Paragraph 55(3.01)(a)

Administrative Policy

29 March 2021 External T.I. 2020-0839571E5 - Common-law partner

A and B, who have been cohabiting in a conjugal relationship for 10 years and who each owned 50% of the common shares of Opco, commenced on...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Common-Law Partner | ceasing to be common-law partners after 90 days of separation did not retroactively make them unrelated for prior transactions | 123 |

27 April 2004 External T.I. 2004-0062091E5 F - 55(3)(a)

The children shareholders of two corporations (S1 and S2) that have been controlled for a number of years by their parents, transfer a portion of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(4) | s. 55(4) inapplicable where parent retains control for the protection of parent’s economic interests | 173 |

Paragraph 55(3.01)(g)

Administrative Policy

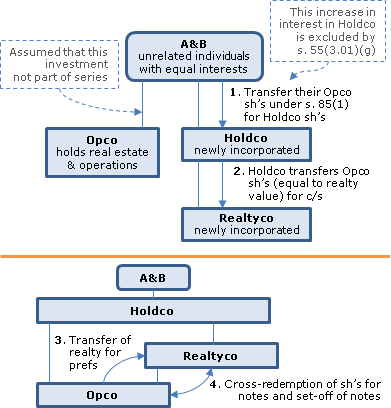

2024 Ruling 2023-0989121R3 F - Internal reorganization - 55(3)(a) and 55(3.01)(g)

Background

Prior to the preliminary transactions, Opco’s issued and outstanding shares were held by three unrelated individuals: Messrs. A and B...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(2) | 2 unrelated individuals were the settlors for each other’s family trust | 162 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | estate freeze transactions represented to be independent of subsequent transfer | 152 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) - Subparagraph 55(3)(a)(ii) | s. 55(3.01)(g) applied to the transfer (fresh after an estate freeze) by unrelated shareholders of Opco to a new Holdco, with an Opco realty spin-off to a new Realtyco sister | 274 |

2015 Ruling 2015-0605901R3 F - Présomption de gain en capital

Background. Opco, a CCPC, in addition to holding residential condos on upper floors, holds the “Vacant Premises” for the purpose of leasing...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) - Subparagraph 55(3)(a)(ii) | spin-off of real estate beneath new common holdco of unrelated shareholders | 107 |

| Tax Topics - Income Tax Act - Section 249.1 - Subsection 249.1(7) | taxation year end changed to immediately before building spin-off | 95 |

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(1) - Paragraph 186(1)(b) | year end selection to avoid Pt. IV circularity | 97 |

14 April 2015 External T.I. 2015-0570021E5 F - Présomption de gain en capital

{kind=link}

After referring to the CRA response to Q. 14(b) [16(b) below?] at the 2014 APFF Roundtable including the caution provided, the questioner...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) | application of safe harbour where holdco interposed before spin-off transaction | 62 |

10 October 2014 APFF Roundtable Q. 16, 2014-0538031C6 - APFF 2014 Q. 16 - Capital gain

Facts

The exception in s. 55(3)(a) would not be available where a new corporation was created in the series. Consider this example:

- Husband,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(2) - Paragraph 251(2)(b) - Subparagraph 251(2)(b)(i) | incorporator related to corporation | 67 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) | interposition of holdco to permit related-person spin-off compliant with s. 55(3)(a)(ii) and (v) | 933 |

Articles

David Carolin, Manu Kakkar, Boris Volfovsky, "Tax Alchemy and Paragraph 55(3.01)(g): Converting a 55(3)(b) Divisive Reorganization into a 55(3)(a) Related-Party Butterfly", Tax for the Owner-Manager, Vol. 24, No. 1, January 2024, p. 7

Spin-off of real estate by Opco owned by 2 arm’s length shareholders does not comply with s. 55(3)(a) (p. 7)

Opco is owned on an 85-15 basis by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) | interposition of a Middleco in a spin-off transaction can put it back onside s. 55(3)(a) | 157 |