Subsection 115(1) - Non-resident’s taxable income in Canada

Paragraph 115(1)(a)

Subparagraph 115(1)(a)(i)

Cases

Hurd v. The Queen, 81 DTC 5140, [1981] CTC 209 (FCA)

The employment income referred to in s. 115(1)(a)(i) includes stock option benefits that are deemed by s. 7 to have been received by an employee...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 115 - Subsection 115(2) - Paragraph 115(2)(e) - Subparagraph 115(2)(e)(i) | 11 | |

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(4) | 95 | |

| Tax Topics - Treaties - Income Tax Conventions - Article 13 | meaning of exchange | 33 |

See Also

Martin v. The King, 2024 TCC 153

The taxpayers (two baseball players), who performed 40% of their duties in Canada rather than the US, agreed with the Toronto Blue Jays (the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Salary Deferral Arrangement | taxpayers' RCAs were not SDAs because they provided for reasonable pensions | 501 |

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(1) - Paragraph 6(1)(a) - Subparagraph 6(1)(a)(ii) | s. 6(1)(a)(ii) exclusion applied only after the computation of the non-resident taxpayers’ Canadian-source income | 531 |

| Tax Topics - Income Tax Act - Section 207.5 - Subsection 207.5(1) - Refundable Tax | overview of RCA rules | 222 |

| Tax Topics - Income Tax Act - Section 5 - Subsection 5(1) | RCA contributions would be employment income under ss. 5(1) or 6(1)(b) absent the s. 6(1)(a)(ii) exclusion | 393 |

| Tax Topics - Treaties - Income Tax Conventions - Article 15 | US baseball players were taxable only on their income generated in playing in Canada | 139 |

Blank v. Commissioner of Taxation, [2015] FCAFC 154, aff'd [2016] HCA 42

The taxpayer was employed by Glencore International AG (“GI”) or a subsidiary from November 1991 to December 2006, with his employment in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(1) - Paragraph 6(1)(a) | phantom profit participation unit amounts not income until paid by employer rather than when due | 737 |

| Tax Topics - General Concepts - Payment & Receipt | payments under phantom units not received when they vested | 344 |

Mullen v. The Queen, 2012 DTC 1154 [at at 3358], 2012 TCC 139 (Informal Procedure)

The taxpayer's exercise of stock options while he was resident in China gave rise to taxable income in Canada because he had received those stock...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4) - Paragraph 152(4)(a) - Subparagraph 152(4)(a)(i) | non-residence claim was implausible | 199 |

| Tax Topics - Income Tax Act - Section 163 - Subsection 163(2) | superficial attempt to change residence | 199 |

| Tax Topics - Income Tax Act - Section 2 - Subsection 2(1) | 229 |

Price v. Canada, 2013 DTC 5024 [at at 5615], 2012 FCA 332, aff'g 2011 DTC 1334 [at 1879], 2011 TCC 449

The taxpayer was a Barbados-resident Canadian citizen who worked as a pilot for Air Canada. His pay was based predominantly on flight time. He...

Sutcliffe v. The Queen, 2006 DTC 2076, 2005 TCC 812

The taxpayer was a U.S. resident who was employed by Air Canada as a pilot on domestic flights (between Toronto and other Canadian cities) and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 15 | 93 |

Austin v. The Queen, 2003 DTC 2181, 2004 TCC 6

A non-resident Canadian Football League football player was entitled to have the portion of his employment income that was not subject to Canadian...

Varnam v. Deeble, [1985] BTC 150 (C.A.)

In determining the level of employment income "attributable to duties performed outside the United Kingdom", reference should be had to the amount...

Administrative Policy

16 April 2024 Internal T.I. 2023-0964831I7 - Guaranteed payments to non-resident athletes

A resident of the US, who had entered into a 6-year employment contract (covering years 20X1 to 20X6) with a Canadian team, suffered a serious...

