Subsection 15(1.1) - Conferring of benefit

Cases

Wong v. R., 99 DTC 458, [1999] 2 CTC 2173 (TCC)

It was accepted that the effect of an arrangement under which family members subscribed for non-voting Class B common shares of a corporation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Purpose/Intention | "it may reasonably be considered" imported an objective test | 208 |

Wu v. R., 98 DTC 6004, [1998] 1 CTC 99 (FCA)

The spouse of the taxpayer held the sole Class A voting common share of a corporation. The corporation had also issued Class B non-voting common...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Purpose/Intention | 75 |

Administrative Policy

2015 Ruling 2015-0604051R3 - Internal Reorganization

The U.S. parent (XXXco1) of a Canadian corporation (Canco1) transferred a portion of its Class A common shares of Canco1 to a U.S. subsidiary...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) - Subparagraph 55(3)(a)(iii) | note resulting from share redemption required to be vapourized on amalgamation/GAAR assessment required to reduce outside Canadian basis that US parents “paid for” by paying 5% Canadian withholding tax/rep re pubco share value being unaffected | 899 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(1.11) | s. 55(3)(a) rulings conditional on U.S. parents accepting GAAR assessments to reduce their outside basis | 230 |

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(2) | extensive reps required re series of transactions | 47 |

10 October 2014 APFF Roundtable Q. 19, 2014-0538041C6 F - 2014 APFF Roundtable, Q. 19 - Stock dividend

Mr. X holds all 100 of Opco's Class A shares with a fair market value of $1,000,000 and nominal ACB and PUC. Opco pays a stock dividend comprising...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(c) | SI apportionment to stock dividend prefs | 251 |

| Tax Topics - Income Tax Act - Section 74.4 - Subsection 74.4(2) | non-application to stock dividend, cf. s. 86 reorg | 255 |

| Tax Topics - Income Tax Regulations - Regulation 6205 - Subsection 6205(2) | purpose test in Reg. 6205(2)(a) is not necessarily accomplished by all estate freezes/"arrangement" broad | 413 |

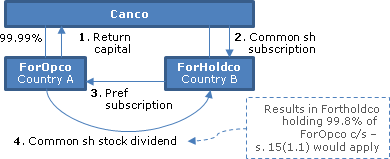

26 November 2013 CTF Roundtable, 2013-0507981C6 - Stock dividend by a foreign corporation 15(1.1)

{kind=link}

Under a proposed ruling request, Canco, which directly owned approximately 99.99% of all the common shares of ForOpco, which was resident in...

1 April 2003 External T.I. 2003-0004125 F - Freeze by Paying a Stock Dividend

A CCPC (Opco) paid a stock dividend of preferred shares with a fair market value of $800,00 and a paid-up capital of $80 to its sole shareholder,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 74.4 - Subsection 74.4(2) | non-application to stock dividend | 108 |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(b) | imputed disposition to which s. 69(1)(b) applied where common shares issued at undervaluation to children’s trust | 131 |

| Tax Topics - General Concepts - Effective Date | price-adjustment clause to redemption value of preferred shares did not accord with IT-169 | 183 |

25 March 1999 External T.I. 9805975 F - 15(1.1) STOCK DIVIDEND AFTER AN ESTATE FREEZE

S. 15(1.1) was inapplicable to a stock dividend issued a few months after a corporate freeze by father given that it was paid to all shareholders...

9 May 1990 Meeting (October 1990 Access Letter, ¶1474)

S.15(1.1) generally does not apply where the stock dividend by itself does not significantly reduce the value of a specified shareholder's...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 22 | |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | 93 |

Subsection 15(1.3)

See Also

Touchette v. The King, 2025 CCI 195

Gagnon J confirmed, as to the majority of the expenses concerned, CRA assessments which denied the deduction by a corporation (“9134”) of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(16) | s. 248(16) did not require the inclusion of ITCs claimed on expenses given that the related GST had been netted against the ITC amount rather than treated as an expense | 237 |

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(x) - Subparagraph 12(1)(x)(vi) | ITCs claimed on denied expenses were not income by virtue of s. 12(1)(x)(vi) since the associated GST had not been treated as an expense | 273 |

Subsection 15(1.2)

Articles

Mark Coleman, Daniel A. Bellefontaine, "Forgiveness, Foreign Affiliates and FAPI: a Framework", Resource Sector Taxation (Federated Press), Vol. X, No. 1, 2015, p.694

Priority of s. 15(1.2) rule (pp. 698-9)

[T]he existence of this rule suggests that a forgiven shareholder loan will typically be considered a...

Subsection 15(1.21)

Administrative Policy

23 March 2004 External T.I. 2003-0049031E5 F - Paragraphe 15(2) de la Loi et "montant remis"

In 2003, Opco made an interest-free loan to the adult child of its sole shareholder in order to pay the tuition fees of the child, who was not an...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2) | loan that was anticipated to be forgiven was not a bona fide loan, so that s. 15(2) did not apply | 190 |

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(11) - Investment Contract | loan that was anticipated to be forgiven was not in fact a loan | 122 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) - Excluded Obligation | loan included in income under s. 15(2) was excluded obligation re its subsequent forgiveness | 209 |

26 February 2004 External T.I. 2003-0045471E5 F - Prêt à un actionnaire

ABCco carries on a written communications consulting business and does not carry on a money lending business in the ordinary course of its...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2.4) - Paragraph 15(2.4)(e) | housing loan not excluded if comparable employees would not have received it | 208 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Incurring of Expense | forgiven amount not deductible in computing income | 112 |

Subsection 15(1.4) - Interpretation — subsection (1)

Paragraph 15(1.4)(c)

Administrative Policy

4 June 2024 STEP Roundtable Q. 2, 2024-1003641C6 - Salary to Family Members

Where a corporation pays wages to an individual employee who is not a shareholder but does not deal at arm’s length with a shareholder and a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | s. 248(28) applied to avoid double taxation under s. 15(1) and s. 5 | 165 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | s. 248(28) applied where overpayment of wages was a s. 15(1) benefit | 53 |

6 December 2016 External T.I. 2016-0666841E5 F - Sale of property for POD less than FMV

Opco’s shares are held as to 40%, 40% and 20% by Holdco A, Holdco B and Holdco C, which are wholly owned by three individual shareholders (A, B...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) | s. 246(1) applicable to indirect shareholder benefit if direct shareholder influenced the benefit conferral | 205 |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | potential application to immediate shareholder re benefit on indirect shareholder | 207 |

24 June 2015 External T.I. 2015-0575911E5 F - Benefit to shareholder or conferred on a person

Corporation A, which has equal unrelated Shareholders 1, 2, 3 and 4, disposes of a capital property to the spouse (who is not herself a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) | benefit conferred on spouse of individual shareholder of parent | 153 |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | benefit conferred on spouse of individual shareholder of parent | 253 |

3 March 2015 Internal T.I. 2014-0527841I7 F - Avantage imposable pour aéronef

In a situation where there was personal use of a corporate aircraft by the individual shareholder (Mr. A) of the "grandfather" (indirect parent)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 13 - Subsection 13(7) - Paragraph 13(7)(c) | apportionment of aircraft use between business and personal | 74 |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | benefits from personal use of corporate aircraft based on the cost of similar benefit from arm's length supplier | 174 |

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) | s. 15(1.4)(c) applied to extend scope of Massicotte indirect benefit doctrine | 857 |

10 October 2014 APFF Roundtable, 2014-0538101C6 F - Avantage automobile en vertu de 15(5)

The son of the sole shareholder of a corporation works for the corporation and receives automobile benefits in the course of his employment. Is...

