Subsection 53(1) - Adjustments to cost base

Paragraph 53(1)(b)

Administrative Policy

16 November 2011 External T.I. 2011-0423861E5 F - paragraph 53(1)b)

Holdco, whose common shares of Opco have a nominal adjusted cost base ("ACB") and paid-up capital ("PUC"), a fair market value ("FMV") of $2 million and safe income on hand ("SIOH") attributable to those shares of $900,000, increases the PUC of those shares by $1 million, and transfers those common shares (or to be more precise, new common shares issued in replacement therefor on the PUC increase) to Opco for cancellation in consideration for the issuance by Opco of (i) preference shares of Opco having an FMV, PUC and ACB (determined under s. 85(1)(g)) of $1 million; and (ii) common shares having a FMV of $1 million and nominal PUC and ACB.

If s. 55(2) did not apply to the s. 84(1) dividend, then the ACB of the common shares of Opco held by Holdco following that PUC increase would be determined under s. 53(1)(b) as the excess of the s. 84(1) deemed dividend of $1 million minus $100,000, being the portion of that dividend that did not come out of SIOH - i.e., $900,000.

On the other hand, if s. 55(2) applied to the s. 84(1) dividend, the ACB of those common shares would be the excess of the s. 84(1) deemed dividend received by Holdco (which, by virtue of s. 55(2) would be limited to the SIOH of $900,000) over the nil portion of that deemed dividend that did not come out of SIOH hand - i.e., also $900,000.

Accordingly, in both scenarios, Holdco would realize a $100,000 capital gain on the "dirty s. 85" transfer of the common shares, i.e., the excess of the agreed amount of $1 million over the ACB of $900,000. No amount would be added to the proceeds of disposition of the common shares because of the exclusion under s. 55(2)(b); and CRA would not apply s. 55(2)(c).

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Capital Dividend Account - Paragraph (a) - Subparagraph (a)(i) - Clause (a)(i)(A) | example of capital gain for CDA purposes being less than the s. 40 capital gain | 511 |

Subparagraph 53(1)(b)(ii)

Administrative Policy

S3-F2-C1 - Capital Dividends

1.30 Where a deduction under subsection 112(1) is permitted on a dividend that results from an increase in paid-up capital, subparagraph 53(1)(b)(ii) prevents what may be described as the non-safe income portion of the dividend being added to the cost of the share on which the dividend was received. However, when such dividend is subject to the application of subsection 55(2), it is considered that a deduction under subsection 112(1) was not permitted in respect of that dividend and there is no denied increase in cost under subparagraph 53(1)(b)(ii).

27 November 2018 CTF Roundtable Q. 2, 2018-0780071C6 - Impact of 55(2) deeming rules

CRA indicated that a dividend arising on a paid-up capital increase to which s. 55(2) applied remains a dividend for s. 53(1)(b)(i) purposes but that such dividend was not permitted a deduction under s. 112(1), for purposes of the application of the basis reduction under s. 53(1)(b)(ii). Conversely, there is a reduction of cost under s. 53(1)(b)(ii) to deny cost on the amount of the dividend that exceeds safe income, and on which a deduction under s. 112(1) was obtained. Thus, cost will not be denied when a dividend on a paid up capital increase has been subject to s. 55(2). CRA stated:

The evolution of the role of subsection 55(2), as reflected in the 2015 legislative amendments to subsections 55(2), 52(3) and paragraph 53(1)(b), invites the conclusion that the application of subsection 55(2) to a dividend should not result in the denial of cost to the property that is received by the dividend recipient on the payment of the dividend.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 52 - Subsection 52(2) | property dividended has cost equal to FMV where subject to s. 55(2) | 104 |

| Tax Topics - Income Tax Act - Section 52 - Subsection 52(3) | cost under s. 52(3) for stock dividend amount to which s. 55(2) applied | 69 |

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Capital Dividend Account - Paragraph (a) - Subparagraph (a)(i) | 53(1)(b)(ii) and 52(3)(a) exclusion limited to where 55(2) did not apply to the stock dividend or PUC increase | 70 |

| Tax Topics - Income Tax Act - Section 112 - Subsection 112(3) - Paragraph 112(3)(b) - Subparagraph 112(3)(b)(i) | stop-loss rule does not apply to the extent of the application of s. 55(2) | 92 |

Articles

Rick McLean, Jeff Oldewening, Jonas Lau, "Capital Gains Stripping and Surplus Stripping", 2017 Annual CTF Conference draft paper

Potential double taxation if safe income crystallized by way of PUC bump (p. 20)

Consequently, for a safe income crystallization, where a PUC bump exceeds safe income on 'hand, the non-safe income dividend can be recharacterized by subsection 55(2) as a deemed capital gain. The critical issue becomes whether double taxation arises on a subsequent disposition of the shares, as the ACB to the dividend recipient of its shares does not increase on account of its deemed capital gain.

Before the 2015 amendments, the CRA stated that double taxation would not be sought. [fn 71: 2011-0415891E5 and 9830665]

Paragraph 53(1)(c)

See Also

Burman v. The Queen, 2003 DTC 1007 (TCC)

The failure of the taxpayer to draw salary from a company of which she was a shareholder did not represent a contribution of capital that could be added to the adjusted cost base of her shares.

Administrative Policy

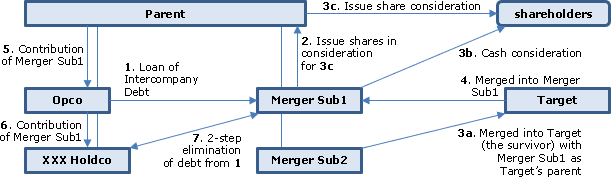

2021 Ruling 2021-0911211R3 - Foreign Takeover

The acquisition of a non-resident target (Target) by a Canadian corporation (Opco) and its Canadian parent (Parent) entailed:

- Parent forming two new stacked non-resident subsidiaries (Merger Sub1 holding Merger Sub2);

- Merger Sub2 being merged into Target with Target being the survivor, with the shareholders of Target having their shares converted into shares issued by Parent and cash paid by Merger Sub1 (which it had borrowed from Opco) and with Merger Sub1 becoming the parent of Target; and

- Merger Sub2 then immediately being merged into Merger Sub1 with Merger Sub1 as the survivor.

In order that Parent could get basis for having issued the share consideration, it was stated in a funding agreement to have issued such shares in consideration for the issuance to it by Merger Sub1 of common shares of Merger Sub1 – and CRA ruled that indeed those shares issued to Parent had a cost to it equal to the FMV of the shares issued by it in turn to the Target shareholders plus any related costs incurred by it.

CRA also ruled that on the first merger, Merger Sub1 disposed of its shares of Merger Sub2 for those shares’ FMV.

CRA further ruled that on the immediately subsequent contribution by Parent of its shares of Merger Sub1 to Opco, it did not realize a gain, and Opco had full cost for those shares pursuant to s. 53(1)(c) – and Opco also was able to increase the PUC of its shares in reliance on s. 84(1)(b) in an amount equal to the FMV of those contributed shares.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Adjusted Cost Base | shares issued to a Canadian parent in consideration for it issuing shares on a Delaware merger had a cost equal to such shares’ FMV/ shares transferred on absorptive merger at FMV | 903 |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(1) - Paragraph 84(1)(b) | permitted increase in PUC of shares of subsidiary to which a contribution of shares was made, equal to those shares’ FMV | 111 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition - Paragraph (k) - Subparagraph (k)(ii) | deposit of shares to voting trust arrangement was not a disposition | 40 |

| Tax Topics - General Concepts - Payment & Receipt | borrowing and payment of funds pursuant to an internal payment direction agreement | 49 |

27 October 2017 Internal T.I. 2017-0694231I7 - Subsection 247(2), surplus, and FAPI

Where, as a result of an s. 247(2) transfer pricing adjustment respecting a transaction between Canco and CFA for the sale of goods or provision of services, an amount is included in computing Canco’s income, would there would be an increase in the adjusted cost base (“ACB”) of Canco’s shares of CFA under s. 53(1)(c)? CRA stated:

Where transfer prices differ from arm’s length terms, it can generally be considered that a benefit is conferred on the person overcharging or underpaying for goods or services. However, there is no general rule in the Act that deems such a conferral of benefit to be a contribution of capital. In this regard, it is notable that paragraph 212.3(10)(b) has specific language to achieve such a result, but that rule is only applicable in the foreign affiliate dumping context. On this basis, it is our view that the benefit conferred in the situation described cannot be considered a capital contribution by Canco to CFA for purposes of paragraph 53(1)(c).

