See Also

Daggett v. MNR, 93 DTC 14, [1992] 2 CTC 2764 (TCC)

A series of transactions pursuant to which the taxpayer used borrowed funds under a daylight loan to subscribe for common shares of a loss company...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Dividend | 34 |

Distribution

See Also

Northern Hot Oil Services Ltd. v. The Queen, 97 DTC 12107 (TCC)

A transaction in which the common shares of a corporation held by the taxpayer were purchased for cancellation for consideration consisting of...

Administrative Policy

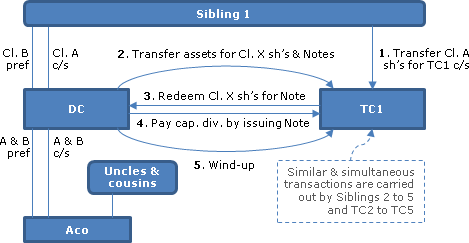

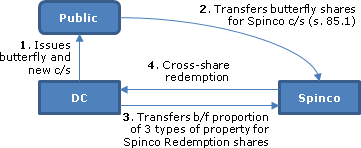

2021 Ruling 2019-0821121R3 - Multi-wing split-up gross asset butterfly

Background

Parentco is equally owned by three holding companies (Holdcos 1, 2, and 3) for three siblings holding preferred shares and their...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 96 | representations re properties being held in co-ownership rather than partnership | 220 |

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(2) - Paragraph 87(2)(a) | purpose of amalgamation was to create a short taxation year | 29 |

2024 Ruling 2023-0998291R3 F - Multi-wings split-up net asset butterfly 55(3)(b)

Background

The distributing corporation (DC), which was owned by a divorced couple (Shareholder 1 and Shareholder 2), held net cash assets and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) - Paragraph 85(1)(b) | excess debt allocated on s. 85(1) transfer of land and building to the land so as to produce capital gains rather than recapture | 230 |

2022 Ruling 2021-0911791R3 F - Single-wing butterfly - Investment company

Background

The distributing corporation (“DC”) is a vehicle for two sisters (A and B) and trusts for the benefit of B's adult children to...

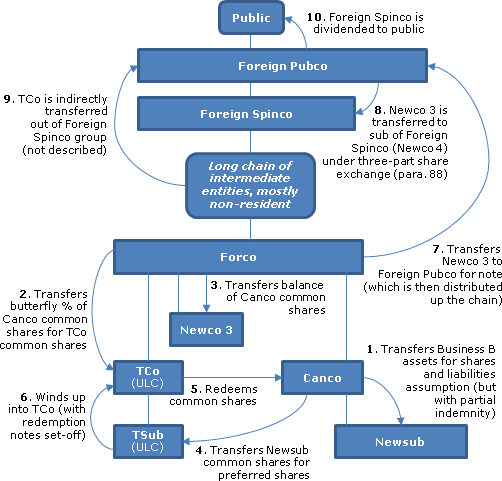

2023 Ruling 2022-0943871R3 - Cross-border spin-off butterfly

CRA has ruled on a relatively straightforward cross-border butterfly. Before the distribution of the shares of Foreign Spinco (holding the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.1) - Paragraph 55(3.1)(b) - Subparagraph 55(3.1)(b)(i) - Clause 55(3.1)(b)(i)(A) - Subclause 55(3.1)(b)(i)(A)(II) | s. 55(3.1)(b)(i)(A)(II) tested at Foreign Spinco level by applying its debt, that does not relate to specific assets, on a pro rata basis | 856 |

2024 Ruling 2024-1008821R3 F - Multi-wings split-up net asset butterfly 55(3)(b)

Background

The common shares and non-voting Class C preferred shares of the distributing corporation (DC) are held by two sisters and its Class E...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(1) - Paragraph 186(1)(b) | Pt. IV circularity avoided through establishing year ends for TCs before DC wound up into TCs | 136 |

2023 Ruling 2022-0957491R3 F - Butterfly Reorganization

Background

Transferor is a holding company holding near-cash and investment property including shares of a public corporation (Corporation). Its...

