Subsection 40(1) - General rules

Cases

Abrametz v. Canada, 2009 DTC 5828, 2009 FCA 111

The taxpayer would have established that he realized a capital loss if he had established the following:

- a fellow shareholder ("Paulhus") of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(12) | 89 |

See Also

Cineplex Inc. v. The King, 2026 TCC 15

A Canadian company with a loss-generating movie-theatre business (“Ventures”) was required to discontinue two of its theaters as a condition...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Start-Up and Close-Down Expenditures | a payment to an affiliate to assume lease obligations, so as to permit a share sale of the payer, was currently deductible | 357 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Start-Up and Liquidation Costs | business termination payment characterized as a commutation of future lease payments was currently deductible | 199 |

Administrative Policy

Calculating and reporting your capital gains and losses

Use the exchange rate that was in effect on the day of the transaction or, if there were transactions at various times throughout the year, you...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(2) | 51 |

Paragraph 40(1)(a)

Administrative Policy

28 April 2008 External T.I. 2007-0243711E5 F - Gains et pertes sur change

Regarding a requested clarification of the second part of paragraph 13 of IT-95R regarding the realization of a foreign exchange gain or loss on...

9 September 1999 Internal T.I. 9902717 F - DÉDUCTIBILITÉ D'UN REMBOURSEMENT DE DETTE

A taxpayer who was required to pay on a mortgage which had been assumed by the purchaser of a property but who subsequently defaulted could not...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(2) - Paragraph 40(2)(g) - Subparagraph 40(2)(g)(ii) | claims against co-owners for their failure to pay their share on defaulted assumed mortgage were not acquired for an income-producing purpose | 163 |

Subparagraph 40(1)(a)(i)

Cases

Martin v. Canada, 2015 FCA 204

The taxpayer's employment at his brokerage employer was terminated. He was unable to find replacement employment or to establish his own financial...

Gaynor v. The Queen, 91 DTC 5288, [1991] 1 CTC 470 (FCA)

In rejecting a submission that the capital gain realized by the taxpayer from the purchase and sale in U.S. dollars of U.S. securities should be...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Amount | 62 |

The Queen v. Demers, 86 DTC 6411, [1986] 2 CTC 321 (FCA)

Although the price stipulated in the agreement for the sale of shares of a corporation ("Chibougamau") was $7,800,000, the agreement also provided...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Proceeds of Disposition | 130 |

See Also

Graphic Packaging Canada Corporation v. The Queen, 2001 DTC 861, [2001] 4 C.T.C. 2399, aff'd 2002 FCA 483

It was found that the taxpayer had acquired shares of a U.S. corporation ("GGM") on the basis of an undertaking that it would make payments to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Superficial Loss | 93 |

Giguère v. Agence du revenu du Québec, 2018 QCCQ 874

The taxpayer received fraudulent advances from a corporation (Groupe Norbourg) managed by her husband. She used the money to purchase a property...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) - Subparagraph 20(1)(c)(i) | fraudulent advance did not qualify as a loan | 202 |

Rio Tinto Alcan Inc. v. The Queen, 2016 TCC 172, aff'd 2018 FCA 124

The taxpayer ("Alcan"), a Canadian public company, incurred fees on capital account respecting its butterfly spin-off of a subsidiary holding a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Legal and other Professional Fees | investment dealer fees incurred respecting the advisability of making hostile takeover were fully deductible under s. 9 | 417 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(bb) | investment dealer fees re advisability of making hostile takeover were fully deductible | 529 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(cc) | legal fees incurred in securing regulatory approval for a hostile bid related to the bidder's business of earning income from shares and interaffiliate sales | 182 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(g) | takeover bid circular costs did not qualify | 102 |

| Tax Topics - Income Tax Act - Section 14 - Subsection 14(5) - Eligible Capital Expenditure | fees incurred in order to acquire shares were excluded/butterfly expenses excluded as taxpayer was not in the business of implementing corporate reorganizations | 365 |

| Tax Topics - Income Tax Act - Section 169 - Subsection 169(2.1) | raising general question of deductibility of fees and listing s. 20(1)(e) did not satisfy s. 165(1.11) | 246 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(e) | failure to advance evidence showing allocation of fees to share consideration | 139 |

| Tax Topics - Statutory Interpretation - French and English Version | finding common meaning of 2 versions of s. 20(1)(bb) | 108 |

Brosamler Estate v. The Queen, 2012 DTC 1193 [at at 3493], 2012 TCC 204 (Informal Procedure)

he estate of a deceased German resident sold three rental properties in BC. The estate added probate and legal fees that were paid in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Adjusted Cost Base | probate fees added to cost | 154 |

Dubois c. La Reine, 2007 DTC 1534, 2007 TCC 461 (Informal Procedure)

The taxpayer had to pay an amount in settlement of the damages claim of the vendor and incurred related legal expenses as a result of a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Start-Up and Liquidation Costs | 100 | |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Contract or Option Cancellation | 94 | |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | legal expenses incurred re cancellation of purchase may be loss from disposition | 90 |

| Tax Topics - Income Tax Act - Section 4 - Subsection 4(1) - Paragraph 4(1)(a) | 152 |

Avis Immobilièn G.M.B.H. v. The Queen, 94 DTC 1039, [1994] 1 CTC 2204 (TCC)

The taxpayer, which was a corporation resident in West Germany, borrowed deutschemarks ("DM") from a German bank to help finance the acquisition...

Capcount Trading v. Evans, [1993] BTC 3 (C.A.)

A capital loss of a British company from the disposal of shares of a Canadian company was to be determined by computing the difference between the...

Campbellton Enterprises Ltd. v. MNR, 90 DTC 1869, [1990] 2 CTC 2413 (TCC)

A bonus equal to three months' interest which the taxpayer paid in order to discharge a mortgage upon the sale of a rental property was deductible...

Samson Estate v. MNR, 90 DTC 1150, [1990] 1 CTC 2223 (TCC)

Professional fees incurred in seeking the cancellation of a zoning by-law were found to have been incurred in order to more easily dispose of the...

Bentley v. Pike, [1981] T.R. 17 (HCJ.)

Mrs. Bentley was considered under the Finance Act 1965 to have acquired, on her father's death in 1967, a 1/6 share of real property situate in...

Administrative Policy

12 June 2025 External T.I. 2025-1051441E5 - Deductibility of BC Home Flipping Tax

The B.C. Residential Property (Short-Term Holding) Profit Tax Act (“RPPTA”) imposes the “BC Home Flipping Tax” where a residential...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Income-Producing Purpose | BC Home Flipping Tax did not qualify under s. 18(1)(a) | 204 |

7 October 2022 APFF Financial Strategies and Instruments Roundtable Q. 3, 2022-0943261C6 F - Average Exchange Rate

Can an average exchange rate be used in computing the gains or losses from the disposition of capital property? CRA responded:

As a general rule,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 261 - Subsection 261(1) - Relevant Spot Rate | circumscribed acceptance of using average exchange rates | 257 |

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(1.1) | use of average exchange rate under s. 39(1.1) is permitted | 36 |

22 January 2020 External T.I. 2014-0559281E5 F - T5008

The T5508 Guide states:

Report only the total proceeds in box 21. Do not deduct any expenses from the proceeds… .

Respecting the application...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 49 - Subsection 49(1) | writing of call option (with deemed nil ACB) is reported as having nil “cost” on T5008 | 99 |

| Tax Topics - Income Tax Regulations - Regulation 230 - Subsection 230(2) | “cost” of call options closed out by writer is nil, not the cost of offsetting call option purchase/cost re short sale is the FMV of the borrowed shares | 351 |

| Tax Topics - Income Tax Act - Section 9 - Computation of Profit | cost of short sale is FMV of borrowed shares | 59 |

15 October 2015 Internal T.I. 2014-0527041I7 F - Disposition de biens

In the course of a discussion not based on a repetition of the applicable facts, CRA stated:

...Avis Immobilien GMBH ... [found that] "for the...

