Cases

626468 New Brunswick Inc. v. Canada, 2019 FCA 306

An individual rolled his apartment building into a Newco in consideration for a mortgage assumption and shares with nominal paid-up capital, and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(c) | safe income from asset sale was reduced by accrued, but not yet payable, taxes on the gain | 361 |

| Tax Topics - General Concepts - Fair Market Value - Shares | FMV of shares reduced by accrued, but not yet payable, corporate income tax on gains | 263 |

Ottawa Air Cargo Centre Ltd. v. The Queen, 2007 DTC 661, 2007 TCC 193, aff'd 2008 DTC 6177, 2008 FCA 54

Lamarre J. rejected the taxpayer's submission that deemed dividends received by the taxpayer were "subject to" Part IV tax in the sense that the...

Canada v. VIH Logging Ltd., 2005 DTC 5095, 2005 FCA 36

Cash dividends paid by a corporation ("Old VIH") to its parent (the taxpayer) in February 1993 came out of safe income of Old VIH given that the...

Canada v. Canadian Utilities Ltd., 2004 DTC 6475, 2004 FCA 234

The two taxpayers, which were subject corporations, indirectly sold their investment in another public corporation ("ATCOR"). This was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | a transaction with an independent purpose and existence nonetheless can form part of a common law series | 244 |

Lamont Management Ltd. v. The Queen, 2000 DTC 6256 (FCA)

Safe income attributable to shares of a Canadian corporation ("Canpac") that were purchased for cancellation in the hands of the taxpayer included...

Brelco Drilling Ltd. v. R., 99 DTC 5253, [1999] 3 CTC 95 (FCA)

The U.S. subsidiary of the taxpayer, in turn, owned seven U.S. resident corporations five of whom had exempt deficits and two of whom had exempt...

Her Majesty the Queen, Appellant v. Nassau Walnut Investments Inc., Respondent, 97 DTC 5051, [1998] 1 CTC 33 (FCA)

Although it had been planned that the portion of deemed dividends received by the taxpayer (arising on the redemption of shares held by it) that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(5) - Paragraph 55(5)(f) | late s. 55(5)(f) designation available | 162 |

| Tax Topics - Statutory Interpretation - Expressio Unius est Exclusio Alterius | express limited relief does not imply no other relief | 74 |

| Tax Topics - Income Tax Act - Section 165 - Subsection 165(1) | taxpayer can amend return on objection in respects relevant to issues surrounding the reassessment | 112 |

The Queen v. Placer Dome Inc., [1997] 1 CTC 72, 96 DTC 6562 (FCA)

After the taxpayer solicited competing bids for the sale of a significant block of shares it held in another public company ("Falconbridge") both...

CPL Holdings Ltd. v. The Queen, 95 DTC 5253, [1995] 1 CTC 447 (FCTD)

The two individual shareholders (Lamothe as to 99% and his wife as to 1%) of a corporation operating a machine shop ("Clem Industrial")...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Onus | 63 |

See Also

D & D Livestock Ltd. v. The Queen, 2013 DTC 1251 [at at 1412], 2013 TCC 318

{kind=link}

After a preliminary reorganization, all of the shares of the taxpayer (consisting of Class A common shares and Class D preference shares) were...

729658 Alberta Ltd. v. The Queen, 2004 DTC 2909, 2004 TCC 474

Each of the two individual taxpayers, who owned one-half of the shares of a Canadian-controlled private corporation ("Comcare") having an accrued...

Kruco Inc. v. The Queen, 2001 DTC 668 (TCC), aff'd 2003 FCA 284

The safe income of a corporation ("Kruger") from which the taxpayer received a deemed dividend did not exclude income resulting from investment...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(1) | 81 | |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | safe income | 211 |

| Tax Topics - Statutory Interpretation - Interpretation Bulletins, etc. | 81 |

Granite Bay Charters Ltd. v. The Queen, 2001 DTC 615 (TCC)

After the individual shareholders ("Cox") of the taxpayer and a related corporation ("Greenstone") had entered into an agreement for the sale of...

