Subsection 90(1) - Dividend from non-resident corporation

See Also

Ahmad v. The Queen, 2013 DTC 1112 [at at 601], 2013 TCC 127 (Informal Procedure)

The taxpayer held 1000 shares in a Bermudan corporation ("Tyco"). In a corporate reorganization, Tyco distributed 250 shares to the taxpayer of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Dividend | 64 |

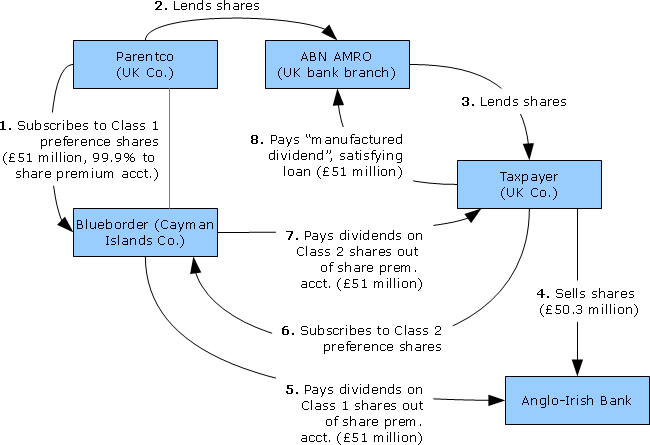

Revenue and Customs Commissioners v. First Nationwide, [2012] BTC 99, [2012] EWCA Civ 278

The taxpayer, in cooperation with two banks, a Cayman Islands corporation and its parent, implemented the following series of transactions:

{kind=link}

The...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Substance | 73 |

Marshall v. The Queen, 2011 DTC 1353 [at at 1976], 2011 TCC 497

The taxpayer was a shareholder of a Bermudian corporation ("Tyco"), and received shares as part of the same spin-off described in Capancini, where...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Dividend | 125 |

Capancini v. The Queen, 2010 DTC 1394 [at at 4569], 2010 TCC 581 (Informal Procedure)

Under a reorganization, the Canadian-resident taxpayer received, in exchange for shares he previously held of Tyco International Ltd. (a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Dividend | 134 |

Morasse v. The Queen, 2004 DTC 2435, 2004 TCC 239 (Informal Procedure)

The taxpayer, who held American Depositary Receipts for a Mexican public company (Telmex) became the owner of an equal number of shares of another...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | 116 | |

| Tax Topics - Income Tax Act - Section 86.1 - Subsection 86.1(2) | 105 |

Cangro Resources Ltd. v. MNR, 67 DTC 582 (TAB)

A payment received by the taxpayer that was stated to be made out of "paid-in capital and paid-in surplus" pursuant to the provisions of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | 118 | |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Dividend | distributions out of share premium based on number of shares held were dividends | 231 |

Robwaral Ltd. v. MNR, 60 DTC 1025, [1960] CTC 16 (Ex Ct), briefly aff'd 64 DTC 5266 (SCC)

A private Ontario company declared a dividend on December 21, 1953 payable to common shareholders of record on December 31, 1953, and then drew...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Payment & Receipt | dividend not received until cheque received | 41 |

Administrative Policy

25 August 2014 External T.I. 2014-0528361E5 - premium on redemption of foreign affiliate shares

After noting that in 2012-0439741I7 "we indicate that upon redemption of MRPS [mandatory redeemable preference shares], the redemption premium...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Dividend | redemption premium is proceeds | 76 |

30 April 2013 Internal T.I. 2012-0439741I7

withdrawn by CRA on 25 August 2014

Mandatory Redeemable Preferred Shares ("MRPS"): are voting; have a mandatory redemption date approximately 10...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Dividend | treatment of MRPS as equity | 198 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Share | treatment of MRPS as equity | 193 |

12 July 2011 External T.I. 2010-0391621E5 - Capital Gains Distributions

Capital gains distributions made to Canadian-resident shareholders by U.S. non-diversified closed-ended management investment companies, comprised...

21 October 2004 Internal T.I. 2004-0060131I7 - Characterization of Foreign Dividend

The distribution of amounts out of a share premium account of a foreign corporation that could have been declared and paid as a dividend under the...

18 March 2002 External T.I. 2002-0120065 F - Avoir fiscal français - 20(11)

A Canadian-resident received a $10,000 dividend from a French company as reduced by French withholding tax of 15% ($1,500) and by the avoir fiscal...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 10 | subsequent refund to Canadian shareholder of French avoir fiscal treated as a dividend payment for dividend withholding purposes | 79 |

7 April 2000 External T.I. 2000-0016275 F - Spin-off to individual shareholders

The Agency confirmed that a foreign spinoff should be treated as a dividend given that the shareholders received the property in proportion to...

