Cases

Haworth & Ors v Commissioners for His Majesty's Revenue and Customs, [2025] EWCA Civ 822

The UK-resident taxpayers sought to avoid capital gains tax respecting the disposal of shares by family trusts of which they were the settlors by...

Methanex Trinidad (Titan) Unlimited v The Board of Inland Revenue (Trinidad and Tobago), [2025] UKPC 20

Methanex Trinidad paid U.S.$85.4 million in dividends to its Barbados parent (Methanex Barbados), which promptly paid dividends to its Cayman...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 10 | dividend which was on-paid immediately nonetheless benefited from the Trinidad-Barbados Treaty exemption | 471 |

Commissioners for His Majesty's Revenue and Customs v GE Financial Investments, [2024] EWCA Civ 797

A US company (“GEFI Inc.”) and UK company (“GEFI”) in the GE group formed a Delaware LP (“LP”) with GEFI Inc. as the 1% general...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 5 | passive holding of intercompany loans was not carrying on business for purposes of PE definition in UK-US Treaty | 225 |

Canada v. Alta Energy Luxembourg S.A.R.L., 2021 SCC 49, [2021] 3 S.C.R. 590

In considering whether there had been a treaty-shopping abuse of the Canada-Luxembourg Treaty by virtue of the taxpayer, which had its legal seat...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | Treaty shopping to avoid capital gains tax on Canadian resource assets was contemplated, and not a Treaty abuse | 660 |

| Tax Topics - Treaties - Income Tax Conventions - Article 13 | utilization of the business property exemption by a Luxembourg conduit accorded with the bargain negotiated by Canada, which was to encourage investment by such investors | 605 |

| Tax Topics - Treaties - Income Tax Conventions | subsequent OECD Treaty commentary not followed | 198 |

| Tax Topics - Statutory Interpretation - Treaties | additional consideration in Treaty context of giving effect to the contractual bargain | 237 |

Commissioner of Taxation v Pike, [2020] FCAFC 158

The deteriorating situation in 2004 in Zimbabwe (where they had been born) prompted the taxpayer and his spouse to leave with their children for...

Landbouwbedrijf Backx B.V. v. Canada, 2019 FCA 310

When a Netherlands couple immigrated to Canada in 1998 to acquire a dairy farm here, they created a structure under which the farm was held in a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 2 - Subsection 2(1) | notwithstanding sole Netherlands director, decision-making was made by the shareholders in Canada | 169 |

| Tax Topics - Income Tax Act - Section 128.1 - Subsection 128.1(1) - Paragraph 128.1(1)(c) | s. 128.1(1)(c) step-up turned upon becoming resident in Canada | 368 |

CGI Holding LLC v. Canada (National Revenue), 2016 FC 1086

The taxpayer (“CGI”) was a Delaware LLC which, in 2007, was subject to 25% withholding tax on a dividend of $142 million from a Nova Scotia...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 227 - Subsection 227(10.1) | s. 227(10.1) application nullified as CRA not given enough time | 220 |

Trieste v. Canada, 2012 FCA 320, aff'g 2012 DTC 1125 [at 3133], 2012 TCC 91

Lamarre J. found that the taxpayer, a U.S. citizen, was resident in Canada during the relevant tax period, pursuant to Art. IV(2)(b) of the...

St. Michael Trust Corp. v. Canada, 2010 DTC 5189 [at at 7361], 2010 FCA 309, aff'd sub nom Fundy Settlement v. Canada, 2012 DTC 5063 [at 6881], 2012 SCC 14

Barbados trusts, which were resident in Barbados under ordinary principles but which were deemed to be resident in Canada under s. 94(1)(b), were...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | accessing Treaty residence not abusive | 120 |

| Tax Topics - Income Tax Act - Section 94 - old | 209 |

Morris v. Canada (National Revenue), 2009 FC 434

In finding that a Barbados trust was resident in Barbados and not in Canada for purposes of the Barbados-Canada Income Tax Convention, Simpson,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 116 - Subsection 116(2) | 49 |

Bujnowski v. Canada, 2006 DTC 6071, 2006 FCA 32

The taxpayer, who lived and worked in the United States for ten months in 2001 (throughout which period his wife continued to live in the family...

