Subsection 212(2) - Tax on dividends

Cases

Canada v. Hutchison Whampoa Luxembourg Holdings S.À R.L., 2025 FCA 176, aff'g sub nom. Husky Energy Inc. v. The King, 2023 TCC 167

Before a Canadian public corporation (“Husky”) paid a dividend on its shares, two significant shareholders of Husky resident in Barbados (the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 10 | a securities loan between residents of two Treaty countries did not change the beneficial ownership of the transferred shares | 345 |

| Tax Topics - General Concepts - Substance | agreements styled as securities lending agreements were not such in their legal substance | 202 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(1) | CRA assessments of dividend payer under s. 215(6) and “protective assessments” of dividend recipients under s. 212(2) were “troubling” in light of Galway principle | 239 |

| Tax Topics - Income Tax Act - Section 215 - Subsection 215(6) | CRA decisions to make “protective assessments” of the dividend recipients under s. 212(2) in addition to assessing the dividend payers under s. 215(6) was troubling under Galway | 98 |

Placements Serco Ltee v. The Queen, 84 DTC 6098, [1983] CTC 307, [1983] DTC 5347 (FCTD), aff'd 88 DTC 6125 (FCA)

The withholding tax is exigible inter alia on the payment of amounts that are deemed by Part XIII (e.g., S.212.1(1)) to be dividends. S.212(2)...

The Canada Southern Ry. Co. v. The Queen, 82 DTC 6244, [1982] CTC 278 (FCTD), rev'd 86 DTC 6097, [1986] 1 CTC 284 (FCA)

Where the taxpayer agreed with an American parent ("Penn Central") that annual rentals, which Penn Central was in effect obligated to pay to the...

See Also

Husky Energy Inc. v. The King, 2023 TCC 167, aff'd sub nomine Hutchison Whampoa Luxembourg Holdings S.À R.L. 2025 FCA 176

Before a Canadian public corporation (“Husky”) paid a dividend on its shares, two significant shareholders of Husky resident in Barbados (the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 10 | recipient of dividends on borrowed shares was not their beneficial owner because of requirement to pay dividend compensation payments | 270 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(1) - Tax Benefit | no tax benefit under s. 215(6) from targeted reduced rate of dividend withholding if in base transaction, the Canadian dividend payer would have withheld at the higher rate | 347 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | the residence, beneficial owner, and voting requirements in the Canada-Luxembourg Treaty fully expressed the rationale for the 5% Treaty-reduced rate on dividends | 413 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | transactions were carried out to reduce Part XIII tax rather than avoid Barbados income tax | 131 |

Administrative Policy

19 November 2019 Roundtable, 2019-0829611C6 - TEI 2019 Conference Question E1- Pays or Credits

In response to questions as to how a Canadian corporation may recover Part XIII tax that it has withheld on a dividend cheque issued to a US...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) | IC 77-16R4 meaning of “credited” confirmed | 193 |

10 February 2011 External T.I. 2010-0387151E5 - Deemed Disposition of Shares by a Non-Resident

On the redemption of shares of a non-resident which are taxable Canadian property, any resulting deemed dividend that is subject to Part XIII tax...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 116 - Subsection 116(5) | potential s. 116(5) withholding not reduced by Pt XIII tax | 44 |

October 1992 Central Region Rulings Directorate Tax Seminar, Q. G (May 1993 Access Letter, p. 230)

The unreasonable portion of salaries or bonuses paid to non-resident shareholder-managers will be subject to Part XIII tax under ss.15(1),...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | 24 |

20 July 1992 External T.I. 5-921355

S.212(2) does not apply to a distribution of paid-up capital by a Canadian corporation to which s. 84(4.2) applies, because s. 84(4.2) does not...

IC 77-16R4 – Non-Resident Income Tax, 11 May 11 1992

Exemption on portfolio dividends paid to a foreign government

Sovereign Immunity

50. Under the Doctrine of Sovereign Immunity, the Government of...

4 March 1992 T.I. (December 1992 Access Letter, p. 20, ¶C82-106, Tax Window, No. 17, p. 23, ¶1778)

The deemed dividend arising on the reduction of paid-up capital of term preferred shares of a Canadian-controlled private corporation held by a...

4 October 1991 T.I. (Tax Window, No. 10, p. 16, ¶1498)

Where a public corporation plans to distribute, as a dividend in kind, all the shares of a wholly-owned subsidiary which have a fair market value...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Shares | 59 |

17 January 1984 Income Tax Severed Letter

In the past our position has been that the doctrine would apply to the national government but not to political subdivisions. The State Immunity...

Articles

Todd Miller, Ryan Morris, "Canadian Subsidiary Guarantees for Foreign Parent Borrowings", Tax Notes International Vol. 34, No. 1, 5 April 2004, p. 63.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) | 0 |

Subsection 212(3) - Interest — definitions

Fully exempt interest

Administrative Policy

2012 Ruling 2011-0431891R3 - XXXXXXXXXX

A financial institution (the "Issuer") will accumulate a pool of mortgages [presumably CMHC-guaranteed in most cases] and sell an undivided...

