Subsection 245(0.1)

Administrative Policy

17 May 2023 IFA Finance Update

First 2 paras. are restatements from original GAAR materials

- The first two paragraphs in s. 245(0.1) were restatements of those made...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) - Paragraph 245(3)(b) | 174 | |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4.1) | 260 |

Subsection 245(1) - Definitions

Tax Benefit

Cases

Magren Holdings Ltd v. Canada, 2024 FCA 202

The taxpayers were private companies controlled by a resident individual (Grenon), whose RRSP held 58% of the units of a publicly traded income...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | it is an abuse of the capital gains system to recognize a capital gain increment to a CDA account when there was no net change in economic position | 566 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(2) | it is reasonable to assess a 60% tax under s. 245(2) if that was the quantum of tax whose avoidance represented the tax benefit | 212 |

| Tax Topics - General Concepts - Ownership | RRSP trust transferred the ownership of the income fund units in which it transacted | 325 |

| Tax Topics - General Concepts - Sham | finding of sham must consider what are in fact the real transactions | 50 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition - Paragraph (e) | transfer of property by a trust is a disposition unless to an agent | 114 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(6) | capital gain can be distributed on a redemption of units | 298 |

The Gladwin Realty Corporation v. Canada, 2020 FCA 142

Noël CJ determined that transactions that generated a capital dividend to the taxpayer that was approximately double the capital gain generated...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | generating and utilizing a CDA increase whose subsequent reversal would never matter was abusive | 597 |

Canada v. Bank of Montreal, 2020 FCA 82

On unwinding a tower structure, a Nevada subsidiary LP of BMO realized FX gains on repaying U.S.-dollar borrowings, but completely offset that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(2) | former s. 39(2) extended to FX gains on s. 39(1) dispositions | 495 |

| Tax Topics - Income Tax Act - Section 112 - Subsection 112(3.1) | s. 39(2) deeming of loss to be from FX rather than shares applied to s. 112(3.1) | 463 |

| Tax Topics - Statutory Interpretation - Interpretation/Definition Provisions | deeming provision applied to all provisions of the Act where it was not explicitly limited | 396 |

Fiducie financière Satoma v. Canada, 2018 FCA 74

In order to strip surplus of an operating corporation (“Gennium”) controlled by the Pilon family, a dividend paid by Gennium was distributed...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | using ss. 75(2) and 112(1) for tax-free dividends to trust thwarted s. 112(1) object to tax earnings when ultimately distributed | 319 |

| Tax Topics - Income Tax Act - Section 3 | pervasive rule that the same income is not to be taxed in 2 persons’ hands | 148 |

| Tax Topics - Statutory Interpretation - Double Taxation/Deduction (Presumption Against) | inclusion of income in more than one taxpayer’s hands is contrary to s. 3 | 294 |

| Tax Topics - Income Tax Act - Section 112 - Subsection 112(1) | abusive to use s. 112(1) so as to avoid ultimate taxation of individuals | 180 |

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(2) | use of s. 75(2) to access s. 112(1) deduction for dividend in fact received by family trust, was abusive | 286 |

| Tax Topics - Income Tax Act - Section 82 - Subsection 82(2) | s. 82(2) supports the primacy of s. 75(2) over the actual dividend recipient | 60 |

Copthorne Holdings Ltd. v. Canada, 2012 DTC 5006 [at at 6536], 2011 SCC 63, [2011] 3 S.C.R. 721

The taxpayer's shareholders circumvented the rule in s. 87(3), which required that the paid-up capital ("PUC") of a subsidiary corporation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Stare Decisis | high threshold for reversing not met | 193 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | policy of s. 87(3) is to avoid preservation of PUC on parent and sub amalgamation | 372 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | "in contemplation" could be retrospective | 341 |

| Tax Topics - Statutory Interpretation - Expressio Unius est Exclusio Alterius | implied exclusion principle | 109 |

Canada Trustco Mortgage Co. v. Canada, 2005 SCC 54, [2005] 2 S.C.R. 601, 2005 DTC 5523

McLachlin C.J. and Major J. stated (at para. 20):

If a deduction against taxable income is claimed, the existence of a tax benefit is clear, since...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | policy of CCA provisions relied on cost irrespective of risk mitigation | 211 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | "in contemplation" references "because of" or "in relation to" | 127 |

| Tax Topics - Statutory Interpretation - Certainty | interpretive approach should be consistent with tax law being certain, predictable and fair, | 131 |

| Tax Topics - Statutory Interpretation - Ordinary Meaning | primacy to ordinary meaning if unequivocal | 96 |

Canadian Pacific Ltd. v. The Queen, 2000 DTC 2428, [2001] 1 CTC 2190 (TCC), rev'd 2001 FCA 398

In finding that there was a tax benefit to the taxpayer in borrowing in Australian dollars at a higher rate than would be applicable to a...

