Subsection 125(1) - Small business deduction

Cases

Scandia Plate Ltd. v. The Queen, 83 DTC 5009, [1982] CTC 431 (FCTD)

Ownership of the shares of an alleged Canadian-controlled private corporation was not acquired by a Canadian resident from a Swedish company...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | 100 | |

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Canadian-Controlled Private Corporation | 28 |

Administrative Policy

31 January 2018 External T.I. 2016-0676431E5 - foreign tax credit on employees profit sharing

Are foreign taxes allocated from an employees profit sharing plan to an individual on a T4PS limited to 15% for foreign tax credit purposes? CRA...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 144 - Subsection 144(8.1) - Paragraph 144(8.1)(b) | 15% limitation on FTC credit | 93 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(11) | no s. 20(11) deduction for foreign taxes respecting EPSP income allocated to beneficiary | 107 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(12) | no s. 20(12) deduction to EPSP beneficiary | 108 |

13 June 2017 STEP Roundtable Q. 8, 2017-0693381C6 - Single-member disregarded U.S. LLC

A single-member disregarded U.S. limited liability company (“SMLLC”), whose member is a resident of Canada, is factually resident in Canada...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 26 | no relief under Art. 26(1) of US Treaty re LLC with U.S.-source income and single Canadian-resident member | 145 |

| Tax Topics - Treaties - Income Tax Conventions - Article 29 | single member LLC with dual resident member could elect to be C-Corp and S-Corp, and then consider applying for relief under Art. 29(5) | 158 |

20 June 2016 External T.I. 2016-0648481E5 F - Small business deduction and GRIP

CRA accepted that a corporation may choose not to take the small business deduction so as to increase its general rate income pool account,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Adjusted Taxable Income | CCPCs can choose to forego the small business deduction so as to maximize their GRIP | 118 |

26 March 2012 External T.I. 2012-0440441E5 F - Déduction accordée aux petites entreprises

General and superficial response to question as to when the small business deduction is available.

3 March 2011 External T.I. 2010-0380751E5 F - Déduction accordée aux petites entreprises

A corporation, that carries manages a convenience store under a franchise agreement, is not responsible for rent, inventory purchases and...

92 C.R. - Q.50

A corporation that is a trader in securities is entitled to the small business deduction.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Income of the Corporation for the Year From an Active Business | 26 |

85 C.R. - Q.56

Where a firm performs engineering activities in respect of a project both at its office in Canada and the foreign project site, only income...

IT-73R6 "The Small Business Deduction" 26 March 2002

5 ...In examining the ordinary dictionary meaning of these words, "incident to" generally includes anything that is connected with or related to...

Articles

Perry Truster, "Expanding into the U.S", Tax for The Owner-Manager, Vol. 2, No. 1, January 2002

Ancillary business activities in the U.S., although not carried on through a permanent establishment there, will not give rise to income eligible...

Durnford, "The Distinction Between Income from Business and Income from Property, and the Concept of Carrying on Business", 1991 Canadian Tax Journal, p. 1131.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 129 - Subsection 129(4) - Canadian Investment Income | 0 |

Paragraph 125(1)(a)

Subparagraph 125(1)(a)(i)

Clause 125(1)(a)(i)(B)

Administrative Policy

23 January 2025 External T.I. 2024-1030091E5 - Specified Corporate Income - Realtor Commissions

A real estate broker carried on his practice through a wholly-owned corporation (A Co), which received all of its commissions, net of service...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Specified Corporate Income - Paragraph (a) - Subparagraph (a)(i) | a corporation could earn active business income through another private corporation if the true customers were third parties | 245 |

26 January 2023 External T.I. 2021-0887661E5 - Small Business Deduction - Related

CRA indicated that where two CCPCs, wholly-owned by Mr. or Mrs. X, did not provide services or property, directly or indirectly, in any manner...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Specified Corporate Income - Paragraph (a) - Subparagraph (a)(i) | 2 related but not associated CCPCs do not have their SBD ground under s. 125(1)(a)(i)(B) if they have no business dealings with each other | 139 |

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(5.1) - Paragraph 125(5.1)(a) | non-associated but related corporations not required to aggregate their taxable capital | 89 |

23 February 2021 External T.I. 2018-0769891E5 F - 125(7) "revenu de société déterminé"

The definition "specified corporate income" is used in the rule indicating that the portion of the income of a Canadian-controlled private...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | presumption that two 50% shareholders act together to control the corporation | 147 |

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Specified Corporate Income - Paragraph (a) - Subparagraph (a)(i) - Clause (a)(i)(B) - Subclause (a)(i)(B)(I) | services income from multiple private corporations referenced in s. (a)(i)(A) can be bad income for purposes of the substantially all test | 477 |

7 February 2018 External T.I. 2017-0706401E5 - Specified corporate income, streaming of expenses

Where a corporation earns income eligible for the “small business deduction” (SBD) and income that is ineligible due to the “specified...

20 April 2017 External T.I. 2016-0679721E5 - The small business deduction

SellCo A and SellCo B sell all of their fishing catch to BuyCo (also a CCPC), although BuyCo purchases the majority of its fish from unrelated...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Specified Corporate Income | sales of product to private corporation in which brother or father of the vendor shareholder has a controlling interest | 316 |

Subsection 125(3) - Associated corporations

See Also

Deneschuk Building Supplies Ltd. v. The Queen, 96 DTC 1467, [1996] 3 CTC 2039 (TCC)

After the taxpayer had filed a form T2013 allocating the $200,000 business limit between it and another corporation, the Minister reassessed the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(7) | 50 | |

| Tax Topics - Income Tax Act - Section 166 | 32 |

Administrative Policy

19 October 2000 External T.I. 2000-0027795 F - SOCIETES PRIVEES SOUS CONTROLE CDN

Corporations controlled (but less than 90% owned) by a Crown corporation in which a provincial government was a 100% shareholder would be...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 181.5 - Subsection 181.5(6) | corporations controlled by the provincial Crown would not be required to share their capital deduction | 69 |

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Canadian-Controlled Private Corporation | corporations controlled by the provincial Crown treated as CCPCs | 61 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Person | provincial Crown is a person | 20 |

Paragraph 125(3)(b)

See Also

Monsell v. The Queen, 2019 TCC 5 (Informal Procedure)

In confirming the correctness of a reassessment of a corporation (Newgate) denying it the small business deduction, D’Auray J stated (at paras...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | CRA has the onus of substantiating assessments underlying s. 160 assessments where it had superior records access | 324 |

| Tax Topics - General Concepts - Onus | onus on CRA where it, rather than taxpayer, had access to the records underlying a reassessment | 230 |

Subsection 125(3.2)

Administrative Policy

20 October 2022 External T.I. 2020-0869681E5 - Specified Corporate Income

Mr. A owned 50% of a real estate management company (Hco), which derived substantially all of its income from providing services to a corporation...

| Other locations for this summary | |

|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(3.2) | permitted assignment of business limit to the extent of “specified corporate income” |

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Specified Corporate Income - Paragraph (a) - Subparagraph (a)(i) | services income earned from an arm’s length CCPC was ineligible under (a)(i) | 239 |

29 January 2018 External T.I. 2017-0713051E5 - Business limit assignment

A Canadian-controlled private corporation (“first CCPC”) with a calendar year end assigns a portion of its business limit (“BL”) to...

Articles

Dino Infanti, "Assignment of Small Business Limit Creates Filing Headaches", Tax for the Owner-Manager (Canadian Tax Foundation), Vol. 18, No. 1, January 2018, p 3

Example of s. 125(3.2) assignment of business limit (BL) of CCPC (receiving services from Serviceco) to Serviceco (p. 3)

Assume that Mr. A owns...