2024 Ruling 2023-0987001R3 - Public Spin-Off Butterfly

CRA ruled on butterfly spin-off transactions to effect the split-up of DC2, a public corporation, into two publicly listed companies: DC2 and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.02) | successive butterflies to effect the creation of a 2nd public corporation/ lower-tier butterfly by a “specified wholly-owned corporation” | 938 |

2021 Ruling 2021-0904311R3 F - Butterfly Reorganization

Background

Transferor is a farming corporation whose Class A common and Class D preferred shares are both held by two resident brothers (A and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 191 - Subsection 191(5) | specified amount included in shares issued on butterfly distribution | 200 |

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(1) - Paragraph 186(1)(b) | circularity avoided through intervening taxation year end of transferee corp | 74 |

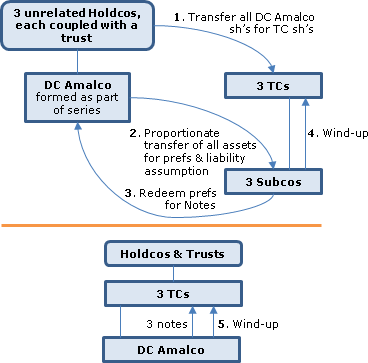

2021 Ruling 2020-0848061R3 - Sequential Butterfly

Background

Aco to Eco are corporations held by unrelated individuals (A to E) or their families or family trusts. They wish to separate their...

2021 Ruling 2020-0852541R3 F - Split-up XXXXXXXXXX Butterfly

CRA provided standard rulings for a one-wing split-up butterfly respecting the “Transferor,” which computed the income from its business...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(1) - Paragraph 186(1)(b) | resolution of Part IV tax circularity issue on butterfly to be resolved by local TSO | 80 |

2022 Ruling 2021-0884331R3 - Gross Asset Butterfly

Background

The shares (being preferred and common shares) of DC, whose assets (other than minor cash) consisted solely of publicly-traded shares,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 86 - Subsection 86(1) | s. 86 exchange by articles of amendment of pref into common | 86 |

2021 Ruling 2020-0863171R3 - Gross basis split-up Butterfly

Background

DC owns four rental properties (Properties 1, 2, 3 and 4) which generate business income rather than being a specified investment...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(2) - Paragraph 88(2)(b) - Subparagraph 88(2)(b)(ii) | butterfly with preliminary safe income dividend to increase ACB to pre-1972 CSOH, avoiding capital gain on wind-up | 190 |

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(1) - Paragraph 186(1)(b) | request to TSO for short taxation year to avoid dividend circularity on split-up butterfly | 233 |

2020 Ruling 2018-0772291R3 F - Multi-wings split-up net asset butterfly 55(3)(b)

Background

The Corporation, which is held by Holdco, three siblings (Child 1, 2 and 3) and three trusts (Newtrust 1, 2 and 3) for the benefit of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(1) - Paragraph 186(1)(b) | split-up butterfly that avoids Pt IV tax circularity by a subsequent wind-up of the distributing corporation | 153 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) - Forgiven Amount | no application of s. 80 where notes owing by corporation to its shareholders are distributed to them on its winding-up | 173 |

2019 Ruling 2018-0758411R3 - Multi-wing split-up net asset butterfly

Current structure

DC, which is the beneficial owner of a rental real estate property (representing a specified investment business), is held by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(1) - Paragraph 186(1)(b) | Pt. IV tax circularity avoided through winding-up dividend in subsequent year | 144 |

2018 Ruling 2017-0733011R3 - Split-up Butterfly

Current structure

The shareholders of DC (a Canadian-controlled private corporation) are A and her two adult children, B and C, each holding...

2018 Ruling 2017-0714411R3 - Butterfly Reorganization

Current structure

The shareholders of DC, a Canadian-controlled private corporation carrying on a farming business are Mother, holding...

2017 Ruling 2017-0699201R3 - Cross-border Butterfly

Current Structure

Foreign Parentco, which is governed by the laws of (foreign) Country 1 and has two classes of issued and outstanding shares...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Permitted Exchange - Paragraph (b) | cross-border butterfly including preliminary transfer of DC to foreing parent to come within “permitted exchange” | 444 |

| Tax Topics - Income Tax Act - Section 143.3 - Subsection 143.3(3) | s. 143.3(3) inapplicable on a 4-party exchange | 234 |

| Tax Topics - Income Tax Act - Section 54 - Adjusted Cost Base | full cost of property acquired under 4-party exchange | 222 |

| Tax Topics - Income Tax Act - Section 212.1 - Subsection 212.1(1.1) - Paragraph 212.1(1.1)(b) | application on 4-party exchange | 291 |

