Subsection 132.2(1) - Definitions re qualifying exchange of mutual funds

Qualifying Exchange

Administrative Policy

2024 Ruling 2023-0962031R3 - mutual fund reorganization

CRA ruled on the creation, on a rollover basis, of a master, or “aggregator,” mutual fund trust, so that those unitholders of five existing...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(1) | creation of an aggregator fund on a s. 107.4 and 132.2 rollover basis | 652 |

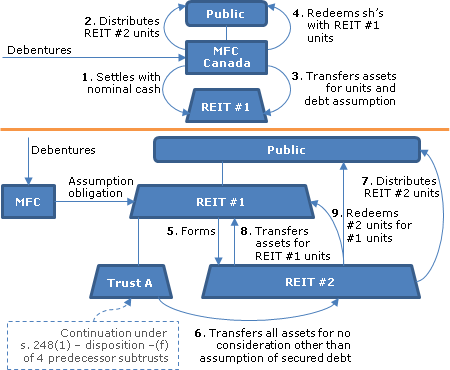

2017 Ruling 2016-0660321R3 - Reorg of REIT to simplify multi-tier structure

Background

Fund, which is a REIT under s. 122.1, holds notes and all the units of a unit trust (“Sub-Trust”). Sub-Trust owns the Class A LP...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(2) - Paragraph 107.4(2)(a) | s. 107.4 transfer of sub-trust’s assets to sister MFT trust | 460 |

| Tax Topics - Income Tax Act - Section 98 - Subsection 98(3) | drop down of LP 1 into LP 2 followed by immediate s. 98(3) wind-up of LP 1 into LP 2 and GP of LP1, followed by immediate taxable sale by GP to LP 2 | 146 |

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) | no taxable benefit where wholly-owned partnership renounces the right to receive units of its “parent” REIT | 325 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | no disposition of partnership interests or property on conversion of general to limited partnership or adding right of renunciation of a MFT unitholder | 165 |

| Tax Topics - Income Tax Act - Section 132.2 - Subsection 132.2(3) - Paragraph 132.2(3)(g) - Subaragraph 132.2(3)(g)(vi) - Clause 132.2(3)(g)(vi)(C) - Subclause 132.2(3)(g)(vi)(C)(I) | renunciation by subsidiary partnership of transferee MFT of units that otherwise would be issuable on the redemption of its incestuous holding in transferor MFC | 245 |

2013 Ruling 2013-0492731R3 - qualifying disposition -mutual fund trust

The elimination of the subtrust of an open-end listed mutual fund trust (the "Fund") was to be accomplished by the subtrust transferring its...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(1) | elimination of REIT sub trust through s. 107.4 transfer to new "in house" MFT and s. 132.2 merger of MFT into REIT | 644 |

| Tax Topics - Income Tax Act - Section 132 - Subsection 132(6) | MFT's trustee not to be a director of a sub | 119 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | no disposition on MFT units consolidation back to the previous number, occurring outside a Plan of Arrangement | 107 |

2013 Ruling 2013-0488351R3 - Conversion of a MFC to a MFT

{kind=link}

The same (mutual fund corporation) taxpayer as for 2013 Ruling 2011-0395091R3 ("MFC to MFT Conversion") (immediately below) obtained essentially...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(1) | conversion of MFC to MFT and subtrust elimination | 180 |

| Tax Topics - Income Tax Act - Section 21 - Subsection 21(1) | election of GP to capitalize loss before elimination of subtrust | 204 |

2013 Ruling 2011-0395091R3 - MFC to MFT Conversion

{kind=link}

Background

Taxpayer, which is a listed mutual fund corporation, wishes to convert to a mutual fund trust (so that following the conversions...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(1) | 210 | |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | deductible interest on internal assumption (no release) | 159 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition - Paragraph (f) | consolidation of 4 subtrusts into 1 using (f) | 178 |

5 May 1995 External T.I. 9511935 - NEWLY ESTABLISHED FUND

Where a mutual fund corporation transfers its assets to a newly established unit trust that will not meet the distribution requirements under...

Articles

Hugh Chasmar, "Corporate Class Funds", Canadian Tax Highlights, Vol. 25, No. 8, August 2017, p. 6

Expansion of s. 132.2 to permit division of multi-class MFC into multiple MFTs (p. 7)

[Under] proposed section 132.2…a multi-class MFC with 20...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 131 - Subsection 131(4.1) | 276 |

Subsection 132.2(3) - General

Paragraph 132.2(3)(a)

Articles

Darcy De Moche, Greg Johnson, "Recent Developments and Transactions Affecting Income Funds and Royalty Trusts", 2005 Conference Report, c. 17.

Forms

T1169 "Election On Disposition Of Property By A Mutual Fund Corporation (Or A Mutual Fund Trust) To A Mutual Fund Trust

Paragraph 132.2(3)(g)

Subaragraph 132.2(3)(g)(vi)

Clause 132.2(3)(g)(vi)(C)

Subclause 132.2(3)(g)(vi)(C)(I)

Administrative Policy

2017 Ruling 2016-0660321R3 - Reorg of REIT to simplify multi-tier structure

Background

As a result of quite a number of other transactions, a REIT (the “Fund”) holds the Class A LP Units of the Partnership (as well as...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 132.2 - Subsection 132.2(1) - Qualifying Exchange | use of the s.132.2 merger and a renunciation of most of the units otherwise issuable on the merger in order to eliminate a REIT corporate subsidiary held through an LP and a sub-trust | 1006 |

| Tax Topics - Income Tax Act - Section 107.4 - Subsection 107.4(2) - Paragraph 107.4(2)(a) | s. 107.4 transfer of sub-trust’s assets to sister MFT trust | 460 |

| Tax Topics - Income Tax Act - Section 98 - Subsection 98(3) | drop down of LP 1 into LP 2 followed by immediate s. 98(3) wind-up of LP 1 into LP 2 and GP of LP1, followed by immediate taxable sale by GP to LP 2 | 146 |

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) | no taxable benefit where wholly-owned partnership renounces the right to receive units of its “parent” REIT | 325 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | no disposition of partnership interests or property on conversion of general to limited partnership or adding right of renunciation of a MFT unitholder | 165 |