Lamont Management Ltd. v. R., 99 DTC 871, [1999] 3 CTC 2576 (TCC)

In light of the specific code provided in s. 55(5), it was found that the safe income attributable to shares redeemed in the hands of the taxpayer...

943963 Ontario Inc. v. R., 99 DTC 802, [1999] 4 CTC 2119 (TCC)

The taxpayer (a Canadian-controlled private corporation) received $1.2 million upon the purchase for cancellation of shares, having a paid-up...

Meager Creek Holdings Ltd. v. The Queen, 98 DTC 2073, [1998] 4 CTC 2090 (TCC)

Two Canadian corporations owned by the taxpayer paid significant dividends to the taxpayer shortly before the February 1990 federal Budget on the...

Brelco Drilling Ltd. v. R., 98 DTC 1422, [1998] 3 CTC 2208 (TCC), rev'd 99 DTC 5253 (FCA)

The taxpayer, in computing the safe income attributable to its shares of another corporation ("Tricil") was not required to deduct the exempt...

Les Placements E&R Simard Inc. v. The Queen, 97 DTC 1328 (TCC)

On September 10, 1988, the taxpayer transferred its assets to a subsidiary ("Alimentation 1988") in consideration for a demand promissory note and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | 152 | |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Safe-Income Determination Time | subsequent redemption of preferred shares was not assimilated to the series in which they were issued one or more year previously, given different objectives for each and lack of interdependence | 175 |

Deuce Holdings Ltd. v. R., 97 DTC 921, [1998] 1 CTC 2550 (TCC)

Bell TCJ. found that the safe income of the corporation in question should be computed on an after-tax basis, but should not be reduced by a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(b) | 69 |

Gestion Jean-Paul Champagne Inc. v. MNR, 97 DTC 155, [1996] 2 CTC 2537 (TCC)

In connection with a buy-out of an individual's interest in a corporation ("Champagne") by his brother, the individual and his wife transferred...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(5) - Paragraph 55(5)(f) | 44 |

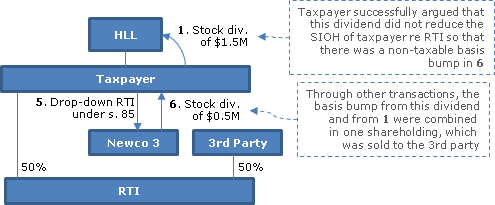

454538 Ontario Ltd. v. MNR, 93 DTC 427, [1993] 1 CTC 2746 (TCC)

Two brothers (the "Mazzoccas"), who constituted two of the three equal shareholders of a corporation ("Tri-M"), transferred their shares of Tri-M...

Administrative Policy

7 October 2021 APFF Roundtable Q. 9, 2021-0901101C6 F - Part IV tax exception vs eligible and non-eligible

Suppose that Holdco has eligible refundable dividend tax on hand (“ERDTOH”) and non-eligible refundable dividend tax on hand (“NERDTOH”)...

7 October 2021 APFF Roundtable Q. 5, 2021-0900951C6 F - Safe income and Part IV tax

9711005 indicated, before the bifurcation of RDTOH into the eligible refundable dividend tax on hand (“ERDTOH”) and non-eligible refundable...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(c) | full use can be made of safe income even though there is an immediately subsequent use of Pt. IV tax exclusion | 224 |

18 December 2017 External T.I. 2017-0714971E5 F - Application of subsection 55(2)

Example 1, Scenario 1 is summarized as follows:

Opco, which had refundable dividend tax on hand ("RDTOH") of $383,333 and no safe income paid a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(1) - Paragraph 186(1)(b) | s. 55(2) application does not reduce s. 186(1)(b) initially reported Pt IV tax | 297 |

21 November 2017 CTF Roundtable Q. 6, 2017-0724071C6 - Circular calculations Part IV tax

Holdco receives a dividend of $400,000 that is subject to Part IV tax of $153,333 (38.33% of $400,000) equalling the connected payer’s dividend...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(1) - Paragraph 186(1)(b) | refunded Pt IV tax payable not reduced by application of s. 55(2) | 181 |

