Subsection 52(1) - Cost of certain property the value of which included in income

Administrative Policy

22 December 2021 External T.I. 2021-0914081E5 - RPP in-kind distribution

Where surplus from an individual pension plan trust (IPP) is distributed as an in-kind distribution to the sole member, what is the cost to the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 149 - Subsection 149(1) - Paragraph 149(1)(o) | taxable capital gain from distribution-in-kind of RPP property was exempted | 99 |

21 June 2021 External T.I. 2019-0815871E5 F - 83(2)b) and cost

S. 52(1) does not deem a promissory note issued to a shareholder in payment of a capital dividend to have a cost equaling the dividend amount (as...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Adjusted Cost Base | promissory note issued in satisfaction of a capital dividend has full cost | 135 |

14 November 2007 Internal T.I. 2007-0254601I7 F - Paiement incitatif - Bon de souscription

After finding that the value of a share purchase warrant granted to an asset vendor by the parent of the purchaser, as an inducement to enter into...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(x) - Subparagraph 12(1)(x)(iii) | value of share purchase warrant granted to asset vendor as an inducement to agree to a longer term services agreement with purchaser was includible under s. 12(1)(x) | 157 |

11 March 2014 Internal T.I. 2013-0513221I7 F - Stock options

Publico determined to grant stock options to its directors and consultants, as a result of which a private corporation ("Corporation"), that had...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | double income inclusion under s. 56(2) or (4) to consulting corporation, and under s. 15(1) to its shareholder, where consultant's options issued directly by client to shareholder | 113 |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | s. 56(2) benefit where corporation implicitly consented to consultant's options being issued by client directly to its shareholder | 170 |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(4) | implicit transfer by corporation when stock options earned by it were issued directly by its client to its shareholder | 175 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | s. 248(28) does not prevent a double income inclusion to corporation under s. 56 and shareholder under s. 15 | 226 |

| Tax Topics - Income Tax Act - Section 9 - Timing | no s. 9(1) income inclusion from consultant being granted stock options until exercise | 226 |

| Tax Topics - General Concepts - Fair Market Value - Options | stock options with no in-the-money value could have nil FMV | 134 |

6 August 2013 External T.I. 2012-0469481E5 F - Benefit under trust

An estate sold personal-use real estate to one of its beneficiaries for a price less than the property's fair market value, so that s. 69(1)(b)(i)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 105 - Subsection 105(1) | taxable benefit on sale to beneficiary at undervalue was not eliminated under s. 105(1)(a) when beneficiary sold the property | 132 |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(b) | taxable benefit added to acb | 133 |

17 December 2003 Internal T.I. 2003-0047367 F - Benefit Conferred on Non-arm's Length Person

Opco sold the property of its former business to one of its shareholders at an undervalue, without any change to Opco’s share capital. The...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | s. 84(2) inapplicable on sale by defunct corporation of its assets at an undervalue to one of its shareholders | 195 |

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) | s. 246(1) applicable to sale of assets by corporation to employee-shareholder at an undervalue | 189 |

30 June 2003 External T.I. 2003-0182875 F - TRANSFERT DE POLICE D'ASSURANCE

CCRA indicated that where a permanent life insurance policy was distributed gratuitously by a private corporation to a shareholder, who was deemed...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | benefit where permanent life or critical illness policy transferred gratuitously to shareholder as new policyholder | 230 |

| Tax Topics - Income Tax Act - Section 148 - Subsection 148(9) - Adjusted Cost Basis | ACB bump on policy distribution to shareholder equal to s. 15 benefit excess over CSV | 206 |

3 January 2003 External T.I. 2002-0143965 - Shareholder Benefit on First Share Issue

When an amount was included in the income of an initial subscriber for a share of a corporation on the basis that the nominal subscription price...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | 94 |

18 May 2001 External T.I. 2000-0040405 F - Revenu protégé - options

Where an amount was included in a shareholder’s income under s. 15(1) on the grant to it of options to acquire the corporation’s shares, the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(c) | ACB increase to options as a result of s. 52(1) reduced the safe income otherwise allocable to the shares acquired on the options’ exercise | 148 |

24 June 1999 External T.I. 9830665 F - DIVIDENDE EN ACTIONS PRIV ET PAR BILLET

A corporation (Opco) paid a $100,000 dividend in kind that was not covered by safe income to its parent Holdco, so that s. 55(2) applied to deem...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | double taxation of s. 55(2) gain on dividend in kind avoided by excluding gain on subsequent sale of the dividended property | 243 |

| Tax Topics - Income Tax Act - Section 52 - Subsection 52(3) - Paragraph 52(3)(a.1) | nil cost of preferred shares issued on dividend in kind by virtue of s. 52(3)(a.1) since deemed not to be a dividend by s. 55(2) | 149 |

Income Tax Technical News, No. 11, September 30, 1997, "U.S. Spin-Offs (Divestitures) - Dividends in Kind"

The cost of shares received as a dividend-in-kind will be equal to the amount of dividend included in the shareholder's income.