Allchin v. Canada, 2004 DTC 6468, 2004 FCA 206

The taxpayer, who held a green card and worked in the hospital industry selling hospital supplies throughout the United States, was thereby a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 180 - Subsection 180(3) | correctness standard for isolated legal error | 62 |

| Tax Topics - Treaties - Income Tax Conventions | technical explanations | 28 |

Crown Forest Industries Ltd. v. Canada, 95 DTC 5389, [1995] 2 S.C.R. 802, [1995] 2 CTC 64

Some of the income derived from a corporation incorporated in the Bahamas was effectively connected with the conduct by it of a business in the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions | 83 |

Placrefid Ltd. v. The Queen, 92 DTC 6480, [1992] 2 CTC 198 (FCTD)

A Panamanian corporation was resident in Switzerland for purposes of the Canada-Swiss Convention given that its Panamanian incorporation was "a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 6 | 131 |

See Also

Revenue Commissioners v Susquehanna International Group Ltd & ors, [2025] IECA 123

The taxpayers were Irish resident companies, which were part of a group whose ultimate parent was a single member LLC (“SIH LLC”), which was...

G E Financial Investments v.The Commissioners for Her Majesty's Revenue & Customs, [2021] UKFTT 0210 (Tax Chamber), ultimately aff'd [2024] EWCA Civ 797

A US company (“GEFI Inc.”) and UK company (“GEFI”) in the GE group formed a Delaware LP (“LP”) with GEFI Inc. as the 1% general...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 5 | somewhat isolated (albeit in large amounts) loan activity in US did not represent a business under UK concepts and therefore did not entail a US PE under the UK-US Treaty | 508 |

| Tax Topics - Treaties - Income Tax Conventions - Article 24 | UK would have been required to accord foreign tax credit to dual resident company if the US had imposed its taxes in accordance with the PE article | 169 |

Landbouwbedrijf Backx B.V. v. The Queen, 2021 TCC 2

When a Netherlands couple immigrated to Canada in 1998 to acquire a dairy farm here, they created a structure under which the farm was held in a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 128.1 - Subsection 128.1(1) - Paragraph 128.1(1)(c) | no application because taxpayer became a Canadian resident prior to the property's acquisition | 246 |

| Tax Topics - General Concepts - Estoppel | Minister not precluded from reassessing contrary to initial acceptance of non-residency in returns as filed | 109 |

| Tax Topics - General Concepts - Evidence | need to adduce expert legal evidence as to tax residency in foreign jurisdiction | 88 |

GE Energy Parts Inc. v. Commissioner of Income Tax (International Taxation), ITA 621/2017, 21 December 2018 (High Court of Delhi)

The assesses were non-resident companies (“GE Overseas”) in the General Electric (GE) group who used the services of (i) expatriate employees...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 7 | portion of profits attributable to marketing estimated at 26% | 116 |

Landbouwbedrijf Backx B.V. v. The Queen, 2018 TCC 142, confirmed on s. 2(1) grounds, remitted for reconsideration on s. 128.1(1)(c) and Treaty grounds 2019 FCA 310

A Netherlands corporation was found to be resident in Canada by virtue of its central management and control being in Canada. (Its sole...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 2 - Subsection 2(1) | the central management and control of a B.V. with a sole Dutch director was in Canada | 319 |

| Tax Topics - Income Tax Act - Section 128.1 - Subsection 128.1(1) - Paragraph 128.1(1)(c) | no application of s. 128.1(1)(c) as central management and control had been in Canada from the time of the investment | 284 |

Davis v. The Queen, 2018 TCC 110

The taxpayer (Mr. Davis) had moved to Massachusetts to work as an engineer for 10 years before his return to Canada following the elimination of...

Anson v. HMRC, [2015] UKSC 44

The relevant provision of the UK-US Treaty required that the UK tax on LLC distributions be "computed by reference to the same profits or income...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Corporation | profits of LLC earned directly by members | 42 |

| Tax Topics - Treaties - Income Tax Conventions - Article 24 | UK LLC member had a personal (non-proprietary) entitlement to his share of LLC profits as they arose | 485 |

| Tax Topics - Treaties - Income Tax Conventions - Article 3 | scheme in Treaty article for allocating income between jurisdictions amounted to a definition of "source" | 88 |

Commissioner of Taxation v. Resource Capital Fund III LP, [2014] FCAFC 37 (Fed. Ct. of Austr.)

The appellant ("RCF") was a Caymans limited partnership, with more than 97% of its capital held by a diversified group of US residents,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Other | mining information not to be valued separately at reproduction cost | 296 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Taxable Canadian Property | mining information not to be valued separately at reproduction cost | 296 |

| Tax Topics - Treaties - Income Tax Conventions - Article 13 | mining information not to be valued separately at reproduction cost | 296 |

Black v. The Queen, 2014 DTC 1046 [at at 2882], 2014 TCC 12, briefly aff'd 2014 FCA 275

In 2002, the taxpayer was resident both in Canada and the U.K. for domestic tax purposes, but by virtue of Art. 4, para. 2(a) of the Canada-U.K...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Interpretation Act - Subsection 45(2) | amendments usually change the Act | 185 |

| Tax Topics - Statutory Interpretation - Other/Conflicting Statutes | presumption against inconsistency | 99 |

| Tax Topics - Treaties - Income Tax Conventions - Article 29 | Treaty residence not domestically applicable | 281 |

Resource Capital Fund III LP v. Commissioner of Taxation, [2013] FCA 363 (Fed. Ct. of Austr.), rev'd supra.

