Subsection 261(1) - Definitions

See Also

Premier Fasteners Inc. v. The King, 2026 TCC 2

The taxpayer’s revenues had been substantially understated as a result inter alia of not translating sales figures expressed in US dollars or...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(7) | CRA can use the s. 152(7) alternative assessment approach at any time | 175 |

| Tax Topics - Income Tax Act - Section 163 - Subsection 163(2) | taxpayer not providing sufficient resources to support its bookkeeping amounted to gross negligence | 316 |

Canadian Tax Results

Administrative Policy

26 May 2016 IFA Roundtable Q. 3, 2016-0642111C6 - PUC of Shares of a FC Reporter

CRA considered that a Canadian corporation (“Issuer”) which has the U.S. dollar as its elected functional currency nonetheless is required to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(3) | Canadian corporation with a USD functional currency can be subject to Part XIII withholding obligations on its USD prefs resulting from FX fluctuations | 129 |

Elected Functional Currency

Administrative Policy

S5-F4-C1 - Income Tax Reporting Currency

One-time election

1.11 ... A taxpayer need not make an election every year as the language of the requirement described at s. 262(3) is such that,...

Functional Currency

Administrative Policy

S5-F4-C1 - Income Tax Reporting Currency

One-time requirement

...The requirement to have a functional currency need only be met for the first tax year to which the taxpayer intends the...

28 November 2010 Annual CTF Roundtable, 2010-0385891C6 - Functional Currency Tax Reporting - CTF 2010

{kind=link}

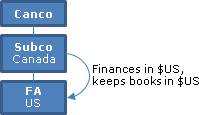

A Canadian public company (Canco), which carries on business primarily in Canada, incorporates Subco to hold its shares of a U.S. controlled...

8 October 2010 Roundtable, 2010-0373651C6 F - Monnaie fonctionnelle - PCGR et NIIF

Is a corporation required to rely on GAAP in interpreting the words "for financial reporting purposes" in the “functional currency”? CRA...

Articles

Eric Bretsen, Heather Kerr, "Tax Planning for Foreign Currency", 2009 Conference Report (CTF), C. 35.

Removal in new definition of principal business and consolidated financial statement requirements (pp. 35:32-33)

The new definition removed the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 261 - Subsection 261(18) | 174 | |

| Tax Topics - Income Tax Act - Section 261 - Subsection 261(20) | 183 |

Qualifying Currency

Finance

29 July 2019 Finance Comfort Letter respecting Functional currency tax reporting - currency of Japan

In response to a submission to this effect, Finance stated:

We agree that it would be appropriate to permit taxpayers to elect to determine their...

Relevant Spot Rate

Administrative Policy

7 October 2022 APFF Financial Strategies and Instruments Roundtable Q. 3, 2022-0943261C6 F - Average Exchange Rate

When and for what length of period is it acceptable to use an average exchange rate? CRA responded:

[F]or purposes of determining a taxpayer's...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(1) - Paragraph 40(1)(a) - Subparagraph 40(1)(a)(i) | use of average exchange rates for capital property dispositions not generally accommodated | 120 |

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(1.1) | use of average exchange rate under s. 39(1.1) is permitted | 36 |

GST/HST Memorandum 3-6 Conversion of Foreign Currency July 2018

ETA s. 159 provides that the consideration for a supply expressed in a foreign currency shall be converted using the exchange rate on the day the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 159 | 675 |

27 April 2017 Internal T.I. 2017-0684831I7 - Changes to relevant spot rate

What will CRA accept as “another rate of exchange that is acceptable to the Minister” under the relevant spot rate definition? CRA...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 261 - Subsection 261(7) | must use Bank of Canada rate on conversion | 110 |

S5-F4-C1 - Income Tax Reporting Currency

Potential CRA acceptance of average rate

1.6 ... [I]t may be possible to use an average exchange rate to convert certain items of income.

10 October 2014 APFF Roundtable Q. 9, 2014-0538631C6 F - 2014 APFF Roundtable, Q. 9 - Currency conversions average foreign exchange rate

When asked to comment on the exchange rate to use for interest, dividends and capital gains, CRA stated, after referring to the reference in the...

