Subsection 186(1) - Tax on assessable dividends

See Also

Les Entreprises Michèle L'Heureux Inc. v. The Queen, 94 DTC 1693, [1995] 1 CTC 2850 (TCC)

Dussault TCJ. accepted the Minister's "successive calculation method" in solving the circularity issues arising where in the course of a butterfly...

Administrative Policy

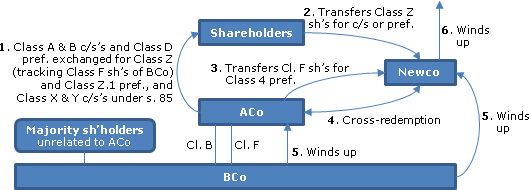

2014 Ruling 2014-0533601R3 - Spin-off butterfly - subsection 55(2)

A spin-off butterfly reorganization by DC entail a cross-redemption of shareholdings (being the "DC Butterfly Shares" and the "Spinco Redemption...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | spin-off by CCPC under Plan of Arrangement of two businesses/matching of PUC of cross-shareholdings to match Part IV tax/leased property as business property | 978 |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(1) | stated capital distribution effected by set-off | 77 |

| Tax Topics - Income Tax Act - Section 86 - Subsection 86(1) | new common shares distinct on basis of right to interim financials | 97 |

2014 Ruling 2013-0513211R3 - Butterfly Transaction

In a butterfly reorganization for the split-up of DC into three TCs, the Part Iv tax circularity problem is addressed by having DC transfer its...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | transfer to TC subco to avoid Part IV circularity/88(2) wind-up of DC/83(2.1) rep | 470 |

30 June 2014 Internal T.I. 2013-0508411I7 F - Part IV Tax and the Dividend Refund

As a result of a tuck under transaction, Investments and XX each held shares in the other. Investments, which had an RDTOH balance at year end,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4) - Paragraph 152(4)(a) - Subparagraph 152(4)(a)(i) | failure to circularly calculate Part IV tax and dividend refund is neglect given published TIs | 268 |

2013 Ruling 2013-0502921R3 - Split-Up Butterfly - Farm

{kind=link}

Butterfly

A standard split-up butterfly of D commences with DC paying a dividend (through issuing demand notes) to each of Son1, Son2 and Mother...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | split-up b/f of CCPC with discontinued farm and unresolved circularity issue | 609 |

2013 Ruling 2012-0443081R3 - Distribution of pre-72 Capital Surplus on Hand

(Amended only re one ruling in 2013-0512531R3)

{kind=link}

Current situation

ACo, which is a Canadian-controlled private corporation (with an RDTOH...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Personal-Use Property | 118 | |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(2) | 737 |

2013 Ruling 2012-0449611R3 - single-wing butterfly reorganization

{kind=link}

Existing situation

DC, which is a CCPC beneficially owning rental real estate encumbered with mortgages (the "Buildings") and which carries on a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | single-wing b/f with acquisition of control of DC by its remaining shareholder (helpful re circularity issue) | 566 |

93 C.R. - Q. 44

RC is prepared to consider requests for refunds of Part IV tax paid by a parent for a year in which it received a dividend from a subsidiary (that...

4 March 1991 T.I. (Tax Window, No. 2, p. 15, ¶1183)

A private corporation is required to pay Part IV tax under s. 186(1)(b) irrespective whether the payor corporation actually applies for the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 129 - Subsection 129(1) | 22 |

IT-474R "Amalgamations of Canadian Corporations" under "Rules Respecting Shareholders, Option Holders and Creditors" under "Non-Resident Shareholders"

"A non-resident holder of shares of a predecessor corporation which constitute taxable Canadian property need not comply with the procedures set...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(1) | 0 |

Articles

Michael N. Kandev, Alan Shragie, "RDTOH on Butterfly", Canadian Tax Highlights, Volume 16, Number 11, November 2008, p. 2.

Use of sub of TC to avoid circularity (p.2)

CRA document 2007-0237361R3 suggests an approach that may permit an allocation of a share of the RDTOH...

