Subsection 84.1(1) - Non-arm’s length sale of shares

Cases

Wild v. Canada (Attorney General), 2018 FCA 114

Mr. Wild stepped up the adjusted cost base of his investment in a small business corporation (PWR) by transferring his PWR common shares to two...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | surplus-stripping transactions were not subject to GAAR before the surplus had in fact been stripped | 377 |

Fiducie famille Gauthier v. Canada, 2012 FCA 76, aff'g 2011 DTC 1343 [at 1917], 2011 TCC 318

The taxpayer, a family trust, made a non-arm's-length sale of shares to a numbered corporation ("4041763 or "404") for a promissory note of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Shares | 258 |

Canada v. Olsen, 2002 DTC 6770, 2002 FCA 3

The taxpayer transferred shares of a corporation ("Leader") to corporations controlled by the taxpayer's children and spouses in consideration for...

See Also

Carter v. The King, 2024 TCC 71

The appellant, her cousin (“McAllister”) and her father held 40%, 40% and 20% of the common shares of Brown’s Paving Ltd. (“BPL”),...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | a sale of the taxpayer’s Opco shares to her cousin’s holdco for cash funded by an Opco dividend, was arm's length | 339 |

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(2) | no evidence that controlling shareholder of Opco did not deal at arm’s length with the holding company which was alleged to control Opco under s. 186(2) | 136 |

Crean v Canada (Attorney General), 2019 BCSC 146

The executed documents indicated that an individual (Thomas) sold his shares of a corporation (Crean Holdings) to the Newco of his brother...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Rectification & Rescission | a sale agreement rectified to turn it into a 2-step sale that no longer generated a s. 84.1 dividend | 325 |

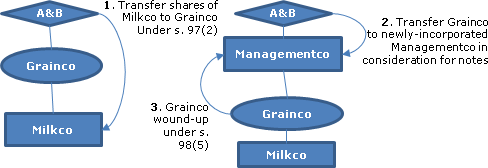

1245989 Alberta Ltd. v. The Queen, 2017 TCC 51, rev'd sub nom. Wild v. Canada, 2018 FCA 114

In order to protect the assets of an Alberta an oil field rental company (“PWR”), whose sole shareholder was Mr. Wild and whose shares of PWR...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | use of PUC-averaging rule to bump outside PUC was abusive | 273 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(5) | assessment of PUC without current income effect | 34 |

Poulin v. The Queen, 2016 TCC 154, briefly aff’d sub nomine Turgeon v. The Queen, 2017 FCA 103

CRA successfully applied s. 84.1 to a transaction in which one of the two major shareholders of a Quebec CCPC (Mr. Turgeon) agreed to sell some...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | sale to the special-purpose Holdco of an independent employee was essentially a surplus-stripping transaction rather than an arm’s length sale | 635 |

Fiducie Famille Gauthier v. The Queen, 2011 DTC 1343 [at at 1917], 2011 TCC 318, aff'd 2012 FCA 76

The taxpayer, a family trust, made a non-arm's-length sale of shares to a numbered corporation for a promissory note of approximately $2.6...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Substance | 233 |

Estate of the late Donald Mills v. The Queen, 2010 DTC 1301 [at at 4078], 2010 TCC 443, aff'd 2011 DTC 5124, 2011 FCA 219

The taxpayer exchanged shares for a promissory note. Under s. 84.1(1)(b), the receipt of the promissory note resulted in a deemed dividend. The...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(p) - Subparagraph 20(1)(p)(i) | no bad debt if deemed dividend | 77 |

McMullen v. The Queen, 2007 DTC 286, 2007 TCC 16

The taxpayer and an unrelated individual ("DeBruyn") accomplished a split-up of the business of a corporation ("DEL") of which they were equal...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | 270 | |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 198 | |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | mutual benefit and same advisors insufficient to establish non-arm's length in structured sale transaction | 257 |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | 229 |

Lloyd v. The Queen, 2002 DTC 1493 (TCC)

Although the taxpayer signed an agreement with a holding company for the sale of shares in a company ("READ") to the holding company, Bowman...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | taxpayer can attack own transaction as legally ineffective | 138 |

| Tax Topics - General Concepts - Tax Avoidance | taxapyer can argue legally ineffective transactions | 139 |

| Tax Topics - Income Tax Regulations - Schedules - Schedule II - Class 1 - Paragraph 1(q) | 70 |

Administrative Policy

7 October 2022 APFF Roundtable Q. 8, 2022-0942151C6 F - Surplus stripping

In order for Brother to avoid the application of s. 84.1 to a sale of his shareholding of Opco (representing ½ of its common shares) to a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.11) | range of factors considered | 182 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(2) | permissible use of sale through subsidiary to avoid s. 84.1 | 85 |

7 October 2021 APFF Financial Strategies and Instruments Roundtable Q. 8, 2021-0899701C6 F - Post-mortem planning - Pipeline

In order to implement pipeline planning, the estate of an individual ("Estate") generally incorporates a new corporation ("Newco") to which it...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | a pipeline transaction can use an existing corporation rather than a Newco | 187 |