31 August 1999 APFF Roundtable Q. 3, 9920920 F - RAPATRIEMENT DU CAPITAL D'UNE LLC

Publico, a Canadian public corporation, invested $1 million in its wholly-owned US affiliate which is an LLC under the American corporate law....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(3) | return by LLC of unit subscription to unitholder treated as a PUC distribution | 97 |

28 October 1997 External T.I. 9711965 - RETURN OF CAPITAL FROM A U.S. CORPORATION

Whether a capital distribution made to a Canadian shareholder of a U.S. corporation would be a dividend or a return of capital for Canadian tax...

Income Tax Technical News, No. 11, September 30, 1997, "U.S. Spin-Offs (Divestitures) - Dividends in Kind"

8 January 1996 External T.I. 9428025 - RETURN OF CAPITAL FROM A DELAWARE CORPORATION

It is the Department's view that a dividend can include any distribution of property by a corporation to its shareholders that is not a return of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(3) | all distributions from Delaware corps are dividends | 92 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Dividend | 92 | |

| Tax Topics - Treaties - Income Tax Conventions - Article 10 | 108 |

8 December 1995 External T.I. 9415515 - PAID-UP CAPITAL REDUCTIONS- DELAWARE CORPORATIONS

FA1, a Delaware corporation, wishes to make a cash distribution to Canco by reducing its capital. However, as under Delaware corporate law a cash...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(3) | capital distribution by Delaware corp | 141 |

24 March 1994 External T.I. 9402855 - DISTRIBUTIONS FROM FOREIGN TRUSTS

Dividends received from a non-resident corporation, including a mutual fund, are generally included in income as dividend income for the Canadian...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(13) | income distributions received by a Canadian resident from a non-resident trust are income under s. 104(13)(c) | 157 |

Articles

Tina Korovilas, Drew Morier, "Non-Corporate Vehicles in the Foreign Affiliate Context", 2018 Conference Report (Canadian Tax Foundation), 20:1 – 114

Most pro rata corporate distributions are dividends (pp. 20:16-17)

Cangro Resources … held that for the purposes of the Act, “dividend” was...

Subsection 90(2) - Dividend from foreign affiliate

Administrative Policy

17 May 2023 IFA Roundtable Q. 3, 2023-0964551C6 - T1134 Supplement

Finance indicated that given that (as stated in the Explanatory Notes) ss. 90(2) and (5) provided a comprehensive definition of what constituted a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 233.5 | T1134 should be timely-filed with missing information noted | 162 |

2016 Ruling 2015-0617351R3 - payments under a German profit transfer agrmt “PTA"

Current structure

XX2, an indirect controlled foreign affiliate of a Canadian public corporation, is the sole limited partner of a German KG, and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(8.1) | survivor merger of two German CFAs | 44 |

11 April 2017 Internal T.I. 2016-0670541I7 - Foreign affiliate share redemption

Canco owned 100% of the preferred shares of a Barbados International Business Company (“FA”), all of whose common shares are held by a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Dividend | redemption proceeds might in part be a dividend under Barbados law | 147 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(6) - Paragraph 95(6)(b) | skewing exempt surplus to Canco could engage s. 95(6) | 137 |

2015 Ruling 2014-0541951R3 - Foreign Affiliate Debt Dumping

A limited liability partnership (FA1) will pay a distribution proportionately to its partners who directly comprise (i) a limited partner...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(9) - Paragraph 212.3(9)(b) - Subparagraph 212.3(9)(b)(ii) | s. 212.3(9)(b)(ii) PUC restoration for upper-tier QSCs on the payment by a U.S. LLP of a proportionate “dividend” to lower tier CRIC partners | 349 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Corporation | proportionate distribution by LLP treated as dividend | 128 |

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(3) | two Canadian corporate partners immediately beneath the U.S. border are QSCs respecting investments made by lower-tier CRICs in a U.S. LLP | 238 |

26 May 2016 IFA Roundtable Q. 6, 2016-0642081C6 - German Organschafts

Under an “Organschaft,” a German corporation (“Parentco”) and another corporation resident in Germany (“Subco”) enter into a Profit...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(a) - Subparagraph 95(2)(a)(ii) - Clause 95(2)(a)(ii)(B) | profit transfer payments made by a German sub to German parent are s. 90(2) dividends not within s. 95(2)(a)(ii)(B) after 2016 | 153 |