Potter, "Part IV Tax Complications in Butterfly Transactions", 1992 Canadian Tax Journal, No. 4, p. 992.

Paragraph 186(1)(a)

Administrative Policy

26 November 2020 STEP Roundtable Q. 11, 2020-0839891C6 - Subsection 104(19)

A Canadian resident personal trust receives a dividend from ACo, and distributes the dividend to B Co (a beneficiary) to which A Co is connected...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(19) | dividend subject to Pt IV tax because payer and corporate beneficiary no longer connected at December 31 effective date of all s. 104(19) designations | 85 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(13) | designated dividend included in individual’s terminal return which has a December 31 year end | 129 |

| Tax Topics - Income Tax Act - Section 249 - Subsection 249(1) - Paragraph 249(1)(c) | individual has a calendar year, even in terminal year | 149 |

30 April 2019 Internal T.I. 2018-0757591I7 F - Part IV tax and trust

A discretionary family trust ("Trust") receives a cash taxable dividend on June 20, 2017 on its non-voting common shares of Opco (whose voting...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(19) | s. 104(19)-designated dividend not received as dividend until trust year end | 223 |

3 June 2016 External T.I. 2016-0647621E5 F - Dividend designation from a trust - timing

A dividend is received by a family trust from a Canadian-controlled private corporation with only operating assets (Opco) and immediately...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(19) | designation not effective until end of year | 230 |

28 April 2004 External T.I. 2004-0066231E5 F - Connected Corporations

Two related corporations (Holdco A and B, with calendar years) held 51% and 49% of the single class of shares (common shares) of Opco (which had a...

6 February 2004 External T.I. 2004-0057821E5 F - Connected Corporations

Opco, which was held as to 51% of its shares (being common shares) by Holdco A (with a calendar year) and 49% by Holdco B (which dealt at arm’s...

Paragraph 186(1)(b)

Administrative Policy

2024 Ruling 2024-1008821R3 F - Multi-wings split-up net asset butterfly 55(3)(b)

Under a two-wing split-up net asset butterfly, the five siblings who were the shareholders of the distributing corporation (DC) transferred their...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | net asset split-up butterfly of DC with cash and near-cash property (defined in detail) and investment property (stock market portfolio) | 435 |

2023 Ruling 2023-0998411R3 F - Butterfly Reorganization

The proposed transactions in 2022-0957491R3 F entailed initial distributions by an estate and trust, followed by the implementation of a split-up...

2021 Ruling 2021-0904311R3 F - Butterfly Reorganization

On a butterfly transaction, Pt. IV tax circularity issues are avoided by having a year end for the transferee corporation (Newco) occur between...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | butterfly transaction for a farming corp (DC) of two brothers coupled with an immediate gift of shares of DC and TC to their respective sons under s. 73(4.1) | 544 |

| Tax Topics - Income Tax Act - Section 191 - Subsection 191(5) | specified amount included in shares issued on butterfly distribution | 200 |

2021 Ruling 2020-0852541R3 F - Split-up XXXXXXXXXX Butterfly

In its closing comments on a proposed one-wing split-up butterfly in which a portion of the farm business of the “Transferor” was transferred...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | one-wing split-up butterfly with a preliminary cash distribution of life insurance proceeds | 263 |

2021 Ruling 2020-0863171R3 - Gross basis split-up Butterfly

CRA ruled on a butterfly split-up of a rental property company (which was considered to carry on an active business because it had more than five...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | CRA rules on gross asset butterfly with preliminary safe income dividend to increase ACB to exceed pre-1972 CSOH | 614 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(2) - Paragraph 88(2)(b) - Subparagraph 88(2)(b)(ii) | butterfly with preliminary safe income dividend to increase ACB to pre-1972 CSOH, avoiding capital gain on wind-up | 190 |

2020 Ruling 2018-0772291R3 F - Multi-wings split-up net asset butterfly 55(3)(b)

CRA ruled on a simple butterfly for the split-up of a CCPC distributing corporation (DC) with cash, and investment assets, between the respective...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | split-up butterfly of investment co (DC) between three siblings' transferees (TCs) with extinguishment of TC notes on DC wind-up | 399 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) - Forgiven Amount | no application of s. 80 where notes owing by corporation to its shareholders are distributed to them on its winding-up | 173 |