See Also

Madison Pacific Properties Inc. v. The King, 2023 TCC 180

The appellant (“MPP”) was an insolvent, publicly traded, mining company with accumulated net capital losses of $72.7 million. In order for two...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | acquisition of close to legal control of a Lossco by two arm’s length companies in a different business to access its losses was an abuse | 452 |

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(4) | two acquirers of most of the equity of a Lossco were acting in concert so as to constitute a group | 465 |

Husky Energy Inc. v. The King, 2023 TCC 167, aff'd sub nomine Hutchison Whampoa Luxembourg Holdings S.À R.L. 2025 FCA 176

Before a Canadian public corporation (“Husky”) paid a dividend on its shares, two significant shareholders of Husky resident in Barbados (the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 10 | recipient of dividends on borrowed shares was not their beneficial owner because of requirement to pay dividend compensation payments | 270 |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(2) | tax under s. 212(2) imposed on the basis of payment of dividend to a non-resident rather than on the basis of who is the beneficial owner | 405 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | the residence, beneficial owner, and voting requirements in the Canada-Luxembourg Treaty fully expressed the rationale for the 5% Treaty-reduced rate on dividends | 413 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | transactions were carried out to reduce Part XIII tax rather than avoid Barbados income tax | 131 |

Damis Properties Inc. v. The Queen, 2021 TCC 24

Five corporate taxpayers sought to increase their after-tax return from the sale by their farm partnerships of the farm by transferring their...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | s. 160 did not apply to a sale of companies holding cash sales proceeds to a purchaser who purported to eliminate the tax liability | 785 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | no avoidance transaction where there was no intention to avoid the provision purportedly abused | 339 |

| Tax Topics - Income Tax Regulations - Regulation 1102 - Subsection 1102(1) - Paragraph 1102(1)(c) | software was not acquired with an income-producing purpose | 282 |

| Tax Topics - General Concepts - Onus | unfair to place the onus on taxpayer re facts which taxpayer could not reasonably be expected to know | 339 |

Rogers Enterprises (2015) Inc. v. The Queen, 2020 TCC 92

Various transactions were implemented to ensure that, at the death of Ted Rogers in 2008, a Canadian-controlled private corporation (“CGESR”)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | taking full credit to the CDA for insurance proceeds received, notwithstanding a positive ACB of the policyholder, reflected the policy of the CDA text | 415 |

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Capital Dividend Account - Paragraph (d) - Subparagraph (d)(iii) | 2016 amendment changed the law so as to reduce CDA bump by policyholder’s ACB | 259 |

The Bank of Montreal v. The Queen, 2018 TCC 187, aff'd 2020 FCA 82

The taxpayer (BMO) used a tower structure for a U.S.$1.4 billion financing of its U.S. subsidiaries in which a subsidiary Nevada LP of BMO applied...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(2) | pre-2011 version of s. 39(2) extended to capital property dispositions as well as capital obligation settlements | 699 |

Fiducie Financière Satoma v. The Queen, 2017 TCC 84, aff'd 2018 FCA 74

In order to strip surplus of an Opco, Opco (indirectly) paid dividends to Holdco 1, which made a capital contribution of those funds to Holdco 2,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | use of s. 75(2) attribution rule and s. 112(1) DRD to extract surplus to a family trust was abusive | 569 |

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(2) | s. 75(2) application ousts dividend inclusion to income recipient (in absence of GAAR) | 114 |

Gervais v. The Queen, 2016 TCC 180, aff'd 2018 FCA 3

The taxpayer’s wife (Mrs. Gendron) purchased 1.04M preferred shares from the taxpayer (Mr. Gervais) at a cost of $1.04M (with Mr. Gervais not...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | basis averaging scheme to transfer half of a capital gain to the taxpayer’s wife was an abuse of the attribution rules | 429 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | comparison with outright sale and gift | 193 |

MacDonald v. The Queen, 2012 TCC 123, rev'd 2013 DTC 5091 [at 5982], 2013 FCA 110

The emigration of the Canadian taxpayer to the United States would have caused the shares of his wholly- owned New Brunswick corporation ("PC") to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | no abuse in surplus stripping if integration | 368 |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | 354 |

Administrative Policy

4 June 2003 Internal T.I. 2003-0006967 F - Province de résidence d'une fiducie

A trust resident in Quebec avoided tax by making the election under s. 104(13.1) to be deemed to retain its income (notwithstanding its actual...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 2 - Subsection 2(1) | Thibodeau applied to find that trust with Quebec trustee therefore was resident in Quebec | 162 |

| Tax Topics - Income Tax Act - Section 120 - Subsection 120(2) | Quebec abatement available even where no Quebec tax was payable on the income (due to abuse of s. 104(13.1) election) | 145 |

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(2) | s. 75(2)(a)(i) inapplicable re settlor being beneficiary of trust beneficiary’s estate/ s. 75(2)(b) inapplicable re power of settlor to replace trustees | 303 |

93 C.M.TC - Q. 11

Where a non-resident of Canada enters into a series of transactions designed primarily to secure an exemption or reduction from Canadian tax under...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 12 | 65 |

Transaction

Cases

Canada v. Canadian Pacific Ltd., 2002 DTC 6742, [2002] 3 F.C. 170, 2002 FCA 98

The Crown argued that CP's act of denominating the debentures in Australian dollars was in and of itself a transaction and that it amounted to an...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | primary purpose of a borrowing in a tax-advantageous currency was to raise money | 290 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | transaction not to be recharacterized until after a determination of abuse | 283 |

R. v. Goldstein (1988), 42 C.C.C. (3d) 548 (Ont CA)

With respect to the interpretation of s. 548(1) of the Criminal Code, Houlden J.A. stated (p. 557) "the words 'the same transaction', in my...