Paragraph (a)

Subparagraph (a)(i)

Subparagraph (a)(iii)

See Also

Laval Technopole v. Agence du revenu du Québec, 2018 QCCQ 6352

The various appellants were companies that promoted commercial development, or cultural, sporting or tourist activities, in their respective...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Agency | 192 | |

| Tax Topics - Income Tax Act - Section 149 - Subsection 149(1) - Paragraph 149(1)(c) | municipally influenced companies were agents of the municipality | 82 |

Participating debt interest

Administrative Policy

3 December 2024 CTF Roundtable Q. 13, 2024-1038261C6 - Standard Convertible Debentures and Part XIII Tax

In a departure from 2009-0320231C6 (which indicated that there generally will be no excess under s. 214(7) on the conversion by the original...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 214 - Subsection 214(7) | FMV excess on conversion of a convertible debenture is deemed interest under s. 214(7) | 238 |

2021 Ruling 2020-0865991R3 - Code 3 - 212(1)(b)(ii) and Linked Notes

Proposed Note issuance

A Canadian public corporation (ACO), whose common and preferred shares are traded on an exchange, will issue unsecured and...

25 November 2021 CTF Roundtable Q. 16, 2021-0911911C6 - Convertible Debentures

When asked to provide an update on its views expressed in 2013-0509061C6 on whether convertible debentures give rise to participating debt...

2020 IFA-YIN Seminar on COVID-19 Guidelines, Q.16

CRA confirmed that 2013-0509061C6 continues to represent CRA’s position.

2018 Ruling 2018-0766771R3 - Commodity linked notes

In order to fund general corporate purposes, ACo will issue senior unsecured notes on a private placement basis for 100% of their principal amount...

2016 Ruling 2016-0664041R3 - Participating debt interest - contingent payment

Loan terms

Canco will borrow funds from an arm’s length lender resident in a Treaty country under a term loan (the “Loan”) with required...

2016 Ruling 2015-0602711R3 - Interest on Notes to Non-Residents

CRA ruled that interest was not participating debt interest respecting subordinated notes with conventional terms other than that, on a redacted...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) - Subparagraph 20(1)(c)(i) | deductible interest on subordinated debt with mandatory insolvency conversion | 216 |

21 January 2015 Internal T.I. 2014-0547431I7 - "Excluded amount" under clause 20(1)(e)(iv.1)(C)

An amount payable to a lender on specified events such as an IPO and computed as X% of a modified computation of NAV was found by CRA (after...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(e) | payment to creditor excluded as based on negotiated estimate of formula approximating share value | 330 |

2014 Ruling 2014-0539791R3 - Paragraph 212(1)(b)

CDS trust entered into credit default swaps (CDS) with a counterparty (a non-resident Bank) desiring credit protection for its bond portfolios and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(b) | creditors' approval of CCAA plan of compromise for the debtor trust did not cause them to not deal at arm's length with trust | 386 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | creditors' approval of CCAA plan of compromise for the debtor trust did not cause them to not deal at arm's length with trust | 204 |

2014 Ruling 2014-0523691R3 - Non-Viable Contingent Capital

Aco, a public corporation, will issue (at no discount or only a shallow discount) the "Notes" which: will rank equally with its other unsecured...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | non-viable contingent capital sub debt of bank respected as non-participating interest debt | 164 |

2014 Ruling 2013-0514551R3 - Convertible Debentures and Paragraph 212(1)(b)

Aco, a pubic corporation, will issue units consisting of convertible debentures (teh "Pubic Debentures" and warrants to acquire its common shares....

26 November 2013 Annual CTF Roundtable, 2013-0509061C6 - Part XIII Tax & Standard Convertible Debentures

[R]egular periodic interest payments made by public corporations pursuant to the terms and conditions of standard convertible debentures do not...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 214 - Subsection 214(8) - Paragraph 214(8)(c) | interest and premium on standard convertible debenture not participating | 81 |

18 March 2014 External T.I. 2013-0515631E5 - Criteria for Standard Convertible Debentures

"CRA cannot provide certainty concerning the application of Part XIII tax to the very broad range of situations in which convertible debentures...

2013 Ruling 2013-0475701R3 - MIC deemed interest & participating debt interest

The Corporation, a "mortgage investment corporation" under s. 130.1(6), pays dividends which take into account, inter alia, its income and...

2012 Ruling 2011-0418721R3 - Convertible Notes

amendments made by 2014-0532411R3 shown in italics

PUBCO, which is a listed public corporation and a taxable Canadian corporation, completed an...

23 May 2013 IFA Round Table, Q. 9

- What is the CRA's current position with respect to the application of Part XIII tax to convertible and exchangeable debentures owned by foreign...

1 May 2009 IFA Roundtable Q. 12, 2009-0320231C6 F - Convertible Debt Obligations

Traditional convertible debentures are: unsecured subordinated obligations of a public corporation issued in Canadian dollars for their face value;...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 214 - Subsection 214(7) | no deemed interest on conversion of traditional convertible debenture | 186 |

Income Tax Technical News, No. 41, 23 December 2009 Under "Definition of 'Tax Shelter' - Subsection 237.1(1)

If a particular premium on a convertible debt obligation represented participating debt interest, all interest on the obligation would be...

29 May 2009 External T.I. 2008-0301391E5 - EBITDA

Where (in order to reflect the resulting increased credit worthiness of the borrower) the interest on a loan decreases as the ratio of debt to...