2021 Ruling 2020-0868661R3 F - Section 84.1 – Leveraged Buyout

Background

Holdco (a.k.a. Gesco) holds real estate which it leases to Opco, which carries on an active business in Canada. Mr. X (an investor),...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | ruling that buyout was an arm’s length transaction | 123 |

29 November 2016 CTF Roundtable Q. 6, 2016-0669661C6 - 84.1 and the Poulin/Turgeon Case

CRA largely repeated a statement made at the 2016 APFF Roundtable, Q.20 (also in response to the Poulin decision) respecting employee buyco...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(1) - Total Charitable Gifts - Paragraph (c) - Subparagraph (c)(ii) | right of GREs to carry forward donations for five years | 109 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | touchstones for accommodation party | 184 |

7 October 2016 APFF Roundtable Q. 20, 2016-0655831C6 F - Employee Buycos and the Poulin Case

CRA accepts the finding in Poulin that the structuring of a sale transaction so that the vendor secured a tax advantage (the capital gains...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | Poulin distinction between accommodation parties and tax advantaged arm’s length dealings accepted | 188 |

2 May 2016 External T.I. 2016-0633351E5 F - Descarries Case and Document no. 2015-0610711C6

In rejecting a submission that 2015-0610711C6 had improperly reversed 2005-0134731R3 F on the basis that the purpose of section 84.1 is only “to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | Descarries not to be construed narrowly | 176 |

24 November 2015 CTF Roundtable Q. 11, 2015-0610711C6 - Impact of the Descarries decision

In 2005-0134731R3 F, Mr. X realized a capital gain of selling all of the common shares of HOLDCO to his children in consideration for promissory...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | contrary to GAAR to use basis stepped up under CGD to create a capital loss permitting surplus extraction | 494 |

2014 Ruling 2014-0526361R3 F - Post Mortem Pipeline

An estate of B, and a spousal trust for which B had been the spouse, which on death acquired (Class F) preference shares of a portfolio...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | step up of PUC of freeze pref shares for purposes of pipeline transaction | 315 |

25 November 2012 CTF Roundtable, 2013-0479402C6 - Employee Buycos - comments from CRA Panel

Employees of Opco received Opco shares as incentives under an Opco employee share ownership plan ("ESOP"). Under the terms of the ESOP, on...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | stock option share Buyco not at arm's length | 202 |

3 July 2012 External T.I. 2012-0443421E5 F - 84.1 and partnership

{kind=link}

A and B are Canadian-resident spouses who have not utilized their capital gains exemption and who each hold 50 Class A shares (the only issued...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | s. 245(2) has been applied to the use of a partnership to avoid s. 84.1 | 536 |

7 October 2011 Roundtable, 2011-0412121C6 F - Interaction between S. 84.1 and S. 85(2.1)

Where shares with a high PUC and low ACB are transferred by an individual under s. 85(1) to Holdco for shares with the same high-low attributes,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(2.1) | s. 85(2.1) does not apply where s. 84.1(1) applies even if there is no grind under the s. 84.1(1)(a) formula | 166 |

1 October 2010 External T.I. 2010-0378681E5 F - Déduction pour gain en capital

Would the capital gains deduction be available to an individual who disposes of all of the shares of "Opco") to another corporation ("Sonco")...

7 July 2010 External T.I. 2010-0370611E5 F - Purchase of Shares by Subsidiary - Sec. 245

A CRA response at the 2005 APFF Roundtable (2005-0141061C6) dealt with the situation where Mr. X, an arm’s length shareholder owning 20% of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | position that an individual potentially can realize a capital gain by selling shares to a Newco sub of the corporation for cash does not depend on there being a s. 87 or 88 merger of Newco and the corporation | 264 |

28 August 2008 External T.I. 2008-0287611E5 F - Surplus Stripping

Regarding a proposed series of transactions whose purpose was to convert a taxable dividend that would otherwise have been paid by Opco into a...

5 October 2007 APFF Roundtable Q. 10, 2007-0243171C6 F - Surplus Stripping

Scenario (a)

Mr. X, who holds all of Opco, exchanges all of his Opco common shares for retractable preferred shares of Opco. Mr. X then subscribes...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | leveraged Employeeco buyout could be an arm’s length transaction | 127 |

12 January 2005 External T.I. 2004-0106161E5 - Application of par. 84.1(1)(b) on a sale of shares

Under transactions in which Mr. A sells a portion of his shares of a family farm corporation ("Farmco") to a newly incorporated subsidiary ("Xco")...

7 December 2004 External T.I. 2004-0103061E5 F - Non Arm's Length Sale of Shares-Surpl. Stripping

A professional partnership with three members disposes of all the shares of the services corporation ("Serviceco" - rendering services to the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | scheme of Act requires that a corporate distribution be treated as income, regardless of form | 138 |

29 June 2004 External T.I. 2004-0078951E5 F - Non Arm's Length Sale of Shares, Surplus Stripping

An individual ("A") holds preferred shares in a holding corporation ("HOLDCO") with an ACB equaling their FMV of $500,000 as a result of a...

