Subsection 212.1(1) - Non-arm’s length sales of shares by non-residents

See Also

Dairy Queen Canada Inc. v. The Queen, 95 DTC 634, [1995] 2 CTC 2543 (TCC)

Bell TCJ. found on the basis of the testimony of various executives that shares of a Canadian corporation ("OJC") were acquired by the taxpayer's U.S. payment as agent for the taxpayer. Accordingly, s. 212.1 did not apply when the shares of OJC subsequently were transferred into the name of the taxpayer.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Shares | 82 |

Administrative Policy

11 July 2007 External T.I. 2006-0192101E5 F - Disposition d'actions par un non-résident

A non-resident individual who had acquired shares of a Canadian real estate company with a low paid-up capital and a high adjusted cost base (stepped up on the death of that individual’s spouse) was deemed to receive a dividend equaling the excess over the shares’ PUC when they were disposed of to another wholly-owned Canadian corporation for a note. CRA noted that none of the relevant proposals in the 1998 federal budget had been implemented.

Subsection 212.1(1.1)

Paragraph 212.1(1.1)(a)

Administrative Policy

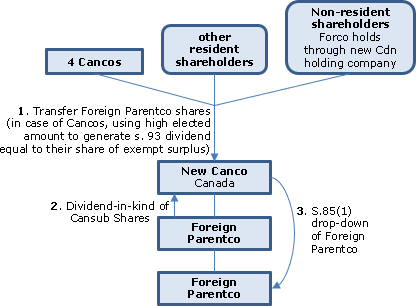

2025 Ruling 2024-1030121R3 - FA Inversion

Background

Foreign Parentco, which is resident in a country with which Canada has a tax treaty (Country 2), wholly owns a Canadian operating subsidiary (Cansub), which is governed by the corporate laws of a province (Act 2), and whose shares do not constitute taxable Canadian property. Foreign Parentco is a foreign affiliate to some of its Canadian shareholders (Canco 1, Canco 2, and Canco 4). Its other shareholders are Forco (governed by the laws of Country 2), a non-resident trust and minority Canadian and non-resident shareholders (each holding under 10% of the shares of Foreign Parentco, which are of a singe class). The shareholders of Country 2 and has minority foreign shareholders. All shareholders are unrelated.

Foreign Parentco has various subsidiaries in County 2 through which it carries on trust and investment activities.

Proposed Transactions

- Forco will transfer all its shares of Foreign Parentco to a corporation newly formed by it under Act 2 (New Holdco) in consideration for common shares of New Holdco.

- Canco 1, Canco 2, and Canco 4 will transfer all their shares of Foreign Parentco to a corporation newly formed under the CBCA (New Canco) in consideration for New Canco common shares, and will elect under s. 85(1) so as to generate a capital gain that will instead be deemed to be a dividend paid by Foreign Parentco out of its exempt surplus pursuant to an election under s. 93(1).

- The minority Canadian shareholders will simultaneously transfer their Foreign Parentco shares to New Canco on an s. 85(1) rollover basis in consideration for New Canco common shares.

- Simultaneously with the above transfers, New Holdco and the non-resident shareholders will transfer their Foreign Parentco shares to New Canco in consideration for common shares of New Canco.

- Foreign Parentco will distribute its Cansub shares as a dividend in kind to its sole shareholder (New Canco), with New Canco claiming the maximum deduction available under s. 113(1).

- New Canco will transfer all its Foreign Parentco shares to Cansub on an s. 85(1) rollover basis in exchange for common shares of Cansub.

Rulings

Pursuant to s. 212.1(1.1)(a), Foreign Parentco will be deemed to receive a dividend from Cansub as a result of the dividend-in-kind equal to the excess of the FMV of the distributed Cansub shares over their paid-up capital.

The resulting deemed dividend will be a dividend for purposes of s. 212(2) and Art. X(2) of the Treaty.

Such deemed dividend will be excluded from the description of A in FAPI definition by virtue of para. (c) thereof.

For purposes of B of the FAPI definition, such deemed dividend will be excluded from Foreign Parentco’s proceeds of disposition in computing its taxable capital gain from the disposition of its shares of Cansub by reason of para. (k) of the definition of proceeds of disposition in s. 54.

Such deemed dividend, less the applicable Canadian withholding tax, will be included in computing Foreign Parentco’s exempt surplus in respect of New Canco by virtue of subpara. (v) of A, and subpara. (iii) of B, of the definition of “exempt surplus” in Reg. 5907(1).

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Accrual Property Income - A - Paragraph (c) | A(c) exclusion for a s. 212.1(1.1) deemed dividend received by the FA on paying a dividend-in-kind of its Cansub to its Cdn Holdco | 245 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Accrual Property Income - B | para. (k) – proceeds of disposition exclusion for a s. 212.1(1.1) deemed dividend received by the FA on paying a dividend-in-kind of its Cansub to its Cdn Holdco | 245 |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Exempt Surplus - A - Subparagraph (v) | A(v) inclusion in exempt surplus for a s. 212.1(1.1) deemed dividend received by the FA (with exempt surplus) on paying a dividend-in-kind of its Cansub to its Cdn Holdco | 233 |

Paragraph 212.1(1.1)(b)

Administrative Policy

2017 Ruling 2017-0699201R3 - Cross-border Butterfly

CRA ruled on a cross-border butterfly which entailed assets of the “Transferred Business” being transferred indirectly to a wholly-owned non-resident subsidiary (Foreign Spinco) of a non-resident public company (Foreign Parentco) or to a wholly-owned non-resident subsidiary of Foreign Spinco (Foreign Spinco Sub) – with a view to the shares of Foreign Spinco being dividended out to the shareholders of Foreign Parentco at the transactions’ completion. One of the indirect assets of Foreign Parentco was a Canadian corporation (DC) which held the Canadian portions of both the Transferred Business and the “Retained Business.”

