Cases

Canada v. DAC Investment Holdings INC., 2026 FCA 35

With a view to its imminent disposition of the shares of a subsidiary (its only asset, which it had acquired two weeks previously on a rollover...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 123.3 | rationale of ss. 123.3 and 123.4 included avoidance of tax deferral on investment income | 180 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(2) | s. 245(2) only permits the denial of tax benefits rather than other reasonable adjustments | 220 |

Deml Investments Limited v. Canada, 2025 FCA 204

In early 2008, the sale of resource properties by an arm’s length vendor (Transglobe) to the parent (Direct Energy) of the taxpayer (DEML) was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(d) | rationale of s. 88(1)(d) is to push onto sub’s non-depreciable property the ACB of the sub’s shares that otherwise would be lost on the winding-up | 325 |

Total Energy Services Inc. v. Canada, 2025 FCA 77

In September 2007, a company (“Nexia”), which traded in loss companies, acquired all of non-voting common shares of an insolvent public...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(5) | Deans Knight applied to the acquisition of a public lossco by a SIFT trust | 275 |

Madison Pacific Properties Inc. v. Canada, 2025 FCA 20

Under a “restart” plan, the appellant changed its name, spun out its existing mining assets so that it was a shell with only tax losses, and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | series of transactions included the subsequent loss utilization which motivated corporate restart transactions | 248 |

Magren Holdings Ltd v. Canada, 2024 FCA 202

The taxpayers were private companies controlled by a resident individual (Grenon), whose RRSP held 58% of the units of a publicly traded income...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(1) - Tax Benefit | avoidance of Pt. III tax liability was a tax benefit | 529 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(2) | it is reasonable to assess a 60% tax under s. 245(2) if that was the quantum of tax whose avoidance represented the tax benefit | 212 |

| Tax Topics - General Concepts - Ownership | RRSP trust transferred the ownership of the income fund units in which it transacted | 325 |

| Tax Topics - General Concepts - Sham | finding of sham must consider what are in fact the real transactions | 50 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition - Paragraph (e) | transfer of property by a trust is a disposition unless to an agent | 114 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(6) | capital gain can be distributed on a redemption of units | 298 |

3295940 Canada Inc. v. Canada, 2024 FCA 42

The taxpayer (3295) was a holding company with a minority shareholding in a target company (Holdings) with a low ACB, whereas the holding company...

The King v. MMV Capital Partners Inc., 2023 FCA 234

A venture capital corporation (MMV) acquired 49% of the voting common shares of the respondent while in interim bankruptcy proceedings and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(5) | abuse of s. 111(5) for unrelated corporations to use losses from another business | 295 |

Deans Knight Income Corp. v. Canada, 2023 SCC 16

The non-capital losses of $90M, and other tax attributes (the “Tax Attributes”) of the taxpayer, were effectively sold to arm’s length...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(5) | rationale of s. 111(5) addresses where there is a change in the identity of those behind a corporation | 416 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | lender to distressed corporation may have de facto control | 118 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | series includes transactions undertaken before or after the series in relation to the series | 75 |

Canada v. Alta Energy Luxembourg S.A.R.L., 2021 SCC 49, [2021] 3 S.C.R. 590

A Blackstone limited partnership and a U.S. shale company transferred their investment in a Canadian subsidiary (Alta Canada), that was to develop...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 13 | utilization of the business property exemption by a Luxembourg conduit accorded with the bargain negotiated by Canada, which was to encourage investment by such investors | 605 |

| Tax Topics - Treaties - Income Tax Conventions - Article 4 | a company resident under Luxembourg domestic law (its legal seat was there), and that was “liable to be liable to tax,” was resident there for Treaty purposes even though a conduit | 386 |

| Tax Topics - Treaties - Income Tax Conventions | subsequent OECD Treaty commentary not followed | 198 |

| Tax Topics - Statutory Interpretation - Treaties | additional consideration in Treaty context of giving effect to the contractual bargain | 237 |

Canada v. Deans Knight Income Corporation, 2021 FCA 160, aff'd 2023 SCC 16

The non-capital losses of $90M, and other tax attributes of the taxpayer, were effectively sold to arm’s length investors pursuant to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(5) - Paragraph 111(5)(a) | the object and spirit of s. 111(5) is abused on an arm’s length acquisition of “actual” (albeit, not de jure) control of a Lossco | 522 |

The Gladwin Realty Corporation v. Canada, 2020 FCA 142

The taxpayer, a private real estate corporation, rolled a property under s. 97(2) into a newly-formed limited partnership, with the LP then...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(1) - Tax Benefit | tax benefit did not arise until alleged excessive CDA utilized outside a corporate group | 261 |

Canada v. Alta Energy Luxembourg S.A.R.L., 2020 FCA 43, aff'd 2021 SCC 49

A Blackstone LP and a U.S. shale company transferred their investment in a Canadian subsidiary (Alta Canada), that was to develop a shale...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 13 | Treaty shopping was not an abuse | 391 |

Birchcliff Energy Ltd. v. Canada, 2019 FCA 151

A newly-launched public corporation (“Predecessor Birchcliff”), accessed the losses of a Lossco (Veracel), in order to shelter the profits...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(7) - Paragraph 256(7)(b) - Subparagraph 256(7)(b)(iii) - Clause 256(7)(b)(iii)(B) | policy is to exclude the truly larger corporation (ignoring transitory cash) from loss streaming rules | 299 |

Madison Pacific Properties Inc. v. Canada, 2019 FCA 19

Predecessors of the taxpayers had been acquired for their losses in transactions where less than 50% of their voting shares, but more than 90% of...

2763478 Canada Inc. v. Canada, 2018 FCA 209

An individual did not sell his shares of an operating company (Groupe AST) directly to a third-party purchaser, but instead transferred them on a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | 9 month separation did not avoid series | 290 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | not each transaction in series effecting an estate freeze had that objective | 417 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(6) | individual allegedly suffering double taxation re s. 245(2) denial of capital loss of his corporation failed to apply under s. 245(6) within 180 days | 327 |

Canada v. 594710 British Columbia Ltd., 2018 FCA 166

The taxpayer was a holding company which wholly-owned a “Partnerco” holding an approximate ¼ limited partnership interest in a strata...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | stock dividend followed by redemption of the stock dividend shares effected in combination a transfer of property for no consideration | 334 |

| Tax Topics - Income Tax Act - Section 103 - Subsection 103(1) | s. 103(1) likely applies to the allocation of most of the partnership profits at year end to a lossco that never had significant economic interest or risk in the partnership business | 327 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(8) | s. 152(8) cured an error in an assessment as to when the taxation year in question commenced | 371 |

| Tax Topics - Income Tax Act - Section 96 - Subsection 96(1) - Paragraph 96(1)(f) | purpose of s. 96 is for income allocation to be allocated in accordance with economic participation | 102 |

Pomerleau v. Canada, 2018 FCA 129

To simplify the facts somewhat by ignoring transactions in which the taxpayer accessed tax attributes of his sister, the taxpayer wanted to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2) - Paragraph 84.1(2)(a.1) - Subparagraph 84.1(2)(a.1)(ii) | GAAR applied to converting soft ACB (generated from crystallizing the capital gains deduction) into pseudo-hard ACB under s. 53(1)(f.2) for use in extracting surplus | 497 |

Wild v. Canada (Attorney General), 2018 FCA 114

Mr. Wild stepped up the adjusted cost base of his investment in a small business corporation (PWR) by transferring his PWR common shares to two...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) | transactions to bump PUC did not abuse s. 84.1 prior to use of such PUC to strip surplus | 207 |

