Cases

EYEBALL NETWORKS INC. v. HER MAJESTY THE QUEEN, 2021 FCA 17

Before finding that s. 160 did not apply to a s. 55(3)(a) spin-off transaction in which each component transaction entailed a value-for-value...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | s. 160 did not apply to s. 55(3)(a) where each step involved a value-for-value exchange (including the cross-share redemptions) | 565 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | “series of transactions” requires at least one tax-driven transaction | 284 |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(9) | a shareholder whose shares have been redeemed has provided valuable consideration therefor by surrendering its shares | 136 |

| Tax Topics - General Concepts - Fair Market Value - Other | note supported only by pref, then note, of a sister had full FMV | 132 |

St-Pierre v. Canada, 2018 FCA 144

A private corporation that sold eligible capital property in 2008 declared a capital dividend in the year in an amount which included the untaxed...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2) | retroactive judgment annulling a dividend did not retroactively give rise to a shareholder debt for the annulled amount | 624 |

Anderson v Benson Trithardt Noren LLP, 2016 SKCA 120, aff'd 2017 SCC CanLii 8568

When CRA gave notice in 2013 of a proposed audit, the taxpayer’s accounting firm realized that it had failed to instruct the taxpayer’s...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Rectification & Rescission | drop-down documents could not be declared retroactive to the previously-agreed effective date, as this would undercut the Tax Court | 286 |

Nussey v. Canada, 2001 DTC 5240, 2001 FCA 99

The two sons of the taxpayer had transferred to him shares of a family corporation. The shareholders' agreement provided that, on the death of a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Mistake | 160 | |

| Tax Topics - Income Tax Act - Section 70 - Subsection 70(5) | 112 |

Stone's Jewellery Ltd. v. Arora, [2000] GSTC 168 (Alta. Ct. Q.B.)

A transaction in which a company paid for a real estate property but the shareholders (who were not registered for GST purposes and, therefore,...

Sussex Square Apartments Ltd. v. R., 99 DTC 443, [1999] 2 CTC 2143 (TCC), aff'd 2000 DTC 6548, [2000] 4 CTC 203, Docket: A-40-99 (FCA)

After the taxpayer had, for some time, been disposing of apartments suites which it held under a headlease by way of assignment rather than a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(a) | assignment of lease for lump sum gave rise to taxable profit whereas subleasing for lump sum gave rise to s. 12(1)(a) receipt and s. 20(1)(m) reserve | 134 |

| Tax Topics - General Concepts - Stare Decisis | 40 | |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(m) | lump sum received for granting of 99-year subleases were eligible for s. 20(1)(m) reserve | 118 |

Barnabe Estate v. Minister of National Revenue, 99 DTC 5387, [1999] 4 CTC 5 (FCA)

The Court, in reversing a finding of the trial judge, found that the deceased taxpayer had entered into an oral agreement with his corporation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) | 44 |

The Queen v. Larsson, 97 DTC 5425 (FCA)

An order of the British Columbia Supreme Court made in 1993 that mortgage payments made from November 1989 onward by the taxpayer on a house that...

Dale v. R., 97 DTC 5252, [1997] 2 CTC 286 (FCA)

Before finding that an order of the Nova Scotia Supreme Court (obtained without the federal Crown being a party to the proceedings) retroactively...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Rectification & Rescission | retroactive effect of nunc pro tunc rectification order | 177 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Dividend | 78 | |

| Tax Topics - Income Tax Act - Section 83 - Subsection 83(2) | 78 | |

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) | retroactive validation by Superior Court of preference share issuance was effective for s. 85 purposes | 171 |

| Tax Topics - Statutory Interpretation - Provincial Law | 140 |

Greenway v. Canada, 96 DTC 6529 (FCA)

Various conditions contained in an agreement for the acquisition of a MURB development by co-investors including the contractor's undertaking to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Start-Up and Liquidation Costs | 72 | |

| Tax Topics - General Concepts - Ownership | taxpayer was beneficial owner of MURB investment notwithstanding defects in agreement to acquire title from title holder | 142 |

Kettle River Sawmills Ltd. v. The Queen, 92 DTC 6525, [1992] 2 CTC 276 (FCTD)

Timber rights were not acquired on the intended adjustment date of March 26, 1974 but instead were acquired no earlier than the time that the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 13 - Subsection 13(21) - Depreciable Property | status does not turn on whether CCA actually claimed | 69 |

R. v. Hutton, [1990] 2 CTC 258 (Alta. C.A.)

The taxpayer fraudulently caused his employer to pay invoices for work on renovation to his home in 1983 and 1984. After the renovations were...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 239 - Subsection 239(1) - Paragraph 239(1)(d) | no wilful evasion if by time for return filing, the amount no longer was income | 119 |

Shaw v. The Queen, 89 DTC 5194, [1989] 1 CTC 386 (FCTD), aff'd 93 DTC 5213 (FCA)

The efficacy of a pre-incorporation contract was recognized.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Substance | 35 | |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Property | 22 | |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(4) | 266 |

Bouchard v. The Queen, 83 DTC 5193, [1983] CTC 173 (FCTD)

Before holding that the Statute of Frauds did not preclude a finding that the taxpayer held land in trust for his son and daughter-in-law,...