Tax Reporting Currency

Administrative Policy

9 March 2016 Internal T.I. 2015-0612501I7 - ITA 261(21) anti-avoidance

CRA considered that s. 261(21) did not apply to deny an FX loss sustained by a Canadian subsidiary (“Holdco”) of a non-resident parent...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 261 - Subsection 261(20) - Paragraph 261(20)(b) | s. 261(21) cannot apply to an FX hedging contract between a Canco which has the Canadian dollar as its functional currency and its parent which uses another currency | 274 |

Subsection 261(2) - Canadian currency requirement

Cases

Ferlaino v. Canada, 2017 FCA 105

The former Director of Taxes at a large Canadian corporation argued unsuccessfully that the computation of his s. 7(1)(a) benefits on exercising...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(1) - Paragraph 7(1)(a) | exercise price of employee stock options should be translated at the exercise-date spot rate | 195 |

Canada v. Agnico-Eagle Mines Limited, 2016 FCA 130

The taxpayer ("Agnico-Eagle") issued US$143M of convertible debentures (the equivalent of Cdn.$230M) and they were mostly converted into shares at...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(2) | conversion of a U.S.-dollar convertible debenture resulted in no FX gain based on the appreciation in the underlying shares | 331 |

Korfage v. The Queen, 2016 TCC 69 (Informal Procedure)

On his retirement from a U.S. employment in September 2000, the taxpayer (a Canadian resident) elected under the terms of his pension plan to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 18 | deduction for U.S. pension income deduction translated at exchange rate for year of receipt | 140 |

See Also

Halwachs v. Agence du revenu du Québec, 2022 QCCQ 5817

The ARQ estimated (and assessed accordingly) unreported income of the taxpayer from offshore investments for his 2008 to 2010 taxation years based...

Agnico-Eagle Mines Limited v. The Queen, 2015 DTC 1008 [at at 43], 2014 TCC 324, aff'd 2016 FCA 130

In 2002, the taxpayer ("Agnico") issued US-dollar denominated debentures which were convertible at the holders' option into common shares at a...

| Other locations for this summary | |

|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(2) | U.S. dollar principal of a convertible debenture should be considered on conversion to have been settled at the historical exchange rate when the conversion price was set |

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Evidence | expert opinion on domestic law excluded | 33 |

Ferlaino v. The Queen, 2016 TCC 105 (Informal Procedure)

Smith J rejected arguments of the taxpayer that the computation of his s. 7(1)(a) benefits on exercising options on the shares of the listed U.S....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(1) - Paragraph 7(1)(a) | exercise price of employee stock options to be translated at the exercise-date spot rate | 215 |

| Tax Topics - Income Tax Act - Section 110 - Subsection 110(1.5) - Paragraph 110(1.5)(a) | purpose of satisfying exercise price test | 278 |

Administrative Policy

S3-F4-C1 - General Discussion of Capital Cost Allowance

Pre-acquisition FX

1.50 ...Generally, the relevant spot rate on the date of acquisition should be used to convert the amount to Canadian dollars....

20 November 2015 External T.I. 2014-0539951E5 - Foreign Currency Denominated Dividends

A U.S.-listed corporation, which has not filed a s. 261(3) election, periodically declares and pays dividends in U.S. dollars. Can it make...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(14) | U.S.-dollar dividends translated at spot rate on payment date | 49 |

24 November CTF Annual Roundtable, Q.10

Where a specified non-resident shareholder of a Canadian corporation (“Canco”) makes a foreign currency loan to Canco, what foreign exchange...

9 October 2015 APFF Financial Strategies and Instruments Roundtable Q. 5, 2015-0588981C6 F - Foreign currency stock market transactions

As CRA considers that shares sold on a stock exchange are disposed of on the settlement rather than trade date, it considers that the U.S. dollar...

10 June 2014 Ministerial Correspondence 2014-0529961M4 - Capital gains on property in foreign currency

On the sale of capital property in foreign currency, the proceeds of disposition are converted using the exchange rate at the time of the sale,...