9 January 2004 External T.I. 2003-0037425 - Application of Section 84.1

A farming partnership between a husband and wife transfers its business to a newly-incorporated corporation ("Opco") whose common shares are held...

12 June 2003 External T.I. 2003-0019725 F - Sale of Holding' Shares to OPCO

Three unrelated individuals (X, Y and Z), in addition to holding some of the shares of Opco directly, also held Opco shares through their...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | 3 unrelated individuals likely acting in concert where they act without separate interests to achieve a basis step-up re transactions that are irrelevant to the business of the other party (Opco) | 217 |

26 March 2003 External T.I. 2003-0008645 F - Non-Arm's Length Sale of Shares

Regarding whether a transaction in which a holding company owned equally by a married couple (Mr. and Ms. B) sold 50% of the common shares of Opco...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | family relationship (e.g., uncle/nephew) are more likely to give rise to NAL transaction | 93 |

28 March 2003 External T.I. 2002-016665

Mr. and Mrs. A, and Mr. and Mrs. B, hold 26%, 12%, 26% and 12%, respectively of the common shares of a small business corporation (“OPc”) and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | 145 |

22 May 2001 External T.I. 2000-0047245 F - Divorce

Prior to their divorce, Mr. A transferred to Ms. A a portion of his shares of Opco and Ms. A exchanged her shares of Opco for freeze preferred...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | reciprocal transactions completed after divorce would be non-arm’s length | 268 |

15 February 2001 External T.I. 1999-0008405 F - Lien de dépendance

Y sold his wholly-owned corporation (Yco) to a corporation (Xco) owned by an unrelated individual (X), in consideration for $100,000 in cash ...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | holding of secured note for 80% of purchaser’s assets potentially could give rise to de facto control | 107 |

5 February 2001 External T.I. 2001-0067135 F - Dividend-General

A, an individual holding 50% of the shares of Bco, with a nominal ACB and PUC, sells those shares to Cco in consideration for a $100,000 note of...

4 November 1998 External T.I. 9801695 - WHETHER A PARTNERSHIP IS A TAXPAYER

A partnership that transfers shares will be considered to be a person and a taxpayer for purposes of s. 84.1.

23 December 1993 External T.I. 9326885 F - The Application of Section 84.1 of the Income Tax Act

RC's practice is to apply s. 84.1 where the conditions for its application are present given that its provisions do not give RC any administrative...

1993 A.P.F.F. Round Table Q. 4

It is not relevant to the application of s. 84.1 whether the subject corporation and the purchaser corporation were connected before the...

29 January 1990 T.I. (June 1990 Access Letter, ¶1264)

The sale by Mr. and Mrs. A of all the shares of Holdco to a corporation owned by their daughter and son-in-law in consideration for a promissory...

18 December 1989 T.I. (May 1990 Access Letter, ¶1220)

An estate which acquires shares of a deceased person under a testamentary trust acquires the shares from a person with whom it was not dealing at...

October 1989 Revenue Canada Round Table - Q.11 (Jan. 90 Access Letter, ¶1075)

s. 84.1 will not apply where an individual taxpayer exchanges common shares of a corporation for preferred shares of the same corporation -...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 50 | |

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) | 75 |

18 Aug. 89 T.I. (Jan. 90 Access Letter, ¶1082)

s. 84.1 does not apply to the disposition by an individual of 1/2 of his common shares of Opco to Opco in exchange for preference shares of Opco...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110.6 - Subsection 110.6(2.1) | 67 | |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(5) | 87 |

Articles

Anthony Strawson, Timothy P. Kirby, "Vendor Planning for Private Corporations: Select Issues", 2017 Conference Report, (Canadian Tax Foundation), 11:1-28

Use of holding companies to create CDA and s. 84.1, to defer tax on a sale by individual shareholders (pp. 11:19-20)

- Opco is a CCPC.

- Opco has an...

David Wilkenfeld, "Section 84.2 Update", Tax for The Owner-Manager, Vol. 2, No. 1, January 2002.

Paragraph 84.1(1)(a)

Administrative Policy

31 August 2005 Internal T.I. 2005-0134831I7 F - Capital Gains Exemption Strip

Each of two brothers, who already held some of “their” shares of Opco through their respective holding companies (Holdco 1 or Holdco 2) had,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | the use of s. 40(3.6)(b) for surplus-stripping purposes would be referred to the GAAR Committee | 122 |

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(3.6) | individuals holding high-ACB/low-PUC prefs and low ACB/PUC common shares preserved that ACB under s. 40(3.6)(b) for surplus-stripping purposes on their prefs’ redemption | 91 |

25 March 1999 External T.I. 9806475 F - ACCESSING SURPLUS AS ALLOWED BY S. 84.1

Alfred wholly owned Bco and Aco. The ACB of his Aco shares was subject to a reduction under s. 84.1(2)(a) or 84.1(a.1).

Alfred transferred his...

