Subsection 50(1) - Debts established to be bad debts and shares of bankrupt corporation

Cases

Sunatori v. Canada, 2011 DTC 5153 [at at 6175], 2011 FCA 254

The taxpayer was the sole shareholder and employee of a corporation. The corporation paid him his entire salary on December 31 each year, which...

Simmonds v. Canada (Minister of National Revenue), 2006 DTC 6083, 2006 FC 130

In reviewing an adverse response of the Minister to a request of the taxpayer that the Minister grant under s. 152(4.2) the taxpayer's request for...

Turner v. The Queen, 2000 DTC 6442, 2001 FCA 289, 2001 FCA 33 (FCA)

The trial judge erred in finding that the taxpayer should have elected under s. 50(1)(b) in respect of his share investment in a company for 1984...

See Also

Kokai-Kuun Estate v. The Queen, 2015 TCC 217

In denying the recognition by the taxpayer of a capital loss under s. 50(1)(a), Lyons J stated (at paras. 55, 58, 62, 67):

In Harris v The Queen, The text of this content is paywalled except for the first five days of each month. Subscribe or log in for unrestricted access.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Adjusted Cost Base | interest carrying charges on vacant land not added to ACB | 88 |

Gaumond v. The Queen, 2014 DTC 1024 [at at 98], 2014 TCC 339 (Informal Procedure)

The Canadian-controlled private corporation ("GMG") of which the taxpayer was the principal shareholder made a proposal in May 2011 under the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(1) - Paragraph 39(1)(c) | renounced debt is not disposed of to anyone/s. 50 not available where debt settled in year | 277 |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(9) | s. 84(9) not for greater certainty | 137 |

St-Hilaire v. The Queen, 2014 TCC 336 (Informal Procedure)

The taxpayer made non-interest bearing advances to a wholly-owned incorporated radio station. On 8 August 2008, the corporation made a proposal...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(1) - Paragraph 39(1)(c) | acceptance of bankruptcy proposal caused debt to disappear before taxpayer's year end | 226 |

Coveley v. The Queen, 2014 DTC 1041 [at at 2771], 2013 TCC 417, aff'd 2014 FCA 281

The taxpayers were a married couple employed by a technology research corporation ("cStar"), and one taxpayer was also a shareholder. They lent a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(2) - Paragraph 40(2)(g) - Subparagraph 40(2)(g)(ii) | write-off of loans from shareholder v. employee/spouse | 154 |

Kyriazakos v. The Queen, 2007 DTC 373, 2007 TCC 66

The taxpayer advanced funds to a start-up company, sold the shares to a friend and, after the sale, made no attempt to collect the advances from...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(2) - Paragraph 40(2)(g) - Subparagraph 40(2)(g)(ii) | corporation sold before advance | 64 |

Netolitzky v. The Queen, 2006 DTC 2953, 2006 TCC 172

In finding that the taxpayer was entitled to claim business investment losses in respect of portions of amounts advanced to him by a company run...

Hopmeyer v. The Queen, 2006 DTC 2919, 2006 TCC 185

At the time in question the corporation was serving customers as usual, employees were working as usual, orders were being taken and filled,...

Litowitz v. The Queen, 2005 DTC 1469, 2005 TCC 557

In finding that the taxpayer had realized an allowable business investment loss with respect to an advance owing to him, Bowman C.J. noted (at p....

Keating v. The Queen, 2005 DTC 743, 2005 TCC 296 (Informal Procedure)

A loan owing to the taxpayer by a corporation owned by her but which had been depleted of its assets by her estranged husband had become a bad...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Legal and other Professional Fees | fees incurred in oppression action re stripping of corpoate assets were capital expenditures | 40 |

Jacques St-Onge Inc. v. The Queen, 2003 DTC 153 (TCC)

The taxpayer was able to claim an allowable business investment loss with respect to its investment in a subsidiary that had been incorporated to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Purpose/Intention | 97 |

Campbell v. The Queen, 2000 DTC 2528 (TCC)

Before going on to find that the taxpayer had realized an ABIL in his 1994 taxation year, as claimed by him, Hamlyn T.C.J. stated (at p. 2530):

"A...