Paragraph 125(3.2)(d)

Administrative Policy

5 April 2018 Internal T.I. 2017-0728581I7 - Ss 125(3.2) & 125(8) amending the business limit

In essentially confirming 2009-0351721E5 to the effect that an associated group of Canadian-controlled private corporations can file amended T2...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(8) - Paragraph 125(8)(c) | partner assignment of its SPBL may be amended within the statute-barring period – and can be sliced and diced | 239 |

Subsection 125(4) - Failure to file agreement

Articles

Louis, "Family Trusts - Panacea or Ticking Time Bomb?", Canadian Estate Planning and Administration Reporter, August 2, 1994, p. 1

Description of various circumstances in which the use of discretionary trusts can result in corporations becoming associated.

Subsection 125(5)

Paragraph 125(5)(a)

Administrative Policy

4 March 2009 External T.I. 2009-0306401E5 F - Plafond des affaires

A group of corporations with a fiscal period end of February 28, 2007, amended their fiscal period end to December 31, 2007. Does s. 125(5)...

4 November 2002 Internal T.I. 2002-0160697 F - REPARTITION DU PLAFOND

On February 7, 2000, control of Aco, was acquired by a third party, resulting in a deemed taxation year-end under s. 249(4) and in a second...

Subsection 125(5.1) - Business limit reduction

Administrative Policy

7 October 2020 APFF Roundtable Q. 13, 2020-0852251C6 F - Small Business Deduction

The definition of “adjusted aggregate investment income” (whose amount can grind the business limit) excludes capital gains from “active...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Adjusted Aggregate Investment Income | s. 55(2) gain from a share can qualify as a gain from an active asset for AAII purposes | 180 |

25 January 2018 External T.I. 2017-0709241E5 - Subsections 125(3.2) & 125(5.1)

Does the assignment of the business limit under s. 125(3.2) occur before or after the business limit reduction in s. 125(5.1)? After noting that...

14 September 2017 External T.I. 2017-0685121E5 F - Associated corporations

Three children each of whom wholly-owns a Childco are also, along with their parent, the discretionary beneficiaries of a family trust owning all...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(1.2) - Paragraph 256(1.2)(f) - Subparagraph 256(1.2)(f)(ii) | Childco associated with Parent-controlled corp whose non-voting equity is held by family trust | 85 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(2) - Paragraph 256(2)(b) - Subparagraph 256(2)(b)(ii) | election under s. 256(2)(b)(ii) busts s. 256(2)(a) transitivity but not association with 3rd corporation | 310 |

21 January 2013 External T.I. 2012-046881E5

In response to a query regarding the business limit reduction under s. 125(5.1) in a situation where a Canadian-controlled private corporation was...

16 January 2008 External T.I. 2007-0232751E5 F - Éléments "A" et "B" du paragraphe 127(10.2)

Xco, a Canadian-controlled private corporation, wholly-owns Yco, a U.S. corporation, with no taxable income in Canada and whose profits are taxed...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 127 - Subsection 127(10.2) | expenditure limit does not take into account income of associated non-resident that has no Canadian PE or other Canadian nexus | 338 |

Articles

Stan Shadrin, Alex Ghani, Josh Harnett, "Corporate Partnership May Avoid the Paragraph 125(5.1)(b) Grind", Tax for the Owner-Manager, Vol. 20, No. 4, October 2020, p.4

Example of requirement to recognize all AAII from investment portfolio where spousally-owned Investco (pp. 4-5)

Opco… is wholly owned by Mr. X,...

Tim Barrett, Kevin Duxbury, "Corporate Integration: Outbound Structuring in the United States After Tax Reform", 2018 Conference Report (Canadian Tax Foundation), 18:1-76

Double-counting of adjusted aggregate investment income (AAII) of CFA twice towards passive income restriction in s. 125(5.1)(b) (p. 18:32)

[A]n...

Martin Lee, Thanusan Raveendran, "Possible Anomaly in the Passive Income SBD Grind?", Canadian Tax Focus, Vol. 9, No. 4, November 2019, p.1

Example of avoidance of s. 125(5.1) limitation where sub with realized passive gain is wound-up (p. 1)

… Holdco…wholly owns an Opco that...

Michael Goldberg, "The Passive Investment Rules and Their Associates", Tax Topics (Wolters Kluwer), No. 2426, September 6, 2018, p. 1

Passive income clawback under s. 125(5.1)(b) (p. 1)

[T]he Passive Income Claw-Back will begin once adjusted aggregate investment income in excess...

Paragraph 125(5.1)(a)

Administrative Policy

26 January 2023 External T.I. 2021-0887661E5 - Small Business Deduction - Related

Mr, X wholly-owned ACo and his wife, Mrs. X, wholly-owned BCo. ACo and BCo were not associated. Would ACo and BCo be required to aggregate their...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Specified Corporate Income - Paragraph (a) - Subparagraph (a)(i) | 2 related but not associated CCPCs do not have their SBD ground under s. 125(1)(a)(i)(B) if they have no business dealings with each other | 139 |

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(1) - Paragraph 125(1)(a) - Subparagraph 125(1)(a)(i) - Clause 125(1)(a)(i)(B) | 2 related but not associated CCPCs with no cross-business dealings did not have an s. 125(1)(a)(i)(B) grind | 79 |

Paragraph 125(5.1)(b)

Administrative Policy

27 November 2018 CTF Roundtable Q. 16, 2018-0780031C6 - 2018 CTF - Q16 - Passive Income Reduction Rules

Holdco and Opco are associated and both have 12-month taxation years ending on 30 June 2019 and 2020. Holdco has investment income of $150,000...

20 September 2018 External T.I. 2018-0771871E5 - Passive Income Reduction and the Business Limit

At all relevant times, a Canadian-controlled private corporation (ACo) with a calendar taxation year and having income of $500,000 per year of...

Articles

Jeanne Cheng, "The Small Business Deduction and the AAII Grind: Is It a Real Problem?", Tax for the Owner-Manager, Vol. 21, No. 3, July 2021, pp. 1-2

S. 125(5.1) grind (p. 1)

- Under s. 125(5.1)(b), when a CCPC, together with any corporations associated with it, earns more than $50,000 of...

Subsection 125(5.2)

Administrative Policy

26 November 2020 STEP Roundtable Q. 14, 2020-0839961C6 - Adjusted Aggregate Investment Income

Would s. 125(5.2) would apply where a corporation transfers active assets to a corporation that is related but not associated? Before indicating...

7 June 2019 STEP Roundtable Q. 16, 2019-0798461C6 - Passive Income

Opco, which is owned by five Holdcos each of which are related to one another but not associated, has established a pattern of paying dividends...

Subparagraph 125(6)(b)(ii) [repealed]

Cases

The Queen v. B & J Music Ltd., 83 DTC 5074, [1983] CTC 50 (FCA)

Since the cumulative deduction account is stated to include "the corporation's taxable income" rather than "the corporation's taxable income while...

Subsection 125(7) - Definitions

Active Asset

Administrative Policy

2 May 2024 External T.I. 2024-1003831E5 - Active assets - intangible assets

Would intangible assets of an active business carried on by a corporation, such as goodwill, customer list, licenses, franchises and quotas, be...

Active Business Carried On by a Corporation

Administrative Policy

10 October 2024 APFF Roundtable Q. 1, 2024-1028361C6 F - Règles de revente précipitée

A Canadian-controlled private corporation (Amalco), which had fewer than five full-time employees and whose principal activity was property...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(13) - Paragraph 12(13)(b) | there are no reorganization continuity rules to avoid triggering a flipped property gain from a disposition upon completion of a reorganization/ meaning of housing unit | 291 |

5 October 2018 APFF Roundtable Q. 17, 2018-0768881C6 F - entreprise exploitée activement – revenu de location

Realtyco is a CCPC holding in Canada six buildings each containing 50 residential units, which it rents out. The sole services provided by it to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Specified Investment Business | principal purpose means main or chief objective | 143 |

16 November 2004 External T.I. 2004-0081941E5 - SIB-leasing of portable trailers&equipment

The activity of leasing portable trailers and equipment would not constitute carrying on a specified investment business as the trailers and...