2017 Ruling 2016-0646891R3 - Pipeline and subsequent Split-up butterfly

CRA ruled on a combined pipeline and split-up butterfly transaction respecting DC, which invested in marketable securities, and the shares in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | pipeline coupled with split up butterfly in favour of TCs for grandchild residuary trusts | 543 |

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(1) - Paragraph 186(1)(b) | circularity avoided through 2nd dividend arising on winding-up of DC | 145 |

2017 Ruling 2016-0674681R3 - Sequential Split-Up Butterfly

Background

DC1 holds cash and cash-like assets (e.g., money market funds or GICs), marketable securities and has an RDTOH and CDA balance. Its...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 129 - Subsection 129(1) | capital gain deliberately triggered to generate CDA and RDTOH addition and year end change granted to isolate dividend refund | 543 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.1) - Paragraph 55(3.1)(a) | sale of securities for cash proceeds that are reinvested, and tendering shares for shares of offeror | 58 |

| Tax Topics - Income Tax Act - Section 249.1 - Subsection 249.1(7) | CRA accommodates year end change so that dividend refund of full RDTOH balance is generated in Year 1 | 210 |

2016 Ruling 2015-0616291R3 - Cross-Border Butterfly

Background

All of the common shares of Canadian DC are owned by Forco 2 which, in turn, is wholly-owned by Forco 1 which, in turn, is...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Permitted Exchange | two successive permitted exchanges contemplated | 205 |

2013 Ruling 2012-0459781R3 - Cross border butterfly

Overview

This was a cross-border butterfly of a Canadian spin business (already packaged into a subsidiary of DC) by DC to TC, an indirect...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.2) - Paragraph 55(3.2)(h) | 4-party exchange to avoid s. 55(3.2)(h) | 115 |

| Tax Topics - Income Tax Act - Section 212.1 - Subsection 212.1(1.1) - Paragraph 212.1(1.1)(b) | PUC grind where shares issued in 4-party exchange | 220 |

2015 Ruling 2014-0552871R3 - Split-Up Butterfly

Background

Mr. D and Mr. E (and their respective families), with the two families being unrelated, decided to split up the business of the CCPC...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(b) | post-butterfly sale of distributed shares by one TC to the other | 61 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(24) | deferred revenue treated as boot | 53 |

2015 Ruling 2014-0558831R3 - No-type of property spin-off butterfly

Background

DC is a public corporation all of whose multiple-voting (common) shares (“DC MVS”) and some of whose subordinate-voting (common)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(1.4) | replacement stock options issued by Spinco treated as boot | 112 |

| Tax Topics - Income Tax Act - Section 86 - Subsection 86(1) | new common shares with same attributes as old subject to rights of new special shares/ pro rata PUC | 164 |

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) - Paragraph 85(1)(d) | proration of CEC preliminary to butterfly | 156 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | splitting of fee for management of 2 divisions not a disposition of contract | 145 |

8 June 2016 CTF Technical Seminar: Update on s. 55(2)

CRA indicated that it cannot confirm in the context of a butterfly that the pro-rata requirement in s. 55(1) is met where the shares issued are...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(b) | integration principle/expanded scope/no contemplated sale required/no blanket exemptons/policy similar to boot rules | 375 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(c) | safe income appropriately reduced by incentive reductions | 31 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.5) | significant reduction in value of nominal value share | 90 |

27 April 2016 External T.I. 2016-0633101E5 F - Attribution of safe income

After discussing the allocation of safe income between two classes of discretionary dividend common shares, CRA added this comment (TI...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(c) | discretionary dividend will not reduce safe income attributable to the other class of discretionary dividend shares to the extent the dividend is taxable under s. 55(2) | 346 |

2015 Ruling 2014-0548491R3 - Split-up XXXXXXXXXX Butterfly

A split up of DC's business among three brothers (A, B and C) and their respective immediate families is accomplished by split-up style butterfly...

2015 Ruling 2013-0490651R3 - Single-wing Split-up Farm Butterfly

DC carries on a farming business. There is a single-wing butterfly transfer of its three types of property to TC, to which Sibling 1 has...