2006 Ruling 2006-0208001R3 - Post-amble to paragraph 212(1)(b)

Where holders of notes receive at maturity a return linked to the performance of three mutual funds, the post-amble under s. 212(1)(b) will not...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(b) | participation based on mutual funds | 60 |

2005 Ruling 2005-0161521R3 - Postamble of 212(1)(b)

An interest rate under a term facility intended to qualify for the exemption under s. 212(1)(b)(vii) was equal to LIBOR plus a spread which...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Subparagraph 212(1)(b)(vii) | 99 | |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(b) | variable interest tracked creditworthiness | 99 |

8 January 2003 External T.I. 2002-0173135 - INTEREST POSTAMBLE

A loan amendment would provide that the interest rate would increase if the debt to EBITDA ratio exceeded 3.0. Would the former exclusion from...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(b) | 43 |

9 October 2001 External T.I. 2001-0096655 - Interest Exemption From Part XIII

CCRA "would not generally consider interest that is computed by reference to a stock index as satisfying the exception conditions described in the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Subparagraph 212(1)(b)(vii) | 42 | |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(b) | stock index link | 102 |

22 November 2000 External T.I. 2000-0046375 - WITHHOLDING TAX ON INDEX LINKED DEBT

The Agency would not generally consider the return computed by reference to a foreign stock index to be "computed by reference to revenue,...

| Other locations for this summary | |

|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(b) | Stock index link |

16 May 2000 External T.I. 2000-0011015 - WITHHOLDING TAX ON INDEX-LINKED INTEREST

Before concluding that it generally would be acceptable for the interest rate on a debt instrument to vary in accordance with the value of a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(b) | 123 |

Articles

Daniel Lang, Larissa Tkachenko, "Withholding Tax Implications of Participating Interest in Convertible Debt", CCH Tax Topics, No. 1916, November 27, 2008, p. 1.

Subsection 212(3.1)

Administrative Policy

3 December 2024 CTF Roundtable Q. 3, 2024-1038151C6 - Notifiable Transactions

The list of notifiable transactions for purposes of s. 237.4(3) essentially includes a non-resident person (NR1) entering into an arrangement to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 237.4 - Subsection 237.4(4) - Paragraph 237.4(4)(b) | B2B reporting engaged where loan from immediate NR parent (funded in turn in part with debt from ultimate parent) bears reduced (10%) withholding | 625 |

Income Tax Mandatory Disclosure Rules Consultation: Sample Notifiable Transactions (Finance Release Webpage), 4 February 2022

The notifiable transactions designated by CRA pursuant to draft s. 237.4(3) with the concurrence of Finance include:

Avoidance of Part XIII tax...

Articles

Ian Bradley, Denny Kwan, Dian Wang, "Is The Back-to-Back Withholding Tax Regime an Effective Anti-Treaty-shopping Measure?", Canadian Tax Journal, (2016) 64:4, 833-58

Non-application of B2B rules to dividends paid by Canadian (p. 856)

The back-to-back rules do not apply to dividends paid by Canadian taxpayers...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 11 | 174 | |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.2) | 424 | |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.9) - Paragraph 212(3.9)(b) | 159 |

Paragraph 212(3.1)(c)

Administrative Policy

17 November 2015 Roundtable, 2015-0614241C6 - 2015 TEI Liaison Meeting Q.6 - Specified Right

Non-resident Parentco and its subsidiaries, including Canco, have a notional cash pooling arrangement that has been established with an...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(6) - Paragraph 18(6)(c) | cross-border notional cash-pooling arrangement produced intermediary debt | 95 |

Articles

Mark Coleman, "Treaty Shopping and Back-to-Back Loan Rules", Power Point Presentation for 28 May 2015 IFA Conference in Calgary.

{kind=link}

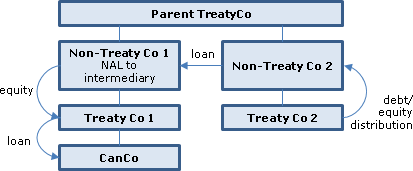

Where CanCo receives an interest-bearing loan from its immediate parent (Treaty Co 1), which is funded by equity from the parent (Non-Treaty Co...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.1) - Paragraph 212(3.1)(d) | 90 | |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Accrual Tax | 139 |

Steve Suarez, "Canada Releases Revised Back-to-Back Loan Rules", Tax Notes International, October 27, 2014, p. 357.

Introduction of requirement for strong causal connection (p. 361)

Two aspects of the revised secondary obligation definition merit further...

Steve Suarez, "An Analysis of Canada's Latest International Tax Proposals", Tax Notes International, September 29, 2014, p. 1131.

29 August revised version of description of intermediary ("secondary") debt (pp. 1134-5)

[T]he revised proposal deletes a requirement in the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.1) - Paragraph 212(3.1)(e) | 209 | |

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(9) | 169 |

Subparagraph 212(3.1)(c)(ii)

Articles

Nik Diksic, Sabrina Wong, "Cross-Border Lending Practices", 2017 CTF Annual Conference draft paper

Loss of specified right exclusions where a NR bank lends to Canco through a non-resident affiliate (pp. 12-13)

NR1 borrows from a third-party bank...

Paragraph 212(3.1)(d)

Articles

Nik Diksic, Sabrina Wong, "Cross-Border Lending Practices", 2017 CTF Annual Conference draft paper

Cannot benefit from ultimate funder withholding rate if immediate funder rate is higher (p. 11)

Consider … where NR1 (treaty country [with 10%...

Mark Coleman, "Treaty Shopping and Back-to-Back Loan Rules", Power Point Presentation for 28 May 2015 IFA Conference in Calgary.