Burns v. The Queen, 94 DTC 1370, [1994] 1 CTC 2364 (TCC)

The taxpayers were entitled to write-off 1/2 of the debts owing to them at the end of 1986 by a company ("WFC") given that on October 25, 1986...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(2) - Paragraph 40(2)(g) - Subparagraph 40(2)(g)(ii) | 140 |

Administrative Policy

S4-F8-C1 - Business Investment Losses

End of year references taxpayer

1.23 ... [T]he end of the tax year refers to the tax year of the taxpayer making the subsection 50(1) election....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Small Business Corporation | "substantially" and "principally" | 38 |

| Tax Topics - Income Tax Act - Section 50 - Subsection 50(1.1) | 247 | |

| Tax Topics - Income Tax Act - Section 50 - Subsection 50(1) - Paragraph 50(1)(a) | Proactive collection efforts | 157 |

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(2) - Paragraph 40(2)(g) - Subparagraph 40(2)(g)(ii) | connection between loan and income-producing purpose | 320 |

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(9) | Example | 182 |

| Tax Topics - Income Tax Act - Section 164 - Subsection 164(6) | Limitation on BIL carryback | 96 |

17 October 2014 Internal T.I. 2014-0535121I7 F - Hypothèque et créance irrécouvrable

In order to facilitate a sale, a real estate agent (the "Broker") provided financing to the purchaser by way of a second-ranking hypothec (which...

11 October 2013 APFF Roundtable, 2013-0495671C6 F - Déduction d'une partie d'une créance irrécouvrable

When asked how CRA's position - that a debt must be unrecoverable in its entirety before it could qualify as a bad debt under s. 50(1) - could be...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(p) - Subparagraph 20(1)(p)(i) | 20(1)(p)(i) deduction for trade debts of a customer are determined on a receivable by receivable basis | 151 |

3 January 2014 External T.I. 2013-0482081E5 - Nil value partnership units

A limited partnership "has ceased all activity but has not legally ceased to exist;" and "all partnership funds have been lost in a failed...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | no disposition of interests in inactive partnership until dissolution | 99 |

9 November 2012 CTF Atlantic Roundtable, 2012-0465981C6 - CTF Atlantic - Filing Electronically

When a tax return is filed electronically, how can the taxpayer satisfy a requirement to "elect in the return" (see s. 50(1)) or "by letter...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 220 - Subsection 220(3.5) | 166 | |

| Tax Topics - Income Tax Regulations - Regulation 1101 - Subsection 1101(5b.1) | 166 |

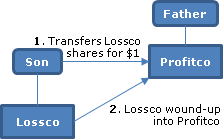

5 October 2012 APFF Roundtable, 2012-0454061C6 F - Transfer of a Lossco to a related corporation

Example 1

{kind=link}

Son claims an ABIL under s. 50(1) with respect to his share investment in a wholly-owned corporation (Lossco), which had ceased active...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Shares | non-capital losses of corporation taken into account in valuing its shares | 162 |

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(1) - Paragraph 111(1)(a) | related but not affiliated transfer of Lossco shares to father's or brother's company | 267 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1.1) | lossco losses maintained on father-son or sibling transfers and s. 88(1.1) wind-up | 266 |

16 December 2003 Internal T.I. 2003-04616

With respect to the situation where a parent corporation ("Parentco") would elect to have s. 50(1) apply in respect of the shares of one of its...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Shares | 106 |

8 January 2002 External T.I. 2001-0096005 - BAD DEBTS AND CARRYING ON A BUSINESS

A debt would not qualify as being bad, i.e., completely uncollectible, by virtue only of a decision having been made that the debtor corporation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Small Business Corporation | old trade receivable may not be active | 67 |

15 June 1998 Internal T.I. 9802347 - BUSINESS INVESTMENT LOSSES

A corporation that had made a general conveyance of all its assets to its shareholder in the course of voluntary dissolution proceeding, with the...