Paragraph 15(1.4)(e)

Finance

Comment on s. 15(1.4)(e) in the 16 May 2018 IFA Finance Roundtable

Most of the 2016 technical amendment proposals were enacted in the second Budget Bill for 2017. However, in the case of the foreign demergers rule...

Subsection 15(1.5)

Administrative Policy

2021 Ruling 2020-0875391R3 - Post-acquisition restructuring

The Taxpayer (a Canadian public corporation with a widely-dispersed shareholder base) and Pubco (a corporation, governed by the laws of (foreign)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.1 - Subsection 212.1(4) | application of s. 212.1(4) where ultimate joint acquisition of most of NR Target structure by Cdn. Taxpayer and NR Pubco, but with Taxpayer maintaining control of Target's Canco until it is sold to Taxpayer to eliminate the sandwich structure | 941 |

Paragraph 15(1.5)(a)

Articles

Tim Barrett, Andrew Morreale, "Foreign Affiliate Update", 2019 Conference Report (Canadian Tax Foundation), 35: 1 – 53

Share cancellation requirement

- The s. 15(1.5)(a) demerger rule does not apply where the shares of the demerging corporation are cancelled, which...

Paragraph 15(1.5)(c)

Articles

Tim Barrett, Andrew Morreale, "Foreign Affiliate Update", 2019 Conference Report (Canadian Tax Foundation), 35: 1 – 53

Undesirability of gain if demerger of top-tier affiliate

- Where the demerger is of a top-tier affiliate whose FMV exceeds the net surplus and the...

Subsection 15(2) - Shareholder debt

Cases

St-Pierre v. Canada, 2018 FCA 144

The taxpayer was the sole shareholder and director of a Quebec corporation (the “Corporation``) that realized an eligible capital amount on a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | retroactive judgment of a Superior Court effectively treated as only having prospective effect for ITA purposes | 425 |

Canada v. Gillette Canada Inc., 2003 DTC 5078, 2003 FCA 22

Some of the shares held by the taxpayer in its French subsidiary were purchased for cancellation by the subsidiary in consideration for the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Payment & Receipt | replacement with different currency note | 60 |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(13.1) - Paragraph 212(13.1)(b) | 117 |

Magicuts Inc. v. Canada, 2001 DTC 5665, 2001 FCA 332

Whether there was an amount owing by the taxpayer to its non-resident parent turned on whether accounts between them were netted. The Court found...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Loss v. Loss | trade receivable contributed on capital account to sub | 68 |

Wallace v. Canada, 98 DTC 6326 (FCA)

The taxpayer became indebted to a company of which he was a sole shareholder as a result of a bank calling in a guarantee by the company of a loan...

Dunlop v. The Queen, 95 DTC 5351, [1995] 2 CTC 149 (FCTD)

The taxpayer failed to establish that a loan had been made to him directly by a brokerage firm ("Walwyn") rather than from a corporation ("Canam")...

The Queen v. Silden, 93 DTC 5362, [1993] 2 CTC 123 (FCA)

The taxpayer, who was an employee of a Norwegian multinational corporation ("Musnor") was transferred to Canada and issued 1/3 of the shares of a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Interpretation Bulletins, etc. | 84 |

Nellis v. The Queen, 86 DTC 6377, [1986] 2 CTC 216 (FCTD)

"The purpose of Section 15 of the Income Tax Act is to prevent a corporation from distributing its profits to its shareholders under the guise of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 76 | 47 |

Schlamp v. The Queen, 82 DTC 6274, [1982] CTC 304 (FCTD)

The amount of a loan, made by a company to its shareholder for the purchase by him of a home for occupation by his family, was added to his income.

See Also

Commissioner of Taxation v Bendel, [2026] HCA 18

The corporate trustee (“Gleewin”) of a discretionary trust resolved to set aside, for the benefit of two beneficiaries (Mr. Bendel and a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(24) | at common law, an amount became payable when the trustee set it aside for payment | 437 |

Malamute Contracting Inc. v. The King, 2025 TCC 47

A small contracting company made regular bi-weekly payments to its two shareholders (Mr. and Mrs. Lynch) in amounts equal to an even gross salary...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 5 - Subsection 5(1) | cheques to the shareholders labelled as (and treated rather like) “payroll” in fact were shareholder advances | 260 |

St-Pierre v. The Queen, 2017 TCC 69, rev'd 2018 FCA 144

The taxpayer was the sole shareholder and director of a Quebec corporation (``2869``) that realized an eligible capital amount on a disposition on...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Estoppel | limited estoppel remedies in Quebec/no abusive conduct by CRA | 459 |

| Tax Topics - General Concepts - Unjust Enrichment | taxpayer was unjustly enriched when he received capital dividends that subsequently were declared to not have been validly paid as dividends | 85 |

Erb v. The Queen, 2000 DTC 1401 (TCC)

The taxpayers, along with related persons owned shares of a corporation ("Enterprises") and received draws from a partnership, of which they and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Specific v. General Provisions | 68 |

Lemoine v. The Queen, 96 DTC 1655 (TCC)

The taxpayer was unsuccessful in his attempt to establish that a loan received by him from a controlled corporation (Lemoine Inc.) was in fact a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Illegality | prohibited loan recognized | 33 |

Haynes v. The Queen, 94 DTC 1906, [1995] 1 CTC 2515 (TCC)

Before finding that the taxpayer had received $210,000 from his corporation as an appropriation rather than a loan, Margeson TCJ. stated (p. 1910)...

285614 Alberta Ltd. and Maplesden v. Burnet, Duckworth & Palmer, [1993] WWR 374, 8 BLR (2d) 280 (Alta. Q.B.)

Te defendant was found to be negligent in not advising of the risk that the signing by the individual plaintiff of a demand promissory note as...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Negligence, Fiduciary Duty and Fault | failure to advise that opinion might be incorrect | 160 |

Laflamme v. MNR, 93 DTC 50, [1992] 2 CTC 2596 (TCC)

In finding that the inclusion of the amount of a loan made to the taxpayer by a corporation owned by his father in the taxpayer's income was not...

Tonolli Canada Ltd. v. Minister of National Revenue, 91 DTC 520, [1991] 1 CTC 2607 (TCC)

After a venture carried on through a U.S. subsidiary which was owned by the taxpayer and its Netherlands parent proved to be unsuccessful, the...

Wolinsky v. MNR, 90 DTC 1854, [1990] 2 CTC 2417 (TCC)

The non-payment of interest did not constitute the "making of a loan" for purposes of the pre-1982 version of the provision, although it resulted...

Miconi v. MNR, 85 DTC 696, [1985] 2 CTC 2457 (TCC)

A real estate property was found to be beneficially owned by the taxpayer rather than by a corporation controlled by him, with the result that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(2) | 95 |

Heal v. MNR, 80 DTC 1169, [1980] CTC 2199 (TCC)

Before finding that an advance by the company of which the taxpayer was the principal shareholder to aid in his construction of a home was...

Administrative Policy

Income Tax Folio S3-F1-C1, Shareholder Loans and Debts, April 10, 2025

Characterizing as loan

- 1.14 The determination of whether a loan has been received or a debt incurred is not based on accounting entries, which...

