Cases

Bosa v Canada, 2025 BCSC 1284

The petitioners were the beneficiaries of a family trust, who sought to rectify the terms of the Trust Indenture to clarify that the assets of the...

Agence du revenu du Québec v. Structures GB Ltée, 2025 QCCA 134

The shareholders of a Canadian-controlled private corporation (“Structures”) implemented a reorganization that was intended to crystallize the...

Pyxis Real Estate Equities Inc. v. Canada (Attorney General), 2025 ONCA 65

A plan was implemented for successive capital dividends to be paid up a chain of corporations so that the individual who was the ultimate...

Pierre Elliott Trudeau Foundation v. Millenium Golden Eagle International (Canada) Inc., File No. 500-17-125795-230 (Quebec Superior Court)

The plaintiff (the Foundation) received two donations, each of $70,000, from the defendant (Millenium) in July 2016 and July 2017. These amounts...

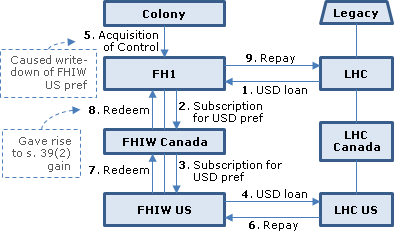

Evans v. Attorney General of Canada, 2024 ONSC 1955

After a discretionary family trust realized a capital gain from a share sale, the sole trustee passed a resolution in that year providing that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(6) | trust allocation resolution rectified to set out specific amounts | 232 |

Williams Moving & Storage (B.C.) Ltd. v. Canada (Minister of National Revenue), 2024 BCCA 160

A drafting error (involving an inappropriate duplication of text) in the proposal which was approved by the creditors of an insolvent company...

Slightham et al. v. AGC, 2023 ONSC 6193

The two applicant trusts were formed in order to acquire the common shares of a corporation (“Signature”) in an estate freezing transaction. ...

Les Structures G.B. Inc. v. A.G. Canada, 2023 QCCS 3510, rev'd 2025 QCCA 134

Four individuals held their indirect holdings of 10%, 10%, 5% and 5% of the common shares of a Canadian-controlled private corporation...

Agence du revenu du Québec v. Samson, 2023 QCCA 332

The respondent (Samson) and a corporation (Bourgade) implemented a plan set out in a tax-planning memo of a tax advisor that contemplated that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 50 - Subsection 50(1) - Paragraph 50(1)(b) - Subparagraph 50(1)(b)(iii) | no loss realized under s. 50(1)(b)(iii) unitl year end rectifed | 229 |

Canada (Attorney General) v. Collins Family Trust, 2022 SCC 26

Two operating companies each implemented a plan, suggested by a tax advisor, to protect their assets from creditors. In each case, a holding...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(1) | Minister required to assess based on an unexpected case law development | 365 |

| Tax Topics - Income Tax Act - Section 220 - Subsection 220(1) | s. 220 required the Minister to assess based on new judicial interpretation | 177 |

Mandel v. 1909975 Ontario Inc., 2020 ONSC 5343

In order to avoid a deemed disposition under the s. 104(4) 21-year deemed realization rule, two family trusts for the children of Mr. Mandel or...

Collins Family Trust v Canada (Attorney General), 2019 BCSC 1030, aff'd 2020 BCCA 196, rev'd 2022 SCC 26

After noting that the applications before him for the rescission of transactions entailing reliance on an interpretation of s. 75(2) that was...

Crean v Canada (Attorney General), 2019 BCSC 146

Two of the petitioners were two brothers (Thomas and Michael) who each owned 50 of the 100 issued and outstanding common shares of a holding...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) | share sale for Newco note generated s. 84.1 dividend before its rectification | 233 |

Re 5551928 Manitoba Ltd., 2018 BCSC 1482

The petitioner, a Manitoba corporation with 24 shareholders, passed a resolution on November 20, 2015 that recited that “the company has a...

