Subsection 75(2) - Trusts

Cases

Fiducie financière Satoma v. Canada, 2018 FCA 74

A tax plan turned upon dividends that in fact were paid to a family trust (Satoma Trust) being attributed under s. 75(2) to a corporation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(1) - Tax Benefit | tax benefit to trust from tax-free dividend even though not distributed to a beneficiary | 277 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | using ss. 75(2) and 112(1) for tax-free dividends to trust thwarted s. 112(1) object to tax earnings when ultimately distributed | 319 |

| Tax Topics - Income Tax Act - Section 3 | pervasive rule that the same income is not to be taxed in 2 persons’ hands | 148 |

| Tax Topics - Statutory Interpretation - Double Taxation/Deduction (Presumption Against) | inclusion of income in more than one taxpayer’s hands is contrary to s. 3 | 294 |

| Tax Topics - Income Tax Act - Section 112 - Subsection 112(1) | abusive to use s. 112(1) so as to avoid ultimate taxation of individuals | 180 |

| Tax Topics - Income Tax Act - Section 82 - Subsection 82(2) | s. 82(2) supports the primacy of s. 75(2) over the actual dividend recipient | 60 |

Canada v. Sommerer, 2012 DTC 5126, 2012 FCA 207

The taxpayer (a Canadian-resident individual) sold shares of a Canadian company to an Austrian private foundation (privatstiftung) which had been...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(1) | Austrian foundation likely not a trust | 181 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(5) | 84 | |

| Tax Topics - Treaties - Income Tax Conventions | treaty applies to economic double taxation | 356 |

| Tax Topics - Treaties - Income Tax Conventions - Article 13 | attributed gain not included | 415 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | s. 75(2) should not be applied to attribute the same gain to 2 taxpayers | 115 |

Fraser v. The Queen, 91 DTC 5123 (FCTD), aff'd 95 DTC 5684 (FCA)

Subsection 75(2) did not apply to income earned by unit holders in a trust which used the subscription proceeds for the units to acquire mortgages...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(2) | 76 |

The Queen v. Quinn, 73 DTC 5215, [1973] CTC 258 (FCTD)

Under a contract with the Canadian Scholarship Trust Fund it was agreed that interest on funds deposited by the taxpayer would be transferred to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(c) | 87 | |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | 92 |

See Also

Fiducie Financière Satoma v. The Queen, 2017 TCC 84, aff'd 2018 FCA 74

The taxpayer was found to be subject to s. 245(2) respecting a surplus-stripping plan that relied on dividends that in fact were paid to a family...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | use of s. 75(2) attribution rule and s. 112(1) DRD to extract surplus to a family trust was abusive | 569 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(1) - Tax Benefit | tax benefit even though corporate surplus stripped in favour of family trust had not so far been distributed | 215 |

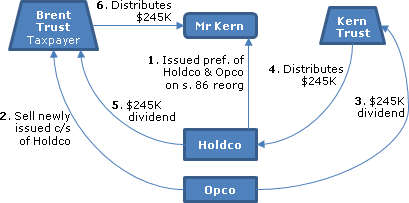

Brent Kern Family Trust v. The Queen, 2013 DTC 1249 [at at 1396], 2013 TCC 327, aff'd 2014 FCA 230

{kind=link}

The facts (see para. 29 of the Reasons, which states the opposite of para. 6 of the poorly-drafted Statement of Agreed Facts) appear to be...

Sommerer v. The Queen, 2011 DTC 1162 [at at 845], 2011 TCC 212, aff'd 2012 FCA 207

The taxpayer (a Canadian-resident individual) transferred shares of a Canadian company to an Austrian private foundation (privatstiftung) which...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | retroactive amendment respected | 282 |

| Tax Topics - Statutory Interpretation - Treaties | 57 | |

| Tax Topics - Treaties - Income Tax Conventions | 176 |

Garron Family Trust v. The Queen, 2009 DTC 1568, 2009 TCC 450, aff'd sub nom St. Michael Trust Corp. v. The Queen, 2010 DTC 5189 [at 7361], 2010 FCA 309, aff'd sub nom Fundy Settlement v. Canada, 2012 SCC 14

In the course of the reorganization of the share structure of a Canadian holding company ("PMPL") for a Canadian automotive business, two newly...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 157 |

Howson c. The Queen, 2007 DTC 141, 2006 TCC 644

Monies advanced by the taxpayer to a family trust were found to be a loan rather than a contribution of capital, notwithstanding that a loan...