15 September 2015 External T.I. 2015-0583221E5 F - Redemption by a cooperative of its own shares

Is a gain realized by a cooperative corporation, on the redemption of its own preferred shares, taxable? CRA responded:

[N]o provision of the Act...

S4-F2-C1 - Deductibility of Fines and Penalties

1.22 If a fine or penalty (such as a mortgage prepayment penalty) is incurred in connection with the disposition of a capital property, the fine...

10 June 2013 STEP Round Table Q. 10, 2013 0480411C6 (Brosamler decision)

CRA considers Brosamler Estate to be confined to "a very specific fact situation," noting that the legal and probate fees in issue would have been...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Adjusted Cost Base | 85 |

11 January 2013 External T.I. 2012-0436771E5 - Sale of a business

The sole shareholder of Aco is required under the terms of the share sale agreement to repay, in full, at closing, a bank loan owing by Aco and an...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(9.1) | penalty paid by shareholder | 85 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(e) | corporation continued to be able to deduct unamortized issue expenses notwithstanding that its shareholder paid off the debt | 109 |

15 November 2012 External T.I. 2012-0461291E5 F - Frais judiciaires pour clarifier une servitude

A taxpayer who owned both a lakeside lot on which the taxpayer had a cottage and an adjoining lot (the "second lot") on which there was an...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Adjusted Cost Base | no comment on whether legal costs to avoid expanded easement were ACB addition | 78 |

24 April 2012 Internal T.I. 2011-0400671I7 F - Honoraires professionnels

A law firm (Advisor B) that was acting for both the purchasers and vendors (Mr. B and Corporation D) of shares of Corporation A was paid an agreed...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Start-Up and Liquidation Costs | fees incurred by individual before intention to form a corp did not qualify as pre-incorporation expenses | 486 |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | meaning of “benefit” | 164 |

4 September 2007 Internal T.I. 2007-0237791I7 F - Gain et perte sur taux de change

The taxpayer had a US dollar bank account into which it deposited US dollars from its sales and from which it lent US dollars to affiliates (in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(2) - Paragraph 40(2)(g) - Subparagraph 40(2)(g)(ii) | s. 40(2)(g)(ii) extended to FX losses on non-interest-bearing loan to parent | 25 |

7 June 2007 External T.I. 2007-0228831E5 F - Pénalité au rachat d'une obligation

When a bondholder requested an early repayment of its bonds, it was required to pay a premium that was withheld first from any accrued but unpaid...

29 July 2004 Internal T.I. 2003-0023761I7 F - Contrat de SWAP d'équité

After concluding that the payment, on the termination of an equity swap, by the taxpayer of the swap termination payment gave rise to a capital...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Loss v. Loss | loss on equity swap entered into in monetization transaction was on capital account | 163 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | termination of equity swap contract entailed the disposition of property | 67 |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Futures/Forwards/Hedges | equity swap was to hedge the risk under a capital borrowing, so that loss on closing out the swap was on capital account | 358 |

22 January 2004 External T.I. 2003-0006191E5 F - Frais et montant reçus lors de poursuite

A broker was sued for his alleged mismanagement of the portfolios (held on capital account) of a holding corporation, its principal shareholder...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | legal fees paid by corporation in suit by it and its shareholder and his RRSP should be allocated pro rata to them even though the joint incremental costs were minimal | 190 |

| Tax Topics - Income Tax Act - Section 54 - Proceeds of Disposition - Paragraph (f) | damages received for portfolio mismanagement could be proceeds under para. (f) | 87 |

11 December 2003 External T.I. 2003-0015975 F - calcul du gain/perte sur disposition

Under a Court-approved proposal to avoid the bankruptcy of a corporation, when Mr. A sold his shares of the corporation, he was required to pay a...

5 November 2003 Internal T.I. 2003-0037977 F - FRAIS POUR ANNULER UNE OFFRE D'ACHAT

An individual rescinded his agreement to purchase an immovable that he had initially intended to acquire for the purpose of renting it out, and...

8 September 2003 Internal T.I. 2003-0010407 F - Gains et pertes sur change étranger

The Directorate indicated that an article, stating that the way to compute the capital gain on the disposition of shares of a US corporation was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(2) | s. 39(2) applies to interest on US mortgage | 201 |

9 June 2003 Internal T.I. 2003-001330

Legal fees incurred, following the disposition by the taxpayers of a property, in a dispute as to the amount of the final payment due to the...

31 January 2003 External T.I. 2002-0161555 F - VENTE D'UN IMMEUBLE LOCATIF

The taxpayer signed an agreement with the tenant in which the taxpayer undertook to pay the tenant the rent paid over the past 12 months if he...

17 July 2001 External T.I. 2001-0068355 F - DEDUCTION D'UN BONI A UN EMPLOYE

Regarding whether a performance bonus paid to an employee based on the appreciation in value of a capital property that the employer disposed of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Oversight or Investment Management | investment performance bonus to be deductible would need to be incurred as part of the activity of managing the investments | 93 |

11 January 2001 Internal T.I. 2000-0037167 F - CLAUSE D'AJUSTEMENT DE PRIX

Compensation received by the share purchaser pursuant to an indemnity clause in the share sale agreement in respect of losses sustained by the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Adjusted Cost Base | post-closing indemnity payments received by purchaser reduced the ACB of its purchased shares | 118 |

29 March 2000 Internal T.I. 2000-0001367 F - PAIEMENT POUR SE LIBERER D'UNE HYPOTHEQUE

The taxpayers were not otherwise released from their liability under a mortgage on a property on the property’s purchase. A sum paid by them to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(9.1) | s. 18(9.1) did not apply to payment to be released from contingent payment obligation on assumed mortgage | 54 |

21 October 1993 Income Tax Severed Letter 9325325 - Mortgage Pay-out Penalties

Where penalty payments are made in order to pay off a mortgage, or reduce the interest rate on a mortgage, prior to the sale of the mortgaged...

26 January 1993 Memorandum (Tax Window, No. 28, p. 15, ¶2399)

Legal fees incurred by a taxpayer in a year subsequent to the sale of a capital property in order to collect the proceeds of disposition will not...

91 CR - Q.29

Where a landlord makes an inducement payment outside the ordinary course of its business to facilitate the sale of a building by increasing the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Timing | 14 |

18 November 1991 Memorandum (Tax Window, No. 11, p. 19, ¶1537)

S.40(1)(a)(i) may reduce the taxpayer's capital gain on the sale of shares where under the agreement the taxpayer is required to use a portion of...

89 C.M.TC - "Leasing Costs"

"payments made in contemplation of the sale of the property, i.e., to bring the property to full occupancy to enhance the sellling price ... are...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Contract or Option Cancellation | 42 |

Subparagraph 40(1)(a)(iii)

Cases

Pineo v. The Queen, 86 DTC 6322, [1986] 2 CTC 71 (FCTD)

The reserve was not available in respect of a demand promissory note received by the vendors as partial consideration for the sale of shares of a...

The Queen v. Derbecker, 84 DTC 6549, [1984] CTC 606 (FCA)

In S.40(1)(a)(iii)(A), "the words 'due to him' look only to the taxpayer's entitlement to enforce payment and not to whether or not he has...

Neder v. The Queen, 82 DTC 6022, [1981] CTC 501 (FCA)

Where a taxpayer has been reassessed so as to include in his income a taxable capital gain, a S.40(1)(a)(iii) reserve is not available to the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Land | 66 |

See Also

Alguire v. The Queen, 95 DTC 532 (TCC)

In 1981, the taxpayer sold the shares of a corporation owned by him to his mother for $600,000 under an oral agreement that she would pay him when...