Canada Life Insurance Company of Canada v. Canada (Attorney General), 2018 ONCA 562

A Canada Life subsidiary (CLICC) clearly intended to realize an accrued loss on its LP interest in a subsidiary partnership by winding it up. This...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 98 - Subsection 98(5) | pro-rata winding-up of partnership followed by winding up of one former partner into the other engaged s. 98(5) per CRA | 92 |

Fournier v. Agence du revenu du Québec, 2018 QCCQ 786

On August 15, 2007, Mr. Fournier sold land to a family corporation (“Canada Inc.”) for a purchase price that was satisfied by the issuance by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | taxable benefit assessment relied on an inaccurate notarial deed, which could be corrected after the assessment | 218 |

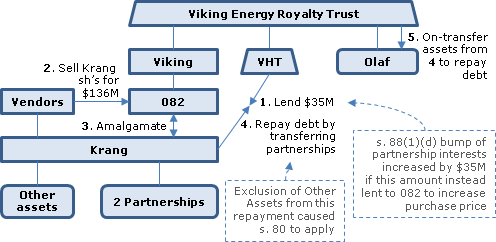

Harvest Operations Corp. v. Attorney General of Canada, 2017 ABCA 393

A last-minute requirement of a lender (“ATB”) to the target corporation (“Krang Energy”) for ATBH’s loan to be repaid on closing...

Greither Estate v. Canada (Attorney General), 2017 BCSC 994

627291 B.C. Ltd., which was jointly owned by two German residents (Karoline Greither and her husband), rented a B.C. property to a related company...

BC Trust v. Canada (Attorney General), 2017 BCSC 209

The petitioner was a personal trust, with another trust (“Alta Trust”) as its sole income and capital beneficiary. In 2012, CRA made a...

Canadian Forest Navigation Co. Ltd. v. Canada, 2017 FCA 39

The taxpayer’s Barbados and Cyprus subsidiaries paid amounts to the taxpayer in 2004, 2005 and 2006 as dividends and then, following CRA...

Jean Coutu Group (PJC) Inc. v. Canada (Attorney General), 2016 SCC 55, [2016] 2 S.C.R. 670

The taxpayer (“PJC Canada”), a Quebec corporation, implemented a plan, to neutralize the effect of FX fluctuations on its investment in a U.S....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Interpretation Act - Section 8.1 | desriable for convergence of principles and outcomes inside and outside Quebec | 161 |

Canada (Attorney General) v. Fairmont Hotels Inc., 2016 SCC 56, [2016] 2 S.C.R. 720

With a goal of ensuring foreign exchange tax neutrality, Fairmont Hotels Inc. (“Fairmont”) entered into a “reciprocal loan arrangement”...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Interpretation Act - Section 8.1 | convergence in civil/common law rectification | 95 |

Anderson v Benson Trithardt Noren LLP, 2016 SKCA 120, aff'd 2017 SCC CanLii 8568

The taxpayer’s accountants met with him on October 6, 2011, when it was agreed that he would transfer personally-owned land and equipment on s....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | transaction documents not declared effective to date transaction agreed to in principle | 187 |

Slate Management Corporation v Canada (Attorney General), 2016 ONSC 4216

A purchaser (“SCC”) used a newly-formed AcquisitionCo (“GTA”) to acquire a Target (“HCC”). The three corporations then amalgamated. ...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(d) | three-party non-sequential amalgamation busted bump | 118 |

Non Corp Holdings Corp. v. Canada (Attorney General), 2016 ONSC 2737

The corporate applicant intended to distribute the applicable portion of a “capital gain” (likely, goodwill proceeds) from a business sale as...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Capital Dividend Account - Paragraph (c.1) | capital dividend incorrectly dated before year end | 79 |

Birch Hill Equity Partners Management Inc. v Rogers Communications Inc., 2015 ONSC 7189

The general partner of an Ontario limited partnership (“Atria”) granted stock options on its Class C shares to 10 Atria executives. The...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 6204 - Subsection 6204(1) - Paragraph 6204(1)(a) | board had discretion to determine fixed liquidation entitlement | 127 |

Canada Life Insurance Co. of Canada v. A.G of Canada, 2015 DTC 5128 [at at 6378], 2015 ONSC 281, rev'd 2018 ONCA 562

In order that the applicant ("CLICC") could realize an accrued capital loss on its 99% limited partner interest in a subsidiary limited...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 98 - Subsection 98(5) | rectification to avoid s. 98(5) rollover | 255 |

Telus Communications Inc. v. A.G. of Canada, 2015 ONSC 6245

The Telus group had a tiered partnership structure. Its management decided that Telus would make a multi-tier alignment election under s. 249.1(9)...