29 November 2016 CTF Roundtable Q. 4, 2016-0671491C6 - 55(2) and Part IV Tax

A dividend is received by Holdco from an Opco, which under the new s. 55(2) rules is no longer exempted from s. 55(2) even though the Part IV tax...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Capital Dividend Account - Paragraph (a) | s. 55(2) application to dividend as a result of a Pt IV tax refund does not generate CDA for on-payment of that dividend | 283 |

9 October 2015 APFF Roundtable Q. 15, 2015-0595641C6 F - Surplus Stripping and GAAR

Less overall tax is paid if, rather than Opco paying a taxable dividend to one of its shareholders (A, an individual), A rolls his shares into a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | GAAR did not apply where a taxpayer deliberately triggered the application of s. 55(2) | 133 |

9 October 2015 APFF Roundtable Q. 12, 2015-0595601C6 F - Proposed legislation - subsection 55(2)

Holdco holds shares of Opco with a nominal ACB and no safe income. In a corporate reorganization "aimed at protecting the assets of Opco, whose...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(b) | transaction targeted at reducing FMV of Opco shares for creditor-proofing was caught | 249 |

27 June 2014 External T.I. 2013-0498191E5 F - Interaction entre 55(2) et l'impôt de partie IV

On a cross-share redemption between two connected Canadian-controlled private corporations, neither of which has a refundable dividend tax on hand...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(1) - Paragraph 186(1)(b) | Part IV tax on cross-redemptions takes into account the Part I tax (and RDTOH addition) generated by s. 55(2) application thereto | 352 |

7 October 2013 Internal T.I. 2013-0504081I7 F - Interaction between 55(2) and 40(1)(a)(iii)

Vendor sold blocks of shares in the capital of a corporation (the “Purchaser”) to the Purchaser, with the purchase price being payable over a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(1) - Paragraph 40(1)(a) - Subparagraph 40(1)(a)(iii) | reserve available for s. 55(2) gain on purchase for cancellation of shares where redemption proceeds payable on an earnout basis | 268 |

| Tax Topics - General Concepts - Payment & Receipt | distinction between promissory note as conditional or absolute payment | 249 |

2012 Ruling 2011-0403291R3 - Treaty exempt sale

{kind=link}

Following a preliminary reorganization (including an amalgamation of predecessors of Amalco so as to "consolidate the tax attributes"), all the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | partnership distribution to one of partners not disposition of the partnership interests | 74 |

| Tax Topics - Treaties - Income Tax Conventions - Article 13 | Treaty step-up to avoid the application of s. 55(2) to a spin-off made to effect an arm's length sale of the rump | 337 |

14 March 2014 Internal T.I. 2013-0499141I7 - IRC 338(h)(10), "earnings" and safe income

An indirect wholly-owned foreign affiliate ("FA") of Canco made an arm's length purchase of all the shares of "US Holdco," whose wholly-owned...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Earnings | "notional" deduction arising from Code s. 338(h)(10) step-up excluded | 137 |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Exempt Earnings | no carve out for goodwill gains | 142 |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(2) - Paragraph 5907(2)(f) | "notional" deduction arising from Code s. 338(h)(10) step-up of non-purchased goodwill reversed under Reg. 5907(2)(f) rather than (b) | 453 |

21 March 2014 External T.I. 2012-0471021E5 - Safe income and section 34.2

The fiscal period of a partnership ends on June 30, 2013 but the taxation year-end of the private corporation which is a member is December 31,...

16 April 2009 External T.I. 2008-0294631E5 F - Interaction between 55(2) and 186(1)

An individual wholly-owned Holdco, which held all of the preferred shares of Opco (also, with a calendar year end), whereas Opco’s common shares...