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(1) - Paragraph 53(1)(c) | German profit transfer payment to loss subsidiary is contribution of capital | 158 |

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(x) | loss compensation payment under Organschaft | 123 |

8 January 2016 Internal T.I. 2015-0604491I7 - mandatory redeemable preferred shares

CRA applied the two-step approach to entity classification to find that MRPS (Luxembourg hybrid instruments which were “very similar to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Share | MRPS (Luxembourg hybrid instruments which were “very similar to traditional shares under Canadian business corporations statutes”) were equity | 731 |

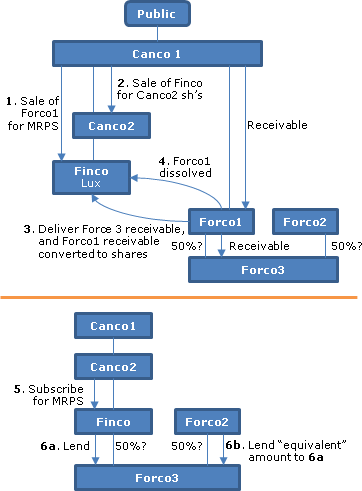

2015 Ruling 2014-0527961R3 - Deemed dividend under subsection 90(2)

underline;">: €/US$ share structure. The constating documents of FA (which is a wholly-owned subsidiary of Canco that was incorporated and is...

17 June 2014 External T.I. 2013-0506731E5 - Immigration

An individual shareholder immigrates to Canada, thereby becoming a Canadian resident, and then receives $1,000 from a wholly-owned non-resident...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Payment & Receipt | note satisfied dividend | 83 |

| Tax Topics - Income Tax Act - Section 128.1 - Subsection 128.1(1) | dividend receivable acquired on immigration | 141 |

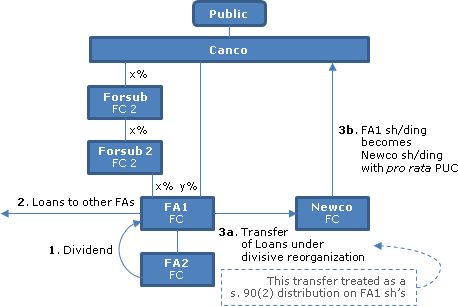

2013 Ruling 2012-0463611R3 - Foreign Divisive Reorganization

{kind=link}

Structure

Canco, a Canadian public company, directly owns a portion of the shares of FA1. FA1 is a controlled foreign affiliate of Canco...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) - Paragraph 15(1)(b) | 452 |

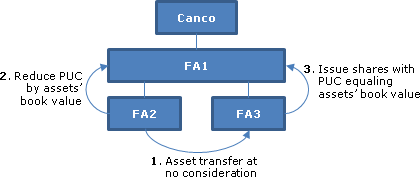

23 May 2013 IFA Round Table, Q. 2

{kind=link}

Canco owns 100% of the shares of FA1 and FA1 owns 100% of the shares of FA2. FA3 is either formed with nominal assets by FA1 or comes into...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) - Paragraph 15(1)(b) | 219 |

Articles

Melanie Huynh, Paul Barnicke, "German Organschafts", Canadian Tax Highlights, Vol. 24, No. 6, June 2016, p. 5

Unclear whether CRA view on application of s. 90(2) to Organschaft profit transfers applies where s. 90(2) applies retroactively (p. 6)

Referring...

Michael Gemmiti, "FA Dividends Must be Pro Rata", Vol. 3, No. 3, August 2013, p. 7

The new pro rata rule can present problems. For example, a US LLC (which qualifies as an FA of a taxpayer) may have only one class of units but...

Patrick W. Marley, Kim Brown, "Foreign Mergers and 'Demergers' Under Recent Canadian Proposals", Tax Management International Journal, 10 February 2012, Vol 41, No. 2, p. 86

A demerger, which under the foreign corporate law, might be viewed as one stream splitting into two, might not qualify under draft s. 90(2) as a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | 46 | |

| Tax Topics - Income Tax Act - Section 52 - Subsection 52(2) | 88 |

Geoffrey S. Turner, "Upending the Surplus Ordering Rules: Implications of the New Regulation 5901(2)(b) Election", CCH Tax Topics, No. 2079, p. 1, 12 January 2012

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5901 - Subsection 5901(2) - Paragraph 5901(2)(b) | 32 |

Elaine Buzzell, "Distributions of Share Premium by Foreign Affiliates", Corporate Finance, Vol. XVII, No. 2, 2011, p. 1962

Includes discussion of the treatment under the previous version of s. 90 of payments out of a share premium account as a dividend or shareholder...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5901 - Subsection 5901(2) - Paragraph 5901(2)(b) | 9 |