Administrative Policy

2025 Ruling 2024-1042991R3 - Ruling - XXXXXXXXXX Agreement Payments

Background

Under an agreement with an Indian band, a third party agreed to make payments to the First Nation, including the First Milestone...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(6) | promissory note issued to Indian band (but not band members) to evidence undistributed income that was payable to them | 136 |

| Tax Topics - Income Tax Act - Section 3 - Paragraph 3(a) | milestone payment received by Indian band form resource company was not income to the band members when distributed to them | 97 |

10 October 2024 APFF Roundtable Q. 15, 2024-1028451C6 F - Paiement d’une dépense d’une fiducie et paragraphe 75(2) L.I.R.

Regarding whether the payment of professional fees by a trustee or beneficiary of a trust triggers the application of s. 75(2), CRA stated:

[T]he...

2024 Ruling 2023-0989121R3 F - Internal reorganization - 55(3)(a) and 55(3.01)(g)

Before Opco (whose shares were held by three unrelated individuals, Messrs. A, B and C) was to effect a real-estate spin-off to a new sister...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.01) - Paragraph 55(3.01)(g) | transfer of real estate to separate Realtyco beneath a newly-formed Holdco | 605 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | estate freeze transactions represented to be independent of subsequent transfer | 152 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) - Subparagraph 55(3)(a)(ii) | s. 55(3.01)(g) applied to the transfer (fresh after an estate freeze) by unrelated shareholders of Opco to a new Holdco, with an Opco realty spin-off to a new Realtyco sister | 274 |

4 June 2024 STEP Roundtable Q. 7, 2024-1003611C6 - AET and Subsection 75(2)

The trust deed for an alter ego trust provided that no capital distributions, including any capital gains, could be made while the settlor (who...

15 June 2022 STEP Roundtable Q. 11, 2022-0929331C6 - Joint Spousal or Common-law Partner Trust

After a joint spousal or common-law partner trust is created with a contribution of jointly-owned property by an individual and the individual’s...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 73 - Subsection 73(1.01) - Paragraph 73(1.01)(c) - Subparagraph 73(1.01)(c)(iii) | once a joint spousal etc. trust is established, the s. 73(1) rollover applies to non-jointly contributed property of a spouse | 93 |

15 June 2021 STEP Roundtable Q. 5, 2021-0883001C6 - Income Attribution from AET

Would s. 75(2) apply in the following independent scenarios?

(a) A taxpayer settles an alter ego trust and contributes an interest in a limited...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 82 - Subsection 82(2) | application of s. 82(2) where s. 75(2) applies to dividend income allocated by a partnership | 125 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(5) | substituted property rule does not apply to "second generation income" | 128 |

17 July 2019 Internal T.I. 2017-0718021I7 - Deregistration of TFSA

A trust lost its status as a tax-free savings account (“TFSA”) because it contravened the registration restriction on borrowing money. It...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 146.2 - Subsection 146.2(5) - Paragraph 146.2(5)(c) | s. 75(2) applied to TFSA when it ceased to qualify | 211 |

7 June 2019 STEP Roundtable Q. 12, 2019-0798301C6 - Attribution under 75(2)

CRA acknowledged that, in Satoma, Noël CJ. noted that express exclusions in most of the attribution provisions (e.g., s. 74.1) of the attributed...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 204 - Subsection 204(1) | Satoma has not changed the CRA view that trusts must report income that is attributed to the settlor under s. 75(2) | 290 |

29 May 2018 STEP Roundtable Q. 11, 2018-0748241C6 - Subsection 104(13.4)

For taxation years ending after 2015, where the lifetime beneficiary of an alter ego trust dies, the trust will have a deemed year end on the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(6) - Paragraph 104(6)(b) - Element B - Subparagraph (i) | s. 104(4) gain is taxable in an alter ego trust | 141 |

16 February 2017 Internal T.I. 2016-0669881I7 - 75(2) applicability to trust

Under the terms of the trust indenture for a family trust, the settlor is one of two original trustees, all decisions must be made unanimously,...