Paragraph 84.1(1)(b)

Administrative Policy

11 October 2019 APFF Roundtable Q. 1, 2019-0819401C6 F - Interaction between par. 84.1(1)(b) and 129(1(a)

In 2002-0128955, CRA indicated that a deemed dividend under s. 84.1(1)(b) would not generate a dividend refund (DR). CRA has now stated:

[W]e have...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 129 - Subsection 129(1) | reversal of position that s. 84.1(1)(b) dividends do not generate dividend refunds | 144 |

25 November 2012 Roundtable, 2013-0479401C6 F - Employés et Achat Ltée commentaires panel ARC

In order to facilitate the disposition of shares of departing employees who had purchased their shares under an employee share ownership plan,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | Buyco that is formed by employer to purchases departing employees’ shares is NAL | 118 |

5 October 2012 APFF Roundtable, 2012-0454091C6 F - GRIP and deemed dividend pursuant to 84.1(1)(b)

Mr and Mrs X hold all the shares of Corporation A and B, respectively (both private corporations). Mr X sells all his shares of Corporation A to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(14) | s. 84.1 deemed dividend paid to an individual could be an eligible dividend notwithstanding him not being a shareholder of the payer | 269 |

30 May 2007 External T.I. 2006-0183851E5 F - Paragraphs 83(2) and 84.1(1)

Mr. X transfers high-low preferred shares of Opco 1 to Opco 2 (both held by him and related persons) in consideration for a note, such that he is...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 83 - Subsection 83(2) | s. 83(2) election can be made on a s. 84.1 deemed dividend | 152 |

Subsection 84.1(2) - Idem [Non-arm’s length sale of shares]

See Also

Emory v. The Queen, 2010 DTC 1074 [at at 2901], 2010 TCC 71

The taxpayer and another individual ("Chen") owned 27% and 73%, respectively of the shares (being common shares) of a corporation ("Sona"). S....

Administrative Policy

25 July 1994 External T.I. 9407865 - 85(4)

Where a transferor has acquired a subject share from a non-arm's length individual, the amount of any capital gain realized by the non-arm's...

13 April 1994 External T.I. 9405015 - NON-ARM'S LENGTH SALE OF SHARES

An individual owns all the voting shares of a corporation ("Opco") and shares (including non-voting special shares) of Opco representing...

30 November 1991 Round Table (4M0462), Q. 10.1 - Non-Arm's Length Relationship and Death (C.T.O. September 1994)

Shares acquired by a taxpayer from his deceased spouse are acquired from a person with whom the taxpayer is not dealing at arm's length and are,...

Paragraph 84.1(2)(a.1)

See Also

Pomerleau c. La Reine, 2016 TCC 228, aff'd 2018 FCA 129

The family Opco was held by a holding company (Groupe Pomerlau Inc.), whose Class F shares were held by the taxpayer, his mother and his three...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | abusive avoidance of s. 84.1 by converting soft into hard ACB | 261 |

Côté-Létourneau v. The Queen, 2010 DTC 1116 [at at 3092], 2007 TCC 91

The Court rejected a submission of the taxpayers that shares issued to them by a corporation were not acquired by them: in order for them to...

Administrative Policy

2017 Ruling 2016-0629511R3 - Post-Mortem Planning and Extraction of "Hard ACB"

CRA ruled on a pipeline involving Opco shares inherited by an individual whose ACB consisted of both “soft” ACB (attributable to V-Day value...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | pipeline transfers of shares with both “soft” and “hard” ACB | 663 |

9 October 2015 APFF Roundtable Q. 14, 2015-0595631C6 F - Indirect Monetization of CGD

Following Descarries, CRA will no longer issue rulings in which an individual can in effect use shares (e.g., preferred shares) whose ACB was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | Descarries not consistent with use of ACB on a previous capital gains crystallizatin to create a capital loss for use on a sale | 169 |

9 October 2015 APFF Roundtable Q. 7, 2015-0595561C6 F - Computation of adjusted cost base and section 84.1

The capital gains deduction was claimed in the terminal return of an individual (X) for shares which were bequeathed to his son, and the son then...

10 August 2015 External T.I. 2015-0602751E5 - Capital gains deduction and section 84.1

The taxpayer and his wife acquire all the shares, qualifying as qualified small business corporation shares, of a corporation (the "Corporation")...

6 February 2004 Internal T.I. 2003-0052831I7 F - Application of subparagraph 84.1(2)(a.1)(ii)

The TSO proposed to assess a deemed dividend arising on the redemption by the taxpayer (“Daughter”) of Class D preferred shares (of...

Finance

2017 CTF Finance Roundtable, Q.9

Finance is struggling with whether it is possible to provide relief for intergenerational transfers of businesses without generating quite...

2017 CTF Finance Roundtable, Q.8

There will not be a complete carve-out for pipeline transactions. It is difficult to see how the current results obtained using pipelines do not...