Fiducie financière Satoma v. Canada, 2018 FCA 74

In order to strip surplus of an operating corporation (“Gennium”) controlled by the Pilon family, a dividend paid by Gennium was distributed...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(1) - Tax Benefit | tax benefit to trust from tax-free dividend even though not distributed to a beneficiary | 277 |

| Tax Topics - Income Tax Act - Section 3 | pervasive rule that the same income is not to be taxed in 2 persons’ hands | 148 |

| Tax Topics - Statutory Interpretation - Double Taxation/Deduction (Presumption Against) | inclusion of income in more than one taxpayer’s hands is contrary to s. 3 | 294 |

| Tax Topics - Income Tax Act - Section 112 - Subsection 112(1) | abusive to use s. 112(1) so as to avoid ultimate taxation of individuals | 180 |

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(2) | use of s. 75(2) to access s. 112(1) deduction for dividend in fact received by family trust, was abusive | 286 |

| Tax Topics - Income Tax Act - Section 82 - Subsection 82(2) | s. 82(2) supports the primacy of s. 75(2) over the actual dividend recipient | 60 |

Canada v. Oxford Properties Group Inc., 2018 FCA 30

A corporation (“BPC”), which was mostly owned by a Canadian pension fund (“OMERS”), obtained the agreement of a predecessor of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(d) | s. 88(1)(d) bump is intended to permit the transfer of ACB that otherwise would be lost to another property that is taxed in the same way | 371 |

| Tax Topics - Income Tax Act - Section 98 - Subsection 98(3) - Paragraph 98(3)(c) | s. 98(3)(c) bump is intended to avoid gain realization where there has been no economic gain | 267 |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(11) | 3-year time limitation in s. 69(11) did not establish safe harbor for avoidance of recapture on sale after that period | 382 |

| Tax Topics - Income Tax Act - Section 100 - Subsection 100(1) | purpose is to ensure that latent recapture will be recognized on sale to tax exempt | 254 |

| Tax Topics - Income Tax Act - Section 97 - Subsection 97(2) | object includes ultimate taxation of the deferred gain | 234 |

| Tax Topics - Income Tax Act - Section 171 - Subsection 171(1) | GAAR question as to determining a provision’s object was subject to correctness standard | 169 |

| Tax Topics - Statutory Interpretation - Hansard, explanatory notes, etc. | statement that amendment was for “clarification” was self-serving | 209 |

| Tax Topics - Statutory Interpretation - Interpretation Act - Subsection 45(2) | determination of whether amendment merely clarified requires review of pre-amendment state of law | 146 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(2) | consequential s. 245(2) adjustment must be scaled to the abuse | 391 |

GUY GERVAIS V. HER MAJESTY THE QUEEN, 2018 FCA 3

The taxpayer’s wife (Mrs. Gendron) purchased 1.04M preferred shares from the taxpayer (Mr. Gervais) at a cost of $1.04M (with Mr. Gervais...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 74.2 - Subsection 74.2(1) | purpose of ensuring that a gain deferred under interspousal rollover is attributed back to the transferor | 241 |

Univar Holdco Canada ULC v. Canada, 2017 FCA 207

A non-resident's acquisition of the shares of a Netherlands public company (Univar NV) indirectly holding the shares of a valuable Canadian...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.1 - Subsection 212.1(4) | using old s. 212.1(4) to extract surplus from a non-resident target’s Canadian sub was not abusive | 371 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(2) | the result achieved (no s. 212.1 withholding) accorded with the underlying policy of permitting surplus stripping as part of an arm’s length acquisition | 109 |

Canada v. Superior Plus Corp., 2015 DTC 5118 [at at 6319], 2015 FCA 241, aff'g 2015 TCC 132

The Superior Plus Income Fund (the "Fund") effectively converted (in accordance with the distribution method contemplated under s. 107(3.1)) into...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Solicitor-Client Privilege | non-tax legal opinion produced on discovery which potentially supported a GAAR argument did not entail implied waiver of tax memos until used in evidence | 200 |

Inter-Leasing, Inc. v. Ontario (Revenue), 2014 ONCA 575

In order to minimize provincial income tax, a Canadian corporate group restructured so that various intercompany debts were owing (on a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 115 - Subsection 115(1) - Paragraph 115(1)(a) - Subparagraph 115(1)(a)(ii) | holding intercompany loans was not a business, corporate objects presumption not applied | 366 |

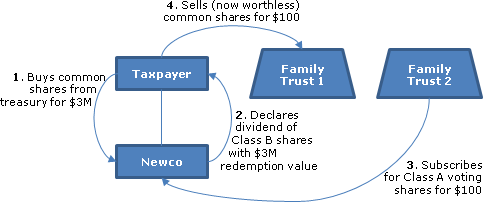

Canada v. Global Equity Fund Ltd., 2013 DTC 5007 [at 5526], 2012 FCA 272

{kind=link}

The taxpayer subscribed for common shares of a new subsidiary for approximately $5.6 million, which then declared a stock dividend in the form of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(9) | on appeal to FCA, Crown could not introduce new arguments that required further evidence | 295 |

1207192 Ontario Limited v. Canada, 2012 DTC 5157 [at at 7396], 2012 FCA 259, aff'g 2011 DTC 1301 [at 1686], 2011 TCC 383

{kind=link}

This was a companion case to Triad Gestco.

The taxpayer, which had realized a capital gain of $2,974,386, transferred cash and marketable...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | purpose objectively determined | 141 |

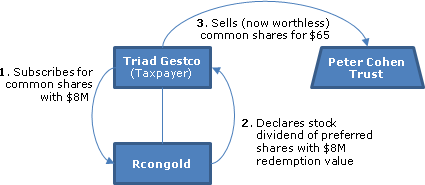

Triad Gestco Ltd. v. Canada, 2012 DTC 5156 [at at 7385], 2012 FCA 258

{kind=link}

The taxpayer, which was directed and controlled by Mr. Cohen, and which had realized a capital gain of approximately $8 million, transferred $8...

Canada Safeway v. Alberta, 2012 DTC 5133 [at at 7271], 2012 ABCA 232

This case was a companion decision to Husky Energy.

{kind=link}

An Alberta taxpayer ("CSL") borrowed $600 million from its Alberta parent ("CSHL") over the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | focus on whether individual transactions are avoidance transactions | 139 |

Husky Energy v. Alberta, 2012 DTC 5132 [at at 7262], 2012 ABCA 231

{kind=link}

Copthorne Holdings Ltd. v. Canada, 2012 DTC 5006 [at at 6536], 2011 SCC 63, [2011] 3 S.C.R. 721

The ultimate controlling family members decided that a Canadian subsidiary ("Copthorne I") should be amalgamated with a wholly-owned subsidiary of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Stare Decisis | high threshold for reversing not met | 193 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(1) - Tax Benefit | tax benefit illuminated by comparison to reasonable and simpler alternative | 425 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | "in contemplation" could be retrospective | 341 |

| Tax Topics - Statutory Interpretation - Expressio Unius est Exclusio Alterius | implied exclusion principle | 109 |

St. Michael Trust Corp. v. Canada, 2010 DTC 5189 [at at 7361], 2010 FCA 309, aff'd sub nom Fundy Settlement v. Canada, 2012 DTC 5063 [at 6881], 2012 SCC 14

After finding against the taxpayers on the grounds inter alia that two Barbados trusts were resident in Canada, Sharlow, J.A. found that if...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 94 - old | 209 | |

| Tax Topics - Treaties - Income Tax Conventions - Article 4 | 86 |

Lehigh Cement Limited v. Canada, 2010 DTC 5081 [at at 6844], 2010 FCA 124

After the terms of the debt owing by the taxpayer to a non-resident affiliate were amended so that they would comply with various requirements of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Legislative History | 90 |

Canada v. Remai, 2009 DTC 5188 [at at 6257], 2009 FCA 340

In order to make promissory notes that he had donated to a charitable foundation cease to be non-qualifying securities, the taxpayer arranged for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | providing a favour is consistent with arm's length dealing | 222 |

| Tax Topics - Statutory Interpretation - Redundancy/ reading in words/ speaking in vain | provision not to be interpreted such that it can never apply | 40 |

Collins & Aikman Products Co. v. The Queen, 2009 DTC 1179 [at at 958], 2009 TCC 299, aff'd 2010 DTC 5164 [at 7293], 2010 FCA 251

The taxpayer ("Products"), which was a corporation resident in the U.S., transferred the shares of its subsidiary ("CAHL"), which was non-resident...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Payment & Receipt | payment by direction | 142 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(1.12) | 190 | |

| Tax Topics - Statutory Interpretation - Retroactivity/Retrospectivity | 72 |

Canada v. Landrus, 2009 DTC 5085 [at at 5840], 2009 FCA 113

A partnership of which the taxpayer was a member ("Roseland II") and another partnership ("Roseland I") owning a similar and adjacent condominium...