See Also

MNR v. Granite Bay Timber Co. Ltd., 58 DTC 1066, [1958] CTC 117 (Ex Ct), briefly aff'd 59 DTC 1262 (SCC)

In finding that a resolution of the shareholders to wind-up a company was a "transaction" for purposes of s. 8(3) of the 1948 Act, Thurlow J....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | the shareholders had a common purpose in determining to wind-up the company | 223 |

Finance

Modernizing and Strengthening the General Anti-Avoidance Rule, Department of Finance Consultation Paper, 11 August 2022

Extending “transaction” to include a choice

- Given the findings in Canadian Pacific and Spruce Credit (pp. 10-11), it may be appropriate to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | 130 | |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 904 |

Subsection 245(2) - General anti-avoidance provision

Cases

Canada v. DAC Investment Holdings INC., 2026 FCA 35

With a view to its imminent disposition of the shares of a subsidiary, the taxpayer continued to the British Virgin Islands. As a result, it...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | it was an abuse of s. 250(5.1) and of ss. 123.3 and 123.4 for a CCPC to continue to BVI before realizing a capital gain | 370 |

| Tax Topics - Income Tax Act - Section 123.3 | rationale of ss. 123.3 and 123.4 included avoidance of tax deferral on investment income | 180 |

Magren Holdings Ltd v. Canada, 2024 FCA 202

The taxpayers were private companies controlled by a resident individual (Grenon), whose RRSP held 58% of the units of a publicly traded income...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | it is an abuse of the capital gains system to recognize a capital gain increment to a CDA account when there was no net change in economic position | 566 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(1) - Tax Benefit | avoidance of Pt. III tax liability was a tax benefit | 529 |

| Tax Topics - General Concepts - Ownership | RRSP trust transferred the ownership of the income fund units in which it transacted | 325 |

| Tax Topics - General Concepts - Sham | finding of sham must consider what are in fact the real transactions | 50 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition - Paragraph (e) | transfer of property by a trust is a disposition unless to an agent | 114 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(6) | capital gain can be distributed on a redemption of units | 298 |

Quinco Financial Inc. v. Canada, 2018 FCA 137

Webb JA rejected a submission that no interest accrued by virtue of a GAAR reassessment between the balance-due date of a taxation year for which...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 161 - Subsection 161(1) | interest is added as usual to a GAAR assessment | 322 |

| Tax Topics - Income Tax Act - Section 157 - Subsection 157(1) - Paragraph 157(1)(b) | GAAR assessment for prior year was payable as at the balance-due date | 182 |

Canada v. Oxford Properties Group Inc., 2018 FCA 30

If the taxpayer had sold three buildings directly to tax-exempt purchasers, it would have realized recapture of depreciation of $116M and a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | using the s. 88(1)(d) bump on newly-formed rental property LPs to avoid indirect recapture income under s. 100(1) was abusive | 975 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(d) | s. 88(1)(d) bump is intended to permit the transfer of ACB that otherwise would be lost to another property that is taxed in the same way | 371 |

| Tax Topics - Income Tax Act - Section 98 - Subsection 98(3) - Paragraph 98(3)(c) | s. 98(3)(c) bump is intended to avoid gain realization where there has been no economic gain | 267 |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(11) | 3-year time limitation in s. 69(11) did not establish safe harbor for avoidance of recapture on sale after that period | 382 |

| Tax Topics - Income Tax Act - Section 100 - Subsection 100(1) | purpose is to ensure that latent recapture will be recognized on sale to tax exempt | 254 |

| Tax Topics - Income Tax Act - Section 97 - Subsection 97(2) | object includes ultimate taxation of the deferred gain | 234 |

| Tax Topics - Income Tax Act - Section 171 - Subsection 171(1) | GAAR question as to determining a provision’s object was subject to correctness standard | 169 |

| Tax Topics - Statutory Interpretation - Hansard, explanatory notes, etc. | statement that amendment was for “clarification” was self-serving | 209 |

| Tax Topics - Statutory Interpretation - Interpretation Act - Subsection 45(2) | determination of whether amendment merely clarified requires review of pre-amendment state of law | 146 |

Winter v. The Queen, 90 DTC 6681, [1991] 1 CTC 113 (FCA)

Marceau J.A. accepted the following submission of Mr. Cumyn (p. 6683):

"There is a natural order to the provisions of the Income Tax Act with...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | s. 56(2) applied to taxpayer rather than 15(1) to son-in-law as de minimis shareholder | 74 |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | s. 56(2) inapplicable if actual transferee was taxable on the amount | 171 |