Articles

Joint Committee, "Part D of Tax Planning Using Private Corporations – “Converting Income into Capital Gains” Proposals", 2 October 2017 Joint Committee Submission

Effect of expanded rule on post-mortem transfers (pp. 8-14)

The expanded s. 84.1 rule produces a greater impediment to the transfer of family...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 246.1 | 512 |

Subparagraph 84.1(2)(a.1)(ii)

Cases

Pomerleau v. Canada, 2018 FCA 129

An individual taxpayer engaged in transactions to extract surplus from a family holding corporation (Groupe Pomerleau Inc.) to the extent that the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | purpose of s. 84.1 was broader than the application of its words | 487 |

Administrative Policy

10 October 2024 APFF Roundtable Q. 12, 2024-1028931C6 - Article 84.1 L.I.R.

(a)

In 2020, Mr. X married the daughter of Mr. Y and also acquired the shares of PME Inc. from Mr. Y (who claimed the capital gains exemption). In...

2021 Ruling 2021-0887301R3 F - Post-mortem pipeline transaction

Father bequested his shares of an investments holding company (Aco) directly to his surviving wife (Mother) and to a spousal trust (Trust) for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | double pipeline entailing the application of s. 84.1 and s. 88(1)(d) bump | 368 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(d.3) | application of s. 88(1)(d.3) to pipeline involving shares that had been stepped up under s. 104(4) | 141 |

2021 Ruling 2021-0907591R3 F - Post-mortem Pipeline

X died holding all the shares of Holdco (an investment management company). X and a non-arm’s length individual had claimed the s. 110.6(2.1)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | pipeline transactions (coupled with s. 88(1)(d) bump) for which the deceased had claimed a capital gains deduction | 365 |

28 May 2010 External T.I. 2010-0359871E5 F - Déduction pour gain en capital

Qualified small business corporation shares are disposed of by the taxpayer to a child for FMV proceeds during the taxpayer’s lifetime or on...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110.6 - Subsection 110.6(2.1) | deduction available on NAL disposition inter vivos or on death | 141 |

17 March 2005 External T.I. 2005-0118601E5 F - Sale of Shares-Transfer of Family Business

An individual ("A") wholly-owning Holdco, held Holdco common shares with a nominal FMV, ACB and PUC, and Holdco preferred shares having an FMV of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | GAAR could apply where previous capital gains crystallization transaction indirectly generated a capital loss on a pref redemption transaction | 445 |

15 April 2002 External T.I. 2002-0128145 F - 84.1(2)(a.1) of the Act

Mr. X exchanges all the common shares of Opco (the “old common shares”), which are qualified small business corporation shares and have a...

Paragraph 84.1(2)(b)

Administrative Policy

23 June 2010 Internal T.I. 2010-0368161I7 F - 84.1

Three individuals (A, B, and C) each held 1/3 of the shares of Holdco, and Holdco and another individual, D, each held ½ of the shares of Opco. ...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2.2) - Paragraph 84.1(2.2)(b) | s. 84.1(2.2)(b) group can include a non-voting shareholder | 125 |

7 December 2004 External T.I. 2004-0104321E5 F - Non Arm's Length Sale of Shares

A was one of eight individuals holding all of the shares (of a single class) of Opco. (Specifically, each of A, B, C and D held 18.75%, and each...

Paragraph 84.1(2)(e)

Administrative Policy

11 December 2024 External T.I. 2024-1039101E5 F - Vertical amalgamation & former paragraph 84.1(2)(e)

S. 84.1(2.3)(a)(i), as part of the former (private-member bill) intergenerational business transfer rules, provided that if, otherwise than by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(2) - Paragraph 87(2)(j.6) | s. 87(2)(j.6) does not apply for purposes of the “old” s. 84.1(2)(e) intergenerational transfer rules | 147 |

15 February 2023 External T.I. 2022-0953991E5 F - Paragraph 84.1(2)(e) and amalgamation

S. 84.1(2)(e) as it currently read deemed a taxpayer who had disposed of qualified small business corporation shares or shares of the capital...

15 December 2021 External T.I. 2021-0907881E5 - Bill C-208 - Entry into Force

Did the amendments to s. 84.1 pursuant to Bill C-208 (did not contain a coming into force provision) apply to dispositions of shares that occurred...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Retroactivity/Retrospectivity | no "necessary implication” that amendments applied to dispositions before Royal Assent | 225 |

Articles

Allan Lanthier, "The general anti-avoidance rule and family surplus strips", Canadian Accountant, 12 August 2021

Overview of s. 84.1(2)(e)

- S. 84.1(2)(e) indicates that an individual selling qualified small business shares or shares of a family farm or...

Allan Lanthier, "Tax relief for family business transfers: A legislative fiasco – Part I / Tax relief for family business transfers: A legislative fiasco – Part II", Canadian Accountant, 8 July 2021 (Part I) and 9 July 2021 (Part II)

Overview

- Bill C-208 generally provides that an individual selling qualified small business shares or shares of a family farm or fishing...

Subsection 84.1(2.1)

Administrative Policy

29 May 2018 STEP Roundtable Q. 17, 2018-0744141C6 - S.84.1 and Capital Gains Reserve

S. 84.1(2.1) indicates that for purposes of the adjusted cost base reduction under s. 84.1(2)(a.1)(ii)) respecting a non-arm’s length transfer...