17 December 2018 Internal T.I. 2016-0659031I7 F - Attendance of board of directors meeting by phone

Regarding non-resident directors who participate outside Canada and by telephone at board meetings of a resident corporation held in Canada, the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 104 - Subsection 104(2) | no withholding on non-resident directors’ fees from duties not exercised in Canada | 95 |

20 January 2021 Internal T.I. 2019-0832211I7 - Cross-border Restricted Share Units

The following approach (which is generally informed by that in the OECD Commentary to allocating cross-border stock option benefits) is followed...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 126 - Subsection 126(1) | source of RSU benefit for FTC purposes determined based on an OECD-inspired hybrid methodology approach | 485 |

21 February 2018 External T.I. 2017-0702061E5 - RCA contributions and taxable inc earned in Canada

A Canadian professional sports team has established an RCA for the benefit of an athlete employee under which each required employer contribution...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 8 - Subsection 8(1) - Paragraph 8(1)(m.2) | no deduction permitted where plan provided only for a lump sum payment or where it was excluded from SDA treatment by para. (j) (re athletes) | 212 |

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(1) - Paragraph 6(1)(a) - Subparagraph 6(1)(a)(ii) | s. 6(1)(a)(i) exclusion applied first before s. 4 allocation of income between Canada and U.S. | 151 |

16 June 2014 External T.I. 2013-0515431E5 - International traffic and airline enterprise

During peak season, Canco, which transports passengers to destinations inside and outside Canada, is supplied planes and non-resident pilots and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 115 - Subsection 115(4) | non-resident's provision of crew and aircraft to Canadian airline | 150 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - International Traffic | non-resident's provision of crew and aircraft to Canadian airline | 109 |

| Tax Topics - Income Tax Act - Section 81 - Subsection 81(1) - Paragraph 81(1)(c) | non-resident's provision of crew and aircraft to Canadian airline | 109 |

| Tax Topics - Income Tax Regulations - Regulation 102 - Subsection 102(1) | Reg. 102 withholding or waiver notwithstanding Treaty exemption | 166 |

| Tax Topics - Treaties - Income Tax Conventions - Article 15 | U.K company's provision of crew to Canadian airline/Reg. 102 withholding or waiver notwithstanding Treaty exemption | 291 |

S5-F2-C1 - Foreign Tax Credit

The geographic source of employment is generally the physical place where the individual performs the related duties. Where this references more...

10 December 2012 External T.I. 2011-0429721E5 F - OETC - Employee stock options benefits

A resident employee, who exercises employee stock options a few years after their grant by the corporate employer, performed duties both in Canada...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 122.3 - Subsection 122.3(1) - Paragraph 122.3(1)(d) | s. 7(1)(a) benefit apportioned based on Canadian and overseas duties performed - generally in year options issued | 156 |

25 September 2012 B.C. CTF Roundtable, 2012-0459411C6 - Allocation of cross-border employee stock options

Formerly, CRA generally had presumed for purposes of applying the domestic provisions of the Act (s. 115(1)(a)(i)) that an employee stock option...

6 July 2012 Internal T.I. 2012-0440741I7 - stock option benefit derived by US resident

USCo, which is a qualifying person for purposes of the Canada-US Income Tax Convention and is a wholly-owned subsidiary of a Canadian public...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 153 - Subsection 153(1) - Paragraph 153(1)(a) | employer reimburser of stock option benefit amount subject to withholding obligation | 348 |

| Tax Topics - Treaties - Income Tax Conventions - Article 15 | U.S. subs qualifies as payer of (therefore exempt) stock option benefit/domestic v. Treaty method | 404 |

7 May 2009 External T.I. 2008-0276181E5 - Stock Option Benefits

a US-resident individual who is a director of a Canadian public corporation, who receives retainer fees in excess of $10,000 annually and who is...

4 December 2003 External T.I. 2001-01177

Where rights under a share appreciation rights plan are granted while an employee is resident in Canada, but redeemed when the employee is a...

27 August 2003 Internal T.I. 2003-0019857 F - Attribution de dividendes par un RPEB

An employee profit sharing plan (EPSP) received dividends from taxable Canadian corporations that were included in computing its income and that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(1) - Paragraph 6(1)(d) | dividends allocated to a non-resident beneficiary by an EPSP were taxable to the extent that the allocation related to duties performed in Canada | 184 |

28 January 2003 External T.I. 2002-0147405 F - Crédit d'impôt pour emploi à l'étranger

CCRA indicated that leave periods in Canada of employees engaged (when working) on a U.S. services contract did not stop the period of 6 months’...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 122.3 - Subsection 122.3(1) | leave periods in Canada count towards the period of 6 months’ employment under foreign project if not terminated before leave commences | 322 |

19 January 2001 External T.I. 2000-0058405 - STOCK OPTIONS AND NON-RESIDENT

"Generally, the stock option benefit relating to the options granted to an individual while he or she is employed by a foreign employer while the...

