Administrative Policy

15 May 2019 IFA Roundtable Q. 8, 2019-0798841C6 - Active Trade or Business Test under the LOB Clause

Canco (which is purely a holding company for FA carrying on business in a third country) pays a dividend to USco, which is owned by individuals...

8 September 2017 External T.I. 2014-0549771E5 - Article XXIX-A:3

The sole beneficiary of a trust (the “Trust”) that is resident in the U.S. for purposes of the Canada-U.S.Treaty is the parent of a US group...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(2) - Paragraph 251(2)(b) - Subparagraph 251(2)(b)(i) | a trust is related to a sub of its corporate trustee | 74 |

| Tax Topics - Treaties - Income Tax Conventions - Article 3 | "person related thereto" defined by ITA meaning of "related person" | 39 |

5 November 2015 Internal T.I. 2013-0496401I7 - XXIX-A(3) - Active Trade or Business Exception

To help fund the indirect acquisition of NR-Target (which was not resident in Canada or the U.S.) by Canco (an indirect subsidiary of non-resident...

2 December 2014 CTF Roundtable, Q. 7

In what circumstances would CRA consider a US business to be "substantial" in relation to a Canadian business for purposes of Art. XXIX-A, para. 3...

Factor

(US vs. CAN)

Situation A

Situation B

Situation C

Situation D

To date… Rulings has not...

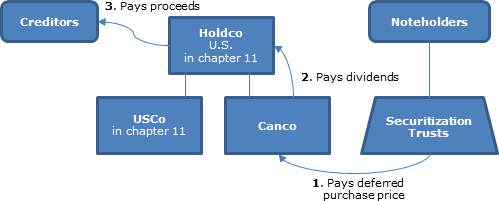

2014 Ruling 2013-0511761R3 - Cross-border financing Canada - USA

{kind=link}

ForSub, which is a U.S.-resident wholly-owned C-Corp subsidiary of ForCo, an LLC, will acquire from ForCo an interest-bearing note (the CanSub...

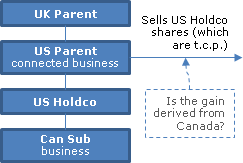

22 May 2014 May IFA Roundtable, 2014-0526711C6 - Article XXIX-A(3) of the US Treaty

{kind=link}

UK Parent owns US Parent, which owns US Holdco (whose shares are taxable Canadian property) which owns Can Sub. US Parent sells US Holdco. Does...

26 November 2013 CTF Roundtable, 2013-0507961C6 - Article XXIX-A LOB provisions

Q. 5(a) Super-voting shares

Where a company has multiple classes of voting shares, with one or more of the classes thinly traded or not at all,...

2013 Ruling 2012-0471921R3 - Deemed dividend on return of capital

{kind=link}

Canco and U.S. Holdco

Canco, which is an unlimited liability company, is wholly owned by U.S. Holdco, which is resident in the U.S. for purposes...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 4 | PUC increase and distribution | 402 |

28 November 2010 Annual CTF Roundtable, 2010-0387001C6 - Canada-US Treaty LOB - Treatment of Interest

Canco has both qualifying active business income from a Canadian business that is connected with an active trade or business (the connected...

17 May 2012 IFA Roundtable, 2012-0444151C6 - Hybrid Partnerships and Branch Tax Liability

The two partners of a partnership which has elected to be a domestic corporation for Code purposes are: a corporation which is resident in the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 10 | 265 |

2012 Ruling 2012-0435211R3 - Article XXIX-A(3) of the Canada-US Tax Convention

{kind=link}

Holdco, which had been a listed U.S. company, was taken private by L5, which is a fund whose members are not known. Holdco and its subsidiary,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 10 | 170 |

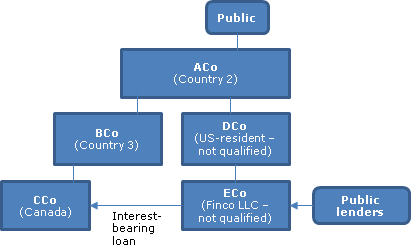

2012 Ruling 2012-0458361R3 - Cross-Border Financing

{kind=link}

ECo, which is fiscally transparent for U.S. purposes and resident in the U.S. (a.k.a., Country 1) but is not a qualifying person (as defined in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 4 | derivative benefit re loan interest | 309 |

28 June 2010 External T.I. 2009-0329511E5 - United States - Dividend Withholding Rate

A U.S. resident citizen is the sole shareholder of a U.S. Subchapter S corporation (S-Corp), which is the sole shareholder of a U.S. LLC (which is...

12 April 2010 External T.I. 2009-0317941E5 - Canada-US Tax Convention - Article XXIX A

How will CRA interpret "paid or payable...directly or indirectly" in Art. XXIX A(2)(e) and (4)(b) of the Canada-U.S. Convention? CRA...

8 December 2009 TEI Roundtable Q. 4, 2009-0347701C6 - Qualifying person & multiple shares

The correspondent noted that in Canada, if each class of shares of a public company with multiple classes must be considered separately for...

16 September 2009 Roundtable, 2009-0336401C6 - Article XXIX A(3) of the Canada-U.S. Tax Treaty

Regarding whether Canadian-source income has been derived by a U.S. resident in connection with an active trade or business in the U.S., CRA...

28 May 2009 Internal T.I. 2009-0319161I7 - Canada-US Treaty - Article XXIX A(3)

CRA will therefore interpret the term 'registered securities dealer' to mean:

- a 'registered securities dealer' for the purposes of the Income...

Income Tax Technical News, No. 41, 23 December 2009 Under "Definition of 'Tax Shelter' - Subsection 237.1(1)

Assume that USco carries on an active business in the United States (other than an investment business). USco owns all of the shares of Canco, a...

17 July 2008 IFA Roundtable, 2008-0272361C6 - Limitation of Benefits

Will CRA look through LLCs and other entities that are fiscally transparent for US purposes, in applying paras. 2(d) and (e) of "qualifying...

Articles

Steve Suarez, "Canada to Unilaterally Override Tax Treaties with Proposed New Anti-Treaty-Shopping Rule", Tax Notes International, 3 March 2014, 797-806.

Comment on Jim Wilson article (below)/inappropriateness of main purpose test in new anti-Treaty shopping rule (p. 804)

As noted by that learned...

Koichiro Yoshimura, "Clarifying the Meaning of 'Beneficial Owner' in Tax Treaties", Tax Notes International, November 25, 2013, p. 761.

Alternative OECD-suggested approaches to Limitations-on-Benefits clauses (p.767)

1. Approaches as Proposed in the OECD...

Angela W. Y. Yu, Grace W. Loh, "Ambiguity in the U.S.-Canada Treaty's Publicly-Traded Test Should Be Resolved in Favor of Canadian Dual-Class Public Companies", Tax Management International Journal, 2011, p. 589

There are no valid policy reasons to prevent a dual-class public company from aggregating its share classes to satisfy; the publicly-traded test...

Elinore J. Richardson, Stephanie Wong, "Cross-Border Financing Into Canada More Difficult Under Canada's New LLB Provision", Corporate Finance, Vol. XVI, No. 1, 2009, p. 1734

Vern Krishna, "Limitation on Treaty Benefits: Part One", Canadian Current Tax, Vol. 20, No. 1, October, 2009, p. 1.

Edward Miller, "Potential Limitations of the Limitation on Benefits Clause in the Fifth Protocol to the Canada-U.S. Income Tax Convention", International Tax, CCH, December 2007, No. 37, p. 4.

Finance

12 August 2013 Consultation Paper on Treaty Shopping – The Problem and Possible Solutions:

Invitation for comments.

The Government invites...