Subsection 92(1) - Adjusted cost base of share of foreign affiliate

Paragraph 92(1)(a)

Administrative Policy

27 June 2008 External T.I. 2007-0247551E5 - FAPI and Part XIII Tax

Two wholly-owned U.S.-resident subsidiaries of Canco (CFA1 and CFA2) carry on a U.S. active business through a U.S. general partnership (FP)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 96 | DRUPA partnership | 38 |

| Tax Topics - Income Tax Regulations - Regulation 5900 - Subsection 5900(3) | partnership between 2 CFAs was a Cdn-resident person for s. 91(5) purposes | 68 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Accrual Property Income - A - Paragraph (b) | FA dividends received by NR partnership between 2 CFAs (FP) not excluded from FAPI, but deduction under s. 91(5)/ Reg. 5900(3) to FP | 298 |

| Tax Topics - Income Tax Act - Section 91 - Subsection 91(5) | s. 91(5) deduction eliminated net FAPI inclusion to CFA members of foreign partnership receiving foreign dividends from partnership subsidiary | 107 |

4 September 1990 Ruling 59693 F - Amounts Deductible in Respect of Dividends Received

F, a controlled foreign affiliate of C, a taxable Canadian corporation earned foreign accrual property income ("FAPI") in its 1990 taxation year...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 91 - Subsection 91(5) - Paragraph 91(5)(b) | s. 92(1)(a) ACB bump for current year’s FAPI is treated for s. 91(5)(b)(i) purposes as occurring immediately before a dividend paid in that year out of such FAPI | 251 |

Articles

Allan Lanthier, "FAPI or Taxable Surplus Dividend", Canadian Tax Highlights, Vol. 23, No. 2, February 2015, p. 4.

Dispute as to whether FA earns ABI or FAPI (p. 4)

Assume that Canco owns CFA and that the relevant years are all before 2012. In year 1, CFA earns...

Subsection 92(4)

Articles

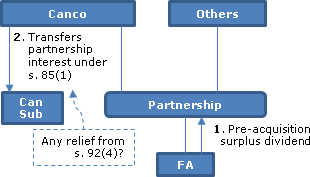

Ben Cen, "Planning for FA Distributions Paid Through a Partnership", Canadian Tax Focus, Vol. 10, No. 2, May 2020, p. 6

Addition under s. 92(4) of proceeds on partnership interest disposition where previous s. 113(1)(d) deduction, even where a rollover transaction...

Subsection 92(5) - Deemed gain from the disposition of a share

Administrative Policy

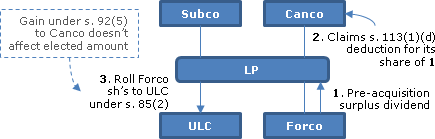

7 May 2014 Internal T.I. 2012-0433731I7 - Application of subsections 92(5) and (6)

{kind=link}

Two Canadian corporations ("Canco" and "Subco") were the respective limited and general partners of "LP" which, in turn, held all of the shares...

22 May 2014 IFA Roundtable, 2014-0526751C6 - Adjusted cost base of foreign affiliate shares

{kind=link}

Will the CRA provide administrative relief in circumstances where the partnership interest or foreign affiliate shares are disposed of as part of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(6) | no relief from interest and penalties | 117 |

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(6) | s. 90(6) relationship tested at time of loan | 367 |

Articles

Geoffrey S. Turner, "ACB Adjustments for Foreign Affiliate Shares Held Through Partnerships", International Tax (Wolters Kluwer CCH), No. 79, December 2014, p. 1.

No immediate ACB grind for pre-acq dividends received by partnership (p.4)

Thus, instead of applying the regular ACB reduction rule in subsection...

Paul Barnicke, Melanie Huynh, "FA Shares Held in Partnership", Canadian Tax Highlights, Vol 22, No 6, June 2014, p. 8

Additional problem where partner is an FA (pp. 8-9)

The problem created by subsections 92(4) to 92(6) is not limited to structures in which a...