Subsection 90(3) - Qualifying return of capital

Administrative Policy

20 March 2015 External T.I. 2014-0535971E5 - Meaning of "paid-up capital" in subsection 90(3)

How is the paid-up capital of a US LLC computed for purposes of s. 90(3)? Would the paid-up capital be computed differently if the US LLC were...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Paid-Up Capital | LLC with partner capital-account style LLC Agreement does not have PUC | 74 |

6 December 2011 TEI Roundtable Q. 5, 2011-0427001C6 - 2011 TEI Q#5 - Distributions from Foreign Corp.

Under what circumstances will CRA apply subsection 15(1) to distributions of share premium? CRA stated:

[T]he proper approach for determining the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | share premium | 30 |

2004 Ruling 2004-0065921R3 - Conversion of corporations into LLCs

Conversions of corporations incorporated under the laws of Delaware and California into limited liability corporations would not result in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | conversion into California or Delaware LLC | 104 |

9 May 2002 Internal T.I. 2002-0135307 F - Application du paragraphe 39(2)

The Directorate indicated that if, under the Delaware corporate law governing a return of contributed surplus by a Delaware subsidiary of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(2) | distribution by Delaware subsidiary that did not result in s. 40 application thereby did not engage s. 39(2) | 100 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Dividend | a dividend is any corporate distribution other than of PUC | 99 |

31 August 1999 APFF Roundtable Q. 3, 9920920 F - RAPATRIEMENT DU CAPITAL D'UNE LLC

Publico, a Canadian public corporation, invested $1 million in its wholly-owned US LLC. Regarding the tax treatment of a repatriation of that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(1) | LLC return of subscription treated as PUC distribution | 159 |

1998 Ruling 9818653 - PAYMENT OF DIVIDEND BY XXXXXXXXXX CORPORATION

USco1, a subsidiary of Canco (held directly and through a Canadian subsidiary), will declare and make a distribution which will qualify as a...

8 January 1996 External T.I. 9428025 - RETURN OF CAPITAL FROM A DELAWARE CORPORATION

It is the Department's view that a dividend can include any distribution of property by a corporation to its shareholders that is not a return of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(1) | all distributions from Delaware corps are dividends | 92 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Dividend | 92 | |

| Tax Topics - Treaties - Income Tax Conventions - Article 10 | 108 |

8 December 1995 External T.I. 9415515 - PAID-UP CAPITAL REDUCTIONS- DELAWARE CORPORATIONS

FA1, a Delaware corporation, wishes to make a cash distribution to Canco by reducing its capital. However, as under Delaware corporate law a cash...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(1) | capital distribution by Delaware corp | 141 |

Articles

Tim Fraser, Jim Samuel, "The Preacquisition Surplus Election: More Than Meets the Eye?", Canadian Tax Journal (2021) 69:2, 595 - 627

Tertium quid distributions under foreign corporate law (p. 602)

- Not all foreign affiliate distributions fit neatly into the categories of a...

Subsection 90(4) - Connected person or partnership

Administrative Policy

17 May 2022 IFA Roundtable Q. 14, 2022-0926441C6 - Partnership and Subsection 90(3)Election

A limited partnership (LP) - whose 90% general partner is FA1 (held by Canco1) and whose 10% limited partner is FA2 (held by Canco2, which is...

Articles

David Bunn, Sandra Slaats, "A Critique of Proposed Subsections 90(4) to (10)", International Tax Planning, Vol XVII, no. 1, 2011

Technical deficiencies discussed include that there is a double income inclusion where a a foreign subsidiary of a partnership makes a loan the...

Drew Morier, "Canadian Proposals Mark a Decade of Changes to the Foreign Affiliate Rules", Journal of International Taxation, January 2012, p.26

Discusses application of rule where cash is not redeployed within a Canadian controlled group.

Jason D. Durkin, "Upstream Loan Rules - Why Now?", CCH Tax Topics, No. 2073, 1 December 2011, p. 1

Includes references to technical deficiencies.