25 February 2022 External T.I. 2020-0873761E5 F - Shareholder loan

On January 1, 2019, the Corporation (which had a calendar year) made the loan of $1,000, bearing interest at 5% per annum, to a shareholder (Mr....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80.4 - Subsection 80.4(3) - Paragraph 80.4(3)(b) | s. 80.4(2) does not apply to accrued and unpaid interest on a loan | 196 |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2.6) | s. 15(2) applies separately to accrued and unpaid interest on a shareholder loan, but s. 80.4(2) does not apply to such interest | 142 |

2 October 2014 External T.I. 2013-0506551E5 - Transitioning from 15(2) to a PLOI

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2.11) | PLOI election unavailable for pre-2012 loan that is repaid and relent/ s. 15(2) applies only to 1st loan | 210 |

27 February 2014 External T.I. 2013-0506401E5 - Loan from a partnership to an individual

{kind=link}

A partnership between Holdco1 as the 99.9% LP and Holdco2 as the 0.1% GP makes a $2 million non-interest-bearing demand loan to the taxpayer, the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | bona fide loan not a transfer | 165 |

2010 Ruling 2010-0353141R3 - Related Foreign Entity Financing

a loan from a controlled foreign affiliate to a related non-resident entity will not trigger the application of s. 15(2) and Part XIII.

7 September 2006 External T.I. 2006-0172841E5 F - 15(2) - employé non-actionnaire au moment du prêt

CRA indicated that s. 15(2) can apply to a non-shareholder, non-connected employee who receives a loan from the employer to enable the employee to...

8 October 2004 APFF Roundtable Q. 4, 2004-0088411C6 F - Prêt à une société de personnes par une société

Two individuals equally own a corporation and have equal interests in a professional partnership. The corporation on-lends the proceeds of a loan...

30 April 2004 External T.I. 2003-0045851E5 F - L'affaire Gillette Canada inc.

Does CRA agree with the TCC and FCA Gillette Canada decisions regarding the application of ss. 15(2) and (2.1)? CRA responded:

We disagree with...

23 March 2004 External T.I. 2003-0049031E5 F - Paragraphe 15(2) de la Loi et "montant remis"

In 2003, Opco made a loan to the adult child of its sole shareholder in order to pay the tuition fees of the child, who was not an employee. The...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(11) - Investment Contract | loan that was anticipated to be forgiven was not in fact a loan | 122 |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1.21) | inclusion under s. 56(2) avoided second inclusion under s. 15(1.21) | 296 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) - Excluded Obligation | loan included in income under s. 15(2) was excluded obligation re its subsequent forgiveness | 209 |

23 January 2001 External T.I. 2000-0045445 F - DETTE D'UN ACTIONNAIRE - FIDUCIE

Opco, a private corporation carrying on a business, indirectly acquires a capital property by forming a trust, advancing $10,000 to it with the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(b) | where Opco makes a loan to a wholly-owned trust, the shareholder of Opco does not deal at arm’s length with the trust | 80 |

17 February 1997 External T.I. 9640655 - LOAN TO A FUTURE SHAREHOLDER

S.15(2) does not apply to a loan made by a corporation to an individual who only becomes a shareholder of the corporation after the loan is made.

25 November 1993 Income Tax Severed Letter 9323577 - Interest Costs on Bridge Financing upon Relocation

RC's policy is that an employee will not be subject to a taxable benefit for the interest costs associated with bridge financing arrangements...

5 January 1993 T.I. 923226 (November 1993 Access Letter, p. 491, ¶C9-290; (Tax Window, No. 28, p. 16, ¶2375)

A loan may still qualify after its transfer at fair market value to a related corporation by which the employee is also employed, because the...

92 C.R. - Q.43

Where an open or running account of a shareholder with a corporation is cleared at every year-end by the payment of salaries or dividends, s....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(j) | 36 |

19 November 1990 T.I. (Tax Window, Prelim. No. 2, p. 19, ¶1050)

Because the application of s. 15(2) is determined only at the time the debt is incurred, it will not apply by virtue only of the debtor having...

October 1989 Revenue Canada Round Table - Q3 (Jan. 90 Access Letter, ¶1075)

A partnership is a person for purposes of s. 15(2).

84 C.R. - Q.16

"Taxpayer" in s. 20(1)(j) is considered to include a partnership where a loan subject to s. 15(2) previously has been included in the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Taxpayer | 23 |

80 C.R. - Q.39

If a person who holds shares as a nominee or trustee is not in his personal capacity a shareholder of the corporation or a related corporation and...

80 C.R. - Q.7

The holding of the shares by a trustee will not cause the loss of the exemption, provided that the shareholder was the beneficial owner.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | 34 |

IT-119R4 "Debts of Shareholders and Certain Persons Connected With Shareholders" 7 August 1998

Articles

John Lorito, Trevor O'Brien, "International Finance – Cash Pooling Arrangements", 2014 Conference Report, (Canadian Tax Foundation), 20:1-33

Withholding based on net increase (p. 16)

If the shareholder loan rules apply to loans made by a Canadian resident corporation to a non-resident,...

Randy S. Morphy, "The Modern Approach to Statutory Interpretation, Applied to the Section 15 Anomaly in Foreign Affiliate Financing", Canadian Tax Journal, (2013) 61:2, 367-85: summary under s. 15(2.3).

Chris Van Loan, "Canada Revenue Agency Rules Positively on Second Tier Financing Structure", Business Vehicles, Vol. XIII, No. 4, 2010, p. 713.

Singer, "Shareholder Loan Can Be Used to Acquire Recreational Home Outside of Canada", Taxation of Executive Compensation and Retirement, December 1990/January 1991, p. 381.

"Loan May Be Disqualified Where it is Made to Acquire Dwelling Already Occupied as Owner", Taxation of Executive Compensation and Retirement, March 1990, p. 249.

Paragraph 15(2)(a)

Administrative Policy

27 October 2004 External T.I. 2004-0088581E5 F - Prêt à un actionnaire

CRA indicated that where s. 15(2.4)(b) applies, this exception continues to apply if, subsequent to obtaining the loan, the individual is no...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2) - Paragraph 15(2)(b) | exception unavailable to the extent loan funded renovations | 73 |

Paragraph 15(2)(b)

Administrative Policy

27 October 2004 External T.I. 2004-0088581E5 F - Prêt à un actionnaire

CRA indicated that the availability of the s. 15(2.4) exception was questionable given that the individual was the sole employee and shareholder...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2) - Paragraph 15(2)(a) | exception continues to apply following cessation of employment | 30 |

Subsection 15(2.01)

Articles

Sam Li, "The Revised Shareholder Loan Rules", International Tax Highlights, Vol. 3, No. 4, November 2024, p. 9

Excluded loan scope (p. 11)

S. 15(2.01) of the August 12, 2024 draft legislation proposes to exclude from the application of s. 15(2) a loan the...

CPA Canada, "Submission regarding Technical Amendments Legislation in Budget 2024 included in the August 2024 Draft Legislation", 11 September 2024 CPA Canada submission

Insufficient scope to the s. 15(2.01) exceptions re foreign subsidiaries held through foreign partnerships (pp. 2-4)

- Notwithstanding the...

Subsection 15(2.1)

Administrative Policy

25 November 2021 CTF Roundtable Q. 8, 2021-0911881C6 - ss 15(2) and FA rules

A partnership (P), whose partners (FA1 and FA2) are foreign subsidiaries of Canco, borrows money from another foreign subsidiary (FA3) of Canco in...