Following a s. 86 exchange by Foreign Parentco of its old common shares of DC for new common shares and “DC Special Shares”, and before the butterfly distribution to a Canadian subsidiary of Foreign Spinco Sub (TCo), there is a four-party exchange under which Foreign Parentco transfers its DC Special Shares to a newly-formed Canadian sub of Foreign Spinco Sub (TCo), TCo issues common shares to Foreign Spinco Sub, Foreign Spinco Sub issues shares to Foreign Spinco and Foreign Spinco issues shares to Foreign Parentco. The amount added to the stated capital of the TCo Common Shares will equal the FMV of the DC Special Shares rather than the lesser amount under s. 212.1(1.1)(b) as “simply a matter of convenience, in terms of executing the necessary corporate resolutions to effect these steps”. CRA ruled:

[T]he provisions of paragraph 212.1(1.1)(b) will apply to reduce the aggregate PUC of the TCo Common Shares that TCo issued to Foreign Spinco Sub on the Four-Party Share Exchange, to an amount equal to the aggregate PUC, immediately before the transfer, of the DC Special Shares so transferred by Foreign Parentco to TCo, as described in Paragraph 32(b)

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | cross-border butterfly with 4-party exchange and preceding distribution of DC to foreign parent to qualify as permitted exchange/rental property valued at nil/post-butterfly equaling cash payment | 1140 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Permitted Exchange - Paragraph (b) | cross-border butterfly including preliminary transfer of DC to foreing parent to come within “permitted exchange” | 444 |

| Tax Topics - Income Tax Act - Section 143.3 - Subsection 143.3(3) | s. 143.3(3) inapplicable on a 4-party exchange | 234 |

| Tax Topics - Income Tax Act - Section 54 - Adjusted Cost Base | full cost of property acquired under 4-party exchange | 222 |

2013 Ruling 2012-0459781R3 - Cross border butterfly

This was a cross-border butterfly of a Canadian spin business (already packaged into a subsidiary of DC) by DC to TC, an indirect subsidiary of Foreign SpinCo, before Foreign SpinCo was distributed up the chain for inclusion in the assets of New Foreign PubCo, which would then be dividended by the current parent (Foreign PubCo) to its public shareholders. Rather than using the usual 3-party exchange in order to avoid the application of s. 55(3.2)(h) (see Desjardins and Diksic), here a 4-party exchange was contemplated among affiliated corporations, i.e., including both the immediate non-resident parent (Foreign SpinCo Sub) and non-resident grandparent (Foreign SpinCo) of TC in a circular exchange of consideration - so that TC issued its shares to Foreign SpinCo Sub in consideration for the acquisition of special shares of DC from DC's non-resident parent ( Foreign Sub 5 ).

In the context of this 4-party share exchange, the increase in the paid-up capital in respect of the shares of TC issued to Foreign Spinco Sub occurred "by virtue of the disposition" of the special shares of DC by Foreign Sub 5 to TC. Accordingly, s. 212.1(1)(b) (now, s. 212.1(1.1)(b)) applied to grind the PUC of the shares so issued by TC to an amount equal to the PUC of the DC special shares.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | cross-border butterfly reversing previous amalgamation and using 4-party exchange | 1120 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.2) - Paragraph 55(3.2)(h) | 4-party exchange to avoid s. 55(3.2)(h) | 115 |

Subsection 212.1(4) - Where section does not apply

Cases

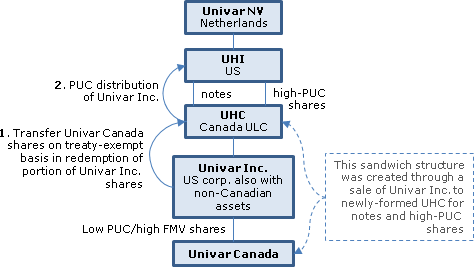

Univar Holdco Canada ULC v. Canada, 2017 FCA 207

A non-resident's acquisition of the shares of a Netherlands public company (Univar NV) indirectly holding the shares of a valuable Canadian subsidary (Univar Canada) with nominal paid-up capital was structured to effectively step-up the paid-up capital of the shares of Univar Canada to fair market value by using the pre-2016 version of s. 212.1(4). This was accomplished by setting up a sandwich structure immediately after the acquisition, under which a new Canadian unlimited liability company, capitalized with notes and high-PUC shares, held the shares of a U.S. corporation holding Univar Canada – so that such U.S. corporation could distribute the shares of Univar Canada (on a Treaty-exempt basis) to its controlling Canadian purchaser (the ULC) without technically being affected by the s. 212.1(1) deemed dividend rule. ( See the more detailed summary of the TCC decision.))

In finding that these transactions were not an abuse of s. 212.1, Webb JA stated (at paras. 21-22)):

If shares of a Canadian corporation with an accumulated surplus are sold by a non-resident vendor to another Canadian corporation with whom that vendor is dealing at arm’s length, section 212.1 of the ITA does not apply. A non-resident person could provide funds to the Canadian purchaser to fund the purchase price for the shares and the following the closing use the surplus in the Canadian corporation that was acquired to repay that non-resident person the funds that were advanced. Thus … the purpose of section 212.1 … was not to prevent the removal from Canada, by an arm’s length purchaser of a Canadian corporation, of any surplus that such Canadian corporation had accumulated prior to the acquisition of control.

…The shares of Univar NV were acquired in an arm’s length transaction and, at the time that such shares were acquired, the avoidance transaction was contemplated. Therefore, the avoidance transaction would be part of the series of transactions by which control of Univar Canada was indirectly acquired in an arm’s length transaction. Whether the surplus of the Canadian corporation is removed by completing the alternative transactions described … above or by completing the transactions that were done in this case, the same surplus is removed from Canada.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | cross-border surplus-stripping transaction was not abusive as it occurred in same series as arm's length acquisition | 404 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(2) | the result achieved (no s. 212.1 withholding) accorded with the underlying policy of permitting surplus stripping as part of an arm’s length acquisition | 109 |

See Also

Univar Holdco Canada ULC v. The Queen, 2016 TCC 159, rev'd 2017 FCA 207

At the time of the acquisition of Univar NV (a Netherlands public corporation), the shares of a Canadian operating subsidiary (“Univar Canada”), having a relatively nominal paid-up capital (“PUC”) and adjusted cost base (“ACB” and a fair market value (“FMV”) of $892 million, were held by a U.S. corporation (“UNAC,”), which was an indirect subsidiary of Univar NV and a predecessor of UHI referred to immediately below. In order to in effect step up the PUC of the shares in Univar Canada, the group first created (as described in greater detail in the paragraph below) a sandwich structure in which a U.S. subsidiary (“UHI”) of Univar NV held notes and all the shares (having PUC and ACB equal to their FMV) of the appellant (“UHC” – which had been formed for the purposes of these transactions), UHC held all the shares of a U.S. subsidiary (“Univar Inc.”), and Univar Inc. held all the shares of Univar Canada. This sandwich structure permitted Univar Inc. to transfer all the shares of Univar Canada to UHC (on a Treaty-exempt basis) as redemption proceeds for a portion of its shares without a deemed dividend arising under s. 212.1(1), through reliance on the exemption under the pre-2016 version of s. 212.1(4) for transfers to a (Canadian) purchaser (UHC) that controlled the non-resident transferor (Univar Inc.). UHC then distributed its remaining shares of Univar Inc. to UHI as a return of capital, and UHI and Univar Inc. amalgamated.