20 July 2004 External T.I. 2004-0062031E5 F - Actif utilisé dans entreprise exploitée activement

A corporation owned a large area of vacant land in Canada (for instance, in an industrial park) and, as the corporation wished to locate in the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110.6 - Subsection 110.6(1) - Qualified Small Business Corporation Share - Paragraph (c) - Subparagraph (c)(i) | vacant land not used in carrying on a business if merely subdivided and sold | 325 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Business | an adventure is not “carried on” if there is insufficient activity | 225 |

4 July 2001 External T.I. 2001-0068885 F - Entreprise Exploitée Activement

Regarding whether an auto-leasing company had an "active business carried on by a corporation," CCRA noted that the specified investment business...

14 September 2000 External T.I. 2000-0030125 - DAY TRADER-SMALL BUSINESS DEDUCTION

A day trader who incorporated his business likely would qualify for the small business deduction.

Adjusted Aggregate Investment Income

Administrative Policy

3 April 2023 Internal T.I. 2023-0967941I7 - Adjusted Aggregate Investment Income

In response to a query as to whether the adjusted aggregate investment income (“AAII”) of a corporation for a taxation year, which is relevant...

7 October 2020 APFF Roundtable Q. 13, 2020-0852251C6 F - Small Business Deduction

In indicating that a deemed capital gain resulting from the application of s. 55(2)(b) or 55(2)(c) can be considered to be a gain from the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(5.1) | s. 55(2) gain from active-asset shares do not grind business limit | 103 |

Paragraph (c)

Administrative Policy

11 October 2022 External T.I. 2020-0856421E5 - Adjusted AII and Deemed ABI

Payer, a Canadian-controlled private corporation carrying on an active business, pays fair market value rent for the use of real property owned by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 129 - Subsection 129(6) - Paragraph 129(6)(a) - Subparagraph 129(6)(a)(i) | rents excluded from property income by s. 129(6)(a)(i) were also excluded from the recipient's AAII | 54 |

Canadian-Controlled Private Corporation

Cases

Kaleidescape Inc. v. MNR, 2014 ONSC 4983

In order to try to qualify a Canadian corporation ("K-Can'), which economically was a subsidiary of a U.S. corporation ("K-US"), as a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Rectification & Rescission | clarification that directions to a trustee shareholder were to be made by the mooted CCPC's board rather than a non-resident executive | 419 |

Canada v. Bioartificial Gel Technologies (Bagtech) Inc., 2013 DTC 5155 [at at 6361], 2013 FCA 164

In the two taxation years in question, non-residents held 60%, then 70%, of the voting (Class A) shares of the taxpayer. However, provisions of...

Canada v. Perfect Fry Company Ltd., 2008 DTC 6472, 2008 FCA 218

The taxpayer, a Canadian-resident corporation, was wholly owned by a Canadian public corporation ("Perfect Fry") which, in turn, was controlled by...

Sedona Networks Corporation v. Canada, 2007 DTC 5359, 2007 FCA 169

An agreement under which a Canadian-resident private corporation ("Ventures") was accorded the right to exercise, in its sole discretion, the...

Silicon Graphics Ltd. v. Canada, 2002 DTC 7113, 2002 FCA 260

The taxpayer, which was a Canadian corporation with Canadian management, had effected a public offering of its common shares in the U.S. as a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | must be right to affect board or directly influence shareholders | 187 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(6) | 65 | |

| Tax Topics - Statutory Interpretation - Hansard, explanatory notes, etc. | 23 | |

| Tax Topics - Statutory Interpretation - Interpretation Act - Subsection 45(2) | 56 | |

| Tax Topics - Statutory Interpretation - Interpretation Bulletins, etc. | 64 |

Parthenon Investments Ltd. v. Canada (National Revenue), 97 DTC 5343 (FCA)

All the voting shares of the taxpayer were owned by a Canadian corporation all of whose voting shares were owned by a U.S. corporation. All the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | 44 |

International Mercantile Factors Ltd. v. The Queen, 90 DTC 6390, [1990] 2 CTC 137 (FCTD), aff'd 94 DTC 6365 (FCA)

A Canadian-controlled private corporation ("Rieris") held 25% of the common shares of the taxpayer and an additional number of Class A shares...

Scandia Plate Ltd. v. The Queen, 83 DTC 5009, [1982] CTC 431 (FCTD)

"The word 'controlled' as used in the context of the definition means de jure control and not de facto control."

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | 100 | |

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(1) | 178 |

See Also

Durocher v. The Queen, 2016 DTC 1013 [at 2584], 2015 TCC 297, aff'd 2016 CFA 299

The nine resident-individual taxpayers held all the shares of a Canadian corporation (“RJCG”) directly up until April 2005 and indirectly...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Illegality | potential illegality of an option to acquire control of a private corporation did not nullify the option, so that the corporation was not a CCPC | 171 |

| Tax Topics - Income Tax Act - Section 110.6 - Subsection 110.6(1) - Qualified Small Business Corporation Share | potential illegality of 3rd-party option to acquire control of a subsidiary corporation did not nullify the option, so that the subsidiary was not a CCPC | 201 |

Bioartificial gel technologies (Bagtech) inc. v. The Queen, 2013 DTC 1048 [at at 228], 2012 TCC 120, aff'd 2013 FCA 164 supra.

In the two taxation years in question, non-residents held 60%, then 70%, of the voting (Class A) shares of the taxpayer. However, provisions of...

Perfect Fry Company Ltd. v. The Queen, 2007 DTC 588, 2007 TCC 133, aff'd supra 2008 DTC 6472, 2008 FCA 218

Paris J. found (at p. 600) that paragraph (b) of the definition "was not intended to require an attribution of the ownership of shares of a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4) - Paragraph 152(4)(c) | 92 |

Avotus Corporation v. The Queen, 2007 DTC 215, 2006 TCC 505

A non-resident shareholder of the taxpayer, who owned one-half of the taxpayer's shares and, by virtue of being chairman, was entitled pursuant to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Evidence | 70 | |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | 91 | |

| Tax Topics - Income Tax Act - Section 9 - Agency - Agency | 97 | |

| Tax Topics - General Concepts - Effective Date | retroactive agency agreement | 124 |

McClintock v. The Queen, 2003 DTC 576, 2003 TCC 259

The Minister took the position that the taxpayer ceased to be a Canadian-controlled private corporation on July 17, 1990 when it completed an...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Shares | 50 |

Administrative Policy

24 March 2017 External T.I. 2016-0662381E5 F - Control - unanimous shareholders agreement

A mooted Canadian-controlled private corporation (Opco) had its voting common shares held 50-50 by a single non-resident, and by three Canadian...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(5) - Paragraph 251(5)(b) - Subparagraph 251(5)(b)(i) | highly contingent secondary call right of a non-resident on shares of minority residents undercuts for CCPC purposes their USA right to appoint half the board | 601 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(5) - Paragraph 251(5)(b) - Subparagraph 251(5)(b)(ii) | no application if non-resident under USA cannot control board decision to redeem residents’ shares – applies if automatic redemption requirement | 470 |

10 June 2016 STEP Roundtable Q. 7, 2016-0634911C6 - Deemed Resident Trust and CCPC Status

A trust which is factually non-resident but which is deemed to be resident in Canada under s. 94(3) controls a Canadian corporation. Would the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 94 - Subsection 94(3) - Paragraph 94(3)(a) | CCPC status not included in s. 94(3)(a) | 42 |

6 May 2014 CALU Roundtable, 2014-0523301C6 - Control - unanimous shareholders agreement

Does CRA accept Bagtech? After referring to the position in ITTN no. 44) that "unanimous shareholder agreements are not to be considered in...

