Subsection 256(1) - Associated corporations

Paragraph 256(1)(a)

Cases

The Queen v. W. Ralston & Co., 96 DTC 6488, [1996] 3 CTC 346 (FCTD)

100 voting common shares of the taxpayer were held by members of the Cohen family, and the 100 voting preferred shares of the taxpayer were held...

Harvard International Resources Ltd. v. Provincial Treasurer of Alberta, 93 DTC 5254, [1993] 1 CTC 329 (Alta. Q.B.)

The taxpayer held an undivided 99.328% interest in the 100 outstanding common shares of a corporation ("Holdings") and another corporation...

The Queen v. Imperial General Properties Ltd., 85 DTC 5500, [1985] 2 CTC 299, [1985] 2 S.C.R. 288

The Wingold group held 90 common shares of the taxpayer and the Gasner group held 10 common shares and 80 voting cumulative preference shares with...

Allied Farm Equipment Ltd. v. MNR, 73 DTC 5036, [1972] CTC 619 (FCA)

Given that s. 39(4) of the pre-1972 Act applied only for the purposes of s. 39, which provided a reduced rate of tax for certain Canadian...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(1) - Paragraph 256(1)(d) | 129 |

Donald Applicators Ltd. v. MNR, 69 DTC 5122, [1969] CTC 98 (Ex Ct), briefly aff'd 71 DTC 5202, [1971] CTC 402 (SCC)

498 Class B shares in the capital of each of ten companies was held by a corporation ("Saje") and 2 Class A shares were held in each corporation...

Minister of National Revenue v. Dworkin Furs (Pembroke) Ltd. et al., 67 DTC 5035, [1967] CTC 50, [1967] S.C.R. 223

Dworkin Furs Ltd. owned 48% of the issued shares of Dworkin Furs (Pembroke) Limited in its own name and 2% in the names of Roy Saipe and Helen...

See Also

Kruger Wayagamack Inc. v. The Queen, 2015 DTC 1112 [at at 667], 2015 TCC 90, aff'd 2016 FCA 192

The taxpayer was capitalized, and its common shares then were held, on a 51-49 basis, by a business corporation ("Kruger") and a Government of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Shares | non-assignable put right ignored | 98 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(2) - Paragraph 251(2)(b) - Subparagraph 251(2)(b)(i) | de jure control requires strategic control, not merely operational control | 93 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(1.2) - Paragraph 256(1.2)(c) | effect of s. 256(1.2)(g) is as if company were run by 3rd party | 254 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | de facto control requires strategic control, not merely operational control | 216 |

Administrative Policy

1 February 1999 External T.I. 9823715 - PERSONAL SERVICES BUSINESS

It is generally the Department's view that a foreign corporation is a 'person' for purposes of the Act unless the context clearly indicates...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Personal Services Business | 52 | |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Person | 52 |

23 June 1995 External T.I. 9510475 - ASSOCIATED CORPORATIONS

Where a corporation ("Supplyco") owns 50% of the shares of another corporation ("Distributorco") which is a franchisee of Supplyco, Supplyco will...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | 137 |

1993 APFF Roundtable, Q.1

Where a wholly-owned subsidiary ("Holdco II") of Holdco I is the sole general partner of three limited partnerships which, in turn, each hold 1/3...

IT-64R3 "Corporations

Paragraph 256(1)(b)

Cases

Southside Car Market Ltd. v. The Queen, 82 DTC 6179, [1982] CTC 214 (FCTD)

"[S]ince the language of paragraph 256(1)(b) sets forth two distinct circumstances when two corporations are associated, namely, when controlled...

The Queen v. Mars Finance Inc., 80 DTC 6207, [1980] CTC 216 (FCTD)

It was stated, obiter, that where the Court has to decide whether two corporations are associated by reason of being controlled by the same...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(1) - Paragraph 256(1)(e) | 40 |

H.A. Fawcett & Son, Ltd. v. The Queen, 80 DTC 6195, [1980] CTC 293 (FCA)

A legatee of a control bloc of shares who was also the sole executor of the estate obtained control of the company immediately upon the death of...

International Iron & Metal Co. Ltd. v. Minister of National Revenue, 72 DTC 6205, [1972] CTC 242, [1974] S.C.R. 898, aff'g 69 DTC 5445, [1969] CTC 668 (Ex Ct)

A corporation ("Burland") was owned by nine children of four fathers. The taxpayer ("International Iron") would have been indirectly controlled by...

Minister of National Revenue v. Consolidated Holding Co., 72 DTC 6007, [1972] CTC 18, [1974] S.C.R. 419

Two individuals (Harold Gavin and Robert Gavin) each owned 50% of the shares of one corporation ("Consolidated") which in turn owned 43.7% of the...

Vina-Rug (Canada) Limited v. Minister of National Revenue, 68 DTC 5021, [1968] CTC 1, [1968] S.C.R. 193

Because John Stradwick, Jr., his brother W.L. Stradwick and H.D. McGilvery, who collectively owned more than 50% of the shares of Stradwick's and...

Vineland Quarries and Crushed Stone Ltd. v. MNR, 66 DTC 5092, [1966] CTC 69 (Ex Ct), briefly aff'd 67 DTC 5283 (SCC)

In finding that under the above arrangement, Vineland and S. & T. "were controlled by the same ... group of persons" (i.e., Saunder and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Ownership | 52 |

Yardley Plastics of Canada Ltd. v. MNR, 66 DTC 5183, [1966] CTC 215 (Ex Ct)

Two corporations whose voting shares were held as follows

| Shareholder | Canadian Moldings | Yardley Plastics |

| Hill | 4.6% | 28% |

| Hill... |

See Also

Ferronnex Inc. and Quincaillerie Brassard Inc. v. Minister of National Revenue, 91 DTC 559, [1991] 1 CTC 2330 (TCC)

A corporation ("Fercomat") was found to be controlled by the same group of persons as each of two other corporations ("Quincaillerie" and...

Express Cable Television Ltd. v. MNR, 82 DTC 1431, [1982] CTC 2447 (TRB)

A partnership of corporations (variously referred to as "Welsh Antenna" and "Antenna Systems") held a majority of the shares of one corporation...

King George Hotels Ltd. v. MNR, 68 DTC 635 (TAB)

The taxpayer, which was indirectly controlled by children of the Leier family, was found to be associated with the corporation ("J.P.") that was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Taxpayer | 25 |

Buckerfield's Ltd. v. MNR, 64 D.T.C 5301, [1964] CTC 504 (Ex Ct)

Two companies that were vigorous competitors (Pioneer and Federal) each owned one-half of the shares of two other companies (Buckerfield's and...

Administrative Policy

5 April 1995 External T.I. 9414745 - STOP LOSS

S.256(7)(b) will apply where the same group of unrelated individuals controls an amalgamated corporation as controlled both the predecessors.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(7) - Paragraph 256(7)(b) | 62 |

80 C.R. - Q.25

A person who is the registered and beneficial owner of the shares of one company is the "same person" for purposes of s. 256(1)(b) where he also...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Private Corporation | 35 |

IT-64R3 "Corporations

Association and Control - after 1988".