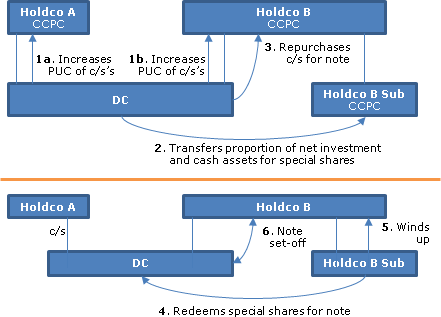

2014 Ruling 2014-0533601R3 - Spin-off butterfly - subsection 55(2)

{kind=link}

Current structure

DC, which is a Canadian-controlled private corporation, carries on the production, processing and sale of XX (the "DC Retained...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(1) | matching of PUC of cross-shareholdings to match Part IV tax | 152 |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(1) | stated capital distribution effected by set-off | 77 |

| Tax Topics - Income Tax Act - Section 86 - Subsection 86(1) | new common shares distinct on basis of right to interim financials | 97 |

2014 Ruling 2014-0530961R3 - Cross-Border Butterfly

{kind=link}

Overview

In connection with a spin-off by a U.S. public company (Foreign PubCo) of a U.S. subsidiary (Foreign Spinco) to which one of its...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.1) - Paragraph 55(3.1)(b) - Subparagraph 55(3.1)(b)(i) | pro rata allocation of Foreign Spinco debt | 180 |

| Tax Topics - Income Tax Act - Section 86.1 - Subsection 86.1(2) | spin-off by U.S. pubco of U.S. spinco after Canadian butterfly | 115 |

2014 Ruling 2013-0513211R3 - Butterfly Transaction

{kind=link}

Current structure

The Class A common shares of DC1, a CCPC, are owned equally by Holdco1, Holdco2 and Holdco3 and its Class J preferred shares...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(1) | split-up CCPC butterfly was structured to avoid Part IV circularity | 95 |

2014 Ruling 2013-0498651R3 - Single-Wing Split-up Butterfly

underline;">: Background. The sole shareholders of DC, which holds a farm property, are two siblings (Sibling1 and Sibling2) and their respective...

2014 Ruling 2012-0446701R3 - Butterfly reorganization

Split-up butterfly is "being undertaken to allow each of [cousins] B and C to carry on separate farming operations from one another, and to...

2014 Ruling 2012-0432441R3 - Butterfly reorganization

Standard split-up butterfly of DC for division of DC between families of Brother 1 and 2.

2013 Ruling 2013-0491651R3 - Cross-Border Butterfly

{kind=link}

Overview

The ordinary shares of Foreign PubCo, which was formed under the laws of Country 1, trade on Exchange 1. The worldwide business...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.1) - Paragraph 55(3.1)(a) | preliminary LP acquisition, cross-border debt repayments and dividend: not part of series | 230 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.1) - Paragraph 55(3.1)(b) - Subparagraph 55(3.1)(b)(i) | cross-border b/f with 3-party exchange, pro rata application of upper tier debt, cash-out of ineligible shareholders | 501 |

| Tax Topics - Income Tax Act - Section 86 - Subsection 86(1) | exchange for substantively identical common shares | 124 |

2013 Ruling 2013-0502921R3 - Split-Up Butterfly - Farm

{kind=link}

Structure

The DC is a CCPC owned (as to both DC-Class A (common) and DC-Class D (pref)) by Son1, Son2 and Mother and which formerly had carried...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(1) | split-up b/f of farm CCPC with unresolved circularity issue | 242 |

2014 Ruling 2013-0498951R3 - Split-up Butterfly

A standard split-up butterfly for the pro rata division of the assets (mostly portfolio shares) of DC (a CCPC with no liabilities other than...

2013 Ruling 2013-0490341R3 - No-type of property spin-off butterfly

{kind=link}

Preliminary

As a preliminary step under a plan of arrangement, the shareholders of Old Pubco (a Canadian public corporation dealing at arm's...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | post butterfly FX loan by TC to DC | 242 |

2013 Ruling 2013-0475681R3 - Family holding butterfly transaction

{kind=link}

Facts

DC is a CCPC holding company whose assets consist of the shares of Aco (controlled by uncles, aunts and cousins), which are investment...