Lipson v. Canada, 2009 DTC 5528, 2009 SCC 1, [2009] 1 S.C.R. 3

The taxpayer's wife ("Jordanna") borrowed $562,500 from the Bank of Montreal under an interest-bearing demand promissory note in order to purchase...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 74.1 - Subsection 74.1(1) | purpose of attribution rules: preventing use of related-person status to reduce tax when transferring property/attribution of interest expense | 248 |

Canada v. MIL (Investments) S.A., 2007 DTC 5437, 2007 FCA 236

In March 1993 an individual ("Boulle") transferred his shares of a Canadian public junior exploration company ("DFR") to the taxpayer, which was a...

Mathew v. Canada, 2005 DTC 5538, 2005 SCC 55, [2005] 2 S.C.R. 643

An insolvent trust company ("STC") transferred a portfolio of mortgages with unrealized losses to a partnership of which a wholly-owned subsidiary...

Canada Trustco Mortgage Co. v. Canada, 2005 SCC 54, [2005] 2 S.C.R. 601, 2005 DTC 5523

The taxpayer purchased trailers from the U.S. user of the trailers ("TLI"), with the taxpayer appointing TLI as its agent to hold title on its...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(1) - Tax Benefit | tax benefit if taxable income reduction or on basis of comparison to alternative | 132 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | "in contemplation" references "because of" or "in relation to" | 127 |

| Tax Topics - Statutory Interpretation - Certainty | interpretive approach should be consistent with tax law being certain, predictable and fair, | 131 |

| Tax Topics - Statutory Interpretation - Ordinary Meaning | primacy to ordinary meaning if unequivocal | 96 |

Canada v. Imperial Oil Ltd., 2004 DTC 6044, 2004 FCA 36

The Court affirmed the finding of the Tax Court that the claiming of an investment allowance by the taxpayer on short-term loans made by it close...

Canada v. Produits Forestiers Donohue Inc., 2003 DTC 5471, 2002 FCA 422

In order to realize an allowable business investment loss on its investment in a corporation ("DMI") held jointly by it and a third party...

Novopharm Ltd. v. Canada, 2003 DTC 5195, 2003 FCA 112

A profitable Canadian corporation ("Novopharm") acquired losses approximating $20 million of an arm's-length corporation ("Lossco") through a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | borrowing to receive deemed dividend | 352 |

Canada v. Canadian Pacific Ltd., 2002 DTC 6742, [2002] 3 F.C. 170, 2002 FCA 98

The taxpayer borrowed 216 million in Australian dollars under debentures bearing interest at 16.125% per annum and that had been issued at a 2%...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | primary purpose of a borrowing in a tax-advantageous currency was to raise money | 290 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(1) - Transaction | an aspect of a transaction is not a transaction | 249 |

OSFC Holdings Ltd. v. Canada, 2001 DTC 5471, 2001 FCA 260

After becoming insolvent, a company ("Standard") in the mortgages business established a partnership, transferred a mortgage portfolio to the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | significant disparity between tax benefit and commercial return from transaction | 263 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | s. 248(10) assimilates a subsequent transaction to a common-law series if it has some connection with the series and is completed in contemplation thereof | 344 |

| Tax Topics - Statutory Interpretation - Interpretation Bulletins, etc. | 70 | |

| Tax Topics - Statutory Interpretation - Interpretation/Definition Provisions | deeming v. definition provisions | 46 |

Longley v. Minister of National Revenue, 99 DTC 5549, [1999] 4 CTC 108 (B.C.S.C.)

Quijano J. found that GAAR would not apply to an arrangement under which taxpayers made contributions to a fringe political party on the basis...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Hansard, explanatory notes, etc. | 69 |

See Also

Somerset Limited v. The King, 2026 TCC 123

The taxpayer, which had been a B.C. corporation and a Canadian resident since its incorporation in 1943, sought to cease being a “Canadian...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Canadian corporation | BC corp that had been continuously resident in Canada from 1943 and then continued to BVI would qualify under (b) as a foreign incorporation that was continuously resident | 312 |

Wuswig Inc. v. The King, 2025 TCC 147

The taxpayer (“Wuswig”), a CBCA corporation, wholly owned a U.S. holding company (“Southridge Holdings”), whose shares had an accrued...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(1.11) | notice of determination issued for a statute-barred year was valid given inter alia that the tax assessed was for non-statute-barred years | 204 |

D'Arcy v. The King, 2025 TCC 128

The individual taxpayers, who equally owned the shares, being common shares, of an operating company, Tech/Pro, with a nominal paid-up capital...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) | PUC averaging to permit the extraction of PUC in excess of the individuals’ investment in the corporation was abusive | 220 |

Harvard Properties Inc. v. The King, 2024 TCC 139

A Calgary shopping mall was sold by Harvard Properties and the other co-owners to a third party (“Abacus”) in a share sale transaction but at...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | sale of shares, in a structured transaction, at a price that did not reflect a discount for the underlying accrued taxes, was indicative of non-arm's length dealing | 643 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | transaction premium to a share-sale valuation was not reflective of ordinary commercial dealings | 431 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(2) | GAAR alternative basis was not statute-barred where the primary assessment (under s. 160(2)) was not subject to statute-barring | 197 |

| Tax Topics - General Concepts - Fair Market Value - Shares | shares of company whose only assets were escrowed for an imminently-closing sale transaction did not have any value | 285 |

Lark Investments Inc. v. The King, 2024 TCC 30

A week before realizing a $119 million capital gain, the taxpayer, which until then was wholly-owned by a Canadian-resident individual, issued...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Other Legislation/Constitution - Federal - Tax Court of Canada Rules (General Procedure) - Section 63 | Crown’s vague pleading that GAAR applied to convert a CCPC to non-CCPC was struck, but with leave to amend | 251 |

| Tax Topics - Other Legislation/Constitution - Federal - Tax Court of Canada Rules (General Procedure) - Section 8 | fresh start rule inapplicable where defects in Crown’s pleading did not become apparent until a subsequent procedural stage | 230 |

| Tax Topics - Income Tax Act - Section 169 - Subsection 169(1) | process behind assessment not relevant to its validity | 100 |

ARQ v. Kone Inc., 2024 QCCA 678

The taxpayer (“KQI”), a Canadian operating subsidiary in the Kone multinational group, used group funds advanced to it by a group company...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Sham | agreement to treat a repo as a loan for US tax purposes did not support “sham” | 237 |

DAC Investment Holdings Inc. v. The King, 2024 TCC 63, rev'd 2026 FCA 35

With a view to its imminent disposition of the shares of a subsidiary which it had acquired on a rollover basis, the taxpayer continued to the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 123.3 | object of s. 123.3 was to impose refundable tax only on CCPCs | 214 |

| Tax Topics - Income Tax Act - Section 123.4 - Subsection 123.4(1) - Full Rate Taxable Income - Paragraph (b) - Subparagraph (b)(iii) | rate reduction for investment income was intended to apply to non-CCPCs since they did not enjoy refundable tax | 253 |

| Tax Topics - Income Tax Act - Section 250 - Subsection 250(5.1) | rationale of s. 250(5.1) is to equate the place of continuance of a corporation with its place of incorporation | 205 |

DEML Investments Limited v. The King, 2024 TCC 27, rev'd in part 2025 FCA 204

In early 2008, the sale of petroleum and natural gas (PNG) rights by an arm’s length vendor (Transglobe) to the parent (Direct Energy) of the...