See Also

Harvard Properties Inc. v. The King, 2024 TCC 139

Boyle J found that the taxpayer’s transactions had subjected it to a liability under s. 160 for the tax liability of a person with whom it was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | sale of shares, in a structured transaction, at a price that did not reflect a discount for the underlying accrued taxes, was indicative of non-arm's length dealing | 643 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | transaction premium to a share-sale valuation was not reflective of ordinary commercial dealings | 431 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | avoidance on a non-arm’s length relationship so as to avoid the application of s. 160 would be a GAAR abuse | 434 |

| Tax Topics - General Concepts - Fair Market Value - Shares | shares of company whose only assets were escrowed for an imminently-closing sale transaction did not have any value | 285 |

Univar Holdco Canada ULC v. Canada, 2017 FCA 207

The application of s. 212.1 to the distribution of a Canadian subsidiary of Univar NV immediately following an arm’s length acquisition of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.1 - Subsection 212.1(4) | using old s. 212.1(4) to extract surplus from a non-resident target’s Canadian sub was not abusive | 371 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | cross-border surplus-stripping transaction was not abusive as it occurred in same series as arm's length acquisition | 404 |

594710 British Columbia Ltd. v. The Queen, 2016 TCC 288, rev'd 2018 FCA 166

Income account treatment of the profits realized by a condo-project limited partnership (HLP) was avoided through the corporate partners (the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | indirect transfer of property to taxpayer did not entail departure from FMV | 462 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | GAAR did not apply to the sale to a lossco of partner corps with pending condo sale profit allocations | 660 |

| Tax Topics - Income Tax Act - Section 96 - Subsection 96(1) - Paragraph 96(1)(f) | LP profits can be allocated to purchasing partner at year end | 278 |

Quinco Financial Inc v. The Queen, 2016 TCC 190, aff'd 2018 FCA 137

On similar facts, Bocock J followed J.K. Read in rejecting a taxpayer argument that as a taxpayer could not apply GAAR to itself without CRA...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 161 - Subsection 161(1) | interest on GAAR assessment accrues from the day after the balance-due date | 221 |

CIT Financial Ltd. v. The Queen, 2003 DTC 1138, 2003 TCC 544

Bowman A.C.J. noted that GAAR should not be applied if other sections of the Act are effective to eliminate the beneficial tax results sought by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Other | 88 | |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(a) | 88 |

C.I.R. (New Zealand) v. Challenge Corporation Ltd., [1986] BTC 442 (PC)

The taxpayer acquired all the shares of a corporation ("Perth") with $5.8 million of tax losses from an arm's length vendor for a purchase price...

Administrative Policy

2022 Ruling 2022-0937661R3 F - 104(4) and pipeline transaction

The Directorate considered that a distribution of the property of a trust under s. 107(2) before its 21st anniversary to a corporate beneficiary...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | pipeline transaction to raise the funds for the application of the CRA s. 104(5.8) GAAR position to an inter vivos trust used to try to avoid the 21-year deemed disposition | 653 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(5.8) | GAAR applicable to trust holding a corporate beneficiary that was distributed property from an inter vivos trust approaching its 21st anniversary | 116 |

7 October 2022 APFF Roundtable Q. 8, 2022-0942151C6 F - Surplus stripping

In order for Brother to avoid the application of s. 84.1 to his sale of half the shares of Opco to his sister’s corporation (Sister-Holdco), he...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) | incorporating a sub through which a share sale will occur so as to avoid s. 84.1 is not per se GAARable | 179 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.11) | range of factors considered | 182 |

Alexandra MacLean, "CRA Audits of Large Corporations - The view from ILBD" under Responses to recent adverse decisions – Wild, 27 November 27 2018 CTF Annual Conference.

Wild found that transactions that boosted the paid-up capital of shares held by the taxpayer should not be addressed by applying the general...

29 November 2016 CTF Roundtable Q. 7, 2016-0672091C6 - GAAR Assessment Process

In discussing the role of the GAAR Committee, CRA indicated that where the transactions under audit by the Tax Services Office are similar to...

Articles

Anthony V. Strawson, Trent J. Blanchette, "GAAR Amendment Targets Tax Attributes Before They Are Used", Tax for the Owner-Manager, Vol. 22, No. 3, July 2022, p. 6

Amendments to include future use of attributes (p. 6)

- Draft amendments to override the Wild line of cases would extend the concept of “tax...

