Subsection 212.3(1) - Foreign affiliate dumping — conditions for application

Administrative Policy

28 August 2025 External T.I. 2022-0929921E5 - Application of subsection 212.3(1)

One month after Canco made a $1M loan to its wholly-owned U.S. subsidiary (USco), the individual who wholly-owned Canco ceased to be a resident of...

Articles

Raj Juneja, Pierre Bourgeois, "International Tax Issues That Get in the Way of Doing Business", 2019 Conference Report (Canadian Tax Foundation), 36:1 – 42

FAD rules apply even where no debt dumping or surplus stripping involved

- The foreign affiliate dumping (FAD) rules were intended to target two...

Peter Lee, Paul Stepak, "PE Investments in Canadian Companies", draft 2017 CTF Annual Conference paper

Quaere whether FAD rules apply to a non-s. 87(11) amalgamation (pp. 15-16)

[T]here is no explicit relief for an amalgamation is not described in...

Sabrina Wong, "Summary of International Amendments in Bill C-63, Budget Implementation Act, 2017, No. 2", International Tax (Wolters Kluwer CCH), No. 97, December 2017, p. 6

Uncertainty in September 16, 2016 amendments respecting “other Canadian corporation” (p. 8)

[W]ith respect to the September 16, 2016 proposed...

Philip Halvorson, Dalia Hamdy, "An Overview of the Foreign Affiliate Dumping Rules", (OBA article), 23 February 2016

Purpose of s. 212.3(1)(b)(i) safe harbour (p. 3 at f.n. 7)

The purpose of the safe harbor rule is to reduce impediments to corporate takeovers....

Brett Anderson, Daryl Maduke, "Practical Implementation Issues Arising from the Foreign Affiliate Dumping Rules", 2014 Conference Report, (Canadian Tax Foundation), 19:1-49

{kind=link}

FAD rules apply only to 1st tier FA investments (p. 34)

[A]s a result, certain transactions with similar economic results Can give rise to an...

Ian Bradley, "Living with the Foreign Affiliate Dumping Rules", Canadian Tax Journal (2013) 61:4, 1147-66.

Engagement of rules where investors pool through holding company (p. 1152)

Investments in Canadian corporations are often made by groups of...

Paragraph 212.3(1)(a)

Subparagraph 212.3(1)(a)(ii)

Articles

Dean Kraus, John O’Connor, "Foreign Affiliate Dumping: Selected Issues", 2017 Annual CTF Conference draft paper

Example of application of s. 212.3(1)(a)(ii) to loan made by resident individual’s company to a CFC held by his U.S. brother through a US...

Paragraph 212.3(1)(b)

Articles

Mark Jadd, Daniel Safi, "When a Non-Resident Might Qualify as a “Parent” Under the FAD Rules: A Potential for Retroactive Application?", International Tax Highlights, Vol. 4, No. 1, February 2025, p. 4

Scenario (p. 4)

- A widely-held private corporation resident in Canada (the “CRIC”) will emigrate from Canada for non-tax reasons. However, a...

Joint Committee, "Foreign Affiliate Dumping, Derivative Forward Agreement and Transfer Pricing Amendments Announced in the 2019 Federal Budget", 24 May 2019 Submission of the Joint Committee

- It is understood that the expansion to non-resident controlling individuals or non-arm’s length groups is not aimed principally at CRICs...

Dean Kraus, John O’Connor, "Foreign Affiliate Dumping: Selected Issues", 2017 Annual CTF Conference draft paper

Relevance of partnership agreement to control of corporations held by a limited partnership (p. 10)

[T]he “very capacity to act” [fn 50: Duha...

Peter Lee, Paul Stepak, "PE Investments in Canadian Companies", draft 2017 CTF Annual Conference paper

No s. 245(4) abuse where use of a Canadian GP to avoid FAD rules (pp. 15, 16)

[T]he purpose of the FAD rules is to deter foreign multi-nationals...

Subsection 212.3(12)

Administrative Policy

15 May 2024 IFA Roundtable Q. 5, 2024-1007581C6 - Late-filed PLOI election and reassessment of the affected taxation year(s)

Where a late-filed PLOI election is made prior to the three-year limitation period referred to in s. 15(2.12) or 212.3(12) but no reassessment is...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4) - Paragraph 152(4)(b) - Subparagraph 152(4)(b)(iii) | a late-filing of a PLOI election does not cause the related deemed interest to be statute-barred | 201 |

15 May 2024 IFA Roundtable Q. 4, 2024-1007571C6 - Late-filed PLOI election

S. 15(2.12) or s. 212.3(12) allows for a late filing of a PLOI election by up to three years provided that the late filing penalties are paid by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2.12) | revised procedure for filing late PLOI election under s. 15(2.12) | 156 |

Subsection 212.3(1.1)

Articles

Brett Anderson, Daryl Maduke, "Practical Implementation Issues Arising from the Foreign Affiliate Dumping Rules", 2014 Conference Report, (Canadian Tax Foundation), 19:1-49

PUC offset filing deadline could arise before acquisition of control (p. 19:31)

The policy reasons for implementing a one-year time frame within...

Subsection 212.3(2) - Foreign affiliate dumping — consequences

Commentary

Where the conditions set out in s. 212.3(1) are satisfied, s. 212.3(2) can then apply to deem dividends by the CRIC to its (non-resident) parent...