Total Energy Services Inc., 2024 TCC 12

In September, 2007, most of the equity of an insolvent public corporation (“Xillix”) was acquired by the company (“Nexia”) of two...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(5) | s. 256(7)(c.1) merely clarified that the acquisition of a public company lossco by a SIFT trust was an abuse of s. 111(5) | 326 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | acquisition of loss company and its merger with a loss user 1 ½ years later were part of the same series | 230 |

Madison Pacific Properties Inc. v. The King, 2023 TCC 180

The appellant (“MPP”) was an insolvent, publicly traded, mining company with accumulated net capital losses of $72.7 million. In order for two...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(4) | two acquirers of most of the equity of a Lossco were acting in concert so as to constitute a group | 465 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(1) - Tax Benefit | in the alternative transaction, two acquirers of the shares of a Lossco would have been acting in concert so as to be a group that acquired control of the Lossco | 291 |

Husky Energy Inc. v. The King, 2023 TCC 167, aff'd sub nomine Hutchison Whampoa Luxembourg Holdings S.À R.L. 2025 FCA 176

Before a Canadian public corporation (“Husky”) paid a dividend on its shares, two significant shareholders of Husky resident in Barbados (the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 10 | recipient of dividends on borrowed shares was not their beneficial owner because of requirement to pay dividend compensation payments | 270 |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(2) | tax under s. 212(2) imposed on the basis of payment of dividend to a non-resident rather than on the basis of who is the beneficial owner | 405 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(1) - Tax Benefit | no tax benefit under s. 215(6) from targeted reduced rate of dividend withholding if in base transaction, the Canadian dividend payer would have withheld at the higher rate | 347 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | transactions were carried out to reduce Part XIII tax rather than avoid Barbados income tax | 131 |

Québecor Inc. v. The King, 2023 TCC 142

In December 2005, the appellant (“Québecor”) held 54.72% of the shares of another holding company (“Québecor Media”) which, in turn,...

Kone Inc. v. ARQ, 2022 QCCQ 9892, aff'd 2024 QCCA 678

The taxpayer (“KQI”), which was a resident Canadian corporation engaged in an elevator and escalator installation and repair business and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Sham | substance of a repo as a secured loan for US tax purposes did not establish that it was a sham | 309 |

Mony v. The King, 2022 TCC 120

The taxpayer, agreed to sell his shares of a Canadian-controlled private corporation (“Créaform”), having a nominal ACB, to third parties. On...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | transaction can be chosen to be more tax-advantageous than an alternative, and still not be an avoidance transaction – but here, a transaction was effected solely for tax reasons | 467 |

Frucor Suntory New Zealand Limited v Commissioner of Inland Revenue, [2022] NZSC 113

In January 2002, a New Zealand “Buyco” (DHNZ) in the Danone group had acquired a NZ target company. In March 2003, in connection with the...

Coopers Park Real Estate Development Corporation v. The Queen, 2022 TCC 82

The taxpayer, which had been assessed under s. 245(2) to deny the carryforward of losses and credits, sought the discovery of proposals made by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Other Legislation/Constitution - Federal - Tax Court of Canada Rules (General Procedure) - Section 83 - Subsection 83(1) | documents reviewed by the GAAR Committee, in a similar case that then was applied to the taxpayer, were discoverable | 454 |

3295940 Canada Inc. v. The Queen, 2022 TCC 68, rev'd 2024 FCA 42

Following preliminary transactions, on June 28, 2004, a Canadian holding company (“Micsau”) held all the shares, having a fair market value...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 83 - Subsection 83(2) | use of capital dividend to avoid s. 55(2) abused the capital dividend system | 533 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(d.2) | indirect use of high outside basis in the taxpayer’s shares as compared to basis in shares sold by it was contrary to the policy of prohibiting a bump of the inside basis | 195 |

Magren Holdings Ltd. v. The Queen, 2021 TCC 42, aff'd on other grounds 2024 FCA 202

The appellants engaged in transactions which were intended to result in the realization by them of substantial capital gains (resulting in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 185 - Subsection 185(3) | Part III tax assessments of distributions of gains that were denied outside the Part I tax normal reassessment period were not statute-barred | 314 |

| Tax Topics - Income Tax Act - Section 185 - Subsection 185(1) | no requirement to issue separate assessment for each election, and no remedy for inordinate time to issue assessments | 396 |

| Tax Topics - General Concepts - Ownership | acquisition of income fund units to be held for a few days before their redemption did not represent an acquisition of beneficial ownership | 549 |

| Tax Topics - General Concepts - Sham | transactions did not result in real capital losses | 306 |

| Tax Topics - Income Tax Act - Section 184 - Subsection 184(3) | election was not available where a CDA sham | 365 |

Grenon v. The Queen, 2021 TCC 30, aff'd in part 2025 FCA 129

In order that the taxpayer’s RRSP could indirectly invest in operating businesses in which he and/or two business colleagues had a management...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 4801 - Paragraph 4801(a) - Subparagraph 4801(a)(i) - Clause 4801(a)(i)(A) | distribution of units that included significant purchases by minors and by adults who did not pay for their own units, was unlawful | 756 |

| Tax Topics - Income Tax Act - Section 204.2 - Subsection 204.2(1.1) | alleged distribution from non-qualified investment was not an over-contribution | 277 |

| Tax Topics - General Concepts - Window Dressing | window-dressing is a deception about intention | 312 |

| Tax Topics - Income Tax Act - Section 207.1 - Subsection 207.1(1) | non-qualified investments not “included” in annuitant’s income because it was never assessed | 346 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4) | CRA’s assessing listed taxable RRSPs in a T3GR global return was not of the taxpayer’s (also listed) RRSP /inappropriate reliance in legal opinion on certificate of fact was carelessness | 441 |

| Tax Topics - Income Tax Act - Section 207.2 - Subsection 207.2(3) | CRA’s assessment of Pt. XI.1 shown on the T3GR for all RRSPs of one type did not start the normal reassessment period for the taxpayer’s RRSP since no tax shown for it | 370 |

| Tax Topics - Income Tax Regulations - Regulation 4900 - Subsection 4900(1) - Paragraph 4900(1)(d.2) | distribution was not lawful because the issuer had not complied with the OM exemption, which was the exemption that it had chosen to rely on | 290 |

MMV Capital Partners Inc. v. The Queen, 2020 TCC 82, rev'd 2023 FCA 234

A venture capital corporation (“MMV Finance”) was issued, early in 2011, voting common shares of a corporation (“MMV”) (that was in...