2019 Ruling 2018-0758411R3 - Multi-wing split-up net asset butterfly

A butterfly split-up of a DC holding rental property between two transferee corporations (the TCs) for two unrelated families, with undivided...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | butterfly split-up of rental property into co-ownership arrangement, completed by wind-up of DC into TCs and subsequent dividend refund distribution | 571 |

2018 Ruling 2018-0749491R3 - 55(3)(a) Reorganization

A DC which holds a rental property and an investment portfolio and is owned by Parent and his four children will spin off its investment portfolio...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) - Subparagraph 55(3)(a)(ii) | spin-off of investment portfolio (but not rental property) by DC to 4 children’s respective TCs which father controls with special voting shares | 574 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(4) | Parent reps that he will control the TCs for commercial reasons | 288 |

11 October 2018 External T.I. 2018-0771831E5 - Part IV Circular Calculation on cross redemption

In the context of a group of corporations undertaking a reorganization involving share redemptions between multiple corporations, with one or more...

2018 Ruling 2017-0683941R3 - Split-up transactions

Mother along with an arm’s length business associate (“Investor”) wanted to use some of the assets of the family business corporation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) - Subparagraph 55(3)(a)(ii) | split-up to resolve business differences between daughter and mother, with relevant significant investment of arm's length investor in further transferee company | 758 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | arm's length investment in proposed purchaser of spinco assets not part of spin-off series | 229 |

2017 Ruling 2016-0646891R3 - Pipeline and subsequent Split-up butterfly

CRA ruled on a combined pipeline and split-up butterfly transaction respecting DC, which invested in marketable securities, and the shares in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | pipeline coupled with split up butterfly in favour of TCs for grandchild residuary trusts | 543 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | combined pipeline and split-up butterfly | 144 |

18 December 2017 External T.I. 2017-0714971E5 F - Application of subsection 55(2)

2017-0724071C6 indicated that where Holdco receives a dividend of $400,000 that was subject to Part IV tax of $153,333 (38.33% of $400,000)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2) | relationship between Part IV tax and s. 55(2) and related amended return filings | 477 |

21 November 2017 CTF Roundtable Q. 6, 2017-0724071C6 - Circular calculations Part IV tax

Holdco receives a dividend of $400,000 that is subject to Part IV tax of $153,333 (38.33% of $400,000) equalling the connected payer’s dividend...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2) | where Holdco receives a dividend subject to refundable Pt IV tax and to s. 55(2), two different dividends should be reported for Pt IV and s. 55(2) purposes | 396 |

2017 Ruling 2016-0675881R3 - Paragraph 55(3)(a) Internal Reorganization

CRA ruled on a s. 55(3)(a) split-up of a real estate rental corporation (Canco) whose common shares were held by Son Holdco and Daughter Holdco...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) | division of rental real estate company between holdcos for 2 children but with parents' holdco retaining voting control | 579 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(4) | s. 55(3)(a) split-up between Newcos for two siblings which were related due to multiple-voting shares held by the father’s and mother’s Holdco | 170 |

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) - Paragraph 85(1)(e) | UCC on s. 55(3)(a) spin-off prorated based on relative capital cost rather than FMV | 174 |

2015 Ruling 2015-0605901R3 F - Présomption de gain en capital

The proposed transactions contemplate (in para. 24) respecting a spin-off of real estate by Opco to newly-incorporated Realtyco that Opco (with...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.01) - Paragraph 55(3.01)(g) | separation of real estate assets beneath new holdco formed by unrelated shareholders | 567 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) - Subparagraph 55(3)(a)(ii) | spin-off of real estate beneath new common holdco of unrelated shareholders | 107 |

| Tax Topics - Income Tax Act - Section 249.1 - Subsection 249.1(7) | taxation year end changed to immediately before building spin-off | 95 |