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) | s. 247(2) transfer pricing adjustment for sales undercharges to a CFA does not decrease the ES of the CFA | 166 |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(2) | effect on surplus balances of foreign transfer-pricing adjustment might be reversed under Reg. 5907(2) | 157 |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Earnings - Paragraph (a) | surplus could be adjusted by transfer-pricing adjustment | 140 |

26 May 2016 IFA Roundtable Q. 6, 2016-0642081C6 - German Organschafts

Under an “Organschaft,” a German parent (“Parentco”) and its German subsidiary (“Subco”) can enter into an agreement under which Subco agrees to annually transfer its entire profit determined in accordance with German (statutory) GAAP to Parentco, and Parentco agrees to compensate Subco for any loss incurred under German GAAP. CRA confirmed that, at least in the simple case where Parentco wholly-owns Subco through ownership of a single class of shares, the annual profit transfers will be deemed to be dividends under s. 90(2).

Under the base case scenario (where there is one class of shares wholly-owned by Parentco), CRA would view a profit transfer payment made by Parentco to Subco in respect of an accounting loss of Subco as being a contribution of capital made by Parentco to Subco for purposes of s. 53(1)(c). Such a payment would not be taken into account in computing the earnings, income or loss of either Subco or Parentco.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(2) | profit transfer payments by German sub to its German parent deemed to be dividends under s. 90(2) | 319 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(a) - Subparagraph 95(2)(a)(ii) - Clause 95(2)(a)(ii)(B) | profit transfer payments made by a German sub to German parent are s. 90(2) dividends not within s. 95(2)(a)(ii)(B) after 2016 | 153 |

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(x) | loss compensation payment under Organschaft | 123 |

1 December 2009 Internal T.I. 2009-0324951I7 F - Prix de base rajusté des actions d'une société

The individuals Shareholders of the Corporation incur capital expenditures respecting its Building. In indicating that there generally was an increase to the ACB of their shares, the Directorate stated:

[A] transaction that otherwise increases the capital of a corporation without any consideration being given by the corporation in respect of that increase may result in a contribution of capital … . For example, a contribution of capital occurs where a shareholder has fully paid for shares with no par value and subsequently agrees to make an additional contribution to the corporation (e.g., to remove a deficit or to provide funds for expansion, without the issuance of any additional shares). However, paragraph 53(1)(c) will apply only where a contribution of capital to a corporation by a taxpayer holding shares of the capital stock of the corporation results in an increase in the fair market value of the shares of the capital stock held by the taxpayer. …

[Here] the capital expenditures incurred by the Shareholders with respect to the Building constitute a contribution of capital to the Corporation. Accordingly, to the extent that such contribution would result in an increase in the fair market value of the shares held by the Shareholders in the Corporation, we would be of the view that paragraph 53(1)(c) would apply to provide for an increase in the ACB of such shares.

16 May 2005 Internal T.I. 2005-0119061I7 F - Montant d'aide-actions

Regarding a subscription for shares of its subsidiary by M Co, the Directorate stated:

If M Co pays more for the shares than their fair market value ("FMV"), it would be deemed by paragraph 69(1)(a) to have acquired them at that FMV. In that case, the reduction in the cost to M Co of acquiring the shares under paragraph 69(1)(a) could constitute a capital contribution by M Co for the purposes of paragraph 53(1)(c).

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(x) - Subpargraph 12(1)(x)(viii) | funding of film production company by shares rather than loan would not give rise to assistance | 181 |

| Tax Topics - Income Tax Act - Section 125.4 - Subsection 125.4(1) - Assistance - Paragraph (a) | conversion of loan that was taxable assistance into shares is not itself assistance] | 192 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) - Excluded Obligation - Paragraph (a) | conversion of loan that was taxable assistance under s. 12(1)(x) into shares with lower FMV would not give rise to forgiven amount | 304 |

| Tax Topics - Income Tax Regulations - Regulation 1106 - Subsection 1106(1) - Excluded Production - Paragraph (a) - Subparagraph (a)(iii) | transfer of all the revenues to a film implies a transfer of its copyright | 191 |

| Tax Topics - General Concepts - Ownership | transfer of the economic benefit of copyright entails transfer of its ownership | 149 |

5 December 2003 External T.I. 2002-0165195 - Debt Forgiveness in Foreign Affiliates

Canco is a corporation resident in Canada that has subsidiaries in the US and the UK. Canco has a US subsidiary ("CFA1"), which has US dollar non-interest bearing loans payable to Canco (the "CFA1 debt"). The CFA1 debt was used by CFA1 to acquire shares of CFA1's US subsidiaries which are also were CFAs and finance their active business operations.

A contribution of capital would be considered to occur that results in an addition to the adjusted cost base to Canco of its shares of CFA1 when the CFA1 debt is absolutely forgiven by Canco.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) - Commercial Debt Obligation | hybrid (active business/FAPI) debt is commercial debt obligation | 136 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 136 | |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(g.1) | 78 | |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Earnings | 63 | |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(2) - Paragraph 5907(2)(f) | forgiveness gain did not relate to active business items | 123 |

14 July 1999 External T.I. 9917685 - FOREIGN AFFILIATE EARNINGS COMPUTATION

When FAl (wholly-owned by Canco) makes a capital contributes of depreciable capital property with a fair market value of $200, and a cost of $100, to FA2, which is resident in the same foreign country and is wholly-owned by FA1, the adjusted cost base of the shares of FA2 held by FAl would be increased by an amount equal to the fair market value of the property transferred to FA2 (i.e. $200) pursuant to s. 53(1)(c).

92 C.R. - Q.28

Discussion of distinction between phrases "contribution of capital" and "contributed surplus"

The acquisition of par value shares at a price in excess of their par value does not entail a contribution of capital for purposes of s. 53(1)(c). Instead, the cost of the shares is determined on ordinary principles.

10 January 1992 CGA Roundtable, Q. 19, 7-912224

A corporation converts a debt owed to one of its shareholders, with whom it does not deal at arm’s length, to shares when the corporation is in a deficit position. The adjusted cost base of the shares received is reduced to their fair market value. Would this transaction be a contribution of capital that would increase the adjusted cost base of the shares issued pursuant to s. 53(1)? The Department responded:

The Department would consider that proportion of such part of the amount of the contribution as cannot reasonably be regarded as a benefit conferred by the shareholder on a related person (other than the corporation) to be a contribution of capital that would increase the adjusted cost base of the shares of a corporation pursuant to paragraph 53(1)(c) of the Act only if there was a real increase in the value of the shares of the corporation as a result of the conversion. Moreover… the value of the debt converted (rather than the principal amount) must be considered the amount paid to acquire the shares in determining whether the amount so paid exceeds the fair market value of the shares acquired for the purposes of paragraph 69(1)(a)… ..

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110.6 - Subsection 110.6(7) | 56 | |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) | 72 | |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(a) | FMV of debt rather than amount owing | 57 |

September 1991 Memorandum (Tax Window, No. 9, p. 7, ¶1444)

Where a corporation issues par value shares for cash in excess of their par value, the subscriber's ACB is computed by reference to the purchase price and other cost of acquisition, and s. 53(1)(c) has no application.

88 C.R. - Q.36 (p. 53:49)

[A] transaction that otherwise increase the capital of a corporation in respect of that increase may result in a contribution of capital for the purposes of paragraph 53(1)(c)....[A]n absolute forgiveness of debt owing by a corporation to a shareholder would be an example of such a transaction. The provisions of subsection 80(1) would, of course, apply to the forgivness.

