Subsection 85(1) - Transfer of property to corporation by shareholders

Cases

Barnabe Estate v. Minister of National Revenue, 99 DTC 5387, [1999] 4 CTC 5 (FCA)

A farmer, before dying, made an oral agreement with a corporation owned by him to transfer the assets of a farming business to it. It was found...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | transaction effective at time of informal oral agreement | 147 |

Dale v. R., 97 DTC 5252, [1997] 2 CTC 286 (FCA)

The taxpayers agreed with the corporation controlled by them to transfer an apartment building to the corporation in consideration for the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | retroactive superior court order has retroactive effect for tax purposes | 174 |

| Tax Topics - General Concepts - Rectification & Rescission | retroactive effect of nunc pro tunc rectification order | 177 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Dividend | 78 | |

| Tax Topics - Income Tax Act - Section 83 - Subsection 83(2) | 78 | |

| Tax Topics - Statutory Interpretation - Provincial Law | 140 |

Deconinck v. The Queen, 90 DTC 6617, [1990] 2 CTC 464 (FCA)

Although on the taxpayer's evidence an election form filed by the taxpayer was intended to accord rollover treatment for the conveyance by the...

See Also

Les Développements Iberville Ltée v. Agence du Revenu du Québec, 2018 QCCA 1886 (Quebec Court of Appeal)

Three affiliated Quebec corporations avoided (or so they thought) most of the Quebec tax on the sale of Quebec real estate at a gain of around...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | abuse to use rollover provisions to avoid rather than defer tax | 683 |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Real Estate | property bifurcated between capital and income portion on acquisition | 98 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Improvements v. Repairs or Running Expense | improvements to leased retail premises were not demonstrated to be made only at tenants’ requests | 106 |

| Tax Topics - Income Tax Regulations - Regulation 402 - Subsection 402(6) | purpose of inter-provincial allocation rules is for 100% of income to be allocated and taxed | 558 |

| Tax Topics - Income Tax Act - Section 249.1 - Subsection 249.1(1) | no policy of permitting differing Quebec and federal year ends | 196 |

Dale v. The Queen, 94 DTC 1100, [1994] 1 CTC 2303 (TCC), aff'd supra.

The taxpayers agreed with a corporation controlled by them to transfer an apartment building to the corporation in consideration for the issuance...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | 78 | |

| Tax Topics - Statutory Interpretation - Drafting Style | 93 |

The Queen v. Miller, 90 DTC 6335, [1990] 2 CTC 4 (FCTD)

Collier, J. indicated that "common sense dictates" that where the taxpayer's income for a year was increased as a result of a Revenue Canada...

Cox v. I.R.C., [1988] BTC 37 (HCJ)

An obligation to file returns was not satisfied when "to be advised" or "details to follow" were entered against certain items.

Ward-Stemp v. Griffin, [1988] BTC 12 (HCJ)

Walton, J. stated, obiter, that it might be arguable that a statutory requirement to make an election "in such form and manner as the Board may...

The Queen v. Leslie, 75 DTC 5086, [1975] CTC 155 (FCTD)

On the incorporation of a business the agreement purported to transfer net assets having a value of $5,078 and goodwill having a value of $20,222...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | no asset backing for note - no benefit until paid | 93 |

Deltona Corp. v. MNR, 71 DTC 5186, [1971] CTC 297 (Ex Ct), briefly aff'd 73 DTC 5180, [1973] CTC 215 (SCC)

An election filed by a predecessor corporation for the amalgamated corporation to be taxed as an NRO was invalid. "I can find no suggestion of any...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 133 - Subsection 133(8) - Non-Resident-Owned Investment Corporation | 143 | |

| Tax Topics - Income Tax Act - Section 250 - Subsection 250(4) | although an amalgamated corporation was "continued" from its predecessors on amalgamation, it came into existence on the amalgamation | 120 |

Administrative Policy

2020 Ruling 2020-0854091R3 - Safe Income and Section 47

The proposed transactions included Parent exchanging all its Common Shares of Subsidiary on a s. 85(1) rollover basis for non-voting redeemable...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(c) | safe income of common shares acquired on a s. 88(1) wind-up averaged with directly-purchased common shares/ no safe income reduction on redemption of high ACB prefs | 426 |

15 September 2020 IFA Roundtable Q. 1, 2020-0853411C6 F - IFA 2020 Roundtable – T2057 & Functional Currency

Where the parties to a s. 85 rollover transaction have different tax reporting currencies (as defined in s. 261(1)), in what currency should the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 261 - Subsection 261(5) - Paragraph 261(5)(a) | different currency reporting of s. 85(1) rollover where one party has elected a functional currency | 63 |

5 October 2012 Roundtable, 2012-0451291C6 F - Subsection 85(1) and UMIR Marketplace Rules

The questioner referred to securities’ law requirements that certain transactions occur on the exchange rather than on an off-market basis. CRA...

2015 Ruling 2015-0589471R3 - Earnout

In connection with the implementation of an earnout transaction for the purchase of Holdco common shares by a key employee, the (corporate)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(g) | 5-year earnings based earnout for sale of Holdco common shares by Opco to key employee | 841 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Safe-Income Determination Time | safe income determination time for a subsequent contemplated annual common share dividend was immediately before that dividend rather than a prior dividend or s. 55(3)(a)(ii) or (v) increase | 654 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(c) | utilization of safe income as earned through a contemplated succession of dividends of all the annual earnings | 203 |

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(1) - Paragraph 7(1)(a) | transactions for using s. 7 rules on sale of non-treasury shares | 212 |

9 October 2015 APFF Roundtable Q. 21, 2015-0598291C6 F - Filing deadline for various forms

As Saturdays are "public holidays" as defined in the Interpretation Act, s. 35, if the return filing deadline of the taxpayer falls on a Saturday...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Interpretation Act - Section 26 | where a return filing deadline falls on a Saturday, the deadline for related forms also is extended to the Monday | 92 |

29 January 2015 Internal T.I. 2014-0544651I7 - Section 85 transfer of Swap Contracts

The taxpayer entered into cross-currency (U.S.$/Cdn$) Swap Contracts with a counterparty respecting the issuance of U.S.-dollar notes issued by it...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Inventory | swap contract treated as inventory | 55 |

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1.1) | swap contract treated as inventory | 180 |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Foreign Exchange | swap contract treated as inventory | 55 |

S4-F7-C1 - Amalgamations of Canadian Corporations

1.61 If the laws governing an amalgamation provide that the predecessor corporations are continued in the amalgamated corporation, the...