Administrative Policy

2 April 2025 External T.I. 2019-0818321E5 F - Reverse Earnout

On the closing date for the sale by Opco of the assets, being capital property with an ACB of $150,000, of one of its two businesses to an arm's...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(g) | capital gains and then capital loss treatment of an asset sale made on a reverse earnout basis accepted, where the targets were not achieved | 327 |

S4-F7-C1 - Amalgamations of Canadian Corporations

1.95 A person entitled to a reserve under paragraph 20(1)(n), subparagraph 40(1)(a)(iii) or subparagraph 44(1)(e)(iii) in respect of an amount...

24 February 2014 External T.I. 2013-0505391E5 F - Clause de earnout renversé

CRA confirmed its position in 2000-0051115 that:

Where the cost recovery method is not used and the sale price of a property is not certain at the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(g) | no capital gains reserve on reverse earn-out for a share sale | 230 |

7 October 2013 Internal T.I. 2013-0504081I7 F - Interaction between 55(2) and 40(1)(a)(iii)

Vendor sold blocks of shares in the capital of a corporation (the “Purchaser”) to the Purchaser, with the purchase price being payable over a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2) | s. 40(1)(a)(iii) reserve available where redemption proceeds payable on earnout basis | 173 |

| Tax Topics - General Concepts - Payment & Receipt | distinction between promissory note as conditional or absolute payment | 249 |

16 November 2001 External T.I. 1999-0009295 - Reserve deemed capital gain

Decision summary 55-066 dated 29 November 29 1985 addressed whether a shareholder could claim a reserve under s. 40(1)(a)(iii) when its shares...

20 September 2001 Internal T.I. 2001-0091517 F - CHOIX LORS DE DISPOSITION DE BIA

The Directorate indicated that there is nothing in s. 14(1.01) limiting the application of the deeming rules provided in ss. 14(1.01)(a) to (c),...

17 November 1999 External T.I. 9901265 - 97(1) AND A RESERVE

"[W]here and individual transfers property to a partnership under subsection 97(2) of the Act and receives, in addition to a partnership interest...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 97 - Subsection 97(2) | 112 |

31 March 1995 External T.I. 9430115 - interest in a family farm partnership & capital gains RESERVE

A reserve may not be claimed where an individual transfers property to a partnership pursuant to s. 97(1) and receives as consideration a...

93 C.R. - Q. 41

Re whether changes to the terms of a take back note or mortgage result in loss of the reserve.

10 October 1991 T.I. (Tax Window, No. 11, p. 14, ¶1515)

Where the original due date on a vendor take-back mortgage or promissory note is extended by agreement, the entitlement of the vendor to continue...

21 August 1991 T.I. (Tax Window, No. 8, p. 6, ¶1403)

The entitlement of a vendor to claim a reserve where a promissory note was accepted only as evidence of the purchaser's obligation for the unpaid...

14 February 1991 T.I. (Tax Window, Prelim. No. 3, p. 12, ¶1119)

A vendor take-back mortgage, whose scheduled payments of principal are substantially deferred due to the financial difficulty of the purchaser,...

IT-236R2 "Reserves - Dispositions of Capital Property"

IT-436R "Reserves - Where Promissory Notes are Included in Disposal Proceeds"

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Payment & Receipt | 45 |

Articles

Smith, "Corporate Restructuring Issues: Public Corporations", 1990 Corporate Management Tax Conference Report, pp. 6:6-6:8: discussion of claiming of reserve by vendor under a take-over bid.

Clause 40(1)(a)(iii)(C)

Administrative Policy

24 July 2001 External T.I. 2001-006547 F - RESERVE POUR GAIN EN CAPITAL

No capital gains reserve was available to a taxpayer who disposed of real estate in exchange for shares of a public corporation which could not be...

Paragraph 40(1)(b)

Administrative Policy

18 August 2014 External T.I. 2014-0540361E5 F - CDA and the deeming rules of 40(3.6) or 112(3)

A corporation's capital dividend accounts will not be reduced by a loss on the redemption of shares held by it where such loss is deemed to be nil...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Capital Dividend Account | no capital loss for CDA purposes where ss. 112(3) and 40(3.6) stop-loss rules apply | 128 |

Subsection 40(2) - Limitations

Paragraph 40(2)(a)

Subparagraph 40(2)(a)(ii)

Administrative Policy

18 May 2004 External T.I. 2004-0069691E5 F - Incorporation des professionnels

Each of the partners, all individuals, in a partnership (a SENC) transfers their interest therein to the same corporation and each becomes a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 98 - Subsection 98(3) - Paragraph 98(3)(b) | WIP subject to s. 34 election is tranferred at nil | 149 |

| Tax Topics - Income Tax Act - Section 34 | insolvency practice carried on by accountants does not qualify as accountancy | 79 |

| Tax Topics - Income Tax Act - Section 249.1 - Subsection 249.1(2) | s. 249.1(2) not engaged by virtue only of no income being allocated to the partner | 236 |

Paragraph 40(2)(b)

Cases

Cassidy v. Canada, 2011 FCA 271

The taxpayer sold his six-acre rural property after it was rezoned for residential use as a result of an application made on behalf of owners of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Principal Residence - Paragraph (e) | 251 |

The Queen v. Joyner, 88 DTC 6459, [1988] 2 CTC 280 (FCTD)

In 1972, 14 acres of land which the taxpayer had acquired in 1965 was prohibited, by virtue of an Order in Council passed pursuant to the...

The Queen v. Yates, 83 DTC 5158, [1983] CTC 105 (FCTD), aff'd 86 DTC 6296 [1986] 2 CTC 46 (FCA)

It was held that the gain from the disposition of a portion of a principal residence was completely exempt since "it was not argued that, by its...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Principal Residence | 10 acres, which was the minimum size permitted by zoning restrictions, satisfied the necessary-for-residential use requirement | 60 |

See Also

Francoeur v. Agence du revenu du Québec, 2016 QCCQ 11906

Aubé, J found that an entrepreneur who had followed a pattern of building and selling residences, realized a capital gain eligible for the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Real Estate | somewhat quick flip by a builder was eligible for the principal residence exemption | 343 |

Cassidy v. The Queen, 2010 DTC 1336 [at at 4287], 2010 TCC 471

The taxpayer sold his six-acre rural property after it was rezoned for residential use as a result of an application made on behalf of owners of...

Administrative Policy

15 July 2024 External T.I. 2023-0990221E5 - Principal Residence Exemption-Condo parking Spaces

A taxpayer acquired a condominium unit and one parking space in 2017 for personal use, then acquired a second parking space on separate title in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Principal Residence | more than one parking space potentially may be part of a condo “housing unit” | 246 |

11 October 2019 APFF Roundtable Q. 2, 2019-0812611C6 F - Résiliation d'un bail - Lease cancellation

A tenant had been annually renewing a lease of a condo since the time the condo was first leased in July 2013. The condo was sold in February...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(z) | s. 20(1)(z) applies notwithstanding s. 18(1)(a) but is subject to source rule in s. 20(1) preamble | 193 |

| Tax Topics - Income Tax Act - Section 54 - Principal Residence | lease termination payment received by tenant was eligible for principal residence exemption | 116 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) | s. 20(1)-preamble source rule applied | 148 |

5 October 2018 APFF Financial Strategies and Instruments Roundtable Q. 11, 2018-0761571C6 F - Missing info on disposition of principal residence

CRA has summarized the detailed filing requirements for reporting a principal residence disposition and making the designation. CRA also...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Principal Residence - Paragraph (c) | CRA is only waiving penalties for late-filed principal residence dispositions for 2017 and 2016 returns | 355 |

6 October 2017 APFF Roundtable Q. 3, 2017-0709011C6 F - Désignation d’un bien comme résidence principale

On page 2 of Schedule 3 of the return for the year of disposition of a principal residence, if the individual checks the box for Case 1, would...

| Other locations for this summary | |

|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(2) - Paragraph 40(2)(b) | no loss of bonus year if standard designation |

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Principal Residence - Paragraph (c) | an individual accessing the “+1” rule on a principal residence disposition need not complete Form 2091 | 253 |

17 October 2014 Internal T.I. 2014-0546091I7 F - Indemnités lors d'une négociation de gré à gré

An individual who purchased a residential property received indemnity payments from the vendor, pursuant to a negotiated indemnity clause, to...