Administrative Policy

2015 Ruling 2015-0604051R3 - Internal Reorganization

In connection with a s. 55(3)(a) distribution of a Canadian subsidiary (Canco3) to a sister chain of companies held by U.S. parents, s. 212.3(2)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) - Subparagraph 55(3)(a)(iii) | note resulting from share redemption required to be vapourized on amalgamation/GAAR assessment required to reduce outside Canadian basis that US parents “paid for” by paying 5% Canadian withholding tax/rep re pubco share value being unaffected | 899 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(1.11) | s. 55(3)(a) rulings conditional on U.S. parents accepting GAAR assessments to reduce their outside basis | 230 |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1.1) | pro-rata highly dilutive stock dividend | 117 |

28 May 2015 IFA Roundtable Q. 10, 2015-0581641C6 - IFA 2015 Q.10: 111(4)(e) election and 212.3

The taxpayer was a foreign-controlled CRIC. Following the acquisition of control of its non-resident parent, it made a s. 111(4)(e) designation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(10) - Paragraph 212.3(10)(a) | deemed investment under s. 111(4)(e) | 109 |

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(18) - Paragraph 212.3(18)(a) | deemed investment under s. 111(4)(e) | 109 |

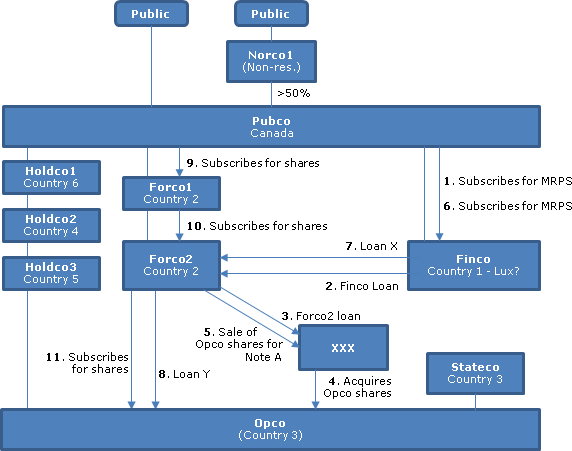

2012 Ruling 2012-0452291R3 - XXXXXXXXXX - ATR

{kind=link}

Existing structure

A Canadian public company (Pubco) has x% (apparently, over 50%) of its common shares held by a non-resident public company...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 17 - Subsection 17(2) | 571 | |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Share | MRPS were shares | 147 |

Articles

Kim Maguire, Jeffrey Shafer, "Trends in Buy/Sell Transactions", draft 2021 Conference Report

Application of FAD rules in exchangeable share structures (p. 8)

- Includes a discussion (at pp. 14-18) of various issues (mostly US other than...

Joint Committee, "Technical Amendments Package of September 16, 2016", Submission letter of 15 November 2016

Expansion of s. 212.3(2)(a) to “other Canadian corporations”

S. 212.3(2)(a) is being expanded to investments other than by a CRIC in its own...

Ian Crosbie, "Recent Transactions of Interest, Part I", 2015 CTF Annual Conference paper

Summary description for acquisition of Yukon target with mostly U.S. assets (“Kodiak”) by U.S. public corp (“Whiting”) (pp....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(c.3) - Subparagraph 88(1)(c.3)(i) | 149 |

Brett Anderson, Daryl Maduke, "Practical Implementation Issues Arising from the Foreign Affiliate Dumping Rules", 2014 Conference Report, (Canadian Tax Foundation), 19:1-49

Two interpretations of subject corporation acquired under earnout agreement: PV all investment obligations at investment time; or succession of...

Ian Bradley, "Living with the Foreign Affiliate Dumping Rules", Canadian Tax Journal (2013) 61:4, 1147-66.

Irreversibility of deemed dividend (p. 1155)

Unlike a PUC reduction, a deemed dividend cannot be reversed at a later date. In fact, withholding...

Subsection 212.3(3) - Dividend substitution election

Commentary

Draft s. 212.3(3) provides for a joint election to be made to allow for all or a portion of a dividend that would otherwise be deemed, under s....

Administrative Policy

2015 Ruling 2014-0541951R3 - Foreign Affiliate Debt Dumping

A U.S. corporation will indirectly subscribe for units in a (presumably U.S.) limited liability partnership (FA1) by subscribing for preferred...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(9) - Paragraph 212.3(9)(b) - Subparagraph 212.3(9)(b)(ii) | s. 212.3(9)(b)(ii) PUC restoration for upper-tier QSCs on the payment by a U.S. LLP of a proportionate “dividend” to lower tier CRIC partners | 349 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Corporation | proportionate distribution by LLP treated as dividend | 128 |

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(2) | proportionate LLP distribution to three direct or indirect general or limited partners treated as dividend on single class of shares | 110 |

23 May 2013 IFA Round Table, Q. 6(h)

In response to a query as to whether a s. 212.3(3) dividend substitution election can be made even if there is no qualified substitute corporation...

Articles

Philip Halvorson, Dalia Hamdy, "An Overview of the Foreign Affiliate Dumping Rules", (OBA article), 23 February 2016

Background to introduction of Foreign-Affiliate Dumping rules (p.2)

[P]art of the Advisory Panel’s mandate was to provide recommendations to...

Subsection 212.3(4) - Qualifying substitute corporation

Cross-Border Class

Commentary

In order for a class of shares of a CRIC or qualifying substitute corporation (QSC) to qualify as a "cross-border class" under the current draft...

