Subsection 56.4(1) - Definitions

Eligible Corporation

Administrative Policy

Michael Coburn, "Practical Strategies for Dealing with the Restrictive Covenant Provisions," 2014 Conference Report, (Canadian Tax Foundation), 8:1-29

Residency requirement (p.8:15)

[I]f a Canadian-resident shareholder of Foreignco provides a non-competition covenant in conjunction with the sale...

Eligible Interest

Administrative Policy

11 October 2013 APFF Roundtable, 2013-0495691C6 F - Clause restrictive

Mr. X sells all the shares of Holdco, which holds all the shares of Opco 1 and Opco 2, to Buyco, which is at arm's length. He grants a non-compete...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56.4 - Subsection 56.4(3) - Paragraph 56.4(3)(c) | non-solicitation clause/divergence of covenanter and seller | 394 |

| Tax Topics - Income Tax Act - Section 56.4 - Subsection 56.4(7) - Paragraph 56.4(7)(b) | non-solicitation clause could be treated as part of a non-compete | 167 |

| Tax Topics - Income Tax Act - Section 56.4 - Subsection 56.4(7) - Paragraph 56.4(7)(f) | maintenance of Holdco fmv/divergence of seller and covenanter | 255 |

Articles

Mark Woltersdorf, "Restrictive Covenants – The Final Chapter (For Now) – Part I", CCH Tax Topics, No. 2132, 17 January 2013, p. 1 at p. 3

It is uncertain why the above definition [of eligible interest] excludes shares of a corporation where, for example, that corporation owns all of...

Restrictive Covenant

Cases

Pangaea One Acquisition Holdings XII S.A.R.L. v. Canada, 2020 FCA 21

The taxpayer (“Pangaea”) was a Luxemburg s.à.r.l. that was one of the shareholders of a Canadian corporation (“Public Mobile”). The...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(i) | an agreement with another shareholder to enter into a share sale with a 3rd party was a restrictive covenant | 213 |

See Also

Pangaea One Acquisition Holdings XII S.À.R.L. v. The Queen, 2018 TCC 158, aff'd 2020 FCA 21

The appellant (“Pangaea”) was a Luxemburg s.à.r.l. that was one of the shareholders of a Canadian corporation (“Public Mobile”). The...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(i) | lump sum paid for non-resident's concurrence in share sale was for restrictive covenant | 187 |

Administrative Policy

16 August 2017 Internal T.I. 2017-0701291I7 - Exclusive Distributorship Rights

In consideration for a lump sum, a non-resident in a Treaty country (NRco) granted an arm’s length Canadian company (Canco) the exclusive right...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(d) - Subparagraph 212(1)(d)(i) | Farmparts likely excluded application to product distributorship right/product name on product not a valuable use of trademark | 507 |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(d) | lump sum non-contingent payment for distributorship right was not a royalty | 120 |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(i) | a lump sum paid to a non-resident for granting an exclusive right to distribute its product in Canada was subject to s. 212(1)(i) withholding | 216 |

| Tax Topics - Treaties - Income Tax Conventions - Article 12 | lump sum paid for distributorship rights was not a royalty | 243 |

20 November 2014 Internal T.I. 2014-0539631I7 - Restrictive Covenants-Part XIII (Luxembourg)

After CanCo had sold shares of a partly-owned subsidiary (SubCo), it made a payment to the other share vendor (LuxCo) pursuant to what was assumed...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 22 | restrictive covenant payment not eligible for relief under Lux Treaty | 266 |

| Tax Topics - Treaties - Income Tax Conventions - Article 7 | restrictive covenant payment not eligible for relief under Lux Treaty | 148 |

12 July 2011 Internal T.I. 2010-0366321I7 - Tax treatment of break fees received

A break fee received by the taxpayer would be included in its income under s. 56.4(2) if it were not already included in income under s. 9(1) or...

Articles

Sze Yee Ling, Nathan Wright, "Restrictive Covenants: Some Reminders", Canadian Tax Focus, Vol. 7, No. 1, February 2017, p. 7

Two examples of what arguably are restrictive covenants (p. 7)

[T]ypical commercial transactions may unknowingly trigger the restrictive covenant...

Michael Coburn, "Practical Strategies for Dealing with the Restrictive Covenant Provisions", 2014 Conference Report (Canadian Tax Foundation), 8:1-29

Examples of scope (p. 7)

Examples of agreements, undertakings or waivers that appear to be caught by the definition of restrictive covenant...