Zhang v. The Queen, 2015 DTC 5084 [at at 6035], 2015 BCSC 1256

The taxpayer (Mr. Zhang) briefly sought advice from his tax accountant (Bob) as to how he could extract funds from his Chinese operating company...

Fairmont Hotels Inc. v. A.G. Canada, 2015 ONCA 441, aff'g 2014 ONSC 7302, leave granted, SCC docket 36606

{kind=link}

Harvest Operations Corp v. A.G. (Canada), 2015 DTC 5067 [at at 5904], 2015 ABQB 327

{kind=link}

The Bump Mistake

A predecessor in interest of the applicant ("Viking") entered a multi-step acquisition and restructuring transaction to acquire...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Estoppel | taxpayer estoppel when it claimed a tax benefit from its mistake rather than promptly seeking rectification | 206 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(c) | failure to fund debt repayment through increased purchase price | 162 |

Mac's Convenience Stores Inc. v. A.G. of Canada, 2015 QCCA 837

The appellant, which was a wholly-owned Ontario subsidiary of a Quebec corporation ("CTI"), paid a $136 million dividend to CTI in connection with...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(5) - Equity Amount - Paragraph (a) | dividend triggered application of thin cap rules | 65 |

A.G. Canada v. Le Groupe Jean Coutu (PJC) Inc., 2015 QCCA 838, aff'd 2016 SCC 55

The professional advisors of the respondent ("PJC Canada") recommended two alternatives ("Scenarios 1 and 2") for it to neutralize the effect of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Accrual Property Income | FAPI from loan by CFA to Canco | 59 |

Kaleidescape Inc. v. MNR, 2014 ONSC 4983

The applicant ("K-Can") was intended to qualify as a Canadian-controlled private corporation. Its outstanding shares consisted of 100 Class A...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Canadian-Controlled Private Corporation | USA did not affect decision-making status of board | 203 |

Canada (Attorney-General) v. Brogan Family Trust, 2014 ONSC 6354

The respondent family trust obtained a rectification order, to permit trust distributions to minor grandchildren beneficiaries, on 26 November...

Fairmont Hotels Inc. v. A.G. Canada, 2014 ONSC 7302, aff'd supra, rev'd 2016 SCC 56

In order to facilitate the acquisition in 2002 of a hotel in Washington by a REIT ("Legacy") of which it was the manager, Fairmont Hotels Inc....

Jaft Corporation v. Canada (AG), 2014 DTC 5080 [at at 7056], 2014 MBQB 59

CRA had found that the applicant's research into solutions for Sick Building Syndrome based on air treatment qualified for scientific research and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 171 - Subsection 171(1) | superior court declined jurisdiction to consider equitable remedy that bore heavily on parallel tax court proceedings | 195 |

Re: Pallen Trust, 2014 DTC 5039 [at at 6726], 2014 BCSC 305, aff'd 2015 BCCA 222

Quebec (Agence du revenu) v. Services Environnementaux AES inc., 2013 DTC 5174 [at at 6466], 2013 SCC 65, [2013] 3 S.C.R. 838

Riopel Facts

Mr. Riopel was the sole shareholder of "JPF-1" and he and his wife (Ms. Archambeault) held 60% and 40% of the shares of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Interpretation Act - Section 8.1 | 103 |

Kanji v. Attorney General of Canada, 2013 DTC 5058 [at 5824], 2013 ONSC 781

The taxpayer settled a family trust in 1992 with $5000, which was used to purchase shares in a business corporation. The family trust acquired a...

.Mac's Convenience Stores Inc. v. Couche-Tard Inc., 2012 DTC 5118 [at at 7149], 2012 QCCS 2745 (Queb Sup Ct), aff'd supra

The taxpayer paid a $136 million dividend to the non-resident corporate defendant when it was indebted to the defendant. This reduced the...

FNF Canada Company v. Canada (Attorney General), 2012 NSSC 217

The applicant, incorporated by a U.S. corporation ("Fidelity National"), received $23,659,000 from Fidelity National in order to finance its...

Orman v. Marnat Inc., 2012 DTC 5052 [at at 6814], 2012 ONSC 549

The applicants and the respondents (which were corporations held by the applicants) were defrauded in a Ponzi scheme. The applicants took the...