Dividend Time

Commentary

The "dividend time" is defined as the investment time, where the CRIC is controlled by the parent at the investment time, and the first to occur...

Articles

Philip Halvorson, Dalia Hamdy, "An Overview of the Foreign Affiliate Dumping Rules", (OBA article), 23 February 2016

Prevention of stuffing by accommodating vendor within 1 year before CRIC acquisition (p. 6)

In the geneal case, one would expect that the...

Qualifying Substitute Corporation

Commentary

A qualifying substitute corporation (QSC) is defined in draft s. 212.3(4) as a Canadian-resident corporation that is controlled by the parent...

Subsection 212.3(5) - Modification of terms — paragraph (10)(e)

Commentary

S. 212.3(5) affects the application of s. 212.3(10)(e), which deems there to be an investment by a corporation resident in Canada (a CRIC) in a...

Subsection 212.3(6)

Articles

Philip Halvorson, Dalia Hamdy, "An Overview of the Foreign Affiliate Dumping Rules", (OBA article), 23 February 2016

Prevention of structured access to 30% intra-Canadian exception (p.5)

[G]iven that the CRIC must be controlled by a non-resident person in the...

Subsection 212.3(7) - Reduction of deemed dividend

Commentary

S. 212.3(7) potentially provides that a dividend which otherwise would be deemed to be paid by a corporation resident in Canada (a CRIC) under s....

Administrative Policy

12 June 2015 External T.I. 2015-0583821E5 - 212.3(7)(d) - Prescribed information

The filing requirements of s. 212.3(7)(d)(i) will be met where a letter (containing the information listed below) is filed by the CRIC with its T2...

Articles

Joint Committee, "Technical Amendments Package of September 16, 2016", Submission letter of 15 November 2016

Penal consequences of not filing

A late-filing dividend under s. 212.3(7)(d) is not eligible for the dividend substitution election under s. 212.3(3)

Brett Anderson, Daryl Maduke, "Practical Implementation Issues Arising from the Foreign Affiliate Dumping Rules", 2014 Conference Report, (Canadian Tax Foundation), 19:1-49

{kind=link}

Potential conflict between NR parent and 3rd party Cdn. investor re application of s. 212.3(7)(a) (p.29)

Figure 16 illustrates an example where...

Paul Barnicke, Nelson Ong, "FA Dumping: PUC Offset", Canadian Tax Highlights, Volume 22, Number 10, October 2014, p. 5.

Retroactive requirement in October 2014 proposals to file form for PUC offset (pp. 5-6)

Under the August 2013 proposals, [the] PUC offset was...

Ian Bradley, "Living with the Foreign Affiliate Dumping Rules", Canadian Tax Journal (2013) 61:4, 1147-66.

Insufficient PUC where deferred purchase price (p. 1156)

Timing issues can also occur if a CRIC purchases foreign affiliate shares and payment of...

Charles Taylor, "Foreign Affiliate Dumping Developments", International Tax, No. 72, October 2013, p. 9

Adverse thin cap impact of automatic grind under s. 212.3(7) (p. 10)

While PUC reduction is generally preferable to a withholding tax cost, there...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(9) | 149 |

Paragraph 212.3(7)(d)

Administrative Policy

4 June 2025 External T.I. 2024-1039701E5 - Subparagraph 212.3(7) and Part XIII

A corporation resident in Canada (the “CRIC”) was deemed by s. 212.3(2)(a) to pay a dividend (the “Initial Dividend”) to its non-resident...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 227 - Subsection 227(10) | there is no need to assess a CRIC whose s. 212.3(7)(d) liability for failure to use its cross-border PUC has been eliminated through a late s. 212.3(7)(d)(i) filing | 282 |

| Tax Topics - Income Tax Act - Section 227 - Subsection 227(8.3) - Paragraph 227(8.3)(b) | s. 227(8.3)(b) interest where late-filing of s. 212.3(7)(d)(i) offset form | 46 |

Subsection 212.3(8) - Paid-up capital adjustment

Commentary

S. 212.3(8) provides for a potential upward adjustment to the paid-up capital of shares where such PUC has been reduced under s. 212.3(2)(b) or s....

Subsection 212.3(9) - Paid-up capital reinstatement

Commentary

Where the PUC of a class or series of shares of a CRIC (or, as discussed further below, qualifying substitute corporation) was reduced under s....

Administrative Policy

22 May 2014 IFA Roundtable Q. 1, 2014-0526691C6 - IFA 2014 - CRIC Guarantees of debt for no fee

{kind=link}

Forco, a controlled foreign affiliate Canco (which in turn is controlled by non-resident Parent, but with a minority of its shares held by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(10) - Paragraph 212.3(10)(b) | imputed benefit from no-fee guarantee | 355 |

23 May 2013 IFA Round Table, Q. 6(b)

The PUC reinstatement rule in s. 212.3(9) applies where the PUC of a CRIC that was previously suppressed is reduced as part of the redemption of...

23 May 2013 IFA Round Table Q. 6(g)

Do internal dispositions give rise to "proceeds" for the purposes of s. 212.3(9)(c)(ii)(A), and does it matter whether the CRIC retains a complete...

Articles

Philip Halvorson, Dalia Hamdy, "An Overview of the Foreign Affiliate Dumping Rules", (OBA article), 23 February 2016

PUC reinstatment rule avoids a double PUC grind or recognizes deployment of proceeds in Canada (p.8)

[A] investment by a foreign-controlled CRIC...

