Subsection 74.5(1) - Transfers for fair market consideration

Administrative Policy

29 April 1994 T.I. 933662 (C.T.O. "Attribution Rules")

Where an individual (the transferee) has acquired an income-producing property from his spouse and given to the transferor a demand promissory...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 74.5 - Subsection 74.5(2) | 107 |

15 June 1992 T.I. 921368 (December 1992 Access Letter, p. 18, ¶C56-208)

No payment will be considered to occur pursuant to an agreement between the parties to the effect that interest on a promissory note will be...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Payment & Receipt | 38 |

Articles

Summerville, "Income Splitting may be Implemented by Transferring Residential Property to Spouse", Taxation of Executive Compensation and Retirement, December 1989/January 1990

In a 24 August 89 Technical Interpretation, RC passed favourably on a transaction whereby a high income spouse transfers to his low income spouse...

Paragraph 74.5(1)(c)

Administrative Policy

23 June 2010 External T.I. 2010-0365581E5 F - Règles d'attribution de l'article 74.2

An individual disposed of capital property to a discretionary trust (whose beneficiaries were the individual and spouse and their children) in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(2) | s. 75(2)(a)(i) is satisfied where a person transferring to a trust holds a capital interest in that trust | 129 |

Subsection 74.5(2) - Loans for value

Administrative Policy

29 April 1994 T.I. 933662 (C.T.O. "Attribution Rules")

Where an individual (the transferee) has acquired an income-producing property from his spouse (the transferor) in consideration for a demand...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 74.5 - Subsection 74.5(1) | 109 |

27 October 2020 CTF Roundtable Q. 11, 2020-0860981C6 - Refinancing Prescribed Rate Loans

An individual, who used a loan ("Loan 1") bearing interest at the prescribed rate (2%) to purchase securities for $100,000, now wishes to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 74.1 - Subsection 74.1(3) | a 1% prescribed-rate loan can effectively replace a 2% loan if the latter loan is repaid with sales proceeds | 193 |

10 June 2013 STEP Canada Roundtable, 2013-0480271C6 - Prescribed Rate Loan - 2013 STEP Roundtable Q 2

Can the interest rate on a loan to a spouse or other family member remain fixed at the current prescribed rate of 1% (so that there is no income...

29 April 1994 External T.I. 9336625 F - Attribution Rules

An individual (the Transferee) acquired an income producing property from the Transferee’s spouse (the Transferor) in consideration for a demand...

21 October 1991 T.I. (Tax Window, No. 12, p. 20, ¶1544)

Where a loan is made on September 30, 1991 with interest payable annually, the exemption will apply only if the interest due on September 30, 1992...

19 July 1989 T.I. (Dec. 89 Access Letter, ¶1047)

No attribution of income will be made in the situation where father loans a newly-established trust with his minor children as beneficiaries the...

79 C.R. - Q.5

Re criteria for a "genuine" loan.

Articles

Michael Goldberg, Vincent Didkovsky, "Refinancing Prescribed-Rate Loans Used for Income Splitting", Canadian Tax Focus, Vol. 10, No. 3, August 2020, p.2

Objective of refinancing loan to take advantage of lower prescribed rate (p. 2)

[M]any practitioners are likely to consider whether loans in...

Paragraph 74.5(2)(b)

Administrative Policy

5 October 2018 APFF Financial Strategies and Instruments Roundtable Q. 10, 2018-0761551C6 F - Attribution rules and promissory note

On June 1, 2018, Mrs. B lent $500,000 to Mr. B at the prescribed rate of interest (2%) and, at the beginning of January 2019, Mr. B issued a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Payment & Receipt | promissory note could not be issued as payment in context of income attribution rules | 83 |

Subsection 74.5(3) - Spouses or common-law partners living apart

Administrative Policy

5 October 2012 Roundtable, 2012-0453201C6 F - Règles d'attribution- séparation & décès

Two common-law partners - within the meaning of s. 248(1) - separated on June 1, 2012 and started living separate and apart because of a breakdown...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 13 - Subsection 13(1) | recapture from rental property is property income from that property | 74 |

24 April 2006 External T.I. 2006-0166041E5 F - Transfert de biens entre époux séparés

In 1991, the spouses jointly purchased an immovable ("Immovable1" located in Canada which was intended to serve as their principal residence upon...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(4) | s. 40(4) feeds principal residence claim of spouse after she acquires the co-ownership interest of her separated husband for $1 | 306 |

88 C.R. - Q.54

RC is aware that the provision may not be workable, because spouses typically are unable to settle the terms of their separation agreement in the...