S1-F3-C2 - Principal Residence

No designation before ordinary habitation

2.29 If a taxpayer acquires land in one tax year and constructs a housing unit on it in a subsequent...

7 October 2016 APFF Roundtable Q. 2, 2016-0652841C6 F - Changement partiel d’usage - immeuble locatif et résidentiel

S1-F3-C2 “Principal Residence” para. 2.7 states that a housing unit includes a unit in a duplex. However, in 2011-0417471E5, CRA indicated...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 45 - Subsection 45(1) - Paragraph 45(1)(c) | switch between which triplex units used for personal/ family rental or 3rd-party rental did not trigger change of use | 249 |

| Tax Topics - Income Tax Act - Section 54 - Principal Residence | triplex contained separate housing units | 151 |

7 October 2016 APFF Roundtable Q. 3, 2016-0652851C6 F - Annulation d'une promesse d'achat sur une maison

As a result of breach of a puchaser's obligation to purchase a personal residence, the individual vendor received $50,000 in damages from the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(1) - Paragraph 39(1)(b) | no capital loss for damages paid for breach of purchase obligation | 73 |

10 June 2016 External T.I. 2015-0590371E5 F - Résidence principale - stationnement

Where a parking space was acquired as part of the purchase of a residential condo unit, the parking space can thereafter form part of the condo...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Principal Residence - Paragraph (e) | a parking space can form part of a condo housing unit | 241 |

13 March 2013 External T.I. 2012-0473291E5 F - Société de personnes - maison détruite par le feu

The Taxpayer was a partner of a partnership carrying on a farming business and owning more than half a hectare of land on which there was a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 44 - Subsection 44(5) - Paragraph 44(5)(a.1) | replacement property generally is expected to have the same material characteristics | 159 |

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(2) - Paragraph 40(2)(c) | s. 40(2)(c) unavailable re disposition of building only from fire | 111 |

5 October 2012 Roundtable, 2012-0453961C6 F - Copropriété indivise (50-50) d'un triplex

An individual held a triplex equally with his father in undivided co-ownership and also lived in one of the equally sized units as his principal...

23 January 2008 External T.I. 2007-0237251E5 F - Résidence principale - Destruction d'un triplex

A taxpayer owns a triplex that was completely destroyed in a fire. He ordinarily inhabited part of the triplex as his principal residence before...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Principal Residence - Paragraph (e) | garage remaining after destruction of triplex by fire was part of the contiguous land | 171 |

25 July 2007 External T.I. 2007-0224601E5 F - Application de l'alinéa 40(2)b)

A taxpayer acquired a residence and the subjacent land in 20X1, ordinarily inhabited it for three years, then in 20X4, demolished it without...

23 May 2007 External T.I. 2006-0215721E5 F - Application de l'alinéa 40(2)b)

A taxpayer acquired a cottage and the subjacent land in 1998, and ordinarily inhabited the cottage until 2002, when he demolished it and built a...

11 May 2007 External T.I. 2006-0214351E5 F - Transfert d'un droit de propriété

A and his wife B, had been undivided owners of a duplex since 1999, and lived in one of the units with their daughter C, while the other was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Property | an occupied unit in a co-owned duplex can be designated as a principal residence | 97 |

6 December 2006 External T.I. 2006-0152101E5 F - Disposition d'un domaine résiduel

A farmer disposes of his principal residence to a family farm corporation while retaining a life estate in it until he and his spouse die.

CRA...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 43.1 - Subsection 43.1(2) - Paragraph 43.1(2)(b) | ACB addition to residual interest in farm principal residence disposed of to family farm corporation | 233 |

4 March 2003 External T.I. 2002-0150985 F - TRANSFERT-RESIDENCE PRINCIPALE

CCRA indicated that the principal residence deduction could be utilized on a transfer of the residence by the individual to a wholly-owned...

11 April 1995 External T.I. 9507405 - 40(2)(B)

A non-resident who disposes of his principal residence can reduce the amount of the resulting capital gain by virtue of the fact that the...

16 February 1995 Mississauga Breakfast Seminar, Q. 4

Discussion of interaction between capital gains election under s. 110.6(19) and claiming of principal residence exemption for some (but not all)...

88 C.R. - Q.55

The taxpayer is not required to review his use and enjoyment of the property on a year by year basis respecting the half-hectare test.

80 C.R. - Q.24

Where a taxpayer purchased a vacant lot and later constructed his principal residence on it, the denominator will include the years that he owned...

Subparagraph 40(2)(b)(ii)

Administrative Policy

17 June 2025 STEP Roundtable Q. 10, 2025-1054541C6 - Principal Residence Exemption and Subsection 73(1) Transfer to a Life Interest Trust

An individual over 65 transfers both a city property and a recreational property, each of which would otherwise have qualified as the transferor's...

Paragraph 40(2)(c)

Administrative Policy

13 March 2013 External T.I. 2012-0473291E5 F - Société de personnes - maison détruite par le feu

The Taxpayer was a partner of a partnership carrying on a farming business and owning more than half a hectare of land on which there was a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(2) - Paragraph 40(2)(b) | partner can use the principal residence exemption re gain allocated by partnership from disposition of personally-used principal residence, including following s. 44 deferral | 263 |

| Tax Topics - Income Tax Act - Section 44 - Subsection 44(5) - Paragraph 44(5)(a.1) | replacement property generally is expected to have the same material characteristics | 159 |

Paragraph 40(2)(e)

See Also

Plant National Ltd. v. MNR, 89 DTC 401 (TCC)

As a consequence of the disposition by the taxpayer of voting preference shares of a corporation ("Enterprises") to Enterprises, Enterprises...

Administrative Policy

12 May 1992 Memorandum 921006 (May 1993 Access Letter, p. 194, ¶C38-156)

Because there is only a deemed disposition under s. 50(1)(a) and not an actual disposition, s. 40(2)(e) does not apply to a loss arising under s....

25 March 1991 T.I. (Tax Window, No. 1, p. 7, ¶1170)

The word "person" in s. 40(2)(e) includes "persons". Accordingly, if X Co. is controlled by Mr. X and Mrs. X together, s. 40(2)(e) will apply to a...

10 January 1990 T.I. (June 1990 Access Letter, ¶1257)

s. 40(2)(e) generally will not apply to the winding-up or liquidation of a foreign affiliate provided that under the relevant foreign corporate...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(9) | 58 |

86 C.R. - Q.22

The phrase "was controlled" means controlled at the time of the disposition.

Paragraph 40(2)(e.1)

Administrative Policy

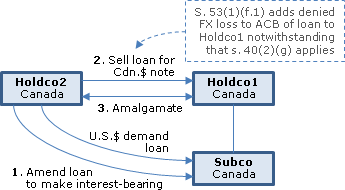

2014 Ruling 2013-0479701R3 - Transfer of US dollar loan

{kind=link}

Current structure

Holdco2, which is wholly-owned by Mr. X (a Canadian resident), made seven non-interest-bearing demand U.S-dollar loans...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(2) | amendment of non-interest bearing loan to be interest-bearing | 34 |

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(2) - Paragraph 40(2)(g) - Subparagraph 40(2)(g)(ii) | s. 40(2)(e.1) trumped s. 40(2)(g)(ii) so that US Loan ACB preserved | 122 |

| Tax Topics - Income Tax Act - Section 80.01 - Subsection 80.01(3) | S. 40(2)(e.1) trumped s. 40(2)(g)(ii) so that US Loan ACB preserved | 207 |

2012 Ruling 2011-0426051R3 - Debt Restructuring

{kind=link}

Opco is a Canadian resource company whose liabilities far exceed the value of its assets. It is the indirect subsidiary of a foreign parent and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80.01 - Subsection 80.01(4) | ATR-66 debt tuck-under and wind-up transactions | 354 |

Articles

Mike J. Hegedus, "Paragraph 40(2)(e.1) Versus Subparagraph 40(2)(g)(ii): Potential Conflict?", Resource Sector Taxation (Federated Press), Vol. IX, No. 4, 2014, p.684.