4 June 2014 External T.I. 2014-0517151E5 - S. 17.1 and debt denominated in foreign currency

A non-resident corporation owes a foreign-currency denominated amount to a CRIC which is a pertinent loan or indebtedness (a "PLOI"), as defined...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 17.1 - Subsection 17.1(1) | prescribed interest on foreign currency PLOI translated at spot rate when loan made | 194 |

14 January 2011 External T.I. 2004-0098601E5 - Foreign currency borrowings and ss 214(7) and (8).

In our view, pursuant to subsection 261(2) of the Act, the discount and yield tests set out in paragraph 214(8)(c) of the Act for a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 214 - Subsection 214(15) | 93 | |

| Tax Topics - Income Tax Act - Section 214 - Subsection 214(7) | FX movements can cause deemed interest | 89 |

| Tax Topics - Income Tax Act - Section 214 - Subsection 214(8) - Paragraph 214(8)(c) | 113 |

Articles

Chris Van Loan, Peter Lee, "Agnico Eagle Mines Limited v. The Queen", International Tax, Wolters Kluwer CCH, No. 80, February 2015, p.1.

Amount paid by Agnico for the extinguishing of its debentures was fond to be U.S.$1,000, being the amount for which the common shares were issued...

Janette Y. Pantry, Soraya M. Jamal, "The Thin Cap Rules: Revisiting the Foreign Exchange Anomaly", Corporate Finance, 2011, p. 1934

Discussion of effect of s. 261(2)(b) on the thin capitalization rule.

Patrick Marley, Amanda Heale, "New Foreign Currency Rules: Are They Functional?", International Tax, CCH, December 2007, No. 37, p. 7.

Paragraph 261(2)(b)

See Also

9189-7397 Québec Inc. v. Agence du revenu du Québec, 2018 QCCQ 4692

On April 29, 2008, the taxpayer (“ST Productions”) entered into a contract with a film producer (“Troublemaker”) to produce special...

Administrative Policy

10 October 2024 APFF Financial Strategies and Instruments Roundtable Q. 2, 2024-1023251C6 F - Use of an average rate for coupons

In the case of foreign-currency denominated stripped coupon, could CRA accept the use of an average exchange rate for the conversion into Canadian...

3 November 2023 APFF Financial Strategies and Instruments Roundtable Q. 10, 2023-0978651C6 - Exchange rate for a stripped interest coupon

Where a taxpayer other than a financial institution holds a stripped coupon denominated in a foreign currency on which interest is deemed to...

3 December 2019 CTF Roundtable Q. 2, 2019-0824381C6 - Foreign taxes paid

CRA indicated that for purposes of claiming the foreign tax credit under s. 126 in situations where the foreign tax is paid at a different time...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 126 - Subsection 126(1) | taxpayers can translate under s. 126 foreign taxes at the exchange rate applied to the related income | 186 |

| Tax Topics - Treaties - Income Tax Conventions - Article 24 | US and UK Treaties do not eliminate FTC requirement that the taxes be paid | 251 |

27 November 2018 CTF Roundtable Q. 14, 2018-0779911C6 - Foreign exchange

What foreign exchange rate is applied to the accrued interest on an FX-denominated debt to which s. 20(14) applies?

CRA indicated that in applying...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(14) | accrued interest translated on transfer date | 53 |

29 September 2007 External T.I. 2006-0204361E5 F - Gain et perte sur change étranger

A trader in U.S. securities used funds in a U.S.-dollar account to purchase the securities, with proceeds being deposited to that account. CRA...

14 January 2000 Internal T.I. 9927897 F - OPERATIONS SUR MARCHE A TERME

Regarding the exchange rate to use for commodity futures transactions carried out in the US, the agency indicated that, consistent with IT-95R,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Commodities, and commodities futures and derivatives | speculator could change from capital treatment to income method for his commodity futures transactions | 156 |

Subsection 261(3) - Application of subsection (5)

Forms

T1296 "Election, or Revocation of an Election, to Report in a Functional Currency"

[F]or tax years that begin after July 12, 2013, the election to...