Income Tax Technical News, No. 34, 27 April 2006 under "Delaware Revised Uniform Partnership Act"

The Kruco case.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 96 | Delaware LPs with separate personality are not corps | 21 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | 160 | |

| Tax Topics - Income Tax Act - Section 132 - Subsection 132(6) | majority of subsidiary board not to be MFT trustees/guarantees re non-wholly owned subs scrutinized | 105 |

| Tax Topics - General Concepts - Transitional Provisions and Policies | 0 | |

| Tax Topics - Treaties - Income Tax Conventions - Article 5 | 17 | |

| Tax Topics - Income Tax Act - Section 132 - Subsection 132(6) - Paragraph 132(6)(b) - Subparagraph 132(6)(b)(i) | guarantee must be highly integrated with trust’s core investment undertaking/limited overlap with subsidiaries' boards | 434 |

3 June 2003 External T.I. 2003-0012075 F - Safe Income and 104(13.1) Designation

An amount designated by a personal trust in respect of its corporate beneficiary under s. 104(13.1) would not be included in determining the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(c) | income retained by a trust under s. 104(13.1) and then distributed to its corporate beneficiary was not included in the latter’s safe income | 166 |

14 December 2000 Internal T.I. 2000-0034037 - safe income

The safe income on hand of a corporation, is not reduced by non-capital losses of a corporation within the group that is acquired by it, although...

2000 Ruling 2000-0003253 - Safe income

Where a share is exchanged for a second share on a rollover basis, the full safe income on hand attributable to the first share owned by the...

Income Tax Technical News, No. 16, 8 March 1999

Reference to Brelco case.

1999 Ruling 9910443 - SAFE-INCOME DETERMINATION TIME

The safe income attributable to shares of a corporation that were sold to an arm's length purchaser included gain arising from an s. 111(4)(e)...

1999 APFF Round Table, Q. 4 (No. 9M19190)

A loss that is denied under s. 40(2)(g)(ii) will be deducted when calculating safe income on hand.

17 September 1997 External T.I. 9721415 - INTERACTION OF SUBSECTION 55(2) & DIVIDEND REFUNDS

The fact that a dividend refund has been received by the payor of a dividend is not normally relevant to consideration of the following...

29 August 1997

Confirmation of policy expressed in the Read paper (1988 Conference Report) respecting the redemption of preferred shares which were received as a...

26 August 1997 External T.I. 9713655 - SAFE INCOME - INCESTUOUS SHAREHOLDINGS

Where a wholly-owned subsidiary owns shares in the capital of its parent company, an allocation of safe income must be made to the shares of the...

16 June 1997 External T.I. 9711005 - SAFE INCOME/PART IV TAX

Any dividend paid by a payer corporation is considered to be paid first out of the safe income on hand attributable to the recipient corporation's...

17 March 1997 External T.I. 9632725 - SAFE INCOME ENTITLMENTS OF ALPHABET SHARES

Discussion of the safe income entitlement of alphabet shares.

16 July 1996 External T.I. 9604915 - 55(2)-NOT APPLY WHERE SALE & REDMPTION DIFFERENT SERIES.

Where preferred shares issued by Newco on the roll-in to Newco of shares of Opco, have a dividend entitlement equal to dividends received by Newco...

6 May 1996 External T.I. 9611245 - SAFE INCOME-PROVISION FOR CAPITAL ITEM, DIVIDENDS

A write- down in the carrying value of a capital asset to reflect an accrued loss inherent in the property, will not reduce safe income on hand...

Income Tax Technical News, No. 7, 21 February 1996 (cancelled)

After referring to the Clem Industrial case, Mr. Hiltz stated:

"Ordinarily, if an arm's length sale of shares occurs within a short time after a...

1996 Ontario Tax Conference Round Table, "Purpose Test in Subsection 55(2)", 1997 Canadian Tax Journal, Vol. 45, No. 1, pp. 231-214

Discussion of CPL Holdings Ltd. v. The Queen, 95 DTC 5253 (FCTD).

5 July 1995 External T.I. 9416065 - CALCULATION OF SAFE INCOME

Discussion of a situation where a Canadian-controlled private corporation ("Holdco") transfers an asset on a rollover basis to a...

28 March 1995 External T.I. 9430955 - SAFE INCOME STOCK SPLITS

"Generally, when a portion of the capital gain inherent in the shares of a corporation is crystallized, the Department's approach ... is to...