28 April 2016 External T.I. 2015-0594461E5 - Subsection 84.1(2.1)

Does the phrase “the amount in respect of which a deduction under section 110.6 was claimed in respect of the transferor’s gain from the...

Subsection 84.1(2.2)

Paragraph 84.1(2.2)(b)

Administrative Policy

23 June 2010 Internal T.I. 2010-0368161I7 F - 84.1

Three individuals (A, B, and C) each held 1/3 of the shares of Holdco, and Holdco and another individual, D, each held ½ of the shares of Opco. ...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2) - Paragraph 84.1(2)(b) | s. 84.1(2)(b) inapplicable to individual’s transfer of ½ of Opco to Holdco (owned by 3 unrelated individuals) for note and non-voting pref | 212 |

Subsection 84.1(2.3)

Paragraph 84.1(2.3)(a)

Administrative Policy

3 May 2022 CALU Roundtable Q. 3, 2022-0928721C6 - Recent Changes to Section 84.1

The Taxpayer, age 65, retired in the summer of 2021 and thereupon sold and transferred (the “First Disposition”) all the shares (the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2.3) - Paragraph 84.1(2.3)(b) | purported s. 84.1(2.3)(b) numerical limitation is meaningless and of no effect | 111 |

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2.3) - Paragraph 84.1(2.3)(c) | documentary requirements are mandatory | 132 |

Paragraph 84.1(2.3)(b)

Administrative Policy

3 May 2022 CALU Roundtable Q. 3, 2022-0928721C6 - Recent Changes to Section 84.1

S. 84.1(2.3)(b) appears to be targeted at reducing the capital gains deduction calculated under ss. 110.6(2) or (2.1) based on the taxable capital...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2.3) - Paragraph 84.1(2.3)(a) | disposition is “by reason of death” if a causal link/ if s. 84.1(2.3)(a) applies, s. 84.1 inapplicable if the transaction with the purchaser is not within s. 84.1 | 587 |

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2.3) - Paragraph 84.1(2.3)(c) | documentary requirements are mandatory | 132 |

Paragraph 84.1(2.3)(c)

Administrative Policy

3 May 2022 CALU Roundtable Q. 3, 2022-0928721C6 - Recent Changes to Section 84.1

S. 84.1(2.3)(c) provides that the taxpayer must provide the Minister with an independent assessment of the FMV of the subject shares and an...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2.3) - Paragraph 84.1(2.3)(a) | disposition is “by reason of death” if a causal link/ if s. 84.1(2.3)(a) applies, s. 84.1 inapplicable if the transaction with the purchaser is not within s. 84.1 | 587 |

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2.3) - Paragraph 84.1(2.3)(b) | purported s. 84.1(2.3)(b) numerical limitation is meaningless and of no effect | 111 |

Subparagraph 84.1(2.3)(c)(ii)

Administrative Policy

17 June 2025 STEP Roundtable Q. 2, 2025-1051581C6 - Succession of Family Business

Can shares (which do not amount to control) of the purchaser corporation be held by a trust where the parent is a contingent beneficiary in the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2.31) - Paragraph 84.1(2.31)(d) | trustees are not considered to be owners of the shares held by the trust | 223 |

| Tax Topics - General Concepts - Ownership | trustee are not owners of shares in the corpus | 57 |

Paragraph 84.1(2.3)(i)

Administrative Policy

10 October 2024 APFF Roundtable Q. 2, 2024-1028371C6 - Transfert intergénérationnel d’entreprise – nouvelles règles

A parent wishes to access the s. 84.1(2.31) or (2.32) rules regarding a transfer of shares of Parent Inc. (constituting qualified small business...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2.32) - Paragraph 84.1(2.32)(c) - Subparagraph 84.1(2.32)(c)(i) | retention of special voting shares by parent would preclude access to s. 84.1(2)(e) exception | 222 |

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2.32) - Paragraph 84.1(2.32)(a) | s. 84.1(2)(e) exception is available only for the 1st disposition if the subject corporation shares are sold in tranches | 315 |

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2.32) - Paragraph 84.1(2.32)(f) - Subparagraph 84.1(2.32)(f)(ii) | s. 84.1(2.32)(f)(ii) not satisfied if substantial unpaid purchase price at end of 10 years | 171 |

Subsection 84.1(2.31)

Paragraph 84.1(2.31)(a)

Administrative Policy

9 October 2025 APFF Roundtable Q. 6, 2025-1071481C6 F - Transfert intergénérationnel d’entreprise – entité pertinente du groupe

An individual (X) held all the shares of Opco, which were qualified small business corporation shares (QSBCS) and also held all the shares of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2.32) - Paragraph 84.1(2.32)(a) | no prohibition against the use of the intergenerational transfer rules on a simultaneous sale of 2 QSBCS corps (one a specified group entity) to a childco | 221 |

3 December 2024 CTF Roundtable Q. 10, 2024-1038231C6 - Intergenerational Business Transfers

One of the “intergenerational transfer” rule requirements, in s. 84.1(2.31)(a) or (2.32)(a), is that a previous inter-generational exception...

