Subsection 215(1) - Withholding and remittance of tax

See Also

Curragh Inc. v. The Queen, 94 DTC 1894, [1995] 1 CTC 2163 (TCC)

There was no written assignment or other convincing evidence that a loan that an Australian corporation ("Giant") had made to the taxpayer had...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 215 - Subsection 215(3) | agent liability under s. 215(3) does not relieve principal of laibility under s. 215(1) | 151 |

| Tax Topics - Income Tax Act - Section 216 - Subsection 216(4) | s. 216 does not relieve payor of liability | 109 |

Nestle Enterprises Ltd. v. MNR, 92 DTC 1001, [1991] 2 CTC 2627 (TCC)

On January 17, 1989 the taxpayer withheld $535,579 of tax on a payment to a non-resident. On February 14, 1989 it mailed a cheque for that sum to...

Administrative Policy

2 June 2026 STEP Roundtable Q. 6, 2026-1089191C6 - Timing of Trust Remittance under Part XII

Pursuant to s. 214(3)(f)(i), where an amount has been made payable, but has not been paid or credited, by a trust to a non-resident beneficiary...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 214 - Subsection 214(3) - Paragraph 214(3)(f) | application of its 15-day remittance policy in Guide T4061 to a deemed payment under s. 214(3)(f)(i) | 171 |

T4061 NR4 - Non-Resident Tax Withholding, Remitting, and Reporting

Remittance by 15th of the following month

You have to remit your non-resident tax deductions so that the Canada Revenue Agency (CRA) receives them...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 216 - Subsection 216(4) | effective date | 99 |

16 August 2017 Internal T.I. 2015-0622751I7 - Part XIII Tax on Benefit to Non-resident

A foreign subsidiary of Canco (Opco) in turn wholly-owned a non-resident “Finco,” which made an interest-free loan to a non-resident sister of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(9) | s. 15(9) applies to interest-free loan between two foreign affiliates | 285 |

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | use of s. 160 to collect s. 15(9) liability of indirect FA on dividends paid to Canco | 275 |

| Tax Topics - Income Tax Act - Section 227.1 - Subsection 227.1(1) | s. 227.1 liability can extend to NR directors of a CFA | 176 |

| Tax Topics - Income Tax Act - Section 214 - Subsection 214(3) - Paragraph 214(3)(a) | benefit from interest free loan by CFA to Canco sister deemed to be a dividend subject to Pt XIII tax | 177 |

| Tax Topics - Income Tax Act - Section 80.4 - Subsection 80.4(2) | extra-territorial application of s. 80.4(2) | 134 |

IT-494 "Hire of Ships and Aircraft from Non-Residents"

Where rent for the use of a ship is paid in advance, so that the actual time spent in Canada has not yet been established, it is acceptable to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(d) | 0 | |

| Tax Topics - Income Tax Act - Section 227 - Subsection 227(8) | 54 | |

| Tax Topics - Income Tax Act - Section 255 | 23 |

IC 77-16R3 "Non-Resident Income Tax"

IC 76-12R4

"The payor can accept the name and address of the payee as being that of the beneficial owner unless there is reasonable cause to suspect...

Forms

NR7-R "Application for Refund of Part XIII Tax Withheld"

Subsection 215(2) - Idem [Exception - corporate immigration]

See Also

Havlik Enterprises Ltd. v. MNR, 89 DTC 159, [1989] 1 CTC 2262 (TCC)

Rip, J. stated, obiter, that "the words 'or otherwise' in subsection 215(2) provide that an agent or other person who pays or credits an amount on...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(b) | 100 | |

| Tax Topics - Income Tax Act - Section 215 - Subsection 215(6) | 113 |

Administrative Policy

19 March 2002 External T.I. 2002-0120785 F - Allocation de retraite - 212(13)(d)

An individual worked for 10 years in Canada for a Canadian corporation, then ceased to be resident and worked the next 12 years for a sister U.S....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(j.1) | s. 212(1)(j.1) applicable to the extent that the retiring allowance paid by the US employer to the non-resident retired employee is invoiced to the predecessor affiliated employer in Canada | 187 |

IC-12R4 "Applicable Rate of Part XIII Tax on Amounts Paid or Credited to Persons in Treaty Countries" under "Beneficial Ownership"

Discussion of circumstances in which the payor can accept the name and address of the payee as being that of the beneficial owner.