28 May 1996 External T.I. 9601625 - INCOME OF NR, ACTORS AND ATHLETES

"Where the duties of a particular office or employment are performed partly in Canada and partly outside of Canada, a reasonable apportionment of...

30 November 1995 Ruling 9626393 - XXXXXXXXXX, PHANTOM STOCK PLAN

RC declined to rule that a non-resident director's fees could be allocated to Canada only to the extent of the number of days worked in Canada...

2 December 1993 Income Tax Severed Letter 933330A F - Non-Resident Exercises Stock Option (4093-U5-100-15)

Where a U.S.-resident was employed for several years by a wholly-owned Canadian subsidiary of a U.S. public company and in the course of his...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 15 | 222 |

13 June 1991 T.I. (Tax Window, No. 4, p. 28, ¶1299)

Disability payments received by a U.S. resident under a disability policy maintained by his former employer will be subject to Canadian tax if the...

12 September 1990 T.I. (Tax Window, Prelim. No. 1, p. 18, ¶1015)

A non-resident director of a Canadian corporation who exercises his stock option is taxable under s. 7(1) to the extent that the granting of the...

81 C.R. - Q.56

The territorial source of employment income is the place where the related duties are normally performed.

IT-420R3 "Non-Residents - Income Earned in Canada"

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 2 - Subsection 2(3) - Paragraph 2(3)(b) | 0 |

IT-168R3 "Athletes and Players Employed by Football, Hockey and Similar Clubs" under "Non-Residents"

Articles

Tobias, "Taxing Benefits Realized by Former Canadian Residents", Taxation of Executive Compensation and Retirement, March 1994, p. 889

The author argues that Canada has no right to tax the benefit resulting from the exercise or realization of employee stock options on shares of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(4) | 71 |

Finley, "Non-Resident Directors' Fees May Be Subject to Withholding in Canada", Taxation of Executive Compensation and Retirement, October 1990, p. 348

RC has acknowledged that where a non-resident director participates in a meeting held by teleconference call, his fees are not income from duties...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 101 | 69 |

Subparagraph 115(1)(a)(ii)

Cases

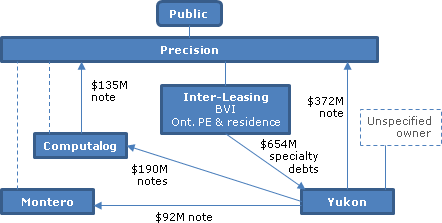

Inter-Leasing, Inc. v. Ontario (Revenue), 2014 ONCA 575

{kind=link}

In order to minimize Alberta corporate tax, the Precision group of companies reorganized, as a result of which:

- Interest-bearing debts were...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | underlying rationale for exempting property income was no broader than the text | 454 |

See Also

Commissioner of Taxation v Resource Capital Fund IV LP Commissioner of Taxation v Resource Capital Fund IV LP, [2019] FCAFC 51

Two Caymans investment LPs, whose limited partners were mostly U.S. residents, realized income-account gains from the disposal, pursuant to an...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(1) | assessment must bring to the attention of the assessed person that it has been assessed to tax | 258 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Taxable Canadian Property - Paragraph (d) | mine assets included processing operations | 434 |

Resource Capital Fund IV LP v Commissioner of Taxation, [2018] FCA 41 (Federal Court of Australia), rev'd on various grounds [2019] FCAFC 51

Two Caymans investment LPs (“RCF IV” and RCF V”) whose limited partners were mostly U.S. residents, realized gains from the disposal of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Shares | private equity fund LP with 5-year holding objective realized share gain on income account | 175 |

| Tax Topics - Treaties - Income Tax Conventions - Article 3 | each U.S.-resident partner of a Caymans PE LP carried on a U.S. “enterprise” | 234 |

| Tax Topics - Treaties - Income Tax Conventions - Article 13 | exclusion in Art. 13 of Aust.-U.S. Treaty for real property dispositions extended to shares of Australian holding company holding mining leases through grandchild | 420 |

| Tax Topics - General Concepts - Stare Decisis | lower court not bound by a point of law that was assumed rather than examined by a higher court | 292 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(1) | assessment of partnership was assessment of partners | 89 |

| Tax Topics - Treaties - Income Tax Conventions - Article 6 | Art. 6 extends common law meaning of real property | 198 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Taxable Canadian Property - Paragraph (d) | shares of lithium mining and processing company were derived principally from the processing rather than mining operation and, thus, were not taxable Australian real property | 514 |

| Tax Topics - Income Tax Act - Section 218.3 - Subsection 218.3(1) - Canadian Property Mutual Fund Investment | shares of Australian mining company were primarily attributable to the processing rather than mining operations | 142 |

| Tax Topics - General Concepts - Fair Market Value - Other | processing assets of mining company were more valuable than its mining assets | 238 |