2013-0479701R3 may not have dealt with conflict between s. 40(2))(g)(ii) and s. 40(2)(e.1) (pp. 686-7)

In the third and most recent ruling, the...

Paragraph 40(2)(f)

Cases

Fournier-Giguère v. Canada, 2025 CAF 112

The three taxpayers, who were friends, were reassessed to include income from their poker gambling (of the type Texas Hold’em without limit) for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 3 - Paragraph 3(a) - Business Source/Reasonable Expectation of Profit | poker gambling was conducted as a full-time business through the use of skill and risk minimization techniques | 348 |

Administrative Policy

S3-F9-C1 - Lottery Winnings, Miscellaneous Receipts, and Income (and Losses) from Crime

Lottery Schemes

1.17 Paragraph 40(2)(f) specifies that no taxable capital gain or allowable capital loss results from the disposition of a chance...

Paragraph 40(2)(g)

Administrative Policy

7 October 2021 APFF Roundtable Q. 15, 2021-0901051C6 F - Exemption pour résidence principale

An individual held vacant land from 1990 to 1999 and then occupied a new home constructed thereon as the individual’s principal residence from...

28 January 2002 External T.I. 2002-0116635 F - REEE-REGLE D'ATTRIB. ET PERT NULLE

In finding that s. 40(2)(g) does not apply where a taxpayer transfers property to an RESP, CCRA stated:

[A] capital loss that a taxpayer may...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 74.3 - Subsection 74.3(1) - Paragraph 74.3(1)(a) | s. 74.1(2) does not apply where a taxpayer transfers property to an RESP | 106 |

Subparagraph 40(2)(g)(ii)

Cases

Service v. Canada, 2005 DTC 5281, 2005 FCA 163

The taxpayer, who was a minority shareholder of a corporation ("Homage") engaged in a condominium development project, lent money directly to...

Rich v. Canada, 2003 DTC 5115, 2003 FCA 38

In finding that the taxpayer was entitled to recognize a business investment loss on an interest-bearing loan made by him to a company ("DSM")...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(1) - Paragraph 39(1)(c) | 159 | |

| Tax Topics - Statutory Interpretation - Business Judgment | 68 | |

| Tax Topics - General Concepts - Purpose/Intention | subordinate purpose sufficient | 45 |

Byram v. R, 99 DTC 5117, [1999] 2 CTC 149 (FCA)

The taxpayer was able to deduct losses sustained on interest-free loans made by him to a U.S. operating company of which he was initially a direct...

Cadillac Fairview Corp. v. R., 99 DTC 5121, [1999] 3 CTC 353 (FCA)

The taxpayer was unable to recognize a capital loss in respect of its guarantees of bank loans made to real estate partnerships in which...

Bosa Bros. Construction Ltd. v. The Queen, 96 DTC 6193 (FCTD)

Interest-free advances that the taxpayer made to its U.S. subsidiary were found not to have been made to earn income (e.g., acquiring a product or...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Onus | 132 | |

| Tax Topics - Income Tax Act - Section 13 - Subsection 13(21) - Depreciable Property | depreciable property where CCA had been claimed and allowed | 111 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(p) - Subparagraph 20(1)(p)(ii) | interest-free advances to US sub by developer | 35 |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Real Estate | sale of stratified title property 1 year later on capital account/ secondary intention re ill-affordable property | 210 |

Brown v. The Queen, 96 DTC 6091 (FCTD)

The taxpayer made interest-free loans to a real estate corporation owned by him and others that were used to fund the corporation's obligations to...

Smith v. The Queen, 93 DTC 5351, [1993] 2 CTC 257 (FCA)

No deduction was available under s. 50(1)(a) in respect of a loan made by a corporation to an affiliate in the absence of any evidence that the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | benefit concurred in by taxpayer was not taxable under s. 56(2) as it was taxable to the recipient | 241 |

The Queen v. Lalonde, 84 DTC 6159 (FCTD), aff'd 89 DTC 5286 (FCA)

Two doctors made interest-free advances to a non-profit corporation which had been established to construct and operate an old-age home. Since...

See Also

Fiducie Immobilière JP v. The King, 2022 TCC 7

The appellant, a non-testamentary discretionary trust, made non-interest bearing loans to two companies (“Roseau” and “Spec”) which were...

Coveley v. The Queen, 2014 DTC 1041 [at at 2771], 2013 TCC 417, aff'd 2014 FCA 281

The taxpayers ("Michael and Solbyung"), were a married couple employed by a technology research corporation ("cStar"), and Solbyung was also a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 50 - Subsection 50(1) | bad debt claim, but business as usual | 120 |

Audet v. The Queen, 2012 DTC 1208 [at at 3556], 2012 TCC 162 (Informal Procedure)

The taxpayer, a certified general accountant, guaranteed a loan to one of his clients ("Cuisine Gourmet"), for which he became liable to pay...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Legal and other Professional Fees | fee to recover capital proceeds | 152 |

MacCallum v. The Queen, 2011 DTC 1225 [at at 1308], 2011 TCC 316

A corporation owned by the taxpayer and his wife wholly owned a trucking corporation ("D & N"), and his son wholly owned a small business...

Scott v. The Queen, 2010 TCC 401, 2010 DTC 1273 [at at 3910]

The taxpayer made a loan to a corporation owned by his son and daughter-in-law, whose business failed. Boyle J. allowed the loss because, while...

Alessandro v. The Queen, 2007 DTC 1373, 2007 TCC 411

The taxpayer had satisfied the burden of showing that loans advanced by her to a corporation of which she was only an indirect shareholder but for...

Daniels v. The Queen, 2007 DTC 883, 2007 TCC 179

The taxpayer and his brother used money borrowed by them from the Royal Bank of Canada to purchase debentures from a Canadian-controlled private...

Kyriazakos v. The Queen, 2007 DTC 373, 2007 TCC 66

Non-interest bearing advances that the taxpayer had made to a corporation after she had sold its shares to a friend were found not to have been...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 50 - Subsection 50(1) | no attempt to collect was reasonable | 132 |

Toews v. The Queen, 2005 DTC 1359, 2005 TCC 597

The recognition of a loss realized by the taxpayer on a non-interest bearing loan made by him to a company owned by a family trust was denied...

Proulx-Drouin v. The Queen, 2005 DTC 487, 2005 TCC 116

When the taxpayer paid under her guarantee of debts owing by her husband's corporation, she became a creditor of the corporation by subrogation....

Bernier v. The Queen, 2004 DTC 3235, 2004 TCC 376

The taxpayer was entitled to recognize under s. 39(2) capital losses incurred in a Bahamian margin account when U.S.-dollar margin loans were...

Joncas v. The Queen, 2004 DTC 2315, 2005 TCC 647 (Informal Procedure)

Interest-bearing advances made by the taxpayer to a cooperative corporation of which he was a member were found to have been made for the primary...