{kind=link}

If a loan by U.S. Parent to its "grandchild" Canadian ULC sub (held e.g.,, through a C-Corp sub) is funded by a loan by an LLC sub ("Opco") of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.1) - Paragraph 212(3.1)(c) | 240 | |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Accrual Tax | 139 |

Michael N. Kandev, "Canadian Interest Anti-Conduit Rule Soon to Be Law", Tax Notes International, December 15, 2014, p. 1027

Back-to-back ("B2B") rule in s. 212(3.1) is anti-conduit rule (p. 1028)

The absence of a safe harbor for non-resident non-arm's-length...

Paragraph 212(3.1)(e)

Articles

Edward A. Heakes, "The Proposed Revisions to Back-to-Back Loan Rules", International Tax Planning (Federated Press), Vol. XIX, No. 4, 2014, p. 1357.

Narrowness of aggregation rule in s. 212(3.1)(e)(ii)(B) (p.1359)

[T]he basic thrust of this [de minimis] rule is that if the amount that is...

Steve Suarez, "Canada Releases Revised Back-to-Back Loan Rules", Tax Notes International, October 27, 2014, p. 357.

Narrow 25% safe harbour (p. 363)

There are two basic scenarios in which the de minimis exception is intended to provide relief. The first is when...

Steve Suarez, "An Analysis of Canada's Latest International Tax Proposals", Tax Notes International, September 29, 2014, p. 1131.

De minimis rule in s. 212(3.1)(d)

While Finance is to be commended for trying to accommodate typical multinational group borrowing arrangements,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.1) - Paragraph 212(3.1)(c) | 273 | |

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(9) | 169 |

Subsection 212(3.2)

Articles

Ian Bradley, Denny Kwan, Dian Wang, "Is The Back-to-Back Withholding Tax Regime an Effective Anti-Treaty-shopping Measure?", Canadian Tax Journal, (2016) 64:4, 833-58

Derivative benefits concept under B2B rules can provide relief where ultimate funder has a Treaty-reduced rate that is higher than that of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 11 | 174 | |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.9) - Paragraph 212(3.9)(b) | 159 | |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.1) | 151 |

Sabrina Wong, "Bill C-29 Amendments to the Back-to-Back Rules", International Tax, Wolters Kluwer CCH, December 2016, No. 91, p. 5

Allocation under s. 212(3.2) formula of interest to ultimate funder in excess of actual interest to it (p. 7)

Essentially, the formula allocates...

Subsection 212(3.21)

Articles

Jason Boland, Christopher Montes, "A Detailed Review of the Back-to-Back Loan Rules", 2016 Conference Report (Canadian Tax Foundation), 26:1-32

Potential usefulness of election (p. 26:12)

...This election may prove useful because most Canadian tax treaties limit withholding tax on interest...

Subsection 212(3.3)

Articles

John Lorito, Trevor O'Brien, "International Finance – Cash Pooling Arrangements", 2014 Conference Report, (Canadian Tax Foundation), 20:1-33

{kind=link}

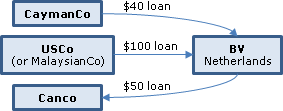

Unavailability of s. 212(3.3) where Canco owes $50 to Netherlands intermediary, which owes $40 to Caymanco and $100 to USCo – because U.S....

Subsection 212(3.4)

Articles

PWC, "Bill C-29 significantly expands back-to-back rules", Tax Insights PWC International Tax Services, Issue 2016-53, 16 November 2016

Example illustrating key difference between the existing and amended rules in a situation Canco and 4 related non-residents (NR1, NR2, NR3 and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.9) - Paragraph 212(3.9)(b) - Subparagraph 212(3.9)(b)(ii) | 169 | |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.91) | 162 |

Subsection 212(3.5)

Articles

Jason Boland, Christopher Montes, "A Detailed Review of the Back-to-Back Loan Rules", 2016 Conference Report (Canadian Tax Foundation), 26:1-32

Overview of s. 212(3.5) (pp. 26:13)

When a relevant funder receives funding (either by way of debt or specified right) which it uses (together...

Subsection 212(3.6)

Paragraph 212(3.6)(a)

Articles

Nik Diksic, Sabrina Wong, "Cross-Border Lending Practices", 2017 CTF Annual Conference draft paper

Whether s. 212(3.6) applies prospectively (p. 6)

[I]f the particular debt or other obligation is issued in Year 1, but the dividend obligation...

Jason Boland, Christopher Montes, "A Detailed Review of the Back-to-Back Loan Rules", 2016 Conference Report (Canadian Tax Foundation), 26:1-32

Application of connectivity test to SPVs (p. 26:16)

...In practice, when an equity subscription is used to fund a special purpose vehicle (SPV)...

Michael N. Kandev, "Canada Expands Back-to-Back Regime: Examining the Character Substitution Rules", Tax Notes International, June 19, 2017, p.1087

Potential application to dividend declared after particular debt has disappeared (p.1091)

[F]or the character substitution rules to apply, the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.8) - Specified Share | 79 | |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.6) - Paragraph 212(3.6)(b) | 351 |

Sabrina Wong, "Bill C-29 Amendments to the Back-to-Back Rules", International Tax, Wolters Kluwer CCH, December 2016, No. 91, p. 5

Potential application to common shares (p. 10)

[T]he Character Substitution Rules…generally apply where a "relevant funder" has an obligation to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.2) | 215 | |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.9) - Paragraph 212(3.9)(b) - Subparagraph 212(3.9)(b)(ii) | 94 |

Finance

26 April 2017 IFA Finance Roundtable, Q.12

[s. 212(3.6)(a) rule was intended to potentially apply re common share dividends]

Canco pays interest...