1994 A.P.F.F. Round Table, Q. 6

"Nothing in the wording of subsection 50(1) of the Act leads us to believe that a portion of a debt may be deemed a bad debt. This interpretation...

6 April 1993 T.I. (Tax Window, No. 30, p. 5, ¶2493)

Anderson v. MNR, 92 DTC 2296 (TCC) (in which a letter of the taxpayer's accountant requesting the application of an allowable business investment...

Central Region Rulings Directorate Seminar, Q. A (May 1993 Access Letter, p. 228)

The deemed disposition likely does not occur on a debt owing by a corporation all of whose other loans have been called by the bank so long as...

17 February 1993 Memorandum 930202 (Tax Window, No. 30, p. 21, ¶2496)

The onus is on the taxpayer to establish that there was a debt owing to him, i.e., "a sum payable in respect of a liquidated money demand,...

1992 A.P.F.F. Annual Conference, Q. 4 (January - February 1993 Access Letter, p. 51)

Given that the dictionary meaning of "insolvent" refers to incapability of paying debts, a corporation that has neither assets nor debt cannot...

23 October 1991 Memorandum (Tax Window, No. 12, p. 23, ¶1548)

An investor who suffers a loss due to fraud may be entitled to claim a capital loss if the criteria in IT-159R3, para. 10 are met.

29 July 1991 T.I. (Tax Window, No. 7, p. 19, ¶1377)

A corporation will not have ceased to carry on a business until the liquidation of all assets capable of being used in an income-earning process...

12 December 1989 T.I. (May 1990 Access Letter, ¶1215)

The cessation of business and the insolvency referred to in s. 50(1)(b)(iii) need not occur in the same year as long as the corporation satisfies...

25 October 89 T.I. (March 1990 Access Letter, ¶1145)

Where a creditor agrees with an insolvent corporation to take less than the full amount owing in exchange for a full and final release of all...

IT-159R3 "Capital Debts Established to be Bad Debts"

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(1) - Paragraph 39(1)(b) | 43 |

Paragraph 50(1)(a)

Administrative Policy

13 November 2003 Internal T.I. 2003-0039637 F - perte sur creance et frais

The taxpayer disposed of shares to an arm’s length purchaser for proceeds payable in instalments, which the purchaser defaulted in paying. The...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Adjusted Cost Base | legal fees to recover deferred proceeds of share disposition do not increase the shares’ ACB | 148 |

S4-F8-C1 - Business Investment Losses

Relevance of NAL relationship

1.34 ... While there is no legal requirement that in all cases a taxpayer must exhaust all legal means of collecting...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Small Business Corporation | "substantially" and "principally" | 38 |

| Tax Topics - Income Tax Act - Section 50 - Subsection 50(1) | End of year references taxpayer | 343 |

| Tax Topics - Income Tax Act - Section 50 - Subsection 50(1.1) | 247 | |

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(2) - Paragraph 40(2)(g) - Subparagraph 40(2)(g)(ii) | connection between loan and income-producing purpose | 320 |

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(9) | Example | 182 |

| Tax Topics - Income Tax Act - Section 164 - Subsection 164(6) | Limitation on BIL carryback | 96 |

21 November 2001 Internal T.I. 2001-0094527 F - PERTE REPUTEE NULLE-BRYAN

CCRA reiterated its position that in order for a capital loss to arise under s. 50(1)(a) from a debt, the debt must be bad in its entirety given...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(2) - Paragraph 40(2)(g) - Subparagraph 40(2)(g)(ii) | Byram now followed re loss on non-interest-bearing shareholder loan to corporation | 57 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(27) | s. 248(27) does not permit partial debt write-off under s. 50(1)(a) | 75 |

