Subsection 80(2) (old)

Administrative Policy

93 C.P.T.J. - Q.38

Where one corporation (Y) lends $100,000 U.S. to an affiliate (X) at a time that the equivalent Canadian dollar amount is $115,000, and the two...

3 June 1992 Income Tax Severed Letter 9130405 - Intercorporate Debt on Amalgamation

Where on the amalgamation of a debtor corporation and creditor corporation, the creditor corporation was owed a trade debt on which it previously...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Account Receivable | 45 |

Subsection 80(1) - Definitions

See Also

Mitchell v. R., [1996] 2 CTC 2659, 97 DTC 607

The taxpayer, who was the general manager of a corporation ("HSS"), acquired debt of another corporation ("LTM") for consideration that was found...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(14) | 49 | |

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(1) - Paragraph 53(1)(e) - Subparagraph 53(1)(e)(iv) | 115 |

Hanson v. The Queen, 95 DTC 311, [1993] 2 CTC 3125 (TCC)

A promissory note that the taxpayer had given as consideration for a limited partnership interest acquired by him was found to be a legally...

Les aliments Kouri Inc. v. MNR, 93 DTC 35, [1992] 2 CTC 2307 (TCC)

The taxpayer paid a relatively nominal amount to acquire all the shares of a corporation ("Grandiose") having substantial non-capital losses and...

National Trust Co. v. Mead, [1990] 5 WWR 455, [1990] 2 S.C.R. 410

The assumption of a mortgage was found not to entail its novation in light inter alia of a clause in the original mortgage which provided that no...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | assumption of loan did not entail its novation | 204 |

MNR v. Mid-West Abrasive Co. of Canada Ltd., 73 DTC 5429, [1973] CTC 548 (FCTD)

Sweet, D.J. indicated that under an arrangement where a Canadian subsidiary agreed to pay interest "when requested" on advances totalling $210,000...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | contingent interest is not payable in respect of the year | 113 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 76 |

Administrative Policy

2007 Ruling 2007-0245281R3 - windup of income trust on sale of assets:3rd party

In connection with the winding-up of an income fund (the "Fund") after the acquisition of all its units, the Fund disposes of its assets...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(3.3) | capital loss on redemption of trust units following distribution of most of its assets including as capital gains distribution | 110 |

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(2) - Paragraph 53(2)(h) - Subparagraph 53(2)(h)(i.1) | no ACB reduction for capital gains distribution by unit trust to bidco | 86 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(21) | trustees making filings on behalf of terminated fund | 48 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | assumed debt traceable to capital distribution | 97 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(6) | realization and distribution of target MFT gain | 101 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 90 |

9 September 2002 External T.I. 2002-0141005 - Debt forgiveness and capital contribution

Canco, which is indebted to an NRO in an amount greater than the value of its assets, receives a contribution of capital from its non-resident...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 37 | |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 52 |

2 August 1994 External T.I. 9418055 - ECONOMIC DEFEASANCE

S.80 would not apply to a defeasance arrangement under which the debtor is not relieved of its legal obligations under the debt instrument but...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 52 |

5 April 1994 T.I. (C.T.O. "Debtor's Gain on Settlement of Debt")

Non-capital losses arising before an acquisition of control can be utilized under s. 80(1)(a) even though the prospects for such losses otherwise...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 36 |

93 C.R. - Q. 46

Pursuant to s. 80(1)(a), non-capital losses for preceding taxation years will not be reduced where they are not deductible in computing the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 52 |

9 May 1994 Internal T.I. 9409347 - SHARES ISSUED FOR DEBT

Where shares are issued in exchange for indebtedness, and the shares have a lower fair market value, s. 80 will apply to the difference...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 44 |

92 C.R. - Q.18

Where s. 87(7) applies to a winding-up by virtue of s. 88(1)(e.2), s. 88(1) will not apply to an obligation of the subsidiary that is assumed on...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 29 | |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1.1) | 29 |

92 C.M.TC - Q.14

Where a debt owing by a cash-basis farmer including accrued but unpaid interest is settled by a cash payment of less than the full amount owing,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(4) | 57 | |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 57 |

91 CPTJ - Q.2

The acquisition of control of a parent holding an intercompany debt (resulting in the application of s. 111(4)(d)) does not result in the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 28 |

November 1991 Memorandum (Tax Window, No. 13, p. 17, ¶1581)

S.80 can be applied only at the partnership level and cannot be applied to the partners.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 18 |

23 October 1991 Memorandum (Tax Window, No. 12, p. 23, ¶1549)

Accounts receivable arising in the normal course of the business of a taxpayer are not capital property of the taxpayer for purposes of s. 80.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 26 |

11 October 1991 Memorandum (Tax Window, No. 11, p. 22, ¶1518)

Where there has been a forgiveness of debt of the taxpayer before the end of the year that the taxpayer has disposed of all its depreciable...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 85 |

10 July 1991 Decision Summary (Tax Window, No. 5, p. 12, ¶1346)

S.80 will not apply to debt restructurings involving an extension of the time to repay or a change in the method of calculating interest at a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 61 |

26 June 1991 T.I. (Tax Window, No. 4, p. 8, ¶1317)

Where $100,000 is lent to A and B on a joint and severable basis and the debt later is settled for $60,000 paid by A and B in proportion to their...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 89 |

3 December 1990 T.I. (Tax Window, Prelim. No. 2, p. 11, ¶1062)

Where receivables are transferred to the debtor corporation in consideration for treasury shares, s. 80 applies if the fair market value of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 34 | |

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1.1) | 23 |

8 November 1990 T.I. (Tax Window, Prelim. No. 2, p. 10, ¶1046)

Ss.69(1)(a) and 80(1) both will be applied where a creditor accepts low fair market value shares in satisfaction of the debt previously owing to it.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(a) | 27 | |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 27 |

90 C.P.T.J. - Q.5

Where the creditors of a corporation in financial difficulty agree to exchange their debt for common shares of the corporation on the basis of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 56 |

11 June 1990 T.I. (November 1990 Access Letter, ¶1524)

Where a parent corporation sells depreciable property to a wholly-owned subsidiary under a sales agreement, the depreciable property is...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 79 | 79 | |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 79 | |

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(5.1) | 79 |

7 June 1990 T.I. (November 1990 Access Letter, ¶1522)

Where a corporate taxpayer makes a gain on the purchase of its obligation where s. 39(3) does not apply, s. 80 will apply to the gain.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 26 |