Paragraph 256(1)(c)

Cases

1056 Enterprises Ltd. v. The Queen, 89 DTC 5287, [1989] 2 CTC 1 (FCTD)

The Minister assessed the taxpayer, whose shares were owned 99% by an individual ("John"), on the basis that John's brother ("William"), who was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Ownership | 76 | |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4) - Paragraph 152(4)(a) - Subparagraph 152(4)(a)(i) | honest and diligent view that no association | 146 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(1) - Paragraph 256(1)(d) | 84 |

See Also

Disher-Winslow Products Ltd. v. MNR, 52 DTC 27 (TAB)

An individual (Edward) was the holder and beneficial owner of substantially all the shares of the taxpayer and his father (Clarence) was the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Ownership | registered shareholder of share held on behalf of another was not its owner | 174 |

Paragraph 256(1)(d)

Cases

Allied Farm Equipment Ltd. v. MNR, 73 DTC 5036, [1972] CTC 619 (FCA)

Each of three brothers owned and controlled one Canadian corporation and, among the three of them, owned and controlled a U.S. corporation. In...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(1) - Paragraph 256(1)(a) | 64 |

1056 Enterprises Ltd. v. The Queen, 89 DTC 5287, [1989] 2 CTC 1 (FCTD)

An individual ("John") was issued 99% of the shares of the appellant ("Cantex") on its incorporation, even though John's brother had provided...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Ownership | 76 | |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4) - Paragraph 152(4)(a) - Subparagraph 152(4)(a)(i) | honest and diligent view that no association | 146 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(1) - Paragraph 256(1)(c) | 76 |

Holiday Luggage Mfg. Co. Inc. v. The Queen, 86 DTC 6601, [1987] 1 CTC 23 (FCTD)

Father and son each owned substantially all the shares of a CCPC, and 30% of the shares of a U.S. corporation. Joyal, J. held that the two CCPC's...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Interpretation Act - Subsection 15(2) | 64 |

Administrative Policy

31 March 2009 External T.I. 2009-0310821E5 F - Associated Corporations - 256

A held 50% of the voting common shares of AB Inc. and his brother (B) held 37.5% of such shares directly and another 12.5% were held by B’s...

4 April 1990 T.I. (September 1990 Access Letter, ¶1439)

Where A is the sole shareholder of A Ltd., and A along with his three brothers are the four trustees, having equal powers, of a testamentary trust...

IT-64R3 "Corporations

Paragraph 256(1)(e)

Cases

The Queen v. B.B. Fast & Sons Distributors, 86 DTC 6106, [1986] 1 CTC 299 (FCA)

William Fast and his wife each owned 50% of the shares of one corporation ("Willmar"), and William Fast and his 4 siblings each owned 20% of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Interpretation Act - Subsection 45(2) | 40 |

Atomic Truck Cartage Ltd. v. The Queen, 86 DTC 6032, [1985] 2 CTC 21, [1985] DTC 5427 (FCTD)

The common shares of three corporations were held by individuals, all of whom were related to each other, as follows:

| Entreprises: | X -... |

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(4) - Related Group | 21 |

The Queen v. Mars Finance Inc., 80 DTC 6207, [1980] CTC 216 (FCTD)

Where the conditions of S.256(1)(e) are met, then it is irrelevant that de facto control of one of the corporations is exercised contrary to the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(1) - Paragraph 256(1)(b) | look to whether the mooted group in fact exercises control | 73 |

Administrative Policy

86 C.R. - Q.18 B.B. Fast.

IT-64R3 "Corporations

Subsection 256(1.1)

Administrative Policy

20 February 1996 External T.I. 9605085 - STOCK DIVIDEND SHARES THOSE OF A SPECIFIED CLASS?

Where a share has been issued as a stock dividend, the consideration for which the share was issued would be considered to be nil.

31 October 1991 T.I. (Tax Window, No. 12, p. 13, ¶1560)

The "amount of unpaid dividends" referred to in s. 256(1.1)(e) may include accumulated but unpaid dividends.

3 September 1991 T.I. (Tax Window, No. 8, p. 3, ¶1437)

A share with no entitlement to dividends generally will comply with s. 256(1.1)(c).

If the share terms provide that the shares will become voting...

Paragraph 256(1.1)(b)

Administrative Policy

15 September 2003 External T.I. 2003-0028075 F - Definition of "Specified Class" Sub 256(1.1)

Zco held Class X shares of ABCco, which satisfied all of the conditions for being a “specified class” except that they carried voting rights....

Paragraph 256(1.1)(d)

Administrative Policy

11 January 2010 External T.I. 2009-0340591E5 F - Specified class - 256(1.1) of the Act

Class A shares of the corporation were issued in three different years (Years 1, 4 and 13). The annual rate of dividend on such shares (expressed...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 51 - Subsection 51(1) | s. 51(1) exchange regarded as the new shares having been issued for consideration equalling the FMV of the old shares | 58 |

Subsection 256(1.2) - Control, etc.

Cases

9044 2807 Québec Inc. v. Canada, 2004 DTC 6636, 2004 FCA 23

Noël J.A. indicated (at p. 6639) that in order to avoid any conflict between applying the results of the de jure control and de facto...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | situs of decision-making power | 268 |

Administrative Policy

89 C.R. - Q.14

Where a minor child owns 10% of the common shares of Holdco which owns 100% of the common shares of Opco, s. 256(1.2)(e) will not be applied more...

88 C.R. - Q.39

RC will identify any group of persons, related or unrelated, without considering whether any group acts in concert.

Paragraph 256(1.2)(a)

Administrative Policy

IT-64R3 "Corporations

Paragraph 256(1.2)(b)

Administrative Policy

18 October 89 Meeting with Quebec Accountants, Q.3 (April 90 Access Letter, ¶1166)

Where A owns 95% of the shares of Corporation A and the other 5% are owned by B, and B owns all the shares of Corporation B, and to fund a...

IT-64R3 "Corporations

Subparagraph 256(1.2)(b)(ii)

Administrative Policy

15 July 1999 External T.I. 9819025 F - SOCIETES ASSOCIEES

Two individuals (X and Y), each held 51% and 49% of the shares of ABC Ltd. through wholly owned corporations (X Ltd. and Y Ltd., respectively). X...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(1.2) - Paragraph 256(1.2)(d) | a corporation deemed by s. 256(1.2)(d) to be owned 51% and 49% by 2 individuals was associated with a corporation each owned directly by them as to 42% each | 195 |

Paragraph 256(1.2)(c)

See Also

Kruger Wayagamack Inc. v. The Queen, 2015 DTC 1112 [at at 667], 2015 TCC 90, aff'd 2016 FCA 192

51% and 49% of the taxpayer's shares (being common shares) were held by a business corporation ("Kruger") and a Government of Quebec corporation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Shares | non-assignable put right ignored | 98 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(2) - Paragraph 251(2)(b) - Subparagraph 251(2)(b)(i) | de jure control requires strategic control, not merely operational control | 93 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(1) - Paragraph 256(1)(a) | de jure or de facto control requires strategic control, not merely operational control | 340 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | de facto control requires strategic control, not merely operational control | 216 |

Administrative Policy

30 May 2007 External T.I. 2006-0218101E5 F - Interaction entre 125.4(1) et 256(1.2)c)

CRA noted that the expanded definition of control in s. 256(1.2)(c) applies only for the purposes of the enumerated provision in its preamble and,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 1106 - Subsection 1106(2) | s. 256(1.2)(c) does not inform the definition of prescribed taxable Canadian corporation | 44 |

8 January 2004 External T.I. 2003-0040575 F - Associated Corporations

Although Mr. X held all of the issued and outstanding shares of Opco, an arm’s length lender (“Lendco”) held a debenture which was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(6) - Paragraph 256(6)(a) | cessation of lender’s right to shares on occurrence of reasonably-expected event must be expressly stated in loan terms | 204 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(1.4) - Paragraph 256(1.4)(a) | lender’s right to acquire 99% of shares in event of insolvency engaged s. 256(1.4)(a) | 73 |

29 June 1995 External T.I. 9510645 - COTRUSTEES OF DIFFERENT TRUSTS SAME PERSONS

"Where the co-trustees of two trusts are the same persons and one of the trusts owns shares representing more than 50% of the fair market value...