27 October 1994 External T.I. 9414365 - SAFE INCOME - FOREIGN AFFILIATES (HAA 5102-3)

When computing exempt or taxable surplus of a foreign affiliate for the purpose of determining safe income of a Canadian corporation with a wholly...

94 CPTJ - Q. 1

Because the Alberta royalty tax credit is not included in a corporation's net income for tax purposes, it would not be included in determining the...

3 May 1993 External T.I. 9236395 F - Safe Income and Part IV Tax

Where X owns 20% of the shares of Opco having a safe income of $100 and a fair market value of $125, and transfers all of such shares to a new...

20 July 1994 External T.I. 9408795 - 55(2)

The rollover under s. 107(2) is accorded the same treatment for safe income purposes as the rollover under s. 85.

On a wind-up of one company into...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(c) | flow-through of safe income on s. 107(2) rollover | 23 |

6 April 1994 External T.I. 9331715 - SAFE INCOME AND SRED EXPENDITURES

Current SR & ED expenses must be deducted in computing the corporation's safe income on hand even if such expenses have not yet been deducted for...

93 C.R. - Q. 15

Safe income on hand will be reduced by large corporations tax.

93 C.R. - Q. 12

Discussion of distinction between "safe income" and "safe income on hand".

3 May 1994 Roundtable Q. 1, 9411620 - SAFE INCOME & ALBERTA ROYALTY TAX CREDITS

Because an Alberta royalty tax credit is not included in a corporation's income for tax purposes, it also is not included in its safe income or...

31 August 1993 Memorandum (Tax Window, No. 33, p. 4, ¶2639)

Impact of investment tax credits and share purchase tax credits on calculation of safe income.

2 February 1993 T.I. (Tax Window, No. 28, p. 5, ¶2414)

Amounts actually expended but not deductible for tax purposes (e.g., 20% of entertainment expenses), and amounts actually expended but deferred or...

20 October 1992 T.I. 910248 (September 1993 Access Letter, p. 413, ¶C38-174)

The deduction under s. 110(1)(k) has no effect on safe income.

92 C.R. - Q.35

RC response to suggestion that s. 55(2) does not apply to a taxable dividend arising out of transactions that were structured by the corporation...

92 C.R. - Q.29

Where a deemed dividend arising on the redemption of a portion of the shares of Opco exceeds the safe income attributable to the redeemed shares...

28 July 1992 External T.I. 5-920803

Where A and B, who are two of the three individual shareholders of OPCO, transfer their common shares of OPCO to separate newly-incorporated...

10 January 1992 Memorandum (Tax Window, No. 17, p. 12, ¶1773)

The reduction in Part I tax caused by the application of available investment tax credits affects the corporation's safe income only in the years...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2) | 19 | |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) | 70 |

10 January 1992 Memorandum (Tax Window, No. 17, p. 12, ¶1773)

The corporation to which assets are transferred in a butterfly may not be amalgamated with another corporation.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2) | 48 | |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) | 70 |

24 February 1992 Memorandum (Tax Window, No. 13, p. 13, ¶1630)

Re circumstances where RC is prepared to consider a reassessment of only the excess of deemed proceeds over safe income notwithstanding the...

23 January 1992 T.I. (Tax Window, No. 12, p. 6, ¶1574)

Where a corporation pays a dividend in kind comprising part of its assets, its safe income must be pro-rated rather than being allocated fully to...

6 June 1991 T.I. (Tax Window, No. 4, p. 12, ¶1282)

Where shares of Opco are redeemed by Holdco giving rise to a deemed dividend of $2.2 million at a time that the safe income of Opco is $1.8...

15 May 1991 T.I. (Tax Window, No. 3, p. 18, ¶1239)

S.55(2) generally will not apply to a deemed dividend which deliberately has been made subject to Part IV tax in order to avoid the application of...

13 March 1991 T.I. (Tax Window, No. 1, p. 20, ¶1140)

Crown royalties and other amounts representing cash outlays which are non-deductible under s. 18(1)(m) should be included in computing safe...

