business - Paragraph (c) | employee equivalents was reduced by employee time described in s. 95(2)(b) | 290 |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Foreign Exchange | short-term debt securities were inventory because they were the raw material for generating swap income | 130 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4.01) - Paragraph 152(4.01)(a) - Subparagraph 152(4.01)(a)(ii) | GAAR is generally a separate matter rather than being subsumed in the allegedly-misused substantive provision | 208 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | application of GAAR required the occurrence of an avoidance transaction (or series) in non-statute-barred years and the relevant previous year’s avoidance transaction did not occur as part of the series | 512 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | hiring of employees 15-years previously to engage foreign bank exception to investment business definition was not part of same series as renewal of foreign bank licence | 228 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | use of Barbados sub to engage in proprietary trading for Canadian parent misused the foreign bank exemption, whose purpose was promoting international competitiveness | 336 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(l) | purpose of s. 95(2)(l) exception was to permit non-resident subsidiaries of Canadian banks and dealers to compete internationally | 190 |

Paragraph (c)

See Also

Loblaw Financial Holdings Inc. v. The Queen, 2018 TCC 182, rev'd on s. 95(1) - investment business - (a) (arm's length conduct) grounds 2020 FCA 79, in turn aff'd 2021 SCC 51

The taxpayer, which was an indirect wholly-owned subsidiary of Loblaw Companies Limited (a Canadian public company) wholly-owned a Barbados...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 165 - Subsection 165(1.11) | requirement met where Crown knew the nature and quantum of the dispute | 269 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Bank | CFA qualified as a foreign bank since it was licensed under Barbados law as an international bank | 123 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Investment Business - Paragraph (a) | Barbados-licensed international bank, which used Loblaw funding to invest responsively to Loblaw considerations, conducted an offside non-arm’s length business | 429 |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Foreign Exchange | short-term debt securities were inventory because they were the raw material for generating swap income | 130 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4.01) - Paragraph 152(4.01)(a) - Subparagraph 152(4.01)(a)(ii) | GAAR is generally a separate matter rather than being subsumed in the allegedly-misused substantive provision | 208 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | application of GAAR required the occurrence of an avoidance transaction (or series) in non-statute-barred years and the relevant previous year’s avoidance transaction did not occur as part of the series | 512 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | hiring of employees 15-years previously to engage foreign bank exception to investment business definition was not part of same series as renewal of foreign bank licence | 228 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | use of Barbados sub to engage in proprietary trading for Canadian parent misused the foreign bank exemption, whose purpose was promoting international competitiveness | 336 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(l) | purpose of s. 95(2)(l) exception was to permit non-resident subsidiaries of Canadian banks and dealers to compete internationally | 190 |

Investment Property

See Also

Barejo Holdings ULC v. The Queen, 2015 DTC 1216 [at at 1405], 2015 TCC 274, aff'd on other grounds 2016 FCA 304

An offshore fund ("SLT"), in which the taxpayer had an interest, invested in instruments (styled as "Notes") of non-resident subsidiaries of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(11) - Investment Contract | "notes" which tracked actively-managed reference pool of assets were "debt" | 732 |

| Tax Topics - Income Tax Act - Section 94.1 - Subsection 94.1(1) | "notes" which tracked actively-managed reference pool of assets were "debt" and "indebtedness" | 184 |

| Tax Topics - Statutory Interpretation - Interpretation Act - Section 8.1 | quaere whether there is a federal law of "debt" or "charity" | 334 |

Leasing Obligation

Administrative Policy

31 July 2014 Internal T.I. 2014-0536581I7 - Foreign affiliate fresh start rules

Canco acquired a non-resident corporation (FA2) which was engaged in a non-Canadian business of licensing intellectual property to third parties...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(a) - Subparagraph 95(2)(a)(ii) - Clause 95(2)(a)(ii)(B) | licensed IP | 101 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(k) | fresh start rule applies even where the indirectly acquired subsidiary (FA2) carried on a passive IP licensing operation in the preceding year | 637 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Accrual Property Income - A | pro rata allocation of expenses required between FAPI and deemed active business income | 120 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(f.1) | deductions taken for whole year before carve-out under para. (f.1) | 164 |

Participating Percentage

Finance

16 May 2018 IFA Finance Roundtable, Q.8

Transfers under ss. 88(3) and 95(2)(c), (d.1) and (e) can be elected under para. (b) of the “relevant cost base” definition in s. 95(4) to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(4) - Eligible Controlled Foreign Affiliate | drafting deficiency in the relevant cost base rules where FAPI under $5,000 | 189 |