The appellant ("RCF") was a Caymans limited partnership, with more than 97% of its capital held by a diversified group of US residents,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Other | 412 | |

| Tax Topics - Treaties - Income Tax Conventions - Article 13 | mine deriving value from information | 412 |

Dysert v. The Queen, 2013 DTC 1070 [at at 373], 2013 TCC 57

The taxpayers were middle-aged "all American" certified cost estimate professionals, with no significant previous exposure to Canada, who came to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 2 - Subsection 2(1) | 169 | |

| Tax Topics - Income Tax Act - Section 250 - Subsection 250(1) - Paragraph 250(1)(a) | 171 |

TD Securities (USA) LLC v. The Queen, 2010 TCC 186

The taxpayer, which was a U.S. limited liability company ("LLC") that carried on business in Canada through a Canadian branch with the income from...

Lingle v. The Queen, 2009 DTC 1705, 2009 TCC 435, aff'd 2010 DTC 5100 [at 6932], 2010 FCA 152

Campbell J. found that the taxpayer's habitual abode was in Canada. She stated at para. 30:

It follows that the proper approach to determining...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 2 - Subsection 2(1) | 37 |

Minin v. The Queen, 2008 DTC 4463, 2008 TCC 429

The taxpayer, who worked on a succession of jobs in the United States and stayed at different places there, was found to have a permanent home...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Timing | 55 | |

| Tax Topics - Income Tax Act - Section 2 - Subsection 2(1) | 72 |

Garcia v. The Queen, 2007 DTC 1593, 2007 TCC 548 (Informal Procedure)

The taxpayer, who was resident both in Canada and the United States in 2003 when he received a bonus that had been earned in 2002, was found to be...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 15 | "derived" referred to geographic source | 72 |

Salt v. The Queen, 2007 DTC 520, 2007 TCC 118

The taxpayer, when he was moved by his employer to Australia rented the Canadian home of him and his wife under 22 1/2 month lease which, under...

Yoon v. The Queen, 2005 DTC 1109, 2005 TCC 366

Given the depth of her roots in South Korea, the taxpayer's centre of vital interests was in South Korea rather than Canada. South Korea also was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Evidence | 59 | |

| Tax Topics - Income Tax Act - Section 2 - Subsection 2(1) | 71 |

Allchin v. The Queen, 2005 DTC 603, 2005 TCC 476

The taxpayer, who stayed in Michigan in a condominium owned by her friends without paying rent and who visited, on a weekly basis, her husband and...

Gaudreau v. The Queen, 2005 DTC 66, 2004 TCC 840, aff'd 2005 DTC 5702, 2005 FCA 388

The taxpayer, who had moved with his wife to Egypt for a four-year work assignment and who maintained their home in Ontario in addition to an...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 2 - Subsection 2(1) | 78 |

Edwards v. The Queen, 2002 DTC 1856 (TCC)

The taxpayer, who was a resident of Canada and was employed as a commercial airline pilot by a wholly-owned subsidiary of a Hong Kong airline...

Wang v. The Queen, 2001 DTC 433 (TCC) (Informal Procedure)

A Chinese national who entered Canada in April 1998 after receiving landed immigrant status and was paid $19,000 by a Chinese company in order for...

McFadyen v. The Queen, 2000 DTC 2473 (TCC), aff'd 2003 DTC 5015 (FCA)

After already having concluded that the taxpayer was not resident in Japan and only resident in Canada, Garon C.J. went on to state (at p....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Other Legislation/Constitution - Charter (Constitution Act, 1982) - Section 1 | 11 |

Boston v. R., 98 DTC 1124, [1998] 1 CTC 2217 (TCC)

The taxpayer was posted to Malaysia, where he lived in rented premises. His wife whom he was having marital difficulties with continued to live in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 2 - Subsection 2(1) | 131 |

Endres v. R., 98 DTC 1101, [1998] 1 CTC 2259 (TCC)

The taxpayer, who had business interest both in Canada and the United States, commenced spending most of the year, other than the summers, in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 2 - Subsection 2(1) | 160 |

Hertel v. MNR, 93 DTC 721, [1993] 2 CTC 2050 (TCC)

The taxpayer, who was born in Germany but had landed immigrant status in Canada, and who had bank accounts, credit cards, real property, a...

Padmore v. IRC, [1987] BTC 3 (Ch. D.), aff'd [1989] BTC 231 (C.A.)

