Subsection 93(1) - Election re disposition of share of foreign affiliate

Cases

Terrador Investments Ltd. v. R., 99 DTC 5358, [1999] 3 CTC 520 (FCA)

In connection with the liquidation of a U.S. corporation owned by the two Canadian corporate taxpayers, they received promissory notes owing by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Interpretation/Definition Provisions | reasonable implication of deemed fiction of a dividend received | 94 |

Administrative Policy

5 September 2018 Internal T.I. 2017-0698241I7 - Interpretation of subsection 93(4)

But for s. 94(3), a Canadian corporation (ACo) would have realized a capital loss of $1 million on the liquidation and dissolution of a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 93 - Subsection 93(4) | FA sub shares acquired “on” disposition of FA parent shares occurring on completion of liquidation and dissolution process | 243 |

| Tax Topics - Income Tax Act - Section 93 - Subsection 93(2.01) | s. 93(2.01) applied to capital loss resulting from s. 94(3) basis bump | 188 |

14 March 1991 Memorandum (Tax Window, No. 1, p. 21, ¶1143)

RC permits only one election to be made with respect to a particular disposition of shares.

Forms

T2107 Election for a Disposition of Shares in a Foreign Affiliate

Instructions

- Separate elections must be made when a disposition of shares in a foreign affiliate involves shares of different classes or when...

Articles

Paul Dhesi, Korinna Fehrmann, "Integration Across Borders", Canadian Tax Journal, (2015) 63:4, 1049-72

Inefficiency of realization of capital gains by CFA of CCPC (p. 1062, 1064)

[T]he realization of capital gains at the CFA level...is rarely good...

Eric Lockwood, Maria Lopes, "Subsection 88(3): Deferring Gains on Liquidation and Dissolution", Canadian Tax Journal (2013) 61:1, 209-28, p. 209

They provide various examples indicating that a taxpayer (Canco) will realize a capital gain on the disposition of its shares of the disposing...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(3.3) | 503 | |

| Tax Topics - Income Tax Regulations - Regulation 5905 - Subsection 5905(7.2) | 651 |

Hetel Kotecha, "The Subsection 93(1) Election - Strategy and Pitfalls", International Tax Planning, 2003, p. 792.

Ron Nobrega, "Technical Bill Amendments Affecting Foreign Affiliate Share Transfers", Taxation Law, Ontario Bar Association, Vol. XIII, No. 3, p. 1.

Schwartz, "Tax-Free Reorganizations of Foreign Affiliates", 1984 Canadian Tax Journal, November-December 1984, p. 1039.

Bradley, "Foreign Affiliates: A Technical Update", 1990 Conference Report, c. 43

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 91 - Subsection 91(5) | 92 |

Forms

T2107 "Election For A Disposition Of Shares In A Foreign Affiliate"

Separate elections have to be made when a disposition of shares in a foreign...

Subsection 93(1.1)

Paragraph 93(1.1)(b)

Articles

Tim Fraser, Jim Samuel, "The Preacquisition Surplus Election: More Than Meets the Eye?", Canadian Tax Journal (2021) 69:2, 595 - 627

Automatic s. 93(1.1) dividend if s. 40(3) gain (p. 599, f.n. 13)

- Ss. 93(1.1) and (1.11) generally provide that any s. 40(3) gain realized by a...

Subsection 93(1.3)

Articles

Tina Korovilas, Drew Morier, "Non-Corporate Vehicles in the Foreign Affiliate Context", 2018 Conference Report (Canadian Tax Foundation), 20:1 – 114

Unavailability of s. 93 regime where partnership interest disposed of (p. 20:49)

[S]ubsection 93(1.3) applies only where the shares disposed of...

Subsection 93(1.11)

Administrative Policy

2017 Ruling 2017-0693751R3 - Transfer of Shares of a Foreign Affiliate

See the diagram for the 2016-0630761R3 transactions.

A Canadian-resident corporation (ACo) wished to transfer its shares of a foreign subsidiary...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(11) - Paragraph 69(11)(b) | s. 69(11)(b) inapplicable to transfer of FA to new FA who will use the excluded property exemption | 324 |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Shares | affiliated transfer of shares at gain equal to exempt surplus did not cause loss of capital property status | 85 |

2016 Ruling 2016-0630761R3 - Transfer of Shares

Background

ACo wholly-owns BCo, which is a foreign corporation with its central management and control in Canada, and FA1, the fair market value...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5901 - Subsection 5901(2) - Paragraph 5901(2)(b) | stated capital distribution from FA treated as pre-acq dividend | 188 |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | no conferral of benefit where CRA required sideways transfer to occur at less than FMV | 221 |

Subsection 93(2)

Administrative Policy

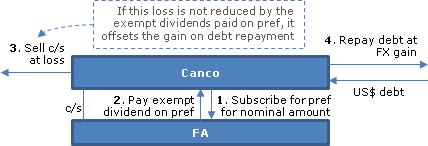

22 December 2009 Internal T.I. 2009-0328141I7 F - 93(2) - Perte due à fluctuation de devises

The Taxpayer, a taxable Canadian corporation, used the proceeds of a U.S.-dollar loan to subscribe for shares of a wholly-owned foreign affiliate...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 93 - Subsection 93(2.01) - Paragraph 93(2.01)(b) | relief under s. 93(2.01)(b) unavailable where matching FX gain is realized in a subsequent year | 158 |

Subsection 93(2.01) - Loss limitation on disposition of share of foreign affiliate