Paragraph 74.5(3)(a)

Administrative Policy

13 July 2005 External T.I. 2005-0131351E5 F - Séparation des conjoints de fait

Common-law partners (Monsieur and Madame) had a child of their union, and then lived separate and apart starting on April 15, 2004 (with Monsieur...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Common-Law Partner | common-law partnership of couple with a child resumed the moment they resumed living together | 109 |

| Tax Topics - Income Tax Act - Section 74.5 - Subsection 74.5(3) - Paragraph 74.5(3)(b) | capital gain is attributed to transferor common-law partner if the property is sold after they resumed their relationship | 121 |

Paragraph 74.5(3)(b)

Administrative Policy

13 July 2005 External T.I. 2005-0131351E5 F - Séparation des conjoints de fait

Common-law partners (Monsieur and Madame) had a child of their union, and then lived separate and apart starting on April 15, 2004 (with Monsieur...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Common-Law Partner | common-law partnership of couple with a child resumed the moment they resumed living together | 109 |

| Tax Topics - Income Tax Act - Section 74.5 - Subsection 74.5(3) - Paragraph 74.5(3)(a) | attribution resumed when cohabitation resumed | 204 |

27 January 2003 Internal T.I. 2002-0177197 F - ATTRIBUTION DU GAIN A UN CONJOINT SEPARE

On the breakdown of their marriage, a couple held various immovable properties in equal co-ownership. Pursuant to a separation agreement, each...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56.1 - Subsection 56.1(4) - Support Amount | net rental income on property received by separated spouse to fund support was rental income, not a support amount | 94 |

Subsection 74.5(5)

Administrative Policy

6 October 2017 APFF Roundtable Q. 9, 2017-0709071C6 F - Corporate Attribution Rules

As a result of a previous estate freeze, A holds the voting freeze preferred shares of Opco (which is not a small business corporation) and a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 74.4 - Subsection 74.4(2) | a second freeze transaction by a family trust could be viewed as an indirect transfer by the original freezor | 416 |

Subsection 74.5(6)

Administrative Policy

10 June 2003 External T.I. 2003-0018915 F - Attribution - Transfers & Loans to Corp.

An individual transferred all the common shares of Cco (which, at no point, was a small business corporation) in a s. 85(1) rollover to a Newco...

30 October 2002 Internal T.I. 2002-0134077 F - ATTRIBUTION DES GAINS EN CAPITAL

Two individuals transferred the shares they held of a particular company to their respective holding companies which, in turn, each disposed of a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 74.2 - Subsection 74.2(1) | indirect transfer where individuals transfer shares to their Holdcos, who transfer such shares to the individuals’ respective spouses | 122 |

Subsection 74.5(7) - Guarantees

Administrative Policy

86 C.R. - Q.44

RC will apply s. 74.5(7) where a third-party lender requires a spouse to guarantee a loan, except where s. 74.5(11) applies.

Subsection 74.5(11) - Artificial transactions

Cases

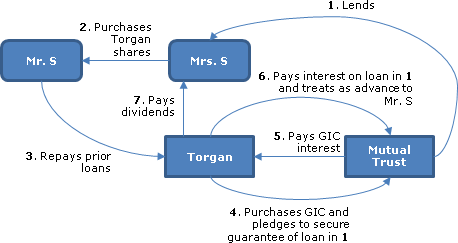

Swirsky v. The Queen, 2013 TCC 73, 2013 DTC 1078 [at at 431], aff'd 2014 FCA 36

{kind=link}

For creditor-proofing reasons, the taxpayer sold shares in a family real estate development company ("Torgan") to his wife, and used the sales...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | 232 | |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 33 |

See Also

Mady v. The Queen, 2017 TCC 112

As a result of a rule change of the Dental College, it was necessary for ownership of all the voting common shares of the professional corporation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Ownership | wife and children did not acquire beneficial interest in shares the taxpayer was to transfer to them, under tax plan, until the share transfer occurred | 263 |

| Tax Topics - Income Tax Act - Section 86 - Subsection 86(2) | family members did not acquire beneficial interest in new shares until after completion of s. 86 reorg | 297 |

| Tax Topics - General Concepts - Fair Market Value - Shares | arm’s length sales price established FMV for closing-date internal transfer of same shares | 482 |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(b) - Subparagraph 69(1)(b)(i) | contemporaneous arm’s length sale price established that shares previously transferred at undervalue | 478 |

| Tax Topics - Income Tax Act - Section 163 - Subsection 163(2) | was not responsible under s. 163(2) for the unbeknownst sharp practice of his tax advisor | 692 |

| Tax Topics - General Concepts - Price Adjustment Clause | no jurisdiction to comment on application of price adjustment clause where the affected taxpayers are not appellants | 233 |

Administrative Policy

24 March 2014 External T.I. 2014-0519661E5 - Subsection 74.5(11) Attribution

A professional who formerly operated an unincorporated professional practice formed a corporation with him and his spouse each subscribing for...

3 May 2001 External T.I. 2001-0069535 F - DEPENSE D'INTERET REGLES D'ATTRIBUTION

A rental apartment building, generating net income after depreciation, was transferred on an s. 73(1) rollover basis for its FMV to the taxpayer's...

Articles

Kevyn Nightingale, "American Professionals in Canada", Canadian Tax Journal, (2017) 65:4, 893-937

Although there may be significant advantages for a Canadian-resident professional to incorporate, challenges arise where the professional (or a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 126 - Subsection 126(1) | 1672 |

Subsection 74.5(12)

Paragraph 74.5(12)(c)

Administrative Policy

23 October 2009 External T.I. 2009-0309861E5 F - Tax-free Savings Accounts

Mr. X makes the only contribution to the TFSA of his wife. After the resulting qualified investment has appreciated, she withdraws all (or a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 143.2 - Subsection 143.2(2) - Paragraph 146.2(2)(c) | contribution by spouse causes cessation as TFSA | 84 |