Scandia Plate Ltd. v. The Queen, 83 DTC 5009, [1982] CTC 431 (FCTD)

Control of a corporation was not acquired until the date for closing the agreement of purchase and sale, when the purchaser acquired ownership of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(1) | 178 | |

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Canadian-Controlled Private Corporation | 28 |

Perini Estate v. The Queen, 82 DTC 6080, [1982] CTC 74 (FCA)

It was held that "interest" calculated from the closing date of a share purchase on outstanding instalments of a purchase price was taxable as...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(c) | parties were entitled to treat conditional interest, when paid, as having retrospective absolute effect | 319 |

Kingsdale Securities Co. Ltd. v. The Queen, 74 DTC 6674, [1975] CTC 10 (FCA)

Since the settlors lacked the requisite intention prior to the execution of settled trusts, the execution of the trust deeds did not have...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(2) | 36 | |

| Tax Topics - Income Tax Act - Section 169 | 84 | |

| Tax Topics - Income Tax Act - Section 172 - Subsection 172(2) | 84 | |

| Tax Topics - Income Tax Act - Section 96 | 19 |

Howard v. The Queen, 74 DTC 6607, [1974] CTC 857 (FCTD)

The BC Supreme Court on February 16, 1970 ordered the taxpayer to pay $200 per month to his wife commencing February 1, 1970. On October 22, 1973...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 60 - Paragraph 60(c) | 85 |

Nelson v. The Queen, 74 DTC 6266, [1974] CTC 360 (FCA)

Although it was the intention of the four related shareholders of a corporation that father hold 100 voting participating shares and each of his...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | 171 |

Guilder News Co. (1963) Ltd. v. MNR, 73 DTC 5048, [1973] CTC 1 (FCA)

The sale in 1964 of shares by a corporation to its sole shareholder at an undervalue gave rise to a benefit to the shareholder notwithstanding...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 121 | 13 | |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | restoration of previous year's detriment was benefit | 231 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Dividend | 70 |

Rose v. MNR, 73 DTC 5083, [1973] CTC 74 (FCA)

It was held that a management services contract between a corporation ("Central Park Estates Limited") and a partnership with an effective date of...

Minister of National Revenue v. Lechter, 66 DTC 5300, [1966] CTC 434, [1966] S.C.R. 655

In the taxpayer's 1955 taxation year, he accepted the Department of Transport's formal offer of settlement for compensation in respect of its...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Timing | 92 |

Falconer v. Minister of National Revenue, 62 DTC 1247, [1962] CTC 426, [1962] S.C.R. 664

The members of a syndicate that had acquired an oil farm-out agreement incorporated a private company ("Ponder") on June 15, 1951, and Ponder...

See Also

Corporation immobilière des Laurentides Inc. v. Agence du revenu du Québec, 2024 QCCQ 5297

Two individuals, who wished to acquire a condo unit in a building (“265”) which was still under construction by the taxpayer (“CILI”),...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 232 - Subsection 232(1) | the satisfaction of a resolutory sales condition nullified the original sale so that reconveyance of the realty to the vendor was not a supply | 572 |

Wise v. The Queen, 2019 TCC 196

An individual leased a building under a 5-year lease with a 5-year renewal option to a corporation (VMS) wholly-owned by her and her son. VMS then...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | no immediate taxable benefit to a landlord-shareholder from improvements made to the leased building by the tenant-corporation | 363 |

Black v. The Queen, 2019 TCC 135

The taxpayer (“Black”) controlled both Hollinger Inc. (“Inc.”) and Hollinger International Inc. (“International”). In 2004, the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) - Subparagraph 20(1)(c)(i) | an ancillary income-earning purpose for making a loan whose terms were never finalized was sufficient to satisfy s. 20(1)(c)(i) | 659 |

| Tax Topics - General Concepts - Payment & Receipt | advance on another party’s behalf established a loan | 141 |

Trower v. The Queen, 2019 TCC 77 (Informal Procedure)

While Ms. Trover was separated from Mr. Trover, their jointly-owned company (Cove) paid amounts into their joint bank account. That same year,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 82 - Subsection 82(1) - Paragraph 82(1)(a) | purported retroactive dividend would not have been agreed to by both directors at the time | 319 |

Bourgault v. The Queen, 2019 TCC 6

The written agreement for the purchase by the taxpayer of shares of a real estate corporation (“Quatre Saisons”) stated that the purchase...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Rectification & Rescission | a rectification judgment was “justifiably obtained” and, therefore, followed for tax purposes | 404 |

De Vries v The Queen, 2018 TCC 166

The two individual shareholders of a corporation (“IPG”) were assessed under s. 160 regarding a dividend they had received from IPG. The...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 224 - Subsection 224(1) | a corporate creditor’s oral agreement to postpone collection of his loan defeated a RTP encompassing that loan | 392 |

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | if requirement to pay assessment had been valid, it would have flowed through with a dividend | 302 |