7 June 2011 Internal T.I. 2011-0397921I7 F - Financement inter-sociétés

Canco makes a loan to a partnership (“XXXXXXXXXX Partnership”) that is wholly-owned by an indirect U.S. parent of Canco (the general partner)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 227 - Subsection 227(6.1) | refund of withholding tax on repayment of loan | 193 |

| Tax Topics - Income Tax Act - Section 80.4 - Subsection 80.4(3) - Paragraph 80.4(3)(b) | s. 80.4 would not apply to a s. 15(2) loan if it is not repaid | 175 |

5 December 2002 Internal T.I. 2002-0171847 F - RESIDENCE D'UNE FIDUCIE

The corporation of which Mr. X is a shareholder makes a loan to the trust of which he is a beneficiary for the construction of a residence which...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Principal Residence - Paragraph (c.1) - Subparagraph (c.1)(ii) | principal residence designation is available in respect of a specified beneficiary even though the residence is rented by the trust to that beneficiary | 78 |

20 January 2000 External T.I. 9918035 F - SOCIETE DE PERSONNES RATTACHEE

Five individuals, who were equal members of a partnership (X P/p) through their respective wholly owned corporations, also were equal direct...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | partnership between 5 equal individual partners likely did not deal at arm’s length with such individuals qua shareholders of their respective corporations that formed a second partnership | 130 |

Subsection 15(2.11) - Pertinent loan or indebtedness

Administrative Policy

28 May 2025 IFA Roundtable Q. 6, 2025-1052631C6 - Earnings of a disregarded US LLC

After indicating that frequent anticipated payments and repayments occurring in a cross-border physical or notional cash-pooling arrangement...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2.17) | illustration of ordering rule for determining whether s. 15(2.17) applies to a cross-border notional cash pooling arrangement | 928 |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2.6) | frequent anticipated payments and repayments occurring in a cross-border physical or notional cash-pooling arrangement likely would be a s. 15(2.6) series | 109 |

Notice to Tax Professionals: Updates to filing process for a pertinent loan or indebtedness election, 25 March 2022

Expanded election disclosure and change to permit election to be made on loan-by-loan basis

… Effective for any elections made on or after April...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(11) | expanded PLOI election disclosure on a loan-by-loan basis | 302 |

“Pertinent loans or indebtedness (PLOI)” under “Understanding Interest” 25 March 2022

Information to be provided in respect of the PLOI election

Currently there is no prescribed form to file a PLOI election. The PLOI election should...

7 November 2014 External T.I. 2014-0542061E5 - Section 15(2.12), follow up to 2014-051943

A CRIC remits Part XIII tax under s. 214(3)(a) on the amount of a loan to non-resident "Parentco" and, more than two years after the end of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 227 - Subsection 227(6) | inability to refund Part XIII tax which disappears on late PLOI election if non-timely application | 165 |

2 October 2014 External T.I. 2013-0506551E5 - Transitioning from 15(2) to a PLOI

Can a s. 15(2) loan made to a non-resident person prior to March 29, 2012 ("Original Loan") be transitioned to the pertinent loan or indebtedness...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2) | s. 15(2) applies only to 1st loan | 0 |

8 September 2014 External T.I. 2013-0482991E5 - 15(2) and related provisions

Debtco, a non-resident corporation which is connected to the non-resident wholly-owning parent (Parentco) of Canco, became indebted to Canco...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2.6) | assignment of debt not its repayment | 163 |

| Tax Topics - Income Tax Act - Section 221.2 - Subsection 221.2(1) | no unpaid liability of non-resident to be reduced re appropriation of unrefunded s. 214(3)(a) tax | 227 |

6 August 2014 External T.I. 2014-0519431E5 - Section 15(2.12)

Is the CRIC required to file an amended return, on late-filing a PLOI election, to reflect the additional s. 17.1(1) interest income? CRA...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 17.1 - Subsection 17.1(1) | amended return not expected | 265 |

18 June 2014 Internal T.I. 2014-0534541I7 - PLOI Elections

Blanket election

Although a taxpayer may file a single written communication containing a PLOI election for various particular amounts owing, that...

Pertinent loans or indebtedness Historical CRA Webpage: 17 January 2014

Required particulars in filing letter

File the election at the tax Centre of the CRIC... . The election must include the following:

- the name and...

23 May 2013 IFA Round Table Q. 6(c)

Will CRA permit a blanket PLOI election (specifying that it is being made for each debt owing from the particular debtor to the particular...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(11) | 96 |

Finance

16 May 2018 IFA Finance Roundtable, Q.9

S. 15(2.11) PLOI elections can be made to elect out of s. 15(2) only by corporations resident in Canada (CRICs) where controlled by a non-resident...

Articles

Bal Katlai, "Simple Planning Around Outbound Loans Using Tax Incentives", Canadian Tax Highlights, Vol. 27, No. 12, December 2019, p. 9

Example of Canco being able to keep a loan to its NR parent outstanding indefinitely by offsetting PLOI interest by SR&ED credits (p. 9)

What if...

Joint Committee, "Foreign Affiliate Dumping, Derivative Forward Agreement and Transfer Pricing Amendments Announced in the 2019 Federal Budget", 24 May 2019 Submission of the Joint Committee

- The ss. 15(2) and (2.11) rules should permit PLOI loans to be made by a CRIC to any non-resident person who is a “parent” under the expanded...

Paragraph 15(2.11)(d)

Administrative Policy

15 May 2024 IFA Roundtable Q. 6, 2024-1007591C6 - PLOI Election Administrative Relief

Effective March 25, 2022, CRA adopted an administrative policy that requires only one PLOI election to be made in respect of each loan or...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(11) - Paragraph 212.3(11)(c) | irreversibility of choice to make a single election unless a separate loan agreement is entered into | 248 |

Subsection 15(2.12)

Administrative Policy

15 May 2024 IFA Roundtable Q. 4, 2024-1007571C6 - Late-filed PLOI election

CRA indicated that it has revised its procedures for the late-filing of a PLOI election. Although this can still be accomplished by the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(12) | revised procedures for the filing of late PLOI elections | 155 |

Subsection 15(2.13)

Administrative Policy

26 May 2016 IFA Roundtable Q. 11, 2016-0642031C6 - PLOI late-filed penalties

A corporation resident in Canada (“CRIC”) has balances of accounts receivable reflecting the accumulation of hundreds of sales including to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(13) | aggregating A/R debits for penalty purposes under review | 87 |

Subsection 15(2.16)

Finance

6 October 2017 APFF Financial Strategies and Instruments Roundtable, Q.13

The Explanatory Notes to s. 15(2.16) indicate that there is no objective of attacking commonplace loan transactions which are not intended to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(5) - Specified Right | right to secure shareholder debt is not per se a specified right | 165 |

Paragraph 15(2.16)(c)

Administrative Policy

8 May 2018 CALU Roundtable Q. 1, 2018-0745491C6 - Back-to-back loans

In 2017-0690691E5 F, a 50% limited partner (Ms. X) funded her investment in a limited partnership (jointly owned with her husband) with a $3M bank...

Subparagraph 15(2.16)(c)(i)

Clause 15(2.16)(c)(i)(B)

Administrative Policy

31 October 2017 External T.I. 2017-0690691E5 F - New section 15 back to back loan rules

99.99% of the units of LP were held by Mr. and Ms. X (spouses) and 0.01% of its units were held by a general partner that was a subsidiary of a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2.16) - Paragraph 15(2.16)(c) - Subparagraph 15(2.16)(c)(ii) | term deposit to secure shareholder loan potentially a specifed right | 199 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(5) - Specified Right | pledged term deposit could be specified right | 115 |

Subparagraph 15(2.16)(c)(ii)

Administrative Policy

31 October 2017 External T.I. 2017-0690691E5 F - New section 15 back to back loan rules

A 50% limited partner (Ms. X) funded her investment in an LP jointly owned with her husband through a $3M bank loan that was secured by a pledge...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2.16) - Paragraph 15(2.16)(c) - Subparagraph 15(2.16)(c)(i) - Clause 15(2.16)(c)(i)(B) | application to a term deposit pledged by a family corporation to secure a business loan taken out by a shareholder | 195 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(5) - Specified Right | pledged term deposit could be specified right | 115 |

14 September 2017 Roundtable, 2017-0703901C6 - CPA Alberta 2017 Q11: Shareholder loans

1. Where the security provided by the corporation may be used only for repayment of the arm’s length debt owing by the shareholder, will the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(5) - Specified Right | excluded provision of corporate security to secure repayment of a shareholder loan | 167 |

May 2017 CPA Alberta Roundtable, ITA Q.11

The Technical Notes to s. 15(2.16) indicate that “it is intended that a specified right will not exist if it is established that all of the net...