Sandra Slats, David Burns, "Canada Considers New Rules on Repatriation", Tax Notes International, Vol 63, No. 9, 29 August 2011, p. 641

General discussion.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 113 - Subsection 113(1) - Paragraph 113(1)(a.1) | 8 |

Subsection 90(6) - Loan from foreign affiliate

Administrative Policy

4 August 2016 Internal T.I. 2016-0645521I7 - 90(6) & sale of creditor affiliate

Where a non-resident subsidiary (FA) of Canco has made a loan to a non-resident subsidiary (SisterCo) of Canco’s non-resident parent (Foreign...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(14) | deduction not dependent on FA being creditor affiliate at repayment time | 215 |

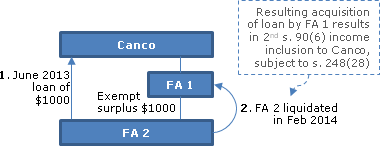

30 October 2014 External T.I. 2013-0488881E5 - Upstream Loan

As a result of a wind-up of a 2nd tier FA following a s. 90(6) loan to Canco, there technically would be a double income inclusion to Canco under...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | no double inclusion following FA creditor wind-up | 60 |

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(3) | notional s. 40(3) gain does not generate surplus | 70 |

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(9) | notional election and double taxation issues | 1332 |

| Tax Topics - Income Tax Regulations - Regulation 5901 - Subsection 5901(1.1) | notional Reg. 5901(1.1) election | 30 |

| Tax Topics - Income Tax Regulations - Regulation 5901 - Subsection 5901(2) - Paragraph 5901(2)(a) | 90-day rule unavailable | 28 |

| Tax Topics - Income Tax Regulations - Regulation 5901 - Subsection 5901(2) - Paragraph 5901(2)(b) | notional Reg. 5901(2)(b) election | 31 |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Underlying Foreign Tax | notional UFT disproportionate election | 37 |

14 November 2013 External T.I. 2013-0499121E5 - upstream loan

{kind=link}

Canco wholly owns FA 1 which wholly-owns FA 2. Each has a calendar taxation year. On December 31, 2012, FA 2 has US$1,000 of exempt and net...

22 May 2014 May IFA Roundtable, 2014-0526731C6 - IFA 2014 Q. 3bb - Upstream Loan

When is the interest on a loan made by a creditor affiliate to a specified debtor treated as indebtedness for purposes of s. 90(6), for example, a...

22 May 2014 IFA Roundtable, 2014-0526751C6 - Adjusted cost base of foreign affiliate shares

- On September 1, 2011 a foreign affiliate (FA) of a corporation resident in Canada (Canco) made a loan to a "specified debtor" in respect of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(6) | no relief from interest and penalties | 117 |

| Tax Topics - Income Tax Act - Section 92 - Subsection 92(5) | no administrative relief even where rollover at partnership level | 210 |

22 May 2014 IFA Roundtable, 2014-0526751C6 - Adjusted cost base of foreign affiliate shares

Will CRA apply IT-119R4 to give administrative relief from interest and penalties relating to the requirement to withhold tax on deemed dividends...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(6) | s. 90(6) relationship tested at time of loan | 367 |

| Tax Topics - Income Tax Act - Section 92 - Subsection 92(5) | no administrative relief even where rollover at partnership level | 210 |

Articles

Clara Pham, "An Unpaid Amount Could Be an Upstream Loan", Canadian Tax Focus, Vol. 5, No. 3, August 2015, p.5.

Potential double inclusion for unpaid fee owing by Canco to FA (p.5)

Assume that Canco owns a foreign affiliate (FA). Both Canco and FA have...

Paul Barnicke, Melanie Huynh, "Upstream Loans: CRA Update", Canadian Tax Highlights, Vol. 21, No. 12, December 2013, p. 3

Their discussion includes a summary of an as-yet unpublished CRA technical interpretation [2013-0499121E5, now summarized above], which dealt with...

Ken J. Buttenham, "Are you Ready for the Upstream Loan Rules?", Canadian Tax Journal, (2013) 61:3, 747-68

Relationships tested when upstream loan arose (pp. 761-2)

The application of subsection 90(6) and other upstream loan rules is based on the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(14) | 402 | |

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(9) | 1010 |

Subsection 90(6.1)

Articles

Joint Committee, "Technical Amendments Package of September 16, 2016", Submission letter of 15 November 2016

No relief where upstream lender ceases to be an FA

The proposed continuity rules in ss. 90(6.1) and (6.11) do not provide relief from an income...

Subsection 90(7) - Back-to-back loans

Administrative Policy

2024 Ruling 2024-1027391R3 - Upstream loans

Background

Canco, which was wholly-owned by Forco 1 (resident in Country 2), held all the shares of a (non-resident) subsidiary (“CFA”)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(8) - Paragraph 90(8)(a) | repayment by CFA of upstream loans before its sale by Canco to non-resident parent | 192 |

26 May 2016 IFA Roundtable, Q. 5

FA2 lends excess liquidity $10M to its wholly-owning parent, FA1, which on-lends the $10M to its wholly-owning Canadian parent, Canco. At the...