Subsection 56.4(2) - Income — restrictive covenants

Administrative Policy

16 February 2016 External T.I. 2015-0618601E5 - Earned or Unearned Revenue

The taxpayer received a lump-sum payment (the “Payment”) from a major supplier (“ACo”) in consideration for entering into a supplier...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(x) | lump sum received on signing 15-year supplier loyalty agreement was immediately recognized inducement | 200 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(m) | no deferral for amount included under s. 56.4(2) or 12(1)(x) | 126 |

8 October 2010 Roundtable, 2010-0373351C6 F - Évaluation d'une clause restrictive

In the context of a sale of 100% of the shares of a private corporation by an executive shareholder to an arm's length purchaser, can the CRA...

Articles

Michael Coburn, "Practical Strategies for Dealing with the Restrictive Covenant Provisions", 2014 Conference Report (Canadian Tax Foundation), 8:1-29

Enforceability of restrictive covenant if no allocation of consideration (pp. 4-5)

[T]here may be a perception that to ensure the legal...

Julie A. Colden, "Restrictive Covenant Update", Canadian Current Tax, Vol. 15, No. 11, August 2005, p. 97.

Nathan Boidman, Michael Kandev, "Controversies in Canada Respecting the Taxation of Non-Competition and Related Payments", Bulletin for International Fiscal Documentation, Vol. 58, No. 10, October 2004, p. 494.

Subsection 56.4(3) - Non-application of subsection (2)

Paragraph 56.4(3)(b)

Articles

Michael Coburn, "Practical Strategies for Dealing with the Restrictive Covenant Provisions", 2014 Conference Report (Canadian Tax Foundation), 8:1-29

S. 56.4(3) as a counter to s. 68(c) (pp.21-22)

[S]ubsection 56.4(3) contains provisions that effectively allow an amount received as consideration...

Paragraph 56.4(3)(c)

Administrative Policy

22 August 2017 Internal T.I. 2017-0688301I7 - Restrictive Covenant

When presented with an agreement for the sale of the shares of a private company under which various shareholders were required to agree to a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56.4 - Subsection 56.4(7) - Paragraph 56.4(7)(b) | non-solicitation covenant included in non-compete | 191 |

11 October 2013 APFF Roundtable, 2013-0495691C6 F - Clause restrictive

Mr. X sells all the shares of Holdco, which holds all the shares of Opco 1 and Opco 2, to Buyco, which is at arm's length. He grants a non-compete...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56.4 - Subsection 56.4(1) - Eligible Interest | must be one, rather than more than one, underlying corp | 92 |

| Tax Topics - Income Tax Act - Section 56.4 - Subsection 56.4(7) - Paragraph 56.4(7)(b) | non-solicitation clause could be treated as part of a non-compete | 167 |

| Tax Topics - Income Tax Act - Section 56.4 - Subsection 56.4(7) - Paragraph 56.4(7)(f) | maintenance of Holdco fmv/divergence of seller and covenanter | 255 |

Subparagraph 56.4(3)(c)(vi)

Administrative Policy

7 April 2005 External T.I. 2004-0103551E5 F - Choix - Engagement de non-concurrence

How should the election be made in the absence of a prescribed form? CRA responded that both the vendor and the purchaser should submit and sign...

Subsection 56.4(6) - Application of subsection (5) — if employee provides covenant

Articles

Kenneth Keung, Riaz S. Mohamed, "Restrictive Covenants for Departing Executives", Taxation of Executive Compensation and Retirement (Federated Press), Vol. 23 No. 4, November 2012, p. 1604.

Receipt of non-compete otherwise than as s. 6(3) income (pp. 1605-6)

The second scenario reviews a situation where a departing employee is also a...

Mark Woltersdorf, "Restrictive Covenants – The Final Chapter (For Now) – Part II", CCH Tax Topics, No. 2135, 7 February 2013, p. 1 at p. 4:

Paragraphs 56.4(6)(e) (arm's length employee exception) and 56.4(7)(d) ("goodwill amount" and "disposition of property" exceptions) provide that...

Paragraph 56.4(6)(e)

Administrative Policy

2 December 2014 CTF Roundtable Q. 3, 2014-0547251C6 - Q.3 - Restrictive Covenants

Would CRA reconsider 2014-0522961C6, so that the allocation in an agreement of $1 of consideration to a restrictive covenant does not constitute...

16 June 2014 STEP Roundtable, 2014-0522961C6 - STEP CRA Roundtable - June 2014

Does the fact that a contract of a restrictive covenant stipulates the amount of $1 as consideration mean that there is consideration, such that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56.4 - Subsection 56.4(7) - Paragraph 56.4(7)(d) | nominal consideration tainting of non-compete | 163 |

Subsection 56.4(7) - Application of subsection (5) — realization of goodwill amount and disposition of property

Paragraph 56.4(7)(b)

Administrative Policy

22 August 2017 Internal T.I. 2017-0688301I7 - Restrictive Covenant

Pursuant to an agreement for the sale of the shares of a private company (the SPA”), various shareholders were required to agree to a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56.4 - Subsection 56.4(3) - Paragraph 56.4(3)(c) | agreement not to solicit employees not assimilated | 224 |