11 October 2013 APFF Roundtable, 2013-0495821C6 F - Share disposition

In order to isolate cost base in preferred shares, a taxpayer transfers his common shares of a corporation to the corporation in exchange for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | no disposition where shares exchanged for identical-attribute shares of a different class | 229 |

7 October 2011 APFF Roundtable Q. 17, 2011-0412171C6 F - 112(7) - Share-for-Share Exchange - 85(1)

Where there is an exchange of 100 common shares in the capital of a corporation for 100 "new" common shares in its capital, there could be...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 112 - Subsection 112(3) | s. 112(3) could still apply if "old" dividend-bearing shares "exchanged" under purported s. 85(1) exchange for "new" but identical shares | 98 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | purported dirty s. 85 exchange of old common shares for new common shares does "not necessarily" entail a disposition | 49 |

| Tax Topics - Income Tax Act - Section 112 - Subsection 112(7) | s. 112(7) does not “technically” apply to a dirty s. 85 exchange of old shares for new shares | 257 |

8 October 2010 Roundtable, 2010-0373231C6 F - Application of subsections 51(1) and 85(1)

In confirming its position in IT-291R3, para. 35, CRA stated:

The Dale case concerned a transferee corporation that had issued shares that were...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 51 - Subsection 51(1) | simultaneous exchange | 50 |

30 April 2009 External T.I. 2008-0296721E5 F - Late filed election 85(7) - Amending transactions

An individual transferred an immovable to his corporation for non-share consideration. The CRA assessed recapture and a capital gain on the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Rectification & Rescission | CRA will not anticipate a judicial rectification | 189 |

10 November 2004 External T.I. 2004-0092561E5 F - 85(1), 248(1) "Disposition"

Mr. X, who holds all 100 common shares of Corporation A having a fair market value, ACB and PUC of $1,000,000, $500,000 and $1000, respectively,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | no disposition to the extent that there is a dirty s. 95 exchange of old common shares for identical new common shares | 261 |

6 July 2004 External T.I. 2004-0081631E5 F - Price Adjustment Clauses

CRA will accept a rollover form filed with a "yes" answer to the question concerning the existence of a price adjustment clause as sufficient...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | no requirement to notify CRA of price-adjustment clause otherwise than by ticking box on any prescribed form | 136 |

| Tax Topics - Income Tax Act - Section 51 - Subsection 51(1) | no requirement to notify CRA of price-adjustment clause regarding a s. 86 or 51 exchange | 95 |

13 July 2004 External T.I. 2004-0058141E5 F - Transfert du droit aux revenus provenant d'un bien

A couple transferred, to their jointly-owned corporation, the right to receive the income from a Quebec rental property for a specified period, in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(3) | assignment of the rents from a rental property to a corporation would result in a disposition to a deemed trust under s. 248(3) | 134 |

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(2) | s. 75(2) applicable to assignment of the rents from a rental property to a corporation giving rise to a deemed trust under s. 248(3) | 93 |

12 November 2003 External T.I. 2002-0121835 - 85(1) - Holdbacks Payable

On a sale by a contractor of its construction contracts to a corporate purchaser, the fair market value of builder's holdbacks assumed by the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) - Paragraph 85(1)(b) | 59 |

6 November 2003 External T.I. 2003-0041355 F - Subsections 110.(19) and 85(1)

CCRA confirmed that a rental property could now be transferred on a s. 85(1) rollover basis to a corporation for agreed amounts corresponding, in...

4 June 2002 External T.I. 2002-0141435 F - Disposition of Shares

The exchange of voting common shares of Zco for voting preferred shares and non-voting common shares of Zco, with such voting common shares being...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | exchange of voting common for voting pref and non-voting common is a disposition | 50 |

9 November 2001 External T.I. 2001-0101685 F - APPLICATION DE 16.1 ET DE 85(1)

A taxpayer may not elect pursuant to s. 85(1) in respect of a property which was the subject of an election pursuant to s. 16.1(1) given that, for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 16.1 - Subsection 16.1(1) - Paragraph 16.1(1)(f) | s. 16.1(1)(f) does not accommodate an s. 85(1) disposition to a corporation | 49 |

19 September 2001 External T.I. 2001-0092085 - Transfer of Obligation under Short Position

The assumption of a short sale obligation of an individual by a corporation controlled by him would result in realization of the accrued gain or...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Computation of Profit | assumption of short sale obligation triggered gain | 33 |

5 July 2001 External T.I. 2001-0089105 F - ECHANGE D"OPTIONS - COUT INDIQUE

CCRA indicated that an RRSP can make a s. 85(1) election like other taxpayers, in which case the cost amount of the shares received by it could be...

7 June 2001 External T.I. 2001-0086165 F - REGLES DE ROULEMENT ET REER

CCRA confirmed that the tax treatment of a transaction subject to s. 85, 85.1, 86 or 87 will not differ where the shareholder is an RRSP (or RRIF).

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(4) | s. 87(4) applies to RRSPs | 47 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Taxpayer | RRSP is a taxpayer | 89 |

3 November 2000 Internal T.I. 2000-0049127 F - CONJOINT DE FAIT DECEDE-CHOIX

The Directorate indicated that an election could be made by a deceased individual along with another (still-alive) individual to be retroactively...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Common-Law Partner | an individual’s common–law partner election could be made by his executor | 84 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Person | a person can make an election through his executor | 67 |

28 June 2000 External T.I. 2000-0028665 F - QUOTAS DÉTENUS DEPUIS MOINS DE DEUX ANS

CCRA indicated that a taxpayer can structure a milk quota rollover under s. 85(1) so as to first dispose of the quota that was not eligible for...

12 May 2000 External T.I. 1999-0008685 F - QUOTA DE LAIT

The Agency indicated that where only a portion of a milk quota transferred by a general partnership to a corporation constituted qualified farm...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110.6 - Subsection 110.6(2) | CGD could be claimed on portion of milk quota eligible as qualified farm property, with s. 85(2) election made to avoid other gain | 147 |

17 March 1997 Internal T.I. 9631007 - INTERACTION OF 85(1) & 110.6(19)

The benefit of making an election under s. 110.6(19) in respect of an eligible capital property or a depreciable property effectively will be lost...

24 May 1995 External T.I. 9420675 - WYOMING LLCS

An interest in a Wyoming LLC receivable by a taxpayer as consideration for the disposition of shares of a foreign affiliate to the LLC would...

Income Tax Technical News, Release No. 3, 30 January, 1995 under "Section 85 (Dale Case)"

While awaiting the decision of the Federal Court of Appeal in the Dale case, RC intends to maintain its current practice of accepting election...

1994 A.P.F.F. Round Table, Q. 42

While awaiting the results of the appeal of the Dale case, RC will allow an election under s. 85(1) where the transferee is required under the...

3 December 1993 External T.I. 9200995 F - Transfer of Farm Inventory to a Corporation

Since the entitlement of a farmer under a gross revenue insurance program constitutes an account receivable to him that relates to the farming...

17 September 1992 T.I. (Tax Window, No. 24, p. 4, ¶2195)

A taxpayer cannot elect under both ss.85(1) and 22 with respect to accounts receivable.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 22 - Subsection 22(1) | 15 |

92 C.R. - Q.20

A joint election can be filed under s. 85(1) with respect to the changing of common shares of a corporation into preferred shares by the filing of...

26 March 1992 External T.I. 5-913338

Where a holding company assumes all of the debt associated with a property acquired by it from its subsidiary, interest on that debt will be...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | 76 |

24 February 1992 Memorandum (Tax Window, No. 13, p. 17, ¶1617)

The minimum permissible agreed amount in respect of the transfer of a partnership interest is nil.

91 C.R. - Q.20

If a taxpayer transfers debt or shares of a taxable Canadian corporation to that corporation in consideration for treasury shares, and those...

10 July 1991 Decision Summary (Tax Window, No. 5, pp. 4-5, ¶1345)

Where on an s. 85(1) roll of real estate with excess mortgage debt, the transferor gives the transferee a promissory note in the amount of the...

14 June 1991 T.I. (Tax Window, No. 4, p. 24, ¶1308)

Share purchase warrants issued by the transferee corporation do not constitute a right to receive shares.

October 1989 Revenue Canada Round Table - Q.11 (Jan. 90 Access Letter, ¶1075)

Where a taxpayer receives an undivided part of a block of flow-through shares following the liquidation of a limited partnership under s. 98(3),...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 50 | |

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) | 35 |

86 C.R. - Q.32

A deferred tax liability does not constitute non-share consideration.