Taxation Year

Administrative Policy

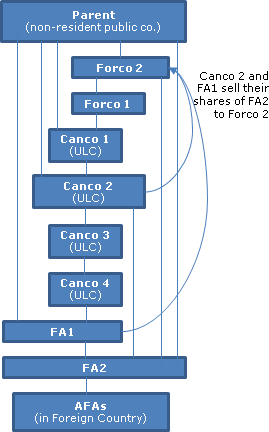

2012 Ruling 2012-0449941R3 - 95(1) - taxation year

{kind=link}

FA2 (which owns directly or indirectly all of the shares of the "AFAs" resident in "Foreign Country") is a controlled foreign affiliate and...

28 January 2008 External T.I. 2005-0165131E5 - Taxation year of a foreign affiliate

The taxation year of a foreign affiliate, for FAPI and surplus account computation purposes, should generally, be the same as the taxation year...

12 July 2000 External T.I. 2000-0036775 - Foreign Affiliates - "Taxation Year"

A change in the statutory and taxation year end (from December 31 to June 30) used by a foreign affiliate for corporate law and foreign taxation...

1 February 1990 Income Tax Severed Letter AC58532 - Foreign Affiliate - Change of Control

In light of its specific wording, s. 95(1)(g) [now, s. 95(1) - taxation year] is not overridden by s. 249(4).

Trust Company

Administrative Policy

15 October 2001 External T.I. 2000-0037355 - Trust Company

An Alberta trust company that offers services to the public as executor, administrator, trustee, bailee etc. and is not authorized to carry on a...

Paragraph 95(2)(a) (historical)

Administrative Policy

14 July 1995 External T.I. 9509775 - 6363-1 FOREIGN AFFILIATES - INVESTMENT BUSINESS

Where loans, which require very little attention once negotiated by a wholly-owned foreign affiliate (the "First Affiliate") which carries on the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Investment Business | 132 |

24 May 1994 External T.I. 9406465 - 6363-1 FOREIGN AFFILIATE - DEEMED ACTIVE BUSINESS INCOME

Discussion of the implications of the 22 February 1994 Budget on the factual situation described below in 16 December 1993 T.I. 932563.

20 May 1993 T.I. (Tax Window, No. 31, p. 3, ¶2509)

Where funds are loaned by FA1 to FA2, which carries on business in the U.S. and, due to the application of the excess interest rule in s. 163(j)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(2) - Paragraph 5907(2)(j) | 109 |

93 C.M.TC - Q. 2

Discussion of treatment of interest paid by one U.S. foreign affiliate to another where only part of the interest paid is deductible under s....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(2) - Paragraph 5907(2)(j) | 33 |

22 July 1991 T.I. (Tax Window, No. 5, p. 15, ¶1326)

Where an international shipping corporation charters a vessel on a bare boat basis from a related foreign affiliate that does not carry on an...

84 C.R. - Q.56

The provisions of s. 95(2)(a)(ii) do not apply where, in certain foreign countries, rules for consolidation permit expenses of one member of the...

80 C.R. - Q.36

An example of income ancillary to an active business is interest earned on working capital that is temporarily invested in short-term bank...

Articles

Chapman, "Foreign Affiliate Amendments: Three Strikes and you are Done", 1995 Canadian Tax Journal, Vol. 43, No. 2, p. 433.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(l) | 0 |

Subsection 95(2) - Determination of certain components of foreign accrual property income

Paragraph 95(2)(a)

Subparagraph 95(2)(a)(i)

Administrative Policy

18 April 2023 Internal T.I. 2020-0864031I7 - Application of subparagraph 95(2)(a)(i)

FA4 and FA5 Subco were US-resident indirect controlled foreign affiliates (CFAs) of Canco in which Canco had a qualifying interest. FA4 owned a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 4 - Subsection 4(1) - Paragraph 4(1)(a) | debt portfolio servicing, and debt portfolio, activities likely were separate businesses | 161 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(b) - Subparagraph 95(2)(b)(i) - Clause 95(2)(b)(i)(B) | s. 95(2)(b)(i)(B) inapplicable where s. 95(2)(a)(i) deemed the property income of the payer CFA to be active business income, i.e., s. 95(2)(a)(i) applied 1st | 78 |

2016 Ruling 2015-0604451R3 - 95(2)(a)(i)

Background

FA6, which is an indirect wholly-owned subsidiary of Canco, directly or indirectly holds eight other wholly-owned subsidiaries (the...

