Cases

R. v. Melford Developments Inc., 82 DTC 6281, [1982] CTC 330, [1982] 2 S.C.R. 504

The exclusion in Article III(5) of the Canada - Germany Income Tax Agreement Act, 1956 of "income (e.g. dividends interest, rents or royalties)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 214 - Subsection 214(15) | 71 | |

| Tax Topics - Treaties - Income Tax Conventions | 59 |

The Queen v. Associates Corp. of North America, 80 DTC 6140, [1980] CTC 215 (FCA)

Guarantee fees received by a U.S. corporation from its Canadian subsidiary did not constitute "interest" within the meaning of the 1942...

See Also

Revenue and Customs v Burlington Loan Management DAC , [2026] EWCA Civ 461

BLM was an Irish-resident investment company which had already acquired a substantial number of proved claims in the administration of Lehman...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Multilateral Instrument - Article 7 - Article 7(1) | purchasing an interest claim on the basis of treaty exemption did not indicate a purpose of “taking advantage” of that exemption | 398 |

| Tax Topics - Treaties - Income Tax Conventions - Article 3 | phrase “one of the main purposes” likely was not to be interpreted on the basis of domestic anti-avoidance jurisprudence | 186 |

Vietjet Aviation JSC v FW Aviation (Holdings) Limited , [2025] EWCA Civ 783

One of the issues in a commercial dispute relating to aircraft financing agreements that were in default was whether the claimant assignee of the...

Aiken Industries Inc v Commissioner of Internal Revenues, (1971) 56 TC 925

A US corporation ("MPI"), owned by a Bahamian company ("ECL"), issued a loan note to ECL for a total principal sum of $2,250,000 carrying interest...

Administrative Policy

15 May 2019 IFA Roundtable Q. 3, 2019-0798741C6 - Participating Debt Interest & US Treaty

2016-0664041R3 dealt with a term loan which included both periodic non-participating interest payments, as well as future additional payments (the...

2017 Ruling 2017-0712731R3 - Amount of withholding tax under paragraph 212(1)(b)

Four non-resident LPs with the same non-resident corporate general partner (GP Co) collectively control Canco through their holdings of a common...

7 September 2016 External T.I. 2014-0563781E5 - Articles 10 and 11 of Canada-UK Treaty

A UK corporation (“GP Co”) is the general partner (with a 1% interest) of a UK limited partnership which is fiscally transparent for UK...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 10 | limited partners generally do not have control over a company’s voting power/an over-10% limited partner is considered to “indirectly” own over 10% of an LP subsidiary | 471 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | limited partners of an LP could deal at arm’s length with a Canadian sub of the LP | 222 |

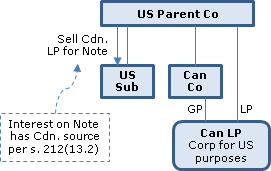

2014 Ruling 2014-0521831R3 - Withholding on interest payments

{kind=link}

Structure

US Parent Co, which is a U.S. public corporation and a qualifying person under the Canada- U.S. Treaty, carries on business in Canada...

26 August 2013 Internal T.I. 2013-0494211I7 - participating debt interest

Canco, which carries on a business of exploring and developing oil and gas properties in Canada (so that its principal assets consist of rights to...

6 September 2013 External T.I. 2013-0478241E5 - U.K. Individual Savings Account (ISA)

Although income earned in a UK Cash ISA is not subject to taxation in the U.K., under the Canadian Income Tax Act ("Act") Canadian residents ......

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(c) | 103 | |

| Tax Topics - Treaties - Income Tax Conventions - Article 18 | 117 |

17 May 2012 IFA Roundtable, 2012-0444041C6 - IFA 2012 - Beneficial Ownership

When asked to "comment on what factors it will take into account in determining beneficial ownership," CRA stated:

Where a recipient of income...

21 May 2009 IFA Roundtable Q. 1, 2009-0321451C6 - Meaning of beneficial owner in Article 10, 11 & 12

In the Prévost Car case, "the Court implied that where an intermediary acts as a mere conduit or funnel in respect of an item of income, the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 10 | 80 |

7 May 2004 IFA Roundtable Q. 1, 2004-0072131C6 - IFA Round Table 2004 Q.1 - 212(13.1)(a)

In the context of a "tower" structure, a partnership of which two taxable Canadian corporations are the partners borrows money from a U.S....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(b) | partnership borrower was transparent | 129 |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(13.1) - Paragraph 212(13.1)(a) | where s. 212(13.1)(a) does not apply, it may be possible to consider a Canadian partner to be an interest payer | 221 |

5 February 2002 Internal T.I. 2000-0058637 - Interest Paid to Non-Resident

Where the Australian branch of a Canadian bank pays interests to an Australian subsidiary of the bank, the interest paid would not be covered by...

