PUC offset filing deadline could arise before acquisition of control (p. 19:31)

The policy reasons for implementing a one-year time frame within...

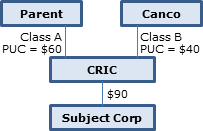

Example of "hollowing out" transaction: subsequent sale of good assets by subject corp. (p. 10)

The explanatory notes issued by Finance with...

{kind=link}

Two interpretations of subject corporation acquired under earnout agreement: PV all investment obligations at investment time; or succession of...

{kind=link}

227(6.2) does not eliminate deemed dividend for non-FAD purposes (p.22)

[S]ubsection 227(6.2) requires the CRA to accept late-filed paragraph...