The department's views on the posible effect of a contributon of capital on the adjusted cost base of the shares of a shareholder who makes the contribution are stated in question 68 of the 1987 Revenue Canada round table.

87 C.R. - Q.68 (p. 47:38)

To what extent would a contribution of capital to an insolvent corporation permit an increase in the cost of shares owned by the contributor under s. 53(1)(c)? What if the taxpayer instead purchases additional shares? The Department responded:

Provided that there is some increase in the value of shares of the corporation owned by the taxpayer as a result of a contribution of capital, the cost to the taxpayer of his shares...would, pursuant to paragraph 53(1)(c), be increased by that proportion of the amount of the contribution as may reasonably be regarded as pertaining to the shares of the corporation owned by him.

On a share subscription, any cost basis denied by s. 69(1)(a) may be treated as a contribution of capital provided there is some increase in the value of the taxpayer's shares.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(a) | 34 |

IT-456R "Capital Property - Some Adjustments to Cost Base," para. 2

A contribution of capital occurs where a debt owing by a corporation to a shareholder is absolutely forgiven.

Articles

Tremblay, "Contributions to Capital - Cost Basis", Canadian Current Tax, October, 1987, p. 1

A court might decide that the fraction is not intended to result in an unfair denial of a portion of an eventual loss, and is merely intended to allocate the bump. RC will generally permit a full basis bump provided that the contributing shareholder receives some value, albeit an unquantifiable one.

Paragraph 53(1)(e)

Subparagraph 53(1)(e)(i)

Administrative Policy

10 May 2017 External T.I. 2017-0687051E5 F - Addition to ACB of a partnership interest

Is an amount included in a corporation’s income under s. 34.2(2) added by virtue of s. 53(1)(e) to the adjusted cost base of its partnership interest? CRA responded:

[T]he amount included under subsection 34.2(2)… will not be included in the corporation's share of the partnership's income from any source. Therefore, for the purposes of subparagraph 53(1)(e)(i), there would be no addition to the ACB to the corporation of the partnership interest in an amount otherwise included in the income of the corporation under subsection 34.2(2).

Furthermore, there is no other provision in paragraph 53(1)(e) for adding, to the ACB of the partnership interest, the amount that would be included in computing the corporation's income under subsection 34.2(2).

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 34.2 - Subsection 34.2(2) | no partnership-interest ACB addition for inclusion | 57 |

2016 Ruling 2015-0617101R3 - 99(1) and timing of ACB adjustment

Background

LPco (a wholly-owned Canadian subsidiary of Parentco) acquired all the shares of GPco (holding all the Class “A” units of a Canadian limited partnership, namely, the “Partnership”) and all the Class “B” and “C” Partnership Units in the Partnership in an arm’s length transaction. Income or loss of the Partnership is annually allocated to the two partners in proportion to their Units. Partnership holds depreciable property used in a Canadian business and also appreciated shares of a subsidiary (Aco).

Proposed transactions

- LPco will transfer its Units to GPco under s. 85(1).

- Upon such transfer, Partnership will legally cease to exist and all its property will be distributed to GPco, and GPco thereupon and thereafter will carry on alone the Partnership business.

- GPco may make s. 98(5)(c) designations, e.g., for its Aco shares.

Rulings

Provided Partnership is a Canadian partnership at the time it ceases to exist and GPco continues to carry on the business of the Partnership, s. 98(5) will apply to the dissolution.

Pursuant to s. 99(1), Partnership’s fiscal period will be deemed to have ended immediately before the time that is immediately before the time Partnership ceased to exist. The income or loss of Partnership for its fiscal period so ended will, to the extent of a Partner’s share thereof, be included in computing the Partner’s ACB of its Partnership interest under s. 53(1)(e)(i) or 53(2)(c)(i). In particular: LPco’s share thereof will be included in determining its ACB of the LPco Partnership Interest immediately before its disposition to GPco; and GPco’s share thereof will be included in determining the ACB to GPco of the GPco Partnership Interest immediately before the time Partnership ceased to exist.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 98 - Subsection 98(5) | on a s. 98(5) wind-up, the ACB of the transferor partner’s interest is bumped by YTD income | 105 |

| Tax Topics - Income Tax Act - Section 99 - Subsection 99(1) | year ending with termination was final partnership year | 116 |

10 October 2014 APFF Roundtable Q. 22, 2014-0538161C6 - APFF Conference, Q. 22 - ACB of interests in a partnership

X Inc. and Y Inc. each hold "tracking units" in a Quebec general partnership ("SENC AB") which, in turn, holds the units of two subsidiary LPs ("SENC A," and "SENC B"). Their A and B units (which are held in different proportions) accord rights to the results of the investment in SENC A and SENC B, respectively. Would CRA consider that X Inc. and Y Inc. hold distinct interests in SENC AB and thereby have distinct ACBs for their A and B units? CRA responded (TaxInterpretations translation):

The CRA does not intend to change its long-standing position to the effect that an interest in a partnership constitutes a single and identical property irrespective whether the capital of the partnership has one or several classes of interest. Consequently, the ACB of the Class A units in the example submitted will not be distinct from the ACB of the Class B units.

1 October 2013 External T.I. 2013-0491571E5 - Partial disposition of partnership interest - ACB

Where a partner disposes of some of its units of a partnership during the year, is there an ACB adjustment for the entire amount of the income allocated to that partner for the fiscal period? After noting that "all of the units that a partner holds in a partnership constitute a single property, i.e. the partner's interest in the partnership" so that, for example, a disposition of "40% of its partnership units…constitutes a partial disposition of its partnership interest," CRA stated:

Where the partial disposition occurs during the fiscal period of the partnership and thus the ACB adjustment for that fiscal period is not reflected in the ACB of the partnership interest for purposes of computing the gain or loss on the partial disposition, it is our view that the ACB of the remaining partnership interest will be increased by that ACB adjustment. Accordingly, the partner would have an ACB adjustment for the entire amount of the income allocated to that partner for the fiscal period despite the partial disposition.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 43 - Subsection 43(1) | disposition of some partnership units a part disposition | 150 |

9 March 2012 External T.I. 2011-0416611E5 - disposition under paragraph 38(a.3)

CRA noted that since the pre-2013 version of s. 53(1)(e)(i)(A) did not explicitly say that the Act was to be read without reference to s. 38(a.3), there was no authority for adding exempt capital gains pursuant to that paragraph in determining the ACB of a partnership interest. (Such reference was added pursuant to the 2013 technical amendment bill.) CRA stated:

Where paragraph 38(a.1) or (a.2) of the Act applies to a donation by a partnership, clause ... 53(1)(e)(i)(A) of the Act ensures that the exempt gains on such a disposition will be added to the ACB of a partner's interest in that partnership and will not be taxed subsequently on a later disposition of that partnership interest.

15 December 2010 External T.I. 2009-0349911E5 F - Calcul du PBR d'une participation dans une SEC

CRA affirmed its position as follows:

… Income Tax Technical News No. 5 … states, in accordance with subparagraph 53(1)(e)(i), that in computing the adjusted cost base of a member's interest in a partnership at a particular time, only the income or loss of the partnership for fiscal periods already ended will be taken into account at that time.