Turning to the previous creation of the sandwich structure, Univar NV sold a portion of its shares of Univar Inc. (theretofore, a wholly-owned subsidiary, and a successor by amalgamation to UNAC and the U.S. parent of UNAC, and holding Univar Canada) to (newly-incorporated) UHI for notes and common shares of UHI, UHI transferred those Univar Inc. shares to (newly-incorporated) UHC for notes and common shares of UHC, and Univar NV transferred its remaining shares of Univar Inc. to UHC for a note which then was assumed by UHI in consideration for issuing common shares.

CRA applied s. 245(2) to assess UHC for Part XIII tax on the amount of the notes which it issued to UHI (rather than the full share-redemption boot of approximately $891 million received on Step 1 in the above diagram) and to reduce the PUC of the shares it issued to UHI. In dismissing UHC’s appeal and finding that the transactions resulted in abusive tax avoidance contrary to s. 245(4) of the Act, V.A. Miller J stated (at paras. 83, 84, 93, 97 and 100):

Subsection 212.1(4) is placed as an exception within an anti-avoidance section… . [I]t is reasonable to infer that subsection 212.1(4) cannot be used so that it would defeat the very application of section 212.1. …[S]ubsection 212.1(4) is aimed at a narrow circumstance where the purchaser corporation, which is resident in Canada, actually controls the non-resident corporation without manipulating the corporate structure to achieve that control.

“[S]ection 84.1…permits PUC to be stepped up through such non-arm’s length transfer to the extent of the transferor’s “hard basis” in the transferred shares. … No such latitude is permitted under section 212.1.”…

If the Appellant’s position prevailed, any non-resident shareholder could reorganize its corporate structure to interpose layers of Canadian resident subsidiaries within its structure to ensure that subsection 212.1 (1) never applies. This cannot have been the intent of Parliament… .

The exception should not apply in the situation where a non-resident owns shares of the Canadian resident purchaser corporation. …

The Appellant fictionally controlled the non-resident, Univar Inc. for less than a day and at all times the Appellant was itself controlled by a non-resident, UHI.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | exception to an anti-avoidance provision should not be interpreted to undercut that anti-avoidance | 259 |

| Tax Topics - Statutory Interpretation - Interpretation Act - Subsection 45(3) | policy of current version of s. 212.1(4) confirmed by proposed amendment | 142 |

Administrative Policy

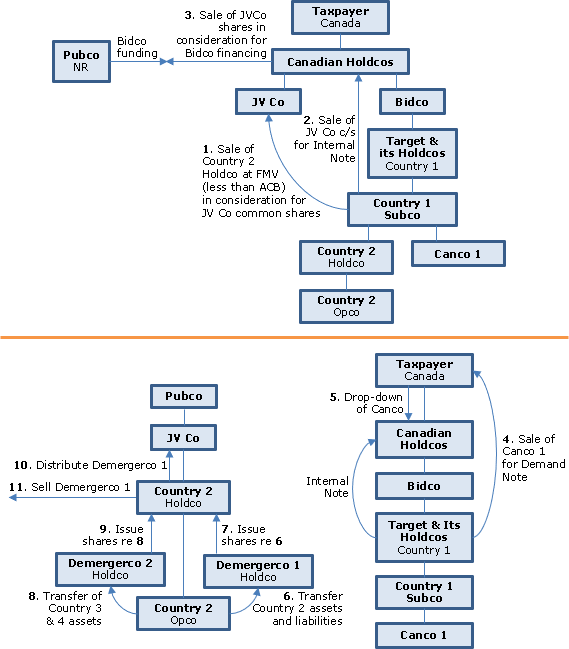

2021 Ruling 2020-0875391R3 - Post-acquisition restructuring

See Intact and Tryg acquisition of RSA for summary of subject transactions as implemented.

Background

The Taxpayer (a Canadian public corporation with a widely-dispersed shareholder base) and Pubco (a corporation, governed by the laws of (foreign) Country 2 and dealing at arm’s length with the Taxpayer) engaged in transactions to permit the Taxpayer, with the assistance of funding indirectly provided by Pubco, to acquire Target (a public limited company governed by the laws of (foreign) Country 1) so that: the Taxpayer will retain Target’s Canadian, Country 1, and certain other international businesses; Pubco will acquire 100% of Target’s businesses in Country 3 and Country 4; and the Taxpayer and Pubco will initially jointly own Target’s business in Country 2 and Country 5 branch business and subsequently sell them to an arm’s length party. An indirect subsidiary of Target (Country 1 Subco) held Canco 1 and also, through Country 2 Holdco, Country 2 Opco, whose shares are excluded property and which holds a number of branches and subsidiaries in Country 2, Country 3, Country 4 and Country 5).

Completed transactions

- A Bidco of the Taxpayer, which was indirectly funded by Pubco (in consideration for being issued JV Co shares in 4 below) and directly by the Taxpayer (through subscriptions through intermediate Canadian holding companies), acquired all the shares of Target pursuant to a court-approved Scheme under the laws of Country 1.

- Country 1 Subco sold all the shares of Country 2 Holdco to JV Co (a newly-established jointly-owned subsidiary of the Taxpayer (through a Canadian holding company subsidiary (“Canada Holdco”)) and Pubco governed by the laws of Country 2, in exchange for common shares of JV Co. The FMV sales price was less than the shares’ ACB.

- Country 1 Subco sold all of its common shares of JV Co at FMV to Canada Holdco in exchange for the “Internal Note.”

- Canada Holdco transferred to Pubco the ownership of a portion of its shares of JV Co in satisfaction of its obligation in 1 above.

- Country 1 Subco sold all the shares of Canco 1 to the Taxpayer in consideration for the “Demand Note” having a principal amount equal to such shares’ FMV.