2013 Ruling 2012-0449611R3 - single-wing butterfly reorganization

{kind=link}

Existing situation

DC, which is a CCPC beneficially owning rental real estate encumbered with mortgages (the "Buildings") and which carries on a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(1) | 562 |

2012 Ruling 2012-0460811R3 - Public Company Spin-Off Butterfly

{kind=link}

Under the proposed transactions for a spin-off butterfly of Spinco by DC (a public corporation and principal business corporation as defined in...

2012 Ruling 2011-0425441R3 - Cross Border Butterfly

{kind=link}

Overview

A non-resident public company (Foreign Pubco) will be spinning off Business A to its shareholders, to be accomplished by a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.1) - Paragraph 55(3.1)(b) - Subparagraph 55(3.1)(b)(i) | upper tier debt applied pro rata re 10% limitation | 383 |

2012 Ruling 2011-0416001R3 - Split-up butterfly

Structure

The DC is a CCPC whose only significant assets is shares (being investment property) of Pubco (a Canadian public company over which...

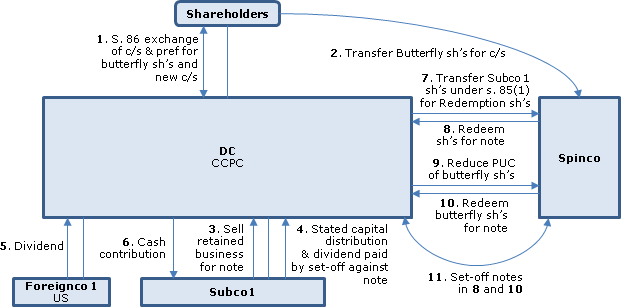

2012 Ruling 2012-0439381R3 - Cross-border spin-off butterfly

{kind=link}

Preliminary transactions

. The transactions entail the spin-off by Foreign Pubco of Foreign Spinco Parent including a Canadian business which...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.1) - Paragraph 55(3.1)(b) - Subparagraph 55(3.1)(b)(i) | 507 |

2012 Ruling 2011-0431101R3 - Cross-border spin-off butterfly

{kind=link}

Background

Foreign Pubco has announced that it will divide itself into three separate publicly traded companies by making a distribution by way...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | interest deduction following b/f cross-redemption | 143 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Permitted Exchange | 429 | |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.1) - Paragraph 55(3.1)(b) - Subparagraph 55(3.1)(b)(i) | 604 |

2012 Ruling 2011-0413661R3 - Butterfly

The distributing corporation ("DC") is controlled by a financial institution ("Owner 1" - perhaps a credit union) and its only assets are a...

7 October 2011 Roundtable, 2011-0399401C6 - Butterfly, life insurance policies, grandfathering

Where two siblings are the shareholders of two transferee corporations which are to receive two life insurance policies taken out by the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.1) - Paragraph 55(3.1)(a) | a policy loan under a life insurance policy to reduce its CSV would trigger s. 55(3.1)(a) | 169 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(4) | s. 55(4) inapplicable if the principal reason for parent’s control of DC was parent's economic interests | 178 |

2009 Ruling 2008-0304371R3 - Single-Wing Butterfly

In a single-wing butterfly of a company whose assets consisted of cash and cash equivalents, tenant receivables and a revenue producing rental...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(24) | portion of assets transferred to transferee corporation on butterfly treated as s. 20(24) payment | 70 |

2008 Ruling 2007-0241221R3 - 55(3)(b) butterfly reorganization

preliminarily to butterfly transactions involving a CCPC (DC) whose individual shareholders are implementing a settlement agreement in respect of...

2008 Ruling 2007-0251681R3 - Butterfly and freeze of an estate

there are two proposed successive butterfly reorganizations in which DC, which is a CCPC whose assets include development real estate, mortgage...

2007 Ruling 2006-0215751R3 - Cross-border butterfly

In a net equity butterfly, after the current liabilities are allocated to cash and near-cash property, "any remaining net FMV of any accounts...

2006 Ruling 2006-0197501R3 - Multiple-wing Butterfly

Vacant land of a distributing corporation used as a parking lot for a facility owned by a subsidiary, and vacant land owned by the distributing...

2006 Ruling 2006-0181061R3 - Butterfly Distribution - XXXXXXXXXX

The cash and near cash property of DC Amalco includes funds in an escrow bank account which, pursuant to the relevant loan agreement, DC Amalco is...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) - Paragraph 85(1)(e) | UCC in butterfly is proportionate UCC | 129 |

2004 Ruling 2003-004375

Where TC receives a butterfly property from DC on spin-off butterfly, the sale by TC of some of the butterflied property back to DC after the...