18 March 1993 Memorandum (Tax Window, No. 32, p. 7, ¶2599)

Where bond coupons are sold for an amount that is different from the discounted amount calculated pursuant to Regulations 7000(2)(b), a capital...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 7000 - Subsection 7000(2) - Paragraph 7000(2)(b) | 19 |

October 1992 Central Region Rulings Directorate Tax Seminar, Q. N (May 1993 Access Letter, p. 233)

The amount included in income under s. 12(9) in respect of a prescribed debt obligation is added in computing the cost to the investor of that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 7000 - Subsection 7000(1) - Paragraph 7000(1)(b) | 13 |

13 June 1991 T.I. (Tax Window, No. 4, p. 14, ¶1306)

Amounts included in income each year in respect of a prescribed debt obligation will be added in computing the adjusted cost base of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 7000 - Subsection 7000(1) - Paragraph 7000(1)(b) | 40 |

Subsection 52(2) - Cost of property received as dividend in kind

Administrative Policy

21 November 2003 External T.I. 2003-0023925 F - Distribution non-admissible au sens de 86.1

A reorganization with a distribution entailed the shareholders of a Mexican company listed on an exchange (“Mexco”) being issued shares in of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 86.1 - Subsection 86.1(2) - Paragraph 86.1(2)(b) | distribution did not qualify because distributed shares were not pre-owned by Mexican distributor | 88 |

27 November 2018 CTF Roundtable Q. 2, 2018-0780071C6 - Impact of 55(2) deeming rules

CRA indicated that where a dividend in kind paid by a corporation is subject to s. 55(2), the dividend recipient will be considered to have...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 52 - Subsection 52(3) | cost under s. 52(3) for stock dividend amount to which s. 55(2) applied | 69 |

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(1) - Paragraph 53(1)(b) - Subparagraph 53(1)(b)(ii) | no basis reduction for s. 84(1) dividend to which s. 55(2) applied | 161 |

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Capital Dividend Account - Paragraph (a) - Subparagraph (a)(i) | 53(1)(b)(ii) and 52(3)(a) exclusion limited to where 55(2) did not apply to the stock dividend or PUC increase | 70 |

| Tax Topics - Income Tax Act - Section 112 - Subsection 112(3) - Paragraph 112(3)(b) - Subparagraph 112(3)(b)(i) | stop-loss rule does not apply to the extent of the application of s. 55(2) | 92 |

7 June 2017 External T.I. 2016-0671731E5 F - Transfer of life insurance policy by dividend in kind

A corporation (“Holdco”) holds a policy on the life of its sole shareholder with an adjusted cost basis (“ACB”), cash surrender value...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 148 - Subsection 148(7) - Paragraph 148(7)(a) | dividend-in-kind of a life insurance policy avoids the policy’s disposition at FMV | 240 |

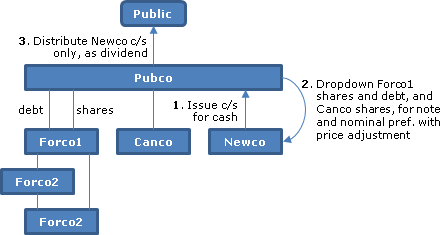

2013 Ruling 2013-0488291R3 - Reorganization of Corporations - Rollover

{kind=link}

Background

Pubco (a Canadian public company) wishes to spin-off Canco and Forco1 (a foreign affiliate) to its shareholders without incurring the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | no ruling on price adjustment clause | 157 |

| Tax Topics - Income Tax Act - Section 215 - Subsection 215(6) | Spinco taking responsibility for Part XIII remittance obligation of Parent | 246 |

Articles

Patrick W. Marley, Kim Brown, "Foreign Mergers and 'Demergers' Under Recent Canadian Proposals", Tax Management International Journal, 10 February 2012, Vol 41, No. 2, p. 86

Ademerger, which under the foreign corporate law, might be viewed as one stream splitting into two, might not qualify under draft s. 90(2) as a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | 46 | |

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(2) | 46 |

Subsection 52(3)