12 July 2016 External T.I. 2014-0560361E5 - Cdn beneficiary of US living trust

In the course of a general discussion of the Canadian tax treatment of a taxpayer holding an interest in a U.S. “living trust,” CRA stated:

A...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(1) | question of fact whether a U.S. revocable living trust is an excluded trust | 134 |

| Tax Topics - Income Tax Act - Section 126 - Subsection 126(1) | whether there is a foreign tax credit for US tax paid by the grantor of a revocable US living trust | 256 |

10 June 2016 STEP Roundtable Q. 13, 2016-0645811C6 - Filing Obligation for 75(2) trust

Reg. 204(1) provides that a trustee having control of or receiving income, gains or profits must file an information return – so that even...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 204 - Subsection 204(1) | s.75(2) trust generating losses need not file T3 returns | 200 |

2015 Ruling 2015-0610391R3 - Whether 75(2) will apply to new trusts

Terms of New Trusts

Two new trusts (the “New Trusts”) are settled by Mr. A and Mrs. A, respectively. The trustees of each New Trust consist...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 108 - Subsection 108(1) - Trust - Paragraph (g) | interests vested (but not distributed) before 21st anniversary | 144 |

13 April 2015 External T.I. 2012-0449141E5 F - Usufruct

A corporation sold the usufruct respecting a property to an arm’s length third party for use as a secondary residence, while retaining the bare...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107 - Subsection 107(2.1) | 107(2.1) application to termination of usufruct created for valuable consideration | 126 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(3) | application of trust provisions to creation of usufruct | 95 |

10 October 2014 APFF Roundtable, 2014-0538241C6 F - 75(2) and definition of "earned income" in 146(1)

5(a)

When a rental property has been transferred to a trust, is rental income attributed to the transferor under s. 75(2) transformed into trust...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 146 - Subsection 146(1) - Earned Income | character preservation of s. 75(2) attributed income | 122 |

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(3.6) | basis adjustment for denied capital loss (otherwise subject to s. 75(2) attribution) at trust level | 208 |

3 October 2014 External T.I. 2013-0476871E5 - Subsection 75(2)

Property settled on a trust includes an LP interest. On termination of the trust, the trust property will revert to the settlor. Will s. 75(2) not...

16 June 2014 STEP Roundtable, 2014-0523061C6 - Trust audit issues

2010-036630117 concerned the sole trustee and capital beneficiary of a trust (the taxpayer) who, had

transferred property to the trust by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(21) | capital gain distributed to different beneficiary | 137 |

| Tax Topics - Income Tax Act - Section 105 - Subsection 105(1) | benefit conferred when trust shares redeemed at undervalue | 196 |

| Tax Topics - Income Tax Act - Section 112 - Subsection 112(3.2) | taxpayer stuck with two-transaction form | 155 |

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(1) - Total Charitable Gifts | executors lacked power to make gift | 92 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Legal and other Professional Fees | legal and accounting expenses | 45 |

16 June 2014 STEP Roundtable, 2014-0523001C6 - Trusts structured to invoke 75(2)

An "evil trust" is structured to deliberately cause the application of subsection 75(2), so as to cause the attribution of dividend income to a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(13) | Brent Kern schemes don't work even if Sommerer issue fixed | 315 |

12 February 2014 Internal T.I. 2013-0508841I7 F - Application of subsection 75(2)

Corp transferred its limited partner interest in a limited partnership ("SEC") to Trust. It then applied s. 75(2) to attribute to itself the...