Angelo Nikolakakis, "Foreign Affiliate Dumping – The New Paid-Up Capital Offset and Reinstatement Rules", International Tax (Wolters Kluwer CCH), October 2014 Number 78, p.1.

No requirement to distribute proceeds of investment (p. 4)

As noted above, the new rules would no longer require any distribution of capital in...

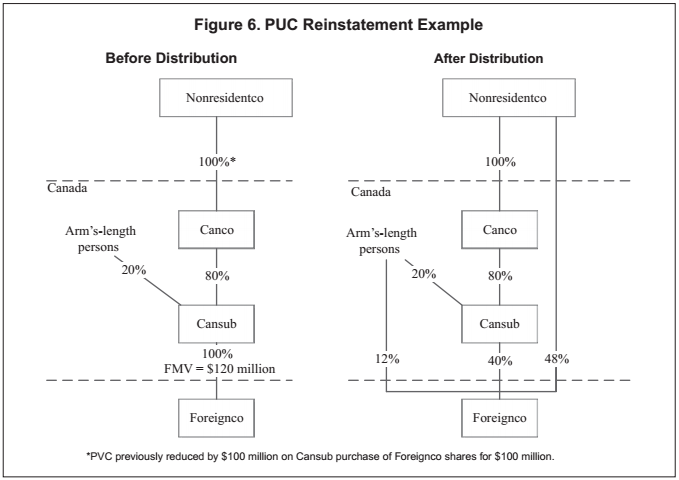

Steve Suarez, "An Analysis of Canada's Latest International Tax Proposals", Tax Notes International, September 29, 2014, p. 1131.

Example of operation of PUC reinstatement rule (p. 1142)

[A] Canadian corporation (Cansub)...originally purchased all of the shares of Foreignco...

{kind=link}

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.1) - Paragraph 212(3.1)(c) | 273 | |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3.1) - Paragraph 212(3.1)(e) | 209 |

Paul Stepak, Eric C. Xiao, "The 88(1)(d) Bump – An Update", 2013 Conference Report (Canadian Tax Foundation), pp.13:1-60

Difficulty in distributing out of a s. 212.3(10)(f) target as a loan repayment rather than PUC distribution (pp. 13:44-45)

{kind=link}

Assume that the final...

Steve Suarez, "Canada's 88(1)(d) Tax Cost Bump: A Guide for Foreign Purchasers", Tax Notes International, December 9, 2013, p. 935

Use of s. 88(1)(d) in buy, bump and sell transactions (p. 937)

The introduction of the foreign affiliate dumping (FAD) rules in 2012 makes the...

Charles Taylor, "Foreign Affiliate Dumping Developments", International Tax, No. 72, October 2013, p. 9

Potential desirability of triggering withholding tax under s. 84(1) (p. 10)

Taxpayers should be sensitive to the potential for double taxation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(7) | 148 |

Henry Chong, "Section 212.3: Missing PUC Adjustments", Canadian Tax Highlights, Vol. 21, No. 5, May 2013, p. 12.

One problem with the PUC reinstatement rules is that a reinstatement applies only to the same class of CRIC or QSC shares that was originally...

Paragraph 212.3(9)(b)

Articles

Joint Committee, "Technical Amendments Package of September 16, 2016", Submission letter of 15 November 2016

Partial reinstatements

The formula in s. 212.3(9)(b)(i) can operate to under-reinstate PUC.

Subparagraph 212.3(9)(b)(ii)

Administrative Policy

15 September 2020 IFA Roundtable Q. 6, 2020-0853561C6 - Subsection 212.3(9) & The GAAR

After March 28, 2012, Canco (wholly-owned by NRco) acquires all the shares of a non-resident corporation (FA1) for $100, thereby effecting a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | circular transactions to effect a s. 212.3(9)(b)(ii) PUC reinstatement abused that provision | 172 |

2015 Ruling 2014-0541951R3 - Foreign Affiliate Debt Dumping

Current structure

Canco1 and Canco2 are wholly-owned subsidiaries of USco5 (a qualifying person under the Canada-U.S. Treaty and an indirect...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Corporation | proportionate distribution by LLP treated as dividend | 128 |

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(2) | proportionate LLP distribution to three direct or indirect general or limited partners treated as dividend on single class of shares | 110 |

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(3) | two Canadian corporate partners immediately beneath the U.S. border are QSCs respecting investments made by lower-tier CRICs in a U.S. LLP | 238 |

Variable A

Clause (b)

Administrative Policy

2016 Ruling 2016-0629011R3 - PUC reinstatement under 212.3(9)

Background

Foreign Parent holds a majority position in Pubco through foreign subsidiaries (Foreign Holdco 2 and Foreign Holdco 1) which, in turn,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(18) - Paragraph 212.3(18)(c) - Subparagraph 212.3(18)(c)(v) | exclusion where (10)(f) corp on-subscribes proceeds in FA investments | 185 |

| Tax Topics - Income Tax Act - Section 261 - Subsection 261(5) - Paragraph 261(5)(a) | cross-border PUC of both lower- and upper-tier CRICs computed both in Cdn$ and U.S.$ where lower-tier CRIC had U.S.$ EFC | 348 |

Subsection 212.3(10) - Investment in subject corporation

Paragraph 212.3(10)(a)

Commentary

S. 212.3(10)(a) provides that an investment in a subject corporation for purposes of the s. 212.3 rules includes an acquisition of shares of the...