- The Taxpayer transferred its Canco 1 shares to a subsidiary (New Canada Holdco) for treasury common shares.

- Various transactions were effected to distribute and set-off the Internal and Demand Note.

Proposed transactions

Pursuant to the “Demerger”, i.e., the division of Country 2 Opco between Demergerco 1 and Demergerco 2 (i.e., Country 2 limited liability companies formed by Country 2 Holdco and Pubco, respectively):

- Country 2 Opco will transfer its Country 2 and Country 5 assets and liabilities (including Country 2 subsidiaries) to Demergerco 1, which in turn will issue to Country 2 Holdco, in respect of the shares of Country 2 Opco owned by Country 2 Holdco, shares having an aggregate FMV equal to the net FMV of the property transferred to Demergerco 1.

- Country 2 Opco will make a transfer of the balance of its assets and liabilities (including Country 3 and 4 subsidiaries) to Demergerco 2, with Demergerco 2 issuing shares of equivalent FMV to Country 2 Holdco.

- Country 2 Opco will be dissolved.

- Country 2 Holdco will distribute its shares of Demergerco 1 to JV Co as a dividend in specie.

- The shares of Demergerco 1 will be sold to an arm’s length purchaser.

Purposes

Including:

The purpose of structuring the funding of the Acquisition in a manner that Pubco would not acquire any equity interest in Bidco was to comply with various anti-trust and regulatory requirements. As a consequence, the conditions of subsection 212.1(4) were satisfied and Pubco did not control Country 1 Subco immediately before the disposition of the shares of Canco 1.

Rulings

Including that:

- S. 212.1(4) will apply to the transfer of the Canco 1 shares from Country 1 Subco to the Taxpayer in 5 above such that s. 212.1(1.1)(a) will not deem a dividend to be paid by Canco 1 to Country 1 Subco.

- Ss. 15(1.5)(a)(i) and 15(1.5)(b) and (c) will apply to the Demerger, such that:

- Country 2 Opco will be deemed to have distributed as a dividend in kind the shares of the Demergerco 1 and Demergerco 2 to Country 2 Holdco in an amount equal to the FMV of those shares;

- any gain or loss of Country 2 Opco from such distribution of the shares will be deemed to be nil;

- each property of Country 2 Opco that becomes property of Demergerco 1 and Demergerco on the Demerger will be deemed to be disposed of by Country 2 Opco for proceeds equal to its FMV, with an acquisition at an equivalent cost to Demergerco 1 and Demergerco 2; and

- s. 15(1)(b) will apply to the dividend in kind such that there will be no s. 15(1) inclusion to Country 2 Holdco.

- such dividend described will not be included in computing Country 2 Holdco’s FAPI pursuant to A(b) of the definition of FAPI in s. 95(1).

- The ACB to Country 2 Holdco of its Country 2 Opco shares will be reduced under s. 92(2) by the portion of the dividend in kind that would have been deductible under s. 113(1)(d) in computing the taxable income of Country 2 Holdco if Country 2 Holdco had been a corporation resident in Canada.

- Description of potential s. 40(3) gain to Country 2 Holdco.

- Description of neutralization of any taxable capital gain realized by Country 2 Holdco by the excluded property rules.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1.5) | application of s. 15(1.5) to demerger to split active businesses between two sets of countries | 328 |

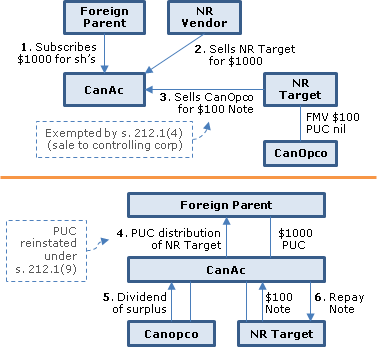

2 December 2014 CTF Roundtable, Q. 4

At the May 2013 IFA Conference, CRA indicated that the GAAR Committee had determined that GAAR applies to cases involving post-acquisition and non-acquisition cross-border PUC planning, but had not recently addressed pre-acquisition PUC planning. Has it considered pre-acquisition PUC planning more recently? Consider the following:

- Foreign Parent subscribes for shares of its wholly-owned Canadian acquisition company (CanAc) having full paid-up capital.

- CanAc acquires from an arm's length vendor the shares of a non-resident corporation (NR Target), which owns high value, low PUC shares of a Canadian operating corporation (CanOpco).

- NR Target sells the shares of CanOpco (which are not taxable Canadian property) to CanAc in consideration for a Note Receivable. S. 212.1 does not apply because of s. 212.1(4).

- CanAc distributes the shares of NR Target to Foreign Parent on a reduction of PUC (which has been restored under s. 212.3(9).)

- The surplus of CanOpco is distributed to CanAc as a dividend (deductible under s. 112(1).)

- CanAc then distributes the same amount outside Canada as a principal repayment on the Note Receivable.

CRA responded:

…GAAR indeed applies. The infusion of capital by Foreign Parent into CanAc and the arm's length acquisition of the shares of NR Target by CanAc do not mitigate the potential for the future payment of Part XIII tax by NR Target on the distribution of CanOpco surplus. The PUC of the shares of CanOpco held by NR Target remains low such that NR Target's access to CanOpco's surplus is reliant on CanOpco making dividend distributions to NR Target.

Subsection 212.1(1) is an anti-surplus stripping rule designed to prevent a non-resident corporation from avoiding Part XIII tax when extracting the corporate surplus of a corporation resident in Canada by way of a disposition of the shares of that corporation to a non-arm's length corporation resident in Canada….

Subsection 212.1(4) is intended to provide relief if there has been no corporate surplus stripped out of Canada and no increase in the ability to strip surplus tax-free out of Canada. …The sale of CanOpco shares to CanAc together with the subsequent transfer by CanAc of NR Target to Foreign Parent sidestep the provisions of subsection 212.1(1) resulting in the surplus of CanOpco being transferred offshore without payment of Part XIII tax by NR Target. It would be inappropriate for subsection 212.1(4) to operate to prevent a deemed dividend arising under [s. 212.1(1)]… in respect of a sale of shares that results in or enables the tax-free distribution of the corporate surplus of CanOpco. Therefore, … the application of subsection 212.1(4) in this case would defeat the objective of section 212.1… .