Accordingly, the distribution in the year of a capital gain realized in the year by an LP triggered a negative ACB gain to a limited partner with a modest “outside” basis.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(3.1) | withdrawal equalling capital gain realized in year by LP triggered negative ACB gain to limited partner | 204 |

15 July 2008 External T.I. 2008-0275471E5 F - Société de personnes/Ajustement au PBR

CRA indicated that until the amendment to s. 99(1) was passed, it intended to apply the law so that the income or loss of a partnership for its last taxation year before its dissolution would be taken into account in calculating the partnership interest.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 99 - Subsection 99(1) | CRA was prepared to rule to avoid double taxation problem prior to the s. 99(1) amendment | 173 |

10 January 2008 External T.I. 2007-0227191E5 F - REVENUS D'UNE SOCIÉTÉ DE PERS. - PART PRIVILÉGIÉE

In connection with a query on the implications of holding a preferred unit in a partnership, i.e., a unit that confers on its holder a preferred share of the partnership's profits or losses, CRA stated:

The total of the units held by a partner in a partnership constitutes a single property which is the partner's interest in the partnership. The aggregate of these units is therefore assigned an adjusted cost base (ACB) under the Act. The characterization of the taxpayer's shares into preferred and common units does not result in the creation of separate properties, but is merely a means of sharing the profits and losses of the partnership.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 103 - Subsection 103(1) | common and preferred units can be used as a mechanism for profits to be allocated to each partner’s interest (a single property) | 185 |

29 October 2002 External T.I. 2002-014633

When presented with a situation where a taxpayer retired from a partnership on September 30, 2001 and at December 31, 2001 had a residual interest in the partnership with a negative ACB, CCRA noted that where the problem was not one of double taxation but rather, of the timing of the adjustment to the ACB of the taxpayer's partnership interest (which, in this instance, would result in a capital gain in 2001 and a capital loss in 2002). Accordingly, the administrative relief discussed in Income Tax Technical News Nos. 5 and 9 would not be available.

15 April 2003 External T.I. 2002-0139305 F - Immigration

At the time of Mr. X’s immigration in 1988, he held an interest in a US rental property partnership (with no debt) which he had acquired in 1983 at a cost of US$300,000 and which had an FMV of Cdn.$650,000 at the time of his immigration. After immigration, he invested an additional Cdn.$50,000 in the partnership, which funded building additions. In 2001, the partnership sold the building at a capital gain of $300,000. The net income of the partnership was always nil and no tax depreciation was claimed.

CCRA indicated that Mr. X would be allocated his share of the capital gain – but that since the ACB of his partnership interest was increased to FMV under former s. 48(3) on his immigration and further increased by his capital contribution and his share of the capital gain, he would realize a capital loss on the partnership winding-up.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 128.1 - Subsection 128.1(1) - Paragraph 128.1(1)(c) | ss. 128.1(1)(b) and (c), unlike former s. 48(3), apply also for CCA/recapture purposes | 163 |

| Tax Topics - Income Tax Act - Section 126 - Subsection 126(1) | FTC can be generated where recapture of depreciation, and denied capital loss, are realized on a US rental building | 67 |

20 September 2000 External T.I. 2000-0043435 F - Associé quittant société de personnes

Regarding whether certain adjustments to the adjusted cost base of a partnership interest held by a partner who withdrew from the partnership during a fiscal period of the partnership would be considered, CCRA stated that when it comes to determining whether it should make certain adjustments to the adjusted cost base of a partnership interest in order to avoid double taxation on a completed transaction, “the decision is first made by our Tax Services Offices following a review of all the facts and documents, which is generally done as part of an audit engagement.”

30 November 1997 Ruling 9803733 - TIMING OF ADJUSTMENTS TO PARTNERSHIP ACB.

Where a limited partner leaves the partnership before the year end, so that s. 98.1(1)(b) deems the retired partner not to have disposed of its residual interest until the end of that fiscal period on the basis that it only receives payment for its partnership interest after it ceased to be a member, RC will treat the ACB of the disposed partnership as having been increased by the income for that year that is allocated to the partner.

Income Tax Technical News, No. 9, 10 February 1997

In the Technical News No. 5, dated July 28, 1995, we mention that in computing the adjusted cost base (ACB) of a partner's partnership interest at a particular time, only the partnership's income or loss for fiscal periods ending before that time will be taken into account. ..

… In circumstances where there is a possibility of double taxation, we are prepared, in the context of a ruling request, to apply the law in a manner such that a taxpayer is not taxed twice on the same amount. For example, if a partner dies or leaves the partnership, we may consider certain adjustments in situations where double taxation arises.

The Department of Finance agrees with our position and is currently reviewing the relevant provisions of the law to establish if legislative amendments are necessary.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Other Legislation/Constitution - Federal - Indian Act - Section 87 | 30 | |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Subparagraph 212(1)(b)(vii) | events must be beyond borrower's control | 79 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | loss transfer must be to affiliated person - related not enough | 50 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | 71 | |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(c.3) - Subparagraph 88(1)(c.3)(ii) | 159 | |

| Tax Topics - Income Tax Regulations - Regulation 4900 - Subsection 4900(12) | 71 |

Income Tax Technical News, No. 5, 28 July 1995

For fiscal periods ending after 28 July 1995, the adjustments to the ACB of a partnership interest in respect of the income or loss of the partnership will be made in accordance with s. 53(1)(e)(i) or 53(2)(c)(i).

27 May 1994 External T.I. 9407285 - PARTNERSHIP - GENERAL

Where an investment partnership provides that a partner who redeems his units partway through the year for their current fair market value shall have taxable income or capital gains allocated to him based on the appreciation in his units to the date of redemption, a partner who redeems a portion of his units partway through the year will be considered to have disposed of a portion of his partnership interest giving rise to a capital gain that will not reflect the addition under s. 53(1)(e)(i) to the adjusted cost base of his remaining partnership interest of the redemption-related allocation of income.

7 June 1991 T.I. (Tax Window, No. 7, p. 9, ¶1366)

Where a partnership is wound-up under s. 98(5), the last fiscal period of the partnership will be considered to have ended immediately before the determination of the ACB of the partnership interests even though both times are "immediately before" the partnership ceasing to exist.

11 March 1991 T.I. (Tax Window, No. 1, p. 5, ¶1155)

Where a corporation which has withdrawn from a partnership has the right to receive the amount in its capital account over time plus interest thereon, the interest will not represent a share of the partnership's income or capital, and will not be added to the ACB of the corporation's partnership interest.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | 49 |

18 April 1990 T.I. (September 1990 Access Letter, ¶1425)

Where B disposes of its partnership interest to the other partner, A, with the result that the partnership ceases to exist, B's share of the partnership profits for the fiscal period that is deemed (by virtue of s. 99(1)) to end immediately before that time will be included in the ACB of B's interest. However, this adjustment will not occur if B disposes of its partnership interest to C. Where B maintains the right to receive a nominal amount of partnership property, RC will question whether this amounts to a residual interest for purposes of s. 98.1 so that B will obtain the appropriate basis adjustment with respect to the second situation.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 98 - Subsection 98(5) | 56 |

88 C.R. - Q.22

Where the accrued gain on the partnership assets is equal to the accrued gain on the partnership units, RC accepts that the gain which the partnership realizes on the dissolution of the partnership as a result of the application of s. 98(2) is added to the ACB to the partner of his partnership units so that a partner realizes no further gain on the disposition of his partnership interest.

Articles

Margaret D. Paproski, "Partnership Interests and Negative ACB", Business Vehicles, Vol. VI, No. 3, p. 257.

Peter Lee, "Dissolution of Partnership - Calculation of Adjusted Cost Base of Partnership Interest", Business Vehicles, Vol. V, No. 4, 1999, p. 273.

Rinfret, "A Review of the AEC Pipelines Limited Partnership", 1997 Corporate Management Tax Conference Report, c. 7

Discussion of Revenue Canada's policy on timing of adjustments to ACB of partnership interests.

Subparagraph 53(1)(e)(iii)

Administrative Policy

9 March 1992 T.I. (Tax Window, No. 17, p. 3, ¶1789)

Re consequences where the partnership is the beneficiary of a life insurance policy in one of the three individual partners; or where the deceased partner's estate will receive all the insurance proceeds.

In the latter case, the ACB of the deceased partner cannot be increased because he is deemed to dispose of his partnership interest immediately before his death and is not a partner at the time the proceeds are received.

3 December 1991 T.I. (Tax Window, No. 15, p. 4, ¶1673)

Where all the partners of a partnership are corporations the partnership carries life insurance on the individuals who were the voting shareholders of the partners, and the corporation owned by a deceased shareholder receives all the proceeds of the life insurance policy in satisfaction of its interest in the partnership, it is only the ACB of that corporation's interest in the partnership that is increased.