Rogers Enterprises (2015) Inc. v. The Queen, 2020 TCC 92

To simplify somewhat, a group of private corporations owned for the benefit of the Rogers family structured their affairs such that one...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(1) - Tax Benefit | no tax benefit where alleged excessive CDA addition was not distributed to individual shareholders | 498 |

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Capital Dividend Account - Paragraph (d) - Subparagraph (d)(iii) | 2016 amendment changed the law so as to reduce CDA bump by policyholder’s ACB | 259 |

Deans Knight Income Corporation v. The Queen, 2019 TCC 76, rev'd 2021 FCA 160

The “Tax Attributes” of a Lossco (the taxpayer) were effectively sold to arm’s length investors pursuant to transactions under which:

- The...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(5) - Paragraph 251(5)(b) - Subparagraph 251(5)(b)(i) | 3rd party was expected to, but could not require, an acquisition of voting control | 589 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(8) | loss streaming rules are conditioned on an acquisition of effective control | 132 |

Gladwin Realty Corporation v. The Queen, 2019 TCC 62, aff'd 2020 FCA 142

The taxpayer, which carried on a commercial real estate business and had September 30 year ends, transferred on a s. 97(2) rollover basis a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Capital Dividend Account - Paragraph (a) | contrary to purpose of the capital dividend rules to fully exempt a capital gains distribution | 300 |

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(3.1) | purpose of s. 40(3.1) is to trigger gain on extraction of excess funds by passive partners | 330 |

| Tax Topics - Income Tax Act - Section 123.3 | no CRA challenge to continuance to BVI to avoid s. 123.3 tax | 96 |

Les Développements Iberville Ltée v. Agence du Revenu du Québec, 2018 QCCA 1886 (Quebec Court of Appeal)

Three affiliated Quebec corporations (Développements, Location and Estrie) would have realized gains totaling $728.9 million (plus recapture of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) | abuse of Quebec equivalents of ss. 85(1) and 97(2) to avoid (rather than defer) tax | 420 |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Real Estate | property bifurcated between capital and income portion on acquisition | 98 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Improvements v. Repairs or Running Expense | improvements to leased retail premises were not demonstrated to be made only at tenants’ requests | 106 |

| Tax Topics - Income Tax Regulations - Regulation 402 - Subsection 402(6) | purpose of inter-provincial allocation rules is for 100% of income to be allocated and taxed | 558 |

| Tax Topics - Income Tax Act - Section 249.1 - Subsection 249.1(1) | no policy of permitting differing Quebec and federal year ends | 196 |

Loblaw Financial Holdings Inc. v. The Queen, 2018 TCC 182, rev'd on s. 95(1) - investment business - (a) (arm's length conduct) grounds 2020 FCA 79, in turn aff'd 2021 SCC 51

The taxpayer, an indirect wholly-owned subsidiary of Loblaws (a Canadian public company), wholly-owned a Barbados subsidiary (GBL), that was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 165 - Subsection 165(1.11) | requirement met where Crown knew the nature and quantum of the dispute | 269 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Bank | CFA qualified as a foreign bank since it was licensed under Barbados law as an international bank | 123 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Investment Business - Paragraph (a) | Barbados-licensed international bank, which used Loblaw funding to invest responsively to Loblaw considerations, conducted an offside non-arm’s length business | 429 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Investment Business - Paragraph (c) | employee equivalents was reduced by employee time described in s. 95(2)(b) | 290 |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Foreign Exchange | short-term debt securities were inventory because they were the raw material for generating swap income | 130 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4.01) - Paragraph 152(4.01)(a) - Subparagraph 152(4.01)(a)(ii) | GAAR is generally a separate matter rather than being subsumed in the allegedly-misused substantive provision | 208 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | application of GAAR required the occurrence of an avoidance transaction (or series) in non-statute-barred years and the relevant previous year’s avoidance transaction did not occur as part of the series | 512 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | hiring of employees 15-years previously to engage foreign bank exception to investment business definition was not part of same series as renewal of foreign bank licence | 228 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(l) | purpose of s. 95(2)(l) exception was to permit non-resident subsidiaries of Canadian banks and dealers to compete internationally | 190 |

Custeau v. Agence du revenu du Québec, 2018 QCCQ 5692, aff'd 2020 QCCA 1496

When the taxpayers’ corporation (“Opco”), a small business corporation, was in financial difficulty, a Quebec regional development fund...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | generation and subsequent use of PUC exceeding taxpayers’ invested capital were not avoidance transactions as this generation was imposed by arm’s length investor | 585 |

Alta Energy Luxembourg S.A.R.L. v The Queen, 2018 TCC 152, aff'd 2020 FCA 43, aff'd 2021 SCC 49

A Blackstone LP and a U.S. shale company held their investment in a Canadian subsidiary (Alta Canada), that was to develop a shale formation in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 13 | a large exploration property in which only six wells had been drilled qualified as immovable property used in the business | 400 |

| Tax Topics - Statutory Interpretation - Interpretation Bulletins, etc. | taxpayers should be able to rely on CRA position in making a capital investment | 125 |

9199-3899 Québec inc. v. Agence du revenu du Québec, 2017 QCCA 1524

In order to reduce Quebec capital tax, the taxpayer lent $350M on a non-interest-bearing basis to its parent on January 27, 2005, and claimed this...

Birchcliff Energy Ltd. v. The Queen, 2017 TCC 234

A newly-launched public corporation ("Birchcliff") sought to access the losses of a lossco ("Veracel") in order to shelter the profits from...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Sham | ephemeral transactions under a Plan of Arrangement were not a sham | 215 |

| Tax Topics - Income Tax Act - Section 251.2 - Subsection 251.2(2) - Paragraph 251.2(2)(a) | proxy which accorded no discretion to a class of shareholders did not render them a group | 221 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | series of transactions found to be an avoidance transaction | 306 |

2763478 Canada Inc. v. The Queen, 2017 TCC 98, aff'd 2018 CAF 209

An individual did not sell his shares of an operating company (Groupe AST) directly to a third-party purchaser. Instead he rolled his shares into...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | not every transaction had estate-freezing objective | 312 |

Fiducie Financière Satoma v. The Queen, 2017 TCC 84, aff'd 2018 FCA 74

$6.3 million in funds was extracted from a private operating company (“Gennium”) by paying those dividends to a holding company (“9134”),...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(1) - Tax Benefit | tax benefit even though corporate surplus stripped in favour of family trust had not so far been distributed | 215 |

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(2) | s. 75(2) application ousts dividend inclusion to income recipient (in absence of GAAR) | 114 |

MP Western Properties Inc. v. The Queen, 2017 TCC 82, aff'd sub nomine Madison Pacific Properties Inc. v. Canada, 2019 FCA 19

Predecessors of the taxpayers had been acquired for their losses in transactions where less than 50% of their voting shares, but more than 90% of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Other Legislation/Constitution - Federal - Tax Court of Canada Rules (General Procedure) - Section 95 - Subsection 95(1) | Crown must produce all documents “considered by officials involved in or consulted during” a GAAR-related audit | 304 |

1245989 Alberta Ltd. v. The Queen, 2017 TCC 51, rev'd sub nom. Wild v. Canada, 2018 FCA 114

An individual (Mr. Wild) stepped up the adjusted cost base of his investment in a small business corporation (PWR) by transferring his PWR common...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) | the use of class PUC-averaging to bump the PUC of personally-held shares was an abuse of s. 84.1 | 701 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(5) | assessment of PUC without current income effect | 34 |

Veracity Capital Corp. v. The Queen, 2017 BCCA 3

The following transactions occurred under a KPMG-advised “Q-Yes” plan for the avoidance of 90% of the B.C. income tax that otherwise would...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Inserting Words | Crown's interpretation entailed the addition of words that were already in a closely related provision | 201 |

594710 British Columbia Ltd. v. The Queen, 2016 TCC 288, rev'd 2018 FCA 166

The taxpayer was a holding company and Canadian-controlled private corporation which wholly-owned a “Partnerco” holding a 24.975% limited...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | indirect transfer of property to taxpayer did not entail departure from FMV | 462 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(2) | GAAR reassessment must reflect the abuse | 315 |

| Tax Topics - Income Tax Act - Section 96 - Subsection 96(1) - Paragraph 96(1)(f) | LP profits can be allocated to purchasing partner at year end | 278 |