MacKay v. The Queen, 2003 DTC 748 (TCC)

After a corporation of which the taxpayer was a significant shareholder entered into a period of financial difficulty, the taxpayer followed the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(1) - Paragraph 39(1)(c) | 119 |

Gordon v. The Queen, 96 DTC 1554, [1996] 3 CTC 2229 (TCC)

The taxpayer caused two related corporations ("Grandview" and "Formete") to advance funds on behalf of a corporation ("Engineering") owned by the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(12) | 85 |

Burns v. The Queen, 94 DTC 1370, [1994] 1 CTC 2364 (TCC)

Five siblings, including the taxpayer, loaned money on a non-interest bearing basis to a corporation ("WFC") as part of transactions that resulted...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 50 - Subsection 50(1) | 111 |

National Developments Ltd. v. The Queen, 94 DTC 1061 (TCC)

The taxpayer, which was a significant shareholder of a Minnesota corporation ("K-Tel") agreed along with another major shareholder ("Tri-State")...

W.F. Botkin Construction Ltd. v. The Queen, 93 DTC 448, [1993] 1 CTC 2765 (TCC)

The purchase price for the sale of the taxpayer's business to a corporation owned by the children of the taxpayer's shareholder was financed by...

Glass v. MNR, 92 DTC 1759 (TCC)

Pursuant to a written agreement with the existing shareholders, the taxpayer purchased 25% of the shares of a land development corporation for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | 97 | |

| Tax Topics - Income Tax Act - Section 54 - Adjusted Cost Base | sum paid to discontinue an injunction was part of cost of mortgage | 104 |

Madaline v. MNR, 91 DTC 1451, [1991] 2 CTC 2658 (TCC)

A loss on a guarantee given by the taxpayer of a loan to his son's business was not made for the purpose of gaining or producing income but,...

O'Blenes v. MNR, 90 DTC 1068, [1990] 1 CTC 2171 (TCC)

At the time that the taxpayer guaranteed amounts owing by a corporation of which her husband was the shareholder and officer, "she was not...

Business Art Inc. v. MNR, 86 DTC 1842, [1987] 1 CTC 2001 (TCC)

Interest-free loans which the taxpayer made to a U.K. subsidiary, which had been established to purchase supplies in the U.K. for resale to the...

Administrative Policy

14 June 2017 External T.I. 2016-0666411E5 - Negative returns on investments

A Canadian-resident taxpayer purchases a negative yield bond for $102 and will receive $100 when it matures in five years. The bond does not pay...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Loans and Financing Charges | negative interest is deductible under s. 9 if there is a reasonable expectation of receiving (positive) interest | 152 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) - Subparagraph 20(1)(c)(i) | negative interest not a contra to positive interest | 150 |

S4-F8-C1 - Business Investment Losses

1.46 ... Where a shareholder provides a guarantee or loan to a corporation in order to provide it capital, a clear connection will generally exist...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Small Business Corporation | "substantially" and "principally" | 38 |

| Tax Topics - Income Tax Act - Section 50 - Subsection 50(1) | End of year references taxpayer | 343 |

| Tax Topics - Income Tax Act - Section 50 - Subsection 50(1.1) | 247 | |

| Tax Topics - Income Tax Act - Section 50 - Subsection 50(1) - Paragraph 50(1)(a) | Proactive collection efforts | 157 |

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(9) | Example | 182 |

| Tax Topics - Income Tax Act - Section 164 - Subsection 164(6) | Limitation on BIL carryback | 96 |

16 June 2016 Internal T.I. 2015-0597971I7 F - Perte réputée nulle - loss deemed nil

Mrs. A, F1 and F2 held, as co-owners, a building whose sole tenant was Corporation, which was owned by Mrs. A. F1 and F2 advanced sums (the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(1) - Paragraph 39(1)(c) | BIL potentially could be recognized on a non-interest bearing loan made to a corporation in which the taxpayer had no equity | 0 |

2014 Ruling 2013-0479701R3 - Transfer of US dollar loan

Holdco2, which is wholly-owned by a Canadian resident individual, made a non-interest-bearing demand U.S-dollar loans (the "US Loan") to the ...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(2) | amendment of non-interest bearing loan to be interest-bearing | 34 |

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(2) - Paragraph 40(2)(e.1) | s. 40(2)(e.1) trumped s. 40(2)(g)(ii) so that US Loan ACB preserved | 207 |

| Tax Topics - Income Tax Act - Section 80.01 - Subsection 80.01(3) | S. 40(2)(e.1) trumped s. 40(2)(g)(ii) so that US Loan ACB preserved | 207 |

6 May 2014 Internal T.I. 2014-0524651I7 - Loss on conversion

Canco indirectly controlled ULC which was the sole member (holding common membership units) of LLC. ULC also held non-interest-bearing Notes...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 51 - Subsection 51(1) | s. 51 applies where issuer had a cash redemption override | 208 |

| Tax Topics - Income Tax Act - Section 51 - Subsection 51(1) | conversion not under Note terms | 185 |

8 July 2013 Internal T.I. 2012-0434991I7 F - Déductibilité d'une perte

As a sideline activity to the practice of his profession, Mr. A and his partners made loans, an activity which required little time in comparison...

| Other locations for this summary | |

|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(2) - Paragraph 40(2)(g) - Subparagraph 40(2)(g)(ii) | per jurisprudence on guarantees, taxpayer’s reason for assuming an obligation (to protect an interest-bearing investment) must be examined |

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(p) - Subparagraph 20(1)(p)(ii) | ordinary business requirement looks to the presence of an organized and continuous system | 251 |

6 December 2012 External T.I. 2012-0463431E5 F - Application of subparagraph 40(2)(g)(ii)

Creditor and Debtor were wholly-owned subsidiaries of the same parent. Creditor made interest-free loans (the "Debts") to Debtor, and subsequently...

2012 Ruling 2010-0386201R3 - Tower structure capitalized by interest-free loans

{kind=link}

Existing structure

Canco, which is a privately-owned taxable Canadian corporation, holds a US limited liability limited partnership ("LLLP")...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(i) | non-interest-bearing loans is made for income producing purposes: generating dividends | 890 |

4 September 2007 Internal T.I. 2007-0237791I7 F - Gain et perte sur taux de change

CRA found that any FX loss realized on a USD loan to the taxpayer’s parent would be denied under s. 40(2)(g)(ii).

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(1) - Paragraph 40(1)(a) - Subparagraph 40(1)(a)(i) | USD loan to parent no longer represented money on deposit, so that funds movement generated FX gain or loss | 269 |

21 June 2007 Internal T.I. 2007-0239681I7 F - perte sur prêts irrécouvrables

In 1999, an individual, Mr. A, acquired shares of a small business corporation (the "Corporation") through his RRSP, and subsequently, personally...

9 June 2005 Internal T.I. 2005-0122511I7 F - Créance irrécouvrable dans une OSBL

Before finding that a loss on an interest-bearing loan made by a director of a not-for-profit organization to the NPO that became a bad debt when...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(1) - Paragraph 39(1)(c) - Subparagraph 39(1)(c)(iv) | loss on interest-bearing loan made by a director to an NPO qualified as BIL if NPO qualified as SBC | 108 |

22 January 2004 Internal T.I. 2003-0047561I7 F - Effet de la délégation puis de la subrogation

The taxpayer sold an immovable to a purchaser who assumed a mortgage on the property. The purchaser subsequently defaulted, and the mortgagee sold...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 42 | payment under covenant of vendor regarding mortgage assumed by purchaser, who defaulted on its assumed obligation, did not generate a s. 42 loss | 168 |

14 January 2004 External T.I. 2003-003875

CRA has accepted the decision in Byram so that, in its view, when the debtor is a wholly-owned subsidiary of the taxpayer, a clear nexus between...

