Subsection 94.1(1) - Offshore investment fund property

Cases

Ludmer v. Attorney General of Canada, 2018 QCCS 3381, aff'd 2020 QCCA 697

The Canadian-resident taxpayers were shareholders of a BVI company (“SLT”) which, in turn, held notes issued by two foreign subsidiaries of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | recurring fee reduction amounts received for no work were income and taxable under s. 56(2) when directed to controlled company | 289 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4) - Paragraph 152(4)(a) - Subparagraph 152(4)(a)(i) | nature of the legal advice relied upon was unclear | 417 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(1) | improper advancing of “settlement” elements that were not sustainable | 45 |

| Tax Topics - Income Tax Regulations - Regulation 7000 - Subsection 7000(2) - Paragraph 7000(2)(d) | mere possibility of locking in value accretion each year did not crystallize the maximum amount of interest respecting the year | 484 |

| Tax Topics - General Concepts - Negligence, Fiduciary Duty and Fault | damages awarded against CRA for inter alia making unreasonable reassessments | 260 |

| Tax Topics - Income Tax Act - Section 3 - Paragraph 3(a) - Business Source/Reasonable Expectation of Profit | recurring fee reduction amounts received for no work were income from a source | 313 |

Barejo Holdings ULC v. Canada, 2016 FCA 304

Boyle J made a pre-hearing determination, pursuant to Rule 58, that two Notes held by St. Lawrence Trading, a non-resident entity, constituted...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(11) - Investment Contract | pointless to determine whether an instrument is debt for purposes of whole Act | 117 |

See Also

Gerbro Holdings Company v. Canada, 2016 TCC 173, briefly aff'd 2018 FCA 197

The taxpayer (“Gerbro”) was a Canadian investment corporation (owned by a family trust but with an elderly income beneficiary, so that Gerbro...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Onus | no taxpayer burden to displace assumptions of mixed fact and law | 71 |

| Tax Topics - Statutory Interpretation - Hansard, explanatory notes, etc. | Minister's statement was false | 130 |

| Tax Topics - Other Legislation/Constitution - Federal - Tax Court of Canada Rules (General Procedure) - Section 145 - Subsection 145(3) | expert's report did not include all the underlying data | 115 |

Barejo Holdings ULC v. The Queen, 2015 DTC 1216 [at at 1405], 2015 TCC 274, aff'd on other grounds 2016 FCA 304

An offshore fund ("SLT"), in which the taxpayer had an interest, invested in instruments (styled as "Notes") of non-resident subsidiaries of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(11) - Investment Contract | "notes" which tracked actively-managed reference pool of assets were "debt" | 732 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Investment Property | "notes" which tracked actively-managed reference pool of assets were "debt" and "indebtedness" | 184 |

| Tax Topics - Statutory Interpretation - Interpretation Act - Section 8.1 | quaere whether there is a federal law of "debt" or "charity" | 334 |

Administrative Policy

24 August 2023 Internal T.I. 2019-0810391I7 - Offshore Investment Fund Property:

What is a “portfolio investment” as used in s. 94.1(1)(b)?

After referring to earlier positions and Gerbro as to the meaning of "portfolio...

23 May 2013 IFA Round Table, Q. 1

Will s. 94.1 apply where a taxpayer invests in and earns income from a widely held offshore mutual fund in a country that does not levy an income,...

10 January 2011 Internal T.I. 2009-0342861I7 - Meaning of "portfolio investment" in 94.1(1)(b)

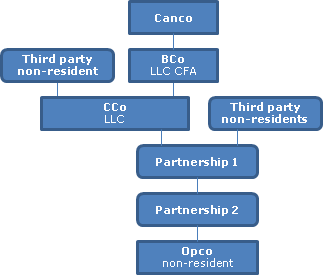

{kind=link}

Canco owns XX% of the voting membership interests in BCO, which is a CFA and an LLC. BCo owns XX% of the voting membership interests in CCo,...

28 August 2003 Internal T.I. 2003-0019767 F - Investissement dans une société étrangère

All the shares of Foreignco, which made investments in stock market shares, were held by Mr. A (apparently, non-resident). Mr. B (apparently,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Controlled Foreign Affiliate | redeemable convertible rights of a Canco investor in Foreignco were not shares, so that Foreignco was not a CFA | 141 |

| Tax Topics - Income Tax Act - Section 17 - Subsection 17(1) | redeemable convertible rights of a Canco investor in Foreignco had not been redeemed, so that they were not debt for s. 17 purposes and Foreignco was not a CFA | 141 |

90 C.R. - Q46

"Portfolio investments" are not confined to interests in non-resident entities which derive their value from passive investments or from those...

25 April 1990 Memorandum (September 1990 Access Letter, ¶1424)

RC has not yet determined whether a beneficiary under discretionary trust, who receives income or capital completely at the discretion of the...

86 C.R. - Q.19

"Portfolio investment" generally has its meaning in commercial practice (e.g., investors, investment managers and investment promoters).

Articles

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 206 - Paragraph 206(1)(d.1) | 11 |

Morrie Hotter, "Foreign Investment Entity Update", Corporate Finance, Vol. XI No. 4, 2004, p. 1118.

Paragraph 94.1(1)(a)

Cases

Barejo Holdings ULC v. Canada, 2020 FCA 47

An offshore fund ("SLT"), in which the taxpayer had an interest, invested in instruments (labelled as "Notes") of non-resident subsidiaries of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Consistency | presumption of consistent expression is not absolute | 252 |

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(11) - Investment Contract | 3 tests for what constituted debt under s. 94.1(1)(a) | 300 |

| Tax Topics - Statutory Interpretation - Redundancy/ reading in words/ speaking in vain | presumption that Parliament was not speaking in vain | 54 |

See Also

Barejo Holdings ULC v. The Queen, 2018 TCC 200, aff'd 2020 FCA 47

Barejo Holdings ULC v. The Queen, 2015 TCC 274 responded to a Rule 58 question by finding that notes held by an open-ended investment fund...

Paragraph 94.1(1)(b)

Articles

Michael N. Kandev, Matias Milet, "Foreign Trusts", 2017 Annual CTF Conference draft paper

Main-reason test generally not met for foreign commercial trusts (pp. 19-20)

“[N]on-resident entity” is defined, at subsection 94.1(2), as...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 94 - Subsection 94(2) - Paragraph 94(2)(k.1) | 298 | |

| Tax Topics - Income Tax Act - Section 94.2 - Subsection 94.2(3) | 460 |

Paragraph 94.1(1)(g)

Administrative Policy

23 August 2023 Internal T.I. 2021-0882371I7 - Dividend payment and 94.1(1)(g)

A wholly-owned non-resident subsidiary (“CFA”) of Canco owned 50% of the common shares of a non-resident corporation (“FA”) which were...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Foreign Accrual Property Income - C | the quantum of offshore investment fund property income earned through a CFA is unaffected by dividends paid by that CFA | 138 |

Subsection 94.1(2) - Definitions

non-resident entity

Administrative Policy

9 June 1991 Memorandum (Tax Window, No. 4, p. 21, ¶1286)

A non-resident trust may be a "non-resident entity" if the tests in ss.94(1)(a) and (b) are met, even if neither ss.94(1)(c) or (d) causes anyone...