[O]ther transactions… carried out by the corporate group after the capitalization of CanAc by Foreign Parent and the acquisition by CanAc of the shares of NR Target as described in facts 1 and 2 above, to achieve the tax-free distribution of the surplus of CanOpco out of Canada…[also] would be viewed by the CRA as abusive… .

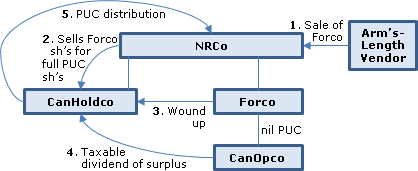

24 May 2013 IFA Roundtable Q. 4, 2013-0483771C6 - 2013 IFA Q4

Consider these facts:

- NRCo owns Forco. Forco owns 100% of a Canadian operating subsidiary (CanOpco). The paid-up capital (PUC) of the shares of CanOpco is nominal.

- NRCo sets up a new Canadian company (CanHoldco), and CanHoldco acquires the shares of Forco for shares of CanHoldco. The PUC of the CanHoldco shares is equal to the FMV of the shares of Forco.

- Forco is wound up into CanHoldco, and the shares of CanOpco are transferred to CanHoldco. S. 212.1(1) does not apply on the transfer.

- CanOpco pays a taxable dividend to CanHoldco in an amount equal to its retained earnings. CanHoldco deducts the dividend from its taxable income under s. 112(1). CanHoldco pays the same amount to NRCo as a reduction of PUC.

What is CRA's position on whether GAAR will apply if the above planning is carried out:

- Pre-acquisition – i.e. NRCo injects equity into CanHoldco, and CanHoldco acquires Forco from an arm's length vendor (assume CanHoldco can't acquire CanOpco directly because NRCO also wishes to acquire Forco's other assets);

- Post-acquisition – i.e. NRCo acquires Forco from an arm's length vendor, then after a number of months transfers Forco to CanHoldco in exchange for shares of CanHoldco; and

- Non-acquisition – i.e. the NRCo, Forco, CanOpco structure has been in place since the inception of CanOpco's business activities, and NRCo transfers the shares of Forco to CanHoldco in exchange for shares of CanHoldco?

Response

: Given that in all three cases, a new Canadian corporation (CanHoldco) is "inserted" to establish cross-border PUC so as to enable surplus of CanOpco to be extracted from Canada, CRA would consider the application of GAAR in each case. CRA stated:

The GAAR Committee has determined that the GAAR applies to cases involving "Post-acquisition" and "Non-acquisition" planning as described above. The GAAR will apply to treat the return of PUC paid by CanHoldco to NRCo as a distribution of a taxable dividend subject to Part XIII withholding tax. The GAAR Committee has not recently addressed the "Pre-acquisition" tax planning case described above. ... If the acquisition of Forco by CanHoldco in all three scenarios occurred after March 28, 2012, section 212.3 would generally apply.

Articles

Nathan Boidman, "Judicial and Legislative Developments Threaten Indirect Canadian Acquisitions", Tax Notes International, Vol. 84, No. 2, 10 October 2016, p. 163

Amendment will attack sandwiches created on 3rd-party acquisitions (p. 168)

The proposed amendment will attack not only an internal reorganization concerning a third-party acquisition, but also a sandwich created upon an acquisition by a third party that is a non-resident.

Application of s. 212.1(4) to Univar transaction (p. 168)

The overall ambit of the proposal can be considered in terms of the Univar matter. In Univar, a U.K. group acquired all the shares of NV for $2 billion. NV owned a Canadian subsidiary, worth $900 million, through a U.S. subsidiary. Univar Canada's PUC was $1 million.

The transaction the parties carried out (a post-acquisition reorganization to create the sandwich) qualified for current subsection (4) but was struck down under GAAR. That transaction would be mechanically addressed by the proposed amendments; new subsection (4)'s exception would not apply, so subsection (1) would apply. If the U.K. buyer had first acquired Univar Canco from its direct U.S. parent, owned by NV, through a new Canco and then acquired NV from the public, would subsection (1) apply? That turns on whether the parties dealt at arm's length at the point of the first transaction and that probably would also turn on the exact relationship between the two transactions. If subsection (1) applied, there would not be any possible eligibility for new subsection (4). Finally, if the buyer acquired NV from the public through a special purpose vehicle (SPV) Canco and then had the direct U.S. owner of Univar Canco sell it to the SPV, new subsection (4) would not be available and therefore subsection (1) would apply. [f.n. 20: If the buyer is a private equity group that acts in a form of co-ownership and each deals at arm's length with the SPV, new subsection (4) should be available. But that would be rare. The proposed exclusion would apply to corporations that have non-arm's-length non-resident shareholders even when the foreign ownership is de minimis. For example, the exclusion will apply if a Canadian resident individual owns 99 percent of an acquiring Canadian corporation and a non-resident sibling owns the other 1 percent. There will be uncertainty in applying the proposal when the Canadian acquiring corporation is owned in whole or in part by a "designated partnership," which is, according to section 212.1(3)(e), a partnership of which either a majority interest partner or every member of a majority interest group of partners (as defined in subsection 251.1(3)) is a non-resident person, because the definitions of non-arm's-length persons and related persons...do not deal with partnerships.] That result is clearly inappropriate. The proposal discriminates against foreign buyers because a domestic buyer would be eligible for subsection (4) in these circumstances. [f.n. 21: The CBA-CPA joint committee submission explains why there is no difference to the Canadian tax base whether purchasers are Canadian or foreign or whether they deal at arm's length or not (as shareholders) with the Canadian corporation that acquires the non-resident corporation.]

Angelo Nikolakakis, "Cross-Border Surplus Stripping – Stripping Bona Fide Non-Resident Purchasers", International Tax (Wolters Kluwer CCH), No. 87, May 2016, p.4

Prejudice to Canadian shareholder of the Canadian purchaser if a non-arm's length non-resident shareholder (p. 7)

[I]f a resident and a non-resident together establish the purchaser corporation as a joint venture vehicle, both are in effect penalized if it is determined that the non-resident does not deal at arm's length with the purchaser corporation….