26 November 1990 T.I. (Tax Window, Prelim. No. 2, p. 7, ¶1037)

Safe income effectively is transferred on an s. 85 rollover or an interspousal rollover under s. 73(1).

90 C.P.T.J. - Q.20

A corporation with safe income of $100 has one shareholder whose shares, all being of one class, have an accrued gain of $200. If the redemption...

29 June 1990 T.I. (November 1990 Access Letter, ¶1516)

Where the individual shareholders of Opco transfer their common shares of Opco to Holdco on a share-for-share exchange, the common shares held by...

June 1990 Meeting of Alberta Institute of Chartered Accountants (November 1990 Access Letter, ¶1499, Q. 7)

Safe income is attributable to a particular class of shares in the same proportion in which each class of shares will be entitled to earnings of...

30 April 1990 T.I. (September 1990 Access Letter, ¶1415)

Employees of Opco, who own all its issued shares, transfer those shares to Newco in exchange for shares of Newco, thereby realizing a capital...

23 March 1990 T.I. (August 1990 Access Letter, ¶1376)

In response to a proposal that entailed purifying a corporation for purposes of the exemption for sales of qualified small business corporation...

23 February 1990 T.I. (July 1990 Access Letter, ¶1322)

If it is known, at the beginning of a series of transactions, that there will be an acquisition of control of the corporation resulting in a...

12 January 1990 External T.I. 59210 - Avoidance of Tax on Capital Gains - Intercorporate Dividends Deemed to be Capital Gain

A sale of an operating division by Opco followed by the payment of a dividend to Holdco equal to the net after tax proceeds of the sale likely...

10 January 1990 T.I. (June 1990 Access Letter, ¶1259)

Where Opco pays a stock dividend of $500,000 in high-low preferred shares, only a pro-rata portion of its safe income is attributable to the...

5 December 1989 T.I. (May 1990 Access Letter, ¶1216)

One corporation ("S1") transfers a capital property under s. 85(1) to a sister corporation ("S2") in consideration for redeemable preference...

15 November 89 T.I. (April 90 Access Letter, ¶1187)

A corporation ("Opco") is owned by siblings who wish to transfer their shares to their children. Each sibling would form a holding company into...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 100 |

89 C.R. - Q.12

The shares of Opco whose value essentially is represented by goodwill, are converted (or "frozen") into high-low preferred shares, which then are...

October 1989 Revenue Canada Round Table - Q.5 (Jan. 90 Access Letter, ¶1075)

Mr. A is not permitted to extract the safe income of a corporation prior to the sale of its shares, by having that corporation pay a stock...

88 C.R. - F.Q.36

S.55(2) will apply if as part of the same series Opco transferred assets to Sisterco, for preference shares which were redeemed, and the shares of...

80 C.R. - Q.4

General guidelines.

Articles

Joint Committee, "Subsection 55(2) Amendments – Follow-Up to Our Meeting with Canada Revenue Agency", 19 January 2018 Joint Committee Submission to Finance respecting s. 2015 s. 55(2) Amendments including appended 20 April 2017 letter to Randy Hewlett on such Amendments

Submission to CRA on s. 55(2.1)(b) purpose test, s. 55(2)(c), s. 55(2.1)(c), s. 55(2) Pt IV exception

The April 20, 2017 letter to the Income Tax...

Doron Barkai, Alexander Demner, "Dealing with New Subsection 55(2): Issues and Strategies", 2016 Conference Report (Canadian Tax Foundation), 6:1–56

Targeted mischief of scaling back Pt IV tax refund (p. 6:10)

[T]he part IV tax exception no longer applies when, as part of a series of...

Bruce Ball, Ken Griffin, Rick McLean, Eric Xiao, "Subsection 55(2) material and Part IV", Submission of the Joint Committee, 13 October 2016

This letter attaches examples which the Committee had informally provided to Finance earlier in 2016. They illustrated concerns that the changes...

Bruce Sinclair, "Current Topics in the Taxation of Real Estate Development", 2014 Conference Report, (Canadian Tax Foundation), 12:1-24.