McPeake v. Canada, 2012 DTC 5042 [at at 6770], 2012 BCSC 132

The petitioners were trustees of a family trust which had been formed in order to permit capital gains on any subsequent sale of the shares of the...

S & D International Group Inc. v. A.G. of Canada, 2011 DTC 5072 [at at 5771], 2011 ABQB 230

The corporate applicant (S & D) carried on a real estate trading and development business. It had three directors, whose wives, the individual...

Bouchan v. Slipacoff, 2010 ONSC 2693

The defendant and plaintiff held shares in an incorporated dental practice. In the course of a civil dispute, the defendant sought leave to plead...

TCR Holding Corp. v. Ontario, [2010] O.J. No. 1238, 2010 ONCA 233

The applicant resulted from several corporations being amalgamated in order that the tax losses of some of the predecessor corporations could be...

Stone's Jewellery Ltd. v. Arora, [2010] CTC 139, 2009 ABQB 656 (Alta QB)

A corporation ("Stone's") had entered into an agreement in 1996 to purchase lands for $500,000. The closing was substantially delayed, and when...

Winclare Management Services Ltd v. Canada (Attorney General), 2009 CanLII 18234 (Ont SC)

The directors of the taxpayer mistakenly declared a dividend in an amount exceeding its capital dividend account, and it elected under s. 83(2) to...

Shafron v. KRG Insurance Brokers (Western) Inc., [2009] 1 S.C.R. 15

The parties entered into an employment contract that included a restrictive covenant, providing that the defendant would not be employed in the...

Aim Funds Management Inc. v. Aim Trimark Corporate Class Inc., [2009] O.J. No. 4798, [2009] GSTC 170, 64 DLR (4th) 261, 2009 CanLII 29491 (Ont. Sup. Ct. J.)

The Minister assessed the applicant, a mutual fund manager, on the basis that a payment to it by mutual funds of deferred sale charges received by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 123 - Subsection 123(1) - Financial Service | 159 |

QL Hotel Service Ltd. v. Minister of Finance, 2008 CanLII 15226 (Ont SCJ), briefly aff'd 2009 ONCA 715

A transfer of tangible personal property by an Ontario corporation ("1006") to a second corporation ("QL") would have been exempt from Ontario...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Rectification & Rescission | 77 |

QL Hotel Service Ltd. v. Minister of Finance, 2008 CanLII 15226 (Ont SCJ), briefly aff'd 2009 ONCA 715

In a property tax dispute, counsel moved to couple the taxpayer's appeal with a rectification application, so that the rectification would serve...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Rectification & Rescission | 174 |

Binder v. Saffron Rouge, 2008 DTC 6112, 2008 CanLII 1662 (Ont. S.C.J.)

The taxpayers were incorporating shareholders of a corporation. Although they realized at the time that a share issue in 2005 to a U.S. investor...

Re Columbia North Realty Co., 2006 DTC 6124, 2005 NSSC 212 (NSSC)

On two occasions, a Nova Scotia company ("Columbia") made cash distributions to its non-resident shareholder, purportedly as distributions of...

Snow White Productions Inc. v. PMP Entertainment, Inc., 2005 DTC 5150, 2004 BCSC 604

As the common intention of the parties to agreements respecting the production of a movie was that it would be eligible for the federal film or...

Performance Industries Ltd. v. Sylvan Lake Golf & Tennis Club Ltd., 2002 SCC 19, [2002] 1 S.C.R. 678

The plaintiff (“Sylvan”) and the defendant (“Performance”) entered into an agreement respecting a golf course that gave Sylvan the option...

Re Razzaq Holdings Ltd (2000), 11 BLR (3d) 157, 2000 BCSC 1829

In 1992 the two shareholders of a corporation purported to transfer a total of 100 Class A shares and 100 Class B shares equally to two holding...

Attorney General of Canada v. Juliar, 2000 DTC 6589, 50 OR (3d) 728, 2000 CanLII 16883 (Ont CA)

The Court confirmed the decision of the trial judge, to rectify an agreement for the transfer by the appellants of half the shares of a company to...

Amalgamation of Aylwards [1975] Ltd. (2001), 16 BLR (3d) 34, 610 APR 181, 2001 CanLII 32734 (Nfld. Sup. Ct. T.D.)