10 April 1990 Memorandum (September 1990 Access Letter, ¶1421)

The loss of the right to sue by prescription does not result in the settlement or extinguishment of the debt.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 22 |

30 October 89 T.I. (March 1990 Access Letter, ¶1146)

Because the disposition of money in Canadian currency would not result in a capital gain or a capital loss, money is not a capital property for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Capital Property | 30 | |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 31 |

89 C.M.TC - Q.21

a partnership is a taxpayer for purposes of ss.79 and 80.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 12 |

88 C.R. - Q.14

Where the debts of a partnership have been settled or extinguished, s. 80(1)(a) will not reduce the losses of the partners.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 23 |

87 C.R. - Q.58

On the conversion of an interest-bearing debt into a non-interest bearing debt, the interest-bearing debt will be settled or extinguished on the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 45 |

86 C.R. - Q.60

Generally, S.80 has no effect where the taxpayer has no loss carryforwards or capital property.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 17 |

80 C.R. - Q.38

Re application of s. 80 to the cancellation of debt on the winding-up of a subsidiary.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 17 |

80 C.R. Q.46

S.6(1)(a) generally will prevail over s. 80 when an employee stock-acquisition loan is forgiven.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 16 |

79 C.R. Q.27

Where a shareholder contributes funds to the corporation which in turn are paid to satisfy the debt owing to him, s. 80 may apply. RC is prepared...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 85 |

IT-293R "Debtor's Gain on Settlement of Debt"

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 0 |

IT-382 "Debts Bequeathed or Forgiven on Death"

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 0 |

IT-239R2 "Deductibility of Capital Losses from Guaranteeing Loans for Inadequate Consideration and from Loaning Funds at less than a Reasonable Rate of Interest in Non-arm's Length Circumstances"

Articles

Schafer, "Tax Implications of Restructuring and Refinancing", 1992 Corporate Management Tax Conference Report, c. 4.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 0 |

Wertschek, "Application of a Corporation's Indebtedness to the Issue Price of its Shares Constitutes the Full Payment of the Debt", Corporate Structures and Groups, Vol. 1, No. 2, 1992, p. 16

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 0 |

Frankovic, "Taxing Times: Foreclosures, Default Sales, Debt Forgiveness, Doubtful and Bad Debts", 1991 Canadian Tax Journal, p. 889.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(p) - Subparagraph 20(1)(p)(i) | 0 | |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 0 |

Durand, "Debt Restructuring for Companies in Financial Difficulty", Tax Aspects of Corporate Financing, CCH Seminars, September 13, 1990

Discussion of authorities supporting the proposition that s. 80 does not apply where a taxpayer in financial difficulty issues shares or debt in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 29 |

Brussa, "Strategies for Troubled Times", 1990 Conference Report, c. 17.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 0 |

Flynn, "Restructuring Financially Troubled Corporations", 1989 Conference Report, c. 19.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 0 |

Couzin, "Debt Restructuring", 1986 Corporate Management Tax Conference Report, p. 140.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 0 |

Commercial Debt Obligation

See Also

Genex Communications inc. v. The Queen, 2010 DTC 1064 [at at 2840], 2009 TCC 583, rev'd 2011 DTC 5061 [at 5707], 2010 FCA 353)

Favreau J. found that non-interest bearing shareholder advances to a corporation satisfied paragraph (b) of the definition of "commercial debt...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - French and English Version | 68 |

Administrative Policy

9 April 2014 Internal T.I. 2014-0519231I7 - Debt forgiveness and guarantees

Forco, a wholly-owned subsidiary of Canco, borrowed under a secured "Borrowing" from a lending syndicate, with Canco providing a guarantee"...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | interest on guarantee obligation non-deductible | 153 |

20 May 2014 External T.I. 2013-0516121E5 F - Debt forgiveness

A compromise by Aco under Division I of Part III of the Bankruptcy and Insolvency Act resulted in reassessments owing by Aco for unremitted GST...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(x) - Subparagraph 12(1)(x)(iv) | BIA settlement of GST interest and penalties included under s. 12(1)(x)(iv) | 157 |

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(2.2) | s. 12(1)(x)(iv) inclusion from BIA settlement of GST interest and penalties could be offset against related expense | 157 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(26) | unremitted GST and QST were not obligation "issued" by debtor | 102 |

| Tax Topics - Income Tax Act - Section 9 - Forgiveness of Debt | BIA settlement of unremitted GST on sales was on capital account | 82 |

12 January 2009 External T.I. 2008-0293901E5 F - Article 80

A small business corporation with nominal accumulated profits purchased for cancellation shares in its capital having nominal capital in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) - Subparagraph 20(1)(c)(ii) | indirect use test also applies to the extent of eligible capital attributable to shares repurchased in consideration for debt issuance | 133 |

5 December 2003 External T.I. 2002-0165195 - Debt Forgiveness in Foreign Affiliates

"If a portion of the debt has been used to earn FAPI, and the remainder to earn active business income, we are of the view that the whole debt...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(1) - Paragraph 53(1)(c) | debt forgiveness as contribution to CFA | 100 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 136 | |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(g.1) | 78 | |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Earnings | 63 | |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(2) - Paragraph 5907(2)(f) | forgiveness gain did not relate to active business items | 123 |

1 December 1999 External T.I. 9927575 F - RENONCIATION A UN DIVIDENDE

In concluding that s. 80 would not apply to dividend waivers, CCRA stated:

Section 80 applies to a commercial debt obligation, i.e., a debt the...

Articles

Marie-Andrée Beaudry, Dean Kraus, "Selected Income Tax Considerations in the Court-Approved Debt Restructurings and Liquidations", 2015 Annual CTF Conference paper

Whether forgiven amount arises on settlement of contractual claims (pp. 13:34-13:35)

In addition to the issue of deductibility of claims for...

Debtor

Cases

Metro Can Construction Ltd. v. The Queen, 2000 DTC 6495, 2001 FCA 227

McDonald J.A. accepted the position of the Crown that former s. 80(1) applied, in computing income at the partnership level, to a partnership...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Interpretation Act - Subsection 45(3) | 101 |

See Also

Metro-Can Construction Ltd. v. R., 99 DTC 29, [1999] 2 CTC 2206 (TCC)

Because s. 80 in its pre-1995 form applied at the partnership level rather than the level of the member partners, the forgiveness of debts owing...