A Jersey partnership comprising over 100 U.K. resident partners and carrying on a trade which was managed and controlled in Jersey, was a body of...

Administrative Policy

2024 Ruling 2023-0984461R3 - Application of Article IV(7)(b)

Background

A corporation (the “Corporation”), which has elected to be taxed as a REIT for US tax purposes and is a qualifying person for...

5 November 2025 External T.I. 2020-0868261E5 - Article XXI Exemption

A 99% interest in a limited partnership (“Third Tier LP”) was held by two U.S.-resident non-profit organizations (the “Tax Exempt...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 21 | Canadian timber royalties derived by US NPOs through a stacked partnership structure were exempted from Pt. XIII tax under XXI(1) of the Canada-US treaty | 229 |

2025 Ruling 2024-1035241R3 - IV(7)(b) & PUC increase

Background

US Parent, which is a qualifying person for purposes of the Canada-US Convention, wholly owns Holdco, a taxable Canadian corporation...

2025 Ruling 2023-0990951R3 - Safe Income Determination Time Monthly Dividends

It was proposed that, rather than continuing to distribute PUC, Partner B will adopt a policy of paying monthly dividends to Partner A of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Safe-Income Determination Time | series of monthly dividends distributing interest income was not a “series” for SIDT purposes | 538 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | each dividend in a preordained succession of monthly dividends had a SIDT immediately before the dividend payment, i.e., no series | 133 |

6 February 2024 Internal T.I. 2022-0936261I7 - Application of the Canada-US treaty to expats

Regarding a corporation (the “Inverted Payer Corporation”) incorporated under the laws of Canada that is subject to the “anti-inversion...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 250 - Subsection 250(5) | withholding tax rules applicable to a Canadian corporation that is a deemed U.S. resident under IRC §7874(b) and not non-resident per s. 250(5) | 252 |

17 May 2023 IFA Roundtable Q. 6, 2023-0964351C6 - Application of the Canada-US Treaty

Base Case

A US corporate REIT that is a qualifying person under the Canada-US Treaty owns US LLC 1, which owns US LLC 2 which, like US LLC 1, is...

5 October 2021 Internal T.I. 2021-0903361I7 - Remittance Basis Taxation - Canada-Barbados Treaty.

Where dividends paid by a resident corporation to a resident personal discretionary trust are deemed pursuant to s. 104(19) to be received by a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 29 | CRA requires proof that a Barbados remittance-based resident has borne tax on Canadian dividend income before providing the Treaty rate reduction | 278 |

17 May 2022 IFA Roundtable Q. 1, 2022-0933371C6 - Meaning of Habitual Abode

Canada’s treaties typically contain tie-breaker rules for individuals. Typically, if the test of the place of the individual’s permanent home...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 2 - Subsection 2(1) | CRA residence test of “significant, secondary or other ties” | 109 |

25 November 2021 CTF Roundtable Q. 4, 2021-0912111C6 - Liable To Tax & Territorial Taxation

Generally, a person must be “liable to tax” in a contracting state to be a resident there for treaty purposes. Per CRA, a person must be...

27 October 2020 CTF Roundtable Q. 5, 2020-0864281C6 - Article IV:6 of the Canada-US Treaty

A U.S. resident owns a French entity (that is fiscally transparent for U.S., but not Canadian or French purposes) that earns Canadian-source...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 10 | choice between application of France and US Convention to dividends paid by Canco at bottom of multi-tier structure | 217 |

18 April 2019 Internal T.I. 2018-0753621I7 - Subsection 247(12)

Parentco, a corporation resident in the U.S. for Treaty purposes, is the only member of Parentco LLC, which is the only member of Sisterco LLC,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(12) | transfer pricing income adjustment re sale to NR sister gave rise to taxable dividend | 110 |

| Tax Topics - Treaties - Income Tax Conventions - Article 10 | secondary adjustment benefit to a NR sister was a dividend for Treaty purposes | 221 |

4 April 2019 Internal T.I. 2017-0736531I7 - Articles IV(6) and X(6) of the Canada-US Treaty

Two U.S. corporations that were “qualifying persons” for purposes of the Canada-U.S. Treaty (USCo1 and USCo2) held 58% and 42%, respectively,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 10 | Art. IV(6) of the Canada-US Treaty works to reduce Canadian branch profits tax earned through multiple stacked LLCs | 186 |

21 November 2017 CTF Roundtable Q. 11, 2017-0724081C6 - ULC-LLC structures & Treaty

A Canadian-resident unlimited liability company (ULC) pays dividends to its two shareholders, which are each disregarded U.S.-resident Delaware...

13 June 2017 STEP Roundtable Q. 3, 2017-0693451C6 - Dual-resident estate and Article (IV)

The estate of a deceased U.S. citizen may be considered a U.S. estate under U.S. domestic law, and also a Canadian resident estate under the ITA...