Tainting from historical non-resident shareholders (p. 7)

[T]he "series" question also gives rise to considerable uncertainty, as well as some clearly inappropriate results. For example, if a Canadian corporation (with no non-resident shareholders) acquires the purchaser corporation from a non-resident seller, and then that purchaser corporation is used to acquire a non-resident corporation that holds an underlying Canadian corporation, subsection 212.1(4) will not apply if the two acquisitions are part of the same "series" even though no non-resident indirectly acquires any interest in the acquired corporation. Similarly, if a Canadian corporation (with no non-resident shareholders) acquires the purchaser corporation from a non-resident seller, and the purchaser corporation already holds a non-resident corporation that in turn holds an underlying Canadian corporation, subsection 212.1(4) will not apply to allow the sandwich to be unwound into the purchaser corporation. [fn 17: It may be possible to unwind the sandwich differently (for example, by first liquidating the acquired Canadian corporation into acquiring Canadian corporation and then unwinding the sandwich into the acquiring Canadian corporation rather than into the acquired Canadian corporation), but it remains to be seen whether that approach would ultimately be feasible. There is also no exclusion for deemed non-arm's length relationships resulting from a paragraph 251(5)(b) right.]

Double deemed dividend on unwinding a double-decker sandwich (p.7)_

Third, these proposals can give rise to inappropriate results even where there is no arm's length acquisition. For example, if a non-resident ("FP") holds a Canadian corporation ("Canco A") that holds a non-resident corporation ("Holdco") that in turn holds an underlying Canadian corporation ("Canco B"), the unwinding of the sandwich can give rise to the inappropriate acceleration of taxation (or even double taxation). Assume that neither Canadian corporation has any PUC, and that their value is 100. There will be two PUC deficiencies of 100. If Holdco distributes Canco B to Canco A, there will be a deemed dividend of 100 from Canco A to Holdco, even though the PUC deficiency remains on the Canco A shares. If Canco A then makes a distribution of 100 to FP, a second dividend or deemed dividend of 100 will arise. This result is inappropriate because the two PUC deficiencies are overlapping and reflect the same economic value. In addition, since the deemed dividend from Canco A to Holdco would be a "downstream dividend", it is unlikely that the-usual treaty-reduced rate of 5% would apply for withholding tax purposes, such that the rate will likely be 15%....

Canadian Pubco or private-equity fund with potential non-arm's length shareholders or partners (pp. 7-8)

[S]ince the provision would refer to a non-resident that owns shares of the capital stock of the purchaser corporation "directly or indirectly", a Canadian public company may not be able to rely on subsection 212.1(4) unless, it could establish that it deals at arm's length with all its non-resident shareholders and with all the non-resident stakeholders of its resident shareholders. There is also the example of a private equity fund that holds a Canadian corporation. If the fund is a partnership, it would be a designated partnership (as defined in paragraph 212.1 (3)(e)) if a majority-interest partner or every member of a majority-interest group of partners (as defined in subsection 251.1(3)) is a non-resident person….Even if the general partner is Canadian, the fund may have a single non-resident direct or indirect member, and thus the question would arise as to whether that member of the partnership deals at arm's length with the corporation controlled by the partnership.

Angelo Nikolakakis, Alain Léonard, "The Acquisition of Canadian Corporations by Non-Residents: Canadian Income Tax Considerations Affecting Acquisition Strategies and Structure, Financing Issues, and Repatriation of Profits", 2005 Conference Report, c. 21, p. 21:8.

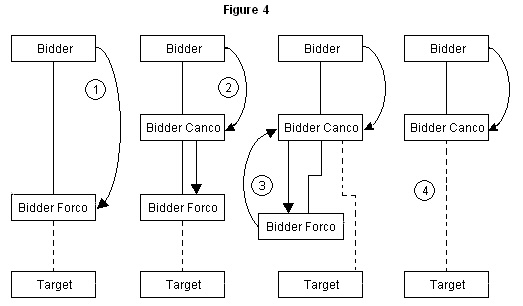

In step 1 of figure 4, Bidder transfers Target to Bidder Forco in exchange for a promissory note ("the Bidder Forco reorganization note") with a face amount equal to the fair market value (FMV) of Target. Section 212.1 does not apply because this is not a transfer of the shares of one corporation resident in Canada to another, and there is no gain from the disposition of the Target shares because they were just acquired in a taxable arm's-length transaction. 30 In step 2, Bidder transfers Bidder Forco shares and the Bidder Forco reorganization note to Bidder Canco in | exchange for Bidder Canco shares and a promissory note ("the Bidder Canco capital note") in an appropriate combination. Again, section 212.1 does not apply, because there is no transfer of the shares of one corporation resident in Canada to another, and there is no gain from the disposition of Bidder Forco shares or the Bidder Forco note because they were just acquired in a taxable transaction. In step 3, Bidder Forco transfers Target to Bidder Canco in exchange for a promissory note ("the Bidder Canco reorganization note") with a face amount equal to the FMV of Target. Section 212.1 does not apply because of subsection 212.1(4): the disposition of Target by Bidder Forco to Bidder Canco is "a disposition by a non-resident corporation of shares of a subject corporation to a purchaser corporation that immediately before the disposition controlled the non-resident corporation," and there is no gain from the disposition of the Target shares because they were just acquired in a taxable transaction. At this point, Bidder Canco holds Bidder Forco as well as the Bidder Forco reorganization note, and is indebted to Bidder Forco under the Bidder Canco reorganization note. Thus, in step 4, the Bidder Forco reorganization note is set off against the Bidder Canco reorganization note. Bidder Forco is then dissolved, such that Bidder Canco is left holding Target; the cross-border tax attributes (PUC and debt) have been increased to the amount of the fresh capital expended by Bidder in respect of the acquisition of Target.

It should also be possible for Target subsequently to be combined with Bidder Canco, although additional considerations will arise, including with respect to capital tax liability concerns (see the discussion below).

Vesely, Roberts, "Takeover Bids: Selected Tax, Corporate, and Securities Law Considerations", 1991 Conference Report, pp. 11:30-11:31

Discussion of technique for avoidance of s. 212.1 where a non-resident acquirer is making a bid for shares of a Canadian target.

Subsection 212.1(6)

Articles

Kyle Lamothe, Alexander Demner, "Retroactive Relief from section 212.1 ‘Look-Through’ Rules Proposed for Post Mortem Pipelines", Tax for the Owner-Manager, April 25, 2025, Vol 25, No. 2, p. 4

Current conduit rule (p. 5)

- In a pipeline transaction where an estate with a non-resident beneficiary transfers its shares of Opco to a Newco in consideration for a note of Newco, Newco will be deemed under the current version of the s. 212.1(6)(b) conduit rule to pay to the non-resident beneficiary a dividend (subject to Part XIII tax) based on the note amount, that is generally proportionate to the relative FMV of that beneficiary's interest in the estate.