Excluded Obligation

See Also

Denthor Developments Ltd. v. The Queen, 97 DTC 667, [1997] 1 CTC 2075 (TCC)

The gain of the taxpayer, which was a land developer, on being discharged pursuant to a settlement agreement of bank indebtedness of $2.2 million...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Forgiveness of Debt | settlement of financing of land inventory on capital account | 59 |

Administrative Policy

10 October 2014 APFF Roundtable Q. 15, 2014-0538151C6 F - 2014 APFF Roundtable, Q. 15 - Section 143.4 & Reverse Earn-out

A newly formed corporation ("Newco") purchases the shares of a target corporation ("Target") for consideration that includes an earn-out clause...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 143.4 - Subsection 143.4(2) | reverse earnout obligation of Buyco re Target shares | 287 |

23 March 2004 External T.I. 2003-0049031E5 F - Paragraphe 15(2) de la Loi et "montant remis"

In connection with finding that if an interest-free loan to the adult child of Opco’s sole shareholder in in 2003 was to be included in the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2) | loan that was anticipated to be forgiven was not a bona fide loan, so that s. 15(2) did not apply | 190 |

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(11) - Investment Contract | loan that was anticipated to be forgiven was not in fact a loan | 122 |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1.21) | inclusion under s. 56(2) avoided second inclusion under s. 15(1.21) | 296 |

29 January 1997 External T.I. 9635975 - PARTNERSHIP TO SOLE PROPRIETOR

"A reduction of the eligible capital expenditure of a taxpayer pursuant to paragraph 14(3)(b) of the Act is a result contemplated by subparagraph...

15 July 2009 External T.I. 2008-0289731E5 - Forgiveness of Accrued Interest

In response to a question whether s. 80 would apply where a creditor waived the right to receive accrued and payable interest on a debt, the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Forgiveness of Debt | purpose and effect of forgiveness | 50 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(2) - Paragraph 80(2)(b) | 197 |

Paragraph (a)

Administrative Policy

20 March 2017 External T.I. 2014-0545591E5 - Upstream Loan and Debt Forgiveness Rules

FA makes a loan to Canco, its wholly-owning parent. Canco then sells its interest in FA to a third party, but due to foreign tax and other...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(9) | potential indefinite application of surplus where upstream loan forgiven after FA sale | 203 |

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(14) | debt forgiveness not a repayment | 56 |

16 May 2005 Internal T.I. 2005-0119061I7 F - Montant d'aide-actions

Prod Co, a wholly owned subsidiary of M Co and a "qualified corporation," produces a Canadian film or video production ("CFVP") at a cost of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(x) - Subpargraph 12(1)(x)(viii) | funding of film production company by shares rather than loan would not give rise to assistance | 181 |

| Tax Topics - Income Tax Act - Section 125.4 - Subsection 125.4(1) - Assistance - Paragraph (a) | conversion of loan that was taxable assistance into shares is not itself assistance] | 192 |

| Tax Topics - Income Tax Regulations - Regulation 1106 - Subsection 1106(1) - Excluded Production - Paragraph (a) - Subparagraph (a)(iii) | transfer of all the revenues to a film implies a transfer of its copyright | 191 |

| Tax Topics - General Concepts - Ownership | transfer of the economic benefit of copyright entails transfer of its ownership | 149 |

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(1) - Paragraph 53(1)(c) | subscription for shares of sub at overvalue constitutes a contribution of capital, generating a s. 53(1)(c) basis bump | 80 |

Forgiven Amount

See Also

Richer v. The Queen, 2009 DTC 1413, 2009 TCC 394

A forgiven amount arose in respect of the indebtedness of the taxpayer for unpaid contribution amounts to a partnership at the time that he...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 163 - Subsection 163(2) | 108 | |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 85 |

Administrative Policy

2020 Ruling 2018-0772291R3 F - Multi-wings split-up net asset butterfly 55(3)(b)

A split-up butterfly of a CCPC distributing corporation (DC) entailed its division between the respective newly-incorporated transferee...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | split-up butterfly of investment co (DC) between three siblings' transferees (TCs) with extinguishment of TC notes on DC wind-up | 399 |

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(1) - Paragraph 186(1)(b) | split-up butterfly that avoids Pt IV tax circularity by a subsequent wind-up of the distributing corporation | 153 |

2016 Ruling 2015-0623731R3 - Subsections 55(2) and (2.1)

Background

As described in 2015-0601441R3, Sub1 and Sub2 (both taxable Canadian corporations and wholly-owned subsidiaries of Parent, a public...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) | requirement to pro-rate PUC | 576 |

| Tax Topics - Income Tax Act - Section 86 - Subsection 86(1) | stated capital of old shares required to be prorated amongst new classes based on relative FMV | 136 |

12 September 2012 Annual CTF Roundtable, 2012-0453381C6 - 2012 CICA Conference

An insolvent (but not bankrupt) company negotiates a settlement with CRA of unpaid source deductions and unremitted GST for less than the balance...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(x) | forgiveness of unremitted GST | 35 |

| Tax Topics - Income Tax Act - Section 9 - Forgiveness of Debt | forgiveness of source deductions on income account | 108 |

28 November 2010 CTF Roundtable, 2010-0387451C6 - Debt forgiveness and Bankruptcy Annulment

IT-293R continues to reflect CRA's view that para. (i) of the definition of "forgiven amount" does not apply in circumstances in which a...

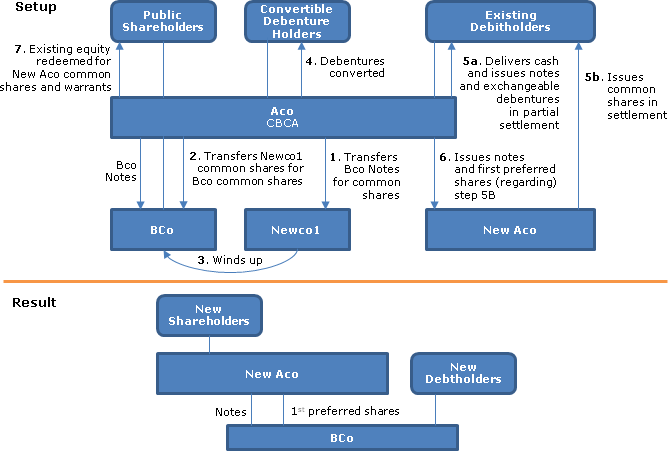

2012 Ruling 2012-0452821R3 - Forgiveness of debt

{kind=link}

Aco is a Canadian public company holding interest-bearing promissory notes (Bco Notes) and shares of a Canadian subsidiary (Bco). Preliminarily...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80.01 - Subsection 80.01(4) | debt elimination through drop-down, transfer and wind-up | 205 |