Subsection 261(5) - Functional currency tax reporting

Paragraph 261(5)(a)

Administrative Policy

15 September 2020 IFA Roundtable Q. 1, 2020-0853411C6 F - IFA 2020 Roundtable – T2057 & Functional Currency

CRA indicated that where the parties to a s. 85 rollover transaction have different tax reporting currencies (as defined in s. 261(1)), it would...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) | dual-currency filing of s. 85 elections where the transferor and transferee have different tax reporting currencies | 87 |

2016 Ruling 2016-0629011R3 - PUC reinstatement under 212.3(9)

A majority of the common shares of a Canadian public corporation (Pubco) were held by foreign holdcos (ultimately controlled by Foreign ‘Parent)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(18) - Paragraph 212.3(18)(c) - Subparagraph 212.3(18)(c)(v) | exclusion where (10)(f) corp on-subscribes proceeds in FA investments | 185 |

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(9) - Paragraph 212.3(9)(b) - Subparagraph 212.3(9)(b)(ii) - Variable A - Clause (b) | PUC restoration where borrowed money dividended up only to the level of a lower-tier CRIC, with cross-border PUC of both lower- and upper-tier CRICs computed both in Cdn$ and U.S.$ where lower-tier CRIC had U.S.$ EFC | 651 |

S5-F4-C1 - Income Tax Reporting Currency

Election not relevant to other tax-payer's results

1.21 ...[I]t is only the Canadian tax results of the taxpayer electing into the functional...

11 July 2013 Internal T.I. 2012-0471111I7 - functional currency

In response to a query as to the basis for CRA's conclusion that s. 261(11)(d ) (which applies only to taxes that are computed "for the particular...

20 September 2012 Internal T.I. 2012-0453071I7 - functional currency

Where Canco (a Canadian resident corportion) has elected a functional currency (i.e. other than the Canadian dollar), it would be permitted to...

Articles

Geoffrey S. Turner, "New and Improved Functional Currency Proposals", International Tax, No. 43, December 2008, p. 1.

Paragraph 261(5)(b)

Administrative Policy

5 May 2021 IFA Roundtable Q. 3, 2021-0888281C6 - IFA 2021 Q.3: 247(3) - C$5 M Threshold & 261(5)

Where a Canadian corporation (“Canco”) with an “elected functional currency” is subject to “transfer pricing income adjustments”...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(3) - Paragraph 247(3)(b) - Subparagraph 247(3)(b)(ii) | C$5M threshold is to be converted on the 1st day of the functional currency company’s taxation year in which the adjustments are made | 210 |

Paragraph 261(5)(c)

Administrative Policy

25 November 2024 External T.I. 2023-0974111E5 - Elected Functional Currency and Expenditure Limit

The “expenditure limit” of Canadian-controlled private corporations for a calendar year (which is gradually reduced as the total of their...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 127 - Subsection 127(10.3) | expenditure limits of associated corporations translated into functional currency at year end | 131 |

31 July 2018 Internal T.I. 2016-0649631I7 - Functional currency - fx gain on refund

Canco, which had elected a qualifying currency as its functional currency, claimed a refund (made in Canadian dollars as required by s. 261(11))...

Subsection 261(6) - Partnerships

Administrative Policy

S5-F4-C1 - Income Tax Reporting Currency

Applies automatically to single-and multi-tier partnerships

1.34 ... [A]lthough the partnership is treated as if it had made a functional currency...

22 April 2013 External T.I. 2012-0471831E5 - Functional currency reporting for partnerships

In response to a query concerning the functional currency reporting requirements for partnerships where a corporate partner has made an election...

Subsection 261(6.1) - Foreign affiliates

Administrative Policy

26 April 2017 IFA Roundtable Q. 4, 2017-0691211C6 - App of s. 261(21) to loan with FA

S. 261(6.1) deems a foreign affiliate, for purposes of computing foreign accrual property income, to have an elected functional currency that is...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 261 - Subsection 261(20) | application of s. 261(21) to deny a hedge of a U.S. dollar loan | 162 |

S5-F4-C1 - Income Tax Reporting Currency

Staggered year ends / FAPI only

1.39 Note that, similar to where a functional currency taxpayer holds an interest in a partnership, it is possible...

Subsection 261(7) - Converting Canadian currency amounts

Administrative Policy

27 April 2017 Internal T.I. 2017-0684831I7 - Changes to relevant spot rate

What exchange rate will CRA permit a taxpayer to use as the “relevant spot rate” as an alternative to the Bank of Canada daily exchange rate?...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 261 - Subsection 261(1) - Relevant Spot Rate | consistent use of Bloomberg, Thomson Reuters or OANDA FX spot rates generally is acceptable | 163 |

S5-F4-C1 - Income Tax Reporting Currency

No discretion to use other than spot rate

1.22 ... Subsection 261(7) provides that ... carried-forward amounts are to be converted from Canadian...