Maya Forestales S.A. c. La Reine, 2005 DTC 514, 2005 TCC 66, aff'd 2008 DTC 6100, 2006 FCA 35

The taxpayer was found to be carrying on business in Canada on the basis that through a Canadian mandatory it offered for sale, in Canada, Costa...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 253 - Paragraph 253(b) | 121 |

Commissioner of Inland Revenue v. Kwong Myle Services Ltd. (2004), 7 ITLR 239 (HK CFA)

The taxpayer (a company incorporated in Hong Kong) underwrote the sale of apartment units in a building erected in mainland China pursuant to an...

Twentieth Century Fox Film Corp. v. The Queen, 85 DTC 5513, [1985] 2 CTC 328 (FCTD)

Before finding that film revenues of the U.S. taxpayer were reasonably attributable to its Canadian distributorship business notwithstanding they...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 802 | 178 | |

| Tax Topics - Income Tax Regulations - Regulation 805 | film revenues were reasonably attributable to a Canadian distributorship business notwithstanding they were also attributable to U.S. movie production | 191 |

Yates v. GCA International Ltd., [1991] BTC 107 (Ch. D.)

In accepting a finding of the Commissioners that the income earned by a U.K. petroleum consulting firm from work done pursuant to a contract with...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 126 - Subsection 126(7) - Non-Business-Income Tax | 190 |

CIR v. Hang Seng Bank Ltd., [1990] BTC 482 (PC)

The gains realized by a Hong Kong bank from the purchase and resale outside Hong Kong of certificates of deposit, bonds and gilt-edged securities...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Interpretation Act - Subsection 45(2) | 51 |

Furness Withy & Co. Ltd. v. MNR, 66 DTC 5358, [1966] CTC 482 (Ex Ct), aff'd 68 DTC 5033, [1968] CTC 35, [1968] S.C.R. 221

The Canadian branch office of the taxpayer, which was a U.K.-resident company earning profits from international shipping conducted by itself and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Evidence | 210 | |

| Tax Topics - Income Tax Act - Section 81 - Subsection 81(1) - Paragraph 81(1)(c) | 211 |

United Geophysical Co. of Canada v. MNR, 61 DTC 1099, [1961] CTC 134 (Ex Ct)

The U.S. parent of the taxpayer rented equipment to the taxpayer for use by the taxpayer in its Canadian operations. Although the U.S. parent was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Agency | company's business not carried on as agent for shareholder | 154 |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(d) | "rent" can be for personalty | 106 |

Commissioner for Inland Revenue v. Nell (1961), 3 S.A. 774 (A.D.)

The taxpayer, who was a consulting electrical and mechanical engineer practising in Johannesburg, visited project sites in Rhodesia for the...

International Harvester Co. of Canada, Ltd. v. Provincial Tax Commission, [1949] A.C. 36 (PC)

The taxpayer, which was an Ontario corporation engaged in the business of manufacturing and selling agricultural implements, carried on its...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 402 - Subsection 402(3) | 127 |

Federal Commissioner of Taxation v. United Aircraft Corp. (1943), 7 A.T.D. 318 (HC)

An American manufacturer of airplanes purported to license its rights to use Australian patents and registered designs to an Australian company in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Property | 41 |

Watson v. Commissioner of Taxation (W.A.) (1930), 1 A.T.D. 61 (HC)

The taxpayer, while practising as a public accountant in Western Australia, agreed with the client that if the taxpayer were able to secure a...