Melançon v. The Queen, 2018 TCC 73

The taxpayer was the sole shareholder of a home construction company. After the CRA auditor noticed that amounts booked as “subcontractor...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | failure of a house construction company to charge a mark-up on its costs incurred for shareholder work generated at taxable benefit/rebooking of “expense” as shareholder advance was retroactive tax planning | 348 |

Mammone v. The Queen, 2018 TCC 24, rev'd 2019 FCA 45

The CRA revocation of a registered pension plan (the “New Plan”) was invalid due to inadvertent failure to comply with the 30-day notice...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4) | RPP revocation beyond the normal reassessment period retroactively validated an unsupportable reassessment under s. 56(1)(a)(i) | 414 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(9) | subsequent retroactive deregistration of RPP also retroactively validated an assessment factually made on basis of plan’s invalidity | 216 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4) - Paragraph 152(4)(a) - Subparagraph 152(4)(a)(i) | subsequent retroactive deregistration of RPP would not establish carelessness in previous return filing | 197 |

| Tax Topics - Income Tax Act - Section 147.1 - Subsection 147.1(12) | subsequent deregistration of RPP beyond normal reassessment period nonetheless retroactively validated reassessment | 95 |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(1) - Paragraph 56(1)(a) - Subparagraph 56(1)(a)(i) | valid assessment for transfer to an RPP that was retroactively deregistered | 85 |

Cook v. The Queen, 2017 TCC 188 (Informal Procedure)

Whether the taxpayer was able to take a deduction for a dependent child depended on whether in the year in question she was considered to have a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118 - Subsection 118(5) | court order retroactively terminating support obligation to the taxpayers’ agreement thereon respected – but s. 118(1) claim denied as entailing proration | 446 |

Gillen v. The Queen, 2017 TCC 163, aff'd 2019 FCA 62

A limited partnership was found to have immediately transferred the beneficial ownership of applications to the Saskatchewan government for potash...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110.6 - Subsection 110.6(14) - Paragraph 110.6(14)(f) - Subparagraph 110.6(14)(f)(ii) | property was not used in a business for s. 110.6(14)(f)(ii) purposes when it was beneficially acquired and dropped-down on the same day | 364 |

| Tax Topics - General Concepts - Ownership | test of beneficial ownership | 112 |

Deragon v. The Queen, 2015 TCC 294

Vendors agreed to sell shares for a sale price of $16 million, of which $2 million was payable in subsequent years only if an EBITDA condition...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Proceeds of Disposition - Paragraph (a) | sales proceeds reduced by subsequent price adjustment clause but included conditional sales proceeds | 480 |

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(g) | reverse earnout amounts included in proceeds | 245 |

Charania v. The Queen, 2015 DTC 1103 [at at 614], 2015 TCC 80 (Informal Procedure)

An individual shareholder of a corporation ("B&N") thought that he was the beneficial owner of his home, but everyone else, including his...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | no shareholder benefit from erroneous property valuation | 314 |

Murphy Estate v. The Queen, 2015 TCC 8

An estate unsuccessfully argued that the effect of the settlement of some estate litigation pursuant to a consent order, which provided for the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 146 - Subsection 146(8.8) | consent order for settlement of estate litigation did not have retroactive effect | 201 |

Al-Hossain v. The Queen, 2014 TCC 379

To secure mortgage financing for his home purchase, the appellant's friend ("Khandaker") agreed to co-sign the mortgage documents and to be placed...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 254 - Subsection 254(2) | co-owner was not occupant and bare trust declaration was too late | 282 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(1) | bare trust declaration was too late | 138 |

James v. The Queen, 2013 DTC 1135 [at at 705], 2013 TCC 164

The British Columbia Court of Appeal ordered a retroactive increase in the monthly amount of the support payments the taxpayer paid to his spouse,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56.1 - Subsection 56.1(4) - Support Amount | retroactive court orders | 113 |

Twomey v. The Queen, 2012 DTC 1255 [at at 3739], 2012 TCC 310

In 2005, the taxpayer sold 78 of his 100 common shares of an Ontario corporation ("115") to the other shareholder ("D.K."), and claimed the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110.6 - Subsection 110.6(1) - Qualified Small Business Corporation Share | records rectified to reflect 24-mo. hold for shares | 282 |

Sommerer v. The Queen, 2011 DTC 1162 [at at 845], 2011 TCC 212, aff'd 2012 FCA 207

In 1996, the taxpayer (a Canadian-resident individual) purported to sell shares of a Canadian company ("Vienna"), while retaining the rights to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(2) | 233 | |

| Tax Topics - Statutory Interpretation - Treaties | 57 | |

| Tax Topics - Treaties - Income Tax Conventions | 176 |

Gestion Forêt-Dale Inc. v. The Queen, 2009 DTC 1378, 2009 TCC 255

After the accountants, over a year later, realized that a reorganization plan resulted in Part IV tax because two corporations were not connected...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 163 - Subsection 163(2) | 35 |

Gagnon v. The Queen, 2008 DTC 3111, 2006 TCC 194

The taxpayer originally signed an agreement for the sale of his half interest in a business (which was found to be held in a corporation) to his...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(3) | 137 |

