Subsection 74.4(2) - Transfers and loans to corporations

Administrative Policy

7 October 2020 APFF Roundtable Q. 15, 2020-0852271C6 F - Corporate attribution rules

Mr. X and Mrs. X, each owning 50% of the common shares of corporation that is not a small business corporation, effect a s. 51 exchange of their...

27 October 2020 CTF Roundtable Q. 10, 2020-0860961C6 - Refreeze and 74.4(2)

CRA confirmed that where an individual exchanges preferred shares received in the course of a previous estate freeze for newly-issued preferred...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 74.4 - Subsection 74.4(3) | a refreeze does not reduce the outstanding amount | 254 |

11 October 2019 APFF Roundtable Q. 16, 2019-0812751C6 F - 74.4(2) and 120.4 interaction

Mr. X effects an estate freeze in favour of a family trust (entailing a s. 51 exchange by him of his shares of Holdco, which is not a small...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 74.4 - Subsection 74.4(2) - Paragraph 74.4(2)(g) | only s. 74.4(2)(g) provides relief from the joint application of the TOSI and s. 74.4(2) rules | 252 |

6 October 2017 APFF Roundtable Q. 9, 2017-0709071C6 F - Corporate Attribution Rules

As a result of a previous estate freeze, A holds the voting freeze preferred shares of Opco (which is not a small business corporation) and a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 74.5 - Subsection 74.5(5) | unborn children and spouse not designated persons re freezer trust | 231 |

May 2016 Alberta CPA Roundtable, Income Tax Q.9

When asked to comment on factors taken into account in deciding if “one of the main purposes” of a transfer or loan is reasonably considered...

8 December 2015 External T.I. 2015-0613401E5 F - Attribution Rules

1st Situation. Mr. and Ms.X are the sole shareholders of Opco and Holdco, respectively. Opco uses excess liquidity to subscribe for preferred...

11 December 2015 External T.I. 2015-0601561E5 F - Attribution Rules

1st Situation. Mr. X instigates an estate freeze for his corporation (Opco), which is a small business corporation (“SBC”) and all of whose...

2 June 2015 External T.I. 2015-0570071E5 F - Attribution Rules Trust

Result of 1st freeze

Trust A (an inter vivos personal trust) holds all the common shares of Opco (a CCPC but not a small business corporation) and...

10 October 2014 APFF Roundtable Q. 19, 2014-0538041C6 F - 2014 APFF Roundtable, Q. 19 - Stock dividend

Mr. X holds all 100 of Opco's Class A shares with a fair market value of $1,000,000 and nominal ACB and PUC. Opco pays a stock dividend comprising...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1.1) | not engaged if stock dividend is proportional | 211 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(c) | SI apportionment to stock dividend prefs | 251 |

| Tax Topics - Income Tax Regulations - Regulation 6205 - Subsection 6205(2) | purpose test in Reg. 6205(2)(a) is not necessarily accomplished by all estate freezes/"arrangement" broad | 413 |

19 September 2011 External T.I. 2011-0410411E5 F - Attribution - Transfers to Corporations

Holdco's Active Shareholders set up a corporate asset protection structure and introduced certain key employees into the shareholding structure,...

S4-F3-C1 - Price Adjustment Clauses

CRA will consider a price adjustment clause to represent pricing at fair market value if:

- the agreement reflects a bona fide intention of the...

1 April 2003 External T.I. 2003-0004125 F - Freeze by Paying a Stock Dividend

In Situation 1, Mr. A holds all the shares of Opco, being 100 common shares having an FMV of $800,000. Opco declares and pays to Mr. A a stock...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1.1) | s. 15(1.1) inapplicable to stock dividend paid to wholly-owning shareholder | 98 |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(b) | imputed disposition to which s. 69(1)(b) applied where common shares issued at undervaluation to children’s trust | 131 |

| Tax Topics - General Concepts - Effective Date | price-adjustment clause to redemption value of preferred shares did not accord with IT-169 | 183 |

23 October 2001 External T.I. 2001-0096525 F - transfer and loans to corp-attribution rules

Mr. X would exchange all of the common shares of X Inc., which is not a small business corporation, for non-voting preferred shares, and (in...

14 June 2001 External T.I. 2000-0060085 F - Transfert à une société

The minor children become the holders of the non-voting common shares of a Holdco, their parents subscribe for shares of Opco and Holdco acquires,...

1 March 2001 External T.I. 2001-0067725 - 74.4 and estate freezes

Subject to s. 74.4(4), the provisions of s. 74.4(2) will apply to a typical estate freeze whether it utilizes s. 85(1) or s. 86.