18 December 2003 Internal T.I. 2003-0044007 F - OPTION D'ACHAT D'ACTIONS RACHETEES

The taxpayer surrendered his stock options to his arm’s-length employer for consideration that was payable partly up front and partly in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(1) - Paragraph 7(1)(b) | full option surrender consideration included under s. 7(1)(b) even though a portion thereof never paid | 170 |

| Tax Topics - Income Tax Act - Section 54 - Capital Property | employee stock option surrender proceeds were not from the disposition of capital property | 84 |

24 September 2003 Internal T.I. 2003-0184097 F - perte au titre de placement

CCRA accepted the correctness of Byram in finding that, since a shareholder made a non-interest bearing loan the a corporation with the...

21 November 2001 Internal T.I. 2001-0094527 F - PERTE REPUTEE NULLE-BRYAN

In finding that a non-interest bearing loan made by the individual shareholder likely satisfied s. 40(2)(g)(ii) in light of Byram, the Directorate...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 50 - Subsection 50(1) - Paragraph 50(1)(a) | no partial bad debt recognition under s. 50(1)(a) | 64 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(27) | s. 248(27) does not permit partial debt write-off under s. 50(1)(a) | 75 |

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(1) - Paragraph 39(1)(c) - Subparagraph 39(1)(c)(ii) | settlement of corporate debt under a bankruptcy proposal did not entail disposition of the debt to the corporation | 89 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(2) - Paragraph 251(2)(b) - Subparagraph 251(2)(b)(i) | shareholder continued to control “his” corporation while it was being administered by a bankruptcy trustee pending approval of a proposal | 83 |

| Tax Topics - Income Tax Act - Section 116 - Subsection 116(5) | settlement under bankruptcy proposal of debt did not entail a disposition of that debt to the corporation | 50 |

7 June 2001 Internal T.I. 2000-0060747 F - PROPOSITION CONCORDATAIRE - PTPE

The Shareholder made various non-interest-bearing advances to a Canadian-controlled private corporation (the Corporation), whose creditors...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition - Paragraph (b) - Subparagraph (b)(ii) | discharge of unsecured debt owing to debtor’s shareholder under bankruptcy proposal was a disposition | 125 |

9 January 2001 Internal T.I. 2000-0058047 F - FRAIS JURIDIQUES

A director was assessed under ETA s. 323 and the Quebec equivalent for unpaid GST/QST of the inactive corporation. After finding that he was not...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Legal and other Professional Fees | director’s legal fees incurred re his liability for unpaid corporate GST were non-deductible | 70 |

18 July 2000 External T.I. 2000-0015915 F - PTPE - INTERET PAYE POUR HONORER CAUTION

An individual who was the sole shareholder of a small business corporation guaranteed a loan to it from a bank. Following its insolvency of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(1) - Paragraph 39(1)(c) - Subparagraph 39(1)(c)(iv) | no BIL on loan from bank to fund guarantee of former SBC’s debt or where subrogated debt of the former SBC arises from voluntary payment of its defaulted debt rather than under guarantee | 257 |

9 September 1999 Internal T.I. 9902717 F - DÉDUCTIBILITÉ D'UN REMBOURSEMENT DE DETTE

The taxpayer and the three other co-owners of a rental property disposed of the property to a third party who assumed the mortgage, but later...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(1) - Paragraph 40(1)(a) | no disposition and, therefore, no capital loss on paying under residual covenant on assumed but defaulted mortgage | 50 |

10 September 1999 External T.I. 9901545 F - DIRECTORS LIABILITY - ABIL

Two individuals (also equal shareholders) who, by virtue of being directors of a corporation that became insolvent, were required to pay GST and...

13 July 1999 External T.I. 9901535 F - PERTE EN CAPITAL - REPUTE NULLE

In finding that a capital loss realized by a corporation, on a non-interest-bearing loan made to a sister corporation that then ceased operations,...

27 January 1999 Internal T.I. 9832187 F - UTILISATION DE PERTES - 40(2)G)(II)

In order to generate a capital loss to offset a capital gain on a share sale, the taxpayer acquired an interest-bearing debt from a related...

17 December 1996 Internal T.I. 9634547 - DISPOSITION OF EMPLOYMENT BONUS NOTES

A loss realized by an employee from the disposition of notes received by him from his employer in lieu of a cash bonus would not be subject to the...

Halifax Round Table, February 1994, Q. 1

A loss realized by a shareholder of a small business corporation on the sale of a non-interest bearing loan to an arm's length party may be...

23 December 1993 Income Tax Severed Letter 9317905 - Allowable Business Investment Loss

Discussion of when a shareholder can recognize a capital loss on a non-interest bearing loan owing to her by the corporation where the shareholder...

91 C.R. - Q.35

Where a holding company is required to have an interest-free debt owing to it by Opco settled for an amount less than its ACB as a condition to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(1) - Paragraph 39(1)(c) | 28 |

21 August 1991 T.I. (Tax Window, No. 8, p. 22, ¶1397)

A director's loss under s. 227.1 will be non-deductible by virtue of s. 40(2)(g).

12 September 1990 T.I. (Tax Window, Prelim. No. 1, p. 10, ¶1016)

Where A transferred a non-interest-bearing debt at a loss to its affiliate, B, and B then sold the debt in an arm's length transaction, the loss...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(1) - Paragraph 53(1)(f.1) | 50 |

15 September 89 Memorandum (February 1990 Access Letter, ¶1105)

The position in IT-445 respecting interest-free loans is still supportable. The Business Art case, in which a Canadian corporation was allowed to...

1 September 89 T.I. (February 1990 Access Letter, ¶1106)

Where a wife guaranteed for no consideration a bank loan to her husband's corporation in which she was not a shareholder, she was unable to claim...

22 Aug. 89 T.I. (Jan. 90 Access Letter, ¶1078)

In light of the Canada Safeway and DWS cases, RC does not accept that when a shareholder incurs a debt to his corporation he does so to indirectly...

81 C.R. - Q.4

Guidelines in the case of a guarantee granted a lender by a sole shareholder of the borrower for no compensation.

IT-239R2 "Deductibility of Capital Losses from Guaranteeing Loans for Inadequate Consideration and from Loaning Funds at less than a Reasonable Rate of Interest in Non-arm's Length Circumstances"

6. Where a taxpayer has loaned money at less than a reasonable rate of interest to a Canadian corporation of which he is a shareholder, or to its...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) | 48 | |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 0 | |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 0 |

IT-390 "Unit Trusts - Cost of Rights and Adjustments to Cost Base"

A capital loss arising when additional units are issued in settlement of a unit holder's right to receive a distribution of a capital gain of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 52 - Subsection 52(6) | 317 |

Articles

Reid, "Capital and Non-Capital Losses", 1990 Conference Report, c. 16

Discussion of deductibility of losses arising from amounts paid under guarantees.

Subparagraph 40(2)(g)(iii)

Administrative Policy

7 October 2016 APFF Financial Strategies and Instruments Roundtable Q. 4, 2016-0651791C6 F - Choix 45(2) et (3) - immeuble à logements

At civil law, land and building are a single property (although this rule is overridden for CCA/recapture purposes). Consequently, if a duplex...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 45 - Subsection 45(3) | invalidity of s. 45(3) elections on duplex units applied only for changes of use after February 21, 2012 | 185 |

| Tax Topics - Income Tax Act - Section 54 - Personal-Use Property | land underlying duplex used 40% personally is not personal-use property | 233 |

| Tax Topics - Income Tax Regulations - Regulation 1102 - Regulation 1102(2) | Reg. 1102(2) deems building to be separate from land and does not bifurcate the land | 176 |

Subparagraph 40(2)(g)(iv)

Clause 40(2)(g)(iv)(B)

Administrative Policy

7 May 2003 External T.I. 2003-0182755 F - Superficial Loss on Shares

The taxpayer’s spouse realized a capital loss on transferring her shares, with an accrued capital loss, for cash proceeds equaling their FMV,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Superficial Loss | transactions for sale by individual to her husband circumvented s. 40(2)(g)(i) through the sale by him back to her RRSP, and could be GAARable | 274 |