Administrative Policy

27 November 2018 CTF Roundtable Q. 2, 2018-0780071C6 - Impact of 55(2) deeming rules

CRA indicated that since Finance’s intent is to give cost to the portion of the stock dividend that is supported by safe income, and also to a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 52 - Subsection 52(2) | property dividended has cost equal to FMV where subject to s. 55(2) | 104 |

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(1) - Paragraph 53(1)(b) - Subparagraph 53(1)(b)(ii) | no basis reduction for s. 84(1) dividend to which s. 55(2) applied | 161 |

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Capital Dividend Account - Paragraph (a) - Subparagraph (a)(i) | 53(1)(b)(ii) and 52(3)(a) exclusion limited to where 55(2) did not apply to the stock dividend or PUC increase | 70 |

| Tax Topics - Income Tax Act - Section 112 - Subsection 112(3) - Paragraph 112(3)(b) - Subparagraph 112(3)(b)(i) | stop-loss rule does not apply to the extent of the application of s. 55(2) | 92 |

Paragraph 52(3)(a)

Administrative Policy

5 October 2018 APFF Roundtable Q. 4, 2018-0768891C6 F - Stock Dividend and Safe Income

The 100 common shares of Opco, having an aggregate FMV of $1,000,000 and an aggregate PUC and aggregate ACB to their holders, of $100, are held as...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.3) | shift in safe income to high-low prefs paid as stock dividend | 688 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.3) | different effect of stock dividend of high-low preferred shares paid to Holdco and trust shareholders |

Subparagraph 52(3)(a)(ii)

Administrative Policy

S3-F2-C1 - Capital Dividends

1.30.1 Where a dividend that is deductible under subsection 112(1) results from the receipt of a stock dividend, subclause 52(3)(a)(ii)(A)(II)...

12 December 2016 External T.I. 2016-0668341E5 F - Stock dividend

Opco pays a stock dividend on its common shares (having a nominal paid-up capital and adjusted cost base) held by Holdco. The stock dividend is...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.3) - Paragraph 55(2.3)(b) | safe income strip using a preferred share stock dividend | 288 |

Articles

Rick McLean, Jeff Oldewening, Jonas Lau, "Capital Gains Stripping and Surplus Stripping", 2017 Annual CTF Conference draft paper

Two main competing interpretations of the “amount” of a stock dividend for purposes of s. 52(3)(a)(ii)(A) (pp. 13-15)

To apply the ACB...

Paragraph 52(3)(a.1)

Administrative Policy

24 June 1999 External T.I. 9830665 F - DIVIDENDE EN ACTIONS PRIV ET PAR BILLET

A corporation (Opco) paid a $100,000 dividend in kind that was not covered by safe income to its parent Holdco, so that s. 55(2) applied to deem...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | double taxation of s. 55(2) gain on dividend in kind avoided by excluding gain on subsequent sale of the dividended property | 243 |

| Tax Topics - Income Tax Act - Section 52 - Subsection 52(1) | cost of note increased only by the taxable capital gain recognized under s. 55(2) in respect of its issuance as a dividend in kind | 153 |

Subsection 52(4) - Cost of property acquired as prize

Cases

The Queen v. Rumack, 92 DTC 6142, [1992] 1 CTC 57 (FCA)

It was found that no inference could be drawn from s. 52(4) that a monthly annuity won by the taxpayer in a lottery was exempt from income tax.

Administrative Policy

84 C.R. - Q. 21

A prize of $1,000 per month has a cost equal to fair market value at the time of obtaining the right to the prize. Thereafter, ss.56(1)(d), 60(a)...

Subsection 52(6)

Administrative Policy

4 February 1992 External T.I. 7-901929 - Tax Window, No. 16, p. 5, ¶1728

Where at the time a taxpayer acquires a unit in a unit trust the value of the unit includes income payable by the trust at year-end and realized...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107 - Subsection 107(2.1) | 26 |

IT-390 "Unit Trusts - Cost of Rights and Adjustments to Cost Base"

Avoidance of double taxation on distribution of non-taxable portion of capital gain

2. Subsection 52(6) ensures that the non-taxable capital gains...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(2) - Paragraph 40(2)(g) - Subparagraph 40(2)(g)(ii) | 35 |

Articles

Botz, "Mutual Fund Trusts and Unit Trusts: Selected Tax and Legal Issues", 1994 Canadian Tax Journal, Vol. 42, No. 4, p. 1037.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(7.1) | 0 | |

| Tax Topics - Income Tax Act - Section 108 - Subsection 108(2) - Paragraph 108(2)(a) | 0 |