7 July 1999 External T.I. 9828165 F - TRANSFERT DE BIENS À UNE SOCIÉTÉ

A person, who has already carried out a partial freeze of a corporation in favour of a trust of which the individual’s children are the...

16 June 1999 External T.I. 9824635 F - TRANSFERT DE BIEN À UNE SOCIÉTÉ

A widower transferred property to a corporation (Holdco) in order to reduce his income and to benefit a discretionary family trust that became a...

28 January 1997 External T.I. 9635055 - attribution under 74.4(2) if 74.1(1) and 74.2(1) apply

"In a situation where subsections 74.1(1) and 74.2(1) of the Act apply to attribute to an individual the income or loss from transferred property...

20 March 1995 External T.I. 9429925 - 74.4(2) AND AMALGAMATION

Where a holding company amalgamates with its operating subsidiary, there will be considered to be a "transfer of property" to the amalgamated...

12 October 1994 External T.I. 9411485 - SECTION 74.4 - SMALL BUSINESS CORPORATION

"Technically the application of subsection 74.4(2) of the Act could change from time to time if a corporation moved from being a small business...

11 May 1994 External T.I. 9130715 - TRANSFER OF PROPERTY RE 74.4(2) AMALGAMATION

Where a corporation ("A") owned by an individual amalgamates with a second corporation ("B") owned by a trust for the benefit of the individual's...

17 February 1994 External T.I. 9401115 - ATTRIBUTION CONTROL CO INVEST IN PREF SHARE OF 2ND CO

S.74.4(2) would not apply where a corporation (as opposed to an individual) transfers or loans property to another corporation unless an...

26 January 1994 External T.I. 9329955 F - Subsections 74.4(2) and 74.5(7) of the Income Tax Act

Where one's spouse guarantees a bank loan made to an investment company owned equally by both spouses, s. 74.5(7) will not permit the interest...

30 March 1993 T.I. (Tax Window, No. 29, p. 23, ¶2454)

There is no provision for a reduction in the amount of attributed income where the income actually earned by the corporation is less than the...

92 C.R. - Q.34

The transferee corporation in s. 74.4(2)(c) is required not only to be a small business corporation at the time of the transfer, but also...

21 August 1992 T.I. (Tax Window, No. 23, p. 24, ¶2154)

Any rights or dividend entitlements attached to preferred shares held by an individual would not by themselves be indicators that a particular...

27 June 1991 Memorandum (Tax Window, No. 4, p. 13, ¶1320)

Discussion of the application of the main purpose test where an individual transfers shares of an operating company to a holding company and those...

11 June 1991 T.I. (Tax Window, No. 4, p. 29, ¶1298)

The fact that the property transferred to the corporation does not produce income (e.g., it is vacant land) may be an indication that the...

2 November 1990 T.I. (Tax Window, Prelim. No. 2, p. 14, ¶1080)

The purpose test in s. 74.4(2) must be applied separately to each transfer of property, with the result that imputed income on a transfer which...

30 January 1990 Memorandum (June 1990 Access Letter, ¶1263)

The receipt by an individual (who some years earlier had effected an estate freeze) of a stock dividend on his preferred shares did not entail a...

ATR-36 (4 Nov. 88)

A favourable ruling is given with respect to an estate freeze involving a trust which will provide that "no amounts will be paid or payable to or...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Shares | 192 | |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | 148 |

86 C.R. - Q.42

A s. 86(1) reorganization always involves a transfer of property (i.e., shares) to a corporation.

Articles

Emes, "Planning for Immigration to Canada from Countries other than the United States", 1993 Corporate Management Tax Conference Report, c. 13.

Discussion of immigrant trusts.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(4.1) | 6 |

Paragraph 74.4(2)(a)

Administrative Policy

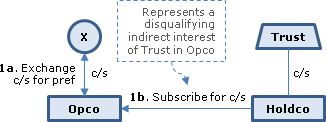

26 November 2021 CTF Roundtable Q. 5, 2021-0911821C6 - Corporate Attribution

A resident individual transfers $100 to Trust (whose beneficiaries include minors, i.e., “designated beneficiaries”), which uses the $100 to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 74.4 - Subsection 74.4(4) - Paragraph 74.4(4)(a) | s. 74.4(4)(a) exception does not apply where the indirect transfer is to a subsidiary of the trust-owned corporation | 145 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Specified Shareholder - Paragraph (e) | beneficiaries of a discretionary trust were specified shareholders of a grandchild trust subsidiary | 55 |