85 CR - Q.52

S.85(1)(e.2) may apply notwithstanding that the taxpayer has obtained an independent valuation. However, a price-adjustment clause is usually...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | 9 |

84 C.R. - Q.47

Where a mortgage to be assumed exceeds the ACB of the property, RC will accept an allocation of the excess to other transferred assets, or as the...

84 C.R. - Q.78

In situations where the tax consequences of an election were unintended and extremely harsh, RC is prepared to provide taxpayers with...

12 December 1980 TI RCT 85-013

Construction holdbacks would be considered to be eligible property. The cost amount of the right would be calculated by eliminating the profit...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1.1) | 51 |

80 CR - Q.14

Adjustments to the agreed amount will be made to reflect changes in V-Day value only.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | 38 |

IT-188R Archived "Sale of Accounts Receivable" 22 May 1984

"The use of the 'rollover' provisions of section 85 precludes the use of the section 22 election ... ."

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 22 - Subsection 22(1) | 116 | |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) | 28 | |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Account Receivable | 226 |

IT-243R4 "Dividend Refund to Private Corporations"

IT-291R3 "Transfer of Property to a Corporation under Subsection 85(1)"

Shares need not be immediately issuable

35. One of the requirements that must be met for section 85 to apply to a transfer of property to a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) - Paragraph 85(1)(b) | allocation of assumed debt amongst transferred properties | 58 |

IT-457R "Election by Professionals to Exclude Work in Progress from Income" under "Meaning of 'Work in Progress'"

IT-489R: "Non-Arm's Length Sale of Shares to a Corporation"

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) - Paragraph 85(1)(e.2) | 0 |

Articles

Michael J. Welters, "Limited Partner's Interest in Partnership Property", Canadian Tax Highlights, Vol. 21,No. 7, July 2013, p. 3 at 4

"…most authorities have concluded that limited partners are the owners of partnership properties." [then discussing Donroy Ltd. (196 F. Supp. 54...

Dunn, Nielsen, "Exchanges of Property for Shares: section 85-Part 2", 1995 Canadian Tax Journal, Vol. 43, No. 2, p. 496.

David W. Smith, "Corporate Restructuring Issues: Public Corporations", 1990 Corporate Management Tax Conference Report, pp. 6:10-6:11

Discussion of relative merits of ss.85.1 and 85(1) elections.

Carsley, "Loan Receivables Denominated in a Foreign Currency", Canadian urrent Tax, July 1988, p. 31

RC has taken the position that for the purpose of determining the cost amount of a foreign currency receivable the amount of the receivable should...

Wise, "The Valuation of Preferred Shares Issued on a Section 85 Rollover", 1984 Canadian Tax Journal, March-April, p. 239.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Shares | 0 |

Sylph, Percival, "Accounting Options for Section 85 Rollovers", CA Magazine, July 1981, p. 42

"The fair market value of the asset to the transferee should recognize the future tax effects of the differences between the tax bases and the...

Forms

T2057 "Election on Disposition of Property by a Taxpayer to a Taxable Canadian Corporation" 23 January 2009

File...at the tax centre serving the...

Paragraph 85(1)(a)

Administrative Policy

7 February 2018 External T.I. 2016-0637221E5 - Rollover of Mineral Rights

The Taxpayer, which is not in the business of exploration and development of mineral properties, wishes to transfer the Property (which may...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 66.2 - Subsection 66.2(5) - Canadian development expense | cost of property added to CCDE or COGPE | 234 |

2016 Ruling 2016-0635101R3 - 55(3)(a) Spin-Off to Use Parent Losses

Subco has entered into an agreement for the sale to an arm’s length purchaser of a property containing parcels of land with accrued capital...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 13 - Subsection 13(21.1) - Paragraph 13(21.1)(a) | where land transferred under s. 85(1) along with terminal loss building, elect high with a view to s. 13(21.1)(a) applying to reduce the land proceeds to ACB | 189 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) | 55(3)(a) spin-off of property already subject to sale agreement to parent before closing date | 592 |

| Tax Topics - Income Tax Act - Section 86 - Subsection 86(1) | s. 86(1) applied where “dirty” s. 85 exchange mechanic used, but no s. 85 election made | 93 |

11 May 2011 External T.I. 2011-0394231E5 F - Subsections 14(1.01) and 85(1) - Quotas

Can the disposition of milk quotas occurring as part of the drop down of a dairy-farming business by a partnership under s. 85(2) be structured so...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110.6 - Subsection 110.6(1.3) | milk quotas could be segregated between those eligible for capital gains deduction and those transferred on rollover basis | 183 |

27 August 1999 External T.I. 9830385 F - INTERACTION OF SECTION OF THE ACTS 11O.6(19)

The Directorate indicated that the benefit of an s. 110.6(19) election in respect of depreciable property, whose cost amount was less than its...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110.6 - Subsection 110.6(19) | benefit of s. 110.6(19) election is lost on a depreciable property’s transfer on an s. 70(6) or 85(1) rollover basis | 157 |

Paragraph 85(1)(b)

Administrative Policy

2024 Ruling 2023-0998291R3 F - Multi-wings split-up net asset butterfly 55(3)(b)

In order to accomplish a multi-wing split-up net asset butterfly of a private corporation (DC) owned by a divorced couple, they will transfer...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | split-up butterfly between a divorced couple where excess debt is allocated to land rather than building to produce capital gains treatment | 453 |

10 March 2004 External T.I. 2003-0047905 - Debt Assumption by Partnership

Three individuals, who are co-owners and actively involved in managing several commercial rental properties and whose tax basis (ACB of land and...

IT-291R3 "Transfer of Property to a Corporation under Subsection 85(1)"

17 … Paragraph 85(1)(b), however, will not apply where the fair market value of the non-share consideration given (including the assumption of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) | 259 |

2003 Ruling 2003-0054013 - Assumption of Debt

A subsidiary is to become a co-obligor of a parent's debts on a s. 85(1) transfer of property from the parent, but the parent will fully indemnify...

12 November 2003 External T.I. 2002-0121835 - 85(1) - Holdbacks Payable

Where a contractor transferred its construction contract to a corporate purchaser, the amount previously withheld by the contractor as a holdback...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) | 38 |

10 April 2003 External T.I. 2002-0170485 - Assumption of Debt

Where a corporation owes $100 to the taxpayer, and the taxpayer transfers a property with an FMV of $300, cost to the taxpayer of $200, and...

6 December 2000 External T.I. 2000-0056485 - assumption of excess debt on sec 85 transfer

Where shares received on an s. 85(1) roll are immediately redeemed by issuing a promissory note, CRA will not consider s. 85(1)(b) to apply, i.e.,...

27 September 2000 External T.I. 2000-0039335 - Change in CCRA's position re 85(1)(b)

The Agency has now reversed its position on the assumption of excess debt in an s. 85(1) rollover transaction (for example, the purchaser assuming...

2000 Ruling 1999-001074

S.85(1)(b) would not apply where the portion of liabilities assumed by the transferee that were in excess of the cost amount of the transferred...