22 December 2009 Internal T.I. 2009-0343331I7 F - Determination of CCPC Status

A Quebec corporation (the “Corporation”) whose only outstanding shares were common shares, agreed in the Contract with a non-resident...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 220 - Subsection 220(2.2) | s. 220(2.2) precluded accepting a late amendment | 81 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | de facto control given control of financing and significant influence on decisions | 222 |

19 October 2000 External T.I. 2000-0027795 F - SOCIETES PRIVEES SOUS CONTROLE CDN

Corporations controlled (but less than 90% owned) by a Crown corporation in which a provincial government was a 100% shareholder were treated as...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(3) | corporations controlled by the provincial Crown, required to share their business limit | 58 |

| Tax Topics - Income Tax Act - Section 181.5 - Subsection 181.5(6) | corporations controlled by the provincial Crown would not be required to share their capital deduction | 69 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Person | provincial Crown is a person | 20 |

29 August 2000 Internal T.I. 2000-0023187 F - Société privée sous contrôle canadien

A corporation (Opco), the voting rights of which were owned as to 1/3 by an individual and as to 2/3 by a limited partnership of which the general...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(2) - Paragraph 251(2)(b) - Subparagraph 251(2)(b)(i) | GP generally controls a corporation whose voting control is held by a limited partnership | 121 |

7 May 1999 External T.I. 9832645 F - IMPACT DE 94(1)C) SUR LES FIDUCIAIRES

In finding that a corporation would not qualify as a Canadian-controlled private corporation if it was controlled, directly or indirectly in any...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 94 - Subsection 94(3) - Paragraph 94(3)(a) | s. 94(1)(c) does not deem the trustees to be resident for CCPC-definition purposes | 40 |

1 September 1995 External T.I. 5-950393

Where a non-resident owns 60% of the voting shares of a Canadian private operating company, that company will not qualify as a Canadian-controlled...

8 December 1994 External T.I. 9419055 - CCPC,NON-RESIDENT

Provided the provisions of ss.265(5.1) and 251(5)(d) do not apply, two non-resident related individuals who each own 50 voting common shares of a...

Income Tax Regulation News, Release No. 3, 30 January, 1995 under "Canadian-Controlled Private Corporation"

The control test envisages situations where over 50% of the shares of the corporation are owned by one or more non-residents or by one or more...

11 September 1992 T.I. (Tax Window, No. 24, p. 15, ¶2202)

A corporation controlled by an individual who is a resident by virtue only of the sojourning rule in s. 250(1)(a) will qualify as a CCPC, assuming...

91 C.R. - Q.9

The ownership of all the common shares of the corporation by a trust all of whose beneficiaries are non-residents will not preclude the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | 23 |

3 October 89 T.I. (March 1990 Access Letter, ¶1153)

s. 256(1.2)(c) relates to whether a corporation is associated, and therefore is not applicable for determining control for purposes of s. 125(7)(b).

3 January 1990 T.I. 5-9256 (Tax Window Files "'Meaning of Canadian-Controlled Private Corporation' - Control Test"

Where a Canadian-resident private corporation owns all the shares of a resident Canadian corporation ("N") which, in turn, owns all the shares of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | 79 |

Paragraph (a)

Cases

Bresse Syndics Inc. v. Canada, 2021 FCA 115

A public company (CO2 Public) operating a high-tech business in the field of carbon dioxide capture and management carried on its SR&ED through a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | a trust deed requirement that the trustees be the Pubco directors gave Pubco de facto control of a trust subsidiary | 306 |

See Also

CO2 Solution Technologies Inc. v. The Queen, 2019 TCC 286, aff'd sub nom. Bresse Syndics Inc. acting for the bankruptcy of CO2 Solution Technologies Inc. v. The Queen, 2021 FCA 115

After a high-tech company (CO2 Public) engaged in the capture and management of carbon dioxide became a public corporation (thereby losing the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(5) - Paragraph 251(5)(b) - Subparagraph 251(5)(b)(i) | a declaration of trust’s requiring the trustees to be the Pubco directors likely represented a s. 251(5)(b)(i) right of Pubco over trust investment | 291 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | a declaration of trust requiring the trustees to be the Pubco directors gave Pubco de facto control of a trust sub | 248 |

Administrative Policy

19 May 2010 Internal T.I. 2008-0279441I7 F - Canadian-controlled private corporation

During the relevant taxation years of Corporation A (which had claimed the small business deduction), its shares were held equally by Corporation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(5) - Paragraph 251(5)(b) - Subparagraph 251(5)(b)(i) | future acquisition right under a USA gave indirect 50% non-resident shareholder de jure control | 104 |

18 February 2000 Internal T.I. 1999-0008457 F - Life Insurance Corporation

The taxpayer. a life insurance corporation which was deemed by s. 141 to be a public corporation, disposed of shares of a private corporation (the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(9) | status of the subject corporation as controlled by a public corporation was determined immediately before the deemed s. 256(9) acquisition time | 134 |

Paragraph (b)

Administrative Policy

14 June 2010 Internal T.I. 2010-0366611I7 F - Determination of CCPC Status

At issue was whether a start-up Canadian private corporation engaged in SR&ED was a Canadian-controlled private corporation (“CCPC”). ...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(5) - Paragraph 251(5)(b) | sole beneficiary of a trust did not have a s. 251(5)(b) right to trust shares | 44 |

| Tax Topics - General Concepts - Agency | application of Kinguk Trawl test of agency | 165 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | non-resident shareholder with 60%+ economic interest, extensive veto rights and responsibility for future funding of R&D work had de facto control | 457 |

27 February 2008 Internal T.I. 2008-0265901I7 F - Canadian-controlled private corporation

A majority of the voting shares of a mooted CCPC were held by non-residents who did not form a group. The taxpayer acknowledged that those shares...

13 January 2003 External T.I. 2002-0176905 F - CPCC Status

CCRA provided an overview of the application of the different CCPC tests to a factual example, and indicated that the para. (b) test would not...

Paragraph (c)

Administrative Policy

4 December 2000 External T.I. 2000-0001715 F - Qualified small business corporation share

Substantially all of the assets of a private corporation (Holdco) were the shares of a connected corporation (Opco) carrying on a Canadian active...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 48.1 - Subsection 48.1(1) | s. 48.1 election could be made respecting the accrued capital gain on shares that ceased to be QSBCS on a narrowing of the CCPC definition re a connected corp. | 104 |

Designated Member

Paragraph (b)

Subparagraph (b)(i)

Administrative Policy

5 October 2018 APFF Roundtable Q. 5, 2018-0768761C6 F - Partage de la déduction accordée aux petites entreprises

The partners of a professional partnership (ABCD LLP) are Messrs. B and D, who hold their partnership interests directly and the personal Holdcos...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(8) | use of personal holding companies precluded assignment | 318 |

Income of the Corporation for the Year From an Active Business

Cases

Borstad Welding Supplies (1972) Limited v. The Queen, 94 DTC 6205, [1994] 1 CTC 395 (FCTD)

The taxpayer, which owned and operated an industrial gas and welding products business disposed of substantially all the working assets of that...

Freeway Properties Inc. v The Queen, 85 DTC 5183, [1985] 1 CTC 222 (FCTD)

The taxpayer company sold land as part of an active business enterprise. It was found that the sale probably would not have taken place if the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(c) | interest required to be prepaid was receivable | 73 |

Sedgewick Co-operative Association Ltd. v. The Queen, 83 DTC 5455, [1984] CTC 14 (FCTD)

"Income ... from an active business" in s. 125(1)(a)(i) refers to "income ... from a business" in ss.9(1), 18(1)(a) and 20(1)(u) and accordingly...