Subsection 215(3) - Idem [Exception - corporate immigration]

Cases

Chilcott v. The Queen, 78 DTC 6111, [1978] CTC 152 (FCTD)

S.215(3) applied to a lawyer ("Chilcott") who placed funds of a non-resident client in the name of "W.D. Chilcott, in trust" and who was treated...

See Also

Curragh Inc. v. The Queen, 94 DTC 1894, [1995] 1 CTC 2163 (TCC)

There was no written assignment or other convincing evidence that a loan that an Australian corporation ("Giant") had made to the taxpayer had...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 215 - Subsection 215(1) | agent's s. 215(3) liability does not relieve taxpayer's s. 215(1) liability | 151 |

| Tax Topics - Income Tax Act - Section 216 - Subsection 216(4) | s. 216 does not relieve payor of liability | 109 |

Administrative Policy

13 April 2005 Internal T.I. 2004-0109071I7 F - Partie XIII et revenus locatifs

A property manager agreed with the owners of condos, including the non-resident owner in question, to rent out the condo on behalf of the owner,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 216 - Subsection 216(4) | services provided by property manager to tenant were sufficiently limited to permit making the s. 216(4) election | 202 |

Subsection 215(6) - Liability for tax

Cases

Canada v. Hutchison Whampoa Luxembourg Holdings S.À R.L., 2025 FCA 176, aff'g sub nom. Husky Energy Inc. v. The King, 2023 TCC 167

Regarding the CRA decisions to not only assess the dividend payer under s. 215(6) but also make “protective assessments” of the dividend...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 10 | a securities loan between residents of two Treaty countries did not change the beneficial ownership of the transferred shares | 345 |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(2) | Tax Court finding that the recipient of a dividend for s. 212(2) purposes was other than the dividend’s beneficial owner was potentially troubling | 222 |

| Tax Topics - General Concepts - Substance | agreements styled as securities lending agreements were not such in their legal substance | 202 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(1) | CRA assessments of dividend payer under s. 215(6) and “protective assessments” of dividend recipients under s. 212(2) were “troubling” in light of Galway principle | 239 |

Cardinal Meat Specialists Ltd. v. Devereux, 92 DTC 6357 (Ont CA)

The respondent, which failed to withhold income tax on a payment to the appellant, was entitled under s. 215(6) to recover from the respondent the...

See Also

3792391 Canada Inc. v. The King, 2023 TCC 37 (Informal Procedure)

The taxpayer was assessed under s. 215(6) for failure to withhold and remit Part XIII tax on rents paid by it in its 2011 to 2016 taxation years...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 227 - Subsection 227(8) | taxpayer failed to establish a due diligence defence | 281 |

Solomon v. The Queen, 2007 DTC 1715, 2007 TCC 654 (Informal Procedure)

After noting that the University of Waterloo and Human Resources and Development Canada had failed to withhold Part XIII tax on pension income and...

Havlik Enterprises Ltd. v. MNR, 89 DTC 159, [1989] 1 CTC 2262 (TCC)

Sales contracts which the Canadian taxpayer ("Havlik") entered into with a Chinese supplier required Havlik to obtain irrevocable letters of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(b) | 100 | |

| Tax Topics - Income Tax Act - Section 215 - Subsection 215(2) | meaning of "or otherwise" | 67 |

Administrative Policy

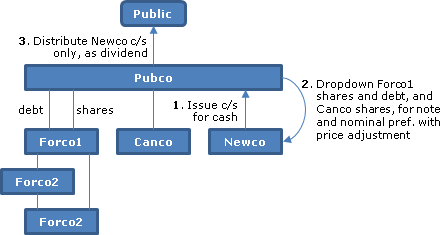

2013 Ruling 2013-0488291R3 - Reorganization of Corporations - Rollover

{kind=link}

Background

Pubco (a Canadian public company) wishes to spin-off Canco and Forco1 (a foreign affiliate) to its shareholders without incurring the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | no ruling on price adjustment clause | 157 |

| Tax Topics - Income Tax Act - Section 52 - Subsection 52(2) | taxable dividend spin-off of thinly capitalized sub | 299 |

16 November 2011 External T.I. 2011-0419191E5 - Foreign Intermediaries & Canadian Owners

Where a foreign financial intermediary ("FFI") has represented to a Canadian financial institution ("CFI") that the beneficial owners of...