Avotus Corporation v. The Queen, 2007 DTC 215, 2006 TCC 505

The taxpayer’s foreign affiliate had acted as the taxpayer’s agent for the purpose of carrying on business (and deducting the losses). Among...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Evidence | 70 | |

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Canadian-Controlled Private Corporation | tie-breaking vote of 50% non-resident shareholder | 92 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | 91 | |

| Tax Topics - Income Tax Act - Section 9 - Agency - Agency | 97 |

Lloyd v. The Queen, 2002 DTC 1493 (TCC)

Although the taxpayer signed an agreement with a holding company for the sale of shares in a company ("READ") to the holding company, Bowman...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Tax Avoidance | taxapyer can argue legally ineffective transactions | 139 |

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) | 76 | |

| Tax Topics - Income Tax Regulations - Schedules - Schedule II - Class 1 - Paragraph 1(q) | 70 |

Fallis v. The Queen, 2002 DTC 1242 (TCC)

Following an assessment of the taxpayer under s. 160 she alleged that there had been a transfer of a one-half interest in a property to her from...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | 122 |

McAnulty v. The Queen, 2001 DTC 942 (TCC)

The time at which the taxpayer's employer agreed to issue shares to her was the time at which the president called her to his desk and told her...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110 - Subsection 110(1) - Paragraph 110(1)(d) | unauthorized grant of rights | 200 |

Glassford v. The Queen, 2000 DTC 2531 (TCC)

O'Connor T.C.J. applied s. 8(3) of the Land Act (BC), which provided that "a disposition of Crown land is not binding on the government until the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Real Estate | 83 |

Horkoff v. The Queen, 97 DTC 621, [1996] 3 CTC 2737 (TCC)

Dividends that were purportedly paid to the taxpayers "as of" December 30, 1990 were dividend income to the taxpayers in their 1991 taxation years...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 82 - Subsection 82(1) - Paragraph 82(1)(a) | back-dated dividend | 67 |

Leung v. MNR, 92 DTC 1090, [1992] 1 CTC 2110 (TCC)

In rejecting a submission of the Crown that the taxpayers were not assisted by a price adjustment clause, Kempo J. noted that they had addressed...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Shares | 177 |

Voukelatos v. MNR, 92 DTC 1076, [1992] 1 CTC 2154 (TCC)

Following the exercise by the taxpayer of a "shot-gun" clause in the shareholders' agreement, it was understood by him and the other shareholder...

Seaman v. MNR, 90 DTC 1909, [1990] 2 CTC 2469 (TCC)

The taxpayer sold shares in 1983 to a trust for his children for proceeds of $388,000 paid by way of demand promissory note. After reassessment of...

Amirault v. MNR, 90 DTC 1330, [1990] 1 CTC 2432 (TCC)

An amendment to the terms of a stock option plan that retroactively increased the exercise price of the options in order to satisfy the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110 - Subsection 110(1) - Paragraph 110(1)(d) | Increase to exercise price did not create new option | 159 |

May Estate v. MNR, 89 DTC 534, [1989] 2 CTC 2305 (TCC)

A court order became effective from the date it was pronounced rather than not taking effect until the date of issuance.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 70 - Subsection 70(6) | 64 |

Pellizzari v. MNR, 87 DTC 56, [1987] 1 CTC 2106 (TCC)

After finding that the taxpayer's employer had conferred a benefit on her in 1979 and 1980, Couture C.J. found that at the time of the decision...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | benefit qua employee | 155 |

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(1) - Paragraph 6(1)(a) | 112 |

Robert Bédard Auto Ltée. v. MNR, 85 DTC 643, [1985] 2 CTC 2354 (TCC)

Before going on to find that the taxpayer had disposed of property on the effective date for a lease-purchase agreement in which land and building...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 13 - Subsection 13(21) - Disposition of Property | 92 |

Spence v IRC (1941), 24 TC 311 (Ct of Sess (1st Div'n))

The taxpayer sold shares to a third party in 1933 under a contract which he subsequently alleged to have been induced by fraud. In 1939 he...

Waddington v. O'Callaghan (1931), 16 TC 187 (KBD)

A father instructed his solicitors that it was his intention to take in his son as a partner effective on the date of the instruction and...

Administrative Policy

7 September 2022 Internal T.I. 2022-0931081I7 - Retroactive support payments

A 2018 court order required retroactive child and spousal support payments to be made by an individual to a former spouse on a monthly basis for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 60.1 - Subsection 60.1(3) | application of s. 60.1(3) to payments already made in the current and preceding year | 388 |

| Tax Topics - Income Tax Act - Section 60 - Paragraph 60(b) | CRA respects the effect of a court order providing that a lump sum payment was in satisfaction of a retroactive periodic support obligation | 276 |

14 January 2022 Internal T.I. 2021-0913891I7 - CERS - Sublease

Although the definition of “qualifying rent expense” for CERS (rent subsidy) purposes generally includes a requirement that the rent be paid...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125.7 - Subsection 125.7(1) - Qualifying Rent Expense | sublease is generally between sublessor and subtenant, so that landlord consent generally is not required (unless expressly stipulated) for the sublease to take effect | 253 |