1996 Corporate Management Tax Conference Round Table, Q. 7

Until it completes its review, RC will permit excess debt to be assumed by the transferee corporation in consideration for the issuance by it of a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | assumption of excess debt | 96 |

1992 A.P.F.F. Annual Conference, Q. 21 (January - February 1993 Access Letter, p. 58)

RC will consider roll-over treatment under s. 85(1)(b) to be available on the transfer of a property subject to mortgage indebtedness in excess of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | 53 |

26 March 1992 T.I. (Tax Window, No. 18, p. 2, ¶1831)

Where, in connection with the transfer by Opco to its parent, Holdco, of property subject to debt in excess of the property's ACB, Holdco first...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | 93 |

Articles

Kim Maguire, Jeffrey Shafer, "Trends in Buy/Sell Transactions", draft 2021 Conference Report

Use of rights to acquire shares of purchaser (pp. 5-6)

- Where the vendor has the contingent right to receive additional shares of the purchaser,...

Commentary [in progress]

Paragraph 85(1)(c)

Administrative Policy

13 August 2013 External T.I. 2012-0471401E5 F - FMV - partnership interest

Where an interest in a professional partnership that has made the s. 34 election has been transferred under s. 85(1) to a corporation, can the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Other | deferred tax liability re deferred (s. 34) partnership income recognition reduces partnership interest FMV | 236 |

| Tax Topics - Income Tax Act - Section 34 | FMV of partnership interest reduced re deferred income taxes on WIP subject to s. 34 election | 41 |

Paragraph 85(1)(c.1)

Administrative Policy

7 July 2005 External T.I. 2005-0122191E5 F - Erroneous Elections in Statute-barred Years

An individual (X) transferred all the shares of Bco to Aco in exchange for a note and common shares, electing under s. 85(1) at an amount thought...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(7) | no need to amend the s. 85(1) election where automatic s. 85(1)(c.1) adjustment | 55 |

| Tax Topics - Income Tax Act - Section 110.6 - Subsection 110.6(19) | no need to amend the s. 85(1) election where the agreed amount was less than the s. 85(1)(c.1) floor | 93 |

26 February 2001 External T.I. 2000-0017635 F - choix modifié et PBR rajusté

An individual transferred a partnership interest to a corporation at an agreed amount equal to the low ACB of the interest resulting from...

Paragraph 85(1)(c.2)

Administrative Policy

IT-427R "Livestock of Farmers"

IT-433 "Farming or Fishing - Use of Cash Method"

Paragraph 85(1)(d)

Administrative Policy

2015 Ruling 2014-0558831R3 - No-type of property spin-off butterfly

A butterfly spin-off by a public corporation (DC) of two business divisions (which it prepackaged in a Newco subsidiary) is preceded by a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | prior drop-down of assets to Newco/split of DC manager's business/CEC proration/replacement option issuance as boot | 1177 |

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(1.4) | replacement stock options issued by Spinco treated as boot | 112 |

| Tax Topics - Income Tax Act - Section 86 - Subsection 86(1) | new common shares with same attributes as old subject to rights of new special shares/ pro rata PUC | 164 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | splitting of fee for management of 2 divisions not a disposition of contract | 145 |

Paragraph 85(1)(d.11)

Administrative Policy

15 November 2006 External T.I. 2004-0083461E5 F - Feb. 2004 Proposals - Paragraph 85(1)(d.11)

CRA noted that the question as to whether the application rule regarding s. 85(1)(d.11) (that it applied in respect of dispositions occurring...

Paragraph 85(1)(e)

Administrative Policy

27 October 2017 External T.I. 2017-0688971E5 F - New Class 14.1

Goodwill of a business was purchased in 2016 for $100,000, resulting in a cumulative eligible capital balance on December 31, 2016 of $75,000...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 13 - Subsection 13(38) - Paragraph 13(38)(c) | a s. 85 roll of purchased goodwill at an agreed amount of unamortized cost can trigger recapture | 250 |

| Tax Topics - Income Tax Act - Section 13 - Subsection 13(39) | non-application on s. 85 roll can result in recapture -but disposition bump available to NAL transferee | 117 |

2017 Ruling 2016-0675881R3 - Paragraph 55(3)(a) Internal Reorganization

CRA also ruled in connection with a s. 55(3)(a) division of the rental real estate and realty assets of Canco between Newco 1 and Newco 2 that the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) | division of rental real estate company between holdcos for 2 children but with parents' holdco retaining voting control | 579 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(4) | s. 55(3)(a) split-up between Newcos for two siblings which were related due to multiple-voting shares held by the father’s and mother’s Holdco | 170 |

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(1) - Paragraph 186(1)(b) | where circular RDTOH calculation arises on spin-off transaction, it is for the TSOs to sort out which corporations should bear Part IV tax | 249 |

27 November 2014 External T.I. 2013-0503861E5 F - Application du paragraphe 248(16)

Where a taxpayer claims an input tax credit under ETA s. 193 on transferring a depreciable building on a rollover basis under ITA s. 85(1), can it...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(16) | ETA s. 193 ITC claim does not reduce UCC under s. 85(1)(e)(i) | 82 |

2006 Ruling 2006-0181061R3 - Butterfly Distribution - XXXXXXXXXX

in a single-wing butterfly in which assets are distributed to a holding company for one of the two brothers which control the corporation, the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | 73 |

25 October 2002 External T.I. 2002-0137705 F - Butterfly

CCRA agreed that it would generally treat the reference in s. 85(1)(e) to "the undepreciated capital cost to the taxpayer of all property of that...

October 1989 Revenue Canada Round Table - Q.6 (Jan. 90 Access Letter, ¶1075)

On the division pursuant to a butterfly reorganization of two depreciable assets of the same class, RC will accept the apportionment of the...

Paragraph 85(1)(e.2)

Administrative Policy

S4-F3-C1 - Price Adjustment Clauses

CRA will consider a price adjustment clause to represent pricing at fair market value if:

- the agreement reflects a bona fide intention of the...

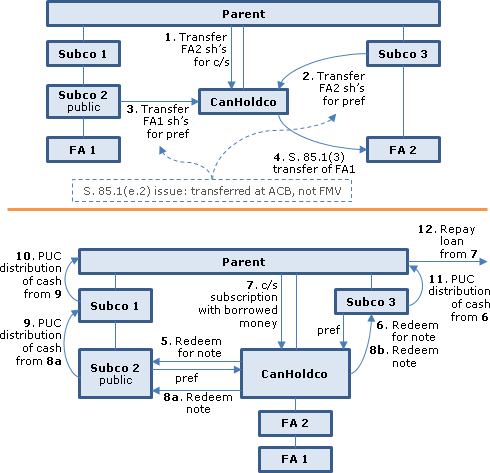

2014 Ruling 2011-0415811R3 - Internal reorganization

{kind=link}

Current structure

Parent, a public corporation which previously had been spun-off by Subco 2 (also a public corporation, but with Subco 1 holding...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | cash distribution to parent of indirect proceeds of internal reorg | 506 |

17 May 2012 Internal T.I. 2012-0437001I7 F - Price Adjustment Clause

A price adjustment clause (PAC) is engaged to increase the fair market value of shares issued to the taxpayer on a s. 85(1) drop-down transaction....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | per Gurberg, a PAC has retroactive effect | 169 |

9 June 2003 External T.I. 2003-0004835 - WHETHER A PARTNERSHIP IS A PERSON

In a s. 97(2) transfer, the partnership is not considered a person related to the taxpayer solely because the taxpayer is a majority interest...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 97 - Subsection 97(2) | 60 |

15 November 2002 Internal T.I. 2002-0162427 F - Price Adjustment Clause & 85(7.1)

Madame exchanged her Class A shares of the corporation for Class D shares having a redemption amount which CCRA subsequently determined was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | large FMV discrepancy suggested lack of bona fide valuation so that price adjustment clause need not be applied/ if applied, s. 85(1) election must be amended | 212 |

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(7) | amended s. 85(1) election must be filed if price-adjustment clause applied | 100 |

1996 Tax Executives Round Table, Q. IV (No. 9639160)

"Generally, where the facts show that the parties to the transaction intended to transfer the property at its fair market value and their efforts...

