Subsection 246(1) - Benefit conferred on a person

Cases

Gestion M.-A. Roy Inc. v. Canada, 2024 FCA 16

Various whole life policies on the life of a resident individual (Mr. Roy) were owned by (i) a holding company (“Gestion Roy”), controlled by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | s. 15(1) benefit where subsidiary pays premiums on whole life policies owned by the taxpayer | 291 |

Laliberté v. Canada, 2020 FCA 97

The founder and controlling shareholder of Cirque du Soleil, had been found by the Tax Court to have received a taxable benefit under s. 15(1) (or...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | any subjective intention of the controlling shareholder not to be enriched did not establish that no taxable benefit | 427 |

| Tax Topics - General Concepts - Onus | Tax Court could determine a taxable benefit percentage (different from that assumed by the Minister) based on all the evidence | 304 |

Consultants Pub Création Inc. v. Canada, 2008 DTC 6610, 2008 FCA 60, aff'g Massicotte v. The Queen, 2006 TCC 618

The taxpayer wholly owned a corporation ("Amadéus") which, in turn, wholly owned another corporation ("Pub Création"), and the taxpayer was also...

The Queen v. Kieboom, 92 DTC 6382, [1992] 2 CTC 59 (FCA)

S.245(2)(c) applied where the taxpayer permitted his wife and, later, his children, to subscribe for non-voting common shares of his private...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 74.1 - Subsection 74.1(1) | 105 | |

| Tax Topics - Statutory Interpretation - Interpretation Bulletins, etc. | 73 |

Sweeney v. The Queen, 90 DTC 6507, [1990] 2 CTC 342 (FCTD)

In 1950, a written agreement between the taxpayer's father and the taxpayer provided that the son could purchase his father's shares in a company...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Other | 170 |

Boardman v. The Queen, 85 DTC 5628, [1986] 1 CTC 103 (FCTD)

Since the taxpayer's legal obligations to his divorced wife were met by a court order which ordered the Registrar of Land Titles to transfer title...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | 148 | |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(4) | 34 |

Mansfield v. The Queen, 83 DTC 5136, [1983] CTC 97 (FCTD), aff'd 84 DTC 6535, [1984] CTC 547 (FCA)

A company netted no cash from the sale of a $5,000 convertible debenture to its employee because it deposited with a bank an amount equal to the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(1) - Paragraph 7(1)(a) | 201 |

The Queen v. Immobiliare Canada Ltd., 77 DTC 5332, [1977] CTC 481 (FCTD)

By purchasing debentures of a sister Canadian resident corporation from its non-resident parent the taxpayer eliminated withholding taxes that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) | sale of bond with accrued interest did not satisfy interest | 178 |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(b) | sale proceeds allocable to expectancy of interest were not interest receipt | 198 |

| Tax Topics - Income Tax Act - Section 76 | 105 |

The Queen v. Esskay Farms Ltd., 76 DTC 6010, [1976] CTC 24 (FCTD)

The taxpayer, wished to sell land to the City of Calgary in consideration for two annual instalments in order to defer a portion of the gain to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Agency | weight given to written agreement terms in finding that intermediary purchased as principal | 122 |

| Tax Topics - General Concepts - Evidence | 81 | |

| Tax Topics - General Concepts - Sham | no sham if documents describe intended legal rights | 354 |

| Tax Topics - General Concepts - Tax Avoidance | no sham if documents describe intended legal rights | 354 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(2) | 143 | |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(n) | 199 | |

| Tax Topics - Income Tax Act - Section 245 - Old | 57 | |

| Tax Topics - Statutory Interpretation - Provincial Law | 58 |

David v. The Queen, 75 DTC 5136, [1975] CTC 197 (FCTD)

As a result of transactions wherein the shares of a company held by the taxpayers were purchased on behalf of a pension plan which then caused the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Evidence | 30 | |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | proceeds from the sale of cash-rich company to pension fund for wind-up 5 months later were "otherwise appropriated ... on the winding-up" | 321 |

Indalex Ltd. v. The Queen, [1988] 1 CTC 60, 88 DTC 6053 (FCA)

It was found that the taxpayer, by purchasing aluminium from a Bermudan affiliate at a price that was 5% higher than what it would have paid if it...