2015 Ruling 2015-0573141R3 - Subparagraph 95(2)(a)(i)

Current structure

Canco (an indirect subsidiary of Parentco) holds the shares of FA4 (a U.S. corporation) through three stacked U.S. subsidiaries...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Exempt Earnings - Paragraph (d) - Subparagraph (d)(ii) - Clause (d)(ii)(A) - Subclause (d)(ii)(A)(I) | US sub, by servicing both its own debt portfolios and that of a U.S. sister, generated exempt earnings to the sister | 144 |

30 September 2013 Internal T.I. 2012-0439661I7 - Income earmarked for future use & 95(2)(a)(i)

A CFA of Canco held funds generated from projects which were owned and operated by FA1, with the funds being "earmarked" for future investment in...

16 May 2007 May 16, CLHIA Roundtable Q. 19, 2007-0229841C6 - Foreign affiliates - deemed active business income

FA1 enters into insurance or reinsurance contracts in the course of carrying on an active business outside Canada, and reinsures the risk...

9 January 2001 External T.I. 1999-0011405 - foreign affiliates - deemed active

FA2 purchases at a discount long-term interest-bearing receivables of FA1 that were generated by sales made by FA1 in the course of its active...

26 October 2000 Internal T.I. 2000-0044387 - Subsection 95(2)(a)(i)

A U.S. controlled foreign affiliate ("USco") of Canco provides management services to various wholly-owned subsidiaries ("Landcos") resident in...

2 September 1999 External T.I. 9622545 - FOREIGN AFFILIATES - INVESTMENT BUSINESS

FA3 has six full time employees who provide geological and administrative services to FA1 and FA2, which are developing resource properties and...

24 August 1999 External T.I. 9701345 - FOREIGN AFFILIATES - DEEMED ACTIVE INCOME

Mr X, a Canadian-resident individual, owns all of FA1 which, in turn owns 100% of FA2. FA1 carries on a US business of acquiring and developing...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Investment Business | employees prorated based on how they spend their time | 265 |

5 February 1997 External T.I. 9611725 - FOREIGN AFFILIATE - FACTORING BUSINESS

A foreign affiliate ("FA") factors receivables of only one client ("Manco"), a related foreign affiliate. The income of FA derived directly from...

21 May 1996 External T.I. 9526865 - 95(2)(A) - DIRECTLY OR INDIRECTLY

Discussion of the application of the "directly or indirectly" test where a loan made by a foreign affiliate of Canco ("FA") to a related...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(6) - Paragraph 95(6)(b) | 55 |

11 October 1996 APFF Roundtable, 7M12910 - APFF ROUND TABLE

A Finance representative stated:

When it is established that the business conducted by the affiliate is a business carried on actively, certain...

16 August 1995 External T.I. 9521235 - 6363-1 DEEMED ACTIVE BUSINESS INCOME

S.95(2)(a)(i) would apply to interest income earned by a foreign affiliate of Canco from financing purchases by arm's length non-resident...

16 December 1993 Income Tax Severed Letter 9325635 - Foreign Affiliate Deemed Active Business Income

Subparagraph 95(2)(a)(i) will apply to interest income received by a Wyoming limited liability company (that is 50% owned by two arm's length...

Articles

Bruce Sinclair, "Current Topics in the Taxation of Real Estate Development", 2014 Conference Report, (Canadian Tax Foundation), 12:1-24.

Non-application of hypothetical income test where mother ship is subsidiary management LP (p. 12:21)

[C]lause (B)…does not have to be met where...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | 913 | |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2) | 1760 |

Grant J. Russell, "'Mothership' Revisited - Canada's Foreign Affiliate Regime and Active Business Income", International Tax Planning, Vol. XV, No. 4, 2010, p. 1076

Criticizes the CRA position that the activities caried on by a management co. would represents a separate business rather than being assimilated...