Subparagraph 212(3.6)(a)(ii)

Articles

Peter Lee, "The Character Substitution Rules", International Tax (Wolters Kluwer CCH), June 2017, No. 94, p. 10

Potential embedded purpose test in s. 212(3.6)(a)(ii) (p. 12)

[A]t the 2017 IFA Conference…the Department of Finance…stated that the provision...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.7) | 491 |

Paragraph 212(3.6)(b)

Articles

Michael N. Kandev, "Canada Expands Back-to-Back Regime: Examining the Character Substitution Rules", Tax Notes International, June 19, 2017, p.1087

Potential non-existence of the situation posited (p. 1092)

[I]t is utterly mysterious how a rent or royalty can be determined, in whole or in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.8) - Specified Share | 79 | |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.6) - Paragraph 212(3.6)(a) | 93 |

Subsection 212(3.7)

Articles

Peter Lee, "The Character Substitution Rules", International Tax (Wolters Kluwer CCH), June 2017, No. 94, p. 10

Exclusion of shareholder funding where indirect debt is higher than direct debt (pp. 13-14)

Consider an arrangement in which "Taxpayer" (a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.6) - Paragraph 212(3.6)(a) - Subparagraph 212(3.6)(a)(ii) | 96 |

Subsection 212(3.8)

Relevant Funder

Articles

Jason Boland, Christopher Montes, "A Detailed Review of the Back-to-Back Loan Rules", 2016 Conference Report (Canadian Tax Foundation), 26:1-32

Observations on scope of “relevant funder” (pp. 26:9-10)

...First, the use of the broadly-defined terms "relevant funder" and "relevant...

Specified Share

Articles

Nik Diksic, Sabrina Wong, "Cross-Border Lending Practices", 2017 CTF Annual Conference draft paper

Whether a common share can be a specified share (p. 8)

[I]t seems reasonable to question whether a common share can, in certain circumstances,...

Jason Boland, Christopher Montes, "A Detailed Review of the Back-to-Back Loan Rules", 2016 Conference Report (Canadian Tax Foundation), 26:1-32

No requirement for specified share to pay dividends( p. 26:14-15)

...For a share to be a specified share, there is no requirement that a payment...

Michael N. Kandev, "Canada Expands Back-to-Back Regime: Examining the Character Substitution Rules", Tax Notes International, June 19, 2017, p.1087

MRPS as example of specified share (p. 1090)

[I]f a Bermuda corporation funds a Luxembourg subsidiary by way of mandatorily redeemable preferred...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.6) - Paragraph 212(3.6)(a) | 93 | |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.6) - Paragraph 212(3.6)(b) | 351 |

Ultimate Funder

Articles

Jason Boland, Christopher Montes, "A Detailed Review of the Back-to-Back Loan Rules", 2016 Conference Report (Canadian Tax Foundation), 26:1-32

General effect of definition (p. 26:10)

...An ultimate funder effectively is a relevant funder (other than the immediate funder) that has funded a...

Subsection 212(3.9)

Paragraph 212(3.9)(b)

Articles

Ian Bradley, Denny Kwan, Dian Wang, "Is The Back-to-Back Withholding Tax Regime an Effective Anti-Treaty-shopping Measure?", Canadian Tax Journal, (2016) 64:4, 833-58

Difficulties of a Canadian licensee in determining whether the B2B rule is applicable (p. 855)

[T]he joint committee on taxation has noted that a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 11 | 174 | |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.2) | 424 | |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.1) | 151 |

Subparagraph 212(3.9)(b)(ii)

Articles

Sabrina Wong, "Bill C-29 Amendments to the Back-to-Back Rules", International Tax, Wolters Kluwer CCH, December 2016, No. 91, p. 5

Likely insufficient information for Canadian taxpayer to evaluate arm’s length test (p.9)

[I]t appears that the "one of the main purposes" test...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.2) | 215 | |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.6) - Paragraph 212(3.6)(a) | 256 |

PWC, "Bill C-29 significantly expands back-to-back rules", Tax Insights PWC International Tax Services, Issue 2016-53, 16 November 2016

Difficulty for the taxpayer in determining ultimate licensing structure (pp. 3-4)

The new back-to-back royalty rules...apply in certain...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.4) | 336 | |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.91) | 162 |

Subsection 212(3.91)

Articles

Jason Boland, Christopher Montes, "A Detailed Review of the Back-to-Back Loan Rules", 2016 Conference Report (Canadian Tax Foundation), 26:1-32

Reasonably allocable requirement (pp. 26:20-21)

It is not clear what is required to prove to the satisfaction of the minister that a portion of...

PWC, "Bill C-29 significantly expands back-to-back rules", Tax Insights PWC International Tax Services, Issue 2016-53, 16 November 2016

Potentially punitive effect of CRA not accepting allocation (p.4)

If the Minister does not accept that the taxpayer's allocation is reasonable,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.4) | 336 | |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.9) - Paragraph 212(3.9)(b) - Subparagraph 212(3.9)(b)(ii) | 169 |

Subsection 212(3.92)

Paragraph 212(3.92)(b)

Subparagraph 212(3.92)(b)(ii)

Subsection 212(4)

Paragraph 212(4)(a)

Cases

Windsor Plastic Products Ltd. v. The Queen, 86 DTC 6171, [1986] 1 CTC 331 (FCTD)

The three shareholders of the taxpayer, each of whom was a minority shareholder and one of whom was related to a non-resident corporation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | shareholders acting in concert | 110 |