Pomerleau c. La Reine, 2016 TCC 228, aff'd 2018 FCA 129

An individual taxpayer engaged in a surplus-stripping transaction similar to transactions in a ruling which CRA had resiled from following...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2) - Paragraph 84.1(2)(a.1) | GAAR applied to converting soft ACB (generated from crystallizing the capital gains deduction) into pseudo-hard ACB under s. 53(1)(f.2) for use in extracting surplus | 717 |

Oxford Properties Group Inc. v. The Queen, 2016 TCC 204, rev'd 2018 FCA 30

A corporation (“BPC”), which was mostly owned by a Canadian pension fund (“OMERS”), obtained the agreement of a predecessor of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | subsequent sale part of series as it utilized the benefit of previous LP packaging and bump transactions | 387 |

| Tax Topics - Income Tax Act - Section 97 - Subsection 97(2) | purpose not to tax underlying recapture on subsequent LP unit sale | 431 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(d) | purpose: to push down ACB of shares of sub to qualifying non-depreciable property | 489 |

| Tax Topics - Statutory Interpretation - Interpretation Act - Subsection 45(2) | subsequent amendment shed light on scope of previous version | 107 |

| Tax Topics - Income Tax Act - Section 100 - Subsection 100(1) | S. 100 operates only on outside basis gain | 290 |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(11) | Parliament provided safe harbour for sales after 3 years | 204 |

| Tax Topics - Income Tax Act - Section 98 - Subsection 98(3) - Paragraph 98(3)(c) | purpose: to preserve high outside basis through push down | 293 |

Gervais v. The Queen, 2016 TCC 180, aff'd 2018 FCA 3

After a third party ("BW") had made an offer to purchase the shares of a Quebec manufacturing company ("Vulcain"), Mr. Gervais sold 1.04M Vulcain...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | comparison with outright sale and gift | 193 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(1) - Tax Benefit | benefit compared to straight sale and gift | 166 |

R. v. Golini, 2016 TCC 174

A family corporation (“Ontario”) used proceeds of a daylight loan to redeem shares of Holdco, which used those proceeds to purchase a life...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | a loan to a shareholder with recourse limited to an asset pledged by the corporation was a shareholder benefit | 589 |

| Tax Topics - General Concepts - Sham | sham doctrine did not apply to a "minor pretence" | 338 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | interest deduction on limited recourse loan | 305 |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(1) | policy of 84(1) | 219 |

Univar Holdco Canada ULC v. The Queen, 2016 TCC 159, rev'd 2017 FCA 207

An acquisition of the shares of a Netherlands public company indirectly holding the shares of a valuable Canadian sub (Univar Canada) with nominal...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.1 - Subsection 212.1(4) | creating a sandwich structure in order to access s. 212.1(4) was an abuse of the s. 212.1(1) anti-surplus stripping rule | 628 |

| Tax Topics - Statutory Interpretation - Interpretation Act - Subsection 45(3) | policy of current version of s. 212.1(4) confirmed by proposed amendment | 142 |

Veracity Capital Corporation v. M.N.R., 2015 DTC 5136 [at 6421], 2015 BCSC 2278, rev'd 2017 BCCA 3

The following transactions occurred under a KPMG-advised plan in order to avoid 90% of the B.C. income tax that otherwise would have been payable...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | investment in LP units with 7.2% return was primarily for tax avoidance reasons/year end selections were avoidance transactions | 491 |

Birchcliff Energy Ltd. v. The Queen, 2015 TCC 232, nullified on procedural grounds 2017 FCA 89

Shortly after it became a public company, a predecessor ("Birchcliff") of the taxpayer entered into an agreement for a major acquisition of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Sham | transitory share issuance under plan of arrangement was not a sham | 177 |

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(5) - Paragraph 111(5)(a) | grant of proxy did not detract from investors acting individually in own interest | 237 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | share subscription was avoidance transaction notwithstanding its "overarching purpose" was financing | 148 |

HMRC v Pendragon plc, [2015] UKSC 37

A scheme, which exploited a UK VAT rule which was intended to avoid double-taxation, so as to avoid tax, was found to be abusive. See summary...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 274 - Subsection 274(4) | scheme, exploiting a rule intended to avoid double-taxation so as to avoid tax, was abusive | 755 |

Superior Plus Corp. v. The Queen, 2015 DTC 1124 [at at 765], 2015 TCC 132, aff'd 2015 FCA 241

The Superior Plus Income Fund (the "Fund") effectively converted (in accordance with the distribution method contemplated under s. 107(3.1)) into...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Solicitor-Client Privilege | disclosure of commercial legal opinion did not entail waiver of privilege for tax legal opinions | 145 |

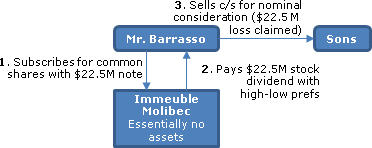

Barrasso v. The Queen, 2014 TCC 156

{kind=link}

The taxpayer, who had realized a capital gain of $30 million earlier in the year, subscribed for Class A common shares of a corporation newly...

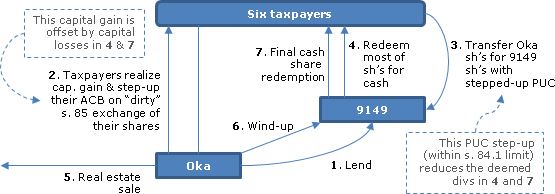

Descarries v. The Queen, 2014 DTC 1143 [at at 3412], 2014 TCC 75 (Informal Procedure)

{kind=link}

The six taxpayers, who were siblings (or a step-daughter of their deceased father), held all the shares, having an aggregate fair market value...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 171 - Subsection 171(1) | free to raise an interpretation not advanced by either party | 83 |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | holdco distribution made out of loan from still-operating sub - s. 84(2) did not apply | 521 |

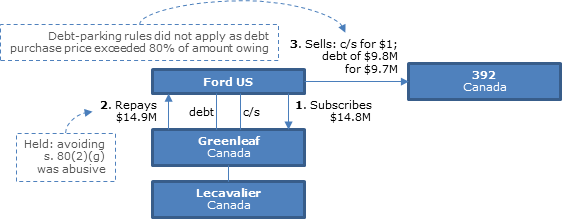

Pièces automobiles Lecavalier Inc. v. The Queen, 2014 DTC 1126, 2013 TCC 310

{kind=link}

A Canadian subsidiary ("Greenleaf") of Ford U.S. paid down to $9,750,000 (including accrued interest) a debt of $24,369,439 (plus accrued...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Evidence | Canadian tax accountant's testimony on US tax consequences accorded little weight | 152 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | debt-paydown transactions were avoidance transactions | 268 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | debt-paydown transactions effected in contemplation of sale transaction were part of same series as the sales transactions | 248 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(2) - Paragraph 80(2)(g) | using cash share subscriptions to convert debt to share equity abused s. 80(2)(g) | 190 |

Gwartz v. The Queen, 2013 DTC 1122 [at at 640], 2013 TCC 86

{kind=link}

The taxpayers ("Brianne and Steven") were minors and beneficiaries of a family trust (the "Trust"). The Trust held all the common shares (as...

Swirsky v. The Queen, 2013 TCC 73, 2013 DTC 1078 [at at 431], aff'd 2014 FCA 36

Paris J. noted obiter (at para. 75) that Overs v. The Queen, 2006 TCC 26, "has been implicitly overruled by the Lipson decision."