Administrative Policy

2021 Ruling 2019-0800191R3 - Carrying on business in Canada.

CRA ruled that the provision of various services by Canco to its immediate foreign parent and to other non-resident members of the group would not...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 2 - Subsection 2(3) - Paragraph 2(3)(b) | a Canadian sub providing computer and admin/ marketing support services to its non-resident parent would not cause the parent to carry on business in Canada | 248 |

17 May 2023 IFA Roundtable Q. 5, 2023-0965771C6 - Remote Work Arrangements

50 of the 1,000 employees of USco (a US C-Corp and a “qualifying person” for purposes of the Canada-US Treaty) are Canadian residents who are...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 5 | whether employee’s home office can constitute a PE of US employer | 359 |

| Tax Topics - Income Tax Act - Section 253 - Paragraph 253(a) | product development from Canadian home office might engage s. 253(a) | 114 |

| Tax Topics - Income Tax Act - Section 253 - Paragraph 253(b) | s. 253(b) does not extend to “invitation to treat” or advertisement | 97 |

7 June 2017 CPTS Roundtable, 2017-0695131C6

What positions has CRA taken regarding when specific oil and gas production activities form part of the same business for s. 111(5) purposes and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 13 - Subsection 13(21) - Proceeds of Disposition | Q.1 - Daishowa extends beyond reforestation and reclamation obligations only on a case-by-case basis | 213 |

| Tax Topics - Income Tax Act - Section 66 - Subsection 66(15) - Canadian Resource Property - Paragraph (d) | Q.2 - a Canadian resource royalty interest requires a right to “take production” | 135 |

| Tax Topics - Treaties - Income Tax Conventions - Article 13 | Q.3 - Canada-U.K. Treaty does not exempt shares deriving their value from Canadian oil and gas licences – even where the Canadian business is carried on “in” them | 193 |

| Tax Topics - Income Tax Regulations - Regulation 1101 - Subsection 1101(1) | Q.5 - normal course dispositions of oil and gas properties generally are not of a separate business | 131 |

| Tax Topics - Income Tax Act - Section 4 - Subsection 4(1) - Paragraph 4(1)(a) | Q.5 - application of Scales test to determining whether there is a separate business | 224 |

| Tax Topics - Income Tax Regulations - Schedules - Schedule II - Class 26 | Q.7 - refinery catalysts are Class 26 property | 87 |

| Tax Topics - Income Tax Regulations - Schedules - Schedule II - Class 49 | Q.8 - taxpayers generally have the documentary evidence on hand to allocate costs between pipelines and pipeline appendages | 117 |

19 June 2015 External T.I. 2013-0475751E5 - Withholding Tax on Royalty Payments

In response to what CRA treated as a general inquiry, it referenced the question of whether the non-resident company (which received royalties...

5 February 2014 External T.I. 2012-0466671E5 - Non-resident source withholdings

Canco will pay a fee to an India partnership providing technical support based on a percentage of the total technical support fee revenues to be...

S5-F2-C1 - Foreign Tax Credit

1.53 While a determination of the place where a particular business (or a part of the business) is carried on (that is, the location of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Agency | Canadian legal principles applied to "agency" | 57 |

| Tax Topics - Income Tax Act - Section 110.5 | creates non-capital losses | 69 |

| Tax Topics - Income Tax Act - Section 115 - Subsection 115(1) - Paragraph 115(1)(a) - Subparagraph 115(1)(a)(i) | apportionment based on where employee is physically present while performing duties | 46 |

| Tax Topics - Income Tax Act - Section 126 - Subsection 126(1) | 605 | |

| Tax Topics - Income Tax Act - Section 126 - Subsection 126(2) | 95 | |

| Tax Topics - Income Tax Act - Section 126 - Subsection 126(4.1) | 36 | |

| Tax Topics - Income Tax Act - Section 126 - Subsection 126(7) - Business-Income Tax | 71 | |

| Tax Topics - Income Tax Act - Section 126 - Subsection 126(7) - Non-Business-Income Tax | 114 | |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(12) | 271 | |

| Tax Topics - Income Tax Act - Section 4 - Subsection 4(3) | 121 |

3 November 2008 External T.I. 2008-0278431E5 F - Déménagement hors Canada du siège soc. de société

In the context of a general discussion of consequences where there was an acquisition of control of a corporation incorporated in Canada in 2005...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 250 - Subsection 250(5) | central management and control test overridden | 122 |

| Tax Topics - Income Tax Act - Section 127 - Subsection 127(9) - Investment Tax Credit - Paragraph (a.1) | ITC potentially available to a non-resident corporation carrying on business in Canada | 97 |

| Tax Topics - Income Tax Act - Section 4 - Subsection 4(1) - Paragraph 4(1)(b) | s. 4(1)(b) requires allocation between Canada and another country on basis of relative profit contribution | 172 |

11 January 2001 Internal T.I. 2000-0001017 - Sourcing of income & foreign tax credit

The Directorate agreed that the taxpayer, which was a Canadian manufacturer transferring some of its goods to a Japanese branch for sale there,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 126 - Subsection 126(2) | 115 |

2005 Ruling 2004-0094821R3 - Carrying on Business in Canada

Ruling given that the expansion of services provided by a Canadian corporation ("Canco") to its affiliated non-resident administrator of...