Administrative Policy

28 May 2015 IFA Roundtable Q. 10, 2015-0581641C6 - IFA 2015 Q.10: 111(4)(e) election and 212.3

Following the acquisition of control of the non-resident parent of a CRIC, the CRIC made a s. 111(4)(e) designation respecting its 100%...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(18) - Paragraph 212.3(18)(a) | deemed investment under s. 111(4)(e) | 109 |

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(2) | no transfer of property on deemed s. 111(4)(e) acquisition | 155 |

Paragraph 212.3(10)(b)

Commentary

S. 212.3(10)(b) provides that an investment in a subject corporation for purposes of the s. 212.3 rules includes a contribution of capital to the...

See Also

Kraft Heinz Canada ULC v. Canada (Attorney General), 2022 BCSC 796

A B.C. ULC made a cash capital contribution to a Dutch cooperative of which it was the sole member. It was realized four months later that this...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Rectification & Rescission | declaration made by the parties that their contribution was annulled under Dutch law appeared to have retroactive effect | 441 |

Administrative Policy

22 May 2014 IFA Roundtable Q. 1, 2014-0526691C6 - IFA 2014 - CRIC Guarantees of debt for no fee

Forco, a controlled foreign affiliate Canco (which in turn is controlled by non-resident Parent, but with a minority of its shares held by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(9) | reinstatement under s. 212.3(9)(c)(ii)(A)(II) through PUC distributions of dividends | 276 |

Paragraph 212.3(10)(c)

Commentary

S. 212.3(10)(c) provides that an investment in a subject corporation for purposes of the s. 212.3 rules includes a transaction as part of which an...

Administrative Policy

23 May 2013 IFA Round Table Q. 6(f)

- Would the CRA accept FIFO as the method to track the origination and settlement of multiple debts that may arise from inter-company dealings or...

Articles

John Lorito, Trevor O'Brien, "International Finance – Cash Pooling Arrangements", 2014 Conference Report, (Canadian Tax Foundation), 20:1-33

Cash pooling advances in the ordinary course (pp. 19-20)

[I]n…2013-0483751C6, the CRA commented that…the ordinary course of business exception...

Ian Bradley, "Living with the Foreign Affiliate Dumping Rules", Canadian Tax Journal (2013) 61:4, 1147-66.

Group working capital management is problematic (p. 1164)

Multinational groups often optimize their cash management by pooling the excess cash...

Paragraph 212.3(10)(d)

Commentary

S. 212.3(10)(d) provides that an investment in a subject corporation for purposes of the s. 212.3 rules includes an acquisition of a debt...

Paragraph 212.3(10)(e)

Commentary

Overview

S. 212.3(10)(e) provides that an investment in a subject corporation for purposes of the s. 212.3 rules includes an extension of either...

Articles

Ian Bradley, "Living with the Foreign Affiliate Dumping Rules", Canadian Tax Journal (2013) 61:4, 1147-66.

Maturity date extension (p. 1159)

Finance has stated that the policy objective of this rule is to treat a term extension as a repayment and...

Paragraph 212.3(10)(f)

Commentary

Overview

In the absence of s. 212.3(10)(f), investments engaging the s. 212.3 rules would be restricted to direct investments (as broadly defined...

Administrative Policy

23 May 2013 IFA Round Table Q. 6(a)

Does CRA consider that the original version of s. 212.3(10)(f) (for transactions before August 14, 2012) capture the indirect acquisition of...

Articles

Raj Juneja, Pierre Bourgeois, "International Tax Issues That Get in the Way of Doing Business", 2019 Conference Report (Canadian Tax Foundation), 36:1 – 42

S. 212.3(10)(f) can encourage bump and run transactions

The structure resulting where a Canadian public corporation, that has no operations in...

Brett Anderson, Daryl Maduke, "Practical Implementation Issues Arising from the Foreign Affiliate Dumping Rules", draft 2014 Annual CTF Coference Report paper.

Exclusion from bad assets of debt receivable from subject corporation (p.8)

[P]arent owns all of the issued and outstanding shares of the CRIC and...

Paragraph 212.3(10)(g)

Commentary

S. 212.3(10)(g) provides that an investment for purposes of s. 212.3 includes an acquisition by a CRIC of an option or interest in (or, under...

Subsection 212.3(11) - Pertinent loan or indebtedness

Commentary

Ss. 212.3(10)(c)(ii), 212.3(10)(d)(ii) and 212.3(10)(e)(i) indicate that an investment in a subject corporation by a CRIC does not include: a loan...

Administrative Policy

Notice to Tax Professionals: Updates to filing process for a pertinent loan or indebtedness election, 25 March 2022

Where a pertinent loan or indebtedness (PLOI) election is made under s. 15(2.11) or 212.3(11) respecting an amount owing by a corporation resident...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2.11) | 605 |

23 May 2013 IFA Round Table Q. 6(c)

Will CRA permit a blanket PLOI election (specifying that it is being made for each debt owing from the particular debtor to the particular...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2.11) | blanket PLOI election | 96 |

Articles

Philip Halvorson, Dalia Hamdy, "An Overview of the Foreign Affiliate Dumping Rules", (OBA article), 23 February 2016

Activation of dead asset under PLOI rules (p. 7)

[T]he FAD Rules are based on the presumption that an investment by a foreign-controlled CRIC in a...