18 July 2006 External T.I. 2005-0162181E5 F - Subsection 74.4(2)

CRA indicated that Ms. B (the common law partner of Mr. A) would be a specified shareholder of Aco (held by her and Mr. A as to 9% and 91% of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Specified Shareholder | 9% shareholder of corporation otherwise held by her spouse becomes a specified shareholder if she wholly-owns a second corporation | 45 |

Paragraph 74.4(2)(f)

Administrative Policy

5 November 1999 External T.I. 9830055 F - DIVIDENDE EN ACTIONS

After noting that a dividend was defined in s. 248(1) to include a stock dividend, CCRA stated:

[F]or the purposes of paragraph 74.4(2)(f), the...

Paragraph 74.4(2)(g)

Administrative Policy

11 October 2019 APFF Roundtable Q. 16, 2019-0812751C6 F - 74.4(2) and 120.4 interaction

CRA rejected the proposition that the main purpose test in s. 74.4(2), and thus the rule itself, should not apply to an estate freeze transaction...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 74.4 - Subsection 74.4(2) | main purpose test can still apply even where designated persons are subject to TOSI | 295 |

Subsection 74.4(3)

Administrative Policy

27 October 2020 CTF Roundtable Q. 10, 2020-0860961C6 - Refreeze and 74.4(2)

An individual exchanges preferred shares received in the course of a previous estate freeze for newly-issued preferred shares with a redemption...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 74.4 - Subsection 74.4(2) | a refreeze does not reduce the quantum of any imputed interest under s. 74.4(2) | 144 |

Articles

Alexander Demner, Nicholas McIsaac, "Freezes and Refreezes: Opportunities and Risks in the Era of Self-Isolation", COVID-19 and Canadian Tax for the Owner-Manager/Canadian Tax Focus (Canadian Tax Foundation), July 2020, p. 5

Technical feasibility of refreeze (p. 6)

[T]he CRA has confirmed that no benefit is conferred on a corporation's common shareholders where the...

Subsection 74.4(4) - Benefit not granted to a designated person

Administrative Policy

2016 Ruling 2014-0552321R3 F - Trust to trust Transfer

A discretionary inter vivos family trust (the “Old Trust”), which was approaching its 21st anniversary, had provisions in its declaration of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition - Paragraph (f) | para. (f) exception applied on transfer from old discretionary inter vivos family trust to new trust with terms considered to be substantively the same | 782 |

| Tax Topics - Income Tax Act - Section 108 - Subsection 108(1) - Trust - Paragraph (g) | trust holding property on its 21st anniversary for minors was not subject to s. 104(4) as their shares would have been deemed under the Trust Deed to be irrevocably determined by then | 413 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(5.8) | 104(5.8) applied to transfer to new trust with the same beneficiaries and essentially the same terms | 51 |

7 November 2014 External T.I. 2014-0549571E5 F - Attribution rule

underline;">: Scenario 1.

{kind=link}

X holds all the common shares of Opco. An inter vivos trust for the minor children of X ("Trust") holds all the common...

30 April 2008 External T.I. 2007-0254311E5 F - Estate Freeze - Attribution Rules

An individual ("Individual") first implemented an estate freeze, whereby his participating shares of Opco were converted into preferred shares,...

8 February 1993 T.I. (Tax Window, No. 29, p. 7, ¶2422)

Where the grandfather of the taxpayer settles a trust of which the taxpayer is a beneficiary, and the taxpayer's father contributes shares of a...

Articles

Manu Kakkar, Alex Ghani, Boris Volfovsky, "Corporate Attribution: Refreeze May Cause Unsolvable Corporate Attribution Problem", Tax for the Owner-Manager, Vol. 18, No. 3, July 2018, p.6

Example of refreeze following a decline in FMV of freeze shares (p. 7)

Mr. X…transfers his common shares of Opco, worth $15 million to Holdco...

Paragraph 74.4(4)(a)

Administrative Policy

26 November 2021 CTF Roundtable Q. 5, 2021-0911821C6 - Corporate Attribution

A resident individual transfers $100 to Trust (whose beneficiaries include minors, i.e., “designated beneficiaries”), which uses the $100 to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 74.4 - Subsection 74.4(2) - Paragraph 74.4(2)(a) | minor beneficiaries of a discretionary trust were specified shareholders of a subsidiary of a corporation held by the trust | 146 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Specified Shareholder - Paragraph (e) | beneficiaries of a discretionary trust were specified shareholders of a grandchild trust subsidiary | 55 |