16 November 1990 T.I. (Tax Window, Prelim. No. 2, p. 8, ¶1052)

Where the partnership agreement provides for an income allocation to the retiring partner in the year of death equal to the life insurance proceeds received by the partnership, s. 96(1.1) will apply to include the amount of the allocation in the deceased partner's estate's income and the ACB of the partnership interest of the remaining partners will be increased under s. 53(1)(e)(iii).

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 96 - Subsection 96(1.1) | 64 |

84 C.R. - Q.25

Where the partnership agreement provides that net life insurance proceeds will be allocable solely to the deceased partner and will be used to pay the estate of the deceased for the partnership interest, no adjustment is possible with respect to the deceased's former interest in the partnership, as the deceased is no longer a partner at the time the proceeds are received.

Subparagraph 53(1)(e)(iv)

See Also

Mitchell v. R., [1996] 2 CTC 2659, 97 DTC 607

The guarantee by the partnership of various obligations of a limited partnership of which he was a member did not form part of the adjusted cost base of his interest in the partnership given that there was not a clearly enforceable right against the taxpayer as surety (the taxpayer had filed a lengthy statement of defence in response to a claim made against him under the guaranty) and given that any amounts evidently paid by him pursuant to the guarantee would be paid to a third party (Central Guarantee Trust Company) rather than to the partnership. The sum in question also did not represent an obligation of the partnership assumed by the taxpayer.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(14) | 49 | |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | set-off | 130 |

Administrative Policy

27 June 2016 External T.I. 2016-0637341E5 F - Partnerships - Negative ACB

Rather than making current distributions of its cash flow to a limited partner, those sums are lent by the LP to the limited partner – then at the beginning of the following year the LP effects a distribution of the applicable share of the previous year’s profits to the limited partner by issuing a demand note to it and pays that note by way of set-off against the loans owing by the limited partner. After finding that the loans might have given rise to an immediate gain under s. 40(3.1), CRA went on to state:

[T]he profits of a limited partnership in a situation such as that described would not be considered as contributions of capital for the purposes of subsection 40(3.13). …

The concept of a contribution of capital to a general partnership (SENC) or limited partnership is not limited to what is mentioned in…your letter. For example, the CRA considers that the assumption by a partner of a partnership debt can constitute a form of contribution of capital.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(2) - Paragraph 53(2)(c) - Subparagraph 53(2)(c)(v) | loan advances to a limited partner may give rise to immediate s. 53(2)(c)(v) grind | 261 |

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(3.1) | loans by LP to partner potentially gave rise to negative ACB gain | 164 |

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(3.13) | retention of partnership profits not a contribution | 146 |

2016 Ruling 2016-0651621R3 - Partnership carried on by sole proprietor

A partnership was wound-up under s. 98(5) as a result of the limited partner transferring its interest under s. 85(1) to the general partner. Immediately before this happened, the general partner assumed a debt that was owing to it by the partnership, with the result that the debt was extinguished by operation of law.

CRA ruled that the ACB of the general partner’s interest for s. 98(5) purposes was increased by the amount of such assumed debt, and that a forgiven amount did not arise on the extinguishing of the debt.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 98 - Subsection 98(5) | the assumption by a partner of a debt owing to it by a partnership bumped the partner’s ACB | 198 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) - Forgiven Amount - Element B - Paragraph B(a) | no forgiven amount where partner assumed debt owing to it by partnership | 48 |

25 April 2013 Internal T.I. 2013-0478511I7 F - Distribution à un commanditaire

After addressing the usual case where a capital gains distribution by a limited partnership (“SEC”) would be respected as such for ITA purposes, but also noting that “where it can be concluded that the amounts paid by SEC to the Limited Partner are in return for services rendered, it would be possible at that time to consider the inclusion of such amounts in computing the partner's business income pursuant to subsection 9(1) to the extent that the services are provided by the Limited Partner in the course of carrying on a business that is separate from the business operated by the SEC,” CRA then stated:

Otherwise, the fair market value of any service contribution by the Limited Partner would be added to the ACB of its partnership interest.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Real Estate | real estate capital gains flowed through to limited partner retained character | 226 |

| Tax Topics - Income Tax Act - Section 96 - Subsection 96(1) - Paragraph 96(1)(f) | allocated capital gains retained their character unless re services performed by partner in course of separate business | 398 |

| Tax Topics - Excise Tax Act - Section 272.1 - Subsection 272.1(1) | distinction between return on partnership investment and services rendered by partner in the course of a separate business | 295 |

8 October 2010 Roundtable, 2010-0373371C6 F - Souscription des unités d'une SEC

The 100 units of a limited partnership (LP), which on an FMV basis has a deficit of $108,000 (i.e., liabilities of $110,000 and assets of $2,000), are held as to 99 and 1 by Partner Inc. and its wholly-owned subsidiary GP Inc., respectively. In order to pay off the bank debt, Partner Inc. subscribes for 100 units of LP for $100,000, so that such debt is discharged and the deficit reduced to $8,000.

(a) Does such subscription represent an acquisition of property by Partner Inc. for purposes of s. 69(1)(a), or is it a "contribution of capital" for s. 53(1)(e)(iv) purposes?

(b) If s. 69(1)(a) so applies, would the difference between the cost of acquiring the additional 100 units and their FMV, i.e., $100,000, be a "contribution of capital" for s. 53(1)(e)(iv) purposes?

CRA responded:

[W]e believe that the partner, in consideration for the $100,000 payment, acquired a greater interest in the partnership by acquiring part of a property. We believe that subsection 69(1) could apply to the acquisition of part of a property, especially since the wording of that provision uses the word "anything".

In this case, to the extent that Partner Inc. has not conferred a benefit on GP Inc. by subscribing for LP units, if the units issued have a value that is less than their issue price, that value (in this case $0), determined in accordance with paragraph 69(1)(a), will be added to the cost of the units. The difference between the amount paid and the value of the units will be added to the ACB of the interest pursuant to paragraph 53(1)(e)(iv).

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(a) | subscription for units of an underwater LP represented an acquisition whose deemed cost was nil | 217 |

3 October 2007 External T.I. 2007-0230671E5 F - Paragraphe 12 du IT-338R2

CRA confirmed that the following statement from IT-338R2, para. 12 continues to represent its position, notwithstanding the archiving of the Bulletin:

To the extent the former partner has assumed the liabilities of the partnership, that former partner is considered to have made a contribution of capital to the partnership immediately before the partnership ceases to exist. For purposes of subparagraph 98(5)(a)(i), this results in an increase to the ACB of the former partner's interest in the partnership under subparagraph 53(1)(e)(iv).

2000 Ruling 2000-0028423 - partnership dissolution under 98(3)

On a winding-up of a partnership, "for the purposes of determining the ACB to each Partner of that Partner's interest in the Partnership for the purposes of subsection 98(3), the Partner's share of the net income of the Partnership for the fiscal period that commenced on XXXXXXXX and will end immediately before 'that time' will be added to the ACB of that Partner's interest in the Partnership as of the time immediately prior to 'that time' pursuant to subparagraph 53(1)(e)(i)".

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(1) - Paragraph 53(1)(e) - Subparagraph 53(1)(e)(iv) | 38 | |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Real Estate | capital property retained that character on s. 98(3) wind-up | 43 |

| Tax Topics - Income Tax Act - Section 98 - Subsection 98(3) | 0% undivided interest | 38 |

2000 Ruling 2000-0028423 - partnership dissolution under 98(3)

In determining the ACB to a partner of its interest in a partnership for the purposes of s. 98(3), that ACB will be increased by liabilities of the partnership assumed by the partner immediately before that time.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(1) - Paragraph 53(1)(e) - Subparagraph 53(1)(e)(iv) | 82 | |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Real Estate | capital property retained that character on s. 98(3) wind-up | 43 |

| Tax Topics - Income Tax Act - Section 98 - Subsection 98(3) | 0% undivided interest | 38 |

29 June 2000 External T.I. 1999-0011495 - ACB Partnership Interest

Where a debt owing to a partner is converted into capital, the amount of such "contribution" and, therefore, the quantum of the resulting increase in ACB of the partner's interest, will be a question of fact.

