{kind=link}

{kind=link}

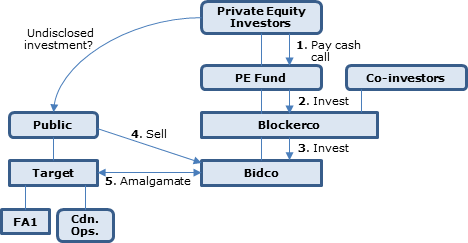

Sequencing of steps (p. 13:35)

The steps set out in the plan generally include the repayment of historic Target debt, the cash-out or rollover of...

Parent relatedness to mooted specifed person from moment of its incorporation if not a shelf corp. (p. 13:22-23)

[A]t the time the parent is...

Remedying under s. 88(1)(d)(c.2)(iii)(A.2) of pre-winding-up agreement for sale of bumped shares

[P]rior to the [s. 88(1)(d)(c.2)(iii)(A.2)]...

{kind=link}

10% attributable property test applied only during the series of transactions (p. 13:12-13)

[W]hen read in a textual, contextual and purposive...

Is debt of Target non-specified property after it is amalgamated with Bidco? (pp. 13:16-19)

On a literal reading of old paragraph 88(1)(c.3),...

Options granted by virtue of employment not part of series (p. 13:29)

[A] stock option granted to an employee by Bidco or Bidco's Canadian parent...

Is debt of Target non-specified property after it is amalgamated with Bidco? (pp. 13:16-18)

On a literal reading of old paragraph 88(1)(c.3),...