Ian Bradley, "Living with the Foreign Affiliate Dumping Rules", Canadian Tax Journal (2013) 61:4, 1147-66.

PLOI elections impracticable where cash pooling (p. 1166)

The PLOI filing obligations may cause practical difficulties in the context of the...

Paragraph 212.3(11)(c)

Administrative Policy

15 May 2024 IFA Roundtable Q. 6, 2024-1007591C6 - PLOI Election Administrative Relief

Effective March 25, 2022, CRA adopted an administrative policy that requires only one PLOI election to be made in respect of each loan or...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2.11) - Paragraph 15(2.11)(d) | CRA effectively indicates that to disengage a single PLOI election, the loan agreement must be replaced | 246 |

Subsection 212.3(13)

Administrative Policy

26 May 2016 IFA Roundtable Q. 11, 2016-0642031C6 - PLOI late-filed penalties

Where a corporation resident in Canada wishes to make PLOI elections respecting intercompany balances resulting from hundreds of intercompany...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2.13) | potential administrative relief on computing late-filed PLOI election penalties on a debit-by-debit basis | 244 |

Subsection 212.3(14) - Rules for paragraph (10)(f)

Paragraph 212.3(14)(a)

Articles

Brett Anderson, Daryl Maduke, "Practical Implementation Issues Arising from the Foreign Affiliate Dumping Rules", 2014 Conference Report, (Canadian Tax Foundation), 19:1-49

Example of "hollowing out" transaction: subsequent sale of good assets by subject corp. (p. 10)

The explanatory notes issued by Finance with...

Subsection 212.3(15) - Control

Commentary

S. 212.3(15) alters the usual rules for determining control, for the purposes of s. 212.3 and for purposes of the corporate immigration rule in s....

Articles

Ian Bradley, "Living with the Foreign Affiliate Dumping Rules", Canadian Tax Journal (2013) 61:4, 1147-66.

Deemed control acquisition on acquisition by indirect controller (p. 1154)

…For Example, one non-resident corporation ("NR 1") owns another...

Subsection 212.3(16) - Exception — more closely connected business activities

Administrative Policy

2 April 2026 External T.I. 2021-0917901E5 - Application of subsection 212.3(16)

A US-resident public company (US Pubco) wholly owns US Holdco, which in turn wholly owned USCo, as well as Canco, which has foreign subsidiaries....

Articles

Raj Juneja, Pierre Bourgeois, "International Tax Issues That Get in the Way of Doing Business", 2019 Conference Report (Canadian Tax Foundation), 36:1 – 42

Exception unavailable where CRIC has no Cdn business

- It is unclear why it is necessary to meet all of the requirements of the s. 212.3(16)...

Joint Committee, "Foreign Affiliate Dumping, Derivative Forward Agreement and Transfer Pricing Amendments Announced in the 2019 Federal Budget", 24 May 2019 Submission of the Joint Committee

- Given the practical infeasibility of complying with the “more closely connected business” (“MCCB”) exception, a replacement relieving...

Paragraph 212.3(16)(a)

Commentary

S. 212.3(16) provides an exception from the application of the foreign affiliate dumping rules to an investment by a CRIC in a subject corporation...

Administrative Policy

6 September 2013 External T.I. 2013-0474671E5 - "more closely connected business activities"

{kind=link}

Canco, which carries on a Canadian active business and is a wholy-owned subsidiary of NR Parent, subscribes for shares of US Holdco (a...

23 May 2013 IFA Round Table Q. 6(d)

If a subject corporation carries on an active business related to the CRIC's Canadian business (e.g. local distributor of goods manufactured by...

Articles

Philip Halvorson, Dalia Hamdy, "An Overview of the Foreign Affiliate Dumping Rules", (OBA article), 23 February 2016

More closely-connected test for investments that otherwise would have been made (p. 8)

This first exception is intended to allow a Canadian...

Paragraph 212.3(16)(b)

Commentary

Ss. 212.3(16)(a) to (c) specify conditions which must all be satisfied in order for s. 212.3(16) to provide an exception from the application of...

Articles

Tim Barrett, Andrew Morreale, "Foreign Affiliate Update", 2019 Conference Report (Canadian Tax Foundation), 35: 1 – 53

Inapplicability of s. 212.3(16) safe harbor for CRIC wholly-owned by individual entrepreneur

- Since “parent” under the expanded FAD rules can...

Peter Lee, Paul Stepak, "PE Investments in Canadian Companies", draft 2017 CTF Annual Conference paper

Scope of requirement for exercise of principal decision-making authority under more closely connected business (MCCB) activities exception...

Paragraph 212.3(16)(c)

Commentary

Ss. 212.3(16)(a), 212.3(16) (b), 212.3(16) (c)(i), 212.3(16) (c)(ii) and 212.3(16)(c)(iii) specify five conditions which must all be satisfied in...

Subsection 212.3(17) - Dual officers

Commentary

S. 212.3(17) is ancillary to the tests in ss. 212.3(16)(b) and (c), which require a majority of the officers of a CRIC - or (under draft...

Subsection 212.3(18) - Exception — corporate reorganizations

Articles

Joint Committee, "Technical Amendments Package of September 16, 2016", Submission letter of 15 November 2016

Effect on look-through rule interpretation

The addition of s. 212.3(18)(b)(viii) may imply that a broader range of transfers are not capable of...

Paragraph 212.3(18)(a)

Commentary

S. 212.3(18) of the Act provides exceptions from the application of the foreign affiliate dumping rules in s. 212.3 for various forms of corporate...