Paragraph 90(7)(a)

Administrative Policy

John Lorito and Trevor O'Brien, "International Finance – Cash Pooling Arrangements," draft version of paper for CTF 2014 Conference Report.

In the case of notional pooling, loans to and from the third party bank may be subject to the upstream loan rules through the application of the...

Subsection 90(8) - Exceptions to subsection (6)

Paragraph 90(8)(a)

Administrative Policy

24 July 2023 Internal T.I. 2020-0841891I7 - Upstream Loan

The taxpayer, a taxable Canadian corporation, had received a non-interest-bearing loan (the “Loan Payable”) in undocumented form from a wholly...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Payment & Receipt | loan owed by taxpayer to FA2 not repaid on winding up of FA2 into FA1, but was then repaid by set-off | 188 |

2024 Ruling 2024-1027391R3 - Upstream loans

Background

A non-resident subsidiary of Canco (“CFA”) had made loans out of its retained earnings (the “Equity Funded Loans”) to Finco 1...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(7) | back-to-back loan rule in s. 90(7) precluded the application of s. 90(6) to “upstream” loans made by a CFA to specified debtors | 492 |

2017 Ruling 2016-0670971R3 - Repayments of upstream loans and series test

Background

Canco3, which was a CRIC (corporation resident in Canada) and an indirect wholly-owned subsidiary of a non-resident corporation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(14) | loan repayment not part of a prohibited series | 143 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | automatic loan renewals did not entail the making of new loans | 58 |

3 March 2017 Internal T.I. 2016-0673661I7 - Upstream loans – allocation of repayments

Prior to August 19, 2011, Canco borrowed $50M (“Advance A”) from its wholly-owned non-resident subsidiary (“FA”), and borrowed a further...

26 May 2016 IFA Roundtable Q. 4, 2016-0642151C6 - Upstream loan converted to PLOI

Canco indirectly distributed $10M of excess cash to its non-resident parent (NRco) in 2010 through a capital contribution by it to a new foreign...

24 November 2015 CTF Roundtable Q. 8, 2015-0610621C6 - FA Liquidation and upstream loans

A loan from a foreign affiliate to its Canadian parent (Canco) generally must be repaid within two years lest the amount of the loan be included...

24 November 2013 CTF Roundtable, 2013-0508151C6 - Upstream Loans

A loan or indebtedness will be considered to have been repaid by a debtor by way of set-off against a receivable of the debtor "if the set-off...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Payment & Receipt | repayment by set-off | 75 |

2013 Ruling 2013-0491061R3 - Upstream Loans

{kind=link}

Non-resident subsidiaries (perhaps resident in the US) of a non-resident public company ("Parent") hold stacked non-resident companies (FA 1 to 4...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(25) - Paragraph 212.3(25)(b) | s. 212.3(25)(b) avoids acquisition on partnership winding-up | 423 |

Articles

Geoffrey S. Turner, "Transitional Tax Treatment of Grandfathered Upstream Loans – Repayment Deadline Approaching", International Tax (Wolters Kluwer CCH), No. 88, June 2016, p. 7

August 19, 2016 repayment deadline for pre-August 20, 2011 loans (p.7)

The paragraph 90(8)(a) carve-out from the upstream loan rules provides...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(9) | 378 | |

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(2.1) | 118 |

Paragraph 90(8)(b)

Articles

Audrey Dubois, "Upstream Loans: Limitation on the Scope of the Moneylending Business Exception", International Tax Highlights, Vol. 1, No. 2 November 2022, p. 9

Existing s. 90(8)(b) exception (p. 9)

- S. 90(8)(b) provides one of the exceptions to the application of s. 90(6), namely, for indebtedness that...

Subsection 90(9) - Corporations: deduction for amounts included under subsection (6) or (12)

Administrative Policy

20 March 2017 External T.I. 2014-0545591E5 - Upstream Loan and Debt Forgiveness Rules

FA makes a loan to Canco, its wholly-owning parent. Canco then sells its interest in FA to a third party, but due to foreign tax and other...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) - Excluded Obligation - Paragraph (a) | s. 80 non-application where s. 90(6) applies to forgiven loan even if offsetting surplus deduction | 156 |

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(14) | debt forgiveness not a repayment | 56 |

28 May 2015 IFA Roundtable Q. 4, 2015-0581501C6 - Upstream loans: ss. 90(9) deduction

Part A: LIFO ordering/s. 113(1)(a) deduction for actual dividends

In 2013 FA, which had exempt surplus ("ES") and net surplus ("NS") of US$100,...