26 April 2017 IFA Roundtable Q. 3, 2017-0691131C6 - U.S. LLPs and LLLPs

Are Florida and Delaware LLPs and LLLPs that are treated by CRA as corporations considered to come within para. IV(6) of the Canada-US Treaty?...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 96 | further extension of grandfathering relief for Florida and Delaware LLPs and LLLPs | 182 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Corporation | general grandfathering of pre-April 26, 2017 LLPs and LLLPs | 115 |

| Tax Topics - Income Tax Act - Section 93.2 - Subsection 93.2(2) | Florida and Delaware LLPs and LLLPs subject to s. 93.2 | 23 |

26 May 2016 IFA Roundtable Q. 9, 2016-0642131C6 - Article IV(7) and S-Corporations

US Parent, which has elected to be treated as an “S-corporation,” so that it is fiscally transparent for Code purposes and its shareholders...

2014 Ruling 2014-0534751R3 - Deemed dividends from ULC holdco and Art IV(7)(b)

{kind=link}

Existing structure

U.S. Parent, which is a qualifying person for purposes of the Canada-U.S. Treaty and whose common shares trade on a recognized...

2014 Ruling 2013-0491331R3 - Introduction of a partnership and Art.IV(7)(b)

{kind=link}

Structure

U.S. Parent (an S Corp. with only U.S.-resident shareholders and a qualifying person by reason of Art. XXIX(2)(a) or (e) of the...

16 June 2014 External T.I. 2014-0516451E5 - Application of Canada-Israel Tax Convention

If the "mind and management" of a BC venture capital corporation (which was incorporated in Canada) resided in Israel, resort would be necessary...

12 February 2014 External T.I. 2013-0486931E5 - Distribution by ULC to a Trust to a NR beneficiary

Trust is resident in Canada, is not subject to s.75(2), has one individual beneficiary (the "Non-resident Beneficiary") who is a a qualifying...

11 October 2013 Roundtable, 2013-0492821C6 F - Question 3 - APFF Round Table

How would the Canada-U.S. Tax Convention (the "Convention") tie-breaker rules apply in a double residency case under the Convention and how could...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Other Legislation/Constitution - Federal - Income Tax Conventions Interpretation Act - Section 4.3 | s. 4.3 precludes application of tie-breaker rule | 45 |

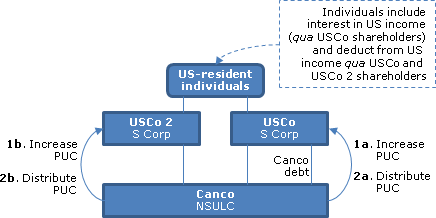

2013 Ruling 2012-0467721R3 - IV(7)(b) & PUC increase

{kind=link}

USCo and USCo2 are each S Corporations whose shares are owned in the same proportions by U.S.-resident and qualifying-person individuals, who are...

2013 Ruling 2012-0471921R3 - Deemed dividend on return of capital

{kind=link}

Canco and U.S. Holdco

Canco, which is an unlimited liability company, is wholly owned by U.S. Holdco, which is resident in the U.S. for purposes...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 29A | base erosion test to be satisfied in current year | 414 |

17 October 2012 External T.I. 2011-0428781E5 - US LLC owned by Canadian residents

USLLC, whose central management and control is in the U.S. and which is owned by two related Canadian residents, owns residential rental...

23 May 2013 IFA Round Table, Q. 10

Are there any new issues with respect to Article IV(6) and (7) of the US treaty?

Response

: Since the 5th Protocol to the Canada-U.S. Treaty, CRA...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 5 | comment on data centre interpretation below | 270 |

S5-F1-C1 - Determining an Individual’s Residence Status

1.41 [T]o be considered liable to tax for the purposes of the Residence article of Canada's tax treaties, an individual must be subject to the...

25 September 2012 B.C. CTF Roundtable Q. 10, 2012-0457591C6 - B.C. CTF 2012 - Q.10 US LLC

As CRA is not in agreement with the decision in TD Securities (which, in any event, involved pre-5th Protocol timeframes). Accordingly:

Treaty...

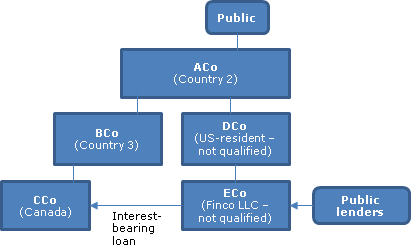

2012 Ruling 2012-0458361R3 - Cross-Border Financing

{kind=link}

ECo, which is fiscally transparent for U.S. purposes and resident in the U.S. (a.k.a., Country 1) but is not a qualifying person (as defined in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 29A | 225 |

2012 Ruling 2011-0430761R3 - Paid-up capital Increase

{kind=link}

Canco1 is a Canadian-resident unlimited liability company which is a wholly-owned subsidiary of Parentco, which is a qualifying person for...