Paul C. Barnicke, Melanie Huynh, "Mother Ship in Foreign Affiliate's Partnership", 2009 Canadian Tax Highlights

Angelo Nikolakakis, "The Taxation of Foreign Affiliates in the Resource Sectors", 2008 Conference Report

Nikolakakis, "Foreign Exchange Fluctuations: Comprehensive Rules are Needed", Corporate Finance, Vol. V, No. 1, 1997, p. 342

Discussion of application of s. 95(2)(a) to the hedging by one foreign affiliate of an income stream received for another foreign affiliate...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(g) | 14 |

Subparagraph 95(2)(a)(ii)

Clause 95(2)(a)(ii)(B)

Administrative Policy

25 November 2021 CTF Roundtable Q. 15, 2021-0911921C6 - Curr Use & 95(2)(a)(ii)(B) & (D)

FA Finco, a foreign affiliate of Canadian Parent, lends money to FA Acquireco LLC (a US fiscally-transparent subsidiary of FA Holdco (which is a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(a) - Subparagraph 95(2)(a)(ii) - Clause 95(2)(a)(ii)(D) - Subclause 95(2)(a)(ii)(D)(I) | acquisition of shares that were not excluded property qualified under current use test | 168 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(a) - Subparagraph 95(2)(a)(ii) - Clause 95(2)(a)(ii)(D) - Subclause 95(2)(a)(ii)(D)(III) | in light of the current-use test, borrowed money used to acquire shares that were not excluded property could satisfy s. 95(2)(a)(ii)(D) | 212 |

2 March 2017 External T.I. 2017-0682291E5 - Swedish/Finnish Profit Transfer Agreements

Many foreign jurisdictions, such as Germany, Sweden and Finland, have profit transfer agreement (“PTA”) mechanisms that allow for full or...

22 June 2016 Internal T.I. 2016-0632821I7 F - 93(2.01) & Capital Contribution

A wholly-owned foreign affiliate (“Luxco1”) of Canco held 1/3 of the shares of a corporation ("NRco"), which was resident in a Treaty country...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 93 - Subsection 93(2.01) | a contribution of FA1 shares to FA2 causes the FA2 shares to be substituted property for s. 93(2.01) purposes | 195 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(5) | ordinary meaning of “substituted” | 121 |

26 May 2016 IFA Roundtable Q. 8, 2016-0642041C6 - s. 95(2)(a)(ii)(B) and borrowing to return capital

Where FA1 borrows $350,000 from a sister (FA3) to make a capital distribution to its Canadian shareholder (Canco) on its Class A common shares,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(2) - Paragraph 5907(2)(j) | interest used to fund return of capital that had been used in an active buisness deductible under Reg. 5907(2)(j) | 219 |

26 May 2016 IFA Roundtable Q. 6, 2016-0642081C6 - German Organschafts

Under an “Organschaft,” a German parent (“Parentco”) and its German subsidiary (“Subco”) can enter into an agreement under which Subco...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(2) | profit transfer payments by German sub to its German parent deemed to be dividends under s. 90(2) | 319 |

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(1) - Paragraph 53(1)(c) | German profit transfer payment to loss subsidiary is contribution of capital | 158 |

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(x) | loss compensation payment under Organschaft | 123 |

28 May 2015 IFA Roundtable Q. 11, 2015-0581571C6 - IFA 2015 Q11: Application of clause 95(2)(a)(ii)(B)

"Borrower FA," which exclusively carries on an active business, borrows money from "Lender FA" to pay a dividend in an amount not exceeding its...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(2) - Paragraph 5907(2)(j) | interest on borrowing to distribute accumulated profits | 172 |

31 July 2014 Internal T.I. 2014-0536581I7 - Foreign affiliate fresh start rules

Canco acquired a non-resident corporation (FA2) which was engaged in a non-Canadian business of licensing intellectual property to third parties...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Leasing Obligation | licensed IP | 68 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(k) | fresh start rule applies even where the indirectly acquired subsidiary (FA2) carried on a passive IP licensing operation in the preceding year | 637 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Accrual Property Income - A | pro rata allocation of expenses required between FAPI and deemed active business income | 120 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(f.1) | deductions taken for whole year before carve-out under para. (f.1) | 164 |

2002 Ruling 2001-0093903 - German Organschaft

Background

Canco, a Canadian public company, holds all the shares of a German Gesellschaft mit beschränkter Haftung (“FA Holdco”) which, in...

29 June 2012 Internal T.I. 2012-0441601I7 - "directly or indirectly"

{kind=link}

Luxco (a Lux subsidiary of Canco) makes an interest-bearing loan (Loan1) to Mereco (which is the non-resident parent of Canco and does not caary...

2004 Ruling 2004-0103111R3 - Foreign affiliates; indirect payment

Ruling that s. 95(2)a)(ii)(B) would apply where a controlled French foreign affiliate made lease payments to a groupement d'intérêt économique...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 113 - Subsection 113(1) | 33 | |

| Tax Topics - Income Tax Act - Section 2 - Subsection 2(1) | 34 | |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Affiliate | 33 |

22 October 2002 Internal T.I. 2002-0149977 - Interest income deemed ABI of A CFA

Where Irishco (a foreign affiliate in which Canco has a qualified interest) lends at a market rate of interest to U.S. Holdco (a wholly-owned...