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | 232 | |

| Tax Topics - Income Tax Act - Section 74.5 - Subsection 74.5(11) | 247 |

MacDonald v. The Queen, 2012 TCC 123, rev'd 2013 DTC 5091 [at 5982], 2013 FCA 110

The taxpayer planned to move to the U.S.. Although the capital gain on the shares of his wholly owned corporation ("PC") that would have arisen...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(1) - Tax Benefit | 306 | |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | 354 |

Antle v. The Queen, 2009 DTC 1305, 2009 TCC 465, aff'd 2010 DTC 5172 [at 7304], 2010 FCA 280

A plan for the taxpayer to avoid capital gains on his sale of shares of a corporation ("PM") would have entailed him gifting the shares to a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 250 - Subsection 250(5) | 132 |

Garron Family Trust v. The Queen, 2009 DTC 1568, 2009 TCC 450, aff'd sub nom St. Michael Trust Corp. v. The Queen, 2010 DTC 5189 [at 7361], 2010 FCA 309, aff'd sub nom Fundy Settlement v. Canada, 2012 SCC 14

Woods, J. rejected a submission of the Crown that it would have represented an abuse of the Canada-Barbados Income Tax Convention to use the gains...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(2) | 130 |

OGT Holdings Ltd. v. Deputy Minister of Revenue (Québec), 2009 DTC 5705, 2009 QCCA 191

The taxpayers engaged in a "Québec shuffle" transaction in which they transferred shares of subsidiaries to a related Ontario purchaser on a...

Landrus v. The Queen, 2008 DTC 3583, 2008 TCC 274, aff'd supra.

A partnership of which the taxpayer was a member ("Roseland II") and another partnership ("Roseland I") owning a similar and adjacent condominium...

McMullen v. The Queen, 2007 DTC 286, 2007 TCC 16

The taxpayer and an unrelated individual ("DeBruyn") accomplished a split-up of the business of a corporation ("DEL") of which they were equal...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | 270 | |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | mutual benefit and same advisors insufficient to establish non-arm's length in structured sale transaction | 257 |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | 229 | |

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) | arm's length: negotiation based on self-interest | 257 |

Ogt Holdings Ltd. v. Deputy Minister of Revenue of Québec, 2006 DTC 6604 (Court of Québec)

The taxpayers accomplished an indirect sale of their indirect investment in an operating company ("Canstar") to an arm's length purchaser ("Nike")...

Ceco Operations Ltd. v. The Queen, 2006 DTC 3006, 2006 TCC 256

The taxpayer transferred assets of a business to a partnership in what was intended to be an s. 97(2) rollover transactions in consideration for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Substance | 99 | |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | 265 | |

| Tax Topics - Income Tax Act - Section 97 - Subsection 97(2) | partnership subscription for taxpayer affiliate pref shares not boot | 263 |

Lipson v. The Queen, 2006 DTC 2687, 2006 TCC 148, aff'd supra.

The taxpayer's wife ("Jordanna") borrowed $562,500 from the Bank of Montreal to fund the purchase of shares of a family company from the taxpayer...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | 251 |

Desmarais v. The Queen, 2006 DTC 2376, 2006 TCC 44

The taxpayer, who held 14.28% of the common shares of a Canadian private corporation ("Consercom") transferred a 9.76% block to a wholly-owned...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | 136 |

Evans v. The Queen, 2005 DTC 1762, 2005 TCC 684

A corporation ("117679") owned by the taxpayer issued a stock dividend of non-voting shares to the taxpayer that were redeemable and retractable...

XCO Investments Ltd. v. The Queen, 2005 DTC 1731, 2005 TCC 655

A partnership owned by the taxpayers admitted a third party ("Woodward") as a member of the partnership with a view to selling an apartment...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 103 - Subsection 103(1) | 130 | |

| Tax Topics - Income Tax Act - Section 96 - Subsection 96(1) - Paragraph 96(1)(f) | 105 |

Canada v. Jabin Investments Ltd., 2003 DTC 5027, 2002 FCA 520

In order to avoid the application of the pre-1994 version of section 80, debt owing by the taxpayer was sold by a bank (for consideration equal to...

Loyens v. The Queen, 2003 DTC 355, 2003 TCC 214

In order that the sale of a real estate property could be accomplished in a manner that utilized the losses of a loss company ("Lobro Stables")...

Hill v. The Queen, 2002 DTC 1749 (TCC)

Under a non-recourse loan owing by the taxpayer and other tenants of an office building to the non-resident landlord, 90% of the cash flow was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Payment & Receipt | funds to support cheques | 143 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | 213 |

Fredette v. The Queen, 2001 DTC 621 (TCC)

A partnership ("SDF") of which the taxpayer and two trusts for his children were the partners owned substantially all the units in a second...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Ownership | 99 | |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Income-Producing Purpose | 91 |

Geransky v. The Queen, 2001 DTC 243 (TCC)

The taxpayer, who owned a portion of the shares of the holding company ("GH") which, in turn, owned an operating company ("GBC") utilized the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | holding company business was continued and underlying assets were not distributed | 307 |

Jabs Construction Ltd. v. R., 99 DTC 729, [1999] 3 CTC 2556

After it was determined as a result of settlement of litigation between the taxpayer and a co-venturer that it would sell its 50% interest in 13...

The Queen v. Central Supply Co. (1972) Ltd., 97 DTC 5295 (FCA)

The taxpayer acquired units in limited partnerships that had incurred Canadian exploration expense and then, within 24 hours and after the...

Gibson Petroleum Co. v. R., 97 DTC 1420, [1997] 3 C.T.C. 2453 (TCC)

The taxpayer which owned one-half of the shares of a company ("Wascana") having non-capital losses that were about to expire, transferred...

RMM Canadian Enterprises Inc. v. R., 97 DTC 302, [1998] 1 C.T.C. 2300 (TCC)

A non-resident corporation ("EC") approached a business associate who, along with two other individuals, formed a Canadian corporation ("RMM") to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 159 - Subsection 159(3) | 167 | |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | 188 | |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | purchaser of cash-rich company without any signifcant separate role did not deal at arm's length | 177 |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | application of s. 84(2) to sale of cash-rich company to accommodation party who quickly paid cash proceeds therefor | 222 |

| Tax Topics - Treaties - Income Tax Conventions | 96 | |

| Tax Topics - Treaties - Income Tax Conventions - Article 10 | 116 |

McNichol v. R., 97 DTC 111, [1997] 2 CTC 2088 (TCC)

The taxpayers sold their shares of a corporation ("Bec"), whose assets (following a sale of real estate) consisted largely of cash, to a corporate...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | 3rd-party purchaser, of cash-rich company, that looked to its own interests dealt at arm's length | 117 |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | 191 |

Administrative Policy

2 June 2026 STEP Roundtable, Q.9

The designations by the Minister of notifiable transactions under s. 237.4 in NT 2023-02 include transactions and series of transactions that seek...

2 December 2025 CTF Roundtable Q. 1, 2025-1080781C6 - Avoidance of subsection 80(3) on settlement of debt.

In Year 1, a corporation resident in Canada ("Parentco") made a $1,000 interest-free loan to its wholly owned Canadian subsidiary ("Subco") and,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 61.3 - Subsection 61.3(1) | use of s. 61.3 to avoid application of s. 80(13) notwithstanding transfer of NCLs to parent, was abusive | 330 |

9 October 2025 APFF Financial Planning Roundtable Q. 3, 2025-1068401C6 - Déductibilité des intérêts et règle générale anti-évitement

Folio S3-F6-C1 stated that a “taxpayer may restructure borrowings and the ownership of assets to meet the direct use test” under s. 20(1)(c). ...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) - Subparagraph 20(1)(c)(i) | restructuring to create direct income-producing use did not contravene GAAR | 115 |

CRA Webpage, General anti-avoidance rule (GAAR), 1 April 2026

The following are examples of tax avoidance schemes where in CRA’s view the GAAR would apply:

Surplus stripping

Transactions – Scenario 1 (use...

10 October 2024 APFF Roundtable Q. 16, 2024-1028961C6 F - Modification de la règle générale anti-évitement

CRA declined to provide further guidance on its interpretation of the GAAR following the introduction of s. 245(4.1), and reiterated some prior...