20 January 2022 Internal T.I. 2021-0877511I7 - CERS- Written Agreement

The definition of “qualifying rent expense” for Canada emergency rent subsidy (“CERS”) purposes includes a requirement that the rent be...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125.7 - Subsection 125.7(1) - Qualifying Rent Expense | a lease could constitute a continuation of an agreement to lease | 264 |

GST/HST Notice 312 Proposed GST/HST Treatment of Supplies of Human Ova and In vitro Embryos May 2019

A proposed GST/HST amendment would zero-rate the supply of an ovum – which would have the effect of rendering the importation of an ovum as a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Schedules - Schedule VI - Part I - Section 6 | 481 | |

| Tax Topics - Excise Tax Act - Schedules - Schedule VII - Section 13 | 390 | |

| Tax Topics - Excise Tax Act - Schedules - Schedule V - Part II - Section 1 - Institutional Health Care Service | assimilation of provision of ovum or embryo to single supply at fertility clinic of institutional health care service | 80 |

27 March 2018 Internal T.I. 2017-0691941I7 F - Investissement frauduleux – Fraudulent Investment

Individuals had “invested” in what turned out to be a Ponzi scheme under which for many years they reported annual income inclusions for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4.2) | s. 152(4.2) reversal of Ponzi interest inclusion must be applied for by 10th anniversary of the taxation year | 252 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(p) - Subparagraph 20(1)(p)(i) | Ponzi scheme investors can generally write off their reinvested interest income in the year the perpetrators are charged | 283 |

5 October 2018 APFF Roundtable Q. 15, 2018-0768861C6 F - Share exchange and statute of limitation

CRA accepted that where a price-adjustment clause retroactively adjusts a tax attribute, such as adjusted cost base, that arose from a rollover...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4) | a price adjustment clause can operate re statute-barred transactions to affect a tax attribute that is used in the current year | 252 |

16 June 2016 External T.I. 2015-0623031E5 F - Application of paragraph 7(1)(b)

On a sale of a corporation, the outstanding employee stock options are surrendered for a price reflecting the sale price for the shares. However,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(1) - Paragraph 7(1)(b) | contingent amount included under s. 7(1)(b), cannot subsequently be excluded | 237 |

9 October 2015 APFF Roundtable Q. 10, 2015-0595671C6 F - Question 10 - Table Ronde APFF 2015

When CRA disallows part of the deduction by a corporation of the management fee charged to it by another (presumably affiliated) corporation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Income-Producing Purpose | generally should be reimbursement for expenses incurred for affiliate | 226 |

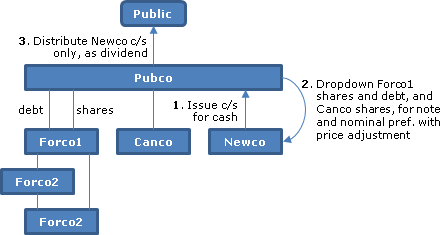

2013 Ruling 2013-0488291R3 - Reorganization of Corporations - Rollover

{kind=link}

Pubco (a Canadian public company) wishes to spin-off non-strategic assets to its shareholders without incurring the expense of a plan of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 215 - Subsection 215(6) | Spinco taking responsibility for Part XIII remittance obligation of Parent | 246 |

| Tax Topics - Income Tax Act - Section 52 - Subsection 52(2) | taxable dividend spin-off of thinly capitalized sub | 299 |

29 October 2013 External T.I. 2013-0507881E5 - Price adjustment clause

A price adjustent clause in the share provisions for preferred shares issued by Opco to the taxpayer in Year 1 in consideration for the transfer...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(3) | price adjustment payment recognized as s. 84(3) dividend when received | 330 |

25 September 2013 External T.I. 2013-0488571E5 F - Repayment of a dividend

Where a taxpayer and his wife repay a portion of the dividends received by them in their 2006 taxation year, can the taxes on those dividends be...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 82 - Subsection 82(1) - Paragraph 82(1)(a) | dividend declared cannot be nullified by subsequent board or shareholder resolution | 139 |

10 June 2013 STEP Roundtable Q. 7, 2013-0480291C6 - 2013 STEP Roundtable Q.7 - Price adjustment clause

The requirement in IT-169 that CRA be notified of the existence of a price adjustment clause was not carried over into S4-F3-C1, and no longer...

S4-F3-C1 - Price Adjustment Clauses

A price adjustment clause will be recognized where there was a bona fide intention to transfer at fair market value as determined by a fair and...