23 January 2014 External T.I. 2013-0500711E5 F - Paragraph 75(2)

The will of Mr. X provided for the bequeathing of some of his property to family inter vivos discretionary trusts. The liquidator (i.e., executor)...

11 October 2013 APFF Roundtable, 2013-0495721C6 F - APFF 2013- Round table question 7

Mr. X, who holds all the common shares of Corporation, exchanges his common shares under s. 51 for preferred shares having an equivalent fair...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Shares | FMV is a question of fact within TCC's discretion | 224 |

11 June 2013 STEP Roundtable Q. 9, 2013-0480351C6 - STEP CRA Roundtable Q9 - June 2013

Respecting whether CRA accepted Sommerer, it stated that the decision stood:

for the general proposition that where property is transferred to a...

23 May 2013 Internal T.I. 2013-0481651I7 F - Attribution rules- business loss

A trust, that was subject ot s. 75(2), incurred losses from stock trading, and treated the resulting losses (which CRA had accepted had been...

14 February 2013 Internal T.I. 2011-0424341I7 F - Amounts forwarded to trustee/beneficiary

The financial advisor of Mother settled a discretionary trust of which Mother and her friend (Y) were the trustees (with decisions to be made...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | s. 56(2) did not apply to trustee/beneficiary of discretionary trust who directed income to her children and did not exercise discretion in her own favour | 218 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(13) | income was received by children beneficiaries as agent for their mother | 263 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(6) - Paragraph 104(6)(b) | Quebec discretionary trust with two named trustees but, in fact, only one trustee, would not be entitled to s. 104(6)(b) deductions | 155 |

23 June 2010 External T.I. 2010-0365581E5 F - Règles d'attribution de l'article 74.2

An individual disposed of capital property to a discretionary trust (whose beneficiaries were the individual and spouse and their children) in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 74.5 - Subsection 74.5(1) - Paragraph 74.5(1)(c) | s. 74.2(1) inapplicable to transfer at FMV of property to a discretionary family trust, with capital gain on property subsequently distributed to spouse of transferor | 129 |

S4-F3-C1 - Price Adjustment Clauses

CRA will consider a price adjustment clause to represent pricing at fair market value if:

- the agreement reflects a bona fide intention of the...

5 July 2012 Internal T.I. 2010-0388551I7 F - Fiducie - retour de sommes

In finding that s. 75(2) did not apply to an estate freeze effected by Father in relation to shares of Holdco in favour of a family trust (the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 105 - Subsection 105(1) | income distributed to daughter-in-law who in fact was not a beneficiary includible in her income under s. 105(1) but not deductible by trust under s. 104(6) | 166 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(13) | capital gain distributed by family trust to children and purportedly lent by them to their parents (also beneficiaries) was instead included in the parents’ income under s. 104(13) | 419 |

| Tax Topics - Income Tax Act - Section 110.6 - Subsection 110.6(6) | Foisy test of mental element accepted | 238 |

4 March 2013 External T.I. 2011-0428661E5 - trust payments to minor

The trustees of a Quebec trust exercise their discretionary power in order to allocate an amount of income or taxable capital gain to a minor...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(24) | promissory note effecting payment of distribution potentially may be delivered after year end | 341 |

5 October 2012 APFF Roundtable, 2012-0453591C6 F - Prêt à une fiducie

The question described a situation where most of the income generated by a discretionary family trust was generated from investments made out of...

5 October 2012 APFF Roundtable, 2012-0453891C6 F - Price Adjustment Clause

A taxpayer (the “freezor”) exchanges his common shares of a corporation for preferred shares of the same corporation, with the purchase price...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | operation of freeze price adjustment clause depends on share actually being adjusted and can apply for s. 75(2) purposes | 337 |

28 November 2010 CTF Roundtable, 2010-0386351C6 - 2010 CTF Q#10 - T3 Reporting and 75(2)

The correspondent asked how to report income attributed to a non-beneficiary settlor under s. 75(2). CRA stated:

Where income is allocated...