Laxton v. The Queen, 88 DTC 6008, [1988] 1 CTC 19 (FCTD), rev'd , in part, 89 DTC 5327 (FCA)

In a joint venture agreement it was agreed that an individual member of the joint venture ("Laxton") would be paid an annual management fee equal...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Specific v. General Provisions | 67 |

MNR v. Enjay Chemical Co. Ltd., 71 DTC 5293, [1971] CTC 535 (FCTD)

In finding that a forgiveness of a portion of the trade indebtedness owing by the taxpayer to a U.S. affiliate would have given rise to a taxable...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Adjusted Cost Base | 30 | |

| Tax Topics - Income Tax Act - Section 9 - Forgiveness of Debt | debt forgiveness related to inventory of operations | 186 |

See Also

Bitton v. Agence du revenu du Québec, 2026 QCCQ 312

The taxpayer used a mid-sized corporate jet owned by one of the subsidiaries in the group predominantly in relation to business travel. However,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | taxable benefit from personal use of a corporate jet valued at US$6500 per hour rather than per Communiqué AD-18-01 | 302 |

Bolduc v. Agence du revenu du Québec, 2025 QCCA 1470

limited partnership (“SEC”) sold condo units for less than their fair market value to (i) the daughter and wife of Mr. Migliara, the founder...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(b) | deemed FMV proceeds on sale by partnership of condos at an undervalue to individuals related to partners | 131 |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | s. 56(2) equivalent applied to sale of condo units at undervalue by partnership to relations of the directing mind of the partnership | 129 |

Gestion M.-A. Roy Inc. v. The King, 2022 TCC 144, aff'd 2024 CAF 16

Various whole life policies on the life of a resident individual (Mr. Roy) were owned by (i) a holding company (“Gestion Roy”), controlled by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | a company’s payment of the premiums on whole life policies of which it was the beneficiary but not owner triggered ss. 15(1) and 246(1) benefits | 468 |

Laliberté v. The Queen, 2018 TCC 186, aff'd 2020 FCA 97

The founder and controlling shareholder of Cirque du Soleil was found to have received a taxable benefit under s. 15(1) (or alternatively, under...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | business benefits from sending shareholder into space were secondary | 491 |

Pelletier v. The Queen, 2004 DTC 3176 (TCC)

Although benefits were conferred on the taxpayers by virtue of their being able to acquire shares of a private company worth $300,000 for a...

Husky Oil Ltd. v. The Queen, 95 DTC 316, [1995] 1 CTC 2184 (TCC), aff'd 95 DTC 5244 (FCA)

The taxpayer, which needed to "shelter" a capital gain previously realized by it, purchased from a vendor with which it dealt at arm's length the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Shares | 82 | |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | common interest of the parties did not evince that each was not acting in its own interests | 133 |

Ovis Brooks v. Minister of National Revenue, 91 DTC 639, [1991] 1 CTC 2551 (TCC)

The taxpayer was deemed under former s. 245(2) to have disposed of an "economic interest" in a corporation wholly-owned by him when he caused it...

Administrative Policy

10 October 2024 APFF Financial Strategies and Instruments Roundtable Q. 1, 2024-1023641C6 - Intercompany loans and taxable benefits

Could CRA confirm that an interest-free loan between two corporations (Aco and Bco) owned by different shareholders does not give rise to a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | inter-corporate bona fide non-interest bearing loan does not engage s. 15 | 191 |

7 October 2022 APFF Financial Strategies and Instruments Roundtable Q. 2, 2022-0936281C6 F - police d'assurance-vie & avantage

Suppose that two brothers resident in Canada each have a Holdco owning 50% of Opco and that, in order to fund the buy-sell agreement on the death...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Expense Reimbursement | premiums paid by parent on a sub’s life insurance policies are non-deductible even if reimbursed on income account | 192 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Financing Expenditures | premiums paid by Holdcos on policies of which their jointly-owned company (Opco) is the beneficiary are non-deductible capital expenditures even if reimbursed by the Opcos | 138 |

2017 Ruling 2016-0660321R3 - Reorg of REIT to simplify multi-tier structure

A Canadian REIT (the “Fund”) holds the units and notes of a subsidiary unit trust (“Sub-Trust”), whose principal asset is most of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 132.2 - Subsection 132.2(1) - Qualifying Exchange | use of the s.132.2 merger and a renunciation of most of the units otherwise issuable on the merger in order to eliminate a REIT corporate subsidiary held through an LP and a sub-trust | 1006 |