20 April 2009 Internal T.I. 2008-0302511I7 - LYONS - Open Market Purchase

On an open market purchase of liquid yield option notes ("Lyons"), s. 80 will not apply on the repurchase if s. 39(3) so applies (i.e., there is a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(3) | s. 80 does not apply to open market purchases | 240 |

22 March 2005 Internal T.I. 2005-0115451I7 F - Extinction d'une remise de dette

The creditor forgave a debt pursuant to an agreement with an improved fortunes clause, such that the forgiveness was subsequently cancelled. Is...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80.01 - Subsection 80.01(10) | repayment deduction under s. 80.01(10) | 129 |

| Tax Topics - General Concepts - Effective Date | CRA assesses based on the state of affairs at year end | 103 |

30 April 2004 External T.I. 2004-005753

Respecting the situation where a wholly-owned corporation with an accounting deficit was wound-up pursuant to s. 238(1)(e) of the Business...

5 December 2002 Internal T.I. 2002-0155667 F - DEDUCTIBILITE DES INTERETS CAPITALISEES

In finding that the debt forgiveness rules would not apply to the compound interest component of interest owing on a loan that had been...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) - Subparagraph 20(1)(c)(i) | capitalized simple interest on loan to acquire common shares was deductible if reasonable expectation of dividends | 134 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(2) - Paragraph 80(2)(b) | debt forgiveness rules do not apply to forgiveness of compound interest | 297 |

18 November 1999 Income Tax Severed Letter 9919576 F - REMISE PARTIELLE - 80

CCRA noted that ss. 248(27) and 80 applied at the time of agreeing to a partial debt settlement - rather than only at the time of final payment. ...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(27) | ss. 248(7) and 80 applied at the time of agreeing to a partial debt settlement | 141 |

27 September 1999 Internal T.I. 9916367 F - REMISE DE DETTE/PRET ETUDIANT

A Quebec government program whereby masters or doctoral students had 25% of the loans received by them discharged if they obtained their degree...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(1) - Paragraph 56(1)(n) | partial loan repayments where students achieved their degrees were prizes for achievement | 100 |

19 March 1999 External T.I. 9905095 F - ASSURANCE VIE ET CDC

Regarding the situation where a borrower paid the insurance premiums on a life insurance policy, and the proceeds of the policy were used to repay...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Capital Dividend Account - Paragraph (d) | CDA addition to borrower where life insurance proceeds paid to creditor | 123 |

23 January 1996 External T.I. 9527905 F - ARTICLE 79 ET 80

"Section 79 has priority over section 80 except if paragraph 80.01(8) has applied in a previous year." [Translation]

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 79.1 - Subsection 79.1(6) | 21 | |

| Tax Topics - Income Tax Act - Section 80.01 - Subsection 80.01(8) | 19 |

19 January 1996 External T.I. 9528105 - FORGIVEN AMOUNT - 2ND PARTNERSHIP TIER

Where a corporation that is active in the operations of a particular partnership is not a member of the particular partnership but, instead, is a...

Articles

Janette Pantry, Carrie Smit, "Tax Considerations in Restructuring under the Companies’ Creditors Arrangement Act", draft 2020 CTF Annual Conference paper

Description of reverse vesting transaction (pp. 17-18)

- In a “reverse vesting transaction”, the obligations of the debtor which are to be...

Element B

Paragraph B(a)

Administrative Policy

15 June 2022 STEP Roundtable Q. 5, 2022-0928231C6 - Trust and Debt Forgiveness

A Canadian resident trust makes a loan to a beneficiary, who uses the loan proceeds for investment purposes. Later, the trust distributes the loan...

2016 Ruling 2016-0651621R3 - Partnership carried on by sole proprietor

Immediately before the winding-up of a partnership under s. 98(5), the general partner assumed a debt that was owing to it by the partnership,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 98 - Subsection 98(5) | the assumption by a partner of a debt owing to it by a partnership bumped the partner’s ACB | 198 |

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(1) - Paragraph 53(1)(e) - Subparagraph 53(1)(e)(iv) | ACB increased by assumption of debt owing to partner by partnership | 93 |

13 January 2016 External T.I. 2015-0604521E5 - ACB increase in paragraph 55(3)(a) reorganization

Described steps included the holder of a "Newco note" (Holdco) transferring the Newco note to Newco (the debtor) as a capital contribution or...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) | GAAR may be applied if the transactions produce an outside basis step-up | 423 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | objectionable for a s. 55(3)(a) spin-off to result in an increase in the aggregate outside basis | 173 |

2013 Ruling 2013-0498551R3 - Loss Consolidation

Lossco, an indirect subsidiary of Parent, will make interest-bearing loans to (profitable) Parent, and Parent will subscribe for redeemable...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(1) - Paragraph 111(1)(a) | loss shift to parent/loans to parent used to redeem prefs/no borrowing capacity rep | 64 |

2010 Ruling 2009-0330901R3 - Reorganization of XXXXXXXXXX

A unit trust (Trust 1) purchases for cancellation most of its units held by its parent (Subco) in consideration for the transfer to Subco of debt...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(2) - Paragraph 53(2)(h) - Subparagraph 53(2)(h)(i.1) | no ACB reduction for capital gain distributed to Trust parent on repurchase of most Trust units notwithstanding parent amalgamation before Trust year end | 432 |

| Tax Topics - Income Tax Act - Section 107 - Subsection 107(2.1) | recognition of capital loss on distribution of capital gain through redemption of most of trust units by corporate unitholder | 100 |

23 June 1999 Internal T.I. 9909067 F - GAIN SUR RÈGLEMENT DE DETTE - DATE

The Directorate found that a debt was not settled for purposes of section 80 on the date of its partial discharge in consideration for the...

Paragraph B(i)

Administrative Policy

Income Tax Mandatory Disclosure Rules Consultation: Sample Notifiable Transactions (Finance Release Webpage), 4 February 2022

The notifiable transactions designated by CRA pursuant to draft s. 237.4(3) with the concurrence of Finance include:

Temporary assignment into...

Articles

Janette Pantry, Carrie Smit, "Tax Considerations in Restructuring under the Companies’ Creditors Arrangement Act", draft 2020 CTF Annual Conference paper

Notwithstanding IT-293R, para. 26, there may be no forgiven amount even though debtor’s proposal subsequently approved (pp. 8-9)

- Although under...