A Newfoundland corporation was amalgamated with what was thought to be a wholly-owned subsidiary in a short-form amalgamation. However, it was...

Dale v. R., 97 DTC 5252, [1997] 2 CTC 286 (FCA)

The taxpayers neglected to have shares that purportedly were issued to them in 1985 added to the authorized capital of the issuing corporation....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | retroactive superior court order has retroactive effect for tax purposes | 174 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Dividend | 78 | |

| Tax Topics - Income Tax Act - Section 83 - Subsection 83(2) | 78 | |

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) | retroactive validation by Superior Court of preference share issuance was effective for s. 85 purposes | 171 |

| Tax Topics - Statutory Interpretation - Provincial Law | 140 |

771225 Ontario Inc. v. Bramco Holdings Co. (1995), 21 OR (3d) 739 (CA), aff'g (1994), 17 OR (3d) 571 (Gen Div)

Ontario farm lands were transferred to a non-resident corporation for the purpose of utilizing losses of that corporation. However, it was...

See Also

Kraft Heinz Canada ULC v. Canada (Attorney General), 2022 BCSC 796

The petitioners were a Dutch cooperative (“Heinz Co-op”) and a B.C. unlimited liability company (“KH Canada”) which was the sole member of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(10) - Paragraph 212.3(10)(b) | a self-help Dutch-law annulment declaration retroactively voided a s. 212.3(10)(b) contribution | 350 |

Bourgault v. The Queen, 2019 TCC 6

On April 15, 2002, the taxpayer signed an agreement for the purchase of shares of a real estate corporation (“Quatre Saisons”) that stated...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | parties justifiably rectified their agreement so that it had retroactive effect | 253 |

Foster v. The Queen, 2016 DTC 1010 [at 2562], 2015 TCC 334

Paris J found that, although a rectification order replaced a series of sales of a fishing licence and equipment with a different series of sales,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(5) | rectification order lead to consequential out-of-period reassessment; out-of-period assessment upheld | 303 |

Baytex Energy Ltd v Canada (Attorney General), 2015 DTC 5057 [at 5807], 2015 ABQB 278 (CanLII)

The applicant (“BEL”) owned and operated oil and gas properties. To address concerns about provincial royalties eroding federal revenues,...

Canadian Forest Navigation Co. Ltd. v. The Queen, 2016 TCC 43, rev'd 2017 FCA 39

The taxpayer’s Barbado and Cyprus subsidiaries paid amounts to the taxpayer in 2004, 2005 and 2006 as dividends and then, following CRA...

Prowting 1968 Trustee One Limited v. Amos-Yeo, [2015] EWHC 2480 (Ch)

In order that the life tenants of two trusts (the 1968 and 1987 settlements) could access a reduced rate of U.K. capital gains tax on a sale of...

Kennedy & Ors v. Kennedy & Ors, [2015] BTC 2, [2014] EWHC 4129

The trustees of a family trust exercised an appointment in favour of beneficiaries including the settlor of the trust (Mr Kennedy). The transfer...

Demers v. The Queen, 2014 TCC 368

The two taxpayers, who had been CN employees, were convinced by two promoters (the Lavignes) to transfer all the funds in their CN pension plans...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 146 - Subsection 146(8) | Superior Court nullification of investment contracts did not nullify RRSP withdrawals | 175 |

0741508 B.C. Ltd. and 0768723 B.C. Ltd. (Re), 2014 BCSC 1791

In 2011, the petitioners conveyed undeveloped B.C. lands to a limited partnership with an affiliated general partner. Due to failed...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 171 - Subsection 171(1) | B.C. HST repeal reduced basic tax content | 111 |

Graymar Equipment (2008) Inc v Canada (Attorney General), 2014 DTC 5051 [at at 6802], 2014 ABQB 154

The applicants were a limited partnership ("FRPDI") and the partnership's wholly owned corporation ("Graymar"). The implementation of a debt...

Giles (as administratrix of Hilda Bolton estate) v. Royal National Institute for the Blind & Ors, [2014] BTC 24, [2014] EWHC 1373 (Ch)

The claimant applied for rectification of a Deed of Variation which altered the provisions of the will of Hilda Bolton with a view to reducing the...