Paragraph 256(1.2)(d)

Administrative Policy

15 July 1999 External T.I. 9819025 F - SOCIETES ASSOCIEES

Two individuals (X and Y), each held 51% and 49% of the shares of ABC Ltd. through wholly owned corporations (X Ltd. and Y Ltd., respectively). X...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(1.2) - Paragraph 256(1.2)(b) - Subparagraph 256(1.2)(b)(ii) | two individuals deemed to own 51% and 49% of a CCPC’s shares were a controlling group under s. 256(1.2)(c) notwithstanding control by one individual alone | 116 |

IT-64R3 "Corporations

Paragraph 256(1.2)(e)

Administrative Policy

8 February 1999 External T.I. 9820355 F - SOCIÉTÉS ASSOCIÉES

Aco was wholly owned by a limited partnership (LP), whose 1% general partner was Bco, a corporation controlled by an unrelated group of persons,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Private Corporation | de jure control of corporation through the closely-held general partner of the LP holding its shares rendered it a private corporation | 159 |

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Canadian-Controlled Private Corporation | GP of LP generally has de facto control of a corporation held by the LP | 236 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(5) - Paragraph 251(5)(b) - Subparagraph 251(5)(b)(i) | employee stock options did not give employees control since none of them individually had options on over 50% of the shares | 122 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(1.4) - Paragraph 256(1.4)(a) | 256(1.4)(a) rendered employees a deemed control group | 215 |

Paragraph 256(1.2)(f)

Cases

Canada v. Propep Inc., 2010 DTC 5088 [at at 6882], 2009 FCA 274

The taxpayer was owned by another corporation (9059) which, in turn, was owned by a Quebec trust whose first-ranking beneficiary was 9059, and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 108 - Subsection 108(1) - Income Interest | 28 | |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(25) | potential beneficiary was a beneficiary | 284 |

Administrative Policy

IT-64R3 "Corporations

Articles

Jeffrey T. Love, Kenneth R. Hauser, "How Various Aggregation Rules Apply to Trusts", 2018 Conference Report (Canadian Tax Foundation), 28: 1-79

Uncertainties re scope of ss. 256(1.2)(f)(ii), (iii) and (iv) (pp. 28:62-63)

Subparagraph 256(1.2)(f)(iii) applies when a beneficiary's share of...

Subparagraph 256(1.2)(f)(ii)

See Also

Moules Industriels (C.H.F.G.) Inc. v. The Queen, 2018 TCC 85

Whether corporations in which two discretionary trusts whose beneficiaries included the children (and their spouses) of Mr. Houle were associated...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(1) | Quebec trusts are considered to be owners of their property for ITA purposes | 224 |

Administrative Policy

14 September 2017 External T.I. 2017-0685121E5 F - Associated corporations

Three children each of whom wholly-owns a Childco are also, along with their parent, the discretionary beneficiaries of a family trust owning all...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(2) - Paragraph 256(2)(b) - Subparagraph 256(2)(b)(ii) | election under s. 256(2)(b)(ii) busts s. 256(2)(a) transitivity but not association with 3rd corporation | 310 |

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(5.1) | making s. 256(2)(b)(ii) election, by eliminating s. 256(2)(a) transitivity, reduces the reduction for taxable capital employed in Canada | 262 |

8 December 2015 External T.I. 2015-0608781E5 F - Associated corporations - discretionary trust

1st Situation: X, who holds all the shares of Newco, and is a beneficiary of a discretionary trust holding all the shares of Opco (so that X is...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(1.3) | no double-counting of shares in applying s. 256(1.3) to shares deemed to be owned by minor trust beneficiaries | 139 |

16 August 2006 External T.I. 2006-0176801E5 F - Subparagraph 256(1.2)(f)(ii)

Mr. X is the beneficiary of a discretionary inter vivos trust. The trust deed provides that when Mr. X dies, his adult son, Mr. Y, will become...

6 January 2004 External T.I. 2003-0052261E5 - Subparagraph 256(1.2)(f)(ii)

A discretionary inter vivos personal resident trust (the "Trust") owns all the shares of Opco. Mr. A (a resident), who is not a trustee but is a...

16 February 2000 External T.I. 1999-0008435 F - Société associées

Two unrelated individuals, Mr. A and Mr. B, held 66% and 34%, respectively, of the shares of Opco2. Mr. A and Mr. B each held 15% of the shares,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(1.3) | application of s. 256(1.3) was insufficient to create a control group | 314 |

Subsection 256(1.3) - Parent deemed to own shares

Administrative Policy

8 December 2015 External T.I. 2015-0608781E5 F - Associated corporations - discretionary trust

Father and Mother each hold 80 shares of Newco and Opco, respectively, and two discretionary trusts, with their three minor children as...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(1.2) - Paragraph 256(1.2)(f) - Subparagraph 256(1.2)(f)(ii) | beneficiary includes beneficially entitled/combined application of 256(1.2)(f)(ii) and 256(1.3), but shares attributed only once] | 595 |

8 December 2015 External T.I. 2015-0610921E5 F - Associated corporations - child under 18

On January 1 of a particular year, “Child”, who is 17 years, becomes the shareholder of Opco (a CCPC with a calendar year which is not managed...

13 October 2000 External T.I. 2000-0038915 - Double-Counting - Associated Corporations

With respect to a situation where father held, as the sole trustee of a discretionary trust for minor children, 24% of the shares of a...

16 February 2000 External T.I. 1999-0008435 F - Société associées

Two unrelated individuals, Mr. A and Mr. B, held 66% and 34%, respectively, of the shares of Opco2. Whether Opco1 was associated with Opco2 turned...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(1.2) - Paragraph 256(1.2)(f) - Subparagraph 256(1.2)(f)(ii) | deemed holding of shares of corporation by each beneficiary of a family trust | 238 |

4 March 1994 External T.I. 9328745 F - Associated Corporations

Where 16% of the shares of a corporation are held by a discretionary family trust and three beneficiaries of the trust (being siblings) are under...

21 August 1992 T.I. 921988 (April 1993 Access Letter, p. 155, ¶C248-133)

Where Mr. A. owns all the shares of X Ltd. and Mrs. A, who owned all the shares of Y Ltd., freezes her interest in Y Ltd. in favour of a...

Subsection 256(1.4) - Options and rights

Administrative Policy

24 July 1998 External T.I. 9807875 - ASSOCIATED CORPORATIONS

Where a corporation and its two 50% shareholders have agreed that the shares held by the shareholder shall be purchased by the corporation in the...

18 June 1998 External T.I. 9805705 - ASSOCIATED CORPORATIONS

In indicating that s. 256(1.4)(b) could apply where pursuant to a unanimous shareholders agreement a corporation would automatically acquire the...

5 February 1993 T.I. (Tax Window, No. 28, p. 3, ¶2411)

S.256(1.4)(a) applies in a situation where the articles of incorporation or a shareholders' agreement for a corporation having three equal common...

91 C.R. - Q.11

Where parties to a shareholders' agreement have made a bona fide attempt to define "permanent disability", their definition will be given weight...

20 April 1990 T.I. (September 1990 Access Letter, ¶1440)

Permanent disability refers to impairments that are expected to last for continuous periods that will exceed the period provided in s....

IT-64R3 "Corporations

Paragraph 256(1.4)(a)

Administrative Policy

7 October 2016 APFF Roundtable Q. 7, 2016-0652971C6 F - Paragraph 251(5)(b) and subsection 256(1.4)

Franchisor and Manager each hold 50% of the shares (being common shares) of Franchisee. The shareholders’ agreement for Franchisee provides, in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(5) - Paragraph 251(5)(b) - Subparagraph 251(5)(b)(ii) | may include right arising after triggering of event over which no control | 274 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(5) - Paragraph 251(5)(b) - Subparagraph 251(5)(b)(i) | right to find 3rd party purchaser | 72 |

28 September 2006 External T.I. 2006-0197841E5 F - Shareholders agreement & 256(1.4)

Four unrelated individuals (A, B, C and D) each hold 25% of the shares (being common shares) of Opco through their respective wholly-owned holding...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(5) - Paragraph 251(5)(b) - Subparagraph 251(5)(b)(i) | technically a contingent right to acquire control where each 25% shareholder has an obligation to acquire shares of another shareholder offering its shares | 127 |

20 April 2005 External T.I. 2005-0119901E5 F - Associated Corporations - Shareholders' Agreement

Two individuals (X and Y) each held all of the shares of Gesco and Holdco, respectively, and each of Gesco and Holdco held ½ of all the shares...