Administrative Policy

5 September 2018 Internal T.I. 2017-0698241I7 - Interpretation of subsection 93(4)

But for s. 94(3), a Canadian corporation (ACo) would have realized a capital loss of $1 million on the liquidation and dissolution of a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 93 - Subsection 93(4) | FA sub shares acquired “on” disposition of FA parent shares occurring on completion of liquidation and dissolution process | 243 |

| Tax Topics - Income Tax Act - Section 93 - Subsection 93(1) | no s. 93 election available where ACB bump under s. 94(3) eliminated gain before application of s. 93(1) | 146 |

22 June 2016 Internal T.I. 2016-0632821I7 F - 93(2.01) & Capital Contribution

A wholly-owned foreign affiliate (“Luxco1”) of Canco held 1/3 of the shares of a corporation ("NRco") resident in a Treaty country. Another...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(5) | ordinary meaning of “substituted” | 121 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(a) - Subparagraph 95(2)(a)(ii) - Clause 95(2)(a)(ii)(B) | inter-affiliate loan generating deemed active business funded out of an interest-free loan from Canco | 105 |

26 May 2016 IFA Roundtable Q. 7, 2016-0642121C6 - 93(2.01) & Capital Contribution

CRA considered that the s. 93(2.01) stop loss rule applied where Canco made a contribution of capital to a foreign subsidiary (FA2) of its shares...

15 August 2014 Internal T.I. 2014-0538591I7 - FX losses on CFA wind-up

A Canadian-resident corporation did not elect under s. 88(3.1) for the winding-up of its wholly-owned controlled foreign affiliate (CFA) to be a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(3.6) | s. 40(3.6) does not apply to winding-up | 159 |

24 November 2013 CTF Roundtable, 2013-0508161C6 - Loss on disposition of shares

{kind=link}

A shareholder having an accrued foreign exchange loss on common shares of an FA and an accrued foreign exchange gain on a related party debt used...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 112 - Subsection 112(3) | loss preservation transactions which avoid s. 112(3) stop-loss rule | 293 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | loss preservation transactions which did not satisfy the s. 93(2.01) requirements | 205 |

25 September 2013 Internal T.I. 2013-0476311I7 F - 93(2), 93(2.01) - Share substituted

{kind=link}

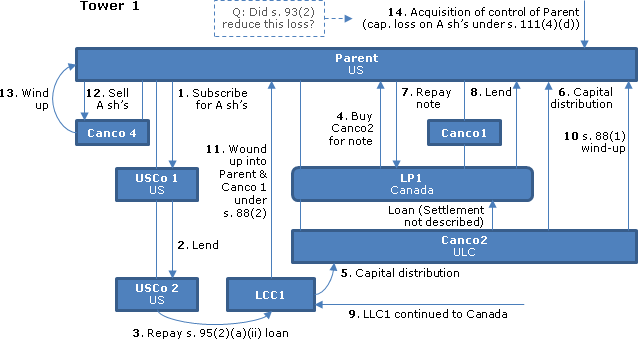

Tower 1

Under a Tower structure (Structure 1) a taxable Canadian corporation (Parent), all of whose shares were held directly or indirectly by a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(5) | s. 248(5) requirement for a legal exchange is engaged by a reference to a substituted share | 199 |

23 May 2013 IFA Round Table Q. 3

What is the CRA's position on the application of the GAAR to a series of transactions undertaken for the purpose of avoiding the application of s....

10 May 2013 Internal T.I. 2012-0464901I7 - 93(2), 93(2.01) - Share substituted

Canco owns all the shares of Forco1, which it transfers to Forco2 for a promissory note payable in U.S. dollars, and then transfers the note to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(5) | 72 |

Articles

Didier Fréchette, Ryan Rabinovitch, "Current Issues Involving Foreign Exchange", 2015 CTF Annual Conference paper

Narrowness of 30-day rule/exclusion for related party debt (pp. 26:46)

Despite the promising comments made in the 2001 comfort letter, the loss...

Nikolakakis, "Foreign Exchange Fluctuations: Comprehensive Rules are Needed", Corporate Finance, Vol. V, No. 1, 1997.

Paragraph 93(2.01)(b)

Administrative Policy

22 December 2009 Internal T.I. 2009-0328141I7 F - 93(2) - Perte due à fluctuation de devises

The Taxpayer, a taxable Canadian corporation, used the proceeds of a U.S.-dollar loan to subscribe for shares of a wholly-owned foreign affiliate...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 93 - Subsection 93(2) | loss under s. 93(2) includes a loss wholly attributable to a fully-hedged FX loss | 207 |

Subsection 93(2.1)

Articles

Didier Fréchette, Ryan Rabinovitch, "Current Issues Involving Foreign Exchange", 2015 CTF Annual Conference paper

Whether substitutions for s. 93(2.1) purposes are not limited to share-for-share transactions (p. 26:47)

The CRA has taken an expansive view of...

Subsection 93(4)

Administrative Policy

5 September 2018 Internal T.I. 2017-0698241I7 - Interpretation of subsection 93(4)

On a liquidation and dissolution (“L&D”) of FA1, it distributed to its parent (ACo) its shares of (wholly-owned) FA2 and FA3 and other...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 93 - Subsection 93(2.01) | s. 93(2.01) applied to capital loss resulting from s. 94(3) basis bump | 188 |

| Tax Topics - Income Tax Act - Section 93 - Subsection 93(1) | no s. 93 election available where ACB bump under s. 94(3) eliminated gain before application of s. 93(1) | 146 |