E.S.G. Holdings Ltd. v. The Queen, 76 DTC 6158, [1976] CTC 295 (FCA)

The circumstances of this case did not differ materially from Rockmore except that the business activities of the taxpayer were turned over to an...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Agency | consequences of carrying on business through agent and employees were the same | 97 |

The Queen v. Rockmore Investments Ltd., 76 DTC 6156, [1976] CTC 291 (FCA)

The taxpayer, which had no full-time employees and made loans to potential borrowers referred to it by independent agents, was held to be engaged...

See Also

Muir Cap & Regalia Limited v. Minister of National Revenue, 91 DTC 533, [1991] 1 CTC 2342 (TCC)

The holding by the taxpayer of substantial term deposits for the future purchase of business premises was "only a collateral purpose ... and the...

Newton Ready-Mix Ltd. v. MNR, 89 DTC 595, [1989] 2 CTC 2369 (TCC)

Funds that were surplus to the day-to-day requirements of the taxpayer's concrete business were invested by it in interest-bearing term deposits....

Administrative Policy

7 March 2002 External T.I. 2001-0091785 - ACTIVE BUSINESS ASSETS - CASH

in finding that cash accumulated to pay annual bonuses to the shareholder-managers was used in the corporation's active business and generated...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110.6 - Subsection 110.6(1) - Qualified Small Business Corporation Share | 384 |

19 July 1996 External T.I. 9607465 - CANADIAN CONTROLLED PRIVATE CORPORATION

In determining whether X Co is a CCPC, where 20% of its shares are held a partnership whose general partner ('Genco") is controlled by a public...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(5) - Paragraph 251(5)(b) | 83 |

14 July 1995 External T.I. 9507915 - LICENSE AGREEMENT REVENUES

"As a general rule, income from a licensing agreement would not be income from an active business because it would be income from a source that is...

26 July 1995 External T.I. 9514695 - ACTIVE BUSINESS ASSETS - SECURITY FOR LOAN

"Where a financing arrangement that is fundamental to the business operations requires certain security to be maintained and it is reasonable to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Small Business Corporation | 104 |

28 April 1993 Internal T.I. 9301657 F - Franchise Royalty Income - Active Business

Discussion of whether lump sum payments received by a franchisor from its franchisees are income from an active business. "If no significant...

92 C.R. - Q.50

Interest or dividend income derived by a corporation that is a trader in securities would pertain to or be incident to its active business.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(1) | 17 |

29 June 1992 T.I. 920958 (December 1992 Access Letter, p. 25, ¶C117-178)

The return of surplus from a pension plan to the employer would constitute active business income provided that the employer's contributions to...

November 1991 Memorandum (Tax Window, No. 13, p. 14, ¶1584)

Funds which a CCPC raises by issuing flow-through shares which require the funds to be expended within 24 months on CEE, etc. will be considered...

90 C.R. - Q56

Recapture of CCA which arises after cessation of a business will be considered to be income whose source is the business in which the asset was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Personal Services Business | 29 | |

| Tax Topics - Income Tax Act - Section 67 | 12 |

October 1989 Revenue Canada Round Table - Q.15 (Jan. 90 Access Letter, ¶1075)

In determining whether term deposits of a corporation which are required as collateral to obtain a line of credit are used in an active business,...

October 1989 Revenue Canada Round Table - Q.17 (Jan. 90 Access Letter, ¶1075)

Where a corporation leases a building to its wholly-owned subsidiary that uses it in its business, with the result that the rent received by the...

IT-73R6 "The Small Business Deduction" 26 March 2002

Reserve claimed against business income is business income when reversed

4. ... If the original gain on the sale of real property was categorized...

Personal Services Business

Cases

Dynamic Industries Ltd. v. Canada, 2005 DTC 5293, 2005 FCA 211

The sole employees of the taxpayer were its sole shareholder ("Martindale") who provided the services of an iron worker and construction manager,...

See Also

Consultants Galaxia Inc. v. Agence du revenu du Québec, 2023 QCCQ 5871

For the three taxation years in issue, the ARQ assessed the taxpayer (“Galaxia”) on the basis that it was carrying on a personal services...

Arora Trading Ltd. v. The Queen, 2019 TCC 98

The appellant (“Arora”) was incorporated on December 18, 2008, and 76% of its shares were held by Ms. Singh, who controlled it. Her husband...

6305521 Canada Inc. v. ARQ, 2017 QCCQ 14869

The ARQ assessed the taxpayer company (“630 Inc.”) on the basis that it carried on a personal services business under the Quebec equivalent of...

Ivan Cassell Limited v. The Queen, 2016 TCC 53

The taxpayer (“ICI”) was owned 75% by an executive (Mr. Cassell) and 25% by his spouse and daughter. ICI derived most of its revenues as fees...

C. J. McCarty Inc. v. The Queen, 2015 TCC 201

The taxpayer ("CJ") was a Canadian corporation owned by an engineer ("McCarty"), his wife and their daughter. CJ entered into a series of three...

9016-9202 Quebec Inc. v. The Queen, 2014 TCC 281

Until 1995, a Quebec garbage collection company ("EBI") employed its garbage collectors and drivers. It then encouraged most of them to each...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 163 - Subsection 163(2) | CRA used penalty as lever to terminate tax avoidance structure | 185 |

G & J Muirhead Holdings Ltd. v. The Queen, 2014 DTC 1067 [at at 3009], 2014 TCC 49 (Informal Procedure)

The taxpayer was owned by its sole employee ("Muirhead") and his wife, and provided well inspection services to an arm's length corporation...

Gomez Consulting Ltd. v. The Queen, 2013 DTC 1125 [at at 670], 2013 TCC 135 (Informal Procedure)

Bédard J found that the taxpayer, wholly owned by an individual ("Almeida"), was operating a personal services business, given that:

- the...

9098-9005 Quebec Inc. v. The Queen, 2012 DTC 1284 [at at 3864], 2012 TCC 324

The taxpayer's director ("Mr. Gitman") and his two sisters inherited equal interests in a number of rental properties and a business, which they...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Office | officer of partnership | 209 |

| Tax Topics - Income Tax Act - Section 96 | partner could be officer but not employee of partnership | 137 |

Peter Cedar Products Ltd. v. The Queen, 2009 DTC 1314, 2009 TCC 463

The principal salesmen and purchasing agents for a brokerage corporation whose business was transacting in cedar shakes and shingles established a...

Robertson v. The Queen, 2009 DTC 679, 2009 TCC 183

The individual taxpayer was the sole shareholder of the corporate taxpayer ("RREL") which, in turn, provided the engineering services of the...

489599 B.C. Ltd v. The Queen, 2008 DTC 4107, 2008 TCC 332

The taxpayer was not carrying on a personal services business given that in addition to five full-time employees it had two part-time employees.

Carreau v. The Queen, 2008 DTC 3106, 2006 TCC 20

A corporation ("9043") of which an individual was the sole shareholder, officer and employee, and which was retained by a contractor of Hydro...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 5 - Subsection 5(1) | 126 |

W. B. Pletch Company Limited v. The Queen, 2006 DTC 2065, 2005 TCC 400

The taxpayer was owned by an individual ("Pletch") and his wife. Pletch served as the president and then as vice-president and director of a...

Galaxy Management Ltd. v. The Queen, 2005 DTC 1558, 2005 TCC 674

The taxpayer, through its key employee, provided sales and purchase services to two companies engaged in the manufacture of knitted garments and...

S & C Ross Enterprises Ltd. v. The Queen, 2002 DTC 2078 (TCC)

The sole shareholder ("Ross") of the taxpayer served as the CFO of a Canadian company ("Clearly Canadian") and also performed services on behalf...