Paragraph 84.1(2.31)(b)

Subparagraph 84.1(2.31)(b)(ii)

Administrative Policy

17 June 2025 STEP Roundtable Q. 1, 2025-1051571C6 - Succession of Family Business

Regarding the requirement in the intergenerational transfer rules in ss. 84.1(2.31) and (2.32) for control of the purchaser corporation by the...

Subparagraph 84.1(2.31)(b)(iii)

Administrative Policy

18 September 2025 CLHIA Roundtable Q. 2, 2025-1067931C6 - Deemed Value of Life Insurance and QSBC

S. 110.6(15)(a)(i) applied for purposes of the requirement in ss. 84.1(2.31) and (2.32) that the subject shares be qualified small business...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110.63 - Subsection 110.63(1) - Qualifying Canadian Entrepreneur Incentive Property | application of s. 110.6(15)(a)(i) to “qualifying Canadian entrepreneur incentive property” definition | 62 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Qualifying Business Transfer | non-application of s. 110.6(15)(a)(i) to “qualifying business transfer” definition | 62 |

Paragraph 84.1(2.31)(c)

Administrative Policy

18 February 2025 External T.I. 2024-1038891E5 - De facto control

A corporation controlled by an adult child acquires all the shares of a subject corporation from the child’s parents, who cease involvement in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | a large term note owing by a child’s purchaser corporation to the parents would not by itself give the parents de facto control under s. 84.1(2.31)(c) | 286 |

Articles

Marissa Halil, David Carolin, Manu Kakka, "Are Section 84.1 Intergenerational Transfers (Mission) Impossible? The Meaning of “De Facto Control” in the Context of Subsection 84.1(2.31)", Tax for the Owner-Manager, Vol. 25, No. 1, January 2025, p. 1

Accommodation of 3-year retention of management while requirement to immediately relinquish de facto control (p.1)

- The immediate...

Subparagraph 84.1(2.31)(c)(iii)

Administrative Policy

15 December 2025 External T.I. 2025-1062551E5 F - Relevant Group Entity

Mr. X owned all the voting shares (with a nominal value) of A, B and D, and held preferred shares of A with a substantial value. D carried on an...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | being the lessor to the subject corporation likely does not signify de facto control | 63 |

2 December 2025 CTF Roundtable Q. 6, 2025-1080701C6 - Intergenerational Business Transfer – Relevant Group Entity

The control test, contained in s. 84.1(2.31)(c), generally requires that the parent(s) not have de facto control, after the disposition to the...

6 May 2025 External T.I. 2024-1010641E5 F - Relevant Group Entity

Mr. A wholly owned both Opco, whose shares qualified as qualified small business corporation shares (QSBCS), and Holdco, which leased commercial...

29 April 2025 External T.I. 2024-1036641E5 F - Relevant Group Entity

Two spouses were the equal shareholders of Opco, which was a small business corporation selling telecommunications services. One of the spouses...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2.32) - Paragraph 84.1(2.32)(c) - Subparagraph 84.1(2.32)(c)(iii) | continued control of the related lessor to an Opco would violate the s. 84.1(2.32)(c)(iii) condition on a sale of Opco to a child’s purchaser corporation | 262 |

Paragraph 84.1(2.31)(d)

Administrative Policy

17 June 2025 STEP Roundtable Q. 2, 2025-1051581C6 - Succession of Family Business

Could shares which did not amount to control of the particular corporation be held by a trust where the parent and the parent's spouse or...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2.3) - Paragraph 84.1(2.3)(c) - Subparagraph 84.1(2.3)(c)(ii) | person does not have an interest in a trust if it is contingent on the death of a person | 229 |

| Tax Topics - General Concepts - Ownership | trustee are not owners of shares in the corpus | 57 |

Paragraph 84.1(2.31)(f)

Subparagraph 84.1(2.31)(f)(i)

Administrative Policy

2 December 2025 CTF Roundtable Q. 5, 2025-1080691C6 - Intergenerational Business Transfer – control requirement in subparagraphs 84.1(2.31)(f)(i) and (2.32)(g)(i)

The intergenerational transfer rules include (in s. 84.1(2.31)(b)(ii) or s. 84.1(2.32)(b)(ii)) a requirement that one or more children of the...

Subparagraph 84.1(2.31)(f)(ii)

Administrative Policy

4 June 2024 STEP Roundtable Q. 6, 2024-1003601C6 - Succession of a Family Business

A. Assuming that a group of children are the indirect purchasers of the subject shares, must it be the same individual who meets the “activity...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2.32) - Paragraph 84.1(2.32)(g) - Subparagraph 84.1(2.32)(g)(ii) | the activity test in s. s. 84.1(2.31)(f)(ii) or 84.1(2.32)(g)(ii) can be met by successive children and regarding only one out of multiple businesses | 289 |

Paragraph 84.1(2.31)(g)

Subparagraph 84.1(2.31)(g)(i)

Administrative Policy

9 October 2025 APFF Roundtable Q. 15, 2025-1071571C6 F - Transfert intergénérationnel d’entreprise et transfert de la gestion

Aco, wholly-owned by Mr. A, held 60% of the units of a general partnership (SENC) and Bco, wholly-owned by an arm’s length third party, held the...