D. Sandler, J. Li, "The Relationship between Domestic Anti-Avoidance Legislation and Tax Treaties", 1997 Canadian Tax Journal, Vol. 45, No. 5, p. 891.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions | 0 | |

| Tax Topics - Treaties - Income Tax Conventions - Article 3 | 0 |

Subsection 245(3) - Avoidance transaction

Cases

Canada (The King) v. MICROBJO PROPERTIES INC., 2023 FCA 157

The taxpayers, who were holding companies for partnerships that had recently agreed to sell their farmlands to third parties, were approached by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | a transaction that split, on the purchaser’s terms, a tax savings purportedly generated by it, was a non-arm’s length transaction | 701 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | parties were not dealing at arm's length in transactions where they did not put their own patrimony in play | 370 |

| Tax Topics - Statutory Interpretation - Interpretation Act - Subsection 45(2) | subsequent amendment confirmed the prior state of the law | 82 |

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(5) | s. 160(5) did not change the prior view that prior facts could be taken into account | 96 |

2763478 Canada Inc. v. Canada, 2018 FCA 209

Prior to the sale of a corporation ("Groupe AST") to a third party, its individual shareholder (“Jobin”) transferred his shares of Groupe AST...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | 9 month separation did not avoid series | 290 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | value shift transactions that permitted the absorption of a real gain by a paper loss abused the basic capital gains regime | 317 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(6) | individual allegedly suffering double taxation re s. 245(2) denial of capital loss of his corporation failed to apply under s. 245(6) within 180 days | 327 |

Canada v. Spruce Credit Union, 2014 DTC 5079 [at at 7044], 2014 FCA 143

The taxpayer and 53 other BC credit unions maintained their required deposit insurance with two corporations ("CUDIC" and "STAB"). Due to a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 137.1 - Subsection 137.1(4) - Paragraph 137.1(4)(c) | allocations in proportion to shareholdings rather than premiums | 304 |

1207192 Ontario Limited v. Canada, 2012 DTC 5157 [at at 7396], 2012 FCA 259, aff'g 2011 DTC 1301 [at 1686], 2011 TCC 383

In the course of applying s. 245 to deny the recognition by the taxpayer of a capital loss, the Court considered and rejected the argument of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | capital loss from value shift did not reflect economic loss; purpose objectively determined | 451 |

Canada Safeway v. Alberta, 2012 DTC 5133 [at at 7271], 2012 ABCA 232

The taxpayer implemented a series of transactions that gave rise to interest deductions in Alberta, with the interest income being received free...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | replacing equity with borrowed money to reduce provincial income not abusive | 285 |

Canada v. Mackay, 2008 DTC 6238, 2008 FCA 105

In order for the taxpayers to acquire an interest in a shopping centre, a bank which held mortgages on the centre that were in foreclosure...

Canada v. Canadian Pacific Ltd., 2002 DTC 6742, [2002] 3 F.C. 170, 2002 FCA 98

The taxpayer borrowed 216 million in Australian dollars under debentures bearing interest at 16.125% per annum and that had been issued at a 2%...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | transaction not to be recharacterized until after a determination of abuse | 283 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(1) - Transaction | an aspect of a transaction is not a transaction | 249 |

OSFC Holdings Ltd. v. Canada, 2001 DTC 5471, 2001 FCA 260

After becoming insolvent, a company ("Standard") in the mortgages business established a partnership, transferred a mortgage portfolio to the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | policy against corporate loss trading | 229 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | s. 248(10) assimilates a subsequent transaction to a common-law series if it has some connection with the series and is completed in contemplation thereof | 344 |

| Tax Topics - Statutory Interpretation - Interpretation Bulletins, etc. | 70 | |

| Tax Topics - Statutory Interpretation - Interpretation/Definition Provisions | deeming v. definition provisions | 46 |

See Also

British Columbia v. Peakhill Capital Inc., 2024 BCCA 246

The Province appealed from an order pronounced in a receivership under the Bankruptcy and Insolvency Act (Canada) approving a reverse vesting...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Other Legislation/Constitution - Federal - Bankruptcy and Insolvency Act - Section 243 | bankruptcy receiver had the jurisdiction under BIA s. 243 to make a reverse vesting order whose purpose was to avoid BC land transfer tax | 357 |

Husky Energy Inc. v. The King, 2023 TCC 167, aff'd sub nomine Hutchison Whampoa Luxembourg Holdings S.À R.L. 2025 FCA 176

Before a Canadian public corporation (“Husky”) paid a dividend on its shares, two significant shareholders of Husky resident in Barbados (the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 10 | recipient of dividends on borrowed shares was not their beneficial owner because of requirement to pay dividend compensation payments | 270 |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(2) | tax under s. 212(2) imposed on the basis of payment of dividend to a non-resident rather than on the basis of who is the beneficial owner | 405 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(1) - Tax Benefit | no tax benefit under s. 215(6) from targeted reduced rate of dividend withholding if in base transaction, the Canadian dividend payer would have withheld at the higher rate | 347 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | the residence, beneficial owner, and voting requirements in the Canada-Luxembourg Treaty fully expressed the rationale for the 5% Treaty-reduced rate on dividends | 413 |

Mony v. The King, 2022 TCC 120

The taxpayer agreed to sell his shares of a Canadian-controlled private corporation (“Créaform”), having a nominal ACB, to third parties. On...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | Gervais followed to find that avoiding capital gains attribution through ACB averaging abused ss. 73(1) and 74.2(1) | 380 |