19 April 2012 Internal T.I. 2012-0436221I7 - LLCs and ULCs and Treaty benefits

Where the members of a fiscally transparent LLC are entitled to Treaty benefits in accordance with Art. XXIX-A of the Canada-US Income Tax...

16 February 2012 External T.I. 2011-0430841E5 - U.S. Grantor Trusts

CRA indicated that if s. 94(3) applied to deem a US grantor trust with US-resident settlors to be a resident of Canada, then Art. IV(6) of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 94 - Subsection 94(1) - Arm's Length Transfer | 34 |

2 February 2012 External T.I. 2012-0434311E5 - Canada-U.S. Tax Convention

in the situation where a Canadian unlimited liability company ("ULC"), which is a disregarded entity for US tax purposes, pays an excessive...

2010 Ruling 2010-0364531R3 - Deemed dividends derived by US Residents

Canco1, which is an Canadian unlimited liability company that is owned, in part, by S corps and by a US limited partnership whose partners are...

2010 Ruling 2010-0361591R3 - Article IV(7)(b) Restructuring

Canco, a ULC and fiscally transparent under the Code, is wholly-owned by USCo, which is a C-Corp and a qualified person for purposes of the...

2010 Ruling 2010-0353101R3 - Article IV(7)(b) Restructuring

If a ULC is prohibited from increasing its paid-up capital, it will instead declare and pay a stock dividend of additional common shares having...

26 October 2010 External T.I. 2009-0339951E5 - Canadian Branch Tax

It is the current practice to treat an S Corporation as a resident of the U.S. for purposes of the Canada-U.S. Convention provided that it is a...

19 August 2010 External T.I. 2009-0344111E5 F - Résidence Société Capital-Risque - Conv Can-France

In finding that a French venture capital corporation ("VCC"), that was resident in France for French taxation purposes by virtue of its domicile...

19 May 2010 IFA Roundtable, 2010-0366521C6 - Canada-United States Tax Convention

A Canadian ULC has interest accrue on a loan from its US-resident parent ("USCo"), with the election being made under s. 78(1)(b) of the Act at...

1 June 2009 External T.I. 2009-0319481E5 - Dividends Paid to S Corporation

The Canadian rate of withholding tax on a dividend paid by a Canadian corporation, that is fiscally transparent for U.S. purposes, to an S Corp of...

19 May 2009 External T.I. 2007-0263441E5 - Tax Treaties

A SOPARFI that has a material economic nexus to Luxembourg will be considered to be a resident of Luxembourg for purposes of the Canada-Luxembourg...

13 June 2007 External T.I. 2007-0226261E5 F - Convention Émirats Arabes Unis

Canco incorporated a wholly-owned subsidiary in Dubai, in the United Arab Emirates (Dubai Co), whose management and control, and the sole...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 3 | undefined term in Convention informed by its domestic interpretation by CRA | 36 |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(11.2) - Paragraph 5907(11.2)(a) | FA required to have its central management and control in the Treaty country in addition to satisfying the Treaty residence test | 251 |

Income Tax Technical News, No. 35, 26 February 2007, "Treaty Residence - Residence of Convenience"

2006 Ruling 2004-0106101R3 - Class of German Arrangement & Treaty Benefits

Ruling that a German open-end real estate fund would be treated as a resident of Germany for purposes of Article 4 of the German Treaty.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(1) | German real estate investment fund treated as trust | 90 |

IC75-6R2 "Required Withholding from Amounts Paid to Non-Resident Persons Performing Services in Canada"

Discussion of limited liability corporations in para. 10 of Appendix A.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 102 - Subsection 102(1) | 0 | |

| Tax Topics - Income Tax Regulations - Regulation 105 - Subsection 105(1) | 0 |

6 August 2004 External T.I. 2004-0066621E5 - Irish Investment Undertakings

Three entities (a unit trust, investment company and limited partnership) which were certified by the Irish Revenue Commissioners to be investment...

3 August 2004 External T.I. 2003-005125

A corporation registered as an Undertaking for collective investment in transferable securities in Ireland would not be eligible as a resident of...

29 March 2004 External T.I. 2004-005483

It has been a long-standing position of the CRA that FCPs, SICAVs and SICAFs are not "liable to tax" and so are not residents of Luxembourg for...

24 March 2004 External T.I. 2003-0032781E5 - Treaty benefits for Irish Investment Undertakings

An Irish Investment Undertaking would not be considered to be a resident of Ireland for purposes of the Canada-Ireland Convention given that it...