24 November 2015 CTF Roundtable Q. 1, 2015-0610691C6 - T2 Late-Filing: Impact on Div. Refund and RDTOH

Will CRA require a dividend recipient to pay Part IV tax if it receives a dividend from a connected dividend payer that had RDTOH at the end of a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 129 - Subsection 129(1) | unclaimed dividend refunds did not reduce the corporation’s RDTOH | 200 |

27 June 2014 External T.I. 2013-0498191E5 F - Interaction entre 55(2) et l'impôt de partie IV

On a cross-share redemption between two connected Canadian-controlled private corporations, neither of which has a refundable dividend tax on hand...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2) | s. 55(2) tax on cross-redemption deemed dividends between connected CCPCs gave rise to circular Part IV tax | 355 |

11 October 2013 Roundtable, 2013-0495801C6 F - Dividend Paid to Trust and Schedule 3 of T2

The trust designates a taxable dividend it received on June 30, 2013 from Opco to its beneficiary, Holdco, whose year-end is June 30. 2013. A...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(19) | s. 104(19) designation is not effective until year end of trust | 167 |

21 January 2009 External T.I. 2008-0266191E5 F - Part IV & Capital Gain Strip

CRA confirmed its position in 9711005 and indicated that its position in 9906255 was no longer valid because of the 943963 Ontario decision. ...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(c) | portion of the dividend received by the recipient corporation that is subject to Pt. IV also includes any safe income attributable to the shares of the payer held by the recipient | 219 |

26 January 2004 External T.I. 2003 - 0047961E5 F - Part IV Circularity

CCRA indicated that it is not prepared to accept the waiver of a dividend refund ("DR") by a corporation in order to avoid the circularity problem...

12 December 2002 External T.I. 2001-0100755 F - Impact of LCB on Dr and Part IV

During its the taxation year ending September 30, 2000 ("2000 TY”), Bco paid its CCPC parent (Aco) a taxable dividend of $223,500, entitling it...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 129 - Subsection 129(2) | general practice to net dividend refund against unpaid Part I tax | 115 |

| Tax Topics - Income Tax Act - Section 164 - Subsection 164(1) | where subsequent loss carryback eliminates the Part I tax and dividend refund (DR), the refund interest is calculated on the initial Part I tax amount even if the DR reversal is paid by set-off | 350 |

| Tax Topics - Income Tax Act - Section 160.1 - Subsection 160.1(1) | interest payable under s. 160.1(1) on the reversed dividend refund where subsequent year’s loss is carried back to eliminate the Part I tax and RDTOH | 283 |

9 June 2000 External T.I. 1999-0010015 F - Interaction entre 55(2) et 186(1)

A purported distributing corporation (Opco), which was owned by two brothers, effected a spinoff of a portion of its capital properties to a Newco...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2) - Paragraph 55(2)(a) | deemed dividends arising under failed butterfly transaction gave rise to double taxation and no Part IV tax | 215 |

9 November 1999 External T.I. 9906255 F - CALCUL DE L'IMPOT P. IV - 55

Holdco, which held the common shares but not the preferred shares of Canco, received a deemed dividend of $2,000,000 from Canco as a result of a...

Articles

David Carolin, Manu Kakkar, "Estate Plans, Trusts, and Dividends: Is There a Gap Here?", Tax for the Owner-Manager, Vol. 21, No. 1, January 2021, p. 1

CRA’s position (e.g., in 2016-0647621E5 and 2013-0495801C6) is that a dividend designated under s. 104(19) by a trust to a beneficiary is not...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(19) | 311 |

Paragraph 186(1)(d)

Administrative Policy

10 February 1999 External T.I. 9800905 F - IMPOT DE LA PARTIE IV

Part IV tax of a subject corporation could not be eliminated pursuant to s. 186(1)(d) through the utilization of its non-capital losses, as they...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(3) - Subject Corporation | Pubco indirectly controlled by an individual was a subject corp | 95 |