Damis Properties Inc. v. The Queen, 2021 TCC 24

Five corporate taxpayers sought to increase their after-tax return from the sale by their farm partnerships of the farm by transferring their...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | s. 160 did not apply to a sale of companies holding cash sales proceeds to a purchaser who purported to eliminate the tax liability | 785 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(1) - Tax Benefit | no tax benefit based on comparison to a commercially unrealistic alternative | 276 |

| Tax Topics - Income Tax Regulations - Regulation 1102 - Subsection 1102(1) - Paragraph 1102(1)(c) | software was not acquired with an income-producing purpose | 282 |

| Tax Topics - General Concepts - Onus | unfair to place the onus on taxpayer re facts which taxpayer could not reasonably be expected to know | 339 |

Agence du revenu du Québec v. Custeau, 2020 QCCA 1496

When a family small business corporation (the “Corporation”) was in financial difficulty, two Quebec regional development funds agreed in 1997...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | s. 248(10) “in contemplation of” test appropriately applied only on a forward-looking basis where the historical transaction was purely commercial | 729 |

Loblaw Financial Holdings Inc. v. The Queen, 2018 TCC 182, rev'd on s. 95(1) - investment business - (a) (arm's length conduct) grounds 2020 FCA 79, in turn aff'd 2021 SCC 51

The taxpayer, which was an indirect wholly-owned subsidiary of Loblaw Companies Limited (a Canadian public company), wholly-owned a Barbados...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 165 - Subsection 165(1.11) | requirement met where Crown knew the nature and quantum of the dispute | 269 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Bank | CFA qualified as a foreign bank since it was licensed under Barbados law as an international bank | 123 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Investment Business - Paragraph (a) | Barbados-licensed international bank, which used Loblaw funding to invest responsively to Loblaw considerations, conducted an offside non-arm’s length business | 429 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Investment Business - Paragraph (c) | employee equivalents was reduced by employee time described in s. 95(2)(b) | 290 |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Foreign Exchange | short-term debt securities were inventory because they were the raw material for generating swap income | 130 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4.01) - Paragraph 152(4.01)(a) - Subparagraph 152(4.01)(a)(ii) | GAAR is generally a separate matter rather than being subsumed in the allegedly-misused substantive provision | 208 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | hiring of employees 15-years previously to engage foreign bank exception to investment business definition was not part of same series as renewal of foreign bank licence | 228 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | use of Barbados sub to engage in proprietary trading for Canadian parent misused the foreign bank exemption, whose purpose was promoting international competitiveness | 336 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(l) | purpose of s. 95(2)(l) exception was to permit non-resident subsidiaries of Canadian banks and dealers to compete internationally | 190 |

Custeau v. Agence du revenu du Québec, 2018 QCCQ 5692, aff'd 2020 QCCA 1496

The two taxpayers (Charles and Philippe, who were brothers) each subscribed nominal amounts for Class A common shares of the family operating...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | no abuse where individuals used PUC thrust upon them by an arm’s length investor (through PUC averaging) to subsequently strip surplus | 298 |

Soucy v. Agence du revenu du Québec, 2018 QCCQ 4845

A direct gift of a vehicle to the taxpayer by her ex-husband would have been subject to Quebec sales tax as they were now unrelated persons. From...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 274 - Subsection 274(3) | double gift was made (avoiding QST) because the property would not have been directly gifted | 246 |

Birchcliff Energy Ltd. v. The Queen, 2017 TCC 234

A newly-launched public corporation ("Birchcliff") accessed the losses of a lossco ("Veracel"), in order to shelter the profits from producing oil...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Sham | ephemeral transactions under a Plan of Arrangement were not a sham | 215 |

| Tax Topics - Income Tax Act - Section 251.2 - Subsection 251.2(2) - Paragraph 251.2(2)(a) | proxy which accorded no discretion to a class of shareholders did not render them a group | 221 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | raising share equity through a lossco immediately before its amalgamation was abusive | 278 |

2763478 Canada Inc. v. The Queen, 2017 TCC 98, aff'd 2018 CAF 209

Prior to the sale of a corporation ("Groupe AST") to a third party, its individual shareholder rolled his shares of Groupe AST into a holding...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | value-shift transactions were abusive | 258 |

Gervais v. The Queen, 2016 TCC 180, aff'd 2018 FCA 3

The taxpayer’s wife (Mrs. Gendron) purchased 1.04M preferred shares from the taxpayer (Mr. Gervais) at a cost of $1.04M (with Mr. Gervais not...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | basis averaging scheme to transfer half of a capital gain to the taxpayer’s wife was an abuse of the attribution rules | 429 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(1) - Tax Benefit | benefit compared to straight sale and gift | 166 |

Veracity Capital Corporation v. M.N.R., 2015 DTC 5136 [at 6421], 2015 BCSC 2278, rev'd 2017 BCCA 3

The following transactions occurred under a KPMG-advised “Quebec Year-end shuffle” or “Q-Yes” plan in order to avoid 90% of the B.C....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | abuse of inter-provincial income allocation formula “designed to prevent both the over-taxation and the under-taxation of income" | 500 |

Birchcliff Energy Ltd. v. The Queen, 2015 TCC 232, nullified on procedural grounds 2017 FCA 89