4 June 1992 T.I. 920847 (December 1992 Access Letter, p. 34, ¶C245-044)

Where, in connection the dissolution of a partnership under s. 98(3) and the recontribution of the property to a new partnership under s. 97(2), a partner borrows money to make a contribution to the old partnership immediately before its dissolution and receives a corresponding distribution of capital shortly after the formation of the new partnership, GAAR will be applied so as to prevent this avoidance of a capital gain on the dissolution of the partnership.

89 C.R. - Q.35

Where one of the partners of a two-person partnership retires or dies, the continuing partner who has assumed the liabilities of the partnership will be treated as having made a contribution of capital to the partnership immediately before the partnership ceased to exist.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 98 - Subsection 98(5) | 28 |

89 C.M.TC - Q.8

where a limited partner has assumed partnership debt as part of the consideration given for the acquisition of his partnership interest, the debt assumed will increase the ACB of his interest.

IT-338R "Partnership Interests - Effects on Adjusted Cost Base Resulting from the Admission or Retirement of a Partner"

Where on a dissolution of a partnership to which s. 98(5) applies the continuing partner has assumed the liabilities of the partnership, that partner is considered to have made a contribution of capital to the partnership, with the result that the ACB of his interest would be increased pursuant to s. 53(1)(e)(iv).

IT-471R "Merger of Partnerships" under "Work in Progress"

The ACB of each partner's interest in a partnership immediately before a distribution of undivided interest pursuant to s. 98(3) will include the partner's proportion of the partnership liabilities assumed by the partners on the dissolution of the partnership.

Subparagraph 53(1)(e)(vi)

Administrative Policy

15 August 2024 External T.I. 2024-1031811E5 - ACB of partnership interest - 53(1)(e)(vi)

2009-0349911E5 dealt with a limited partnership (“LP”) which, in February 2008, realized a capital gain, of which $100,000 was allocable to a limited partner, whose interest had an ACB at the beginning of the (calendar) 2008 fiscal period of LP of $10,000. $100,000 was withdrawn by the limited partner in March 2008, producing a negative ACB gain of $90,000. CRA indicated that this negative ACB gain was added back to that negative ACB, so as to increase the ACB to nil “as at December 31, 2008”, and that the capital gain allocated to the limited partner increased the ACB of its interest to $100,000 on January 1, 2009.

When now asked about this, CRA effectively acknowledged that the quoted date of the ACB increase pursuant to s. 53(1)(e)(vi) was incorrect, and that “the addition of $90,000 under subparagraph 53(1)(e)(vi) should be made on January 1, 2009.”

Subparagraph 53(1)(e)(viii)

Administrative Policy

Income Tax Technical News, No. 12 under "Meals and Beverages at Golf Clubs"

"Amounts referred in subparagraph 53(1)(e)(viii) will not increase the ACB of the partner's interest in the partnership until after the end of the relevant fiscal period of the partnership." However, where a partnership is dissolved under s. 98(3) there will be a timely adjustment under s. 53(1)(e)(viii) provided that a fiscal period of the partnership ends after the distribution of partnership assets to the partner and prior to the partnership interest being disposed of by the partner on dissolution of the partnership.

8 September 1997 External T.I. 9642025 - ACB OF PARTNERSHIP INTEREST - RESOURCE CONTEXT

In considering a situation where all the assets of a resource partnership are distributed on a pro-rata basis to the partners without an election being made under s. 98(3), RC indicated that "amounts referred to in subparagraph 53(1)(e)(viii) of the Act will not increase the ACB of the partner's interest in the partnership until after the end of the relevant fiscal period of the partnership". However, a favourable result would still obtain if the fiscal period of the partnership ends after the distribution of partnership assets to the partner and prior to the partnership interest being disposed by the partner on dissolution of the partnership.

94 C.P.T.J. - Q. 4

Re whether there is a timely adjustment to the partners' ACB where there is a pro-rata distribution of resource properties of a partnership immediately prior to its dissolution.

Paragraph 53(1)(f)

Administrative Policy

7 October 2022 APFF Financial Strategies and Instruments Roundtable Q. 4, 2022-0940941C6 - Stop-loss Rules

On March 15, 2022, an individual disposes of all of his shares (being 2,000) of ABC Pubco, and realizes a capital loss of $10,000. On March 16, 2022, his spouse acquires 2,000 shares of ABC Pubco. In addition, his RRSP had acquired 1,000 shares of ABC Pubco on March 10, 2022. Finally, the individual acquires 500 shares of ABC Pubco on April 13, 2022.

CRA noted that since the number of substituted properties on hand at the end of the period beginning 30 days before and ending 30 days after the disposition of the shares to the taxpayer or an affiliated person was greater than at the time of the disposition, the formula (Deemed nil loss = (the lesser of S, P and B) / S x L) referred to in some CRA positions was inapplicable (i.e., the full $10,000 loss was denied).

In then addressing the question of how the denied loss should be allocated to the replacement shares pursuant to s. 53(1)(f), CRA stated that, in accordance with IT-456R, para. 12, the superficial loss should be determined as if all the affiliated persons involved were one person, and then prorated on the basis of all the substituted properties held by each person at the end of the period.

Consequently, the $10,000 superficial loss would be allocated in proportion to the fractions 1000/3500, 2000/3500 and 500/3500 to increase the ACB of the 1,000 shares acquired by the RRSP, the 2,000 shares acquired by the individual’s spouse and the 500 shares acquired by the individual, respectively.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(3.3) | suspended loss rules engaged by shareholder, and shareholder’s RRSP acquiring and then holding identical shares during the 61-day period | 107 |

| Tax Topics - Income Tax Act - Section 54 - Superficial Loss | formula for prorating superficial loss is inapplicable where the number of shares held by affiliated persons has increased at the end of the 61-day period | 239 |

Paragraph 53(1)(f.1)

Administrative Policy

31 March 2016 External T.I. 2014-0524391E5 F - Debt parking

A corporation disposes of debt of a subsidiary at a substantial loss to another corporation which is related to it (and the subsidiary) by virtue only of s. 251(5)(b). The loss nonetheless is denied by s. 40(2)(e.1) and added to the adjusted cost base of the debt in the acquirer’s hands under s. 53(1)(f.1). However, the debt parking rule in s. 80.01(8) also applies to the acquisition, and deems that debt to be settled for an amount equal to its ACB to the acquirer.

CRA considered that the debt forgiveness rules could thereby apply to the debt because the deemed settlement under s. 80.01(8) occurs at the time of the acquisition, whereas the s. 53(1)(f.1) bump to the acquirer’s ACB occurs only immediately after that time

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80.01 - Subsection 80.01(8) | debt parking rule can apply even if no capital loss is recognized/ applies before s. 53(1)(f.1) add-back | 154 |

12 September 1990 T.I. (Tax Window, Prelim. No. 1, p. 10, ¶1016)

Where a non-interest-bearing debt is transferred at a loss between two corporations controlled by the same person, the loss will be added to the cost amount of the debt to the transferee corporation unless the transferor owns shares of the transferee immediately after the disposition of the debt.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(2) - Paragraph 40(2)(g) - Subparagraph 40(2)(g)(ii) | 67 |

16 February 1990 T.I. (July 1990 Access Letter, ¶1320)

Where a wholly-owned subsidiary transfer shares, which are capital property to it, at a loss to its parent which thereafter holds the shares as inventory, the s. 53(1)(f.1) adjustment will not be available to the parent.