15 November 1990 T.I. (Tax Window, Prelim. No. 2, p. 14, ¶1078)

A taxpayer will not be considered to have conferred a benefit pursuant to s. 85(1)(e.2) where the redemption and retraction amount of preferred...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Shares | 60 |

90 C.R. - Q34

It is not the intention of RC to apply s. 85(1)(e.2) to a "classic" estate freeze provided that the transferor receives retractable preference...

89 C.R. - Q.23

"Where the fair market value of the business assets exceeds the fair market value of the consideration used to pay for the business assets in a...

October 1989 Revenue Canada Round Table - Q.10 (Jan. 90 Access Letter, ¶1075)

s. 85(1)(e.2) will be applicable where the price is less than the fair market value of the property, regardless whether the consideration consists...

88 C.R. - "Demise of the Wingless Butterfly"

s. 85(1)(e.2) will apply where property is transferred from a corporation to its wholly-owned subsidiary if the fair market value of the...

81 C.R. - Q.6

S.85(1)(e.2) will not be applied to transactions which comply with s. 55(3)(b).

IT-489R: "Non-Arm's Length Sale of Shares to a Corporation"

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) | 0 |

Articles

Tung, "Application of the Gifting Provisions of Section 85", Tax Profile, October 1990, p. 42

Discussion of the overstatement of RC in IC 76-19R2, para. 22.

Paragraph 85(1)(e.4)

Administrative Policy

10 September 2012 External T.I. 2012-0446921E5 F - Avantage pour automobile

In 2012, Corporation A disposed of an automobile that had been acquired by it in 2009 at a cost of $40,000 and used by a joint employee of it and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(2) | transfer to related corp stepped down cost for standby charge purposes to FMV | 135 |

IT-521R: "Motor Vehicle Expenses Claimed by Self-Employed Individuals"

IT-522R: "Vehicle, Travel and Sales Expenses of Employees"

Paragraph 85(1)(f)

Administrative Policy

21 January 2002 External T.I. 2001-0078735 F - Droit de recevoir une somme

The shareholders of a CCPC (Xco) agreed to sell their Xco shares to a public corporation (Yco) in consideration for an upfront cash payment, and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Proceeds of Disposition | FMV of contingent right to deferred cash sales proceeds was included in proceeds, with subsequent gain or loss when the contingency was resolved | 224 |

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(g) | s. 12(1)(g) inapplicable to contingent right to receive deferred cash sales proceeds to the extent the share consideration declined in value | 220 |

Paragraph 85(1)(h)

Finance

5 October 2018 APFF Financial Strategies and Instruments Roundtable, Finance Response to Q.6

An individual transfers a directly-held pharmacy business to a wholly-owned Newco in 2017. On January 1, 2017, the cumulative eligible capital...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 13 - Subsection 13(38) | Finance is reviewing the deemed cost of shares received on s. 85 drop-down of transitioned Class 14.1 property | 221 |

Subsection 85(1.1)

See Also

Commissioner of State Revenue v Rojoda Pty Ltd , [2020] HCA 7

An Australian-resident husband and wife (Anthony and Maria) were the equal partners of a partnership (the “AMS Partnership”) and were...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 96 | partnership property is held in trust for the partners | 155 |

Boland v. Boland (1980), 14 Alta. L.R. (2d) 154 (Alta. Q.B.)

Cormack J. found that s. 24 of the Partnership Act (Alberta) (which deemed partnership property consisting of land to be personal property and not...

Seven Mile Dam Contractors v. The Queen in Right of British Columbia (1980), 116 DLR (3d) 398, 1980 CanLII 451 (BCCA)

On a sale of equipment by one partnership ("Seven Mile") to another ("Kootenay Power") in which the two partners of Seven Mile had a 40% and 10%...

Lane v. The Queen, 78 DTC 6535, [1978] CTC 795 (FCTD), briefly aff'd 86 DTC 6568, [1986] 2 CTC (FCA)

Collier J found that the taxpayer's disposition of his interest in a "syndicate" was the disposition of an interest in a partnership so that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 100 | disposition of partnership interest not disposition of underlying property | 61 |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Partnership Interests | partnership interest distinct from partnership property | 107 |

| Tax Topics - Income Tax Act - Section 96 | 20 |

Lavin v. Geffen (1920), 61 SCR 356, aff'g (1920), 51 DLR 203 (Alta. C.A.)

An oral agreement of one partner to purchase the other partner's interest was enforceable, notwithstanding that the assets of the partnership...

Winsby v. Tait, [1941] 2 DLR 81 (SCC), rev'd [1943] 1 DLR 81 (PC)

A provision of the Mineral Act (B.C.), which provided that "no person ... shall be recognized as having any right or interest in or to any mining...

In re Fuller's Contract, [1933] 1 Ch. 652

In commenting on a submission that Re Bourne should be regarded as "a decision that a partner has no beneficial interest in the partnership real...

Porter v. Armstrong, [1926] 2 DLR 340, [1926] S.C.R. 328

Two individuals did not agree to purchase land as partnership property given that in their mind there was no "binding agreement which would...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 96 | 126 |

Boyd v. Attorney General for BC (1917), 54 SCR 532

An Ontario domiciled person had died owning a partnership interest in a partnership that carried on business in Ontario, did not carry on business...

Driver v. Broad, [1893] 1 Q.B. 744 (C.A.)

A debenture containing a floating charge on leasehold property of a company, consisting of a factory and warehouse, constituted an interest in...

Administrative Policy

3 November 2023 APFF Financial Strategies and Instruments Roundtable Q. 6, 2023-0994241C6 F - Consequences of Transfer of DSUs to a corporation

In finding that the rights of an employee under a deferred share unit plan described in Reg. 6801(d) (a "DSU Plan") were not eligible property...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Salary Deferral Arrangement | transfer of DSU to corporation would cause it to cease to qualify, perhaps retroactively | 240 |

| Tax Topics - Income Tax Act - Section 54 - Capital Property | deferred share units were not capital property | 59 |

29 January 2015 Internal T.I. 2014-0544651I7 - Section 85 transfer of Swap Contracts

The taxpayer entered into cross-currency (U.S.$/Cdn$) Swap Contracts with a counterparty respecting the issuance of U.S.-dollar notes issued by it...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Inventory | swap contract treated as inventory | 55 |

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) | swap contract recorded on securities rather than inventory line of T2057 | 251 |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Foreign Exchange | swap contract treated as inventory | 55 |

6 October 2014 External T.I. 2014-0543751E5 F - Rollover of a part of an interest in a partnership

X, who wished to dispose of half of interest (which is capital property) in a partnership to a taxable Canadian corporation in consideration for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Property | partnership interest is one property - but fraction thereof also is property if transferred | 98 |

16 June 2014 STEP Roundtable, 2014-0526561C6 - Capital interest as eligible property for s 85

Can a capital interest in a personal trust qualify as eligible property? After noting that eligible property in s. 85(1.1) includes most capital...