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(2) - Paragraph 107.4(2)(a) | s. 107.4 transfer of sub-trust’s assets to sister MFT trust | 460 |

| Tax Topics - Income Tax Act - Section 98 - Subsection 98(3) | drop down of LP 1 into LP 2 followed by immediate s. 98(3) wind-up of LP 1 into LP 2 and GP of LP1, followed by immediate taxable sale by GP to LP 2 | 146 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | no disposition of partnership interests or property on conversion of general to limited partnership or adding right of renunciation of a MFT unitholder | 165 |

| Tax Topics - Income Tax Act - Section 132.2 - Subsection 132.2(3) - Paragraph 132.2(3)(g) - Subaragraph 132.2(3)(g)(vi) - Clause 132.2(3)(g)(vi)(C) - Subclause 132.2(3)(g)(vi)(C)(I) | renunciation by subsidiary partnership of transferee MFT of units that otherwise would be issuable on the redemption of its incestuous holding in transferor MFC | 245 |

6 December 2016 External T.I. 2016-0666841E5 F - Sale of property for POD less than FMV

Opco is held somewhat equally by three holding companies, each wholly-owned by an individual (A, B or C) who is unrelated to the others. Opco...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1.4) - Paragraph 15(1.4)(c) | application to Holdco shareholder of Opco where Opco conferrred a benefit on child of Holdco's shareholder | 210 |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | potential application to immediate shareholder re benefit on indirect shareholder | 207 |

14 March 2016 External T.I. 2016-0626781E5 - Neuman Type Situation

The only issued and outstanding share of Opco (which has retained earnings of $500,000) is 1 Class A common share, with a fair market value of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | s. 15(1) might apply where spouse subscribes nominal consideration for Opco shares and receives a large discretionary dividend | 226 |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | s. 56(2) likely non-applicable where spouse subscribes nominal consideration for Opco shares and receives a large discretionary dividend | 262 |

| Tax Topics - Income Tax Act - Section 73 - Subsection 73(1) | spousal rollover for Kieboom disposition of economic interest | 82 |

16 April 2012 External T.I. 2011-0411491E5 - Taxation of distributions of a US LLC

In…2011-0411491E5, CRA commented on an interest in a United States Limited Liability Corporation (LLC) held by an Alberta Unlimited Liability...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | taxable benefit where US taxes on LLC income allocated to indirect Cdn member are paid by LLC or intermediate ULC | 161 |

24 June 2015 External T.I. 2015-0575911E5 F - Benefit to shareholder or conferred on a person

Corporation A, is wholly owned by Holdco, which has equal unrelated Shareholders 1, 2, 3 and 4. Corporation A disposes of a capital property to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1.4) - Paragraph 15(1.4)(c) | benefit only conferred on one shareholder (the husband) if wife of one of four sibling shareholders receives benefit | 333 |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | benefit conferred on spouse of individual shareholder of parent | 253 |

3 March 2015 Internal T.I. 2014-0527841I7 F - Avantage imposable pour aéronef

In a wholly-owned stacked structure of three Corporations (C holding D, holding E), Corporation E acquired an aircraft for business use but with...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 13 - Subsection 13(7) - Paragraph 13(7)(c) | apportionment of aircraft use between business and personal | 74 |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | benefits from personal use of corporate aircraft based on the cost of similar benefit from arm's length supplier | 174 |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1.4) - Paragraph 15(1.4)(c) | s. 15(1.4)(c) applied to extend scope of Massicotte indirect benefit doctrine | 170 |

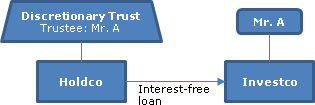

12 December 2012 Internal T.I. 2012-0464411I7 - Indirect Benefit

{kind=link}

A taxable Canadian corporation (Holdco) which is wholly-owned by a trust of which Mr. A is the sole trustee and is a discretionary beneficiary,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 105 - Subsection 105(1) | no benefit under s. 105(1) from interest-free loan | 113 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(e) | fee re distribution borrowing | 159 |

16 April 2012 External T.I. 2011-041149

A Canadian-resident individual owns all the shares of an Alberta unlimited liability company which, in turn, owns a majority of the membership...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Dividend | 157 |

10 January 2011 Internal T.I. 2009-0344251I7 - Application of subsection 246(1)

In a situation where a second-tier subsidiary provides a benefit to the shareholder of a first-tier corporation, s. 246(1) can be applied on its...