10 November 2004 External T.I. 2004-0096991E5 F - Shareholders' agreement

Mr. X holds all the shares of Aco and each of Mr. X and Mr. Y holds ½ of the shares (being common shares) of Zco. A shareholders' agreement...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(5) - Paragraph 251(5)(b) - Subparagraph 251(5)(b)(i) | s. 256(1.4)(a) applied to a right to acquire the other’s shares even though it was reciprocal | 49 |

8 January 2004 External T.I. 2003-0040575 F - Associated Corporations

Although Mr. X held all of the issued and outstanding shares of Opco, an arm’s length lender (“Lendco”) held a debenture which was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(6) - Paragraph 256(6)(a) | cessation of lender’s right to shares on occurrence of reasonably-expected event must be expressly stated in loan terms | 204 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(1.2) - Paragraph 256(1.2)(c) | rule in s. 256(1.2)(c) references de jure control, not de facto control | 73 |

16 June 2003 External T.I. 2003-0020895 F - Association/Convertible Property

Parent Inc., Invest1 Inc. and Invest2 Inc. hold, respectively, 35, 15 and 15 Class A common shares (being all the issued and outstanding shares)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(5) - Paragraph 251(5)(b) | where multiple debenture holders hold convertible debentures, s. 256(1.4)(a) is to be applied as if all the debentures were exercised simultaneously | 86 |

29 October 2001 External T.I. 2001-0092035 F - association related persons

When asked to explain the statement in 9820337 F that the position on the application of s. 251(5)(b) in 9421285 E is not relevant in applying s....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(5) - Paragraph 251(5)(b) - Subparagraph 251(5)(b)(i) | s. 251(5)(b)(i) applies differently than s. 256(1.4)(a) because it does not deem the subject shares to be outstanding | 100 |

9 March 2000 Internal T.I. 2000-0008257 F - Mandat d'inaptitude

In determining whether two corporations are associated, a mandatary under a power of attorney would be deemed under s. 256(1.4) to be the owner of...

8 February 1999 External T.I. 9820355 F - SOCIÉTÉS ASSOCIÉES

Aco was wholly owned by a limited partnership (LP), whose 1% general partner was Bco, a corporation controlled by an unrelated group of persons,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Private Corporation | de jure control of corporation through the closely-held general partner of the LP holding its shares rendered it a private corporation | 159 |

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Canadian-Controlled Private Corporation | GP of LP generally has de facto control of a corporation held by the LP | 236 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(1.2) - Paragraph 256(1.2)(e) | application of s. 256(1.2)(e) to 99% limited partner caused the corporation held by the LP to be associated with any other corp controlled by that limited partner | 155 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(5) - Paragraph 251(5)(b) - Subparagraph 251(5)(b)(i) | employee stock options did not give employees control since none of them individually had options on over 50% of the shares | 122 |

11 January 1999 Internal T.I. 9820337 F - SOCIÉTÉS ASSOCIÉES

The respective Holdcos of two resident individuals each held 50 of the 100 common shares of Opco. Pursuant to a shareholders' agreement, each had...

Paragraph 256(1.4)(b)

Administrative Policy

16 March 2011 External T.I. 2010-0380571E5 F - Application de 251(5)b)(ii) et 256(1.4)b)

The wording of ss. 251(5)(b)(ii) and 256(1.4)(b) is sufficiently broad to cover a situation where a person does not have control over the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(5) - Paragraph 251(5)(b) - Subparagraph 251(5)(b)(ii) | s. 251(5)(b)(ii) does not apply where corporation is required to redeem shares of declared fraudster | 148 |

Subsection 256(2) - Corporations associated through a third corporation

Administrative Policy

17 June 2011 Internal T.I. 2011-0394471I7 F - Associated Corporations - 256

In rejecting a taxpayer view that s. 256(2) permits the multiplication of the small business deduction (“SBD”) in the same corporate group in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(2.1) | list of 5 “useful” factors in determining s. 256(2.1) application | 167 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | Transport M.L. Couture cited as an example | 22 |

26 February 2007 External T.I. 2005-0163391E5 F - Choix en vertu du paragraphe 256(2) de la LIR

A real estate rental company (ABco), which otherwise would be associated with its two 50% shareholders (Aco and Bco, which are wholly-owned by two...

17 January 2007 Internal T.I. 2006-0216331I7 F - Association

After describing an intricate and redacted factual situation regarding the eligibility to the small business deduction (SBD) of numerous...

28 May 2004 External T.I. 2004-0065291E5 F - Corp. associated through a third corp.: 256(2)

X wholly-owned Aco, which held 70% of the shares of Cco, which wholly-owned Dco. X also held 25% of the shares of Bco, with the other 75% held by...

28 April 2004 External T.I. 2004-0066201E5 F - Associated Corporations - Control by same person

A held all the shares of Aco (with calendar years) and 90% of the voting shares of Bco (with June 30 year ends), and his common law partner (B)...

30 October 2003 External T.I. 2003-0037075 F - Associated Corporation and 129(6)

Four brothers (A, B, C and D) each held 25% of the shares of Opco 1 and corporations wholly-owned by the respective brothers (Aco, Bco, Cco and...

15 October 2003 External T.I. 2003-0030905 F - Associated Corporations and 129(6)

Three CCPCs, Aco and Opco, and Bco and Opco, are associated. Aco and Bco, which are not otherwise associated, are deemed by s. 256(2) to be...

1993 External T.I. 9335545 F - Sub — 256(2) and T2144

Re RC's requirements for acceptance of a late-filed Form T2144.

16 June 1993 T.I. (Tax Window, No. 32, p. 12, ¶2607)

An election by a corporation under s. 256(2) will not affect the status of the other two corporations in question for purposes of ss.129(6) and...

6 September 1991 T.I. (Tax Window, No. 9, p. 6, ¶1447)

Example of the application of s. 256(2).

30 March 1990 Memorandum (August 1990 Access Letter, ¶1395)

The phrase "either of the other two corporations" refers to both corporations. In the situation where corporations B, C, D and E are each...

2 November 89 T.I. (April 90 Access Letter, ¶1181)

An election made by a corporation under s. 256(2) not to be associated is valid only for the purposes of section 125 and not for purposes of the...

88 C.R. - F.Q.40

The election by the third corporation should be filed with its return of income for the relevant taxation year.

Paragraph 256(2)(a)

See Also

Agence du revenu du Québec v. 9181-4517 Québec Inc., 2021 QCCA 11

The taxpayer corporation (“9181-4517”) was associated under s. 21.20(b) of the Taxation Act (similar to ITA s. 256(1)(b)) with a second...

Paragraph 256(2)(b)

Subparagraph 256(2)(b)(ii)

Administrative Policy

14 September 2017 External T.I. 2017-0685121E5 F - Associated corporations

Each of Aco, Bco and Cco is wholly-owned by siblings (A, B and C), and their parent (D) holds all the voting non-participating shares of Dco. A,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(1.2) - Paragraph 256(1.2)(f) - Subparagraph 256(1.2)(f)(ii) | Childco associated with Parent-controlled corp whose non-voting equity is held by family trust | 85 |

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(5.1) | making s. 256(2)(b)(ii) election, by eliminating s. 256(2)(a) transitivity, reduces the reduction for taxable capital employed in Canada | 262 |

24 November 2011 External T.I. 2011-0424631E5 F - Subsection 256(2)

CRA confirmed 2003-0051701I7, that a s. 256(2) election causes Aco and Bco not be associated with Cco for s. 125(5.1) purposes, but does not apply...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 181.1 - Subsection 181.1(4) | s. 256(2) election causes Aco and Bco not be associated with Cco for s. 125(5.1), but not ss. 181.1(2) and (4), purposes | 116 |

Subsection 256(2.1) - Anti-avoidance

Cases

Nicole L. Tiessen Interior Design LTD. v. Canada, 2022 FCA 53

An incorporated firm of architects and interior designers restructured, so that their practice was now carried on by a partnership between...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Other Legislation/Constitution - Federal - Federal Courts Act - Section 27 - Subsection 27(1.3) | new issue could not now be raised because it might have generated additional evidence at the TCC | 345 |

Les installations de l'Est Inc. v. The Queen, 91 DTC 5185, [1990] 2 CTC 503, [1990] 1 CTC 324 (FCTD)

It was found that a second corporation was incorporated in order to deal with difficulties the first corporation had been having with its...