2004 Ruling 2004-0082661R3 - Carrying on Business in Canada

Ruling that the delegation by a non-resident service provider ("C Limited") to a non-resident investment fund (the "Fund") of accounting and...

11 May 2000 External T.I. 1999-0009935 F - Droit recevoir allocations et emigration

A medical specialist who was entitled under the Quebec end-of-career-allowance program to receive an annual allowance for five years following his...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 128.1 - Subsection 128.1(4) - Paragraph 128.1(4)(b) | end-of-career allowance receivable be emigrating physician was includible under s. 128.1(4)(b) | 159 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Property | physician’s entitlement to end-of-career allowance was property | 65 |

19 April 2000 External T.I. 1999-001100

Interest on money borrowed by a non-resident individual to make a capital contribution to a partnership that carries on business in Canada through...

1999 Ruling 9920603 - NON-RESIDENT - CARRYING ON BUSINESS IN CDA

Ruling that a Canadian company engaged by a non-resident fund manager to provide accounting and clerical services in Canada would not thereby...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 2 - Subsection 2(3) - Paragraph 2(3)(b) | 40 |

30 November 1996 Ruling 9704923 - CARRYING ON BUSINESS IN CANADA - ADM. SERVICES

Where a non-resident corporation has contracted to perform certain administrative duties for other non-resident corporations, the fact that it has...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 2 - Subsection 2(3) - Paragraph 2(3)(b) | 54 |

1 December 1992 Memorandum (Tax Window, No. 27, p. 11, ¶2352; October 1993 Access Letter, p. 475)

Where a non-treaty country subsidiary of a Canadian corporation manufactures or process goods outside Canada with no purchasing or processing of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 5 | 34 |

8 July 1992 T.I. 921814 (March 1993 Access Letter, p. 87, ¶C248-129)

Discussion of allocation of business income between Canada and a foreign country where: a Canadian corporation, acting as a wholesaler, buys...

IT-420R2 "Non-Residents - Income Earned in Canada", para. 10

Income from property earned in Canada by a non-resident is not subject to tax under s. 115(1) but, rather, may be subject to Part XIII tax.

Articles

Nathan Boidman, "How Will Revised Sourcing Rules Affect Sales of U.S.-Made Goods Abroad?", Tax Notes International, 10 February 2020, p. 655

Computing Pt I tax on Canadian distribution profits of a U.S. producer (p. 657)

Section 4(1)(b) of the ITA provides that when a business is...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 7 | 387 | |

| Tax Topics - Treaties - Income Tax Conventions - Article 24 | 542 |

Jinyan Li, "Rethinking Canada's Source Rules In The Age Of Electronic Commerce: Part I", 1999 Canadian Tax Journal, Vol. 47, No. 5, p. 1077.

Constantine Kyres, "Carrying on Business in Canada", 1995 Canadian Tax Journal, Vol. 45, No. 5, p. 1629.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 2 - Subsection 2(3) - Paragraph 2(3)(b) | 0 | |

| Tax Topics - Income Tax Act - Section 253 | 0 |

Broadhurst, "Financing by Non-Residents", 1992 Corporate Management Tax Conference Report, pp. 9:10 -9:18

Discussion of whether a non-resident purchaser of accounts receivable would be considered to be carrying on business in Canada.