5 March 2014 Internal T.I. 2013-0500891I7 - Hedging

Parent hedged a U.S.-dollar borrowing by entering into foreign currency forward contracts, which were found to have been acquired on capital...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Foreign Exchange | s. 85(1) roll of FX forward to sub | 195 |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Futures/Forwards/Hedges | s. 85(1) roll of FX forward to sub | 195 |

1 May 2013 External T.I. 2012-0459541E5 - Capital interest in a trust

"[T]he capital interest in a personal trust will qualify as eligible property pursuant to subsection 85(1.1) and for the purposes of subsection...

14 April 2009 External T.I. 2007-0238221E5 F - Rights of musician-Transfer

As part of a general response respecting the transfer of rights by a musician to a corporation, CRA stated:

[T]he transfer of a right to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(4) | s. 56(4) generally will apply where royalty is transferred without assignment of copyright, with exception of SOCAN royalty | 165 |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | s. 56(2) not applicable where copyright or royalty interests transferred at FMV | 75 |

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Specified Investment Business | royalty income generated from an active business is itself active business income | 122 |

2004 Ruling 2002-0149781R3 F - Transfer of copyrights

Proposed transaction

Mr. A, a composer, will transfer to a newly-incorporated wholly-owned corporation (“Opco1”) his property used in his...

1998 A.P.F.F. Round Table, Q. 14, 9824750

Know-how is not property. Accordingly, although the know-how relating to a business may be part of the goodwill that is transferred on an...

27 October 1998 External T.I. 9824750 F - KNOW-HOW

In finding that know-how not having IP statutory protection is not “property” and, thus, not “eligible property” – except that it can be...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Property | know-how not having IP statutory protection is not “property” – but can be transferred as part of goodwill | 257 |

23 September 1996 External T.I. 5-962304

The rights of a person to obtain a patent in respect of know-how represent property and, accordingly, can qualify as an eligible property under s....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Property | 27 |

22 June 1995 External T.I. 9224155 F - R&D Pool, Rollover

A pool of unclaimed R&D expenditures is not eligible property, although any capital property the cost of which is included in the pool would be an...

28 March 1995 Internal T.I. 9502507 - RIGHT TO ROYALTY ELIGIBLE PROPERTY

Although "a right to receive income, in or by itself, would generally not be considered capital property", here the taxpayer also owned the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Property | 66 |

94 C.P.T.J. - Q.20

"In order for a right to a royalty income in respect of 'know-how' to qualify as an eligible property, it must be either a capital property or an...

1 September 1994 External T.I. 9413775 - ELIGIBLE PROPERTY & CUM DIVIDENDS

Before indicating that a preferred share with accrued cumulative dividends could be transferred by an individual to a holding corporation under s....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Property | right to accrued dividends is not separate property from the shares | 93 |

3 February 1994 External T.I. 5-923647

Holdbacks and unapproved billings of a contractor are eligible property in respect of which the elected amount can be $1.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(4) | 44 |

9 September 1991 Memorandum (Tax Window, No. 10, p. 16, ¶1476)

Holdbacks receivable of building contractors cannot be transferred on a rollover basis under s. 85(1).

15 August 1991 T.I. (Tax Window, No. 7, p. 19, ¶1393)

Where an individual carrying on a profession has made an election under s. 34 to exclude work-in-progress from income, the work-in-progress is...

8 January 1991 External T.I. 5-902839

It is not possible for a contractor following the completion method to transfer a contract in progress to a subsidiary under s. 85(1) without...

2 January 1991 T.I. (Tax Window, Prelim. No. 3, p. 11, ¶1083)

A butterfly reorganization involving the distribution of land inventory achieved on a rollover basis under ss.97(2) and 90(3) through the use of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 48 |

3 December 1990 T.I. (Tax Window, Prelim. No. 2, p. 11, ¶1062)

A receivable that is capital property is an eligible property which may be transferred to the debtor corporation for treasury shares.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 34 | |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 34 |

90 C.R. - Q.35

Because an interest in a partnership is not considered to be an interest in its underlying assets, a capital interest in a real estate partnership...

30 April 1990 T.I. (September 1990 Access Letter, ¶1423)

RC has not addressed the issue of whether deferred leasing costs constitute property eligible for transfer.

89 C.M.TC - Q.10

a partnership interest in a real estate partnership owned by a non-resident generally is eligible property. "However, where the formation of the...

88 C.R. - Q.24

Seismic data the cost of which is in fact CEE rather than inventory cannot be rolled under s. 85(1).

86 C.R. - Q.50

Since a partnership interest is not considered to be an interest in the underlying assets, an interest in a partnership with real estate inventory...

86 C.R. - Q.54

An interest in a partnership, the underlying property of which consists of Canadian resource property, is not a Canadian resource property.

84 C.R. - Q.48

Although RC accepts that a capital property that is an interest in a partnership, the underlying property of which is real estate inventory, can...

12 December 1980 TI RCT 85-013

Before going to find that the contingent right to receive construction holdbacks was property that could be transferred on a rollover basis, RCT...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) | 29 |

Articles

Donn, "Exchanges of Property for Shares: Section 85 - Part 1", 1995 Canadian Tax Journal, Vol. 43, No. 1, p. 203.

Vesely, "Takeover Bids: Selected Tax, Corporate and Securities Law Considerations", 1991 Conference Report, c. 11.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(1) | 0 |

Wilson, "Shares in a Corporation that Primarily Holds Land Inventory May Not Qualify for a Rollover", Corporate Structures and Groups, Vol 1, No. 2, 1992, p. 27

A taxpayer's shares in a corporation that primarily holds land inventory may be property that is neither capital property nor inventory.

Paragraph 85(1.1)(a)

Administrative Policy

8 July 2020 CALU Roundtable Q. 4, 2020-0842171C6 - Segregated Funds and 85(1)

Ms. A invests $100,000 into a segregated fund policy providing that upon its maturity in 15 years the amount payable it under to her as the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 138.1 - Subsection 138.1(1) - Paragraph 138.1(1)(e) - Subparagraph 138.1(1)(e)(i) | bifurcation of segregated fund policy | 244 |

3 April 2020 External T.I. 2020-0836991E5 - Eligible property and stock options

Stock options of an individual that were not employee stock options and that were held as capital property were eligible property.

16 February 2004 External T.I. 2003-0054091E5 F - Rollover for Contractors

Mr. X who, in computing income from his construction business, used the percentage-of-completion method and excluded contract holdbacks each year,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(4) | s. 56(4) not applied where construction lien holdbacks are transferred on s. 85(1) rollover basis to transferee, which includes them when they become receivable | 123 |

Paragraph 85(1.1)(b)

Administrative Policy

29 April 2008 External T.I. 2006-0215891E5 F - Partnership Interest & Departure Tax

After emigrating from Canada, an individual transferred his interest in a real estate partnership on a s. 85(1) rollover basis to a corporation of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 220 - Subsection 220(4.5) - Paragraph 220(4.5)(a) - Subparagraph 220(4.5)(a)(i) | s. 85(1) rollover of the property triggered the s. 220(4.5) deferred tax | 98 |

Subsection 85(1.11) - Exception

Administrative Policy

29 November 2001 External T.I. 2001-0110985 - TEI, Question 21

In response to a question noting the untenable breadth of s. 85(1.11) the Agency indicated that it "does not have the experience in administering...

Subsection 85(1.3)

Administrative Policy

12 May 2014 External T.I. 2013-0503531E5 F - Discretionary Dividends Shares

{kind=link}

In the context of a general discussion of s. 85(1)(e.2) and after paraphrasing s. 85(1.3), CRA stated (TaxInterpretations translation):

For...