2002 Ruling 2002-0140733 - XXXXXXXXXX - Sequential Butterfly

sequential butterfly. In each butterfly, "to the extent a portion of the cash or near cash property of the [DC] Group is committed by the [DC]...

2000 Ruling 2000-0040663 - Butterfly reorganization

No look-through approach was applied to holdings in public corporation where each holding was less than 20% and neither the taxpayer nor persons...

1999 Ruling 9902623 - BUTTERFLY REORGANIZATION

Where the distributing corporation or a look-through corporation has limited partnership interests, the consolidated look-through approach will be...

30 November 1997 Ruling 9801803 - PUBLIC BUTTERFLY

In determining the net fair market value of property of the distributing corporation, liabilities should be valued at their principal amount...

30 November 1997 Ruling 9800973 - BUTTERFLY RULING (SPIN-OFF)

sales proceeds, in the form of cash and a non-convertible note receivable, which DC received on the sale of its interests in [unspecified assets]...

30 November 1995 Ruling 9632593 - DIVISIVE REORGANIZATION

Vacant land held for development, which was capital property, was categorized as investment property. Any tax accounts, such as the balance of any...

1996 Corporate Management Tax Conference Roundtable, Q. 16 (Canadian Tax Foundation), at 24:19

When does a reorganization end (that is, when are subsequent transactions considered part of the "reorganization" and when are they outside the...

Robert J.L. Read, "Section 55: A Review of Current Issues," 1988 Conference Report (Canadian Tax Foundation), 18:1-28

Wind-up of transferred corporation into the transferee corporation accomplishes indirect transfer; cf. its amalgamation with TC (p. 18:16)

[A]...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Safe-Income Determination Time | 433 |

Articles

Christian Desjardins, Nik Diksic, "Cross-Border Butterflies in the Context of Public Spin-Off Transactions", 2015 CTF Annual Conference paper

Net cash/investment property transferred driven by relative FMV of spun-off business assets (p.29:20)

[T]he CRA requires that the redemption...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.1) - Paragraph 55(3.1)(b) | 2059 |

Permitted Exchange

Administrative Policy

2016 Ruling 2015-0616291R3 - Cross-Border Butterfly

A foreign public company (Foreign Pubco) is to spin-off a newly-formed non-resident subsidiary (Foreign Spinco). preparatoryh to this, there is...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | 2 successive permitted exchanges in cross-border butterfly/deferred revenue not a liability/agreements between DC And TC re certain allocations so as to affect 3 types of property | 1699 |

2012 Ruling 2011-0431101R3 - Cross-border spin-off butterfly

As preliminary transactions to a butterfly distribution by DC, which is owned by a non-resident subsidiary (Foreign Sub 1) of a non-resident...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | interest deduction following b/f cross-redemption | 143 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | cross-border b/f as part of double Code s. 355 spin-off | 1540 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.1) - Paragraph 55(3.1)(b) - Subparagraph 55(3.1)(b)(i) | 604 |

Paragraph (b)

Administrative Policy

2017 Ruling 2017-0699201R3 - Cross-border Butterfly

CRA ruled on a cross-border butterfly which entailed assets of the “Transferred Business” being transferred indirectly to a wholly-owned...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | cross-border butterfly with 4-party exchange and preceding distribution of DC to foreign parent to qualify as permitted exchange/rental property valued at nil/post-butterfly equaling cash payment | 1140 |

| Tax Topics - Income Tax Act - Section 143.3 - Subsection 143.3(3) | s. 143.3(3) inapplicable on a 4-party exchange | 234 |

| Tax Topics - Income Tax Act - Section 54 - Adjusted Cost Base | full cost of property acquired under 4-party exchange | 222 |

| Tax Topics - Income Tax Act - Section 212.1 - Subsection 212.1(1.1) - Paragraph 212.1(1.1)(b) | application on 4-party exchange | 291 |

8 October 2010 Roundtable, 2010-0373211C6 F - Butterfly Transaction - Permitted Exchange

Where after a butterfly transaction, a family trust (whose beneficiaries are persons unrelated to the transferee corporation, the distributing...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.1) - Paragraph 55(3.1)(b) | issuance of shares by TC after the DC distribution without AOC of TC does not engage s. 55(3.1)(b) | 212 |