Relevant loss balance

Administrative Policy

7 October 2011 APFF Roundtable, 2010-0371941C6 F - Application de l'article 80 - fusion/liquidation

Where following an acquisition of control of a subsidiary, non-capital losses and net capital losses of the subsidiary for taxation years ending...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1.1) - Paragraph 88(1.1)(e) | fiction in s. 80(13) is insufficient to preserve non-capital losses of a subsidiary from a business that ceased following an AOC where subsidiary wound-up and parent has forgiven amount | 354 |

Subsection 80(2) - Application of debt forgiveness rules

Paragraph 80(2)(a)

Cases

Dieni v. The Queen, 2001 DTC 290 (TCC)

The transfer of Quebec real estate by the taxpayer to a lender pursuant to a Deed of Giving In Payment which was executed following an action by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 79 - Subsection 79(2) | 102 |

Wigmar Holdings Ltd. v. R., 97 DTC 5203, [1997] 2 CTC 263 (FCA)

The predecessor of the taxpayer ("Diversified Holdings") purchased, in an arm's length transaction, all the shares of another BC company ("860")....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(5) - Paragraph 111(5)(a) | parking-lot (aka development) business of lossco continued after amalgamation with real estate developer notwithstanding two months between sale of parking lot and amalgamation | 148 |

See Also

Central City Financial Services Ltd. v. R., 98 DTC 1021, [1997] 3 C.T.C. 2949 (TCC), aff'd 98 DTC 6645 (FCA)

A hand-written settlement agreement (whose terms were not clearly described in the reasons for judgment) between the guarantor of debt of the...

Carma Developers Ltd. v. The Queen, 96 DTC 1798, [1996] 3 CTC 2029 (TCC), briefly aff'd 96 DTC 6569 (FCA)

Under a plan that was approved by the requisite majority of creditors in accordance with the companies' Creditors Arrangement Act, various classes...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Subparagraph 212(1)(b)(vii) | 157 |

Administrative Policy

7 October 2022 APFF Roundtable Q. 9, 2022-0942281C6 F - Section 80 - proposals under BIA

Pursuant to a proposal under the Bankruptcy and Insolvency Act, Opco and its creditor agreed to write off $600,000 of its $1 million debt and to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(13) | s. 80(13) tax liability does not arise until the forgiveness | 234 |

26 May 2016 Internal T.I. 2016-0628741I7 - Interaction of s. 80 and s. 143.4

The Taxpayer, which for a number of years had gone without paying interest on its Notes, had a Plan accepted in Year X and implemented in Year X+1...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) - Subparagraph 20(1)(c)(i) | interest only deductible in the year paid or payable | 163 |

| Tax Topics - Income Tax Act - Section 143.4 - Subsection 143.4(1) - Right to reduce | right to reduce notwithstanding that conditions precedent to interest forgiveness not yet satisfied | 329 |

| Tax Topics - Income Tax Act - Section 143.4 - Subsection 143.4(4) | s. 143.4(4) caused an immediate income inclusion of prior years’ interest that was to be forgiven at a later date under an approved Plan of Compromise | 185 |

12 October 2016 Internal T.I. 2016-0637781I7 - Employee loan or debt extinguished or settled

Respecting the situation where an employee debt became statute-barred, and the employer then wrote it off because it was thus no longer legally...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(15) | writing-off a statute-barred debt of an employee or remitting for financial hardship triggers benefit | 244 |

21 November 2014 External T.I. 2014-0535361E5 - Debt forgiveness rules

In the course of a general discussion, CRA stated:

Carma Developers Ltd. v. The Queen, [1996] 3 C.T.C. 2029 (T.C.C.), affirmed at [1997] 2 C.T.C....

8 August 2014 External T.I. 2014-0524951E5 - Debt forgiveness; liability on dissolution

Before going on to note that the debt parking rules in ss. 80.01(6) and (8) would in any event deem the debt to be forgiven, CRA noted that in the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80.01 - Subsection 80.01(8) | s. 50 write-down triggers deemed forgiveness | 160 |

2 August 1994 T.I. 941805

Generally, it is the view of RC that s. 80 does not apply to an economic defeasance arrangement.

4 April 1997 External T.I. 9704365 - APPLICATION OF SECTION 80

"Section 80 would apply where a son repays a commercial debt obligation owing to his father from a gift received immediately before and for the...

Paragraph 80(2)(b)

Administrative Policy

13 June 2011 External T.I. 2011-0393561E5 - Debt forgiveness

In the course of a general discussion, CRA stated:

Paragraph 80(2)(b) of the Act is a deeming clause, and, in essence, it provides that for the...

15 July 2009 External T.I. 2008-0289731E5 - Forgiveness of Accrued Interest

In response to a question as to whether s. 80 would apply where interest is waived and forgiven in the same taxation year in which it was accrued,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) - Excluded Obligation | 62 | |

| Tax Topics - Income Tax Act - Section 9 - Forgiveness of Debt | purpose and effect of forgiveness | 50 |

5 December 2002 Internal T.I. 2002-0155667 F - DEDUCTIBILITE DES INTERETS CAPITALISEES

An employee of a CCPC was lent money by the corporation to acquire common shares of the corporation. In the years thereafter, the employee paid no...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) - Subparagraph 20(1)(c)(i) | capitalized simple interest on loan to acquire common shares was deductible if reasonable expectation of dividends | 134 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) - Forgiven Amount | debt forgiveness rules do not apply to forgiveness of compound interest | 90 |

Articles

Joint Committee, "Summary of Feedback on Various Technical Issues", 14 April 2025 Joint Committee Submission

Failure to refer to interest which is not deductible under s. 18.2(2) (pp. 2-3)

- Interest, which is not deductible under the EIFEL rules, is not...

Paragraph 80(2)(g)

See Also

Pièces automobiles Lecavalier Inc. v. The Queen, 2014 DTC 1126, 2013 TCC 310

Prior to its acquisition by an arm’s length purchaser, the Canadian taxpayer used share subscription proceeds from its US parent to pay a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Evidence | Canadian tax accountant's testimony on US tax consequences accorded little weight | 152 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | debt-paydown transactions were avoidance transactions | 268 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | avoidance of debt forgiveness rules was abusive | 277 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | debt-paydown transactions effected in contemplation of sale transaction were part of same series as the sales transactions | 248 |

Corner Brook Pulp and Paper Limited (Formerly Deer Lake Power Company Limited) v. The Queen, 2006 DTC 2329, 2006 TCC 70

In determining the fair market value of shares issues by a subsidiary ("Deerlake Power"), a power company, to its parent in satisfaction of debt...