22 January 1992 T.I. (Tax Window, No. 15, p. 3, ¶1708)

Where two individuals each transfer property to a wholly-owned corporation immediately following which the two corporations are amalgamated, s....

Subsection 85(2) - Transfer of property to corporation from partnership

Cases

Gillen v. Canada, 2019 FCA 62

Webb JA affirmed a finding of D’Arcy J that the beneficial ownership of some applications to the Saskatchewan government for potash exploitation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110.6 - Subsection 110.6(14) - Paragraph 110.6(14)(f) - Subparagraph 110.6(14)(f)(ii) | property was not used in a business for s. 110.6(14)(f)(ii) purposes when it was transferred immediately following its acquisition | 367 |

Administrative Policy

2004 Ruling 2004-0084311R3 - Incorporating a Partnership

On the transfer of the assets of a partnership to a corporation ("Newco") in consideration for shares and a promissory note, for reasons of legal...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Personal Services Business | 99 | |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 93 |

IT-378R "Winding-up of a Partnership" 1 January 1995

2. The consideration received by the partnership for one or more properties disposed of under subsection 85(2) must include at least one share of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(3) | 259 |

IT-457R "Election by Professionals to Exclude Work in Progress from Income" under "Meaning of 'Work in Progress'"

Articles

Bernstein, "Partnership Versus Joint Company", Tax Profile, March 13, 1990

RC will consider the requirements of s. 85(2) to be met where the shares are issued in the names of the partners instead of the name of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 97 - Subsection 97(2) | 25 |

Forms

Form T2058 "Election on Disposition of Property by a Partnership to a Taxable Canadian Corporation"

TP-529-V (Quebec) "Transfer of Property by a...

Subsection 85(2.1) - Computing paid-up capital

Administrative Policy

17 June 2013 Internal T.I. 2013-0475621I7 - PUC adjustment

A non-resident corporation and another taxpayer transferred forward purchase agreements (FPAs) and promissory notes to a Canadian corporation in...

7 October 2011 Roundtable, 2011-0412121C6 F - Interaction between S. 84.1 and S. 85(2.1)

Mr. A transferred his shares of Opco with an ACB and PUC of $100 and $100,000, respectively, to Holdco on a s. 85(1) rollover basis in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) | s. 84.1 can "apply" and thereby prevail over s. 85(2.1) even where there is no s. 84.1 grind | 78 |

7 July 1994 External T.I. 9413315 - INTERNAL CRYSTALLIZATION

Two unrelated persons each owning 50% of the common shares of Opco having a fair market value of $500,000 and an adjusted cost base and paid-up...

27 March 1994 Internal T.I. 9333227 - SHAREHOLDER BENEFIT

Where a taxpayer has transferred property to a corporation pursuant to s. 85(1) and has received consideration in excess of the fair market value...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | 81 |

1992 A.P.F.F. Annual Conference, Q. 1 (January - February 1993 Access Letter, p. 49)

Where an individual exchanges all the common shares of Opco, having an ACB of $100,000, a paid-up capital of $500,000 and a fair market value of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(1) | 50 |

Articles

Ewens, "Forced Share Conversions", 1993 Canadian Tax Journal, No. 6, p. 1407.

Subsection 85(3) - Where partnership wound up

Administrative Policy

14 January 2015 External T.I. 2014-0559731E5 - 85(3) rollover

Is the 60-day requirement in s. 85(3)(b) satisfied if beneficial ownership of land owned by the partnership is transferred within the 60-day...

8 May 2014 External T.I. 2014-0522771E5 - Whether a partnership has ceased to exist

Partner A sold his 50% partnership interest in a Quebec general partnership (the "Partnership") operating a grocery business in the province of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 98 - Subsection 98(1) | continuation of partnership with one partner | 162 |

2012 Ruling 2011-0392041R3 - Incorporation of a Professional Partnership

{kind=link}

Background

. As described below, a professional partnership (the "Partnership") with resident Canadian partners will effectively be converted...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Specified partnership income | former partners providing services through separate corporations to a Newco replacement of their professional partnership | 370 |

20 December 2013 External T.I. 2013-0501831E5 - Partnership - 85(2), (3) and 100(2)

A general partnership will transfer its goodwill, having a nil cost amount, to Corp under s. 85(2) in return for consideration that includes...

30 April 2003 External T.I. 2002-0172485 F - LIQUIDATION SOCIETE DE PERSONNES

A partnership disposed of all of its capital property to the corporation pursuant to s. 85(1) in consideration for the assumption of debt and for...

6 July 1995 External T.I. 9512165 - PARTNERSHIP BUTTERFLY

"Subsection 85(3) requires that property of a partnership be transferred to only one corporation prior to its winding-up. For example, the...

IT-378R "Winding-up of a Partnership" 1 January 1995

3. Subsections 85(2) and (3) taken together provide a means whereby partnership property may be transferred to a corporation and the related...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(2) | 109 |

Paragraph 85(3)(f)

Administrative Policy

17 September 2018 External T.I. 2018-0751571E5 F - Adjusted cost base of property

CRA confirmed that where a flow-through LP transfers it flow-through shares under s. 85(2) to a mutual fund corporation for shares of the MFC, and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 66.3 - Subsection 66.3(3) | s. 66.3(3) does not apply to the cost of shares received on a ss. 85(2) and (3) wind-up of a flow-through share partnership | 263 |

Subsection 85(4)

See Also

Luise Zinkhofer and Bernard Zinkhofer v. Minister of National Revenue, 91 DTC 643, [1991] 1 CTC 2493 (TCC)

Sobier TCJ. accepted the taxpayers' submission that a corporation was not "controlled directly or indirectly in any manner whatever" by them in...

Administrative Policy

24 March 1995 External T.I. 9431545 - EXECUTOR'S YEAR, LOSS ON SALE OF SHARES

"Subsection 85(4) of the Act will not generally apply where all the shares of a corporation held by an estate are disposed of to the corporation...

28 July 1994 External T.I. 9416395 - DENIED LOSS ADDED TO ACB

With respect to whether ss.85(4)(a) and 53(1)(f.1) would apply to the transfer by a corporation and its subsidiary of their respective undivided...

26 January 1994 External T.I. 9336015 F - Immediately After Disposition Meaning

It was submitted that where a taxpayer transfers property to a corporation that is controlled by the taxpayer and shortly thereafter the taxpayer...

8 February 1993 T.I. (Tax Window, No. 28, p. 2, ¶2416)

The capital loss otherwise deemed to be received by the sole individual shareholder of a holding company on the redemption of preferred shares of...

12 January 1993 T.I. 922257 (November 1993 Access Letter, p. 495, ¶C38-178; (Tax Window, No. 28, p. 11, ¶2363)

A foreign exchange loss realized under s. 39(2) on the repayment of a U.S.-dollar loan owing by a non-resident subsidiary to a Canadian...

29 July 1992 Memorandum (Tax Window, No. 21, p. 1, ¶2038)

S.85(4) would not apply where all the shares of a corporation held by an estate are disposed of to a corporation which, immediately following the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | 62 |

20 July 1992 External T.I. 5-901453

If an estate transfers 40% of the shares of a corporation to the son of the deceased before the remaining 60% of the shares are redeemed in the...