5 October 2012 APFF Roundtable, 2012-0453891C6 F - Price Adjustment Clause

The summary (which is more specific than the actual question) describes an estate freeze in which a taxpayer exchanges his common shares of a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(2) | price adjustment clause that is implemented potentially can prevent s. 75(2) application to estate freeze | 319 |

14 June 2012 External T.I. 2012-0443711E5 F - RAP - Annulation de la vente de l'immeuble

In confirming that a judgment declaring a sale of a home to be void would not affect the operation of the HBP rules where the home in question was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 146.01 - Subsection 146.01(1) - Eligible Amount | subsequent court-ordered voiding of home purchase funded with HBP does not affect satisfaction of the HBP conditions | 122 |

24 May 2012 External T.I. 2011-0429991E5 - Price Adjustment Clause

Mr. A engages in an estate freeze transaction in Year 1 in which all his common shares are exchanged in a s. 86 reorganization for preferred...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 70 - Subsection 70(5) | 157 |

17 May 2012 Internal T.I. 2012-0437001I7 F - Price Adjustment Clause

A price adjustment clause (PAC) is engaged to increase the fair market value of shares issued to the taxpayer on a s. 85(1) drop-down transaction....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) - Paragraph 85(1)(e.2) | no need to file amended s. 85(1) election where PAC engaged | 56 |

8 February 2012 Internal T.I. 2011-0431581I7 F - Sous-alinéa 6(1)a)(vi) proposé

Respecting the proposed adoption of s. 6(1)(a)(vi), CRA stated:

[W]e indicated in question 16 of the CRA Roundtable at the 2009 Annual Conference...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 220 - Subsection 220(3.1) | no penalties if taxpayer promptly refiles after announcement that favourable amendment will not proceed | 99 |

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(1) - Paragraph 6(1)(a) - Subparagraph 6(1)(a)(vi) | “studies” are at all levels and bursaries and tuition reimbursements potentially are included | 136 |

7 October 2011 APFF Roundtable Q. 4, 2011-0412071C6 F - Modifying a Capital Dividend Election

Where the directors declare a capital dividend and before the payment date for the dividend the corporation (which has individual shareholders)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 184 - Subsection 184(3) | short-cut method for direct assessment of shareholders for excess amount | 134 |

29 November 2011 Roundtable, 2011-0426361C6 F - Price adjustment clause and redemption of shares

CRA indicated that where there is subsequent payment to the redeemed shareholder as the result of the operation of a price adjustment clause to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(3) | deemed dividend arising from preferred share price adjustment clause arises in the year of actual payment | 150 |

6 December 2011 External T.I. 2010-0384701E5 F - Décès contribuable - Immobilisation admissible

Mr. X bequeathed all his property to his children including goodwill that he had generated over the years from his business, which his estate then...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 70 - Subsection 70(5.1) | application of s. 70(5.1) to bequest of goodwill | 210 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4.2) | CRA policy for adjusting a statute-barred year for a reduction in the 5th year of staged-proceeds sale | 147 |

21 November 2011 External T.I. 2011-0422191E5 F - Price adjustment clause and redemption of shares

if preferred shares with a redemption amount which is subject to a price adjustment clause are redeemed before there is an upward adjustment to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(3) | price adjustment payment recognized as s. 84(3) dividend when received | 54 |

7 October 2011 APFF Roundtable Q. 23, 2011-0412111C6 F - Validity of Price Adjustment Clause

CRA indicated that notwithstanding that para. 26 of IC 76-19R3 has not been modified to this effect, the validity of a price adjustment clause...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(7.1) | validity of price adjustment clause does not depend on filing an amended election | 105 |

7 October 2011 Roundtable, 2011-0411851C6 F - Fiducie de protection d'actifs

For asset protection purposes, Mr. X transferred his preferred shares of Opco to an asset protection trust of which he was the sole beneficiary....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 108 - Subsection 108(1) - Testamentary Trust - Paragraph (b) | distribution of property from asset protection trust directly, rather than via estate, to testamentary trust would taint it | 274 |

8 June 2010 STEP Roundtable Q. 2, 2010-0363071C6

For an amount to be "payable" to a beneficiary in a trust's taxation year, the beneficiary must have an enforceable right to payment by the end of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(24) | distribution note can be issued after year end based on administative delays in calculating income | 237 |

8 October 2009 External T.I. 2009-0338861E5 - Backdating of a completed transaction

A request to vary the income tax consequences of transactions that have already taken place will only be considered if such a variance would...

14 June 2007 Internal T.I. 2007-0229311I7 F - Capital Dividend Account

Subco declared a dividend payable to its parent (Parentco) which, in turn, declared a corresponding dividend to its individual shareholder (Mr....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Capital Dividend Account - Paragraph (b) | recording of dividend payable and dividend receivable between sub and parent was insufficient to constitute the payment of a capital dividend, so that there was no CDA addition | 132 |

| Tax Topics - General Concepts - Payment & Receipt | making accounting entries does not constitute payment of a dividend | 130 |

| Tax Topics - Income Tax Act - Section 184 - Subsection 184(3) | invalid payment of capital dividend (because no payment) was subject to Pt. III tax (given valid s. 83(2) election) for which no s. 184(3) election could be made as no payment | 135 |

21 February 2007 Internal T.I. 2006-0218421I7 F - Pension alimentaire - date d'exécution

CRA indicated that where a 2006 divorce judgment required a reduction in child support obligations retroactive to a date in 2003, the date on...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56.1 - Subsection 56.1(4) - Commencement Day | retroactive nature of a divorce judgment is to be respected | 112 |