5 September 2002 External T.I. 2000-00742

FA1 lends money to FA2 (a Swedish company) which uses the borrowed funds to acquire the shares of FA3 (another Swedish company) whose sole source...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(a) - Subparagraph 95(2)(a)(ii) - Clause 95(2)(a)(ii)(D) | 109 |

10 October 2000 External T.I. 2000-0050385 - Deemed active business income

A sub of Canco in Country B ("Finco") lends money to a wholly-owned subsidiary of Canco in Country A ("Holdco"). Holdco on-lends the money, at a...

6 January 1999 External T.I. 9829785 - FOREIGN AFFILIATE-ACTIVE BUSINESS INCOME

Where a foreign subsidiary of Canco deposits a sum with a foreign bank to secure its guarantee of a loan made by the foreign bank to another...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Excluded Property | 70 |

7 August 1996 External T.I. 9605735 - MEANING OF "DIRECTLY OR INDIRECTLY" IN 95(2)(A)

After being referred to an arrangement under which a foreign affiliate ("Forco"), which has made a loan to a related foreign subsidiary ("Xco"),...

1 February 1996 External T.I. 9517445 - MEANING OF "DIRECTLY OR INDIRECTLY" IN 95(2)(A)

The words "directly or indirectly" in s. 95(2)(a)(ii)(B) "were meant to deal with back-to-back loans in certain fronting arrangements involving...

21 June 1995 T.I. 951091

Where a corporation resident in Canada ("Canco") has a wholly-owned subsidiary that is resident in a designated treaty country ("FA"), and FA...

25 April 1995 External T.I. 9429875 - 6363-1 FOREIGN AFFILIATES DEEMED ABI

Where one wholly-owned U.S. subsidiary ("B") of a Canadian corporation ("A") loans money on an interest-bearing basis to a second wholly-owned...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(2.7) | 90 |

Finance

16 May 2018 IFA Finance Roundtable, Q.6

Among the requirements for s. 95(2)(a)(ii) to deem interest paid by a foreign affiliate to be active business income is that the interest be...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(2) - Paragraph 5907(2)(j) | interest denied under U.S. hybrid rule would be deductible | 85 |

Articles

Ilia Korkh, Eivan Sulaiman, "Outbound Partnerships: FAPI in Unexpected Places", Canadian Tax Highlights, Vol. 27, No. 12, December 2019, p. 10

Interposition of partnership may engage s. 95(2)(a)(ii)(B) (p. 10)

[F]our arm’s-length Canadian corporations (Cancos) each own 25 percent of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 91 - Subsection 91(1) | 158 |

Jack Bernstein, Francesco Gucciardo, "Canada-U.S. Hybrid Financing – A Canadian Perspective on the U.S. Debt-Equity Regs", 26 September 2016, p. 1151

Recharacterization rules under Code s. 385 (p.1152)

Most fundamentally, the proposed regulations would automatically treat what would otherwise be...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | 429 |

Ian Gamble, "Income from a Business or Property: General Principles and Current Issues", 2014 Conference Report, Canadian Tax Foundation, 5:1-32

CFA holding company can hold shares of CFA subs as an investment business (p. 5:19)

[A] top-tier holding affiliate in a foreign country may have...

John Lorito, Trevor O'Brien, "International Finance – Cash Pooling Arrangements", 2014 Conference Report, (Canadian Tax Foundation), 20:1-33

Difficulties in establishing tracing in cash pool (p. 22)

It may be possible for interest earned by a foreign affiliate from deposits/loans made...

Melanie Huynh, Eric Lockwood, "Foreign Accrual Property Income: A Practical Perspective", International Tax Planning, 2000 Canadian Tax Journal, Vol. 48, No. 3, p. 752.

Tasso Lagios, Arda Minassian, "Foreign Accrual Property Income: Pitfalls for the Unwary", 1999 Conference Report, c. 3.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85.1 - Subsection 85.1(3) | 0 | |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Investment Business | 0 |

Ahmed, "Selected Issues Relating to the 1995 Foreign Affiliate Amendments", International Tax Planning, 1997 Canadian Tax Journal, p. 2141.

Lanthier, Tobin, "Intercorporate Financing of Canadian Investment in the United States", Cross-Border Taxation Issues and Developments 1996, International Fiscal Association, p. 211.