Administrative Policy

30 March 2017 Internal T.I. 2016-0636721I7 - Consent fees and withholdings

In order to obtain the agreement of arm’s length non-resident financial institutions to a sale of the shares of Canco to the non-resident...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 214 - Subsection 214(15) - Paragraph 214(15)(b) | whether consent fee was deemed to be interest under s. 212(15)(b) was moot | 126 |

| Tax Topics - Income Tax Regulations - Regulation 105 - Subsection 105(1) | non-resident dealer who attended at Canadian board meetings was rendering services in Canada | 184 |

2011 Ruling 2011-0416891R3 - Fees for Digital Content & Management Services

A US LLC ("Corporation C"), whose sole member was a US corporation qualifying for benefits under the Canada-US Convention, ran a platform for the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 12 | 199 |

Paragraph 212(4)(b)

See Also

Agricultural and Industrial Corporation v. MNR, 91 DTC 1286 (TCC)

Beaubier J. affirmed the disallowance by the Minister of all but $100,000 per year of amounts paid by a Canadian subsidiary to its U.S. parent...

Administrative Policy

IT-468R "Management or Administration Fees Paid to Non-residents" (Archived) 29 December 1999

8. The Department considers that the term "a specific expense"...applies to a particular expense item or a portion thereof, a sum of several...

Subsection 212(5) - Motion picture films

Cases

CBS/Fox Co. v. The Queen, 95 DTC 5631, [1996] 1 CTC 3 (FCTD)

The plaintiff (a U.S. partnership) provided video tape reproduction masters to a wholly-owned Canadian subsidiary, which was entitled in...

MCA Television Ltd. v. The Queen, 94 DTC 6375 (FCTD)

The taxpayer's Netherlands affiliate ("B.V.") was the Canadian distributor of theatrical and television products produced by an American affiliate...

MNR v. Paris Canada Films Ltd., 62 DTC 1338, [1962] CTC 538 (Ex Ct)

The taxpayer, which was a distributor of motion picture films in Canada, made various payments to non-residents for film rights including a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(d) | 107 | |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(5) | 63 | |

| Tax Topics - Treaties - Income Tax Conventions - Article 12 | 60 |

MNR v. Paris Canada Films Ltd., 62 DTC 1338, [1962] CTC 538 (Ex Ct)

The taxpayer, which was a distributor of motion picture films in Canada, made various payments to non-residents for film rights including a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(d) | 107 | |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(5) | 78 | |

| Tax Topics - Treaties - Income Tax Conventions - Article 12 | 60 |

See Also

Vauban Productions v. The Queen, 79 DTC 5186, [1979] CTC 262 (FCA)

The non-resident taxpayer, which had acquired from another film distributor the exclusive right for a limited period of time to show certain films...

Administrative Policy

27 March 2018 External T.I. 2017-0715561E5 - Withholding tax on royalties for streamed content

Canco streams motion picture films and TV shows (the “digital content”) to its Canadian and foreign subscribers (who pay monthly fees) through...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Interpretation Act - Section 35 - Subsection 35(1) - Broadcasting | Interpretation Act definition of broadcasting not applicable to Treaty interpretation of those words | 246 |

| Tax Topics - Treaties - Income Tax Conventions - Article 12 | television and broadcasting included digital streaming | 349 |

5 November 2014 External T.I. 2013-0506191E5 - copyright photographs

A Canadian company pays a non-resident for the use of the photographs in connection with television in Canada (for example in a backdrop to a film...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(d) - Subparagraph 212(1)(d)(vi) | payments for photos before incorporation into TV program were exempt | 100 |

1 May 2014 External T.I. 2013-0514291E5 F - Redevances sur une oeuvre musicale dans un film

Would copyright royalties paid by a resident of Canada to a resident of Belgium respecting the production or reproduction of a musical work to be...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(d) - Subparagraph 212(1)(d)(vi) | copyright royalty for music used in film is exempt notwithstanding s. 212(5) exclusion | 251 |

14 December 2011 Internal T.I. 2011-0424221I7 - copyright music

A licence with a US-resident copyright holder of a musical work enabling the taxpayer to "fix, record, dub and edit the music in synchronized or...

19 April 2011 External T.I. 2011-0392761E5 - Motion picture films, ITA 212(5)

A Canadian-resident company (Canco) uses motion pictures distributed to it by a US and French company by reproducing them in Canada in digitized...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 12 | 92 |

19 February 1997 External T.I. 9616305 - ROYALTY PAYMENTS FOR SHOWING VIDEOS IN PUBLIC

A Canadian corporation that obtains a licence to make videos available to patrons of a health club, who watch videos on installed television sets...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 12 | 108 |

6 March 1995 Internal T.I. 9428767 - VIDEO REPRODUCTION RIGHTS

The phrase "in connection with television" would apply to video tapes destined for private home use.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 12 | 31 |

93 C.R. - Q. 30

RC is prepared to exempt the portion of a particular payment that is solely for the right to use a motion picture film or video tape outside Canada.

5 January 1993, T.I. (Tax Window, No. 28, p. 8, ¶2404)

The reproduction of video cassettes for non-commercial use does not generally fall within the purview of s. 212(5)(b) notwithstanding that a...

Subsection 212(9)

Paragraph 212(9)(d)

Administrative Policy

8 October 2010 Roundtable, 2010-0373501C6 F - Al. 212(9)d) proposé - remboursement

A non-resident reinsurer of Canadian risks may be required to place property in trust in Canada (a "Reinsurance Trust"). Proposed s. 212(9)(d)...