Sale of Projectco before allocation to it by sub LP of condo sale profits (pp. 12:2-3)

Developers often undertake projects in a single-purpose...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | 913 | |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(a) - Subparagraph 95(2)(a)(i) | 203 |

K. A. Siobhan Monaghan, Taxation of Corporate Reorganizations, Chapter 8: Capital Gains Strips and Divisive Reorganizations," (2010, Carswell).

Rick McLean, Understanding Section 55 and Butterfly Reorganizations, 3rd Ed. (2010, CCH).

Matt MacInnis, "Pandora's Box Reopened", CA Magazine, September 2008, p. 48.

Steve Suarez, Firoz Ahmed, "Public Company Non-Butterfly Spinouts", 2003 Conference Report, c. 32.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110 - Subsection 110(1.8) | 0 | |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | 0 |

F. Ahmed, "Allocation of Safe Income to Minority Shareholders", Canadian Current Tax, Vol. 9, No. 3, p. 24.

D. Ewens, "Planning for Safe Income Distribution", Corporate Structures and Groups, Vol. IV, No. 4, 1997, p. 228

Care must be taken when planning for providing a s. 88(1)(d) bump to a purchaser to ensure that safe income distributions are not counter productive.

"Subsection 55(2): Part 1", 1997 Canadian Tax Journal, Vol. 45, No. 2, p. 343.

Hiltz, "Income Earned or Realized: Some Reflections", 1991 Conference Report, c. 15.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 127 - Subsection 127(5) | 0 |

Richter, "The Removal of Accrued Gains and Capital Stockholdings through the Use of 'Safe Income'", 1991 Canadian Tax Journal, p. 1349.

Paragraph 55(2)(a)

Administrative Policy

9 June 2000 External T.I. 1999-0010015 F - Interaction entre 55(2) et 186(1)

A purported distributing corporation (Opco), which was owned by two brothers, effected a spinoff of a portion of its capital properties to a Newco...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(1) - Paragraph 186(1)(b) | s. 55(2)(a) application to failed butterfly precluded application of Pt. IV tax | 192 |

Paragraph 55(2)(b)

Administrative Policy

3 December 2024 CTF Roundtable Q. 8, 2024-1038201C6 - Application of paragraph 55(2)(b)

Canco B repurchased its shares held by its parent, Canco A (which have an ACB and PUC of $100) for $1,000, thereby producing a deemed dividend of...

9 March 2016 External T.I. 2016-0630281E5 F - Redemption of shares and changes to 55(2)

Does the designation by the corporate recipient of part of a dividend as a separate taxable dividend in respect of the portion of the dividend...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(c) | exemption of s. 84(3) deemed dividend not exceeding safe income | 152 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(5) - Paragraph 55(5)(f) | s. 55(2) application to separate dividend | 113 |

Paragraph 55(2)(c)

Administrative Policy

7 October 2011 APFF Roundtable Q. 29, 2011-0412131C6 F - Subsection 55(2) and Capital Dividend Account

If in the year prior to the sale of Opco by Holdco, Opco pays a dividend to Holdco which is subject to s. 55(2), s. 55(2)(b) generally would apply...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Capital Dividend Account - Paragraph (a) - Subparagraph (a)(i) - Clause (a)(i)(A) | CDA addition from application of s. 55(2)(c) is only available in the following years | 99 |

21 November 2017 CTF Roundtable Q. 4, 2017-0724051C6 - Timing of deemed gain under 55(2)

Where s. 55(2) applies to a dividend that is not received on a redemption, acquisition or cancellation of a share to which s. 84(2) or (3)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Capital Dividend Account - Paragraph (a) | an immediate CDA addition for a non-redemption dividend subject to s. 55(2) | 104 |

31 August 2011 External T.I. 2011-0415891E5 F - Increase in stated capital, stock dividends -55(2)

CRA will construe paragraph 55(2)(c) so that the amount deemed not to be a dividend is not taxed as a capital gain twice. Paragraph 55(2)(c) will...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | s. 248(28)(a) applied to reduce capital gain on disposition of preferred shares on which a capital gain had been realized under s. 55(2)(b) | 164 |