Administrative Policy

28 May 2015 IFA Roundtable Q. 10, 2015-0581641C6 - IFA 2015 Q.10: 111(4)(e) election and 212.3

Following the acquisition of control of the non-resident parent of a CRIC, the CRIC made a s. 111(4)(e) designation respecting its 100%...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(10) - Paragraph 212.3(10)(a) | deemed investment under s. 111(4)(e) | 109 |

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(2) | no transfer of property on deemed s. 111(4)(e) acquisition | 155 |

Finance

{kind=link}

Articles

Philip Halvorson, Dalia Hamdy, "An Overview of the Foreign Affiliate Dumping Rules", (OBA article), 23 February 2016

Purpose of s. 212.3(18) exceptions (p. 9)

[T]hese exceptions are generally intended to prevent the application of the FAD rules when there is no...

Finance

Subparagraph 212.3(18)(a)(i)

Articles

Dean Kraus, John O’Connor, "Foreign Affiliate Dumping: Selected Issues", 2017 Annual CTF Conference draft paper

Failure of drop-down by Amalco (resulting from Buyco and Canadian target) to subsidiary of target to satisfy s. 212.3(18)(a)(i) (pp. 18-19)

[A]...

Subparagraph 212.3(18)(a)(ii)

Clause 212.3(18)(a)(ii)(B)

Articles

Peter Lee, Paul Stepak, "PE Investments in Canadian Companies", draft 2017 CTF Annual Conference paper

No relief for a non-s. 87(11) amalgamation of Acquireco, Target and Target subs (p. 15)

[T]here is no explicit relief for an amalgamation is not...

Paragraph 212.3(18)(b)

Commentary

Listed exceptions

S. 212.3(18)(b) provides in a listed set of circumstances (relating to share-for-share transactions at the foreign affiliate...

Paragraph 212.3(18)(c)

Commentary

Exclusion for related party acquisitions of shares of other corporation

S. 212.3(18)(c)(i) provides that s. 212.3(2) (including, by implication,...

Administrative Policy

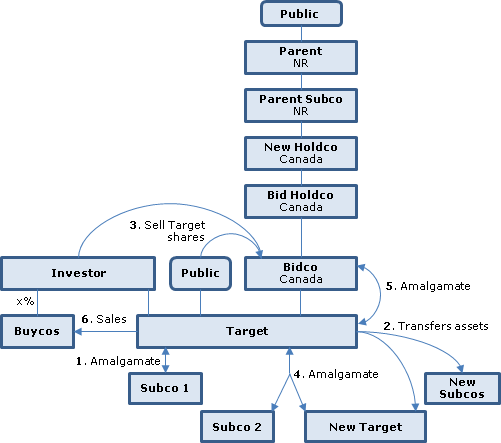

2012 Ruling 2012-0451421R3 - Purchase of Target and bump

{kind=link}

After giving effect to preliminary transactions relating to the Bidco structure:

- a non-resident public company (Parent) is the sole shareholder...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(c.3) - Subparagraph 88(1)(c.3)(i) | guarantee | 32 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(4) - Paragraph 88(4)(b) | Target Amalco 2 formed post-AOC and pre-bump (occurring on amalgamation of Target Amalco 2 with Bidco) is a continuation its predecessors for s. 88(1)(c) midamble purposes/prepackaging transactions before formation of Target Amalco 2/Target asset buyers agree not to purchase Target shares | 995 |

Articles

Philip Halvorson, Dalia Hamdy, "An Overview of the Foreign Affiliate Dumping Rules", (OBA article), 23 February 2016

Supplemented by anti-stuffing meansures (p. 10)

[S]imilar to the rules in paragraph 212.3(18)(a), paragraph 212.3(18)(c) also contains various...

Subparagraph 212.3(18)(c)(ii)

Articles

Joint Committee, "Foreign Affiliate Dumping, Derivative Forward Agreement and Transfer Pricing Amendments Announced in the 2019 Federal Budget", 24 May 2019 Submission of the Joint Committee

- An example of the (likely, many) anomalies that will occur in the operation of the reorganization rules if the scope of the s. 212.3(1) scoping...

Subparagraph 212.3(18)(c)(v)

Administrative Policy

2016 Ruling 2016-0629011R3 - PUC reinstatement under 212.3(9)

Foreign Parent holds a majority position in Pubco indirectly including through Canholdco 2 and Canholdco 1. Pubco is a public corporation that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.3 - Subsection 212.3(9) - Paragraph 212.3(9)(b) - Subparagraph 212.3(9)(b)(ii) - Variable A - Clause (b) | PUC restoration where borrowed money dividended up only to the level of a lower-tier CRIC, with cross-border PUC of both lower- and upper-tier CRICs computed both in Cdn$ and U.S.$ where lower-tier CRIC had U.S.$ EFC | 651 |

| Tax Topics - Income Tax Act - Section 261 - Subsection 261(5) - Paragraph 261(5)(a) | cross-border PUC of both lower- and upper-tier CRICs computed both in Cdn$ and U.S.$ where lower-tier CRIC had U.S.$ EFC | 348 |

Paragraph 212.3(18)(d)

Commentary

S. 212.3(18)(d) provides that s. 212.3(2) (including, by implication, the paid-up capital grind rule in s. 212.3(7)) does not apply to a direct...

