Descripton of physical and notional cash pooling (pp. 2-3)

[I]n general terms there are essentially two types of cash pooling arrangements [fn 1:...

Withholding based on net increase (p. 16)

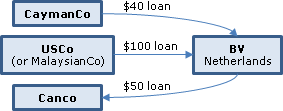

If the shareholder loan rules apply to loans made by a Canadian resident corporation to a non-resident,...

Specified rights (defined as tantamount to ownership) rarely granted to creditors except re cash collateral (p. 9)

[I]n simple terms, a specified...

{kind=link}

Cash pooling advances in the ordinary course (pp. 19-20)

[I]n…2013-0483751C6, the CRA commented that…the ordinary course of business exception...

Net decrease treated as repayment under cash pool (pp.16-17)

It is the position of the CRA [fn 52: …27 of IT-119R4…2006-021516117…and...

CRA relief where a cash pool head account has no presence in Canada and Canco has elected (p. 24)

Assume Canco…has elected to compute its...

{kind=link}

Cash risked in active business (p.20:24-25)

Interest earned by a foreign affiliate on cash/deposits risked in the active business of the foreign...

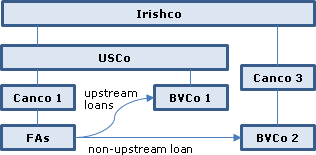

Difficulties in establishing tracing in cash pool (p. 22)

It may be possible for interest earned by a foreign affiliate from deposits/loans made...