Subsection 15(2.17)

Administrative Policy

28 May 2025 IFA Roundtable Q. 6, 2025-1052631C6 - Earnings of a disregarded US LLC

CRA indicated that anticipated frequent and ongoing movements in the account balances of participants to a notional cash-pooling arrangement would...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2.6) | frequent anticipated payments and repayments occurring in a cross-border physical or notional cash-pooling arrangement likely would be a s. 15(2.6) series | 109 |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2.11) | PLOI election available re cross-border cash-pooling arrangement/ simplified PLOI election will be announced | 100 |

Income Tax Folio S3-F1-C1, Shareholder Loans and Debts, April 10, 2025

Overview

1.18 … In very general terms, where the conditions set out in subsection 15(2.16) are met, subsection 15(2.17) deems that the...

Articles

Amanda S.A. Doucette, Britney Wangler, "Normal Borrowing by CCPC Owners Can Create an Income Inclusion", Canadian Tax Focus, Vol. 7, No. 1, February 2017, p. 1

Potential application of s. 15(2.17) where corporation guarantees loan to individual shareholder (p. 1)

[T]he back-to-back loan rules…may have...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(5) - Specified Right | 190 |

Finance

26 April 2017 IFA Finance Roundtable, Q.13

[intention is to limit the imputation of a shareholder loan to Canco to the amount of Canco’s...

Subsection 15(2.18)

Articles

Jason Boland, Christopher Montes, "A Detailed Review of the Back-to-Back Loan Rules", 2016 Conference Report (Canadian Tax Foundation), 26:1-32

FIFO treatment of repayments (p. 26:25)

Finance has indicated that repayments are considered to occur on a first-in-first-out basis, in accordance...

Subsection 15(2.2) - When s. 15(2) not to apply — non-resident persons

Administrative Policy

21 June 1995 External T.I. 9510915 - 6363-1 FOREIGN AFFILIATES - DEEMED ABI

With respect to a loan by a wholly-owned foreign affiliate of a Canadian corporation ("Canco") to a non-resident corporation that was related to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 95 |

Subsection 15(2.3) - When s. 15(2) not to apply — ordinary lending business

Administrative Policy

Income Tax Folio S3-F1-C1, Shareholder Loans and Debts, April 10, 2025

Ordinary course exception

1.28 The exception in S. 15(2.3) can apply where the debtor or borrower is a shareholder or a shareholder employee.

1.30...

2012 Ruling 2011-0417711R3

Canco, which is a grandchild subsidiary of Parentco (a resident of Country 1), borrows money from time to time under note offerings in Canada or...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 17 - Subsection 17(15) - Exempt loan or transfer | 108 |

9 May 2011 External T.I. 2010-0385211E5 F - Entreprise habituelle de prêt d'argent

A corporation whose business it was to purchase and sell shares of private and public corporations, sold all its shares and used the proceeds to...

2007 Ruling 2007-0226281R3 - Withholding Exemption - Use of Finco

Non-resident bondholders make a loan to a corporation ("Finco") which is wholly-owned by a charitable discretionary trust and Finco lends the...

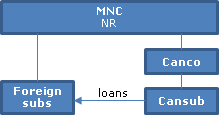

8 February 2006 External T.I. 2004-0064811E5 - Subsection 15(2)

{kind=link}

Cansub is a wholly-owned subsidiary of Canco which, in turn, is wholly-owned by MNC, a non-resident multi-national corporation. All the treasury...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(6) - Paragraph 95(6)(b) | 195 |

2006 Ruling 2006-0211781R3 - Withholding Tax Exemption

Non-resident term lenders make a loan to a newly-incorporated wholly-owned subsidiary ("Finco") of the general partner of a Canadian limited...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Subparagraph 212(1)(b)(vii) | loan to Finco sub of GP with on-loan to LP | 89 |

2006 Ruling 2006-0191881R3 - Witholding Tax Exemption

Ruling that s. 15(2.3) will apply to a loan made by an indirect special purpose finance subsidiary of an income fund to an indirect general...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 132 - Subsection 132(6) | loan guarantees | 56 |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Subparagraph 212(1)(b)(vii) | 141 |

1996 Tax Executive Institute Round Table, Q. X (Draft, No. 963906)

"When a loan is made to a shareholder in the ordinary course of the creditor's business with the same terms and conditions as offered to the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2.4) | 67 |

Articles

John Lorito, Trevor O'Brien, "International Finance – Cash Pooling Arrangements", 2014 Conference Report, (Canadian Tax Foundation), 20:1-33

Descripton of physical and notional cash pooling (pp. 2-3)

[I]n general terms there are essentially two types of cash pooling arrangements [fn 1:...

Randy S. Morphy, "The Modern Approach to Statutory Interpretation, Applied to the Section 15 Anomaly in Foreign Affiliate Financing", Canadian Tax Journal, (2013) 61:2, 367-85:

Example 1 – loan to direct foreign sub (pp. 369-370)

In example 1, a Canadian parent ("Canco") makes an interest-free loan ("the loan") to a...

Guy Fortin, Melanie Beaulieu, "The Meaning of the Expressions ‘In the Ordinary Course of Business' and ‘Directly or Indirectly'", 2002 Conference Report (Toronto: Canadian Tax Foundation, 2003) 36:1-60.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(p) - Subparagraph 20(1)(p)(ii) | 0 |

Subsection 15(2.4) - When s. 15(2) not to apply — certain employees

See Also

Goreham v. The Queen, 2000 DTC 1561 (TCC)

At the time the taxpayer received a loan from a company carrying on a fishing business that was beneficially owned, as to 50%, by the taxpayer and...

Lavoie v. The Queen, 95 DTC 673, [1995] 2 CTC 2709 (TCC)

Before finding that a demand promissory note signed by the taxpayer to evidence a loan made to him by a corporation he controlled did not...

Kalousdian v. The Queen, 94 DTC 1722, [1994] 2 CTC 2127 (TCC)

Mogan TCJ. accepted evidence that a loan made to the taxpayer by a corporation owned equally by him and an unrelated individual was made to him on...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Evidence | 103 |

Spencer v. The Queen, 93 DTC 1222, [1993] 2 CTC 2765 (TCC)

Oral evidence by the individual's shareholder of his intent to repay money that had been advanced to him by a numbered corporation to construct a...

Kanters v. MNR, 92 DTC 1508, [1992] 1 CTC 2413 (TCC)

What at best was an agreement for the shareholders to repay money to the corporation when the operation in which they invested the loaned monies...

Deckelbaum v. MNR, 82 DTC 1636, [1982] CTC 2659 (T.R.B.)

A home purchase loan arrangement was evidenced by a resolution of the corporation authorizing the making of the loan and providing for its...

Fabry v. MNR, 81 DTC 638 (T.R.B.)

The terms of a mortgage owing by the taxpayer to his company the proceeds of which were used to finance the acquisition and completion of...

Hendriks v. MNR, 81 DTC 939, [1981] CTC 3029 (T.R.B.)

Bona fide arrangements for the repayment of a loan from the corporation to the taxpayer were found not to exist in light of the fact that the loan...

Reekie v. MNR, 80 DTC 1447, [1980] CTC 2502 (T.R.B.)

A promissory note and a letter acknowledging indebtedness, which were prepared in the taxation year following the taxation year in which the loan...