20 October 2009 External T.I. 2009-0328441E5 F - Fiducie testamentaire

Under the terms of a deceased person's will, all property is bequeathed in equal shares to the deceased’s children. The heirs, in order to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(8) - Paragraph 248(8)(a) | unlikely to have been a distribution as a consequence of death where mooted testamentary trust formed by beneficiaries by their own agreement | 302 |

30 September 2009 External T.I. 2009-0317641E5 F - Attribution de revenu

Participating shares of Opco were issued to a discretionary trust ("Trust") as part of an estate freeze, and Opco then paid a dividend to the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(6) - Paragraph 104(6)(b) | discretionary trust could distribute, and deduct under s. 104(6), a dividend received by it to a corporate beneficiary incorporated after the dividend’s receipt | 128 |

23 June 2008 External T.I. 2008-0268121E5 F - 75(2) et Prêt consenti à une fiducie

An individual makes an interest-free loan to a discretionary trust of which such individual is one of the beneficiaries. The trust uses the...

23 April 2009 External T.I. 2008-0301241E5 F - Fiducie d'invest. à participation unitaire-75(2)

Units of a unit trust (“UT”) that does not qualify as a mutual fund trust (“MFT”) are issued for monetary consideration to subscribing...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(2) - Paragraph 53(2)(h) - Subparagraph 53(2)(h)(i.1) | CRA could extend IT-369R, para. 10 to avoid ACB reductions to unit trust units where s. 75(2) applies | 301 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | doubtful that s. 248(28)(a) can be applied to preclude ACB grind | 181 |

25 March 2009 External T.I. 2008-0300401E5 F - Fiducie en faveur de soi-même - prêt sans intérêt

Mr. X makes a non-interest bearing loan to an alter ego trust that was established for him. The terms of the loan were established independently...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(13.1) | s. 104(13.1) election generally available where no s. 75(2) application, which is not engaged by the individual’s payment of trust-level taxes | 357 |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(4.1) | s. 56(4.1) inapplicable to NIB loan made by individual to his alter ego trust | 139 |

| Tax Topics - General Concepts - Payment & Receipt | individual pays trust taxes when he receives trust distributions net of such taxes | 34 |

16 December 2008 External T.I. 2008-0279741E5 F - Renonciation au capital d'une fiducie

An individual transfers shares to a trust of which he is the trustee, and he, his wife and children are the capital and income beneficiary. Would...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(9) - Disclaimer | legally impossible for a beneficiary of a discretionary trust to partially renounce income from a specific trust property | 262 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition - Paragraph (i) | non-disposition distribution of non-taxable portion of trust capital gains avoids a gain under s. 107(2.1) | 375 |

| Tax Topics - Income Tax Act - Section 54 - Proceeds of Disposition | settlor’s renunciation of capital interest (but not income interest) prior to trustees’ exercise of discretion to distribute a capital gain would generate nil proceeds and not engage s. 56(2) or (4) | 194 |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(b) | s. 69(1) does not apply to a renunciation of trust capital interest since no disposition "to" any person | 44 |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | s. 56(2) inapplicable to renunciation of capital interest in a trust | 45 |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(4) | s. 56(4) inapplicable to disclaimer of capital interest in a trust | 43 |

9 March 2007 External T.I. 2006-0218501E5 F - Application de 75(2) lors d'une émission d'actions

Would s. 75(2) apply to dividends on shares of a corporation that are subscribed for by a trust where the corporation subsequently could become a...

11 September 2006 STEP Roundtable Q. 4, 2006-0185571C6 - 2006 STEP Conference -Question 4

Although CRA does not apply s. 75(2) to a genuine loan of cash to the trust, this position does not extend to a loan of income-producing property...

2 February 2006 External T.I. 2005-0127351E5 F - Fiducie révocable -Prêt authentique

Regarding the situation where a trust receives bank loans that are guaranteed by Mr. A, who along with his spouse is a trustee, CRA noted:

[A]...