A newly-launched public corporation ("Birchcliff") accessed the losses of a lossco ("Veracel"), in order to shelter the profits from producing oil...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Sham | transitory share issuance under plan of arrangement was not a sham | 177 |

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(5) - Paragraph 111(5)(a) | grant of proxy did not detract from investors acting individually in own interest | 237 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | abusive reverse takeover by Lossco through diverted private placement | 261 |

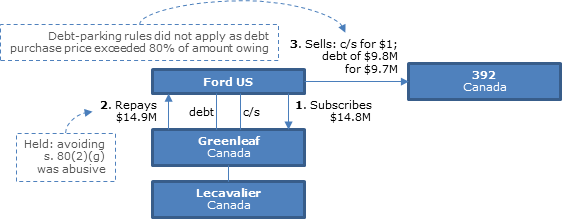

Pièces automobiles Lecavalier Inc. v. The Queen, 2014 DTC 1126, 2013 TCC 310

{kind=link}

A Canadian subsidiary ("Greenleaf") of Ford U.S. paid down to $9,750,000 (including accrued interest) a debt of $24,369,439 (plus accrued...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Evidence | Canadian tax accountant's testimony on US tax consequences accorded little weight | 152 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | avoidance of debt forgiveness rules was abusive | 277 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | debt-paydown transactions effected in contemplation of sale transaction were part of same series as the sales transactions | 248 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(2) - Paragraph 80(2)(g) | using cash share subscriptions to convert debt to share equity abused s. 80(2)(g) | 190 |

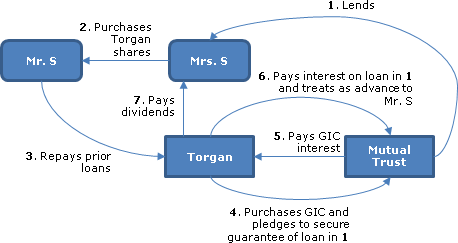

Swirsky v. The Queen, 2013 TCC 73, 2013 DTC 1078 [at at 431], aff'd 2014 FCA 36

{kind=link}

For creditor-proofing reasons, the taxpayer sold shares in a family real estate development company ("Torgan") to his wife, and used the sales...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 33 | |

| Tax Topics - Income Tax Act - Section 74.5 - Subsection 74.5(11) | 247 |

McClarty Family Trust v. The Queen, 2012 DTC 1123 [at at 3122], 2012 TCC 80

A family holding company ("MPSI") paid a stock dividend of preferred shares, having nominal paid-up capital and a redemption amount of $48,000, on...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(3) | 340 |

McMullen v. The Queen, 2007 DTC 286, 2007 TCC 16

The taxpayer and an unrelated individual ("DeBruyn") accomplished a split-up of the business of a corporation ("DEL") of which they were equal...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 198 | |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | mutual benefit and same advisors insufficient to establish non-arm's length in structured sale transaction | 257 |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | 229 | |

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) | arm's length: negotiation based on self-interest | 257 |

MIL (Investments) S A v. The Queen, 2006 DTC 3307, 2006 TCC 460, aff'd 2007 FCA 236

In March 1993 an individual ("Boulle") transferred his shares of a Canadian public junior exploration company ("DFR") to the taxpayer, which was a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | subsequent sale transaction was not assimilated to the previous series where it was a mere possibility | 300 |

| Tax Topics - Statutory Interpretation - Retroactivity/Retrospectivity | 91 | |

| Tax Topics - Treaties - Income Tax Conventions | 148 |

Desmarais v. The Queen, 2006 DTC 2376, 2006 TCC 44

The taxpayer, who held 14.28% of the common shares of a Canadian private corporation ("Consercom") transferred a 9.76% block to a wholly-owned...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | surplus stripping | 235 |

Overs v. The Queen, 2006 DTC 2192, 2006 TCC 26

The taxpayer owed approximately $2.3 million to a wholly-owned corporation. The loan, which had been used by him for personal purposes, would be...

Univar Canada Ltd. v. The Queen, 2005 DTC 1478, 2005 TCC 723

The taxpayer incorporated a Barbados subsidiary ("BarbadosCo") using borrowed money to subscribe for the shares of BarbadosCo, and BarbadosCo used...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(6) - Paragraph 95(6)(b) | no tax avoidance purpose since no base-case intention to have acquired the underlying note | 102 |

Brouillette v. The Queen, 2005 DTC 1004, 2005 TCC 203

The taxpayer facilitated a leveraged buy-out of him and his co-shareholder of a company ("Brouillette Automobiles") by incorporating a corporation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | same advisors insufficient/adverse re price | 199 |

Geransky v. The Queen, docket 98-2383(IT)G (TCC)

The taxpayer, who owned a portion of the shares of the holding ("GH") which, in turn, owned an operating company ("GBC") utilized the enhanced...

Husky Oil Ltd. v. R., 99 DTC 308, [1999] 4 CTC 2691 (TCC)

A Bermuda corporation, which was in financial difficulty and in which the taxpayer had an indirect 35% interest, transferred a drilling vessel,...