Altenhof v. MNR, 73 DTC 239, [1973] CTC 2303 (T.R.B.)

The taxpayer was unable to establish that at the time he received an advance from the corporation arrangements were made for its repayment or that...

Administrative Policy

5 February 2002 External T.I. 2001-0115475 - LOAN TO PURCHASE SHARES

Where a loan which previously had been exempted under s.;15(2.4)(c), (e) and (f) subsequently was assigned to a partnership without being novated,...

26 May 1997 External T.I. 9705455 - Timing when to be specified employee

Where a loan is received by an employee who is not a specified employee at that time, but later in the year becomes a specified employee, the...

1996 Tax Executive Institute Round Table, Q. X (Draft, No. 963906)

"With respect to a loan which is excluded from a shareholder's income by reason of proposed subsection 15(2.4) or (2.5) of the Act, we expect...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2.3) | 125 |

11 August 1995 External T.I. 9509745 - SHAREHOLDER/EMPLOYEE HOUSING LOAN

Where changes to an original loan result in its novation, the new loan, because it serves to refinance an existing debt, will not qualify for the...

Income Tax Regulation News, Release No. 3, 30 January, 1995 under "Paragraph 15(2)(b) and 20(1)(j)"

bona fide repayments of shareholder loans which are the result of the declaration of dividends, salaries or bonuses should not be considered part...

30 March 1994 Internal T.I. 9336137 - ALLOCATION OF S/H LOAN TO FARM AND P/R

Where a loan made by the corporation to the employee exceeds the amount used for a qualified purpose (in this case, because the loan proceeds were...

28 March 1994 External T.I. 9332255 - MEANING OF "DWELLING"

When asked whether the exemption would apply to the making of a loan of $100,000 for the acquisition by an individual of a 20-year lease of a...

17 June 1994 External T.I. 9332295 - shareholder loans-employee gifts loan to spouse for home

"It is our view that a loan will not meet the exclusion requirements of subparagraph 15(2)(a)(ii) of the Act where the individual to receive the...

20 May 1994 External T.I. 9400835 - LOAN TO A SHAREHOLDER

Commercial housing loans specify a term (the maximum of which is normally seven years) under which the loan can be renewed, at which point the...

93 C.R. - Q. 17

It normally is unreasonable and inconsistent with normal commercial practice for a lender to loan a large sum of money without security or not to...

92 C.R. - Q.42

The exception in s. 15(2)(a)(ii) will not apply to loans made or indebtedness arising in respect of repairs, alterations, or renovations to a...

30 November 1991 Round Table (4M0462), Q. 2.3 - Housing Loan (s.15(2)(a)(ii), I.T.A.) (C.T.O. September 1994)

Where changing an interest-bearing loan into an interest-free loan results under the applicable civil legislation in a new security, the new...

30 November 1991 Round Table (4M0462), Q. 2.1 - Automobile Loan (s.15(2)(a)(iv), I.T.A.) (C.T.O. September 1994)

Although RC does not apply tests of minimum degree or percentage of use of an automobile in the performance of the duties of an employee's office...

7 October 1991 T.I. (Tax Window, No. 10, p. 6, ¶1507)

An employee housing loan which was repayable over a 25-year period would not have a reasonable repayment term, although a repayment or renewal...

4 April 1991 T.I. (Tax Window, No. 2, p. 28, ¶1221)

If under the terms of a separation agreement entered into some years after the acquisition of the home, the employee must leave the home, s....

21 September 1990 T.I. (Tax Window, Prelim. No. 1, p. 7, ¶1002)

Where the amount of a loan from an employer in respect of a recreational property ordinarily inhabited by the employee is in excess of the...

86 C.R. - Q.61

The loan need not be interest-bearing in order to demonstrate a bona fide arrangement for repayment.

86 C.R. - Q.63

Where a public corporation makes a bona fide loan to a shareholder qua employee rather than qua shareholder, on the same conditions as to other...

Paragraph 15(2.4)(a)

See Also

Canadian Occidental U.S. Petroleum Corp. v. The Queen, 2001 DTC 295 (TCC)

The taxpayer lent money on an interest-free basis to a non-resident wholly-owned subsidiary in 1988 and then, in November 1994 transferred the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Hansard, explanatory notes, etc. | 74 | |

| Tax Topics - Statutory Interpretation - Inserting Words | 167 | |

| Tax Topics - Statutory Interpretation - Interpretation Act - Subsection 45(2) | 89 |

Administrative Policy

Income Tax Folio S3-F1-C1, Shareholder Loans and Debts, April 10, 2025

Purpose of acquiring shares for employee’s own benefit

- Disposing of shares before the loan is repaid will generally be considered indicative of...

Paragraph 15(2.4)(b)

Administrative Policy

Income Tax Folio S3-F1-C1, Shareholder Loans and Debts, April 10, 2025

Bifurcation

- 1.39 Where a borrower has a total balance of loans owing to a corporation and only a portion was used for one of the described...

Paragraph 15(2.4)(c)

Administrative Policy

Income Tax Folio S3-F1-C1, Shareholder Loans and Debts, April 10, 2025

Purpose of acquiring shares for employee’s own benefit

- Disposing of shares before the loan is repaid will generally be considered indicative of...

15 June 1999 External T.I. 9902745 F - COOPÉRATIVE DE TRAVAILLEURS

Regarding the availability of s. 15(2.4)(c) to a loan by a worker cooperative, the Directorate stated:

The definition of share in subsection...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 136 - Subsection 136(2) | workers’ cooperative qualifies as a cooperative corporation | 65 |

Paragraph 15(2.4)(e)

See Also

Mast v. The Queen, 2013 TCC 309

The taxpayer was the sole shareholder, and he and his wife were the only regular employees, of a corporation engaged in a packaging business. He...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2.4) - Paragraph 15(2.4)(f) | 67 |

Administrative Policy

Income Tax Folio S3-F1-C1, Shareholder Loans and Debts, April 10, 2025

Loan qua shareholder

- 1.59 Factors that may indicate that a loan made by a corporation to a shareholder-employee arose because of a shareholding...

14 June 2019 External T.I. 2019-0808411E5 - Application of 15(2.4) to home purchase loan

A Canadian-controlled private corporation (“Eco”) hires an individual (“Mr. A”) as CEO. Mr. A will also acquire 3% of Eco’s...

4 November 2011 External T.I. 2011-0406271E5 - Sole Shareholder-Employee Home Purchase Loan

A loan made in 2011 by a corporation to its sole shareholder-employee to facilitate the repayment of a secured line of credit used to finance a...

26 February 2004 External T.I. 2003-0045471E5 F - Prêt à un actionnaire

ABCco carries on a written communications consulting business and does not carry on a money lending business in the ordinary course of its...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1.21) | inclusion of home-acquisition loan under s. 15(2) precluded a further inclusion under s. 15(1.21) | 122 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Incurring of Expense | forgiven amount not deductible in computing income | 112 |

19 February 2002 External T.I. 2002-0118495 - S/H LOAN TO EMPLOYEE TO BUY SHARES FROM S/H

A loan made by a closely-held private corporation at the direction of its controlling shareholder to enable an employee to buy shares from such...

9 January 2001 External T.I. 2000-0059995 - SHAREHOLDER LOANS

Before concluding that s. 15(2.4)(b) did not apply to a housing loan received by a specified employee, the Directorate stated that "it has...