2014 Ruling 2013-0514191R3 - Debt restructuring, forgiveness and winding-up

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Principal Amount | non-application of s. 39(2) to exchange of U.S.-dollar notes | 142 |

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(2) | s. 51.1 exchange of U.S.-dollar notes | 142 |

| Tax Topics - Income Tax Act - Section 51.1 | s. 51.1 exchange of U.S.-dollar notes | 142 |

| Tax Topics - Income Tax Act - Section 80.01 - Subsection 80.01(4) | s. 51.1 exchange of U.S.-dollar notes and ATR-66 debt slide | 430 |

Paragraph 53(1)(h)

Administrative Policy

3 May 2010 Internal T.I. 2010-0359631I7 F - Dépenses liées à une résidence non habitée

Following the death of their mother, two adult sisters inherited a property, for which expenses for property taxes, maintenance and insurance were incurred between the date of death and the property’s sale. The property was unoccupied during this period. Could such expenses be added to the adjusted cost base of the property under s. 53(1)(h)?

The Directorate indicated that s. 53(1)(h) was unavailable because the property did not come within the definition of land in s. 18(3) (i.e., there was a building), and then stated:

Where property taxes are not deductible in computing a taxpayer's income from land by virtue of either paragraph 18(1)(a) or paragraph 18(1)(h), the amount of such property taxes cannot be included by virtue of paragraph 53(1)(h) in computing the adjusted cost base of the land.

On the other hand, the cost of a property may include legal fees, commissions, brokerage fees, and any other expenses that were incurred directly in connection with the acquisition of the property or that were incurred for the purpose of disposing of the property.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Adjusted Cost Base | property taxes not added to ACB of inherited property before its sale | 133 |

88 C.R. - Q.68

Where money borrowed to buy land cannot be related to particular parcels, the interest should generally be allocated to all land held during the year in proportion to the cost of each parcel.

Paragraph 53(1)(j)

Administrative Policy

9 February 2010 Internal T.I. 2009-0333571I7 F - Paragraphe 7(1.5) - contrepartie reçue

Employees of a Canadian-controlled private corporation then exercised their options to acquire shares of their employer (Corporation A), and then sold such shares to Corporation B (which became the parent of Corporation A) for a U.S.-dollar purchase price, of which a specified portion was paid in Corporation C shares (the parent of Corporation B) as stated consideration for a specific number of Corporation A shares determined in accordance with the sale Agreement, and the balance was paid in cash. Corporation A intends to report on each employee's T4 slip a benefit based on a s. 7 amount for the cash sale (and with Part I tax being withheld and remitted accordingly), but not regarding the share exchange portion, which it treated as coming within s. 7(1.5). The disclosure to the employees indicated that the adjusted cost base of their shares was increased not only by this immediate s. 7 benefit, but also by the stock option benefit regarding the exchange which had been deferred under s. 7(1.5).

After agreeing with the taxpayers that the s. 7(1.5) rollover was available regarding the share exchange, the Directorate also stated its agreement with this ACB calculation, stating:

Paragraph 53(1)(j) adds to the ACB of the shares that each employee acquired under a stock option the amount of the benefit that the employee is deemed by subsection 7(1) to have received in respect of the acquisition of the shares. In addition, in the case of a security issued after February 27, 2000, paragraph 53(1)(j) allows the amount of the benefit that is deferred from being recognized in the employee's income under subsection 7(1.1) to be added to the ACB.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(1.5) | s. 7(1.5) rollover where employees exchanged specific s. 7(1.1) shares for shares of grandparent, even though they also received cash and PUC distribution | 454 |

| Tax Topics - Income Tax Act - Section 116 - Subsection 116(1) | s. 116 certificate required even for shares disposed of under s. 7(1.5) rollover | 283 |

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(1.4) | non-resident ex-employees will be required to recognize s. 7 benefit deferred by s. 7(1.5) when they dispose of the shares acquired in exchange | 148 |

18 August 2005 External T.I. 2005-0126131E5 - Section 7 Benefit - ACB of CCPC Shares

The ACB addition under s. 53(1)(j) for shares of a CCPC acquired by an employee under a s. 7(2) trust would occur at the time that the trust acquires the shares for the benefit of the employee even though the recognition of that s. 7 benefit is deferred under s. 7(1.1).

Paragraph 53(1)(n)

Administrative Policy

7 October 2011 Roundtable, 2011-0411971C6 F - Appraisal Fees Deductibility

Before indicating that appraisal fees incurred for revaluing capital property, in order to prepare annual financial statements in accordance with IFRS, generally are deductible under s. 9, CRA stated:

[I]n general, the reasonable expenses incurred by a taxpayer in valuing capital property for the purpose of its acquisition or disposition are an addition to the adjusted cost base of that property by virtue of 53(1)(n).

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Improvements v. Repairs or Running Expense | deductible appraisal fees to revalue fixed assets in accordance with IFRS | 109 |

Subsection 53(2) - Amounts to be deducted

Paragraph 53(2)(b)

Administrative Policy

2003 Ruling 2002-0174703 - Foreign Affiliate Reorganization

A great-grandchild foreign subsidiary ("Dco") of a Canadian public corporation ("Aco") and a great-grandchild foreign subsidiary of Aco ("Fco") held through another chain of corporations each hold ownership interest ("quota") in another foreign affiliate of Aco ("Eco"). The two quota holders of Eco agree that the principal assets of Eco will be assigned to a newly-incorporated corporation in the same foreign jurisdiction ("Jco") for no consideration; but that contemporaneously with the creation of Jco and the assignment of property of Eco to Jco, the capital account and retained earnings of Eco will be reduced and added to the capital and retained earnings of Jco (which is owned by Dco and Fco in the same proportions as they owned, and continue to own, Eco).

S.53(2)(b) will apply to reduce the adjusted cost base of the Eco quota held by Dco after the reorganization by an amount equal to the fair market value of the Jco quota received by Dco on the reorganization.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | 132 | |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | 162 |

Paragraph 53(2)(c)

Administrative Policy

27 March 2013 External T.I. 2012-0449661E5 F - Subparagraph 53(2)(c) ITA

In response to a query as to “the effect of the application of subsections 40(3.4) and 112(3.1) on the calculation of the adjusted cost base of an interest in a partnership … where the partnership disposed of shares of a corporation at a loss to an affiliated corporation” and “in the years prior to the disposition, the corporation whose shares were disposed of paid dividends on its shares to the partnership,” CRA indicated that this appeared to be a situation currently under audit, so that it could not comment.

10 January 2005 External T.I. 2004-0075931E5 - adjusted cost base - partnership interest

An amount of foreign non-business income tax allocated by a partnership to a partner and deducted by the partner under s. 20(12) will not result in a reduction to that partner's adjusted cost base of its partnership interest.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(12) | no partnership ACB reduction for partner s. 20(12) deduction | 190 |

Subparagraph 53(2)(c)(i)

Administrative Policy

29 August 2007 Internal T.I. 2007-0219931I7 F - Perte sur taux de change - société de personnes

Canco and a US resident who each held a 50% interest in a US partnership each advanced US$1 million to the partnership and then converted those advances to partnership units at a time that the Canadian dollar had depreciated (from a 1.2 to 1.4 exchange rate) relative to the exchange rate at the time of advance. CRA found that such conversion generated a capital loss to the partnership of $400,000 under s. 39(2) of which $200,000 was allocated to Canco, and that Canco realized a capital gain of $200,000 on its disposition of the advance.

Although Canco acquired an addition to the cost of its partnership interest equaling its proceeds of disposition, the ACB of its interest was reduced by the $200,000 capital loss allocated to it, so that the net effect was no change in the ACB of its overall interest in the partnership.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(2) | s. 39(2) gain to partnership when USD advance owing by it is converted to units | 90 |

Income Tax Technical News, No. 5, 28 July 1995

For fiscal periods ending after 28 July 1995, the adjustments to the ACB of a partnership interest in respect of the income or loss of the partnership will be made in accordance with s. 53(1)(e)(i) or 53(2)(c)(i).