22 March 2005 External T.I. 2004-0098591E5 F - Application de l'alinéa 212(9)d) proposé

CRA indicated that the exemption as then worded did not apply if a provincial rather than federal authority was the party to the reinsurance...

Subsection 212(11) - Payment to beneficiary as income of trust

Administrative Policy

12 June 2023 External T.I. 2022-0956461E5 - Part XIII tax on estate capital distributions

CRA confirmed that a capital distribution that was not derived from a capital dividend, paid by a resident estate to non-resident beneficiaries,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(c) | capital distribution of an estate to a non-resident beneficiary is of “income,” but is not subject to withholding tax | 176 |

| Tax Topics - Income Tax Regulations - Regulation 202 - Regulation 202(1) - Paragraph 202(1)(b) | a capital distribution by an estate to a non-resident beneficiary is deemed to be of “income,” and must be reported on an NR4 | 119 |

22 December 2016 External T.I. 2015-0608201E5 F - Capital distribution from trust & NR4

Although s. 212(11) deems all trust capital distributions to a non-resident beneficiary to be income distributions for Part XIII purposes, s....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 202 - Regulation 202(1) - Regulation 202(1)(c) | all capital distributions made by Canadian-resident trusts to a non-resident beneficiaries must be reported on NR4s | 144 |

18 November 2011 External T.I. 2011-0422441E5 - Capital dividend paid to a Non-Resident

Shares of a Canadian-controlled private corporation held by the estate were redeemed for cash proceeds, with the resulting deemed dividend paid...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(c) | redistribution of capital dividend subject to Part XIII tax | 155 |

9 October 2009 APFF Roundtable Q. 5, 2009-0327001C6 F - Succession canadienne - dividende en capital

When a capital dividend (arising from insurance proceeds) received by an estate is used for the payment of estate taxes, would the distribution of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(c) | allocation of capital dividend between estate duties and NR distribution | 131 |

17 July 2003 External T.I. 2003-0020695 - Distribution from Trust

A trust receives a capital dividend in Year 1 (so that no part of the dividend is included in its income) and in Year 2 it makes a distribution in...

20 October 1997 External T.I. 9715265 - INTERACTION OF SUBSECTION 212(11) & PARAGRAPH 212(1)(C)

"In our view, subsection 212(11) of the Act merely characterizes any amount paid or credited by a trust or estate as income of the trust or...

12 April 1995 External T.I. 9417135 - CANADIAN MUTUAL FUND TRUST-NON-RESIDENT

Taxable capital gains of a mutual fund trust designated to a non-resident unitholder under s. 104(21) would not be taxable in Canada.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(21) | capital gains distributed to non-resident MFT beneficiaries not taxable | 23 |

| Tax Topics - Income Tax Act - Section 118.9 - Subsection 118.9(4) | 10 | |

| Tax Topics - Treaties - Income Tax Conventions - Article 22 | 27 |

Alberta Chartered Accountants Round Table, 2 May 1994, Q. 8, 940956 (C.T.O. "Capital Amount Paid by Trust to Non-Resident (8192)")

S.212(11) does not make all capital distributions by a trust subject to Part XIII tax. Instead, it merely characterizes any amount paid or...

22 February 1994 External T.I. 9329545 - WITHHOLDING TAX - TRUST

S.212(11) does not tax the non-taxable portion of capital gains distributed by an ordinary trust to a non-resident, or any portion of a capital...

IT-465R "Non-Resident Beneficiaries of Trusts" 19 September 1985

- Subject to the exemptions in subsections 212(9), (10), (11.1) and (11.2)… subsection 212(11) provides that any amount paid or credited by a...

Subsection 212(13) - Rent and other payments

Paragraph 212(13)(a)

Administrative Policy

14 November 1997 Internal T.I. 9718226 - 212(13)(A) "RENT"

Annual payments made by a non-resident person carrying on business in Canada to a non-resident software supplier for updates, maintenance and...

Subsection 212(13.1) - Application of Part XIII tax where payer or payee is a partnership

Paragraph 212(13.1)(a)

See Also

The Queen v. Williams, 90 DTC 6399, [1990] 2 CTC 124 (FCA), rev'd 92 DTC 6320 (SCC)

Stone J.A. found that unemployment insurance benefits earned by an Indian were not "property ... situated on a reserve" because the debtor (Her...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Other Legislation/Constitution - Federal - Indian Act - Section 90 | 122 |

Twock v. Estate Duty Commissioners, [1988] 1 WLR 1035 (PC)

A simple contract debt (including a debt payable in futuro) is situate where the debtor resides. In the case of corporate debtors which carry on...

Administrative Policy

13 July 2018 Internal T.I. 2017-0713301I7 - Assumption of accrued interest

As part of the consideration for the drop-down of the assets of a Canadian partnership (whose partners were Canco and its wholly-owned Canadian...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(b) | the covenant of the assuming debtor to pay accrued interest on a debt assumption was a payment in kind subject to Part XIII tax | 357 |

25 May 2004 External T.I. 2003-0039231E5 - Paragraph 212(13.1)(a)

An LP organized in the U.S. but having only Canadian-resident partners, and whose only source of income is dividends and other investment income...