- If the Opco shares instead are transferred by the estate to Newco for high-PUC Newco shares, that PUC will be suppressed by the same amount.

Draft amendment (p. 5)

The August 12, 2024 draft amendments include an amendment to s. 212.1(6)(b) which (retroactively to the February 26, 2018 effective date of the ss. 212.1(5) to (7) look-through rules) will exclude, from the application of the above look-through rule, dispositions of shares by a graduated rate estate (GRE) which had acquired those shares upon the death of a Canadian resident individual.

Scope limitations (p. 5)

Some observations:

- This amendment applies, in the case of resident trusts, to trusts that are GREs at the time of the share disposition, so that the amendment will not provide relief if the transfer occurs after the 36-month period for being a GRE has expired (or GRE status is otherwise compromised), or the subject shares are held in a life interest trust, i.e., an alter ego, spousal, or joint partner trust.

- The amendment will provide no relief if the deceased was a non-resident at death, even if the estate is resident in Canada because of Canadian-resident executors.

- The amendment only applies to shares "acquired... on and as a consequence of" the individual's death. Accordingly, if the shares acquired by the GRE on death are then exchanged before the pipeline transaction, for example, on a share-for-share exchange to isolate value in new preferred shares, the amendment may not apply.

Refund of Part XIII tax under old conduit rule (p. 5)

- The amendment also extends the deadline for a refund application under s. 227(6) to 180 days from the date on which the amendment receives royal assent, so that the Part XIII tax that was over-withheld under the old conduit rule generally can be recovered.

Kyle B. Lamothe, Alexander Demner, "Section 212.1 Post Mortem Pipeline Comfort Letter", Tax for the Owner-Manager, Vol. 20, No. 2, April 2020, p. 8

December 2, 2019 comfort level (p.8)

The comfort letter recognizes that paragraph 212.1(6)(b) can give rise to double-tax results "not consistent with current tax policy." Accordingly, Finance will recommend an amendment to exclude from the lookthrough rules dispositions of shares by graduated rate estates (GREs) arising from the death of a Canadian-resident individual.

Limitations of exclusion (p. 8)

First, the proposed exclusion is restricted to Canadian decedents, notwithstanding that an estate may be factually resident in Canada regardless of the deceased's previous residence.

Second, the exclusion is limited to shares acquired on death. If the Opco shares are exchanged (for example, for fixed-value preferred shares) after death and before the pipeline, relief may be lost. We hope that the forthcoming legislation will include a substituted-property rule to alleviate this issue.

Limitation to GREs (p.8)

… We understand that Finance restricted the comfort letter to GREs in part because subsection 164(6) limits to one year the period within which loss carryback planning is available. In contrast, life interest trusts (LITs)—such as alter ego, spousal, and joint partner trusts—typically have three taxation years to carry back losses.

… LITs are in a materially identical position to GREs … .

Alternate transactions for life interest trusts (pp. 8-9)

… Assume that the LIT transfers its shares of Opco for Holdco shares alone (that is, without receiving any non-share consideration). Paragraph 212.1(1.1)(b) suppresses the PUC of the Holdco shares, but no deemed dividend arises. On a subsequent repurchase or redemption of those shares, the LIT will realize a deemed dividend under subsection 84(2) or (3), but, critically, its POD will be reduced (see paragraph (j) of the POD definition in section 54). The result is a capital loss. Subject to the applicability of any stop-loss rules and the general three-year loss carryback period, the LIT can use that loss to offset its capital gain on death. Thus, only one layer of tax subsists.

Alexander Demner, Kyle B. Lamothe, "Section 212.1 Lookthrough Rules Create Issues for Trusts with Non-Resident Beneficiaries", Tax for the Owner-Manager, Vol. 19, No. 2, April 2019, p. 2

Results of pipeline for estate with non-resident beneficiary where the new Holdco issues notes (p. 3)

Ms. A divided her estate equally between two heirs, one of whom is a non-resident. If a postmortem pipeline is undertaken with Holdco issuing only a promissory note to the estate as consideration for the Opco shares…

- Paragraph 212.1(6)(b) deems each beneficiary of the estate to directly dispose of one-half of Opco's shares to Holdco, and to directly receive one-half of the non-share consideration (the promissory note) received by the estate from Holdco…

- Paragraph 212.1(1.l)(a) deems Holdco to pay a dividend to the non-resident beneficiary equal to the amount by which one-half of the non-share consideration exceeds one-half of the Opco shares' PUC. ...

[I]t appears that ... the dividend deemed to be paid to the non-resident beneficiary does not reduce the estate's process of disposition. ... [N]o similar language [to para. (k) of "proceeds of disposition"] exists for trusts.

Results of pipeline where such estate instead receives shares from Holdco (p. 3)

Materially different consequences appear to occur if the estate only receives shares of Holdco. In such circumstances, no dividend will arise on the initial transfer to Holdco (though subsection 212.1(1.2) appears to be engaged). Instead, paragraph 212.1(l.l)(b) grinds the PUC of the Holdco shares by one-half of the amount by which the increase in PUC of Holdco's shares exceeds the Opco shares' PUC.

On a subsequent repurchase of the Holdco shares, subsection 84(2) or (3) will deem the estate to receive a dividend to the extent that the repurchase price exceeds the shares' PUC (which it can then allocate to the non-resident beneficiary). Critically, however, the estate should also realize a capital loss, since its proceeds of disposition will be reduced by paragraph (j) of that term's definition. The estate can then carry back the capital loss to Ms. A's terminal tax return under subsection 164(6) if the estate is a graduated-rate estate and completes the repurchase within its first taxation year. This step may be particularly beneficial if the corporations have a capital dividend account or a refundable dividend tax on hand balance.

Henry Shew, "Post Mortem Pipeline Fails for Non-Resident Beneficiaries", Canadian Tax Focus, Vol. 9, No. 1, February 2019, p. 1

Result if s. 212.1 applies where a non-resident beneficiary (p. 1)

[A]n estate has three beneficiaries - … and one is a non-resident—and the will provides that the residue … is to be divided equally among the three beneficiaries. The estate owns shares of Opco with an ACB of $100,000 (from the deemed disposition at death) and PUC of $100. One-third of the shares are to go to each beneficiary. If a regular pipeline transaction is performed by the estate—involving the sale of the shares of Opco to a newly incorporated Holdco in exchange for a promissory note—there is a deemed dividend equal to $33,300 … to the non-resident beneficiary….