Clause 53(2)(c)(i)(B)

Administrative Policy

13 January 2009 External T.I. 2008-0296981E5 F - Ajustement au PBR d'une participation

A taxpayer who invested $30,000 in a farming limited partnership was thereafter allocated farm losses for the partnership’s first two taxation years of $25,000, then $75,000, but with the taxpayer limited to a deduction of $8,750 by s. 31. CRA stated:

Under clause 53(2)(c)(i)(B) … the ACB of an interest in a partnership must be reduced by … farm losses without regard to section 31.

… The ACB of the taxpayer's interest would therefore be reduced by $75,000 even though the taxpayer has an unused restricted farm loss of $57,500.

The Act does not allow the unused restricted farm loss to be deducted against the deemed capital gain pursuant to subsection 40(3.1).

Subparagraph 53(2)(c)(v)

Cases

Tesainer v. Canada, 2009 DTC 5749, 2009 FCA 33

Damages received by the taxpayers who were limited partners of a former partnership ("Fenix") from lawyers, as a result of their claim (along with that of the general partner of Fenix on behalf of Fenix) for losses sustained by them as a result of negligent advice by the lawyers (which resulted in the complete loss of the capital of Fenix) were found to have been received by them directly, rather than as a distribution of partnership capital, as alleged by the Crown. Accordingly, such receipt did not give rise to a capital gain to them under s. 98(1)(c) (on the basis that the supposed distribution would have resulted in a negative cost base for their investment in the partnership).

Sharlow, J.A. stated (at para. 17) that the surrogatum principle did not apply as "the settlement payment in this case cannot be said to have replaced a distribution of partnership capital because, as a matter of law, it did not and could not have discharged any claim of the individual plaintiffs against Fenix much less a claim for distribution of partnership capital" and noted (at para. 19) that if the action against the lawyers had instead been settled by the payment of an amount to Fenix, the amount received by Fenix would first have been required to be applied to settle outstanding claims of creditors of Fenix, which did not occur as the amounts were received directly by the taxpayers.

Stursberg v. The Queen, 93 DTC 5271, [1993] 2 CTC 76 (FCA)

The other partners of the partnership consented to a reduction in the taxpayer's partnership interest from 40% to 15%, and to an increase in the partnership interest of a corporation ("WBG") of which he had voting control from 10% to 35%. WBG deposited the sum of $162,500 (representing 25% of the fair market value of the partnership assets) to the partnership, the taxpayer at the same time received a cheque for $162,500 from the partnership, and an amount of $269,812 representing 25/40ths of the taxpayer's 40% share of the partnership losses was transferred in the books of the partnership from the taxpayer to WBG.

Hugessen J.A. found that the payment of $162,500 to the taxpayer did not represent a distribution of capital to the taxpayer for purposes of s. 53(2)(c)(v) "because there [was] no change whatever in the corpus of the partnership capital or in the relative interests therein of any of the other partners" (p. 5275). Instead there was a partial disposition of the taxpayer's partnership interest to WBG, thereby giving rise to a capital gain.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | partial disposition of partnership interest to a related corporation, even though proceeds run through the partnership | 114 |

See Also

Tesainer v. The Queen, 2008 DTC 2807, 2008 TCC 101, rev'd 2009 FCA 33

Damages received by the taxpayer who, along with other partners of a real estate partnership, received damages from the law firm which had handled the private placement of the partnership units, were found to be closer in character to a return of capital rather than something else.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | 70 |

Administrative Policy

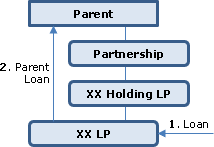

2023 Ruling 2022-0938261R3 - XXXXXXXXXX program secured financing

Background

Parent, a taxable Canadian corporation, can borrow on more favourable terms if it does so, through a special purpose bankruptcy-remote entity (“XX LP”) rather than directly.

Proposed transactions

Parent and a “subsidiary” general partnership of Parent (“Partnership”) will engage in various transactions to set up a bankruptcy remote structure, including Partnership transferring a business on an s. 97(2) rollover basis to a newly-formed bankruptcy-remote subsidiary LP (XX LP), and then transferring its units of XX LP to another newly-formed bankruptcy-remote subsidiary LP (“Holding LP”).

XX LP will then borrow in US dollars from arm’s-length lenders (the “XX Debt”) on commercial terms and provide essentially all of its assets (including the Parent Loan referred to below) as security.

XX LP will then immediately make an unsecured loan (the “Parent Loan”) of the proceeds in US dollars at the same interest rate plus a nominal spread, with a right to defer interest payments, and with a matching maturity date, to Parent, who will use such proceeds to repay indebtedness under a credit agreement

Additional Information

The Partnership received a legal opinion expressing the view that XX LP should be able to transact business with a limited partner and that such limited partnership should be able to make a loan to its limited partner under the applicable provincial Partnership Act.

Rulings

- The proceeds of the Parent Loan will not be considered to be received by Parent on account of, in lieu of payment of, or in satisfaction of a distribution by XX LP, XX Holding LP, or the Partnership for purposes of s. 53(2)(c)(v).

- S. 245(2) will not apply.

The CRA summary indicated that “Parent Loan is a loan under provincial law” and that it “is not an amount in lieu of a distribution because LP is a newly formed partnership with no income or capital prior to the Proposed Transactions”.

10 April 2024 External T.I. 2021-0919231E5 - Foreign tax allocation to a partner

Would the allocation of foreign tax by a partnership to a partner be regarded as a withdrawal by the particular partner that reduced the adjusted cost base (ACB) of its partnership interest? CRA stated:

If the partnership pays the foreign tax on behalf of the partner or the foreign tax is withheld on behalf of the partner in accordance with foreign law from the foreign income paid to the partnership, such amount would be considered [for purposes of s. 53(2)(c)(v)] to be received by the partner on account or in lieu of payment of, or in satisfaction of, a distribution of the partner’s share of the partnership profits or partnership capital. Consequently, subparagraph 53(2)(c)(v) of the Act would reduce the ACB of the partner’s interest in the partnership for the amount of any non-business income tax paid by the partnership on behalf of the partner. …

The reduction in ACB for foreign taxes paid on behalf of a partner may occur prior to the addition to the ACB for the allocation of foreign income to the partner which is made on the first day of the following fiscal period [potentially triggering a negative ACB gain under s. 40(3.1)].

This position on s. 53(2)(c) overruled 2004-0075931E5, which stated:

[P]aragraph 53(2)(c) does not provide for a deduction in computing the adjusted cost base of a taxpayer's interest in a partnership for the amount of any non-business income tax paid to a foreign country through the accounts of the partnership that was allocated to the particular partner … .

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(3.1) | payment by partnership of withholding or other taxes “on behalf of” its partners produces a s.53(2)(c)(v) reduction at payment time that can trigger negative ACB gain | 251 |

| Tax Topics - General Concepts - Payment & Receipt | payment by partnership of withholding tax treated as a distribution to its partners | 99 |

7 October 2022 APFF Roundtable Q. 5, 2022-0947611C6 F - Limited Partnership and Loans

When will CRA treat loans from a limited partnership received by a limited partner in order to avoid a gain under s. 40(3.1) as a distribution of partnership capital or profits per s. 53(2)(c)(v), so that such negative-ACB gain is not avoided?

CRA responded that it “will generally” not do so where the following five tests are satisfied:

1. “The loan is not made on account of or in full or partial payment of a withdrawal of a limited partner's capital contribution.”

2. The total amount of all loans received by the limited partner in respect of a fiscal period of the partnership does not exceed the total of (i) the limited partner's share of the adjusted net income of the partnership for the fiscal period (i.e., s. 53(1)(e)(i) additions minus 53(2)(c)(i) year losses), and (ii) the ACB of the limited partner's interest at the end of the fiscal year - “or, if there is an excess amount, it is not material in the circumstances”.

3. “Shortly after the end of the fiscal period, the partnership declares a distribution payable to the limited partner in an amount equal to the total amount of the loans received by the limited partner during the fiscal period and the distribution is used to settle the loans to the limited partner (in cash or by way of set-off).”