7 May 2004 IFA Roundtable Q. 1, 2004-0072131C6 - IFA Round Table 2004 Q.1 - 212(13.1)(a)

In the context of a ruling request respecting a "tower" structure, a partnership of which two taxable Canadian corporations were the partners...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(b) | partnership borrower was transparent | 129 |

| Tax Topics - Treaties - Income Tax Conventions - Article 11 | 257 |

25 February 1991 Internal T.I. 903237 F - Non-resident Withholding Tax in respect of Royalties

A partnership between two equal arm's length partners (a Canadian corporation and a non-resident corporation) carrys on an active business...

6 February 1990 T.I. (July 1990 Access Letter, ¶1336)

For purposes of determining whether income is earned on a reserve, income from sources other than those enumerated in IT-62 generally will be...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 146 - Subsection 146(1) - Refund of Premiums | 56 |

12 November 1980 Income Tax Severed Letter RCT-0246

A Canadian partnership formed in Canada earns income from U.S. sources. Interest on a borrowing from a non-resident lender is deductible in...

3 November 1980 Income Tax Severed Letter RCT-0247 F

S. 212(13.1)(a) would not apply to mortgage interest paid by a mooted Canadian partnership due to grandfathering. The Department stated:

With the...

Articles

Joint Committee, "August 9, 2022 Technical Amendments - Application of Part XIII tax where payer or payee is a partnership", 22 March 2023 Joint Committee Submission

Impracticability of s. 212(13.1)(a) re foreign partnerships with passive minority, or upstream, Canadian investors (pp. 1-2)

- Proposed s....

Cynthia Morin, Suhaylah Sequeira, "Withholding Tax Obligations: Proposed Amendments to Subsections 212(13.1) and 212(13.2)", International Tax Highlights, Vol. 1, No. 2 November 2022, p. 2

August 9, 2022 amendment to s. 212(13.1)(a)

- The August 9, 2022 proposals would amend s. 212(13.1)(a) to deem a partnership to be a person...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(13.2) | 123 |

Gregory Wylie, "Canada Revenue Agency Comments on Cross-Border Transactions", Tax Notes International, 7 June 2004, p. 991

Comment on CRA position that due to the joint and several liability of Canadian partners of a U.S. partnership, interest on a loan made to a U.S....

J. S. Peterson, "Canadian Taxation of Non-Residents", 1974 Conference Report (Canadian Tax Foundation), p. 262

Effect of introduction of s. 212(13.1)(a) (pp. 264-265)

This amendment is expected to stop a fair amount of tax leakage. For example, it is...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(13.1) - Paragraph 212(13.1)(b) | 284 |

Paragraph 212(13.1)(b)

Cases

Canada v. Gillette Canada Inc., 2003 DTC 5078, 2003 FCA 22

Some of the shares held by the taxpayer in its French subsidiary were purchased for cancellation by the subsidiary in consideration for the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Payment & Receipt | replacement with different currency note | 60 |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2) | 150 |

Administrative Policy

27 March 2013 External T.I. 2012-0450491E5 - Election under s. 216

Where a Canadian-resident tenant pays rent

to a partnership that has one or more partners who are not resident in Canada…the [Part XIII]...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 216 - Subsection 216(4) | tenant not generally expected to withhold | 145 |

30 October 1997 External T.I. 9716735 - : Taxation of Non-Resident Partners

Respecting the application of s. 212(13.1)(b) to payments to a partnership of which there is a non-resident limited partner, CRA stated:

We...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 2 - Subsection 2(3) - Paragraph 2(3)(b) | 51 |

IT-81R "Partnerships - Income of Non-Resident Partners"

No withholding-reduction based on Cdn-resident members

7. ...Where tax is to be withheld under Part XIII because a partnership is deemed by...

Articles

J. S. Peterson, "Canadian Taxation of Non-Residents", 1974 Conference Report (Canadian Tax Foundation), p. 262

Partnership not a person prior to enactment of s. 212(13.1)(b) (p. 263)

.. Part XIII tax applies only in respect of payments to non-resident...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(13.1) - Paragraph 212(13.1)(a) | 161 |

Subsection 212(13.2) - Application of Part XIII tax — non-resident operates in Canada

See Also

Eastern Success Co Ltd In It's Capacity as Trustee Of The Easter Law Trust v. The Queen, 2004 DTC 3521, 2004 TCC 689

The taxpayer, which was a non-resident trust, financed its construction of a condominium project in Canada through a loan from a non-resident...

Administrative Policy

24 February 2000 Internal T.I. 1999-001425

Interest capitalized as inventory pursuant to s. 18(3.1) would be considered to be deductible for purposes of s. 212(13.2). The debtor will be...

1996 Corporate Management Tax Conference Round Table, Q. 8

Where s. 250(5) deems a U.S.-incorporated subsidiary whose central management and control is in Canada, to be resident in the U.S., the subsidiary...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Subparagraph 212(1)(b)(vii) | 42 |

Articles

Cynthia Morin, Suhaylah Sequeira, "Withholding Tax Obligations: Proposed Amendments to Subsections 212(13.1) and 212(13.2)", International Tax Highlights, Vol. 1, No. 2 November 2022, p. 2

Current s. 212(13.2) rule

- The existing s. 212(13.2) rule applies Part XIII tax to a payment made by a non-resident person to another non-resident...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(13.1) - Paragraph 212(13.1)(a) | 265 |

Subsection 212(13.3) - Application of Part XIII to authorized foreign bank

Finance

13 July 2001 Comfort Letter 20010713

"The broad direction of our thinking" is that "it should be possible to provide that the payor's reasonable belief, or a presumption based on the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 105 - Subsection 105(1) | 119 |