2004 Ruling 2004-006020

Ruling re attribution of income to a First Nation (which was exempt under s. 149(1)(c)) from investments transferred by it and exclusion of such...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 149 - Subsection 149(1) - Paragraph 149(1)(c) | 42 |

13 August 2004 Internal T.I. 2004-0076861I7 F - Investissement à l'étranger

A resident individual (the taxpayer) lent a sum to a Barbados borrower pursuant to a debenture contract. Although this characterization was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(c) | return payable on maturity that was not expressed as a percentage or fraction qualified as interest | 263 |

| Tax Topics - Income Tax Act - Section 108 - Subsection 108(2) - Paragraph 108(2)(a) | suspension of redemption right for more than one year would disqualify as s. 108(2)(a) trust | 131 |

3 August 2004 External T.I. 2004-0066431E5 F - Contrat de rente et fiducie

In 2003-004063 CRA concluded that s. 75(2) applied to a donor who, under a charitable annuity arrangement, transferred an amount to a trust in...

13 July 2004 External T.I. 2004-0058141E5 F - Transfert du droit aux revenus provenant d'un bien

A couple transferred, to their jointly-owned corporation, the right to receive the income from a Quebec rental property for a specified period, in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(3) | assignment of the rents from a rental property to a corporation would result in a disposition to a deemed trust under s. 248(3) | 134 |

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) | rollover not available to assignment of the rents from a rental property to a corporation for shares since the transferee was a deemed trust under s. 248(3) | 68 |

29 January 2004 External T.I. 2003-0040631E5 F - Rente de bienfaisance : contrat ou fiducie

Under a "charitable annuities" arrangement, the excess of the amount paid to a trust (a charitable organization) by a donor (who is not a trust...

15 December 2003 External T.I. 2003-0182855 - Fiducie pour Loi au Quebec

Regarding the application of s. 75(2) to a trust of which the settlor was the sole beneficiary, CCRA stated:

Where the income of the trust is...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(3) - Paragraph 248(3)(e) | meaning of “a right as a beneficiary in a trust” is found in s. 248(25) | 184 |

| Tax Topics - General Concepts - Ownership | sole beneficiary of Quebec trust is the beneficial owner of its property | 273 |

| Tax Topics - Income Tax Act - Section 73 - Subsection 73(1.02) - Paragraph 73(1.02)(b) - Subparagraph 73(1.02)(b)(ii) | no change in beneficial ownership on transfer of property to self-benefit Quebec trust | 171 |

18 July 2003 External T.I. 2002-0162985 F - Renonciation et bénéficiaire

A holding company owned by the parents transfer shares of an operating company to a family trust (Trust A) with the parents and children as...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107 - Subsection 107(4.1) - Paragraph 107(4.1)(b) | s. 107(4.1)(b) exclusion applicable if s. 75(2) was applicable at any time | 166 |

4 June 2003 Internal T.I. 2003-0006967 F - Province de résidence d'une fiducie

A trust resident in Quebec avoided tax by making the election under s. 104(13.1) to be deemed to retain its income (notwithstanding its actual...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 2 - Subsection 2(1) | Thibodeau applied to find that trust with Quebec trustee therefore was resident in Quebec | 162 |

| Tax Topics - Income Tax Act - Section 120 - Subsection 120(2) | Quebec abatement available even where no Quebec tax was payable on the income (due to abuse of s. 104(13.1) election) | 145 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(1) - Tax Benefit | scheme generating Quebec abatement without payment of any Quebec tax did not result in a “tax benefit” | 146 |

7 February 2003 External T.I. 2002-012676A - Attribution of NPI Royalty Income

A trust of which the settlor and family members are beneficiaries uses the settlement proceeds to buy a net profits interest in a particular oil...

25 September 2000 External T.I. 2000-0025855 - PRIVATE FOUNDATION - NOVA SCOTIA LIMITED

A Nova Scotia company limited by guarantee would not constitute a trust for purposes of s. 75(2). Corporations incorporated under the Nova Scotia...