Finance

Subclause 95(2)(a)(ii)(B)(II)

Administrative Policy

31 August 2017 Internal T.I. 2016-0680801I7 - Interpretation- subclause 95(2)(a)(ii)(B)(II) Act

A foreign corporation (“FP”) owns 100% of Canco, which wholly-owns two non-resident corporations (“FA1,” a Holdco, and “FALuxco”). FA1...

Articles

Tina Korovilas, Drew Morier, "Non-Corporate Vehicles in the Foreign Affiliate Context", 2018 Conference Report (Canadian Tax Foundation), 20:1 – 114

Dubious textual interpretation of s. 95(2)(a)(ii)(B)(II) (“Cap B”) in 2016-0680801I7 (pp. 20:65-69)

The CRA recently considered the...

Nathan Boidman, Michael N. Kandev, "Expected Adverse Effects of Proposed U.S. Anti-Hybrid Regulations on Inbound Financing by Canadian MNEs", Tax Notes International, February 11, 2019, p. 623

Anti-hybrid rule in IRC s. 267A (p. 624)

The anti-hybrid rule in section 267A(a) simply states that the law will not allow a deduction for any...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 113 - Subsection 113(1) - Paragraph 113(1)(a) | 232 |

Clause 95(2)(a)(ii)(D)

Administrative Policy

27 January 2017 External T.I. 2013-0482351E5 - Clause 95(2)(a)(ii)(D)

Canco wholly-owns two controlled foreign affiliates (“FA Finco” and “FA Holdco”). Canco, FA Finco and FA Holdco have calendar year ends....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(9.1) | s. 18(9.1) applied where loan prepayment penalty was equal to PV of interest thereon | 180 |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(2.7) | loan prepayment penalty fully deducted from surplus when paid | 161 |

24 November CTF Annual Roundtable, Q.9

S. 95(2)(a)(ii)(D) may apply to deem interest payments received by FA #1 from FA #2 (the “Second Affiliate”) in a year on money borrowed by...

28 May 2015 IFA Roundtable Q. 6, 2015-0581601C6 - IFA 2015 Q.6: Reversal of position on 95(2)(a)(ii)(D)

In 2013-0496841I7, CRA took the position that s. 95(2)(a)(ii)(D) did not apply to recharacterize interest on a debt ("Note 2") issued by FA2 to...

21 October 2013 Internal T.I. 2013-0496841I7 - Application of clause 95(2)(a)(ii)(D) ITA

{kind=link}

Following preliminary transactions, Canco held all the membership interest in a U.S. LLC (NR1) as well as 99.99% ownership of a [Netherlands?]...

1 May 2009 CLHIA Roundtable Q. 12, 2009-0317191C6 - CLHIA Roundtable Question #12- 95(2)(a)(ii)(D)

Respecting a situation where Borrower and Subsidiary are resident in Country A and are liable to tax on a worldwide basis in Country B, CRA stated...

5 September 2002 External T.I. 2000-00742

FA1 lends money to FA2 (a Swedish company) which uses the borrowed funds to acquire the shares of FA3 (another Swedish company) whose sole source...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(a) - Subparagraph 95(2)(a)(ii) - Clause 95(2)(a)(ii)(B) | 115 |

2002 Ruling 2002-0138993 - XXXXXXXXXX . - 95(2)(a)(ii)(D)

A foreign affiliate of the taxpayer ("Finco") in Country B makes a loan to a subsidiary of the taxpayer ("Holdco") in Country A. In connection...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(3) | 139 |

1 November 2000 External T.I. 1999-0009725 - Foreign affiliates meaning of group

A wholly-owned subsidiary ("Subco B") of a U.S. operating corporation ("Opco") that was not resident in the United States and that was not part of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Excluded Property | 155 |

25 February 2000 External T.I. 99-000968

A wholly-owned foreign affiliate of Canco ("FA1") lends money to a wholly-owned U.K subsidiary of Canco (UK1) which, in turn, uses the borrowed...

14 May 1997 External T.I. 9605355 - foreign affiliates-meaning group of corporations

General discussion of s. 95(2)(a)(ii)(D)(v).

5 February 1997 External T.I. 9635625 - FOREIGN AFFILIATES - RELEVANT, LIABILITY FOR TAX

Respecting s. 95(2)(a)(ii)(D), RC found that "if an amount is deductible in computing income for income tax purposes, it would generally be...

10 October 1996 T.I. 9630775