9 December 1999 External T.I. 9910665 F - DETTE D'UN ACTIONNAIRE-HABITATION

Regarding a second mortgage loan made by a corporation (Bco) to its sole shareholder and employee (Mr. A) to fund part of the purchase price for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2.4) - Paragraph 15(2.4)(f) | reasonable repayment term determined by reference to ordinary business practice | 77 |

19 October 1998 Internal T.I. 9809597 F - PRÊT À L'HABITATION - 15(2.4)

An operating company (G Inc)., made a home purchase loan to its vice president, who was also a shareholder of a holding company that indirectly...

IT-119R4 "Debts of Shareholders and Certain Persons Connected With Shareholders" 7 August 1998

11. Whether or not a loan made by a corporation to an individual is considered to have been received by that individual in his or her capacity as...

Paragraph 15(2.4)(f)

See Also

Mast v. The Queen, 2013 TCC 309

This case is summarized above under s. 15(2.4)(e). Angers J found that there were no bona fide repayment arrangements for the taxpayer to repay a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2.4) - Paragraph 15(2.4)(e) | requirement to repay at least 50% of principal over 10-year term, with balance at maturity, did not represent bona fide repayment arrangements | 226 |

Davidson v. R., 99 DTC 933, [1999] 3 CTC 2159 (TCC)

Before finding that a loan made by a family company to the taxpayer to finance the acquisition of a home satisfied the requirements for bona fide...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Evidence | 39 |

Administrative Policy

Income Tax Folio S3-F1-C1, Shareholder Loans and Debts, April 10, 2025

Bona fide repayment arrangements

- 1.68 At the time the loan is made, the arrangements for repayment must be such that it is possible to determine,...

24 April 2001 Internal T.I. 2001-0067007 - SHAREHOLDER LOANS

Loans from a corporation to an employee/shareholder that were used to acquire previously issued publicly traded shares of the corporation, where...

9 December 1999 External T.I. 9910665 F - DETTE D'UN ACTIONNAIRE-HABITATION

Regarding a second mortgage loan made by a corporation (Bco) to its sole shareholder and employee (Mr. A) to fund part of the purchase price for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2.4) - Paragraph 15(2.4)(e) | loan to sole shareholder/employee received qua shareholder unless such a loan could be demonstrated to be received by employees | 151 |

IT-119R4 "Debts of Shareholders and Certain Persons Connected With Shareholders" 7 August 1998

12. In considering whether any arrangements for repayment were bona fide, the extent to which the arrangements have been carried out by the...

Subsection 15(2.5)

Administrative Policy

10 October 2025 External T.I. 2025-1076451E5 - Shareholder Loans to Market Maker Trusts

Parentco, a private corporation, wholly owns Opcos, each of which has employees who, under an employee ownership plan, are allowed to acquire and...

Articles

Elizabeth Boyd, Jeremy J. Herbert, "Trusts Holding Shares For Employees", draft 2023 CTF Annual Conference paper

Considerations for structuring a market maker trust (pp. 40-43)

- Given the specified employee rules, market maker trusts are commonly used in...

Subsection 15(2.6) - When s. 15(2) not to apply — repayment within one year

See Also

Magicuts Inc. v. The Queen, 98 DTC 2085, [1999] 1 CTC 2842 (TCC)

There was insufficient evidence to establish that there was an agreed intention between the taxpayer and its non-resident shareholder to set-off...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Loss v. Loss | 114 |

Ozawa v. R., 97 DTC 1500, [1998] 2 C.T.C. 2035 (TCC)

Before going on to find that amounts advanced by a corporation to the taxpayer had not been eliminated by way of set-off against amounts allegedly...

Meeuse v. The Queen, 94 DTC 1397 (TCC)

Each of the loans made to the taxpayer by her husband's company were for separate purposes, for example, financing her acquisition of an...

Uphill Holdings Ltd. v. MNR, 93 DTC 148, [1993] 1 CTC 2021 (TCC)

After noting (at para. 33) that "the object of 15(2)(b) is to prevent the use of a shareholder loan account for indefinite tax deferral purposes...

David Weisdorf v. Her Majesty the Queen, [1993] 2 CTC 2756

At issue was whether an amount, which was lent to the taxpayer, who was "connected" with a shareholder of the corporation (“Steel”), was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Evidence | accounting entries do not create reality | 109 |

Attis v. MNR, 92 DTC 1128, [1992] 1 CTC 2244 (TCC)

The taxpayer initially advanced significant sums to his corporation, but subsequently began to withdraw amounts from it for personal ends. For the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | 78 |

William G. Docherty v. Minister of National Revenue, 91 DTC 537, [1991] 1 CTC 2409 (TCC)

In finding that the elimination of indebtedness of the taxpayer to his corporation by set-off was sufficiently evidenced by information contained...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Evidence | set-off evidenced in working papers | 83 |

Burgeo Trawlers Limited v. Minister of National Revenue, 91 DTC 231, [1991] 1 CTC 2053 (TCC)

At a shareholders' meeting, it was decided that capital of the shareholders would be returned to them by way of offset against advances to the...

Taylor v. MNR, 87 DTC 475, [1987] 2 CTC 2178 (TCC)

At the end of the following taxation year, the taxpayer owed $22,529 to the corporation in respect of advances which it had made to him, and the...

Administrative Policy

28 May 2025 IFA Roundtable Q. 6, 2025-1052631C6 - Earnings of a disregarded US LLC

In the course of discussion of a physical, then a notional cash-pooling arrangement between a Canadian company and affiliated foreign companies,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2.17) | illustration of ordering rule for determining whether s. 15(2.17) applies to a cross-border notional cash pooling arrangement | 928 |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2.11) | PLOI election available re cross-border cash-pooling arrangement/ simplified PLOI election will be announced | 100 |

Income Tax Folio S3-F1-C1, Shareholder Loans and Debts, April 10, 2025

Requirement to amend return where s. 15(2.6) not satisfied

- 1.73 Since it is not known whether the requirements of s. 15(2.6) are met until one...

25 February 2022 External T.I. 2020-0873761E5 F - Shareholder loan

CRA indicated that where a corporation with calendar taxation years makes an interest-bearing loan to its individual shareholder, and the accrued...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2) | s. 15(2) applies separately to accrued and unpaid interest on shareholder loan | 181 |

| Tax Topics - Income Tax Act - Section 80.4 - Subsection 80.4(3) - Paragraph 80.4(3)(b) | s. 80.4(2) does not apply to accrued and unpaid interest on a loan | 196 |

6 April 2018 External T.I. 2018-0738871E5 F - Shareholder

A shareholder (Taxpayer A) who received a loan from a corporation in 2017, repaid the loan at the end of 2018 (after filing Taxpayer A’s 2017...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80.4 - Subsection 80.4(3) - Paragraph 80.4(3)(b) | previous s. 80.4(2) inclusion is reversed when loan is included under s. 15(2) | 110 |

27 February 2018 Internal T.I. 2017-0682631I7 - Subsection 15(2.6) - Series of Loans

Canco (along with other members of the group) was part of a “physical” cash pooling arrangement with a non-resident affiliate (Finco) under...

24 April 2015 External T.I. 2014-0560401E5 - Subsections 15(2) and 227(6.1) and Part XIII tax

Canco assigned a loan (the "Debt") owing to it by a non-resident sister company to their non-resident parent (Parentoco) in repayment of a loan...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 227 - Subsection 227(6.1) | repayment of assigned loan to assignee after 2 years | 162 |

9 October 2015 APFF Roundtable Q. 19, 2015-0595621C6 F - Cash pooling and subsection 15(2)

CRA indicated that it does not have the discretion to not apply s. 15(2), where the applicable statutory exceptions are not available, to amounts...