Maritime Forwarding Ltd v. The Queen, 88 DTC 6114, [1988] 1 CTC 186 (FCTD)

The taxpayer was unsuccessful in his assertions that the main reasons for the separate existence of a company (controlled by a family trust) whose...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Purpose/Intention | 49 |

Kencar Enterprises Ltd. v. The Queen, 87 DTC 5450, [1987] 2 CTC 246 (FCTD)

The taxpayer was formed for income tax estate planning reasons, and the taxpayer's appeal accordingly failed.

Alpha Forming Corp. Ltd. v. The Queen, 83 DTC 5021, [1982] CTC 425 (FCTD)

A direction was made under old S.247(2) respecting 2 corporations the first one of which ("Alpha") was owned primarily by 2 individuals, and the...

The Queen v. Covertite Ltd., [1981] CTC 464, 81 DTC 5353 (FCTD)

The onus under the section was not met by an unsubstantiated explanation by the wife of the chief shareholder of the first company that the second...

Honeywood Ltd. v. The Queen, 81 DTC 5066, [1981] CTC 38 (FCTD)

Since no "positive evidence" was adduced by the Crown to prove that one of the main reasons for the companies' separate existence was the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Evidence | 90 |

Lenco Fibre Canada Corp. v. The Queen, 79 DTC 5292, [1979] CTC 374 (FCTD)

The wife of the owner of two companies incorporated the plaintiff company, which hired her as its sole employee, in order for the plaintiff...

Decker Contracting Ltd. v. The Queen, 79 DTC 5001, [1978] CTC 838 (FCA)

It was argued that the separate existence of a company ("Garyray") owned by the wives of the individual owners of the appellant, did not result in...

Debruth Investments Ltd. v. M.N.R., 75 DTC 5012, [1975] CTC 55 (FCA)

A successful businessman who carried on a real estate business through a company ("Don River") owned by him and his wife set up four separate...

First Pioneer Petroleums Ltd. v. MNR, 74 DTC 6109, [1974] CTC 108 (FCTD)

"[T]he question of fact to be determined is not whether the tax advantage is the main reason but rather whether it is a main reason for the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Income-Producing Purpose | income taxes not incurred to generate profit | 50 |

See Also

Nicole L. Tiessen Interior Design Ltd. v. The Queen, 2021 TCC 29, aff'd 2022 FCA 53

An incorporated firm of architects (the “Corporation”), which received administrative services from a partnership owned principally by trusts...

Prairielane Holdings Ltd. v. The Queen, 2019 TCC 157

The two taxpayers (“PLH” and “SCL”), which were each controlled by two unrelated individuals, would have been associated with each other...

Jencal Holdings Ltd. v. The Queen, 2019 TCC 16

Until 2007, a partnership carrying on a global tire business through subsidiaries, was held indirectly by a family holding company (“KT...

Maintenance Euréka Ltée v. The Queen, 2011 DTC 1319 [at at 1812], 2011 TCC 307

Hogen J. found that the taxpayers' reassessment under s. 256(2.1) was justified, given that (para. 15):

The evidence shows that the two corporate...

Taber Solids Control (1998) Ltd. v. The Queen, 2009 DTC 1899, 2009 TCC 527

Before going on to find that the taxpayer and a corporation owned by the wife of the majority shareholder of the taxpayer, were associated because...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | 98 |

LJP Sales Agency Inc. v. The Queen, 2004 DTC 2007, 2003 TCC 851

The reason for the separate existence of two corporations, one of them owned by the husband, and the other one substantially owned by his wife,...

Saratoga Building Corp. v. MNR, 93 DTC 564, [1993] 2 CTC 2074 (TCC)

A finding was made that none of the main reasons for the separate incorporation of the taxpayers involved tax savings given that they had been...

Administrative Policy

2013 Ruling 2013-0498961R3 - Partner creating a professional corporation

CRA accepted a representation that the professional corporations (ProCorps) whose respective employees and controlling shareholder was a partner...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Specified partnership income | professional partner services corp | 321 |

17 June 2011 Internal T.I. 2011-0394471I7 F - Associated Corporations - 256

In the course of a general discussion, the Directorate described the following factors (taken from Maureen Donnelly and Allister Young, "Deemed...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(2) | s. 256(2) does not multiply the SBD but protects it where particular corporations otherwise are eligible | 182 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | Transport M.L. Couture cited as an example | 22 |

6 November 2008 Internal T.I. 2008-0292561I7 F - DAPE multiple

Four brothers and an unrelated individual, who were actively involved in a succession of construction projects, through their respective...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Personal Services Business | PSBs where 4 brothers and an executive provided all the management services to a jointly owned construction company through their respective managementcos | 164 |

84 C.R. - Q.87

Listing of RC criteria re the "most effective manner" phrase appearing in old s. 247(2)(a).

Subsection 256(3) - Saving provision

Administrative Policy

8 June 2000 Internal T.I. 1999-0012817 F - Sociétés associées

Before going on to find that s. 256(6) did not apply, the Directorate indicated that s. 256(3) did not apply, stating:

Subsections 256(3) and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(6) | s. 256(6)(b) was not satisfied because control also held to protect investment in building and because shares were to be purchased for cancellation rather than redeemed | 135 |

IT-64R3 "Corporations

Paragraph 256(3)(a)

Administrative Policy

28 June 2004 External T.I. 2004-0059311E5 F - Associated Corporations

In response to questions regarding a debenture that was convertible into shares of the issuer (a Canadian-controlled private corporation) by the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(6) | where s. 256(6) applies, it excludes both de jure and de facto control by the creditor | 166 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | the defined phrase includes de jure control | 56 |

Subsection 256(5.1) - Control in fact

Cases

Deans Knight Income Corp. v. Canada, 2023 SCC 16

In discussing the broader scope of the concept of de facto control under s. 256(5.1) as contrasted to that of de jure control under s. 111(5),...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | a transaction where a Lossco became subject to control rights similar to de jure control abused the rationale of s. 111(5) | 526 |

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(5) | rationale of s. 111(5) addresses where there is a change in the identity of those behind a corporation | 416 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | series includes transactions undertaken before or after the series in relation to the series | 75 |

Bresse Syndics Inc. v. Canada, 2021 FCA 115

A public company (CO2 Public) operating a high-tech business in the field of carbon dioxide capture and management carried on its SR&ED through a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Canadian-Controlled Private Corporation - Paragraph (a) | no need to address whether terms of trust deed gave Pubco de jure control over the mooted CCPC as those terms gave Pubco de facto control | 312 |

North American et al. v. The Deputy Minister of Finance, 2019 MBQB 29

At issue was whether a corporation (“533”) whose shares were considered by the applicants to be beneficially owned by Mrs. Carson was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.11) | s. 256(5.11) permits departure from McGillivray | 252 |

Aeronautic Development Corporation v. Canada, 2018 FCA 67

The taxpayer (“ADC”) was denied refundable SR&ED investment tax credits on the basis that a U.S. resident (Mr. Silva) and a U.S. corporation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | sole customer under single contract dominated the company | 317 |

McGillivray Restaurant Ltd. v. Canada, 2016 FCA 99

The taxpayer was controlled de jure by the holder of 760 of its 1000 voting shares (Mrs. Howard). Her husband, as officer and director, made all...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Certainty | subjective interpretive tests to be avoided | 77 |

Plomberie J.C. Langlois inc. v. Canada, 2007 DTC 5662, 2006 FCA 113

In rejecting a submission on behalf of the taxpayer that the Tax Court judge had ignored the terms of a unanimous shareholder agreement in finding...