Subsection 186(2) - When corporation controlled

See Also

Carter v. The King, 2024 TCC 71

The taxpayer, her cousin (“McAllister”) and her father held 40%, 40% and 20% of the common shares of Brown’s Paving Ltd. (“BPL”),...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) | s. 84.1 did not apply to a sale of the taxpayer’s Opco shares to her cousin’s holdco for cash funded by an Opco dividend | 442 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | a sale of the taxpayer’s Opco shares to her cousin’s holdco for cash funded by an Opco dividend, was arm's length | 339 |

Special Risks Holdings Inc. v. The Queen, 84 DTC 6505, [1984] CTC 553 (FCTD), aff'd 86 DTC 6036, [1986] 1 CTC (FCA)

Exactly 1/2 of the common shares of a corporation ("Melling, Hogg") were purchased by the plaintiff, and the other 1/2 were purchased by a United...

Administrative Policy

7 October 2020 APFF Roundtable Q. 17, 2020-0845821C6 F - Part IV tax and trust

A personal trust wholly-owns Opco, which also has a December 31 year end, and has a corporate beneficiary ("Holdco") with a September 30 taxation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(19) | various applications of proposition that an s. 104(19) designation is not effective until the trust’s year end | 761 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(24) | under the ordinary meaning of payable, an amount is payable at a time if it is paid then | 450 |

11 October 2019 APFF Roundtable Q. 12, 2019-0812711C6 - Part IV

The common shares of X Corp. and Y Corp are held equally by two unrelated corporations (A Corp. and B Corp.). Is Y Corp. connected to X Corp. so...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | two 50% shareholders of two corporations likely acting in concert to produce connectedness | 174 |

10 October 2014 October APFF Roundtable Q. 18, 2014-0538081C6 F - 2014 APFF Roundtable, Q. 18 - Connected corporations

Aco holds one share of Cco bearing 1000 votes and Cco holds 100 share of Bco carrying one vote per share. Aco and Cco deal at arm's length. The...

12 January 2011 External T.I. 2010-0388821E5 F - Discretionary dividend

On January 1 of Year 1, Mr. A (the sole shareholder of Holdco) and Holdco subscribed, respectively, $100 and $900 for 100 Class A voting...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(c) | SIOH where two discretionary-dividend classes potentially allocable fully to class with 100% winding-up participation | 259 |

16 November 2006 External T.I. 2006-0204901E5 F - Meaning of Full Voting Rights

The common shares of Opco carry one vote per share at all meetings of the shareholders, except at a meeting where the right to vote is restricted...

10 November 2000 External T.I. 1999-0008375 F - Associates corporations

After confirming that s. 186(2) expanded the concept of control so as to be broader than de jure control, CCRA provided the example of Yco, 90% of...

29 July 1992 T.I. (Tax Window, No. 21, p. 7, ¶2054)

Where an individual owns all the shares of Holdco which, in turn, owns all the shares of Opco, a loan receivable owing by Holdco to Opco will...

15 May 1991 T.I. (Tax Window, No. 6, p. 2, ¶1357)

Where the shares of Parentco are owned by related persons, its subsidiary will be deemed for purposes of Part IV and the definition of a qualified...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110.6 - Subsection 110.6(1) - Qualified Small Business Corporation Share | 35 |

31 July 1989 T.I. (Dec. 89 Access Letter, ¶1053)

A corporation ("Opco") all of whose voting shares are held by an individual is connected with a second corporation which holds the non-voting...

Articles

Stan Shadrin, Manu Kakkar, David Carolin, "Application of Part IV Tax to Amalgamations of Companies Owned by Trusts with Corporate Beneficiaries", Tax for the Owner-Manager, Vol. 22, No. 1, January 2022, p. 1

A horizontal amalgamation may cause a dividend paid to another family corporation through a trust to be subject to Part IV tax (pp. 1-2)

- CRA...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(2.11) | 399 |

Subsection 186(3)

Subject Corporation

Administrative Policy

10 February 1999 External T.I. 9800905 F - IMPOT DE LA PARTIE IV

Opco was connected to Pubco, a public corporation holding 49% of its common shares. Pubco, in turn, had 60% of its common shares held by a wholly...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(1) - Paragraph 186(1)(d) | s. 186(1)(d) does not permit application of non-capital losses subject to the s. 111(5) restrictions | 35 |