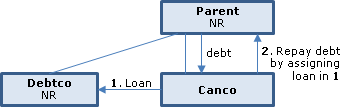

8 September 2014 External T.I. 2013-0482991E5 - 15(2) and related provisions

{kind=link}

Debtco, a non-resident corporation which is connected to the non-resident wholly-owning parent (Parentco) of Canco, is indebted to Canco. Canco...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2.11) | novation of pre-2012 loan | 170 |

| Tax Topics - Income Tax Act - Section 221.2 - Subsection 221.2(1) | no unpaid liability of non-resident to be reduced re appropriation of unrefunded s. 214(3)(a) tax | 227 |

2014 Ruling 2013-0505181R3 - 15(2.6) Series of Loans and Repayments

underline;">: Structure/accounting standards. Parentco, a non-resident and an indirect subsidiary of non-resident Pubco, wholly-owns Canco....

10 January 2014 External T.I. 2013-0506571E5 F - Subsections 15(2) and 15(2.6)

Facts

Each year, Aco makes monthly advances to its sole individual shareholder, A; and each year Aco pays a dividend to A which has the effect of...

23 May 2013 Roundtable, 2013-0483751C6 - Foreign Affiliate Dumping

CRA was asked in the context of s. 212.3(10)(c)(i) whether it would accept FIFO as the method to track the origination and settlement of multiple...

12 June 2012 STEP Roundtable, 2012-0442911C6 - STEP CRA Round Table - June 2012

A shareholder loan repaid by the executors of the shareholder within one year after the end of the creditor's taxation year in which the loan was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(j) | 140 |

15 August 2012 External T.I. 2012-0443581E5 - Shareholder Loans

Before indicating that repayments made in 2011 (which exceeded the shareholder loan balance at the end of 2010), likely could be applied first...

17 February 2004 External T.I. 2003-0033915 - Cash pooling - shareholder benefit

In indicating that a cash pooling arrangement entered into by a Canadian subsidiary with its non-resident parent corporation could result in an...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Payment & Receipt | no automatic set-off | 77 |

6 December 2000 TEI Roundtable Q. 25, 2000-0056035 - SHAREHOLDER LOANS

The CCRA gave a generally favourable response to a question asking for confirmation that the exception in s. 15(2.6) will apply where loans are...

5 October 1992 Income Tax Severed Letter 9219115 - Exempt Shareholder Loans

Yco, a Canadian manufacturing subsidiary of Xco with a calendar year, regularly purchases items from and sells items to Xco in the ordinary course...

92 C.R. - Q.44

Although there is no statutory relief to a non-resident where a particular loan, that previously was subject to s. 15(2) and s. 214(3)(a), is...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(j) | 58 |

5 October 1992 External T.I. 5-921911

Canco makes loans in 1992 and 1993, evidenced by promissory notes, to its U.S. parent, with the loans being repaid by the end of 1993. Would such...

30 November 1991 Round Table (4M0462), Q. 3.4 - Series of Loans and Repayments (C.T.O. September 1994)

S.15(2) will apply where a corporation makes monthly advances to its sole shareholder, with such advances being repaid through a payment of...

18 January 1990 T.I. (June 1990 Access Letter, ¶1256)

Where trade accounts receivable arise from sales of a subsidiary corporation to its non-resident parent, the creation of each account receivable...

IT-119R4 "Debts of Shareholders and Certain Persons Connected With Shareholders" 7 August 1998

27 Repayments are considered to apply first to the oldest loan or debt outstanding ("first-in, first -out basis") unless the facts clearly...

Articles

PWC, "Tax Insights: Cross-border cash pooling arrangements ─ Recent developments", Issue 2018-41, 2 November 2018

CRA expansive view of series in cash pooling context (p.2)

2017-0682631I7 … concluded that transactions occurring as part of a physical cash...

Didier Fréchette, Ryan Rabinovitch, "Current Issues Involving Foreign Exchange", 2015 CTF Annual Conference paper

Conversion into shares on a s. 51 rollover basis nonetheless would give rise to a repayment for s. 15(2.6) purposes (pp. 26: 24-25)

A Canadian...

Subsection 15(3) - Interest or dividend on income bond or debenture

Administrative Policy

IT-52R4 "Income Bonds and Income Debentures"

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Income Bond | 0 |

Subsection 15(5) - Automobile benefit

Cases

Meuse v. The Queen, 94 DTC 6640, [1995] 1 CTC 21 (FCTD)

Because the taxpayer had not filed a form td-5 until the date on which his appeals to the Tax Court were to be heard, he had not adhered to the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Interpretation Act - Section 11 | 60 |

Administrative Policy

5 October 2012 Roundtable, 2012-0454121C6 F - Automobiles de collections

Dozens of collectible vehicles that are treated by a corporation as an investment but its shareholder, who has control of the vehicles at all...

27 October 2004 External T.I. 2004-0080191E5 F - Paragraphes 6(1) et 6(2) de la Loi

An employee, after being subject to a standby charge for four years pursuant to s. 6(1)(e), purchased the automobile from his employer for less...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(1) - Paragraph 6(1)(a) | annual recognition of s. 6(1)(e) standby charges does not reduce quantum of s. 6(1)(a) benefit where subsequent employee bargain-purchase of automobile | 65 |

5 November 2003 Internal T.I. 2003-0043277 F - Benefit-Use of Automobiles

An individual (Y) held 24% of the shares of an automobile sales company ("Opco") whose other shares were held by related individuals through...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) - Paragraph 246(1)(a) | s. 246(1)(a) application re mother’s use of a car of Opco controlled by her son’s Holdco to her rather than son turned on whether her minority Holdco had significant influence over Opco | 288 |

| Tax Topics - Income Tax Act - Section 10 - Subsection 10(1) | automobiles in car dealer inventory used for employee’s personal use remained in inventory, cf. if converted primarily to personal use of shareholder (which would not be a disposition) | 314 |

| Tax Topics - Income Tax Act - Section 9 - Computation of Profit | conversion of automobile in car inventory to personal use of CEO would not entail its deemed disposition nor would the conversion of car inventory to personal use of shareholders | 267 |

Subsection 15(7)

Administrative Policy

5 October 2012 Roundtable, 2012-0451241C6 F - Benefit conferred on a NR shareholder by a NR corp

In the course of finding that the gratuitous use by the non-resident shareholder of a Canadian property of the non-resident corporation likely...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 214 - Subsection 214(3) - Paragraph 214(3)(a) | gratuitous use by NR shareholder of Canadian property of the NR corporation produces a s. 214(3)(a) deemed dividend | 158 |

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) | s. 247(2) could apply to produce s. 212(1)(d) withholding where the NR shareholder of a NR corporation gratuitously uses Canadian corporate property | 92 |

Subsection 15(9)

Administrative Policy

16 August 2017 Internal T.I. 2015-0622751I7 - Part XIII Tax on Benefit to Non-resident

Using funds generated from operations, Opco, which is a foreign affiliate both of its parent (Canco) and grandparent (Can Holdco ), subscribes...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | use of s. 160 to collect s. 15(9) liability of indirect FA on dividends paid to Canco | 275 |

| Tax Topics - Income Tax Act - Section 215 - Subsection 215(1) | CFA liable for failure to "withhold" and remit Pt XIII tax on interest-free benefit on loan to NR sister of its Cdn grandparent | 127 |

| Tax Topics - Income Tax Act - Section 227.1 - Subsection 227.1(1) | s. 227.1 liability can extend to NR directors of a CFA | 176 |

| Tax Topics - Income Tax Act - Section 214 - Subsection 214(3) - Paragraph 214(3)(a) | benefit from interest free loan by CFA to Canco sister deemed to be a dividend subject to Pt XIII tax | 177 |

| Tax Topics - Income Tax Act - Section 80.4 - Subsection 80.4(2) | extra-territorial application of s. 80.4(2) | 134 |