1 February 2002 External T.I. 2001-007820

The exclusion in subparagraph 3(b) of Article XI of the Canada-Argentine Convention is applicable where the payor of the interest is not the final...

30 November 1996 Ruling 9729263 - TRUST DISTRIBUTIONS TO NON-RESIDENT BENEFICIARIES

Ruling that where income of a Canadian trust was distributed to a U.S. partnership, then subject to Article XXIXA of the Canada-U.S. Income Tax...

23 July 1996 External T.I. 9612365 - ARTICLE XI(4) & "INCOME ASSIMILATED TO INCOME"...

A payment by a credit union to a member, in respect of a share of capital stock, which is deemed to be interest by s. 137(4.1) of the Act will be...

24 May 1995 Internal T.I. 9505086 - ART XI(3)(e) Canada-U.S. Income Tax Convention

Where a decision was made with respect to an interest-bearing obligation of a company that the interest due and payable for that year would not be...

1 March 1995 External T.I. 9426805 - WITHHOLDING TAX ON INTEREST (HAA 4093 U5-100-11)

The exemption in the post-1994 version of paragraph 3(d) of Article XI of the Canada-U.S. Convention would apply to exempt interest paid by a...

93 C.M.TC - Q. 15

The reductions in rates of withholding tax pursuant to the 1991 protocol to the Mexico Convention (arising when Mexico agrees to a lower rate in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 5 | 25 |

17 July 1992 T.I. 920168 (January - February 1993 Access Letter, p. 35, ¶C180-134)

Whether an arrangement under which the U.S. seller assigned its receivables, or nominated a U.S. bank as its agent to collect the receivables,...

1 May 1991 Memorandum (Tax Window, No. 3, p. 25, ¶1228)

Discussion of modification to position contained in 4 September 1990 memorandum.

15 November 1990 TI 902937

Interest on a borrowing by a U.S. resident to acquire a rental property in Canada would be subject to Canadian withholding tax if the rental...

4 September 1990 Memorandum (Tax Window, Prelim. No. 1, ¶1013)

Where an individual who has Canadian source income which is fully taxable in Canada (e.g., employment income) but who is deemed by the tie-break...

Articles

Ian Bradley, Denny Kwan, Dian Wang, "Is The Back-to-Back Withholding Tax Regime an Effective Anti-Treaty-shopping Measure?", Canadian Tax Journal, (2016) 64:4, 833-58

Inconsistency of back-to-back s. 212(3.2) rules with Canada’s Treaty obligations (p. 851)

[E]ven LOB rules, which operate in a mechanical...

Abraham Leitner, "BEPS Targets Commonly Used Canada-U.S. Hybrid Structures", Tax Notes International, 9 February 2015, p. 531.

BEPS Report (p. 531)

…‘‘Neutralising the Effects of Hybrid Mismatch Arrangements,'' was released by the OECD on September 16, 2014, as part...

Andrew Spiro, Ian Caines, "Welcome News from the CRA in the Continuing Saga of Cross-Border Convertible Debt", International Tax, Number 73, December 2013, p. 5.

Narrowness of U.S. Treaty definition (p. 8)

The definition of "participating interest", while similar to the Canadian domestic definition, notably...

Marco Rossi, "An Italian Perspective on the Concept of Beneficial Ownership", Tax Notes International, December 23, 2013, p. 1133.

Application of 1977 OECD commentary on beneficial ownershp to Italian manatarios (p. 1139)

The commentary stated that the limitation of tax in the...

Michael N. Kandev, Matthew Peters, "Treaty Interpretation: The Concept of 'Beneficial Owner' in the Canadian Tax Treaty Theory and Practice", Canadian Tax Foundation, 2011 Conference Report, 26:1-60

Is "beneficial owner" a question of legal or economic substance? (p. 3)

On the one hand, "beneficial owner" may be construed in light of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Treaties | 121 |