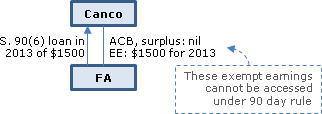

30 October 2014 External T.I. 2013-0488881E5 - Upstream Loan

Scenario 1 [90-day rule unavailable]

{kind=link}

On December 31, 2012, FA has a nil "net surplus" balance and no relevant deficits. In its 2013 (calendar)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | no double inclusion following FA creditor wind-up | 60 |

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(3) | notional s. 40(3) gain does not generate surplus | 70 |

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(6) | no double inclusion following FA creditor wind-up or for 2nd loan in series | 121 |

| Tax Topics - Income Tax Regulations - Regulation 5901 - Subsection 5901(1.1) | notional Reg. 5901(1.1) election | 30 |

| Tax Topics - Income Tax Regulations - Regulation 5901 - Subsection 5901(2) - Paragraph 5901(2)(a) | 90-day rule unavailable | 28 |

| Tax Topics - Income Tax Regulations - Regulation 5901 - Subsection 5901(2) - Paragraph 5901(2)(b) | notional Reg. 5901(2)(b) election | 31 |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Underlying Foreign Tax | notional UFT disproportionate election | 37 |

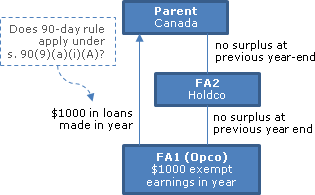

22 May 2014 May IFA Roundtable Q. 3a, 2014-0526721C6 - IFA 2014 Q. 3a(a) - Upstream Loan

{kind=link}

An indirectly-owned foreign affiliate ("FA1") generates substantial exempt surplus during a taxation year and uses the resulting cash flow to...

22 May 2013 IFA Roundtable, 2013-0483791C6 - Upstream Loans

Assume that Canco owns all the shares of FA. FA has $100 of taxable surplus ("TS"), no exempt surplus and no underlying foreign tax (UFT)...

Articles

Tim Barrett, Andrew Morreale, "Foreign Affiliate Update", 2019 Conference Report (Canadian Tax Foundation), 35: 1 – 53

Issues with upstream loan rules

- Remaining issues with the upstream loan rules include:

- “Surplus deficits in entities above the lending entity...

Michael N. Kandev, Sandra Slaats, "Recent Developments in the Foreign Affiliate Area", 2015 Annual CTF Conference paper

Inappropriate reduction of reserve by blocking deficit of intermediate FA Holdco (pp. 31:31-31:34)

One of the fundamental issues with the reserve...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Corporation | 300 | |

| Tax Topics - Income Tax Act - Section 96 | 354 |

Geoffrey S. Turner, "Transitional Tax Treatment of Grandfathered Upstream Loans – Repayment Deadline Approaching", International Tax (Wolters Kluwer CCH), No. 88, June 2016, p. 7

Perennial reserve and inclusion mechanism (p. 6)

When the Canadian taxpayer (or the "specified debtor") finally repays the upstream loan or...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(8) - Paragraph 90(8)(a) | 104 | |

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(2.1) | 118 |

Geoffrey S. Turner, "Upstream Loans and Dispositions of Foreign Affiliate Shares", International Tax (Wolters Kluwer CCH), No. 85, December 2015, p.1

Upstream loan must be repaid to escape rule (p.1)

[U]nder the current rules, anomalous results can be avoided with certainty only by causing the...

Ian Bradley, Marianne Thompson, Ken J. Buttenham, "Recommended Amendments to the Upstream Loan Rules", Canadian Tax Journal, (2015) 63:1, 245-67.

Narrowness of s. 90(11) (p. 261)

{kind=link}

Subsection 90(11) incorporates only the surplus of the downstream foreign affiliates that are directly or...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(14) | 754 |

Ken J. Buttenham, "Are you Ready for the Upstream Loan Rules?", Canadian Tax Journal, (2013) 61:3, 747-68

Uncertainties under s. 90(9) (p. 763)

The operation of subsection 90(9) raises a host of unanswered questions and is probably what will create...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(14) | 402 | |

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(6) | 180 |

Finance

26 April 2017 IFA Finance Roundtable, Q.11

[approbation of CRA workaround for dealing with an upper-tier blocking deficit respecting upstream...

Paragraph 90(9)(b)

Administrative Policy

5 May 2021 IFA Roundtable, Q.8

Canco received a loan from a controlled foreign affiliate (“CFA”) that remained outstanding at the end of years 1, 2 and 3, and was then...