King Rentals Ltd. v. The Queen, 96 DTC 1132, [1995] 2 CTC 2612 (TCC)

The pre-1994 version of s. 80 did not apply to the satisfaction of indebtedness of the taxpayer (a New Brunswick corporation) through the issuance...

Administrative Policy

10 March 1999 External T.I. 9829125 - PRICE ADJUSTMENT CLAUSE & 80(2)(G)

Although a price adjustment clause may be used for satisfying the requirements of s. 80(2)(g), "an acceptable price adjustment clause should not...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | 36 |

Paragraph 80(2)(h)

Administrative Policy

28 February 1996 External T.I. 9601795 - FOREIGN EXCHANGE LOSS

Where a debt denominated in U.S. dollars was replaced by a new debt obligation denominated in Canadian dollars whose amount was equivalent to the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(2) | s. 39(2) rather than s. 80 applicable to replacement with C$ obligation | 49 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(2) - Paragraph 80(2)(k) | 49 |

24 May 1995 CICA Roundtable Q. 4, 9512100 - DEBT FORGIVENESS

There is no forgiven amount where one commercial debt obligation is exchanged for another commercial debt obligation having the same principal...

Articles

Marie-Andrée Beaudry, Dean Kraus, "Selected Income Tax Considerations in the Court-Approved Debt Restructurings and Liquidations", 2015 Annual CTF Conference paper

Changes that reduce debt FMV (p. 13:7)

[C]hanges to certain terms of a debt, such as interest rates and payment schedules, should not lead to a...

Paragraph 80(2)(k)

Administrative Policy

2009 Ruling 2009-0313921R3 - Wind-up of creditor into debtor

Ruling that when a Canadian debtor is wound-up into its Canadian parent and an election under s. 80.01(4)(c) is made, then, in light of s....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80.01 - Subsection 80.01(4) | 37 |

28 February 1996 External T.I. 9601795 - FOREIGN EXCHANGE LOSS

Where a debt denominated in U.S. dollars was replaced by a new debt obligation denominated in Canadian dollars whose amount was equivalent to the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(2) | s. 39(2) rather than s. 80 applicable to replacement with C$ obligation | 49 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(2) - Paragraph 80(2)(h) | 49 |

Articles

Carrie Aiken, Johnson Tai, "Debt Restructuring Transactions – Issues, Strategies and Trends", 2016 CTF Annual Conference draft paper

Facts of conversion of DIP financing and USD bonds to equity (pp. 7-8)

Canco has US$1 billion of bonds (the "Bonds") payable to unrelated parties...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(2.02) | 131 | |

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(12) | 151 | |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | 313 |

Didier Fréchette, Ryan Rabinovitch, "Current Issues Involving Foreign Exchange", 2015 CTF Annual Conference paper

Repayment of FX debt with Cdn-dollar note (pp. 26:31-32)

[T]he application of paragraph 80(2)(k) is less straightforward, however, when the debt...

Carrie Smit, "Debt Restructuring and the Falling Canadian Dollar"

No automatic offset of FX loss against forgiven amount on USD debt restructuring (p. 5)

Canadian corporations undergoing debt restructurings of US...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(2) | 138 |

Thomas A. Bauer, "Restructuring Debt Obligations", 2008 Conference Report

Discussion of issues where US dollar debt is settled in Canadian dollars (an issue raised in 1996 Conference Report article by Firoz Ahmed and...

Paragraph 80(2)(o)

Administrative Policy

2 October 1997 External T.I. 9725425 - FORGIVENESS OF ONE JOINT DEBTOR

"Paragraph 80(2)(o) of the Act results in section 80 only applying to the particular person for his proportionate share ... . Section 80 of the...

Subsection 80(3) - Reductions of non-capital losses

Administrative Policy

17 June 2003 External T.I. 2002-0178255 - FORGIVENESS OF DEBT DEBT AFTER AOC+AMALG

The non-capital losses of a subsidiary which amalgamates with its parent would be available to be applied against a forgiven amount arising on the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(2.1) | 92 |

Articles

Joint Committee, "Excessive Interest and Financing Expenses Limitation Proposals", 5 May 2022 Submission of the Joint Committee

S. 80 should be extended to RIFEs

- Restricted interest and financing expenses should be treated similarly to non-capital losses so that, for...

Marie-Andrée Beaudry, Dean Kraus, "Selected Income Tax Considerations in the Court-Approved Debt Restructurings and Liquidations", 2015 Annual CTF Conference paper

Wind-up of subsidiary (Subco) immediately before CCAA compromise to insulate its non-capital losses (“NOLs”) from s. 80 (p. 13:16)

The winding...

Paragraph 80(3)(a)

Administrative Policy

23 May 2012 Internal T.I. 2011-0418071I7 F - Remise de dettes, PAC

After the taxpayer had settled a commercial debt obligation so as to give rise to a forgiven amount, it was assessed by CRA to increase its...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(8) - Non-Capital Loss - D.2 | debt settlement results in immediate application of forgiven amount to reduce NCL at that time | 226 |

Subsection 80(4) - Reductions of capital losses

Administrative Policy

92 C.M.TC - Q.15

S.80(4) would not apply to accrued but unpaid interest for a cash basis farmer, because such interest is not deductible until paid.

92 C.M.TC - Q.14

Where a debt owing by a cash-basis farmer including accrued but unpaid interest is settled by a cash payment of less than the full amount owing,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 57 | |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(5) | 57 |

11 June 1991 T.I. (Tax Window, No. 4, p. 8, ¶1297)

S.80 does not apply to forgiven interest which was not deductible because of the thin capitalization rules.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | 48 |

Articles

Marie-Andrée Beaudry, Dean Kraus, "Selected Income Tax Considerations in the Court-Approved Debt Restructurings and Liquidations", 2015 Annual CTF Conference paper

Generation of net capital losses (NCLs) to absorb forgiven amount (p. 13:11)

Another common tax planning theme…is to trigger any embedded...