Sheila Holmes Spousal Trust v. Canada (Attorney General), 2013 ABQB 489

The federal Minister assessed the settlor of the appellant trust on the basis that the trust's taxable capital gain and investment income were...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(1) | superior court declines jurisdiction in tax dispute | 215 |

Pitt v. Commissioners for HM Revenue and Customs, [2013] UKSC 26, [2013] WLR (D) 172

The claimant had settled the moneys received as damages for injury to her husband on a discretionary trust of which she and others were trustees. ...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Mistake | mistake re tax consequences justified rescinding settlement of trust | 176 |

Racal Group Services Ltd. v. Ashmore & Ors., [1995] BTC 406 (CA)

A deed for payment of £70,000 to charity, although it was intended to comply with an income tax requirement that the payment be for a period...

Downtown King West Development Corp. v. Massey Ferguson Industries Ltd. (1993), 14 OR (3d) 528 (Ont Ct GD)

Given that a lease as signed did not reflect the terms agreed to in the letter of intent and that a change to the terms of a right of first...

St. Ives Resources Ltd. v. MNR, 90 DTC 1375, [1990] 1 CTC 2539 (TCC), aff'd 92 DTC 6223 (FCTD), briefly aff'd in turn at 94 DTC 6261 (FCA)

In refusing to recognize a price rectification agreement, Sarchuk, J. stated (p. 1378):

"Rectification is an 'equitable remedy' whereby one party...

Administrative Policy

10 October 2014 APFF Roundtable Q. 6, 2014-0538251C6 F - 2014 APFF Roundtable, Q. 6 - Application of subsection 75(2) after Sommerer

CRA declined to comment on Pallen Trust, 2014 BCSC 305, as it had been appealed to the British Columbia Court of Appeal.

10 June 2011 Roundtable, 2011-0404621C6 F - Rectification order in Québec

CRA noted that as the ARQ had sought leave to appeal the AES decision to the Supreme Court and the period for seeking leave in Riopel had not yet...

Income Tax Technical News No. 22, 11 January 2002

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 5 | 73 |

30 April 2009 External T.I. 2008-0296721E5 F - Late filed election 85(7) - Amending transactions

An individual transferred an immovable to his corporation for non-share consideration, and after being reassessed by CRA for the resulting gain,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) | CRA will not accept s. 85 election based on self-help rectification to retroactively issue shares at transfer time | 218 |

18 November 2004 Internal T.I. 2004-0083251I7 - Management Fees

General discussion of the distinction between rectification of mistakes and retroactive tax planning.

18 February 1999 External T.I. 9825635 - VALIDITY OF 104(5.3) ELECTION

The comments in IT-378R, that the validity of an election may not be denied by a taxpayer once it is accepted by the Department, is applicable to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 220 - Subsection 220(3.2) | 98 |

Articles

Jeff Oldewening, Rachel A. Gold, Chris Sheridan, "Statutory Ratification", Canadian Tax Journal, (2016) 64:1, 293-325

Distinction between Juliar and contract rescission cases (pp. 305-306)

Performance Industries and Shafron are non-tax, contract cases. The...

Joel A. Nitikman, "Rectification: Specific Intent? General Intent? What is the Test? – Part II", Tax Topics, Wolters Kluwer, No. 2274, October 8, 2015, p.1.

Test is one simply of true intention, not specific intent (pp. 3-4)

In Juliar,…[t]he key passages from the Court of Appeal are these:…

[I]t is...

Catherine Brown, Arthur J. Cockfield, "Rectification of Tax Mistakes Versus Retroactive Tax Laws: Reconciling Competing Visions of the Rule of Law", Canadian Tax Journal, (2013) 61:3, 563-98

Juliar line of cases (pp. 573-4)

The post-Juliar decisions demonstrate that if the intention of the parties is to put into effect a transaction...

Jean-Philippe Latreille, "Rectification? In Quebec?", CCH Tax Topics, No. 2045, 19 May 2011, p. 1.

Neil E. Bass, "Trends in Sales Tax Litigation", 2008 Conference Report, C.o.

Mitchell Sherman, "Can We Do Another Take?", Tax Notes International, 16 August 2004, p. 631

Discussion of Snow White Productions Inc. v. PNP Entertainment, Inc.

Commentary

Retraoctive effect

As discussed above under Effective Date, an order of the Superior Court that is stated to have retroactive effect also will...