Subsection 90(10)

Articles

Michael Spinelli, Karthika Ariyakumaran, "Upstream Loans Disadvantage Corporate Members of a Partnership", Canadian Tax Focus, Volume 8, Number 4, November 2018, p.5

Loan by CFA of partnership to one of two arm’s length Cdn partners (p.5)

Assume that Canco 1 and Canco 2 are Canadian-resident corporations...

Subsection 90(14) - Repayment of loan

Administrative Policy

2017 Ruling 2016-0670971R3 - Repayments of upstream loans and series test

An LLC subsidiary of a Canadian subsidiary (Canco3 - that was lower down in a corporate group controlled by a U.S. Pubco) received the repayment...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(8) - Paragraph 90(8)(a) | subsequent intercorporate loans and discharges were not part of “series of loans or other transactions and repayments” | 302 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | automatic loan renewals did not entail the making of new loans | 58 |

20 March 2017 External T.I. 2014-0545591E5 - Upstream Loan and Debt Forgiveness Rules

When an upstream loan to Canco from its wholly owned CFA is forgiven following a sale of the CFA, this will not qualify as a repayment of the loan...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(9) | potential indefinite application of surplus where upstream loan forgiven after FA sale | 203 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) - Excluded Obligation - Paragraph (a) | s. 80 non-application where s. 90(6) applies to forgiven loan even if offsetting surplus deduction | 156 |

4 August 2016 Internal T.I. 2016-0645521I7 - 90(6) & sale of creditor affiliate

In 2013, FA, which is wholly-owned by Canco, makes a loan to SisterCo., which is wholly-owned by the non-resident parent of Canco (“Foreign...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(6) | inclusion not dependent of maintenance of creditor affiliate status | 73 |

22 May 2014 May IFA Roundtable, 2014-0526741C6 - Foreign affiliates - upstream loans

CRA has not yet developed any specific positions on the application of the upstream loan rules to cash pooling arrangements and would welcome a...

2013 Ruling 2013-0477871R3 - 5900(1)(a) and dividends from foreign affiliate

A non-resident subsidiary (ForeignHoldco) of a taxable Canadian corporation (Parent) will eliminate a non-interest-bearing loan previously made by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(11.2) | dividends from Malaysian offshore company | 358 |

Finance

1 May 2018 Finance Comfort letter respecting repayment of back-to-back loans under the upstream loan rules

A Bermuda-resident foreign affiliate (“FA 1") of Canco made loans (the "FA 1 Loans") to Forco 1 which, in turn, has made loans (the "Forco 1...

16 May 2018 IFA Finance Roundtable, Q.10

The upstream loan regime in s. 90 provides for income inclusions under s. 90(6) for certain loans and indebtedness owing to foreign affiliates,...

Articles

Ian Bradley, Marianne Thompson, Ken J. Buttenham, "Recommended Amendments to the Upstream Loan Rules", Canadian Tax Journal, (2015) 63:1, 245-67.

Narrowness of repayment rule (p. 251)

There are situations in which an upstream loan may cease to represent a synthetic distribution from a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(9) | 774 |

Ken J. Buttenham, "Are you Ready for the Upstream Loan Rules?", Canadian Tax Journal, (2013) 61:3, 747-68

Application to cash-pooling arrangements (p. 755)

…In practice, it may be challenging for taxpayers and the CRA to determine the correct...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(6) | 180 | |

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(9) | 1010 |

Finance

26 April 2017 IFA Finance Roundtable, Q.10

[relief for where upstream loans no longer are synthetic distributions]

A foreign affiliate (Forco1)...

Subsection 90(15) - Definitions

Articles

John Lorito, Trevor O'Brien, "International Finance – Cash Pooling Arrangements", 2014 Conference Report, (Canadian Tax Foundation), 20:1-33

{kind=link}

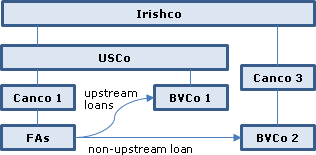

Exclusion for loans to NR subs of related Canadian corporations (pp. 11-12)

Consider…the structure…in which BVCo 1 [a NR sub of the immediate...

specified debtor

(b)

Administrative Policy

2014 Ruling 2013-0510551R3 - Upstream Loans - Specified Debtor

{kind=link}

Current structure

Canco1, a Canadian public corporation, wholly-owns Canco2 and Forco1, which is solely a holding company for the Canco1 equity...

Commentary

S. 90(3) override of s. 90(2)

S. 90(2) deems most distributions to a taxpayer by a foreign affiliate (made pro rata to its shareholding), other...