Subparagraph 115(1)(a)(iii.1)

Administrative Policy

23 January 2015 External T.I. 2013-0509771E5 - Oil & gas payments made to U.S. resident

Mr. A, a U.S. resident, grants the right to drill for or take the oil & gas from his Canadian freehold property to a Canadian company, in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 66.4 - Subsection 66.4(5) - Cumulative Canadian Oil And Gas Property Expense - F | FMV addition and subtraction where drilling rights are granted for royalty | 143 |

| Tax Topics - Income Tax Regulations - Regulation 805 | application to resource royalties | 252 |

| Tax Topics - Treaties - Income Tax Conventions - Article 12 | non-application of Art. 12 of US Treaty to resource royalties | 142 |

| Tax Topics - Treaties - Income Tax Conventions - Article 6 | negative CCDE gain from grant of oil and gas royalty not exempt under US Treaty | 180 |

Subparagraph 115(1)(a)(iii.2)

Administrative Policy

27 February 1991 T.I. (Tax Window, No. 1, p. 10, ¶1167)

If an individual ceases to be a resident of Canada and subsequently disposes of depreciable properties used in a business carried on outside...

Paragraph 115(1)(d)

Paragraph 115(1)(e)

See Also

Matlas, S.A. v. The Queen, 94 DTC 1591 (TCC)

Archambault TCJ. found that losses of the non-resident corporate taxpayer from the operation of a condominium (being its sole investment) were...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 115 - Subsection 115(1) - Paragraph 115(1)(f) | 44 |

Administrative Policy

10 March 1995 Internal T.I. 9501456 - 115(1)(E) (HAA 6815-4)

"An individual who, while a resident of Canada, incurred a non-capital loss from a business carried on in Canada can, assuming the other...

Paragraph 115(1)(f)

See Also

Delancy v. The Queen, 2004 DTC 2907, 2004 TCC 465 (Informal Procedure)

The taxpayer, who was a U.S. resident, and was employed by two Canadian professional football teams, was unable to deduct his living expenses...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 8 - Subsection 8(1) - Paragraph 8(1)(h) | 66 |

Matlas, S.A. v. The Queen, 94 DTC 1591 (TCC)

Archambault TCJ. found that the other deductions referred to in s. 115(1)(f) were deductions other than those referred in paragraphs 115(1)(d) and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 115 - Subsection 115(1) - Paragraph 115(1)(e) | 102 |

Subparagraph 115(1)(b)(ii)

See Also

Pampered Chef, Canada Corp. v. CBSA, [2008] ETC 4514 (CITT)

Individual self-employed sales representatives of the taxpayer secured orders for sales of kitchen products shown at various home parties by them...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Other Legislation/Constitution - Federal - Customs Act - Section 2.1 | 99 |

Subsection 115(2) - Idem [Non-resident’s taxable income in Canada]

Paragraph 115(2)(c)

Cases

Jarlan v. The Queen, 84 DTC 6452, [1984] CTC 375 (FCTD)

Awards which a French resident received for an invention he had made over 10 years previously while still in the employ of the National Research...

Administrative Policy

26 September 2014 External T.I. 2014-0531441E5 - Unfunded LTD plan payment to non-resident employee

A Canadian resident employee, after qualifying for benefits under the unfunded long term disability plan ("LTD Plan") of the Canadian resident...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 153 - Subsection 153(1) - Paragraph 153(1)(a) | employee long-term disability payments: remuneration under ITA; pension under Cda-U.S. Convention | 214 |

| Tax Topics - Treaties - Income Tax Conventions - Article 18 | employee long-term disability payments: remuneration under ITA; pension under Cda-U.S. Convention | 259 |

14 November 2007 External T.I. 2007-0245631E5 F - Retenue à la source -employé à l'étranger

A French national was employed by a Canadian corporation since August 1998 and resided in Canada from that date until July 29, 2007, when he...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 104 - Subsection 104(2) | no source deductions required of Canadian employer for employee exercising duties in France | 131 |

31 October 1995 External T.I. 9507485 - EMPLOYEES AT CANADIAN EMBASSY IN SAUDI ARABIA (8019-6)

Former Canadian residents working at the Canadian Embassy in Riyadh will have their remuneration subject to tax under s. 115(2) since such...