Subsection 80(5) - Reductions with respect to depreciable property

See Also

Richer v. The Queen, 2009 DTC 1413, 2009 TCC 394

After finding that various other provisions subsequent to ss.80(3) and (4) applied only if the taxpayer chose to utilize them, Jorré, J. found...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 163 - Subsection 163(2) | 108 | |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) - Forgiven Amount | forgiveness at time of settlement agreement | 118 |

MNR v. Mid-West Abrasive Co. of Canada Ltd., 73 DTC 5429, [1973] CTC 548 (FCTD)

Sweet, D.J. indicated that under an arrangement where a Canadian subsidiary agreed to pay interest "when requested" on advances totalling $210,000...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | contingent interest is not payable in respect of the year | 113 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | indefinite payment arrangements for interest | 76 |

Administrative Policy

2007 Ruling 2007-0245281R3 - windup of income trust on sale of assets:3rd party

In connection with the winding-up of an income fund (the "Fund") after the acquisition of all its units, the Fund disposes of its assets...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(3.3) | capital loss on redemption of trust units following distribution of most of its assets including as capital gains distribution | 110 |

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(2) - Paragraph 53(2)(h) - Subparagraph 53(2)(h)(i.1) | no ACB reduction for capital gains distribution by unit trust to bidco | 86 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(21) | trustees making filings on behalf of terminated fund | 48 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | assumed debt traceable to capital distribution | 97 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(6) | realization and distribution of target MFT gain | 101 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 90 |

5 December 2003 External T.I. 2002-0165195 - Debt Forgiveness in Foreign Affiliates

"If a portion of the debt has been used to earn FAPI, and the remainder to earn active business income, we are of the view that the whole debt...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(1) - Paragraph 53(1)(c) | debt forgiveness as contribution to CFA | 100 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) - Commercial Debt Obligation | hybrid (active business/FAPI) debt is commercial debt obligation | 136 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(g.1) | 78 | |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Earnings | 63 | |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(2) - Paragraph 5907(2)(f) | forgiveness gain did not relate to active business items | 123 |

9 September 2002 External T.I. 2002-0141005 - Debt forgiveness and capital contribution

Canco, which is indebted to an NRO in an amount greater than the value of its assets, receives a contribution of capital from its non-resident...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 37 | |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 52 |

2 August 1994 External T.I. 9418055 - ECONOMIC DEFEASANCE

S.80 would not apply to a defeasance arrangement under which the debtor is not relieved of its legal obligations under the debt instrument but...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 52 |

5 April 1994 T.I. (C.T.O. "Debtor's Gain on Settlement of Debt")

Non-capital losses arising before an acquisition of control can be utilized under s. 80(1)(a) even though the prospects for such losses otherwise...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 36 |

93 C.R. - Q. 46

Pursuant to s. 80(1)(a), non-capital losses for preceding taxation years will not be reduced where they are not deductible in computing the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 52 |

9 May 1994 Internal T.I. 9409347 - SHARES ISSUED FOR DEBT

Where shares are issued in exchange for indebtedness, and the shares have a lower fair market value, s. 80 will apply to the difference...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 44 |

92 C.R. - Q.18

Where s. 87(7) applies to a winding-up by virtue of s. 88(1)(e.2), s. 88(1) will not apply to an obligation of the subsidiary that is assumed on...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 29 | |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1.1) | 29 |

92 C.M.TC - Q.14

Where a debt owing by a cash-basis farmer including accrued but unpaid interest is settled by a cash payment of less than the full amount owing,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 57 | |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(4) | 57 |

91 CPTJ - Q.2

The acquisition of control of a parent holding an intercompany debt (resulting in the application of s. 111(4)(d)) does not result in the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 28 |

November 1991 Memorandum (Tax Window, No. 13, p. 17, ¶1581)

S.80 can be applied only at the partnership level and cannot be applied to the partners.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 18 |

23 October 1991 Memorandum (Tax Window, No. 12, p. 23, ¶1549)

Accounts receivable arising in the normal course of the business of a taxpayer are not capital property of the taxpayer for purposes of s. 80.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 26 |

11 October 1991 Memorandum (Tax Window, No. 11, p. 22, ¶1518)

Where there has been a forgiveness of debt of the taxpayer before the end of the year that the taxpayer has disposed of all its depreciable...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 85 |

10 July 1991 Decision Summary (Tax Window, No. 5, p. 12, ¶1346)

S.80 will not apply to debt restructurings involving an extension of the time to repay or a change in the method of calculating interest at a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 61 |

26 June 1991 T.I. (Tax Window, No. 4, p. 8, ¶1317)

Where $100,000 is lent to A and B on a joint and severable basis and the debt later is settled for $60,000 paid by A and B in proportion to their...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 89 |

3 December 1990 T.I. (Tax Window, Prelim. No. 2, p. 11, ¶1062)

Where receivables are transferred to the debtor corporation in consideration for treasury shares, s. 80 applies if the fair market value of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 34 | |

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1.1) | 23 |

8 November 1990 T.I. (Tax Window, Prelim. No. 2, p. 10, ¶1046)

Ss.69(1)(a) and 80(1) both will be applied where a creditor accepts low fair market value shares in satisfaction of the debt previously owing to it.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(a) | 27 | |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 27 |

90 C.P.T.J. - Q.5

Where the creditors of a corporation in financial difficulty agree to exchange their debt for common shares of the corporation on the basis of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 56 |

11 June 1990 T.I. (November 1990 Access Letter, ¶1524)

Where a parent corporation sells depreciable property to a wholly-owned subsidiary under a sales agreement, the depreciable property is...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 79 | 79 | |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 79 | |

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(5.1) | 79 |

7 June 1990 T.I. (November 1990 Access Letter, ¶1522)

Where a corporate taxpayer makes a gain on the purchase of its obligation where s. 39(3) does not apply, s. 80 will apply to the gain.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 26 |

10 April 1990 Memorandum (September 1990 Access Letter, ¶1421)

The loss of the right to sue by prescription does not result in the settlement or extinguishment of the debt.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 22 |

30 October 89 T.I. (March 1990 Access Letter, ¶1146)

Because the disposition of money in Canadian currency would not result in a capital gain or a capital loss, money is not a capital property for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Capital Property | 30 | |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 31 |

89 C.M.TC - Q.21

a partnership is a taxpayer for purposes of ss.79 and 80.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 12 |

88 C.R. - Q.14

Where the debts of a partnership have been settled or extinguished, s. 80(1)(a) will not reduce the losses of the partners.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 23 |

87 C.R. - Q.58

On the conversion of an interest-bearing debt into a non-interest bearing debt, the interest-bearing debt will be settled or extinguished on the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 45 |

86 C.R. - Q.60

Generally, S.80 has no effect where the taxpayer has no loss carryforwards or capital property.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 17 |