9044 2807 Québec Inc. v. Canada, 2004 DTC 6636, 2004 FCA 23

The trial judge had correctly found that a corporation ("ML1") whose shares were owned by an individual ("father"), and a corporation ("ML2") 90%...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(1.2) | 89 |

Lanester Sales Ltd. v. The Queen, 2003 DTC 997 (TCC), aff'd 2004 DTC 6461, 2004 FCA 217

Arrangements pursuant to a shareholders agreement under which the franchisor of the taxpayer (which owned 49.9% of the taxpayer's shares) was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | franchise arrangement was arm's length | 82 |

Silicon Graphics Ltd. v. Canada, 2002 DTC 7113, 2002 FCA 260

The taxpayer was found to be a Canadian-controlled private corporation, as neither de jure nor de facto control was held by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Canadian-Controlled Private Corporation | U.S. public shareholders not a group; no de facto control by lender/licensor | 345 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(6) | 65 | |

| Tax Topics - Statutory Interpretation - Hansard, explanatory notes, etc. | 23 | |

| Tax Topics - Statutory Interpretation - Interpretation Act - Subsection 45(2) | 56 | |

| Tax Topics - Statutory Interpretation - Interpretation Bulletins, etc. | 64 |

See Also

BHP Billiton Limited v Commissioner of Taxation, [2020] HCA 5

The appellant, BHP Billiton Limited ("Ltd"), an Australian resident taxpayer, was part of a dual-listed company arrangement (the “DLC...

CO2 Solution Technologies Inc. v. The Queen, 2019 TCC 286, aff'd sub nom. Bresse Syndics Inc. acting for the bankruptcy of CO2 Solution Technologies Inc. v. The Queen, 2021 FCA 115

A high-tech public company (CO2 Public) carried on its SR&ED through a private company (CO2 Technologies) that was held by a discretionary trust...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Canadian-Controlled Private Corporation - Paragraph (a) | a declaration of trust’s requiring the trustees to be the Pubco directors gave Pubco de jure and de facto control of a trust investment | 677 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(5) - Paragraph 251(5)(b) - Subparagraph 251(5)(b)(i) | a declaration of trust’s requiring the trustees to be the Pubco directors likely represented a s. 251(5)(b)(i) right of Pubco over trust investment | 291 |

Aeronautic Development Corporation v. The Queen, 2017 TCC 39

The taxpayer was denied refundable SR&ED investment tax credits on the basis that a U.S. resident (Mr. Silva) and a U.S. corporation controlled by...

Kruger Wayagamack Inc. v. The Queen, 2015 DTC 1112 [at at 667], 2015 TCC 90, aff'd 2016 FCA 192

Kruger Inc. was the 51% shareholder of the taxpayer and was entitled under the unanimous shareholders agreement between it and the other...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Shares | non-assignable put right ignored | 98 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(2) - Paragraph 251(2)(b) - Subparagraph 251(2)(b)(i) | de jure control requires strategic control, not merely operational control | 93 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(1) - Paragraph 256(1)(a) | de jure or de facto control requires strategic control, not merely operational control | 340 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(1.2) - Paragraph 256(1.2)(c) | effect of s. 256(1.2)(g) is as if company were run by 3rd party | 254 |

Solutions MindReady R&D Inc. v. The Queen, 2015 TCC 17

All of the shares of the taxpayer were held by a trust whose two trustees were also directors of a public company and the sole directors of the...

McGillivray Restaurant Ltd. v. The Queen, 2015 DTC 1030 [at at 134], 2014 TCC 357, aff'd supra

The taxpayer's business was a franchised restaurant. Boyle J found that it was required to share the small business deduction with corporations...

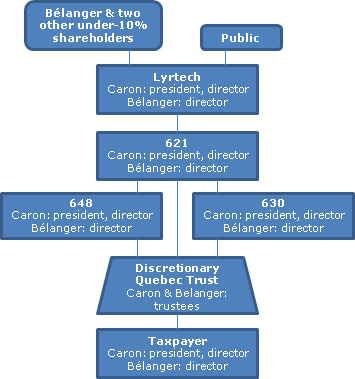

Lyrtech RD Inc. v. The Queen, 2013 DTC 1147 [at at 820], 2013 TCC 12, aff'd 2014 FCA 267

{kind=link}

In order to generate refundable investment tax credits for research and development expenditures, a Canadian public corporation ("Lyrtech")...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(5) - Paragraph 251(5)(b) | s. 248(25) does not apply for s. 251(5)(b) purposes | 337 |

Taber Solids Control (1998) Ltd. v. The Queen, 2009 DTC 1899, 2009 TCC 527

The taxpayer ("Taber 1998") and its majority shareholder ("Ken") were found to have de facto control over a corporation that was owned by Ken's...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(2.1) | 89 |

Brownco Inc. v. The Queen, 2008 DTC 2591, 2008 TCC 58

The taxpayer was subject to the de facto control of the holder of ½ of its shares ("Bost") given that under the unanimous shareholder agreement...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | "free" terms indicative of non-arm's length | 45 |

Corpor-Air Inc. v. The Queen, 2007 DTC 841, 2006 TCC 75

The taxpayer was found to be subject to the de facto control of the husband of the individual who was its sole director, shareholder and officer...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Evidence | 57 |

Avotus Corporation v. The Queen, 2007 DTC 215, 2006 TCC 505

A non-resident shareholder of the taxpayer, who owned one-half of the taxpayer's shares and, by virtue of being chairman, was entitled pursuant to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Evidence | 70 | |

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Canadian-Controlled Private Corporation | tie-breaking vote of 50% non-resident shareholder | 92 |

| Tax Topics - Income Tax Act - Section 9 - Agency - Agency | 97 | |

| Tax Topics - General Concepts - Effective Date | retroactive agency agreement | 124 |

Plomberie J.C. Langlois Inc. c. La Reine, 2006 DTC 2997, 2004 TCC 734, aff'd supra.

The taxpayer and its 50% corporate shareholder were found to be subject to the de facto control of the same person (an individual who was the sole...

L.d.g. 2000 Inc. v. The Queen, 2003 DTC 827 (TCC)

50% of the shares of the taxpayer were acquired by another corporation ("Gestion") following which the two individual shareholders of the taxpayer...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Improvements v. Repairs or Running Expense | 61 |

Transport M.l. Couture v. The Queen, 2003 DTC 817 (TCC), aff'd sub. nom. 9044-2807 supra.

The taxpayer was found to be controlled within the meaning of s. 256(5.1) by another corporation ("Transport Couture") given the economic...

Miller, The Estate of Carl Edward v. The Queen, 2002 DTC 1228 (TCC)

An order of the District Court of Ontario that there be no administration or distribution of an estate pending a decision of the widow of the...

Mimetix Pharmaceuticals Inc. v. The Queen, 2001 DTC 1026 (TCC), briefly aff'd 2003 DTC, 2003 FCA 106

Fifty percent of the voting shares of the taxpayer together with most of its capital (in the form of preferred shares and an interest-free loan)...

Multiview Inc. v. R., 97 DTC 1489, [1997] 3 C.T.C. 2962 (TCC)

Brulé TCJ. applied the criteria in Interpretation Bulletin IT-64R3, para. 17, 19 to find that the taxpayer was not subject to the de facto...