Paragraph 261(7)(h)

Administrative Policy

2 March 2017 External T.I. 2016-0633981E5 - Retained Earnings and Functional Currency Election

Canco’s 2014 financial statements were reported in U.S. dollars (USD) in the consolidated financial statements of its U.S. parent.. Canco made...

20 September 2013 External T.I. 2012-0471261E5 - conversion of CDA into functional currency

How should the capital dividend account of a Canadian corporation ("Canco") be converted from Canadian currency into US dollars, where Canco has a...

Subsection 261(8)

Administrative Policy

S5-F4-C1 - Income Tax Reporting Currency

No netting

1.24 ... [T]here is no provision in section 261 that allows for the netting of amounts payable to, and receivable from, another taxpayer.

Subsection 261(9)

Paragraph 261(9)(a)

Administrative Policy

7 October 2016 APFF Roundtable Q. 17, 2016-0652781C6 F - Functional currency and acquisition of control

Where a taxpayer with an elected functional currency (e.g., the USD) has an accrued FX loss on a debt obligation owing in another foreign currency...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(4) - Paragraph 111(4)(e) | FX gains or losses on pre-transition debts not affected | 229 |

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(10) | exclusion of pre-transition debts | 153 |

Subsection 261(10)

Administrative Policy

S5-F4-C1 - Income Tax Reporting Currency

Overview

1.28 Subsection 261(10) ... causes the accrued income, capital gain, loss or capital loss in respect of a particular pre-transition debt...

Subsection 261(11) - Determination of amounts payable

Administrative Policy

15 May 2019 IFA Roundtable Q. 5, 2019-0798811C6 - Functional currency

Canco, which for all relevant years has filed its returns in U.S. dollars as its functional currency pursuant to an election made under s. 261(3),...

S5-F4-C1 - Income Tax Reporting Currency

Overview

1.53 ... In summary, paragraphs 261(11)(a) and (b) provide the following:

- instalment obligations under paragraph 261(11)(a):

- A...

Paragraph 261(11)(a)

Administrative Policy

21 January 2015 Internal T.I. 2014-0540631I7 - S.261 and loss carryback request

Canco, whose elected functional currency ("EFC") has been the U.S. dollar, deducted non-capital losses from subsequent years in computing its...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 157 - Subsection 157(1) - Paragraph 157(1)(a) | instalment method of a functional currency reporter after loss carryback | 39 |

Subsection 261(12) - Application of subsections (7) and (8) to reversionary years

Administrative Policy

S5-F4-C1 - Income Tax Reporting Currency

Double conversion

1.43 Note that tax attributes that originate in a Canadian currency year of the taxpayer and that are unused at the time of...

13 February 2013 External T.I. 2011-0430921E5 F - S. 261 - Loss carry-back & loss carry-forward

The taxpayer elected in its December 31, 2009 taxation year to adopt the U.S. dollar as its functional currency in accordance with s. 261(2), and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 261 - Subsection 261(15) | carryback of non-capital loss following revocation of functional currency election to functional currency year | 95 |

Subsection 261(14)

Administrative Policy

S5-F4-C1 - Income Tax Reporting Currency

Integration wtih s. 39(2)

1.50 As is the case with subsection 261(10), where subsection 261(14) deems a taxpayer to make a gain or sustain a loss...

Subsection 261(15) - Amounts carried back

Administrative Policy

13 February 2013 External T.I. 2011-0430921E5 F - S. 261 - Loss carry-back & loss carry-forward

The taxpayer elected in its December 31, 2009 taxation year to adopt the U.S. dollar as its functional currency in accordance with s. 261(2), and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 261 - Subsection 261(12) | conversion to U.S. dollar and back again changed non-capital losses | 103 |

Paragraph 261(15)(a)

Administrative Policy

S5-F4-C1 - Income Tax Reporting Currency

Summary of base case

1.57 Paragraph 261(15)(a) applies in situations where the loss year is a functional currency year and the taxpayer wishes to...