80 C.R. - Q.38

Re application of s. 80 to the cancellation of debt on the winding-up of a subsidiary.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 17 |

80 C.R. Q.46

S.6(1)(a) generally will prevail over s. 80 when an employee stock-acquisition loan is forgiven.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 16 |

79 C.R. Q.27

Where a shareholder contributes funds to the corporation which in turn are paid to satisfy the debt owing to him, s. 80 may apply. RC is prepared...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 85 |

IT-293R "Debtor's Gain on Settlement of Debt"

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 0 |

IT-382 "Debts Bequeathed or Forgiven on Death"

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 0 |

IT-239R2 "Deductibility of Capital Losses from Guaranteeing Loans for Inadequate Consideration and from Loaning Funds at less than a Reasonable Rate of Interest in Non-arm's Length Circumstances"

Articles

Schafer, "Tax Implications of Restructuring and Refinancing", 1992 Corporate Management Tax Conference Report, c. 4.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 0 |

Wertschek, "Application of a Corporation's Indebtedness to the Issue Price of its Shares Constitutes the Full Payment of the Debt", Corporate Structures and Groups, Vol. 1, No. 2, 1992, p. 16

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 0 |

Frankovic, "Taxing Times: Foreclosures, Default Sales, Debt Forgiveness, Doubtful and Bad Debts", 1991 Canadian Tax Journal, p. 889.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(p) - Subparagraph 20(1)(p)(i) | 0 | |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 0 |

Durand, "Debt Restructuring for Companies in Financial Difficulty", Tax Aspects of Corporate Financing, CCH Seminars, September 13, 1990

Discussion of authorities supporting the proposition that s. 80 does not apply where a taxpayer in financial difficulty issues shares or debt in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 29 |

Brussa, "Strategies for Troubled Times", 1990 Conference Report, c. 17.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 0 |

Flynn, "Restructuring Financially Troubled Corporations", 1989 Conference Report, c. 19.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 0 |

Couzin, "Debt Restructuring", 1986 Corporate Management Tax Conference Report, p. 140.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(1) | 0 |

Subsection 80(9) - Reductions of adjusted cost bases of capital properties

Administrative Policy

22 March 2017 External T.I. 2016-0666481E5 - Debt forgiveness in a tiered partnership

A bottom partnership (BP) is wound-up into its partners including an upper-tier partnership (TP) in the same year that BP realizes...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(15) | double application of s. 80(15) and dovetailing with s. 80(9) where lower-tier partnership is wound-up into upper-tier partnership | 351 |

10 January 2011 External T.I. 2010-0371021E5 - Debt forgiveness - 80(9)(a)

Debts issued by a partnership will not be considered to be debts issued by a corporate member of that partnership, provided that there is a bona...

Subsection 80(13) - Income inclusion

See Also

Delta 9 Cannabis Inc (Re), 2025 ABKB 52

A licensed producer of cannabis (“Bio-Tech”) had entered CCAA proceedings. A requested reverse vesting order (RVO) contemplated that an...

GKN Sinter Metals - St. Thomas Ltd. v. The Queen, 2006 DTC 3025, 2006 TCC 248

Before going on to consider the interpretation of regulations pursuant to the debt forgiveness rules that have since been repealed, Paris J....

Administrative Policy

7 October 2022 APFF Roundtable Q. 9, 2022-0942281C6 F - Section 80 - proposals under BIA

Pursuant to a proposal under the Bankruptcy and Insolvency Act, Opco and its creditor agreed to write off $600,000 of its $1 million debt and to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(2) - Paragraph 80(2)(a) | forgiveness under a Bankruptcy proposal occurred when it was court-approved | 203 |

2 September 2009 Internal T.I. 2009-0329251I7 F - Application du paragraphe 80(16)

The forgiveness of a commercial debt obligation that ACO had issued in the course of carrying on its business gave rise under s. 80(13) to income...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(16) | s. 80(16) designation under s. 80(11) increased s. 80(13) income inclusion | 215 |

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(8) - Non-Capital Loss - A | s. 61.3 deduction reduced non-capital loss | 293 |

2 June 2003 External T.I. 2003-0002485 - DEBT FORGIVENESS-GIFT FUND

A farmer transfers farm property to an adult child at fair market value taking back a promissory note as consideration, then makes a gift to his...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 74 |

Articles

Chris Lang, "Debt Restructuring Using a Reverse Vesting Order: Tax Issues", Canadian Tax Focus, Vol.15, No. 2, May 2025, p. 2

Overview of Delta 9 (p. 2)

- In Delta 9, a licensed producer of cannabis (the target corporation) had entered CCAA proceedings.

- A requested reverse...

Marie-Andrée Beaudry, Dean Kraus, "Selected Income Tax Considerations in the Court-Approved Debt Restructurings and Liquidations", 2015 Annual CTF Conference paper

Requirement to use related person’s tax attributes on s. 80.04 designation (p. 13:9)

Further considerations arise when a debtor seeks to make a...

Bernstein, "Update on Debt Forgiveness - Part I", Tax Profile, Vol. 4, No. 25, July 1995, p. 269.

Ahmed, "Debt Forgiveness Rules and Share Purchase Transactions", Canadian Current Tax, March 1995, Vol. 5, No. 6, p. 58.

- The creditor must accept the new debtor as principal debtor and not merely as an agent or guarantor; and

- The creditor must accept the new...

Subsection 80(15)

Administrative Policy

22 March 2017 External T.I. 2016-0666481E5 - Debt forgiveness in a tiered partnership

What is the interaction of ss. 80(9) and (15) where a bottom partnership (the “BP”) in a tiered partnership structure has a forgiven amount in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(9) | on wind-up of lower-tier partnership, ACB bump from its s. 80(13) forgeiveness income is included | 202 |

21 June 2005 Internal T.I. 2005-0120341I7 F - Paragraphe 80(15).

Mr. X was a limited partner of a partnership (LP) that realized a gain on the settlement of a commercial debt obligation, and reduced the forgiven...

Subsection 80(16)

Administrative Policy

2 September 2009 Internal T.I. 2009-0329251I7 F - Application du paragraphe 80(16)

In the particular taxation year, a commercial debt obligation that ACO issued in the course of carrying on its business was forgiven. In addition,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(8) - Non-Capital Loss - A | s. 61.3 deduction reduced non-capital loss | 293 |

| Tax Topics - Income Tax Act - Section 80 - Subsection 80(13) | s. 80(13) income was from the debtor's business | 30 |