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(1) - Paragraph 39(1)(c) - Subparagraph 39(1)(c)(ii) | settlement of corporate debt under a bankruptcy proposal did not entail disposition of the debt to the corporation | 89 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(2) - Paragraph 251(2)(b) - Subparagraph 251(2)(b)(i) | shareholder continued to control “his” corporation while it was being administered by a bankruptcy trustee pending approval of a proposal | 83 |

| Tax Topics - Income Tax Act - Section 116 - Subsection 116(5) | settlement under bankruptcy proposal of debt did not entail a disposition of that debt to the corporation | 50 |

Paragraph 50(1)(b)

Subparagraph 50(1)(b)(i)

Administrative Policy

2 October 2006 Internal T.I. 2006-0168081I7 F - Actions d'une société en faillite

After the appointment of a trustee, two subsidiary corporations of the taxpayer corporation filed notices of intention under s. 50.4 of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 50 - Subsection 50(1) - Paragraph 50(1)(b) - Subparagraph 50(1)(b)(iii) | if s. 50(1)(b)(iii) conditions are satisfied in a year, the election can be made in a subsequent year – but not if the corporation was a bankrupt in the first year | 275 |

Subparagraph 50(1)(b)(iii)

See Also

Agence du revenu du Québec v. Samson, 2023 QCCA 332

An individual (Samson) and corporation (Bourgade) implemented a tax-planning memo that contemplated that they would transfer their shares of a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Rectification & Rescission | date of Quebec agreement did not reflect the parties’ existing intention to realize a loss | 309 |

Administrative Policy

2 October 2006 Internal T.I. 2006-0168081I7 F - Actions d'une société en faillite

After the appointment of a trustee, two subsidiary corporations of the taxpayer corporation filed notices of intention under s. 50.4 of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 50 - Subsection 50(1) - Paragraph 50(1)(b) - Subparagraph 50(1)(b)(i) | s. 50(1)(b)(i) satisfied if notice of intention under BIA does not lead to timely filing of proposal – but election must be filed for that rather than subsequent year | 239 |

16 December 2003 Internal T.I. 2003-0046167 F - Section 50- Shares of Insolvent Corporation50(1)

Parentco elected (in reliance on s. 50(1)(b)(iii)) under s. 50(1) respecting its shares of one of a wholly-owned subsidiary ("Lossco") with...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(b) | sale of Lossco with no assets but non-capital losses for nil consideration to another subsidiary generated a gain under s. 69(1)(b) | 125 |

| Tax Topics - General Concepts - Fair Market Value - Shares | shares of corporation that had ceased business and had no assets but had non-capital losses had a significant value | 75 |

Clause 50(1)(b)(iii)(A)

Administrative Policy

21 February 2002 External T.I. 2001-0109765 F - Debts to be Bad Debts of Bankrupt Corp.

In the course of a general response as to the meaning of "insolvent" in s. 50(1)(b)(iii), CCRA stated:

[T]he word "insolvent" should be given its...

Subsection 50(1.1)

Administrative Policy

S4-F8-C1 - Business Investment Losses

can be dissimilar business

1.30 ... [T]he business that commences to be carried on within the 24-month window need not be the same as (or even...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Small Business Corporation | "substantially" and "principally" | 38 |

| Tax Topics - Income Tax Act - Section 50 - Subsection 50(1) | End of year references taxpayer | 343 |

| Tax Topics - Income Tax Act - Section 50 - Subsection 50(1) - Paragraph 50(1)(a) | Proactive collection efforts | 157 |

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(2) - Paragraph 40(2)(g) - Subparagraph 40(2)(g)(ii) | connection between loan and income-producing purpose | 320 |

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(9) | Example | 182 |

| Tax Topics - Income Tax Act - Section 164 - Subsection 164(6) | Limitation on BIL carryback | 96 |