Subsection 261(16)

Administrative Policy

S5-F4-C1 - Income Tax Reporting Currency

Summary of base cases

1.61 Where the subsidiary’s tax reporting currency is the Canadian dollar – either because it has never elected into the...

Paragraph 261(16)(a)

Administrative Policy

2023 Ruling 2022-0949841R3 - Loss Consolidation Ruling

CRA ruled on transactions for the transfer of losses by Lossco to Profitco, which entailed transactions to transfer Lossco losses to its new...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(1) - Paragraph 111(1)(a) | triangular transfer of Lossco losses to Newcos which are then annually transferred to Profitco (with a different functional currency) for s. 88(1.1) wind-up | 563 |

Subsection 261(17)

Administrative Policy

S5-F4-C1 - Income Tax Reporting Currency

Alignment with wind-up rules

1.65 Subsection 261(17) is designed to align the tax reporting currency of each predecessor corporation with that of...

Subsection 261(18) - Anti-avoidance

Administrative Policy

S5-F4-C1 - Income Tax Reporting Currency

Avoidance of prohibition

1.69

Example 3

Facts

Canco elects to report its Canadian tax results in U.S. dollars commencing with its 2008 tax...

Articles

Eric Bretsen, Heather Kerr, "Tax Planning for Foreign Currency", 2009 Conference Report (CTF), C. 35.

Carve-out for commerical transactions

Although this provision is now a broadly applicable anti-abuse rule, it contains a dual-step carve-out for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 261 - Subsection 261(1) - Functional Currency | 139 | |

| Tax Topics - Income Tax Act - Section 261 - Subsection 261(20) | 183 |

Subsection 261(20) - Application of subsection (21)

Administrative Policy

26 April 2017 IFA Roundtable Q. 4, 2017-0691211C6 - App of s. 261(21) to loan with FA

S. 261(6.1) deems a foreign affiliate, for purposes of computing foreign accrual property income, to have an elected functional currency that is...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 261 - Subsection 261(6.1) | application of s. 261(21) to upstream USD loan to Cdn$ indirect parent | 146 |

6 December 2011 TEI-CRA Liason Meeting Roundtable Q. 4, 2011-0426981C6 - Functional Currency Reporting

CRA confirmed its position respecting the example (first raised at the May 2011 IFA Roundtable), that where a parent with a Canadian dollar...

Articles

Eric Bretsen, Heather Kerr, "Tax Planning for Foreign Currency", 2009 Conference Report (CTF), C. 35.

Loss denial arising where U.S. commercial paper issued through U.S. sub (pp. 35:42-43)

Canco…uses the Canadian dollar as its functional...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 261 - Subsection 261(1) - Functional Currency | 139 | |

| Tax Topics - Income Tax Act - Section 261 - Subsection 261(18) | 174 |

Paragraph 261(20)(b)

Administrative Policy

25 November 2021 CTF Roundtable Q. 11, 2021-0911941C6 - 261(21), Loan to FA and Excluded Property

S. 261(6.1) deems a foreign affiliate, for purposes of computing foreign accrual property income (FAPI), to have an elected functional currency...

9 March 2016 Internal T.I. 2015-0612501I7 - ITA 261(21) anti-avoidance

In order to hedge a U.S.-dollar Loan made by it to its Canadian subsidiary (Opco, whose tax reporting currency was the U.S. dollar), Opco (whose...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 261 - Subsection 261(1) - Tax Reporting Currency | non-resident parent would have Canadian dollar as tax reporting currency | 80 |

Subsection 261(21) - Income, gain or loss determinations

Administrative Policy

S5-F4-C1 - Income Tax Reporting Currency

Automatic application of loss denial

1.72 ... The rule applies to deny a loss to the taxpayer where the loss can reasonably be considered to be...

2015 Ruling 2014-0561001R3 - Functional currency election

underline;">: CanULC financial reporting. CanULC, is a wholly-owned subsidiary of Pubco (a U.S. public company), which reports its consolidated...

Articles

John Lorito, Trevor O'Brien, "International Finance – Cash Pooling Arrangements", 2014 Conference Report, (Canadian Tax Foundation), 20:1-33

CRA relief where a cash pool head account has no presence in Canada and Canco has elected (p. 24)

Assume Canco…has elected to compute its...