Bruce E. Morley Law Corp. v. The Queen, 2002 DTC 1547 (TCC)

The shareholder of the taxpayer, who previously had been a partner in a law firm providing, or supervising the provision of, the bulk of legal...

Placements Marcel Lapointe Inc. v. MNR, 93 DTC 821, [1993] 1 CTC 2506, [1993] 1 CTC 2261, [1993] DTC 809 (TCC)

A business of providing construction cost appraisal services, which the taxpayer provided to a corporation through the services of its president...

Crestglen Investments Ltd. v. MNR, 93 DTC 462, [1993] 2 CTC 3210 (TCC)

An individual ("Cipora") was an officer of, and served as the general manager of, the taxpayer and by virtue of holding 25% of its shares, was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 96 - Subsection 96(1) - Paragraph 96(1)(f) | partner could not also be an employee | 95 |

Société de Projets ETPA Inc. v. MNR, 93 DTC 516, [1993] 1 CTC 46 (TCC)

The taxpayer, through the services of its shareholder, prepared advertising brochures and folders for various clients, and had the printing work...

David T. McDonald Co. Ltd. v. MNR, 92 DTC 1917, [1992] 2 CTC 2607 (TCC)

The voting preferred shares of the taxpayer were held by Mr. McDonald and its common shares were held by his wife and children. In finding that if...

533702 Ontario Ltd. v. MNR, 91 DTC 982, [1991] 2 CTC 2102 (TCC)

The taxpayer, which purportedly provided services to the third-party customers of the plumbing business of a corporation ("BPH") owned by the...

Administrative Policy

4 June 2013 Ministerial Correspondence 2012-0455101M4 F - Entreprises de prestation de services personnels

In response to a request suggesting more favourable treatment of incorporated professionals in the information technology sector in Quebec, CRA...

7 October 2011 Roundtable, 2011-0411871C6 F - Employé constitué en société

Two spouses provide trucking services on behalf of a corporation operating a PSB to the same third party. Are they incorporated employees so that...

28 November 2010 CTF Roundtable Q. 21, 2010-0386361C6 - 2010 CTF Q21 - Reasonable Salary for Inc. Prof.

CRA stated that para. 1(j) of IT-189R2 ("Corporations Used by Practising Members of Professions") and para. 17 of IC 88-2 ("General Anti-Avoidance...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 121 |

Income Tax Technical News, No. 41, 23 December 2009 Under "Definition of 'Tax Shelter' - Subsection 237.1(1)

Under the "more than five full-time employees test", CRA accepts that the test is met when a corporation has five full-time employees plus one or...

6 November 2008 Internal T.I. 2008-0292561I7 F - DAPE multiple

Four brothers and an unrelated individual, who were actively involved in a succession of construction projects, through their respective...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(2.1) | application of s. 256(2.1) to SBD multiplication where 4 brothers provided their management services to Opco through their respective managementcos | 218 |

28 June 2005 Internal T.I. 2005-0115721I7 F - Entreprise de prestation de services personnels

Various corporations (the “Corporations”) each provided the services of its individual shareholder to customers of the customer corporation...

2004 Ruling 2004-0084311R3 - Incorporating a Partnership

A professional partnership is converted to a Canadian-controlled private corporation ("Newco") pursuant to ss.85(2) and (3) and former partners...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 93 | |

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(2) | 93 |

90 C.R. - Q56

Recapture of CCA which arises after cessation of a business will be considered to be income whose source is the business in which the asset was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Income of the Corporation for the Year From an Active Business | 29 | |

| Tax Topics - Income Tax Act - Section 67 | 12 |

1 February 1999 External T.I. 9823715 - PERSONAL SERVICES BUSINESS

"It is generally the Department's view that a foreign corporation is a 'person' for purposes of the Act unless the context clearly indicates...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Person | 52 | |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(1) - Paragraph 256(1)(a) | 52 |

17 December 1996 External T.I. 9636055 - Personal Services Business

A foreign corporation is a "corporation" and a "person" for purposes of the Act.

26 February 1991 T.I. (Tax Window, Prelim. No. 3, p. 5, ¶1128)

S.125(7)(d) does not require that the individuals be reasonably regarded as officers or employees of the corporation with respect to the services...

11 September 89 T.I. (February 1990 Access Letter, ¶1122)

Opco, which has imposed a hiring freeze, nonetheless would like to engage services of Mr. A to complete a specific project over a 2-year period on...

IT-73R6 "The Small Business Deduction" 26 March 2002

Common-law test of employment

19. The condition stipulated in [the midamble] is not met if, in the absence of the corporation, there would be no...

IT-168R3 "Athletes and Players Employed by Football, Hockey and Similar Clubs" under "Non-Residents"

Articles

Michael Gemmiti, "Placement Agencies: Insurable and Pensionable Employment", Canadian Tax Highlights", Vol. 22, No. 3, March 2014, p. 10.

Source deduction liability of placement agency (p. 10)

A placement or employment agency is potentially liable to make contributions under the...

Sophie Virji, "Old News, New Trend: Personal Services Business on the Rise", CCH Tax Topics, Number 2192, March 13, 2014, p. 1.

Ubiquity of oil field independent contracors (p.1)

[O]il and gas producers…have often outsourced their oil field work to corporations owned by...

Specified Corporate Income

Administrative Policy

20 April 2017 External T.I. 2016-0679721E5 - The small business deduction

SellCo A and SellCo B sell all of their fishing catch to BuyCo (also a CCPC), although BuyCo 1 purchases the majority of its fish from unrelated...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(1) - Paragraph 125(1)(a) - Subparagraph 125(1)(a)(i) - Clause 125(1)(a)(i)(B) | illustration where sales to related corporation | 105 |

Paragraph (a)

Subparagraph (a)(i)

Administrative Policy

23 January 2025 External T.I. 2024-1030091E5 - Specified Corporate Income - Realtor Commissions

Mr. A wholly owned a personal real estate corporation (A Co) and a holding company (B Co) which, in turn, held 25% of the shares of a real estate...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(1) - Paragraph 125(1)(a) - Subparagraph 125(1)(a)(i) - Clause 125(1)(a)(i)(B) | the specified corporate income carve-out may be avoided by earning active business income through rather than from a private corporation | 248 |

26 January 2023 External T.I. 2021-0887661E5 - Small Business Deduction - Related

Mr. X wholly-owned ACo and his wife, Mrs. X, wholly-owned BCo. ACo and BCo were not associated. Neither company provided services or property,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(1) - Paragraph 125(1)(a) - Subparagraph 125(1)(a)(i) - Clause 125(1)(a)(i)(B) | 2 related but not associated CCPCs with no cross-business dealings did not have an s. 125(1)(a)(i)(B) grind | 79 |

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(5.1) - Paragraph 125(5.1)(a) | non-associated but related corporations not required to aggregate their taxable capital | 89 |

20 October 2022 External T.I. 2020-0869681E5 - Specified Corporate Income

Mr. A owned 50% of a real estate management company (Hco), which derived substantially all of its income from providing services to Wco, which...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(3.2) | permitted assignment of business limit to the extent of “specified corporate income” | 196 |

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(3.2) | permitted assignment of business limit to the extent of “specified corporate income” |

Articles

Joint Committee, "Small Business Deduction Rules under Section 125 of the Income Tax Act - Follow-Up to Our Meeting with Canada Revenue Agency", 2 June 2017 Joint Committee Submission to Finance respecting the Small Business Deduction, appending Submission to Randy Hewlett of the Income Tax Rulings Directorate dated 14 February 2017

Issues with cooperatives (p. 2)

Every farming or fishing Canadian-controlled private corporation (“CCPC”) selling substantially all of its...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Specified partnership income - Paragraph (c) | 62 |

Clause (a)(i)(B)

Subclause (a)(i)(B)(I)

Administrative Policy

23 February 2021 External T.I. 2018-0769891E5 F - 125(7) "revenu de société déterminé"

Opco A (wholly-owned by Mr. A) and Opco B (wholly-owned by Mr. B, who deals at arm’s length with Mr. A) each hold 50% of the shares in Opco D....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | presumption that two 50% shareholders act together to control the corporation | 147 |

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(1) - Paragraph 125(1)(a) - Subparagraph 125(1)(a)(i) - Clause 125(1)(a)(i)(B) | services income from multiple investee private corporations can be bad income for purposes of the specified corporate income - s. (a)(i)(B) safe harbour | 385 |

Paragraph (b)

Administrative Policy

13 June 2017 STEP Roundtable Q. 1, 2017-0693461C6 - Specified corporate income

The determination of what otherwise would be a corporation’s “specified corporate income” for small business deduction purposes is deemed by...