8 October 2010 Roundtable, 2010-0371901C6 F - avantage à l'actionnaire, assurance-vie

Question 2 at the May 4, 2010 CALU Roundtable concerned the situation where (A) Holdco holds an insurance policy on the life of its shareholder,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(x) | reimbursement by sub of premiums potentially includible under s. s. 12(1)(x) where it is the beneficiary of life insurance policy held by parent | 258 |

4 May 2010 CALU Roundtable, 2010-0359421C6 - Shareholder's benefit and life insurance

S. 246(1) could apply where a corporation (Parentco) holds a life insurance policy for which it pays the premiums and designates its subsidiary...

4 December 2009 Internal T.I. 2009-0344991I7 F - Paragraphe 246(1) et le jugement Massicotte

Mr. X, who is the sole shareholder of Holdco, which in turn is the sole shareholder of Opco receives, along with four Opco employees receive...

2 December 2008 Internal T.I. 2008-0270981I7 F - Entreprise de prestation de services personnels

Mr. A wholly-owned Holdco, which held a minority interest in Opco. The principal residence of Mr. A and Ms. A (spouses), held by Holdco, is...

25 February 2008 Internal T.I. 2007-0243871I7 F - Avantages imposables

After finding that a corporation’s payment of the personal expenses of an unpaid director gave rise to s. 6(1)(a) inclusions to him, the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(1) - Paragraph 6(1)(a) | unpaid director was a deemed employee, so that payment of his personal expenses was a s. 6(1)(a) benefit | 131 |

14 June 2007 External T.I. 2006-0209341E5 F - Utilisation d'un bien d'une société de personnes

A partnership in whose farming business the partners are actively involved owns the residence of one of the partners, who does not pay rent, but...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 103 - Subsection 103(1) | personal use of property is a factor going to the reasonableness of the profit-sharing arrangements | 74 |

| Tax Topics - Income Tax Act - Section 96 - Subsection 96(2.2) - Paragraph 96(2.2)(d) | personal use of property could engage s. 96(2.2)(d) | 104 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Income-Producing Purpose | partner’s use of partnership property is addressed by denying partnership income deductions and under s. 103, rather than through benefit-conferral provisions | 112 |

20 March 2007 External T.I. 2006-0173711E5 F - Paiement des impôts d'une fiducie

Mr. A is one of the two trustees for an inter vivos trust for his minor children that provides for the distribution of all income to the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 105 - Subsection 105(1) | s. 105(1) does not apply where trustee pays trust taxes | 109 |

| Tax Topics - Income Tax Act - Section 74.1 - Subsection 74.1(2) | attribution may apply where father pays income tax liability of trust for his children | 107 |

17 December 2003 Internal T.I. 2003-0047367 F - Benefit Conferred on Non-arm's Length Person

The four equal common shareholders of Opco were X (a director and vice president), his wife ("Y"), Y's sister and the sister's husband, and X and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | s. 84(2) inapplicable on sale by defunct corporation of its assets at an undervalue to one of its shareholders | 195 |

| Tax Topics - Income Tax Act - Section 52 - Subsection 52(1) | application of s. 15(1) or 246(1) to property distributed by corporation to shareholder would be added to the property’s ACB | 65 |

6 October 2003 External T.I. 2003-0040145 F - TRANSFERT D'UNE POLICE D'ASSURANCE-VIE

A shareholder transferred a universal life insurance policy, that was an exempt policy, on the individual’s life to a wholly-owned corporation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 148 - Subsection 148(7) | loss on transfer of universal life policy to wholly-owned subsidiary not recognized | 92 |

| Tax Topics - Income Tax Act - Section 148 - Subsection 148(9) - Adjusted Cost Basis - Element A | no taxable benefit when life insurance policy transferred to wholly-owned corporation at less than its FMV | 209 |

25 March 1994 External T.I. 9335505 - INTEREST REDUCE 15(1) BENEFIT

"It our general position that the term 'shareholder' as used in subsection 15(1) of the Act would not include a person who indirectly controls a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | 99 |

93 A.P.F.F. Round Table, Q.17

Where a taxpayer transfers assets to an unrelated corporation applying the s. 85(1) rollover, it is not possible to rule out the application of...

24 March 1993 T.I. (Tax Window, No. 38, p. 1, ¶2490)

Re potential application of s. 246(1) to a holder of common shares where his father exchanges preferred shares of the corporation for preferred...