Subsection 40(3) - Deemed gain where amounts to be deducted from adjusted cost base exceed cost plus amounts to be added to adjusted cost base

Administrative Policy

30 October 2014 External T.I. 2013-0488881E5 - Upstream Loan

Where Canco receives a s. 90(9)(a) notional dividend as a result of a loan from a 2nd tier FA (FA2), it will not be credited for s. 90(9)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | no double inclusion following FA creditor wind-up | 60 |

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(6) | no double inclusion following FA creditor wind-up or for 2nd loan in series | 121 |

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(9) | notional election and double taxation issues | 1332 |

| Tax Topics - Income Tax Regulations - Regulation 5901 - Subsection 5901(1.1) | notional Reg. 5901(1.1) election | 30 |

| Tax Topics - Income Tax Regulations - Regulation 5901 - Subsection 5901(2) - Paragraph 5901(2)(a) | 90-day rule unavailable | 28 |

| Tax Topics - Income Tax Regulations - Regulation 5901 - Subsection 5901(2) - Paragraph 5901(2)(b) | notional Reg. 5901(2)(b) election | 31 |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Underlying Foreign Tax | notional UFT disproportionate election | 37 |

8 October 2010 Roundtable, 2010-0373461C6 F - Retrait d'une société de personnes

Where a general partner whose units have a negative ACB has his units redeemed equally over the course of five years, 20% of the negative ACB will...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 100 - Subsection 100(2) | negative ACB realized pro rata under s. 100(2) as portion of the units are redeemed each year | 201 |

| Tax Topics - Income Tax Act - Section 43 - Subsection 43(1) | all the partner’s units are a single property | 81 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Property | partnership unit is not separate property from other units | 57 |

30 March 1993 Income Tax Severed Letter 9235566 - Motion Picture Films—Capital Cost Allowance

Discussion in Appendix of techniques for postponement of realization of negative ACB by investors in film limited partnership. RC also states that...

Articles

Melanie Huynh, Eric Lockwood, "Foreign Affiliates and Adjusted Cost Base", 2007 Canadian Tax Journal, Issue No. 1

Effect of negative ACB gains on CFA shares that are excluded property

- Canco, wholly-owns CFA 1, which wholly-owns CFA 2. A Canadian dollar (but...

Subsection 40(3.1) - Deemed gain for certain partners

See Also

Gladwin Realty Corporation v. The Queen, 2019 TCC 62, aff'd 2020 FCA 142

The taxpayer, a private real estate corporation, rolled a property under s. 97(2) into a newly-formed LP, with the LP then distributing to the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | using the CDA and negative ACB rules to generate “over-integration” was abusive | 594 |

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Capital Dividend Account - Paragraph (a) | contrary to purpose of the capital dividend rules to fully exempt a capital gains distribution | 300 |

| Tax Topics - Income Tax Act - Section 123.3 | no CRA challenge to continuance to BVI to avoid s. 123.3 tax | 96 |

Administrative Policy

10 April 2024 External T.I. 2021-0919231E5 - Foreign tax allocation to a partner

Would the allocation of foreign tax by a partnership to a partner be regarded as a withdrawal by the particular partner that reduced the ACB of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(2) - Paragraph 53(2)(c) - Subparagraph 53(2)(c)(v) | payment of withholding tax by a partnership “on behalf of its partners is an ACB-reducing distribution to them | 272 |

| Tax Topics - General Concepts - Payment & Receipt | payment by partnership of withholding tax treated as a distribution to its partners | 99 |

29 November 2022 CTF Roundtable Q. 1, 2022-0949781C6 - Loans Made by Limited Partnerships to Limited Partners

2016-0637341E5 stated that s. 53(2)(c)(v) is very broad and could in theory (depending on all relevant facts) apply to the amount of the loans...

7 October 2022 APFF Roundtable Q. 5, 2022-0947611C6 F - Limited Partnership and Loans

2016-0637341E5 indicated that s. 53(2)(c)(v) potentially could apply respecting the amount of loans made by a partnership to a limited partner....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(2) - Paragraph 53(2)(c) - Subparagraph 53(2)(c)(v) | guarded acceptance of distributions of LP profits as loans, followed by set-off against draws in January | 377 |

27 June 2016 External T.I. 2016-0637341E5 F - Partnerships - Negative ACB

Rather than making current distributions of its cash flow to a limited partner, those sums are lent by the LP to the limited partner – then at...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(2) - Paragraph 53(2)(c) - Subparagraph 53(2)(c)(v) | loan advances to a limited partner may give rise to immediate s. 53(2)(c)(v) grind | 261 |

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(3.13) | retention of partnership profits not a contribution | 146 |

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(1) - Paragraph 53(1)(e) - Subparagraph 53(1)(e)(iv) | assumption of loan can be contribution, but not retained profits | 177 |

18 June 2014 External T.I. 2011-0417491E5 - Non-resident's partnership interest

A non-resident corporation (NRco) is deemed under s. 40(3.1)(a) to realize a gain in respect of its limited partnership interest in P, which is...

15 December 2010 External T.I. 2009-0349911E5 F - Calcul du PBR d'une participation dans une SEC

In February 2008, a limited partnership (“LP”) realized a capital gain, of which $100,000 was allocable to Limited Partner A, whose interest...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(1) - Paragraph 53(1)(e) - Subparagraph 53(1)(e)(i) | no ACB bump for gains realized in the year until Day 1 of following year | 98 |

Subsection 40(3.12) - Deemed loss for certain partners

Administrative Policy

2021 Ruling 2021-0895071R3 F - Partnership Reorganization

A limited partnership (Carry LP), that was owned directly or indirectly by two unrelated individuals (A and B) and their families, held a carry...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 98 - Subsection 98(3) | conversion of a carry to a straight-up interest | 476 |

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(3.3) | refusal to rule where shares received on LP s. 98(3) wind-up immediately sold to Carry LP owned by owners of former general partner | 345 |

3 July 2012 External T.I. 2012-0449701E5 - Subsection 40(3.12) and tiered ptnshps

As s. 40(3.12) is limited to corporations, individuals (other than trusts) and testamentary trusts:

[a]n election under subsection...

29 June 2000 External T.I. 2000-0026635 F - APPLICATION 40(3.12) SUITE A 98(6)

A limited partnership (LP), whose two limited partners had realized negative adjusted cost base (ACB) gains, transferred all its assets and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 98 - Subsection 98(6) | s. 98(6) applied on conversion of limited partnership to general partnership | 32 |

Articles

Joint Committee, "Response to Green case", 19 January 2018 Joint Committee Submission to Finance respecting the Green case

Desirability of extending relief from negative ACB gains

Although s. 40(3.12) is intended to address the problem of negative ACB arising from...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(1) - Paragraph 111(1)(e) | 231 |

Subsection 40(3.13)

Administrative Policy

27 June 2016 External T.I. 2016-0637341E5 F - Partnerships - Negative ACB

Rather than making current distributions of its cash flow to a limited partner, those sums are lent by the LP to the limited partner – then at...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(2) - Paragraph 53(2)(c) - Subparagraph 53(2)(c)(v) | loan advances to a limited partner may give rise to immediate s. 53(2)(c)(v) grind | 261 |

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(3.1) | loans by LP to partner potentially gave rise to negative ACB gain | 164 |

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(1) - Paragraph 53(1)(e) - Subparagraph 53(1)(e)(iv) | assumption of loan can be contribution, but not retained profits | 177 |

Subsection 40(3.14)

Paragraph 40(3.14)(a)

Administrative Policy

11 October 2013 APFF Roundtable, 2013-0495861C6 F - Question 20 - APFF Round Table

In the course of a general discussion, CRA stated:

In order not to qualify as a limited partner pursuant to paragraph 40(3.14)(a), it is...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Specified Member | specified member status determined re involvement in daily management or activities | 93 |

Articles