10 October 2024 APFF Roundtable Q. 13, 2024-1027371C6 - Planification post mortem à la suite du décès du bénéficiaire d’une fiducie testamentaire exclusive au conjoint

2012-0456221R3 concerned a spousal testamentary trust which held all the shares of a Canadian investment holding company (Holdco) on the death of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(5) | s. 69(5) wind-up of a Newco can be used by trust to realize a capital loss to offset a capital gain realized by it under s. 104(4)(a) | 309 |

| Tax Topics - Income Tax Act - Section 129 - Subsection 129(1.2) | non-application of s. 129(1.2) where post-mortem planning to prevent double taxation | 192 |

4 June 2024 STEP Roundtable Q. 5, 2024-1003541C6 - Post-Mortem Planning and GAAR

When asked to comment on post-mortem pipelines and s. 164(6) loss carryback plans in light of the amended version of GAAR, CRA referred to its...

29 April 2024 External T.I. 2024-1016011E5 - General Anti-Avoidance Rule

Regarding transactions (including non-arm’s length transactions) to crystalize accrued capital gains prior to June 25, 2024, CRA, after...

28 February 2024 Internal T.I. 2024-1008251I7 - IC 88-2 and new GAAR

Regarding the impact of the Bill C-59 GAAR amendments on the GAAR positions in IC 88-2 and IC 88-2 Supplement 1, CRA stated:

The potential...

29 February 2024 Internal T.I. 2023-0987941I7 - Amendments to GAAR and Advance Income Tax Rulings

Regarding the status of post-mortem pipeline transactions following the amended GAAR rule, the Directorate stated:

The Directorate does not...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | CRA after the GAAR amendments will continue to rule on post-mortem pipelines complying with its published policies, but not on inter vivos surplus stripping by individuals | 250 |

17 May 2022 IFA Roundtable Q. 12, 2022-0926361C6 - Principal Purpose Test (PPT)

Regarding Alta Energy, CRA stated:

The SCC considered a matter central to the CRA’s ongoing efforts to protect Canada’s tax base and the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Multilateral Instrument - Article 7 - Article 7(1) | CRA is monitoring PPT compliance on a priority basis | 317 |

7 October 2021 APFF Roundtable Q. 4, 2021-0900921C6 F - Mind and management et statut de SPCC

A corporation which will generate investment income is incorporated outside Canada (and, thus, is not a Canadian corporation, as per s. 89(1) and,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 123.3 | use of foreign corporation with central management and control in Canada to avoid s. 123.3 tax could be GAARable | 170 |

26 November 2020 STEP Roundtable Q. 12, 2020-0839981C6 - 21 year planning, 107(5) and TCP

In 2017-0724301C6, CRA indicated that it quite possibly was a GAARable circumvention of ss. 107(5) and (2.1) for a Canadian-resident discretionary...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107 - Subsection 107(5) | distributions by a Canadian discretionary trust to a NR-owned Canadian corporate beneficiary of TCP not carved-out in s. 107(5) appear abusive | 288 |

27 October 2020 CTF Roundtable Q. 1, 2020-0860991C6 - ACB increase due to misalignment of ACB

A wholly-owned subsidiary (Subco1) of Parentco effects an s. 55(3)(a) spin-off one of its assets (all the shares of Subco2) to Newco, which is...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(b) | GAAR may apply to spin-offs that effect a disproportionate distribution of high basis assets to the Spinco | 353 |

15 September 2020 IFA Roundtable Q. 6, 2020-0853561C6 - Subsection 212.3(9) & The GAAR

Canco (wholly-owned by NRco) acquired all the shares of FA1 for $100, thereby effecting a reduction of the paid-up capital (PUC) of the common...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(9) - Paragraph 212.3(9)(b) - Subparagraph 212.3(9)(b)(ii) | reinstatement arguably occurs on distributing shares of sub capitalized with daylight loan | 398 |

8 October 2010 Roundtable, 2010-0373621C6 F - Utilisation abusive des fiducies familiales

Examples of the abusive use of family trusts to which CRA has applied GAAR included:

- Capital gains are shifted off-shore through the use of...

8 October 2010 Roundtable, 2010-0373221C6 F - Paid-up capital

Opco, a Canadian-controlled private corporation owning and operating a seniors' residence, and whose shares (which are qualified small business...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) - Paragraph 245(3)(a) | transaction can be an avoidance transaction even where the series is motivated by business reasons | 142 |

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Paid-Up Capital - Paragraph (a) | abusive use of PUC averaging to shift PUC to individuals | 39 |

3 December 2019 CTF Roundtable Q. 13, 2019-0824491C6 - Triangular Amalgamation

In a domestic triangular amalgamation, in which the shareholders of Targetco receive shares of Parentco, and Parentco receives shares of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(9) - Paragraph 87(9)(a.4) | use of a “Midco” on triangular amalgamation “technically” avoids ss. 87(9)(a.4) and (c) limitation | 426 |

3 December 2019 CTF Roundtable Q. 6, 2019-0823581C6 - 21 year planning, 107(5), and TCP

CRA indicated that 2016-0669301C6 and 2017-0693321C6 dealt with an abusive circumvention of s. 104(5.8) through a s. 107(2) rollout by a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107 - Subsection 107(2) | a s. 107(2) rollout of Cdn Realtyco shares (i.e., TCP) to a NR-owned corporate beneficiary is inherently abusive | 255 |

6 February 2019 Internal T.I. 2018-0762101I7 - Ruling request - DSU plan and EPSP

A Canadian public company (Employerco) proposed that the share appreciation right (SAR) units of its employees be converted into an equivalent...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 144 - Subsection 144(3) | proposed use of EPSP trust to produce equivalent of CCPC stock option plan was abusive | 577 |

| Tax Topics - Income Tax Regulations - Regulation 6801 - Paragraph 6801(d) | conversion of SARs to DSUs triggered immediate inclusion under s. 6(1)(a) or 6(11) | 420 |

7 March 2019 CTF GAAR Seminar - Suzanne Saydeh on GAAR Committee

- The approach of the GAAR Committee to surplus-stripping has changed significantly. In 2015-0610701C6, CRA commented that, having regard to the...

7 March 2019 CTF Seminar on GAAR: Alexandra MacLean on GAAR

- If an audit team proposes raising GAAR, there is a mandatory referral to the Abusive Tax Avoidance Division at Headquarters. They do a rigorous...

Alexandra MacLean, "CRA Audits of Large Corporations - The view from ILBD" under Responses to recent adverse decisions – Univar, 27 November 27 2018 CTF Annual Conference presentation.

Univar found that the result of the cross-border surplus-stripping transactions before it could have been equally accomplished if the non-resident...

27 November 2018 CTF Roundtable Q. 5, 2018-0780041C6 - GAAR on PUC reduction

CRA provided two examples of when it would apply GAAR where paid up capital (“PUC”) is reduced to nil in order to avoid a s. 88(1)(b) gain on...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(b) | where Parent acquired the net tax equity in Subco at a bargain price (low share ACB), avoiding a s. 88(1)(b) gain on wind-up through reducing PUC is abusive | 548 |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(3) | no challenge of a reduction of PUC of shares of DC held by TC before redemption | 222 |

9 August 2016 Internal T.I. 2014-0526171I7 - Resettlement of a Trust

A non-resident common-law commercial trust had been settled with cash and Canadian real estate by two (apparently non-resident) corporations. A...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | sale of the two interests in a commercial trust to a 3rd party gave rise to a new trust given that this not contemplated when trust settled | 395 |

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(1) - Paragraph 111(1)(a) | constructive resettlement of trust on sale of beneficial interests therein extinguished its losses | 204 |

13 June 2017 STEP Roundtable Q. 2, 2017-0693321C6 - GAAR and 21-year planning