Subsection 84.1(2.32)

Paragraph 84.1(2.32)(a)

Administrative Policy

9 October 2025 APFF Roundtable Q. 6, 2025-1071481C6 F - Transfert intergénérationnel d’entreprise – entité pertinente du groupe

One of the “intergenerational transfer” rule requirements, in s. 84.1(2.31)(a) or (2.32)(a), is that a previous inter-generational exception...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2.31) - Paragraph 84.1(2.31)(a) | simultaneous sale of QSBCS of an Opco and a Realtyco specified group entity to a childco could satisfy s. 84.1(2.31)(a) or (2.32)(a) | 162 |

10 October 2024 APFF Roundtable Q. 2, 2024-1028371C6 - Transfert intergénérationnel d’entreprise – nouvelles règles

A parent wishes to access the s. 84.1(2.31) or (2.32) rules regarding a transfer of the shares of Parent Inc. (which are qualified small business...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2.32) - Paragraph 84.1(2.32)(c) - Subparagraph 84.1(2.32)(c)(i) | retention of special voting shares by parent would preclude access to s. 84.1(2)(e) exception | 222 |

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2.3) - Paragraph 84.1(2.3)(i) | parent remaining as director of the subject corporation would entail a retention of management | 258 |

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2.32) - Paragraph 84.1(2.32)(f) - Subparagraph 84.1(2.32)(f)(ii) | s. 84.1(2.32)(f)(ii) not satisfied if substantial unpaid purchase price at end of 10 years | 171 |

Paragraph 84.1(2.32)(c)

Subparagraph 84.1(2.32)(c)(i)

Administrative Policy

10 October 2024 APFF Roundtable Q. 2, 2024-1028371C6 - Transfert intergénérationnel d’entreprise – nouvelles règles

A parent wishes to access the s. 84.1(2.31) or (2.32) rules regarding a transfer of Parent Inc. (whose shares constituted qualified small business...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2.3) - Paragraph 84.1(2.3)(i) | parent remaining as director of the subject corporation would entail a retention of management | 258 |

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2.32) - Paragraph 84.1(2.32)(a) | s. 84.1(2)(e) exception is available only for the 1st disposition if the subject corporation shares are sold in tranches | 315 |

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2.32) - Paragraph 84.1(2.32)(f) - Subparagraph 84.1(2.32)(f)(ii) | s. 84.1(2.32)(f)(ii) not satisfied if substantial unpaid purchase price at end of 10 years | 171 |

Subparagraph 84.1(2.32)(c)(iii)

Administrative Policy

29 April 2025 External T.I. 2024-1036641E5 F - Relevant Group Entity

The control test, contained in s. 84.1(2.31)(c), generally requires that the parent(s) not have de facto control, after the disposition to the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2.31) - Paragraph 84.1(2.31)(c) - Subparagraph 84.1(2.31)(c)(iii) | a Realtyco, whose shares qualified as QSBCS based on a related corporation’s active business, would be a “relevant group entity” on a sale of the latter’s shares | 244 |

Paragraph 84.1(2.32)(f)

Subparagraph 84.1(2.32)(f)(ii)

Administrative Policy

10 October 2024 APFF Roundtable Q. 2, 2024-1028371C6 - Transfert intergénérationnel d’entreprise – nouvelles règles

A parent wishes to access the s. 84.1(2.32) rules regarding a transfer of the shares of Parent Inc. (which are qualified small business...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2.32) - Paragraph 84.1(2.32)(c) - Subparagraph 84.1(2.32)(c)(i) | retention of special voting shares by parent would preclude access to s. 84.1(2)(e) exception | 222 |

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2.3) - Paragraph 84.1(2.3)(i) | parent remaining as director of the subject corporation would entail a retention of management | 258 |

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2.32) - Paragraph 84.1(2.32)(a) | s. 84.1(2)(e) exception is available only for the 1st disposition if the subject corporation shares are sold in tranches | 315 |

Paragraph 84.1(2.32)(g)

Subparagraph 84.1(2.32)(g)(i)

Articles

Patricia Houle, Vincent Dansereau, "Intergenerational Transfer of a Business: Is a Post-Sale Merger Problematic?", Canadian Tax Focus, Vol. 15, No. 3, August 2025, p. 1

Scope of s. 87(2)(j.6) (p. 1)

- Although s. 87(2)(j.6) deems the amalgamation of a purchaser corporation and subject corporation to be a...

Subparagraph 84.1(2.32)(g)(ii)

Administrative Policy

4 June 2024 STEP Roundtable Q. 6, 2024-1003601C6 - Succession of a Family Business

One of the requirements under the inter-generational transfer rules in proposed s. 84.1(2.31) (dealing with an immediate intergenerational...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2.31) - Paragraph 84.1(2.31)(f) - Subparagraph 84.1(2.31)(f)(ii) | activity threshold can be satisfied by successive children and in relation to only one out of multiple businesses | 371 |