Paragraph 115(2)(c.1)

See Also

Nonis v. The Queen, 2021 TCC 31

The taxpayer, Mr. Nonis, who was a U.S. resident , had been employed as the general manager of the Toronto Maple Leafs pursuant to an employment...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 4 - Subsection 4(1) - Paragraph 4(1)(b) | s. 4(1)(b) requires allocation of employment income based on situs of physical work | 250 |

Paragraph 115(2)(e)

Subparagraph 115(2)(e)(i)

Cases

Hale v. The Queen, 90 DTC 6481, [1990] 2 CTC 247 (FCTD), aff'd 92 DTC 6473 (FCA)

The taxpayer, while a non-resident of Canada, received $25,000 for the performance of his duties as director of a Canadian company. Although the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(1) - Paragraph 7(1)(b) | 129 | |

| Tax Topics - Treaties - Income Tax Conventions - Article 15 | 106 |

Hurd v. The Queen, 81 DTC 5140, [1981] CTC 209 (FCA)

"Remuneration" does not include a S.7 stock option benefit.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 115 - Subsection 115(1) - Paragraph 115(1)(a) - Subparagraph 115(1)(a)(i) | 32 | |

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(4) | 95 | |

| Tax Topics - Treaties - Income Tax Conventions - Article 13 | meaning of exchange | 33 |

Administrative Policy

20 March 2015 External T.I. 2014-0534301E5 - Canadian Withholding Tax on Retiring Allowance

A lump sum payment in compensation for a loss of employment at a French subsidiary is made by Canco to a non-resident of Canada who had been...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(j.1) | retiring allowance paid to non-resident for loss of non-resident employment | 149 |

| Tax Topics - Treaties - Income Tax Conventions - Article 15 | retiring allowance paid to French individual for loss of non-resident employment | 73 |

| Tax Topics - Treaties - Income Tax Conventions - Article 22 | retiring allowance paid to French individual for loss of non-resident employment | 73 |

Subparagraph 115(2)(e)(ii)

Administrative Policy

1 May 2025 External T.I. 2024-1030911E5 F - Scholarships to non-residents to study French

Non-resident temporary workers take French language courses offered by general Quebec training centres for free, but may receive French language...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.94 | scholarships received by non-resident temporary workers for French language training would be included in their worldwide income s. 118.94 computation purposes | 200 |

Subparagraph 115(2)(b)(ii)

Administrative Policy

14 December 1995 External T.I. 9529255 - INTERNATIONAL SHIPPING-GAIN FROM DISPOSITION OF GOODWILL

Goodwill would be considered personal property for purposes of the exemption in s. 115(2)(b)(ii)(B).

Subsection 115(2.1)

Administrative Policy

27 July 2016 External T.I. 2015-0603271E5 - Subsection 216.1(1) and permanent establishment

A U.S.-resident actor provides Canadian acting services through an LLC or S corp. The 23% withholding tax under ITA s. 212(5.1) on the gross...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 216.1 - Subsection 216.1(1) | late filing under s. 216.1 not accommodated | 216 |

| Tax Topics - Treaties - Income Tax Conventions - Article 16 | Art. 16 of US Treaty permits gross withholding taxation even if PE | 172 |

Subsection 115(3)

Administrative Policy

7 September 2016 External T.I. 2014-0559751E5 - Subsection 115(3)

Would Art. XV of the Canada-U.S. Treaty prevail over s. 115(3) where the Treaty provides more advantageous tax results for a U.S.-resident pilot...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 15 | comparison of Treaty and domestic method for pilot income on annual basis | 109 |

Subsection 115(4) - Non-resident’s income from Canadian resource property

Administrative Policy

16 June 2014 External T.I. 2013-0515431E5 - International traffic and airline enterprise

During peak season, Canco, which transports passengers to destinations inside and outside Canada, is supplied planes and non-resident pilots and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 115 - Subsection 115(1) - Paragraph 115(1)(a) - Subparagraph 115(1)(a)(i) | application of Sutcliffe/Price allocation approach where s. 115(3) not applicable | 150 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - International Traffic | non-resident's provision of crew and aircraft to Canadian airline | 109 |

| Tax Topics - Income Tax Act - Section 81 - Subsection 81(1) - Paragraph 81(1)(c) | non-resident's provision of crew and aircraft to Canadian airline | 109 |

| Tax Topics - Income Tax Regulations - Regulation 102 - Subsection 102(1) | Reg. 102 withholding or waiver notwithstanding Treaty exemption | 166 |

| Tax Topics - Treaties - Income Tax Conventions - Article 15 | U.K company's provision of crew to Canadian airline/Reg. 102 withholding or waiver notwithstanding Treaty exemption | 291 |

93 CPTJ - Q.10

If a non-resident disposes of some, but not all, of its Canadian resource properties, whether ss.115(4)(a) to (c) apply may depend on whether it...