Commissioner of Taxation of the Commonwealth of Australia v. Spotless Services Ltd., 71 ALJR 81, 34 ATR 183, 141 ALR 92

Under arrangements that were characterized as a deposit of funds by the taxpayer in the Cook Islands, the taxpayer received an interest rate on...

RMM Canadian Enterprises Inc. v. R., 97 DTC 302, [1998] 1 C.T.C. 2300 (TCC)

A non-resident corporation ("EC") approached a business associate who, along with two other individuals, formed a Canadian corporation ("RMM") to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 159 - Subsection 159(3) | 167 | |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 235 | |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | purchaser of cash-rich company without any signifcant separate role did not deal at arm's length | 177 |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | application of s. 84(2) to sale of cash-rich company to accommodation party who quickly paid cash proceeds therefor | 222 |

| Tax Topics - Treaties - Income Tax Conventions | 96 | |

| Tax Topics - Treaties - Income Tax Conventions - Article 10 | 116 |

Mark Resources Inc. v. The Queen, 93 DTC 1004, [1993] 2 CTC 2259 (TCC)

Before going on to find that the former s. 245(1) did not prohibit the deduction of interest by the taxpayer, Bowman J. stated, in obiter dicta...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | loss utilization was not income-producing purpose/ gross income test | 177 |

Barclays Mercantile Industrial Finance Ltd. v. Melluish, [1990] BTC 209 (Ch. D.)

The taxpayer ("BMI") acquired a film from the producer ("WBI"), leased it to another corporation at a return that yielded 2.16% per annum on its...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Income-Producing Purpose | 136 | |

| Tax Topics - Income Tax Act - Section 83 - Subsection 83(2.1) | main purpose was to make a profit, not take deduction | 264 |

| Tax Topics - Income Tax Regulations - Regulation 1100 - Subsection 1100(17) | no "lease" where failure to provide exclusive possession | 75 |

Mallalieu v. Drummond, [1983] BTC 380, [1983] 2 All E.R. 1095 (HL)

The court rejected the view that in ascertaining the purpose of an expenditure, the state of mind of the spender is the only relevant factor.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(h) | 64 |

Newton v. Commissioner of Taxation of the Commonwealth of Australia, [1958] A.C. 450 (PC)

In interpreting the provisions of s. 260 of the Commonwealth Income Tax and Social Services Contribution Assessment Act, 1936-1951 (Australia),...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 260 - Subsection 260(1) - Securities Lending Arrangement | "arrangement" | 130 |

Administrative Policy

7 June 2024 External T.I. 2024-1006831E5 - Employment settlements and reporting requirements

The settlement agreement between an employer and a terminated employee protected the employer against any claim in respect of failure to withhold...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 237.3 - Subsection 237.3(1) - Contractual Protection - Paragraph (a) - Subparagraph (a)(i) - Clause (a)(i)(A) | an employee indemnity, in a settlement agreement with the employer, regarding the employer’s failure to withhold, likely is not contractual protection | 190 |

| Tax Topics - Income Tax Act - Section 237.3 - Subsection 237.3(1) - Avoidance Transaction | employment settlement agreement that provided for non-taxable damages without a legal or factual basis likely would be an avoidance transaction | 225 |

23 May 2013 IFA Round Table Q. 4

Given that in all three cases, a new Canadian corporation (CanHoldco) is "inserted" to establish cross-border PUC so as to enable surplus of...

2003 Ruling 2003-03924

The corporate general partner of a Canadian limited partnership operating a business in Canada borrows on an unsecured basis under a loan with a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Subparagraph 212(1)(b)(vii) | 100 |

11 October 1996 APFF Roundtable, 7M12910 - APFF ROUND TABLE

In a situation where Canco subscribes for shares of its Barbados subsidiary, and the Barbados subsidiary loans the same funds to a U.S. subsidiary...

Finance

Modernizing and Strengthening the General Anti-Avoidance Rule, Department of Finance Consultation Paper, 11 August 2022

Narrowing “bona fide purpose”

- It may be appropriate to provide that a “bona fide purpose” does not include foreign (or provincial) tax...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(1) - Transaction | 60 | |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 904 |

Articles

Avery Jones, "Nothing Either Good or Bad, but Thinking Makes it So - The Mental Element in Anti-Avoidance Legislation", 1983 British Tax Review, p. 9, 113.

Paragraph 245(3)(a)

Administrative Policy

8 October 2010 Roundtable, 2010-0373221C6 F - Paid-up capital

CRA indicated that it has concluded in some cases that using PUC averaging to shift PUC to individual shareholders engages GAAR, and “is...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | CRA has concluded in some cases that using PUC averaging to shift PUC to individual shareholders engages GAAR | 283 |

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Paid-Up Capital - Paragraph (a) | abusive use of PUC averaging to shift PUC to individuals | 39 |

Paragraph 245(3)(b)

Administrative Policy

17 May 2023 IFA Finance Update

Change to “one of the main purposes” test modernized the test

- There were suggestions in obiter dicta that, if there is a transaction that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(0.1) | 56 | |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4.1) | 260 |