2003 Ruling 2003-0044063 - Residency, France

Ruling that Mr. X is a resident of France under the Canada-France Tax Convention given that he is liable to tax on worldwide income in France, his...

2 September 1999 External T.I. 9816355 - QUALIFIED SUBCHAPTER S SUBSIDIARY (QSSS)

A qualified subchapter S subsidiary is a resident of the U.S. for purposes of the Canada U.S. Convention, given that the position of the Agency on...

Income Tax Technical News, No. 16, 8 March 1999

Discussion of Crown Forest case.

12 March 1998 External T.I. 9805215 - Barbados trust deemed resident of Canada

Before concluding that Canada had the right to tax a trust that was resident in Barbados and which was deemed to be resident in Canada under s....

10 November 1997 External T.I. 9728445 - U.S. Limited Liability Company - Check-the-Box RULES

A U.S. LLC that elects to be treated as a corporation under the check-the-box rule will be considered a resident of the U.S. given that, as a...

15 August 1997 External T.I. 9711265 - RESIDENCE OF SICAVS

Sociétés d'investissement à capital variable are not considered by RC to be residents of a contracting state as they are not liable to taxation...

17 February 1997 External T.I. 9617535 - BARBADOS ENCLAVE ENTERPRISES

After indicating that the ten-year tax holiday for Barbados Enclave Enterprises does not, by itself, disqualify them from being considered as...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(11.2) | 24 |

18 March 1996 External T.I. 9600675 - treaty residence - barbados insurance companies

A foreign affiliate incorporated in Barbados and licensed under the Exempt Insurance Act, 1983 will not be considered to be "liable to taxation"...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(11.2) | 73 |

22 August 1995 External T.I. 9520405 - TREATY ("RESIDENCE") STATUS OF A "S" CORPORATION

Because an S corporation will be subject to tax in the U.S. on its world-wide income if certain conditions are not met, it is considered to be a...

3 April 1995 External T.I. 9416455 - S CORPS-LLC'S-RES OF A CONTRACTING STATE (HAA 4093 U5-100-4

An S corporation, unlike a limited liability company, is considered to be an entity resident in the U.S. under the Canada-U.S. Income Tax Convention.

25 October 1994 External T.I. 9417505 - LIMITED LIABILITY COMPANY (HAA 4093-U5-100-4)

If any limited liability company is treated as a partnership for purposes of the Internal Revenue Code such that the shareholders rather than the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Corporation | 32 |

27 June 1994 External T.I. 9406005 - CORPORATE STATUS OF A DELAWARE LLC (4093-U5-100-4)

If a Delaware limited liability company is treated as a partnership for purposes of the Internal Revenue Code such that the shareholders rather...

22 March 1994 Internal T.I. 9402046 - CENTRE OF VITAL INTERESTS - XXXXXXXXXX EMPLOYEE (4093- U5-100-4)

Where a taxpayer has not severed his residential ties with Canada, RC must analyze the personal and economic ties over a period of time in order...

93 C.M.TC - Q. 4

The continuance of a corporation incorporated in Canada to the United States will not result in that corporation ceasing to be considered to have...

17 May 1993 T.I. (Tax Window, No. 31, p. 4, ¶2510)

Tax-exempt entities are resident in the jurisdiction in which they are organized.

8 August 1991 T.I. (Tax Window, No. 7, p. 23, ¶1389)

The Canada-U.S. Convention is not intended to benefit individuals, wherever resident, who were subject to tax in the U.S. only by virtue of being...

14 December 1990 T.I. (Tax Window, Prelim. No. 2, p. 4, ¶1047)

In the case of a corporation incorporated in Canada and having its place of effective management in The Netherlands, Canada will not agree that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 250 - Subsection 250(4) | 68 |

Articles

Nakul Kohli, Jiani Qian, "Canadian Residents Earning Income Through Non-Resident US LLCs", Canadian Tax Focus, Vol. 12, No. 1, February 2022, p. 10

Non-application of US Treaty reduction where Canadians receive dividends from a Canco through an LLC (p. 10)

- An LLC with US and Canadian...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) | 149 |

Julie Colden, Éric Lévesque, "An In-Depth Look at the Hybrid Rules in the Fifth Protocol", 2017 Annual CTF Conference

Non-application of IV(6) to non-U.S. LLC shareholders (p. 7)

While Article IV(6) may effectively confer Treaty benefits in respect of U.S....

Brian Kearl, Carl Deeprose, "Leaving Canada's New High Tax Rate Regime: Considerations, Tips and Traps", 2016 Conference Report (Canadian Tax Foundation),32:1-24

Test of a permanent home available (p. 32:9)

In Salt, … [t]he appellant successfully argued that the tie-breaker rules deemed him to be resident...