24 January 2000 External T.I. 1999-0008275 F - APPLICATION DU PARAGRAPHE 75(2)

Mr. A settled an inter vivos discretionary trust of which his son and spouse were the beneficiaries and for which there were three trustees,...

13 October 1999 External T.I. 9832385 - ATTRIBUTION TO CONTRIBUTOR TO A TRUST

Where the settlor of a trust changes his common shares of a corporation into preferred shares and the trust then subscribes for common shares, s....

6 July 1998 External T.I. 9811115 - ATTRIBUTION & GENUINE LOAN

Discussion of when a loan of money by a parent to a trust will qualify as a "genuine loan" so that s. 75(2) does not apply.

May 1998 Advance Life Underwriting Round Table, No. 9807000

Where property held by an RCA trust may revert to the employer corporation that settled the trust, e.g., where employees do not satisfy vesting...

3 December 1997 External T.I. 9622765 - NON-RESIDENT TRUST - ATTRIBUTION

RC noted that, notwithstanding a previous memorandum, it was now its position that "in circumstances where the conditions for the application of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 94 - old | 43 |

10 January 1996 External T.I. 9406865 - NON RESIDENT DISCRETIONARY TRUSTS

Unlike s. 94(1), there is no mechanism for the utilization of foreign tax credits by a person to whom income is attributed under s. 75(2).

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 94 - old | 103 |

21 August 1995 External T.I. 9514275 - 75(2) - ESTATE FREEZE- SUBCRIPTION OF SHARES BY A TRUST

S.75(2) would apply where under the trust agreement, decisions are made by majority vote and the affirmative vote of the settlor must be included...

23 June 1995 External T.I. 9508185 - ATTRIBUTION OF INCOME TO A TRUST

Where contributions made by members of a union to a benefit plan (that was established by the union in accordance with a collective agreement),...

14 June 1994 External T.I. 9405845 - TRUST PROPERTY ACQUIRED BY MORTGAGE

S.75(2) would not apply where a trust acquires a property from an arm's length vendor (who is not a trustee or beneficiary of the trust) in...

28 April 1994 External T.I. 9411115 - ATTRIBUTION

"Where subsection 75(2) of the Act applies to attribute income to a person, that income is never income of the trust for tax purposes and...

27 January 1994 External T.I. 9332575 F - Attribution of Income

S.75(2) will apply where the terms of the trust provide that the transferor of property to the trust (including a transfer for fair market value...

26 September 1994 APFF Roundtable Q. 24, 9422630 F - DROIT D'ACQUÉRIR DE NOUVEAU LE BIEN TRANSFÉRÉ

"The Department considers that subsection 75(2) of the Act could apply if the deed of trust or any other contract between the trustees and a...

1994 I.C.A.A. Round Table, Q.4

Where s. 75(2) applies to the settlor of a non-resident trust who becomes a resident of Canada, income or loss from property settled on the trust...

19 May 1993 T.I. (Tax Window, No. 31, p. 13, ¶2528)

Where a trust indenture allows the settlor to reacquire the contributed property, s. 75(2) will apply even where the relevant provision can apply...

13 January 1993 T.I. (Tax Window, No. 28, p. 20, ¶2380)

A loan to a trust which is a genuine loan as discussed in IT-258R2, paragraph 8 and IT-260R, paragraph 3 would not be considered to result in...

11 August 1992, T.I. 921396 (May 1993 Access Letter, p. 197, ¶C56-226)

S.75(2) would apply if the transferor retains the power to veto distributions of property to beneficiaries or could select beneficiaries from a...

22 July 1992, T.I. 920736 (March 1993 Access Letter, p. 71, ¶C56-219)

Where unanimity was required in respect of any decision by the two trustees of a trust and the settlor was a trustee, s. 75(2)(b) would...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107 - Subsection 107(4.1) | 26 |

1992 A.P.F.F. Annual Conference, Q. 19 (January - February 1993 Access Letter, p. 57)

S.75(2) will apply to a taxpayer who establishes a usufruct for another person with respect to property of which the taxpayer is the naked owner.