1st s. 212.1 requirement: NAL relationship (under ss. 212.1(3)(b) and (a) (p.1)

For section 212.1 to apply, the non-resident person and Holdco must not deal at arm’s length… [P]aragraph 212.1(3)(b) deems a beneficiary of a trust to own the shares that the trust actually owns…Thus, paragraph 212.1(3)(a) applies … and the non-arm's-length relationship of the non-resident person and Holdco is established.

2nd s. 212.1 requirement: disposition to Newco under ss. 212.1(5) and (6) look-through rule (p.1)

Another requirement for section 212.1 to apply is that the non-resident has disposed of Opco shares to Holdco. The new lookthrough provisions of subsections 212.1(5) to (7) put the non-resident person in the place of the estate, and hence this condition is satisfied.

Potential application of s. 212.1(7) if hotchpot clause (p. 1)

Under a "hotchpot" clause the executor has the power to choose which assets go to each beneficiary under the will, taking into account the distribution of assets both inside and outside the estate. In this situation, the effect of subsection 212.1(7) (where its purpose test is satisfied) is that the non-resident beneficiary is deemed to have a 100 percent interest in the estate assets, tripling the deemed dividend to $99,900….

Paragraph 212.1(6)(b)

Administrative Policy

2021 Ruling 2019-0800431R3 - Alter Ego Post-mortem Pipeline and Bump Planning

Around when he was placed in a long-term care facility, the “Deceased” transferred his shares of two companies with investing businesses (Aco and Bco) on a s. 73(1) rollover basis to a newly-formed alter ego trust (“AE Trust”) of which a child (“Child 1”) was the trustee, and Child 1, Child 1’s spouse and their three adult children were beneficiaries with entitlements to income and capital as determined in the discretion of the trustee (except that he could not distribute capital to himself). On the death of the Deceased, there was a deemed disposition of the Aco and Bco shares for their FMV pursuant to s. 104(4)(a).

As a preliminary transaction, it was proposed that the trustee pursuant to a provision of the Trust Deed execute an irrevocable deed to amend the Trust Deed to thereupon remove one of the grandchildren (who was a non-resident) as a beneficiary of AE Trust. The stated purpose was "to preclude the potential application of the provisions of section 212.1 that may otherwise result, to the extent that Grandchild 1 would be a non-resident beneficiary of AE Trust at any relevant time.” (Note that in 2019-0824561C6, CRA adverted to the 2 December 2019 Finance comfort letter, but noted that it did not extend to non-GRE trusts, e.g., a life interest trust, such as AE Trust.)

AE Trust then implemented conventional pipeline transactions.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | pipeline for alter ego trust with preliminary elimination of NR beneficiary and application of s. 88(1)(d.3) | 367 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(d.3) | s. 88(1)(d.3) applied to securities held by investing corportions whose shares were stepped up in hands of alter ego trust and then transferred to and amalgamated under pipeline | 202 |

3 December 2019 CTF Roundtable Q. 5, 2019-0824561C6 - 212.1 Post-mortem Pipeline Transaction

In a post-mortem “pipeline” transaction, a Canadian resident estate (the “Trust”) has full ACB and low paid-up capital in shares of a Canadian-resident private corporation (“Canco”), which it transfers to a non-arm’s length Canadian resident corporation (“Holdco”) for a note (the “Note”). If the Trust has a non-resident beneficiary, such non-resident beneficiary would be deemed to receive a certain proportion of any non-share consideration (the Note) received by the Trust on the disposition of the Canco low paid-up capital shares, resulting in a dividend deemed to be received by the non-resident beneficiary. Would the CRA seek to apply s. 212.1 based on a technical application of the look-through rules?

CRA indicated that, under s. 212.1(6)(b)(i), there will be a deemed disposition by each non-resident beneficiary, based on the fair market value of the beneficiary’s interest in the trust, divided by the fair market value of all the direct interests in the trust. Under s. 212.1(6)(b)(ii), each non-resident beneficiary will be deemed to have received consideration other than the shares of the purchaser corporation, and that consideration received will, again, be equal to the proportion of their interest in the trust. If that amount exceeds the PUC of the disposed-of shares, and all the conditions of s. 212.1(1) have been met for the non-resident beneficiary, that amount in excess of the PUC would generally be a deemed dividend under s. 212.1(1.1).

Notwithstanding the recent comfort letter, the above answer would still be relevant for non-GRE trusts.

Finance

2 December 2019 Comfort Letter - Cross-Border Surplus Stripping & Graduated Rate Estates

Finance first noted that in a pipeline transaction (entailing the estate selling the shares of Canco (whose ACB was stepped up on death) to a newco (NewCanco) for a note of NewCanco, which on its subsequent repayment, effectively extracts the corporate surplus of Canco), each non-resident estate beneficiary is deemed, after giving effect to the look-through rule in s. 212.1(6)(b), to their proportionate share of the promissory note, and will pay tax on the deemed dividend resulting from the excess of that beneficiary’s proportionate share of the promissory note over the paid-up capital of their proportionate interest in the Canco shares. Finance stated:

We agree that the application of paragraph 212.1(6)(b) of the Act can give rise to results in the context of graduated rate estates that are not consistent with current tax policy. Therefore, we are prepared to recommend to the Minister of Finance that the Act be amended to exclude, from the application of paragraph 212.1(6)(b), dispositions of shares by a Canadian resident graduated rate estate of an individual who was resident in Canada immediately before the individual's death, provided that those shares were acquired by the estate on and as a consequence of the individual's death. We also intend to recommend that this proposed amendment apply to dispositions after February 26, 2018.

Articles

Joint Committee, "July 27, 2018 Legislative Proposals", 10 September 2018 Submission

Look-through of corporations (pp. 12-13)

S. 212.1(6)(b), which applies a look-through rule for the purpose of having s. 212.1 apply on a disposition by a partnership or trust is overly broad in that it looks through corporations. For example, when the non-resident seller (NRco) sells its interest in a partnership owning USco which owns Canco representing only 20% of the fair market value of the USco shares, s. 212.1 would appear to apply to the “sale” of the underlying Canco shares.