Rolka v. MNR, 62 DTC 1394, [1962] CTC 637 (Ex Ct)

An individual was found to indirectly control a corporation ("Nelmar") whose "shareholders were merely his nominees, prepared at all times to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Solicitor-Client Privilege | 26 | |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | 173 |

Administrative Policy

15 December 2025 External T.I. 2025-1062551E5 F - Relevant Group Entity

CRA indicated that it was likely that the mere ownership, by a corporation whose control was retained by father, of a building leased to the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2.31) - Paragraph 84.1(2.31)(c) - Subparagraph 84.1(2.31)(c)(iii) | the s. 129(6) income recharacterization rule is not relevant to whether a corporation carries on an active business for purposes of being a relevant group entity | 248 |

18 February 2025 External T.I. 2024-1038891E5 - De facto control

A corporation (the purchaser) controlled by an adult child acquires all the shares of another corporation (the subject corporation) from the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2.31) - Paragraph 84.1(2.31)(c) | parents did not have de facto control of child’s purchaser by virtue only of a large term note taken back by them | 233 |

5 January 2016 External T.I. 2015-0568911E5 F - MRC - Revenu d’entreprise

In the context of noting that a corporation whose capital was held by a municipality nonetheless would not qualify for s. 149(1)(d.5) exemption if...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 149 - Subsection 149(1) - Paragraph 149(1)(d.5) | Quebec regional county municipality is municipality | 150 |

11 October 2013 APFF Roundtable, 2013-0495811C6 F - De Facto Control

S. 188 of the Quebec Business Corporations Act provided that "Unless otherwise provided in the by-laws, in the case of a tie, the chair of the...

11 October 2013 APFF Roundtable, 2013-0493651C6 F - Affiliated persons and de facto control

All the voting common shares of Opco (carrying on an active business) are held by a discretionary inter vivos trust which was settled by the uncle...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(3.61) | exception unavailable for inter vivos trust | 177 |

17 June 2011 Internal T.I. 2011-0394471I7 F - Associated Corporations - 256

Transport M.L. Couture was discussed as an example of the application of s. 256(5.1).

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(2) | s. 256(2) does not multiply the SBD but protects it where particular corporations otherwise are eligible | 182 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(2.1) | list of 5 “useful” factors in determining s. 256(2.1) application | 167 |

14 June 2010 Internal T.I. 2010-0366611I7 F - Determination of CCPC Status

At issue was whether a start-up Canadian private corporation engaged in SR&ED was a Canadian-controlled private corporation (“CCPC”)....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(5) - Paragraph 251(5)(b) | sole beneficiary of a trust did not have a s. 251(5)(b) right to trust shares | 44 |

| Tax Topics - General Concepts - Agency | application of Kinguk Trawl test of agency | 165 |

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Canadian-Controlled Private Corporation - Paragraph (b) | agreement was not a USA since it did not contain an outright transfer of the powers of the directors to the shareholders | 549 |

22 December 2009 Internal T.I. 2009-0343331I7 F - Determination of CCPC Status

A Quebec corporation (the “Corporation”) whose only outstanding shares were common shares, agreed in the Contract with a non-resident...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 220 - Subsection 220(2.2) | s. 220(2.2) precluded accepting a late amendment | 81 |

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Canadian-Controlled Private Corporation | shareholder agreement affecting how the majority of directors exercised their rights was not a USA | 362 |

20 December 2004 External T.I. 2004-0092871E5 F - Arm's Length: de facto control

In 1999-0008405 F, CRA applied IT-64R4 in generally commenting that s. 84.1 could apply where an individual who sold the individual’s shares of...

28 June 2004 External T.I. 2004-0059311E5 F - Associated Corporations

CRA indicated, regarding a debenture that was convertible into shares of the CCPC issuer by the holder (Lenderco) in order to safeguard the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(3) - Paragraph 256(3)(a) | "controlled, directly or indirectly in any manner whatever" includes de jure control | 115 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(6) | where s. 256(6) applies, it excludes both de jure and de facto control by the creditor | 166 |

23 June 1995 External T.I. 9510475 - ASSOCIATED CORPORATIONS

With respect to a situation where one corporation ("Supplyco") owned 50% of the shares of another corporation ("Distributorco") and the majority...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(1) - Paragraph 256(1)(a) | 38 |

20 March 1995 External T.I. 9424295 - 256(5.1) CONTROL AND GOVERNING BODIES

With respect to whether an incorporated professional business would be subject to de facto control by a professional body where an order has been...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | 99 |

1 September 1995 External T.I. 9503925 - C.C.P.C.

A submission that a 60% non-resident shareholder did not control what was alleged to be a CCPC by virtue of terms of the shareholders' agreement...

28 July 1994 External T.I. 9417455 - CCPC STATUS

"In addition to the factors expressed in paragraph 19 of IT-64R3, the Department would also consider the composition of the board of directors,...

91 C.R. - Q.9

Provided that Canadian-resident trustees, in fact, control a private corporation, it would be a CCPC even if it has non-resident beneficiaries.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Canadian-Controlled Private Corporation | 47 |

A.P.F.F. 1990 Round Table, Question 36, No. 9317770

In order for the exception to apply, the arrangement must have been entered into for commercial and not for the purpose of controlling the other...

20 March 1995 External T.I. 9424295 - 256(5.1) CONTROL AND GOVERNING BODIES

With respect to the situation where an incorporated professional is required to carry on business under the supervision and control of an...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | 82 |

12 August 1992 T.I. 921604 (April 1993 Access Letter, p. 155, ¶C248-134; Tax Window, No. 23, p. 12, ¶2130)

Where a shareholder's agreement between two 50% shareholders provides that each shareholder will elect two members of the board of the directors...

29 July 1992 Memorandum (Tax Window, No. 21, p. 4, ¶2037)

Where the chair of a shareholder's meeting has the deciding vote and is one of two 50% shareholders, she generally will have de facto control of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 249 - Subsection 249(4) | 91 |

29 July 1992 Memorandum (Tax Window, No. 21, p. 1, ¶2038)

An estate that does not own voting shares of a corporation nonetheless may be in a position to exercise some influence over the corporation that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(4) | 81 |

29 June 1992 Internal T.I. 7-920444

Discussion of whether persons have effective control with respect to a substantial block of shares in a widely-held corporation where there is...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 249 - Subsection 249(4) | 10 |

91 C.R. - Q.12

Where a 50% shareholder has a casting vote by virtue of being chairperson, the corporation generally will be controlled directly or indirectly in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 249 - Subsection 249(4) | 25 |

20 September 1990 Internal T.I. 7-902376

"The introduction of subsection 256(5.1) expands the judicially based de jure control concept to include de facto control situations where the...

3 January 1990 T.I. 5-9256 (Tax Window Files "'Meaning of Canadian-Controlled Private Corporation' - Control Test"

Where a Canadian-resident private corporation owns all the shares of a resident Canadian corporation ("N") which, in turn, owns all the shares of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Canadian-Controlled Private Corporation | 81 |

22 September 89 T.I. (February 1990 Access Letter, ¶1130)

Father has his corporation invest $150,000 in a corporation owned by his daughter and her husband, by acquiring shares that were retractable at...

89 C.R. - Q.15

"While the ability to elect a majority of the directors, or to control the day to day management and operation of the business, may be...

3 Aug. 89 T.I. (Jan. 90 Access Letter, ¶1086)

RC rejected a submission that "control in fact" means control by a person who does not otherwise control the corporation where that person has any...

88 C.R. - Q.41

The enactment of ss.256(5.1) and 256(1.4) did not alter RC's policy described in IT-64R2, paragraph 31 respecting rights of first refusal and...