Kevyn Nightingale, Amir Pourzakikhani, "A Federal Permanent Establishment, But Not a Provincial One", Tax Topics, Wolters Kluwer, November 3, 2016, No. 2330, p. 1

CRA recently agreed with the position of a U.S.-resident individual who had a services permanent establishment in Canada under the Canada-U.S....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 120 - Subsection 120(1) | 427 |

Corrado Cardarelli, Peter Keenan, "Planning Around the Anti-Hybrid Rules in the Canada-US Tax Treaty", 2013 Conference Report (Canadian Tax Foundation), pp.16:1-27

IV(6)(a) and (b) not satisfied where sole shareholder of ULC is LLC (p.16:6)

Following the approval by the CRA of the two-step process, the...

Jack Bernstein, "Canada-US Tax Traps for LLCs", Canadian Tax Highlights, Volume 22, Number 2, February 2014, p. 11

Relief under U.S. Treaty, Art. IV(6) for US residents only (p.11)

Article IV(6) provides relief from Canadian withholding tax for US residents...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 126 - Subsection 126(1) | 149 | |

| Tax Topics - Treaties - Income Tax Conventions - Article 10 | 120 |

Carl Irvine, Todd Miller, "Canadian Branch Profits Tax - Challenging the Denial of Treaty-Benefits for US LLCs", Newsletter - TerraLex Connections, 26 December 2013

CRA view that Art. X(6) of Canada-U.S. Treaty provides that there only is reduced branch tax for LLC income derived by U.S.-resident members

Edward Tanenbaum, "Where's Your Center of Vital Interests?: Treaty Tie-Breakers", Tax Management International Journal, Vol. 42, No. 5, May 10, 2013, p. 293

Edward Tanenbaum noted that in Podd v. Comr., 2: T.C. Memo 1998-238, aff'd, T.C. Memo 1998-418, the Tax Court initially determined that a...

Jack Bernstein, "Fiscally Transparent Entities and the Canada-US Treaty", Canadian Tax Highlights, Vol. 20, No. 1, January 2012

The rules in Articles IV(6) and (7) of the Canada-US Convention might be summarized by stating that if the taxpayer and the fiscally transparent...

Brian Cleave, "The Treaty Residence of Trusts in the United Kingdom and Canada: Some Thoughts on the Smallwood and Garron (or St Michael Corp) Cases", British Tax Review, 2011, No. 6. p. 705.

Kristen A. Parillo, "Canada Will Litigate U.S. LLC Questions under Fifth Protocol", Tax Notes Internationals, 4 October 2010, p. 7.

Richard Lewin, "Oh What a Tangled Web ..", International Tax, August 2010, No. 53, p. 10.

Discussion of Article IV(7)(b) of the Canada-U.S. Income Tax Convention.

Brad Gordica, Sara McCracken, "Canada-US Protocol: Top Five Issues fro Cross-Border Businesses", 2009 BC Conference Report

Kevin Duxbury, "Canadian-Owned US LLCs More Costly After the Fifth Protocol", Tax for the Owner-Manager, Vol. 9, No. 4, October 2009, p. 8.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 91 - Subsection 91(1) | 0 |

Paul K. Tanaki, amp; Sarah Davidson Ladly:, "Payments by Hybrid Entities under the Revised Canada-United States Income Tax Convention", Corporate Finance, Vol. XV, No. 4, 2009 p. 1710.

Heather O'Hagan, "Canada-U.S. Tax Treaty Protocol - United States Kicks Off Ratification Process", CCH International Tax, No. 41, p. 1, August 2008

Peter A. Glicklich, Abraham Leitner, "New Canada-US Protocol Contains Certain Hybrid Entity Surprises", Selected US Tax Developments, 2007 Canadian Tax Journal, NO. 4

Richard Lewin, "A Change in Protocol: The Fifth Protocol to the Canada-U.S. Income Tax Convention", International Tax, CCH, October 2007, No. 36.

John Avery Jones, "Place of Effective Management as a Residence Tie-Breaker", International Bureau of Fiscal Documentation Bulletin, January 2005, p. 20.

R. Ian Crosbie, "Recent Development affecting Residence under Canada's Income Tax Conventions", Corporate Finance, Vol. VII, No. 2, 1999, p. 606.

D. Ward, "A Resident of a Contracting State for Tax Treaty Purposes: A Case Comment on Crown Forest Industries", 1996 Canadian Tax Journal, Vol. 44, No. 2, p. 408.

Steiss, "Issues Relating to Tax Freeze", 1993 Conference Report, c. 45

Discussion (at pp. 45:14-23) of issues respecting the treatment of partnerships.