Specified Investment Business

Cases

Weaver v. Canada, 2008 DTC 6517, 2008 FCA 238

The taxpayers each owned 25% of the shares of a Canadian-controlled private corporation ("SRP") that headleased reserve land from an Indian band...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Small Business Corporation | previous active business not relevant | 97 |

| Tax Topics - General Concepts - Ownership | beneficial ownership can be transferred orally before date of written agreement | 129 |

| Tax Topics - General Concepts - Agency | business activeness can be attributable to an agent | 181 |

Baker v. Canada, 2005 DTC 5266, 2005 FCA 185

Six individuals employed as custodians for the purpose of providing cleaning services to tenants of the taxpayer, and who worked from 6 p.m. to 10...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Equal Treatment | interpretive standard should not be subjective and variable | 114 |

Lerric Investments Corp. v. Canada, 2001 DTC 5169, 2001 FCA 14

The taxpayer, which employed two full-time employees directly, also had fractional co-ownership interests in eight apartment projects which also...

See Also

1717398 Ontario Inc. (Lost Forest Park) v. The Queen, 2019 TCC 183

The taxpayer, which had one employee, owned and ran a campground consisting of approximately 150 fully-serviced sites for use by mobile...

Rocco Gagliese Productions Inc. v. The Queen, 2018 TCC 136

The taxpayer was wholly-owned by an individual (“Gagliese”) who, through the taxpayer, was retained by clients such as the CBC to compose and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 129 - Subsection 129(4) - Income or Loss - Paragraph (b) | royalty income from reruns was incidental business income | 82 |

Huntly Investments Limited v. The Queen, 2017 TCC 255

The taxpayer owned and rented five buildings (houses and small apartment buildings) in downtown Vancouver. In addition to using an arm’s length...

0742443 B.C. Ltd. v. The Queen, 2014 DTC 1208 [at at 3811], 2014 TCC 301, aff'd 2015 DTC 5115 [at 6304], 2015 FCA 231

The taxpayer, which had two employees including its shareholder, carried on a storage unit rental business.

Before referring to the "principal...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Onus | Minister's pleading of assumptions of law does not relieve taxpayer from entering a case | 106 |

R&C Commrs v. Lockyer & Anor (for Pawson Estate), [2013] UKUT 050 (Tax and Chancery Chamber)

The deceased taxpayer and her three children held equal interests in a bungalow ("Fairhaven"), which they rented out as a holiday property. The...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Investment Business | actively-managed rental property an investment business | 407 |

Langille v. The Queen, 2009 DTC 1103 [at at 564], 2009 TCC 139

The taxpayer who was the sole director and officer of a corporation ("Alland") owned by him and a family trust, lent money in order for Alland to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(1) - Paragraph 39(1)(c) | 139 |

Lee v. R, 99 DTC 925, [1999] 3 CTC 2200 (TCC)

A corporation whose business was the operation of a 68-pad mobile home park on land which it owned was found to be carrying on a specified...

Ben Raedarc Holdings Ltd. v. R., 98 DTC 1218, [1998] 1 CTC 2774 (TCC)

Margeson TCJ. found (at p. 1225) that janitors "who worked all or substantially all of four hours per day, five days a week, throughout the years...

Rogers v. The Queen, 97 DTC 890 (TCC)

A corporation that derived virtually all its income from the rental of a shopping centre owned by it was found to be engaged in a specified...

Canwest Capital Inc. v. The Queen, 97 DTC 1, [1996] 1 CTC 2974 (TCC)

A sum of $5 million was injected into the taxpayer with a view to being utilized in leasing activities. The portion of the sum that the taxpayer...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 129 - Subsection 129(1.2) | 87 |

Crompton v. The Queen, 96 DTC 1700 (TCC)

A corporation owned by the taxpayer and his wife that did a high volume of trading in securities on the Vancouver Stock Exchange was found to be a...

The Queen v. Hughes & Co. Holdings Ltd., 94 DTC 6511, [1994] 2 CTC 170

A practising lawyer who spent approximately 28 hours per year on telephone calls monitoring the business of the taxpayer in addition to making...

Temax Investments Inc. and Mayon Investments Inc. v. Minister of National Revenue, 91 DTC 364, [1991] 1 CTC 2245 (TCC)

The business of the taxpayers which consisted of providing mortgage financing on the security of second, third and fourth mortgages was found to...

Administrative Policy

3 September 2025 External T.I. 2024-1007671E5 - Active business

A corporation with one employee, which was engaged in forest management, generated fees from stumpage and the sale of carbon offset credits....

3 March 2000 Internal T.I. 2000-0002337 F - COOPERATIVES

A cooperative incorporated under the Quebec Cooperatives Act financed the cattle purchases by its members. Its articles stated that its purpose...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 137 - Subsection 137(6) - Credit Union | Quebec cooperative did not qualify as a credit union in light of not being incorporated under the Credit Unions Act and not having statutory authorization to conduct business as a credit union | 125 |

5 March 2024 External T.I. 2023-0962831E5 - Active business income – Income from solar panels

The sole business activity of a Canadian-controlled private corporation (the “Corporation”) was to build a small utility-scale solar array on...

13 February 2020 External T.I. 2019-0826051E5 - Income from a securities trading business

Would the trading of securities, such as speculative futures and options contracts on commodities, by a corporation be on income or capital...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Futures/Forwards/Hedges | a CCPC can have a trading business | 114 |

7 June 2019 STEP Roundtable Q. 7, 2019-0798321C6 - Income Author / Musician

Gagliese Productions found that royalty income of an author/musician was income from services because the person who derived the income was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 129 - Subsection 129(4) - Income or Loss | royalty income was incident to composing active business | 102 |

5 October 2018 APFF Roundtable Q. 17, 2018-0768881C6 F - entreprise exploitée activement – revenu de location

In the course of a general discussion as to whether a Canadian-controlled private corporation with rental properties carried on an active...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Active Business Carried On by a Corporation | question of fact whether a CCPC with too many employees to have a specified investment business carries on a business | 218 |

24 May 2011 External T.I. 2010-0387741E5 F - Revenu d'entreprise exploitée activement

A corporation with fewer than six full-time employees leases six trailers to contractors in order for them to lodge their employees, provides the...

16 June 2010 External T.I. 2009-0335731E5 - SIB and Partnership

CCRA indicated that a business carried on by three corporations as members of a partnership will not be a specified investment business if the...

14 April 2009 External T.I. 2007-0238221E5 F - Rights of musician-Transfer

As part of a general response respecting the transfer of rights by a musician to a corporation, CRA stated:

Although royalty income is generally...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(4) | s. 56(4) generally will apply where royalty is transferred without assignment of copyright, with exception of SOCAN royalty | 165 |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | s. 56(2) not applicable where copyright or royalty interests transferred at FMV | 75 |

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1.1) | right to royalties from SOCAN constituted eligible property | 109 |

20 January 2009 External T.I. 2008-0284681E5 - Specified Investment Business

Canadian-resident family members of a family own shares in 3 holding companies, Holdco #1, Holdco #2 and Holdco #3, which hold partnership...