19 June 1992 T.I. 9218450 (January - February 1993 Access Letter, p. 20, ¶C56-212)

S.75(2) can apply by virtue of a right of the contributor of property to reacquire that property at fair market value.

16 June 1992 External T.I. 5-920008

S.75(2) will apply where the settlor is able to select additional beneficiaries or delete beneficiaries after the creation of the trust.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 2800 - Subsection 2800(3) | 61 |

27 February 1992 T.I. (Tax Window, No. 17, p. 8, ¶1766)

S.75(2) will apply where the settlor, in his capacity of sole trustee, has the discretion as to whom the trust property will be distributed on a...

91 C.R. - Q.8

A genuine loan to a trust, or the unpaid purchase price for a property on an unconditional bona fide sale, will not by itself be considered to...

90 C.R. - Q23

Where a law firm receives funds from its clients to be held in trust pending the application of the funds for disbursements or against fees for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 201 - Subsection 201(2) | 97 |

16 November 89 T.I. (April 90 Access Letter, ¶1175)

Father settles an irrevocable trust of which he is the sole trustee and whose terms are totally discretionary as to income and capital payments,...

88 C.R. - Q.32

Because a bare trust is reversionary and revocable, all income, losses, capital gains and capital losses will be attributed to the transferor.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(2) | 26 |

88 C.R. - Q.48

Capital gains attributed to the transferor by virtue of s. 75(2) are not eligible for the capital gains exemption.

86 C.R. - Q.46

A reversion requires a transfer of property, and the making or repayment of a loan does not constitute a transfer of property.

84 C.R. - Q.30

S.75(2)(b) may apply where the trustee may amend the dispositions of the trust deed with the approval of the settlor.

IT-369R "Attribution of Trust Income to Settlor"

1. ...A genuine loan to a trust would not...by itself result in the application of subsection 75(2)..., if the loan is outside and independent of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | 26 |

Articles

Elie Roth, Tim Youdan, Chris Anderson, Kim Brown, "Classification of Trusts for Income Tax Purposes", Chapter 2 of Canadian Taxation of Trusts (Canadian Tax Foundation), 2016.

Waiver by spouse of entitlement to income under spousal trust (p. 92)

The terms of a spousal or common-law partner trust may include a provision...

Carmen Thériault, "Alter Ego and Joint Partner Trust", 21 Estates, Trusts & Pensions Journal, p. 345.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(4) - Paragraph 104(4)(a) | 0 |

Darling, "Bare Trusts", 1989 Corporate Management Tax Conference, c. 8.

Saunders, "Inter Vivos Discretionary Family Trust: A Potpourri of Issues and Traps", 1993 Conference Report, pp. 37:6-14.

Paragraph 75(2)(a)

Subparagraph 75(2)(a)(i)

Administrative Policy

11 July 2001 External T.I. 2001-0078365 F - APPLICATION DE 75(2) ET 104(4)

Does s. 75(2) apply where the transferor of a property to an inter vivos trust may, under the terms of the trust indenture, be paid the capital...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(4) - Paragraph 104(4)(a) | deemed disposition date for "joint spousal or common-law partner trust" is the later of date of death of settlor and settlor's spouse/ common-law partner, irrespective of being "spousal trust" | 151 |

8 November 2001 External T.I. 2001-0096435 F - Sous-alinéa 75(2)(a)(i) de la Loi

Ms. X created a spousal trust for her trust. It was posited that the trust terminated by operation of law pursuant to Arts. 1294 and 1296 of the...

Subsection 75(3) - Exceptions

Cases

Labow v. Canada, 2012 DTC 5001 [at at 6501], 2011 FCA 305

The taxpayer, who employed both his wife and two part-time employees in his medical practice, deducted $150,000 and $247,691 for contributions he...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 108 - Subsection 108(1) - Trust - Paragraph (a.1) | 213 | |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | settlor with power to dismiss trustee | 84 |