11 October 2013 APFF Roundtable, 2013-0495691C6 F - Clause restrictive

Mr. X sells all the shares of Holdco, which holds all the shares of Opco 1 and Opco 2, to Buyco, which is at arm's length. He grants a non-compete...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56.4 - Subsection 56.4(1) - Eligible Interest | must be one, rather than more than one, underlying corp | 92 |

| Tax Topics - Income Tax Act - Section 56.4 - Subsection 56.4(3) - Paragraph 56.4(3)(c) | non-solicitation clause/divergence of covenanter and seller | 394 |

| Tax Topics - Income Tax Act - Section 56.4 - Subsection 56.4(7) - Paragraph 56.4(7)(f) | maintenance of Holdco fmv/divergence of seller and covenanter | 255 |

Articles

Michael Coburn, "Practical Strategies for Dealing with the Restrictive Covenant Provisions", 2014 Conference Report (Canadian Tax Foundation), 8:1-29

Narrowness of non-compete description in ss. 56.4(3)(c)(ii, 56.4(6)(d), 56.4(7)(b) and 56.4(7)(c) (p. 7)

[I]f a covenant falls within the...

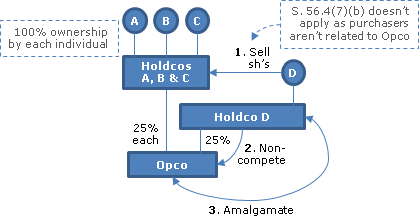

Manu Kakkar, "Paragraph 56.4(7)(b ) Related-Person Problem and Arm's Length Minority Acquisitions", Tax For The Owner-Manager, Volume 14, Number 2, April 2014, p. 8.

{kind=link}

Manu Kakkar, "Section 56.4 Restricted Covenant Trap", Tax for the Owner-Manager, Volume 13, Number 4, October 2013, p. 4:

Assumed facts (Holdco sale transaction) (p. 4)

Assume that Mr. A and Mr. B deal with each other at arm's length. Mr. A and Mr. B are each 100...

Paragraph 56.4(7)(g)

Administrative Policy

2 November 2023 APFF Roundtable Q. 14, 2023-0982951C6 F - Article 56.4 L.I.R. - Clauses restrictives

The CRA webpage entitled "Restrictive Covenant Election" indicates that, since no prescribed form has been published, the transferor and...

Paragraph 56.4(7)(d)

Administrative Policy

16 June 2014 STEP Roundtable, 2014-0522961C6 - STEP CRA Roundtable - June 2014

Does the fact that a contract of a restrictive covenant stipulates the amount of $1 as consideration mean that there is consideration, such that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56.4 - Subsection 56.4(6) - Paragraph 56.4(6)(e) | nominal consideration tainting of non-compete - partly reversed immediately above | 163 |

Articles

Michael Coburn, "Practical Strategies for Dealing with the Restrictive Covenant Provisions", 2014 Conference Report (Canadian Tax Foundation), 8:1-29

Requirement of nil proceeds for covenant: tracing issue (p.14)

[A] grantor of a Non-Competition Covenant could acknowledge that the consideration...

Paragraph 56.4(7)(e)

Articles

Michael Coburn, "Practical Strategies for Dealing with the Restrictive Covenant Provisions", 2014 Conference Report (Canadian Tax Foundation), 8:1-29

Exclusion of hybrid sales and safe income strips (p.15)

[A]ll share repurchases or redemptions, including ones that do not result in an actual...

Paragraph 56.4(7)(f)

Administrative Policy

11 October 2013 APFF Roundtable, 2013-0495691C6 F - Clause restrictive

Mr. X sells all the shares of Holdco, which holds all the shares of Opco 1 and Opco 2, to Buyco, which is at arm's length. He grants a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56.4 - Subsection 56.4(1) - Eligible Interest | must be one, rather than more than one, underlying corp | 92 |

| Tax Topics - Income Tax Act - Section 56.4 - Subsection 56.4(3) - Paragraph 56.4(3)(c) | non-solicitation clause/divergence of covenanter and seller | 394 |

| Tax Topics - Income Tax Act - Section 56.4 - Subsection 56.4(7) - Paragraph 56.4(7)(b) | non-solicitation clause could be treated as part of a non-compete | 167 |

Subsection 56.4(12) - Clarification if subsection (5) applies

Articles

Mark Woltersdorf, "Restrictive Covenants – The Final Chapter (For Now) – Part II", CCH Tax Topics, No. 2135, 7 February 2013, p. 1 at pp. 3-4:

Discussions with the Department of Finance indicate that the intent of paragraph 56.4(12)(b) is to prevent a taxpayer from arguing that an amount...