11 April 2005 External T.I. 2005-0112321E5 F - Price adjustment clause

An estate freeze entailed the exchange by Mr. A of his common shares of Opco by way of purchase for cancellation for Class A preferred shares with...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 51 - Subsection 51(2) | CRA may accept a price adjustment clause adjusting of share consideration on s. 51 exchange if genuine attempt to establish FMV and issue of intervening share cancellation is addressed | 312 |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | where FMV of pre shares received on estate-freeze s. 51 exchange was less than that of the exchanged common shares, CRA would apply s. 51(2), not s. 15(1) | 142 |

21 March 2005 Internal T.I. 2005-0119961I7 F - CCPC STATUS

USco disposed of 50% of the shares of Canco to another corporation ("Holdco" – that was a Canadian-owned Canadian corporation), "retroactive" to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251.2 - Subsection 251.2(2) - Paragraph 251.2(2)(a) | moving from one shareholder to 2 equal shareholders generally entails an acquisition of control unless there is deadlock | 217 |

22 March 2005 Internal T.I. 2005-0115451I7 F - Extinction d'une remise de dette

The creditor forgave a debt pursuant to an agreement with an improved fortunes clause, such that the forgiveness was subsequently cancelled. After...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) - Forgiven Amount | no deduction where forgiven debt is subsequently restored pursuant to improved fortunes clause | 120 |

| Tax Topics - Income Tax Act - Section 80.01 - Subsection 80.01(10) | repayment deduction under s. 80.01(10) | 129 |

6 July 2004 External T.I. 2004-0081631E5 F - Price Adjustment Clauses

CRA indicated that it will accept a rollover form filed with a "yes" answer to the question concerning the existence of a price adjustment clause...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) | ticking "yes" box on election form is sufficient notice of price adjustment clause | 70 |

| Tax Topics - Income Tax Act - Section 51 - Subsection 51(1) | no requirement to notify CRA of price-adjustment clause regarding a s. 86 or 51 exchange | 95 |

2 March 2004 Internal T.I. 2003-0045921I7 F - 118(5) - impact d'une clause rétroactive

A separated couple on their divorce amended the provisions of their custody and support agreement to provide that, retroactive to a prior date,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118 - Subsection 118(5) | homologated order with effect of judgment that retroactively eliminated Monsieur’s support obligation re one of his children did not retroactively eliminate the s. 118(5) prohibition | 282 |

1 April 2003 External T.I. 2003-0004125 F - Freeze by Paying a Stock Dividend

A CCPC (Opco) paid a stock dividend of preferred shares with a fair market value of $800,000 and a paid-up capital of $80 to its sole shareholder,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 74.4 - Subsection 74.4(2) | non-application to stock dividend | 108 |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1.1) | s. 15(1.1) inapplicable to stock dividend paid to wholly-owning shareholder | 98 |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(b) | imputed disposition to which s. 69(1)(b) applied where common shares issued at undervaluation to children’s trust | 131 |

15 November 2002 Internal T.I. 2002-0162427 F - Price Adjustment Clause & 85(7.1)

Madame exchanged her Class A shares of the corporation for Class D shares having a redemption amount which CCRA subsequently determined was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) - Paragraph 85(1)(e.2) | significant FMV shortfall suggested that a benefit was desired to be conferred | 146 |

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(7) | amended s. 85(1) election must be filed if price-adjustment clause applied | 100 |

19 December 2001 Internal T.I. 2001-0109417 - TAXABLE BENEFITS

A revival of a corporation under the CBCA would appear to have retroactive effect and the revived corporation will generally have all the rights...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80.4 - Subsection 80.4(3) | 71 | |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | 42 |

24 May 2001 Internal T.I. 2000-0047827 F - PENSION ALIMENTAIRE-CLAUSE RETROACTIVE

The post-April 1997 agreement that effectively was ratified by the subsequent judgment was conditional on the support payable by Monsieur to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56.1 - Subsection 56.1(4) - Commencement Day - Paragraph (a) | subsequent judgment that varied support in divorce judgment caused a commencement day/ retroactive effective date of consent judgment not respected | 243 |

| Tax Topics - Income Tax Act - Section 56.1 - Subsection 56.1(4) - Support Amount | payment of arrears of periodic support would be periodic support under the related pre-May 1997 consent judgment | 212 |

18 April 2001 Internal T.I. 2001-0069467 - RETRO. AGREEMENT-FILM TAX CREDIT

An amended distribution agreement would not be accepted as retroactively causing a film to no longer be an excluded production given that, prior...

16 November 2000 External T.I. 2000-0035815 F - OPTION D'ACHAT D'ACTION

Regarding whether the taxpayer could modify the transactions carried out in connection with the exercise of a portion of the taxpayer’s stock...

10 March 1999 External T.I. 9829125 - PRICE ADJUSTMENT CLAUSE & 80(2)(G)

Although a price adjustment clause may be used for satisfying the requirements of s. 80(2)(g), "an acceptable price adjustment clause should not...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(2) - Paragraph 80(2)(g) | 36 |

1996 Corporate Management Tax Conference Round Table, Q.9 (CTO "Plans of Arrangement")

Ordinarily, RC will respect the ordering of a series of transactions where the order is specified in a plan of arrangement.

1996 Calgary Round Table, Q. 17 (961680) (CTO Effective and Closing Date")

Discussion of when the date of disposition/date of acquisition for a transaction may be prior to the closing date.