16 April 1992 T.I. (Tax Window, No. 18, p. 12, ¶1861)

Where a parent corporation settles a note receivable from a wholly-owned subsidiary for less than its principal amount, s. 85(4) will apply to...

92 C.R. - Q.19

Where an estate owns all the shares of Opco and 90% of its shares are redeemed, s. 85(4) will deem the capital loss to be nil, with the result...

30 November 1991 Round Table (4M0462), Q. 10.2 - Application of Subsection: 85(4) to an Estate (C.T.O. September 1994)

Re application of s. 85(4) where preferred shares of an estate are redeemed and the common shares are transferred to the children of the deceased.

91 C.R. - Q.42

If all shares held by an estate are disposed of to the corporation but the legal representatives in a personal capacity continue to control the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 164 - Subsection 164(6) | 29 |

27 December 1990 Memorandum (Tax Window, Prelim. No. 2, p. 21, ¶1073)

S.85(4) does not apply to deny a capital loss realized by testamentary trust on the retraction of preferred shares held by it.

Subsection 85(5)

Administrative Policy

10 June 2003 External T.I. 2003-0017065 F - Disp. of Property owned on Dec 31, 71

Mr. X owned a rental property (the “immovable") which he had acquired in 1965 at a cost of $300,000 ($100,000 and $200,000 for the land and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Application Rules - Subsection 20(1) | 2 detailed examples of the application of ITAR 20(1) | 1256 |

Subsection 85(5.1) - Acquisition of certain tools — capital cost and deemed depreciation

Administrative Policy

11 June 1990 T.I. (November 1990 Access Letter, ¶1524)

Where a parent corporation sells depreciable property to a wholly-owned subsidiary under a sales agreement, the depreciable property is...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 79 | 79 | |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 79 | |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 79 |

Articles

Bernstein, "Restructuring Real Estate Syndications that are in Trouble", 1992 Conference Report, c.10

Discussion of transactions that potentially avoid s. 85(5.1) in order to realize a terminal loss.

Subsection 85(6) - Time for election

Administrative Policy

90 C.R. - Q36

The RC position that the "taxation year" referred to in s. 85(6), in the case of a transfer by a partner or proprietor of capital property...

Subsection 85(7) - Late filed election

See Also

Construction PCA Inc. v. Agence du revenu du Québec, 2019 QCCQ 8876

In 2010-2011, the individual taxpayer (“Cusson”) transferred various properties to his real estate corporation (“PCA”) with a view to the...

Administrative Policy

7 July 2005 External T.I. 2005-0122191E5 F - Erroneous Elections in Statute-barred Years

Regarding an individual who had elected at less than the ACB of the transferred shares, CRA stated that s. “85(1)(c.1) results in an automatic...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) - Paragraph 85(1)(c.1) | no need to amend the s. 85(1) election where the agreed amount was less than the s. 85(1)(c.1) floor | 93 |

| Tax Topics - Income Tax Act - Section 110.6 - Subsection 110.6(19) | no need to amend the s. 85(1) election where the agreed amount was less than the s. 85(1)(c.1) floor | 93 |

15 November 2002 Internal T.I. 2002-0162427 F - Price Adjustment Clause & 85(7.1)

Madame exchanged her Class A shares of the corporation for Class D shares having a redemption amount which CCRA subsequently determined was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) - Paragraph 85(1)(e.2) | significant FMV shortfall suggested that a benefit was desired to be conferred | 146 |

| Tax Topics - General Concepts - Effective Date | large FMV discrepancy suggested lack of bona fide valuation so that price adjustment clause need not be applied/ if applied, s. 85(1) election must be amended | 212 |

1994 A.P.F.F. Round Table, Q. 15

Except in very limited circumstances, RC will not allow a parent corporation to file a late election on behalf of a subsidiary that has been...

91 C.R. - Q.21

RC will no longer adjust the agreed amount where the taxpayer has made a reasonable but incorrect effort to determine the V-day value. RC now...

Subsection 85(7.1) - Special cases

Cases

Brent Carlson Family Trust v. Canada (National Revenue), 2021 FC 506

The applicants were family trusts that had implemented a detailed steps memo of the tax advisors (EY) in order to maximize the utilization by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 120.4 - Subsection 120.4(5) | s. 120.4 was engaged as a result of a capital gain being realized on a preliminary NAL transaction rather than subsequent arm's length sale | 382 |

S. Cunard & Company Limited v. Canada (Attorney General), 2012 DTC 5122 [at at 7192], 2012 FC 683

Scott J. found that the Barnabe Estate principle, which allowed elections to be made by the estate of a deceased person, did not apply to a...

Bugera v. MNR, 2003 DTC 5282 (FCTD)

Before dismissing an application for judicial review of a decision of the Minister to not grant a request for the making of late-file elections,...

See Also

Glenogle Energy Inc. v. Canada (Attorney General), 2022 FC 198

In January 2015, the taxpayer transferred resource properties to a limited partnership that was wholly-owned by it, directly and indirectly. The...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 96 - Subsection 96(5.1) | taxpayer failed to provide any explanation to CRA as to why it was not engaged in retroactive tax planning | 395 |

Administrative Policy

7 October 2011 APFF Roundtable Q. 23, 2011-0412111C6 F - Validity of Price Adjustment Clause

At the 2007 APFF Roundtable, CRA stated:

It appears to us that the validity of a price adjustment clause does not depend on the filing of an...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | price adjustment clause does not require filing amended election | 41 |

Information Circular IC 76-19R3, 17 June 1996, para. 15-22; re late and amended elections.

Amenedment to correct unintended tax consequences or faulty valuations or computations

16. We will generally accept an amended election under...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(8) | 59 |

Halifax Round Table, February 1994, Q. 19, 4M00680

Where capital gains are crystallized using an s. 85 election:

as long as a reasonable effort was made to estimate fair market value, the...

90 C.R. - Q37

RC's policy concerning the acceptance of an amended election is as outlined in IC 76-19R2.

86 C.R. - Q33

A submission is required. Examples of situations where it could be accepted are where the parties accounted for the properties as if they were...

Subsection 85(8)

Administrative Policy

9 October 2025 APFF Roundtable Q. 13, 2025-1071541C6 - Irrégularité dans le calcul des pénalités lorsqu’un choix doit être produit

A corporation, whose deadline for filing an s. 85(1) election was the last day of February (February 28), did not file the election until March 28...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Interpretation Act - Section 28 | February 28 to March 31 is one month | 258 |

7 October 2016 APFF Roundtable Q. 1A, 2016-0652951C6 F - Penalty late filed election-subsection 85(8)

Is the late election penalty under s. 85(8) applied on a property-by-property basis? CRA responded:

Where a taxpayer transfers several properties...

Information Circular IC 76-19R3, 17 June 1996, para. 15-22; re late and amended elections.

Penalty estimate required for amended election

21. The Department does not accept an amended or late-filed election made under subsection 85(7) or...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(7.1) | 403 |

26 March 1986 Income Tax Severed Letter RCT 85-243

Regarding the computation in ss. 85(8), 93(6), 96(6) of the period of each month or part of a month commencing on the date the election was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 162 - Subsection 162(1) - Paragraph 162(1)(b) | not passage of a complete month where return required to be filed on Feb 28 is filed on March 29 | 721 |

| Tax Topics - Statutory Interpretation - Interpretation Act - Section 28 | computation of month from is from day X of one month to day X-1 of following month | 178 |

Commentary

Availability of election

Where a taxpayer disposes of property to a taxable Canadian corporation for consideration that includes shares in the...