23 January 2008 Internal T.I. 2007-0258011I7 - QSBC Shares - Partnership Interest

Aco, a Canadian-controlled private corporation, holds rental apartment complexes, and an interest in a partnership (between it and two related...

7 June 2006 External T.I. 2005-0139641E5 F - Employés à plein temps

Does an employee working at least 30 hours per week at a medical clinic qualify as a full-time employee, provided that the employee's work...

21 June 2002 External T.I. 2001-0107705 F - Partie XIII et logiciels d'ordinateurs

CCRA indicated that it was a question of fact whether a CCPC software developer generating royalties from licensing its work was thereby deriving...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(d) | exemption for shrink-wrapped software not applicable where it is downloaded | 249 |

6 June 2002 External T.I. 2002-0133895 F - entreprise de placement determinee

Realtyco, which carried on an active business of operating a rental residential real estate portfolio which was not a specified investment...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 13 - Subsection 13(1) | recapture is treated as income from the business in which the depreciable asset was used | 129 |

26 March 2001 External T.I. 2001-0063925 - SPEC. INVESTMENT BUSINESS

A corporation whose only business was the purchase of accounts receivable from an associated corporation at a discount and the collection of those...

21 February 2001 External T.I. 2000-0047815 - income from partner. from invest.

A property management corporation also hold a minority interest in several partnerships whose only activity is holding rental property. The...

18 July 2000 External T.I. 2000-0016015 F - REEA - LOCATION ET AUTRES SERVICES

Regarding whether the income of a corporation - that offers office space rental services and a conference room, secretarial, reception, telephone...

19 January 1998 External T.I. 9830955 - PAWNBROKER - SPECIFIED INVESTMENT BUSINESS?

A pawnbroker fees would be considered to be interest for the purpose of determining whether a pawnbroker business is a specified investment business.

26 September 1997 External T.I. 9722915 - ROYALTY INCOME AS ACTIVE BUSINESS INCOME

"If a company is in the business of composing music, the income it earns with respect to its copyrighted music would generally be considered...

9 October 1996 External T.I. 9629195 - : Specified Investment Business

The leasing of taxi licences to arm's length parties is a specified investment business unless there are more than five full-time employees.

17 July 1995 External T.I. 9504135 - SPECIFIED INVESTMENT BUSINESS

"In the case of a corporation which carries on a business involving tennis courts and has a weight/exercise room the extent of the services it...

31 March 1995 External T.I. 9501215 - SMALL BUSINESS CORPORATION - XXXXXXXXXX

"It is our opinion that normally a full-service motel operation would be providing a sufficient level of services such that it would not be...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Small Business Corporation | 98 |

27 March 1995 External T.I. 9430105 - SPECIFIED INV. BUS.

No relief is provided in the situation where, for a portion of the year, there are only five full-time employees rather than six.

14 July 1994 External T.I. 9411495 - CAPITAL GAINS EXEMPTION

A partnership having less than six full-time employees that is engaged principally in providing rental spaces for mobile homes and offers no more...

24 March 1994 External T.I. 9401245 - SPECIFIED INVESTMENT BUSINESS

A taxpayer that rents storage facilities to clients who use the facilities to store raw materials used by them in their manufacturing activities...

3 March 1994 External T.I. 9332935 F - Active Business and Asset Used in an Active Business

Although offering a motel, with rooms rented on a daily basis and services provided, will be an active business, it will be a specified investment...

4 February 1994 External T.I. 9325245 F - Small Business Corp

In applying the five full-time employee test with respect to a partner's income from the particular partnership, each full-time employee of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Small Business Corporation | 120 |

91 C.R. - Q.31

Where a corporation has more than five full-time employees, whether interest income is derived from a specified investment business will turn upon...

21 August 1991 T.I. (Tax Window, No. 8, p. 18, ¶1400)

Where a corporation provides rental storage facilities and a moving operation, it is a question of fact whether it is conducting an active...

26 June 1991 T.I. (Tax Window, No. 4, p. 25, ¶1316)

Where a corporation employs three employees in its real estate rental operation and three more who are licensed real estate brokers, it is a...

26 February 1990 T.I. (July 1990 Access Letter, ¶1332)

Generally speaking, royalty income is income from property. However, where it is incidental to an active business carried on by the recipient...

19 September 89 T.I. (February 1990 Access Letter, ¶1123)

A corporation which conducts a seasonal business which employs 10 to 15 employees for six months and 2 or 3 employees for the rest of the year...

11 September 89 T.I. (February 1990 Access Letter, ¶1123)

Where a corporation which is one of a group of corporations in the business of leasing rental properties employs a 7-man maintenance crew which...

88 C.R. - Q.51

Each full-time employee of a particular partnership will be considered to be a full-time employee of each corporate partner. In the case of a...

81 C.R. - Q.30

A corporation may carry on more than one business, one of which may give rise to income from an active business, and another which may give rise...

IT-73R6 "The Small Business Deduction" 26 March 2002

Hotel business is services business

A corporation that operates a hotel is generally considered to be in the business of providing services and...

Paragraph (a)

Administrative Policy

17 June 2004 External T.I. 2003-0045411E5 F - Entreprise de placement déterminée

Xco co-owns several rental properties (in the commercial sector) in co-ownership with other taxpayers with which it deals at arm's length and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 4 - Subsection 4(1) - Paragraph 4(1)(a) | business carried on through partnership is separate from similar business carried on directly by partner | 181 |

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Specified Investment Business - Paragraph (b) | para. (b) may not apply where the SIB is carried on through a partnership | 276 |

Paragraph (b)

Administrative Policy

31 March 2005 External T.I. 2004-0101171E5 F - Entreprise de placement déterminée

XCo employs four people full time in its business of renting out buildings, and YCo, which is associated with it, provides the management,...

17 June 2004 External T.I. 2003-0045411E5 F - Entreprise de placement déterminée

Xco co-owns several rental properties (in the commercial sector) in co-ownership with other taxpayers with which it deals at arm's length and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Specified Investment Business - Paragraph (a) | partnership business is transparent but separate from similar business carried on directly | 181 |

| Tax Topics - Income Tax Act - Section 4 - Subsection 4(1) - Paragraph 4(1)(a) | business carried on through partnership is separate from similar business carried on directly by partner | 181 |

Specified partnership income

Administrative Policy

6 May 2016 External T.I. 2016-0646411E5 - Professional corporation & small business deduction

CRA noted that the 2016 Budget proposes to extend the specified partnership income rules to partnership structures in which a Canadian-controlled...

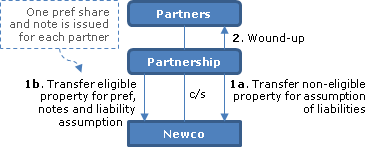

2012 Ruling 2011-0392041R3 - Incorporation of a Professional Partnership

{kind=link}

Ss. 85(2) and(3) Partnership conversion to Newco

All the "Partners" of a professional partnership (the "Partnership") are resident in Canada and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(3) | non s. 85(2) property allocated exclusively to liability assumption, and share/note consideration pre-allocated | 360 |

2013 Ruling 2013-0498961R3 - Partner creating a professional corporation

underline;">: Existing structure. The professional partnership in question already has Non-Incorporated Partners who provide their Professional...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(2.1) | incorporated partners of professional partnership | 114 |

25 February 2014 External T.I. 2012-0448431E5 - Reporting of Income by Estate

A Canadian-controlled private corporation (Corp) is a member of a top-tier holding partnership (Partnership A) which is a direct member of two...

2012 Ruling 2012-0447491R3 - Professional corporation contracting with partshp