Subsection 212.3(18.1)

Commentary

Draft s. 212.3(18.1) provides that the exceptions in s. 212.3(18), which otherwise can apply to stop s. 212.3(2) from applying to various forms of...

Articles

Philip Halvorson, Dalia Hamdy, "An Overview of the Foreign Affiliate Dumping Rules", (OBA article), 23 February 2016

Avoidance of misuse of PLOI exception (p. 10)

Subsection 212.3(18.1)…would prevent a CRIC from first acquiring a debt that was a PLOI (which...

Subsection 212.3(19) - Preferred shares

Commentary

S. 212.3(19) provides that the exceptions in ss. 212.3(16) and 212.3(18)(b) and (d) to the application of s. 212.3(2) do not apply to a CRIC's...

Articles

Philip Halvorson, Dalia Hamdy, "An Overview of the Foreign Affiliate Dumping Rules", (OBA article), 23 February 2016

Preferred share exception (p. 10)

Subsection 212.3(19) overrides the bona fide business exception or the internal reorganization exception on an...

Brett Anderson, Daryl Maduke, "Practical Implementation Issues Arising from the Foreign Affiliate Dumping Rules", 2014 Conference Report, (Canadian Tax Foundation), 19:1-49

s. 212.3(19) can extend to common shares (p. 16)

[C]ommon shares may also be caught if their participation rights are contractually restricted by...

Subsection 212.3(20) - Assumption of debt on liquidation or distribution

Commentary

S. 212.3(20) provides that the rules in ss. 212.3(18)(b)(v) to (vii) – which otherwise except certain types of reorganizations involving foreign...

Subsection 212.3(21) - Persons deemed not to be related

Commentary

S. 212.3(21) deems persons to be unrelated for the purposes of the reorganization exceptions in subsection 212.3(18) if it can reasonably be...

Subsection 212.3(22) - Mergers

Commentary

Continuation/no-acquisition

S. 212.3(22)(a)(i) provides for purposes of s. 212.3 and 219.1(3) and (4) that the "new" corporation resulting from a...

Subsection 212.3(23) - Indirect investment

Commentary

S. 212.3(23) applies to deny the exemption from the application of s. 212.3(2) which otherwise would apply under s. 212.3(16) to an investment by...

Subsection 212.3(24) - Indirect funding

Commentary

Object

The availability of the exemption in s. 212.3(16), from the application of s. 212.3(2) to an investment by a CRIC in a subject corporation,...

Subsection 212.3(25) - Partnerships

Paragraph 212.3(25)(a)

Commentary

S.212.3(25) provides "look-through" rules for the application of the foreign affiliate dumping rules to partnerships. These rules also apply for...

Paragraph 212.3(25)(b)

Commentary

S. 212.3(25)(b) deems (for the various purposes discussed above in relation to s. 212.3(25)(a)) partnership property to be owned by each partner...

Administrative Policy

2013 Ruling 2013-0491061R3 - Upstream Loans

{kind=link}

Non-resident subsidiaries (perhaps resident in the US) of a non-resident public company ("Parent") hold stacked non-resident companies (FA 1 to 4...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 90 - Subsection 90(8) - Paragraph 90(8)(a) | yo-yo transaction: US Salesco is repaid upstream loan by Can Opco 1, and then relends to Can Opco 1 when no longer a parent | 419 |

Articles

Ian Bradley, "Living with the Foreign Affiliate Dumping Rules", Canadian Tax Journal (2013) 61:4, 1147-66.

Control by general partner (pp. 1152-3)

[P]aragraph 212.3(25)(b)…suggests that when applying the control test in subsection 212.3(1), CRIC...

Paragraph 212.3(25)(c)

Commentary

S. 212.3(25)(a) addresses activities, such as investments in subject corporations, effected at the level of the partnership and does not address...

Paragraph 212.3(25)(d)

Commentary

For the purposes of s. 212.3 and other specified sections, s. 212.3(25)(d) deems an amount owing by a partnership to instead be owed by each...

Paragraph 212.3(25)(e)

Commentary

S. 212.3(25)(e) curtails the scope of s. 212.3(25)(a) by providing that it does not apply to the extent of transactions between a partner and the...

Paragraph 212.3(25)(f)

Commentary

S. 212.3(25)(f) deems a person or partnership that is (or is deemed under that paragraph to be) a member of a particular partnership, that itself...

Subsection 212.3(26)

Articles

Henry Shew, "Foreign Affiliate Dumping and Estates with Non-Resident Beneficiaries", Canadian Tax Focus, Vol. 10, No. 1, February 2020, p.9

Example of application of FAD rules to estate with NR beneficiary before considering potential “outs” (p. 9)

[D]eceased (Dad) wholly owns a...

Joint Committee, "Foreign Affiliate Dumping, Derivative Forward Agreement and Transfer Pricing Amendments Announced in the 2019 Federal Budget", 24 May 2019 Submission of the Joint Committee

- The existing s. 212.3(16) exception is simply unworkable where the deemed “controlling” person is a trust beneficiary. In addition, s....

Paragraph 212.3(26)(b)

Articles

Tim Barrett, Andrew Morreale, "Foreign Affiliate Update", 2019 Conference Report (Canadian Tax Foundation), 35: 1 – 53

Quaere whether discretionary trust interests have a nil FMV

- For the purposes of determining the ownership of shares of a corporation...

Commentary

References, in the discussion below of the foreign affiliate dumping rules in s. 212.3, to draft provisions refer to draft legislation released by...