94 CPTJ - Q.19

RC will accept situations where revenue between the effective date of a transaction and the closing date is reported differently for financial...

92 CR - Q.30

RC generally will require that any elections under s. 85 that are affected by a price adjustment clause be amended.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(b) | 35 |

17 August 1992, T.I. 921353 (April 1993 Access Letter, p. 135, ¶C20-1141)

Forgiveness of accrued interest has legal effect from the date of the amendment to the debt obligation or such later date as is provided in the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(3) | 55 | |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(p) - Subparagraph 20(1)(p)(i) | 88 |

91 CR - Q.28

Any income earned prior to the adoption of a pre-incorporation contract by a corporation becomes its income for its first fiscal period and, where...

91 C.R. - Q.41

The date of disposition of property (and, therefore, the date upon which income commences to be earned by the purchaser) is the date the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | 37 | |

| Tax Topics - Income Tax Act - Section 9 - Timing | 50 |

91 CPTJ - Q.25

There have been instances where RC has administratively accepted that income earned between the effective date of sale of an oil and gas property...

16 September 1991 TI (Tax Window, No. 9, p. 9, ¶1451)

RC cautioned that in Dorcas v. MNR, 91 DTC 350 the Tax Court indicated that past events cannot be altered ab initio by steps taken ex post facto.

25 February 1991 TI (Tax Window, Prelim. No. 3, p. 29, ¶1123)

When a court judicially declares a person to have died on the day the person was last seen alive or the day on which it is likely that the person...

10 December 1990 TI (Tax Window, Prelim. No. 2, p. 20, ¶1065)

An annulment of a bankruptcy does not invalidate the application of s. 128 for the period commencing on the date the taxpayer became bankrupt and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 128 - Subsection 128(1) | 33 |

90 CR - Q.58

If the parties fail to notify RC of a price adjustment clause in their tax returns, this failure by itself will not preclude the acceptance of...

27 March 1990 TI (August 1990 Access Letter, ¶1364)

RC will not respect a price adjustment clause which contemplates that a final judgment of a court of competent jurisdiction would be binding as to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | 29 |

14 September 89 T.I. (February 1990 Access Letter, ¶1108)

In response to a submission that expenses incurred between the time of an agreement, and the time that the agreement is reduced to writing, are...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 66 - Subsection 66(12.6) | 38 |

87 CR - Q.70

Where the completion of an asset sale is subject to a true condition precedent (e.g., regulatory approval), then the vendor and purchaser cannot...

85 CR - Q.52

Efficacy of price adjustment clauses is recognized.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) | 48 |

80 CR - Q.14

RC is prepared to issue favourable rulings respecting price adjustment clauses used in an estate freeze, provided that the clause involves...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) | 17 |

IT-396R "Interest Income"

"Where an enforceable agreement for the sale of property is executed but the negotiated price is not paid until a subsequent date, any interest...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(c) | 0 |

IT-169 "Price Adjustment Clauses"

This bulletin has been cancelled and removed from the CRA website. It previously stated:

1

. ...If the parties have agreed that, if the...

IT-216 "Corporation Holding Property as Agent for Shareholder"

- A corporation may hold in trust, as agent for a shareholder, property that was acquired specifically to be held in this way. This situation,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Agency | 0 | |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(1) | 89 |

Articles

Kevyn Nightingale, John Sorensen, "Backdating of Dividends", Tax Topics (Wolters Kluwer), No. 2392, January 11, 2018, p. 1

Additional significance of having dividends paid in 2017 rather than 2018 (p. 1)

ln Canada, 2017 was the last year that dividends could be...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 82 - Subsection 82(1) - Paragraph 82(1)(a) | 290 |

Douglas S. Ewens, Paul Lynch, "Comments on Rectification", 2005 Conference Report, c. 23

Includes comments on CRA's position.

Darcy De Moche, Greg Johnson, "Recent Developments and Transactions Affecting Income Funds and Royalty Trusts", 2005 Conference Report, p. 17:6

Discussion of effect of releasing documents from escrow.

Michel Bourque, "Requirement of Notice to the Canada Customs and Revenue Agency", Tax Litigation, Vol. IX, No. 4, 2001, p. 590.

Jules Lewy, "Making Amends", CA Magazine, January/February 2002, p. 41

Discussion of Juliar by the taxpayer's counsel.

Wilfred M. Estey, "Pre-Incorporation Contracts: The Fog is Finally Lifting", Canadian Business Law Journal, Vol 33, No. 1, February 2000, p. 3.

Wertschek, "The Tax Advisor and Commercial Law: Some Issues", 1993 Conference Report, C. 24, pp. 24:31-39

Discussion of escrow arrangements, and of transactions that cannot be conditional.

Joel A. Nitikman, "When Shares are Issued", Canadian Current Tax, May 1995, Vol. 5, No. 8, p. 79.

Joel A. Nitikman, "Rescission of Contracts for Mistake", Canadian Current Tax, April 1995, Vol. 5, No. 7, p. 63.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | 0 |

Commentary

The tax consequences of transactions often turn upon when they occurred. Documents to legally implement a transaction often are not executed (or...