Subsection 186(4) - Corporations connected with particular corporation

Cases

Canada v. Vefghi Holding Corp, 2025 FCA 143

Partway through its calendar taxation year, a family trust received a dividend from a family corporation, paid that dividend to a corporate...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(19) | whether a s. 104(19) dividend was received by a corporate beneficiary from a connected corporation is tested at the trust year end | 584 |

| Tax Topics - Statutory Interpretation - Interpretation/Definition Provisions | legal fiction treated as arising from a deeming provision must reflect its precise wording | 69 |

Administrative Policy

22 July 1993 External T.I. 9313855 F - Connected Corporations

"The existence of a shareholders' agreement or a voting trust which dictates the manner in which the shares are to be voted will not disqualify...

16 December 1992 T.I. 920178 (November 1993 Access Letter, p. 511, ¶C245-050)

Discussion of whether s. 245 will apply where additional shares are required, or shareholdings are pooled, in order that Part IV tax will not...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 30 |

26 August 1992 T.I. (Tax Window, No. 23, p. 12, ¶2155)

The definition of control in s. 186(2) should be used in applying the tests in s. 186(4) even where those tests relate to provisions outside Part...

25 and 28 March 1991 T.I. (Tax Window, No. 1, p. 5, ¶1178)

A corporation is not "connected" with its wholly-owned subsidiary.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Small Business Corporation | 68 |

90 C.R. - Q26

A corporate beneficiary of a trust will not be considered for purposes of s. 186(4)(b) to own shares held by the trust notwithstanding that the...

IT-269R3 "Part IV Tax on Taxable Dividends Received by a Private Corporation or a Subject Corporation"

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Shares | 63 |

Articles

David Carolin, Marissa Halil, Manu Kakkar, "Not so connected for the capital gains exemption", Tax for the Owner-Manager, Vol. 25, No. 4, October 2025, p. 4

Need for Opco to be connected for respective Holdco shares to satisfy the QSBCS tests (p. 4)

- It is common for unrelated shareholders of Opco to...

Paragraph 186(4)(a)

Administrative Policy

17 August 1999 APFF Roundtable Q. 20, 9921060 F - SOCIÉTÉ BÉNÉFICIAIRE D'UNE FIDUCIE

CCRA agreed that, by virtue of the addition of s. 251(1)(b) deeming a personal trust to be related to a corporate beneficiary that was a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(b) | addition of s. 251(1)(b) caused a corporate beneficiary of personal trust to be related under ss. 186(2) and 186(4)(a) to a trust-controlled corporation paying a dividend to the trust | 52 |

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Capital Dividend Account - Paragraph (a) | no CDA addition re dividend designated to CCPC as a taxable capital gain under s. 104(21) | 52 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(c) | s. 104(19) dividend can come out of safe income | 101 |

Paragraph 186(4)(b)

Administrative Policy

IT-269R4 ARCHIVED - Part IV Tax on Taxable Dividends Received by a Private Corporation or a Subject Corporation 24 April 2006

Generally no connected corp exclusion where dividends received through a personal trust

¶ 16. It is not unusual for a private corporation to be a...

Subsection 186(5) - Deemed private corporation

Administrative Policy

18 December 2001 External T.I. 2001-0073925 - Paragraph 88(1)(e.2) & Subsection 186(5)186(5)

"While subsection 186(5) does not specifically refer to paragraph 88(1)(e.2) it is our view that such reference is not necessary. Therefore, where...

Subsection 186(6) - Partnerships

Administrative Policy

6 November 2013 External T.I. 2013-0485691E5 - Connected Corporation and Part IV Tax

The recipient corporation owns 20% of the shares of a payer corporation (and is thus connected under s. 186(4)(b), and also owns 12.5% of the...

Subsection 186(7) - Interpretation

Administrative Policy

8 January 2003 External T.I. 2002-0173665 - SMALL BUSINESS CORP

Two corporations which have no direct ownership in each other but which are controlled by the same person would be considered to be connected...