Gouin-Toussaint, September 1989 Revenue Canada Round Table (Dec. 89 Access Letter, ¶1040)

A public corporation and a private corporation plan to each acquire ½ of the common shares of a third corporation ("Opco"). The public...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | 98 | |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | 79 |

Gouin-Toussaint, September 1989 Revenue Canada Round Table (Dec. 89 Access Letter, ¶1040)

A daughter who had de jure control of a corporation operating three boutiques was unlikely in the circumstances to run her business independently...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | 98 | |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | 113 |

Gouin-Toussaint, September 1989 Revenue Canada Round Table (Dec. 89 Access Letter, ¶1040)

A non-resident individual involved in the battery-making business in the United States controlled a Canadian corporation of which the non-resident...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | 79 | |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | 113 |

IT-64R4 "Corporations: Association and Control (Archived) 1 November 2004

23. Whether a person or group of persons can be said to have de facto control of a corporation, notwithstanding that they do not legally control...

IT-458R "Canadian-Controlled Private Corporation"

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(6) | 0 |

Articles

Boriana Christov, "De Facto Control", Tax Topics, No. 1978, 4 February 2010, p. 1.

Kroft, "Meaning of de facto Control - Emerging Income Tax Issues", 1991 Conference Report, p. 8:42.

Subsection 256(5.11)

Cases

North American et al. v. The Deputy Minister of Finance, 2019 MBQB 29

Dewar J reversed a finding of the Manitoba Tax Appeals Commission that a corporation (“533”) was subject to de facto control (as described in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | spouse made her own decisions re restaurant | 376 |

Administrative Policy

7 October 2022 APFF Roundtable Q. 8, 2022-0942151C6 F - Surplus stripping

A corporation (Brother-Portfolioco) owned by an individual (Brother) sells a 50% shareholding in Opco to a corporation (Sister-Holdco) owned by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) | incorporating a sub through which a share sale will occur so as to avoid s. 84.1 is not per se GAARable | 179 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(2) | permissible use of sale through subsidiary to avoid s. 84.1 | 85 |

Subsection 256(6) - Idem [Control in fact]

Cases

Silicon Graphics Ltd. v. Canada, 2002 DTC 7113, 2002 FCA 260

In rejecting a submission of the Crown that a U.S. corporation ("Silicon U.S.") had de facto control of the taxpayer and finding that the taxpayer...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Canadian-Controlled Private Corporation | U.S. public shareholders not a group; no de facto control by lender/licensor | 345 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | must be right to affect board or directly influence shareholders | 187 |

| Tax Topics - Statutory Interpretation - Hansard, explanatory notes, etc. | 23 | |

| Tax Topics - Statutory Interpretation - Interpretation Act - Subsection 45(2) | 56 | |

| Tax Topics - Statutory Interpretation - Interpretation Bulletins, etc. | 64 |

Administrative Policy

4 February 2015 External T.I. 2015-0565741E5 - Canadian-controlled private corporation

As a condition to distributing shares of Aco to the beneficiaries of a testamentary trust of which it was sole trustee, the trustee ("Pubco"),...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(11) - Investment Contract | indemnity agreement was not "indebtedness" | 47 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(5) - Paragraph 251(5)(b) | s. 256(5)(b) applied to acquisition right upon default under indemnity | 167 |

8 October 2010 Roundtable, 2010-0373161C6 F - Paragraphs 256(3) and 256(6) ITA

Given the application of s. 256(6) to the entire Act, if the conditions set out in that subsection are otherwise satisfied, can CRA confirm...

28 June 2004 External T.I. 2004-0059311E5 F - Associated Corporations

After indicating, regarding a debenture that was convertible into shares of the CCPC issuer by the holder (Lenderco) in order to safeguard the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(3) - Paragraph 256(3)(a) | "controlled, directly or indirectly in any manner whatever" includes de jure control | 115 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | the defined phrase includes de jure control | 56 |

8 June 2000 Internal T.I. 1999-0012817 F - Sociétés associées

Although s. 256(6)(a) was satisfied, s. 256(6)(b) was not satisfied regarding the shareholding of Holdco1 in Opco1. Although CCRA accepted that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(3) | s. 256(3) does not apply where s. 256(6) does not apply | 192 |

IT-458R "Canadian-Controlled Private Corporation"

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | 0 |

Paragraph 256(6)(a)

Administrative Policy

8 January 2004 External T.I. 2003-0040575 F - Associated Corporations

Although Mr. X held all of the issued and outstanding shares of Opco, an arm’s length lender (“Lendco”) held a debenture which was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(1.4) - Paragraph 256(1.4)(a) | lender’s right to acquire 99% of shares in event of insolvency engaged s. 256(1.4)(a) | 73 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(1.2) - Paragraph 256(1.2)(c) | rule in s. 256(1.2)(c) references de jure control, not de facto control | 73 |

Subsection 256(6.1) - Simultaneous control

Administrative Policy

8 October 2010 Roundtable, 2010-0373241C6 F - Acquisition of Control

In the course of a non-committal response as to whether there is an acquisition of control of a public company when its shareholders exchange most...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(7) - Paragraph 256(7)(d) | question of fact whether somersault transaction results in acquisition of control of a public company | 164 |

17 April 2001 Internal T.I. 2001-0064567 F - SPCC-PARTHENON

The Directorate followed Parthenon in finding that a private corporation, whose shares were held by a public corporation as an intermediary in a...

5 October 2000 External T.I. 2000-0037965 - Application of Parthenon Case - Control

With respect to cases prior to December 1999, it was the Agency's view "that Parthenon does not apply to restrict control of a corporation to only...

Subsection 256(7) - Acquiring control

Paragraph 256(7)(a)

Administrative Policy

22 August 2014 External T.I. 2014-0540751E5 F - Acquisition of control

{kind=link}

Two brothers (A and B) own 100% of the shares of Holdco A and Holdco B, respectively, which, each in turn, owns 50% of the shares of Opco. A...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(2) - Paragraph 251(2)(b) - Subparagraph 251(2)(b)(iii) | cousins part of related control group while fathers alive | 244 |

12 December 2013 External T.I. 2013-0484031E5 - Application of clause 256(7)(a)(i)(B)

A limited partnership which owns less than 50% of the voting shares of a corporation will, as a result of a reorganization of capital, own more...

2011 Ruling 2010-0360921R3 - Change of trustee - control

Opco, which has net capital and non-capital losses, is controlled by a Trust whose trustees are three resident individuals (Trustees 1, 2 and 3)...

22 March 2005 External T.I. 2005-0111811E5 - Acquisition of Control

The transfer of shares from the deceased to trusts the executors of which were his surviving spouse and two children would not result in an...

12 August 1994 External T.I. 9412385 - CHANGE OF CONTROL

If at 10:00 a.m. a corporation ("Bco") issues one common share to an unrelated corporation ("Dco"), and at 10:30 on the same day, Bco acquires the...

22 January 1993 T.I. (Tax Window, No. 28, p. 10, ¶2379)

Where the articles of a corporation provide that the voting rights associated with a particular block of voting shares (representing more than 50%...

23 March 1992 T.I. 913478 (April 1993 Access Letter, p. 156, ¶C248-135)

Where an individual owned all the shares of A Co and controlled B Co by reason of being the sole trustee of a family trust which owned its shares,...

90 C.R. - Q44

Where an individual acquires from a related person the shares of a corporation which has a wholly-owned subsidiary, RC considers that there has...

90 C.R. - Q41

Where there has been an acquisition of shares by more than one person, those persons will be deemed not to have acquired control if each of them...

26 February 1990 T.I. (July 1990 Access Letter, ¶1350)

Where prior to a section 86 reorganization of Opco, 50% of its voting shares were held by Mr. A (through his holding company), 20% by Mrs. A and...

89 C.R. - Q.16

Where two brothers (A and B) each own 50% of the voting shares of Opco and the shares of Opco owned by B are converted into non-voting shares, A...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 249 - Subsection 249(4) | 159 |

October 1989 Revenue Canada Round Table - Q.25 (Jan. 90 Access Letter, ¶1075)