Safe-Income Determination Time

See Also

Les Placements E&R Simard Inc. v. The Queen, 97 DTC 1328 (TCC)

On September 10, 1988, the taxpayer transferred its assets to a subsidiary ("Alimentation 1988") in consideration for a demand promissory note and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | 152 | |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2) | 111 |

Administrative Policy

2025 Ruling 2023-0990951R3 - Safe Income Determination Time Monthly Dividends

Background

A non-resident corporation (“XXco”) wholly owns a Canadian-resident corporation (Partner A) which, along with its wholly-owned...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | each dividend in a preordained succession of monthly dividends had a SIDT immediately before the dividend payment, i.e., no series | 133 |

| Tax Topics - Treaties - Income Tax Conventions - Article 4 | reference to 2-step approach to avoiding IV(7)(a) anti-hybrid rule in Canada-US treaty | 89 |

7 October 2022 APFF Roundtable Q. 14, 2022-0942191C6 F - Safe-income determination time

The incorporation on March 15 by a purchaser of a corporation for the purpose of purchasing the assets of another corporation (the vendor) caused...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(b) | no need for CRA flexibility regarding safe income issues arising from early formation of a Buyco | 307 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | safe income arising on a sale and after the safe-income determination time could be used for subsequent dividends not paid as part of the same series | 156 |

15 November 2016 Roundtable, 2016-0672321C6 - Guidance on determination of safe income

Having regard to the concern that the safe-income determination time is no later than the time immediately before the earliest dividend paid as...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(c) | annually recurring dividends are not a series of transactions for safe-income determination purposes/ CRA provision of old returns/ safe income reduced by contingent amounts | 623 |

2015 Ruling 2015-0589471R3 - Earnout

Background

The equal and unrelated (corporate) shareholders of Holdco (a Canadian-controlled private corporation) wish to accommodate the purchase...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(g) | 5-year earnings based earnout for sale of Holdco common shares by Opco to key employee | 841 |

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) | s. 85(1) rollover available on dirty s. 85 exchange | 92 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(c) | utilization of safe income as earned through a contemplated succession of dividends of all the annual earnings | 203 |

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(1) - Paragraph 7(1)(a) | transactions for using s. 7 rules on sale of non-treasury shares | 212 |

26 June 2003 External T.I. 2003-0021595 F - Distribution of Corporate Property

Two brothers (A and B), and their cousins (C and D, who were brothers) each held 50% of the shares of a holding company ("ABco" and ) ("CDco)" for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107 - Subsection 107(2.1) | illustration of application, by virtue of s. 107(2.001) election, of s. 107(2.1) to distribution of CCPC shares | 157 |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | s. 84(2) inapplicable to s. 107(2.1) wind-up of trust holding a Portfolioco followed by an inter vivos pipeline transaction re Portfolioco | 323 |

2 September 1999 APFF Roundtable Q. 14, 9921000 F - MOMENT DE DETERMINATION DU REVENU PROTEGE

Opco, whose two shareholders - A and B, with 60% and 40% shareholdings, respectively - will incorporate Filco. Opco will transfer a property to...

Robert J.L. Read, "Section 55: A Review of Current Issues," 1988 Conference Report (Canadian Tax Foundation), 18:1-28

Safe income excludes income earned after the commencement of the series (p. 18:4)

The period of time relevant to the calculation of “ the income...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | wind-up of transferred corporation into but not amalgamation with TC | 149 |

Articles

Doron Barkai, Alexander Demner, "Dealing with New Subsection 55(2): Issues and Strategies", 2016 Conference Report (Canadian Tax Foundation), 6:1–56

Annual cash dividends generally not a series (p. 6:17)

One issue to consider is whether annual dividends may be part of the same series of...

Rick McLean, "Subsection 55(2): What Is the New Reality?", 2015 CTF Annual Conference paper

Application of safe-income determination time to annual cash dividends (p. 22:43)

The legislative definition of "safe-income determination...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(b) | 926 | |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.3) | 269 |

Marc Ton-That, Vance Sider, "Understanding Section 55 and Butterfly Reorganizations", 2nd Edition, CCH, 1999

Harshness of cut-off at beginning of series (being, generally, the beginning of sale negotiations) (pp. 34-35)

Prior to the introduction of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | 135 |