90 C.R. - Q.47

Where a Canadian corporation borrows funds from an arm's length lender and the Canadian corporation's non-resident parent guarantees the loan for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 214 - Subsection 214(15) | 102 |

80 C.R. - Q.55

The listing in IT-453 of conferral-of-benefit situations was not intended to be comprehensive.

IT-239R2 "Deductibility of Capital Losses from Guaranteeing Loans for Inadequate Consideration and from Loaning Funds at less than a Reasonable Rate of Interest in Non-arm's Length Circumstances"

Former s. 245(2) may have been applied in situations where there is a material benefit to other shareholders as a result of a minority shareholder...

Paragraph 246(1)(a)

Administrative Policy

15 May 2019 IFA Roundtable Q. 7, 2019-0798821C6 - Subsection 246(1) and Non-Residents

An indirect benefit would be included in computing a non-resident’s income under s. 15(1) if the amount of the benefit were a payment made...

5 November 2003 Internal T.I. 2003-0043277 F - Benefit-Use of Automobiles

The CEO ("X") of an automobile sales company ("Opco"), and X's spouse held 51% and 49% of the shares of a holding company ("HoldcoX"), which held...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(5) | application of s. 15(5) to shareholder’s use of company automobile | 72 |

| Tax Topics - Income Tax Act - Section 10 - Subsection 10(1) | automobiles in car dealer inventory used for employee’s personal use remained in inventory, cf. if converted primarily to personal use of shareholder (which would not be a disposition) | 314 |

| Tax Topics - Income Tax Act - Section 9 - Computation of Profit | conversion of automobile in car inventory to personal use of CEO would not entail its deemed disposition nor would the conversion of car inventory to personal use of shareholders | 267 |

Paragraph 246(1)(b)

See Also

ExxonMobil Canada Resources Company v. The King, 2026 TCC 42

The US parent of the taxpayer (“EM Corp.”), and two other oil and gas companies (“BP Alaska” and “Phillips Alaska”) entered into an...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Onus | non-suit motions should not be entertained after the close of evidence | 178 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4) - Paragraph 152(4)(b) - Subparagraph 152(4)(b)(iii) | the reassessed feasibility costs of the Cdn taxpayer were incurred by it as a result of an assignment of an interest in the related project agreement to it by its NR parent | 341 |

| Tax Topics - General Concepts - Evidence | in the absence of evidence as to the effect of Alaskan law, lex fori was applied | 89 |

| Tax Topics - Income Tax Act - Section 3 - Paragraph 3(a) | the taxpayer’s costs for a pipeline feasibility study were incurred in relation to a source of income (the pipeline or use of the information generated) | 327 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Incurring of Expense | taxpayer incurred costs as a result of a partial assignment to it of an agreement for conducting a feasibility study | 341 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Income-Producing Purpose | income-producing purpose can be secondary | 247 |

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) - Paragraph 247(2)(b) | taxpayer was assigned a portion of a pipeline feasibility project as a likely Canadian participant in any pipeline, and the alternative fee-for-services model was not well established | 268 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(9) | pleading of Part XIII tax arising from the conferral of a benefit was sufficient to ground a Crown argument that the benefit arose under s. 56(2) | 314 |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | entering into a bona fide transaction with a shareholder does not entail the conferral of a benefit | 94 |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | s. 246(1) cannot satisfy the “benefit” requirement of s. 56(2) so as to engage s. 214(3)(a) | 269 |

| Tax Topics - Income Tax Act - Section 214 - Subsection 214(3) - Paragraph 214(3)(a) | s. 214(3)(a) does not deem a s. 56(2) or 246(1) benefit to be a dividend | 286 |

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) - Paragraph 247(2)(a) | terms of cross-border agreement for the sharing of the costs of a pipeline feasibility study were commercially appropriate | 366 |

Subsection 246(2) - Arm’s length

Cases

Jobin v. The Queen, 78 DTC 6538, [1979] CTC 493 (FCTD)

What is now s. 245(3) did not apply to an arm's length sale of all the shares of a company, an operation which admittedly entailed the stripping...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(2) | 22 |

See Also

Extendicare Health Services Inc. v. MNR, 87 DTC 5404, [1987] 2CTC 179 (FCTD)

"[T]he term 'bona fide', when used as an adjective, is generally taken to mean 'honestly', 'genuinely' or 'in good faith'."

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Redundancy/ reading in words/ speaking in vain | 43 |