Words and Phrases - "insolvent"

16 December 2003 Internal T.I. 2003-0046167 F - Section 50- Shares of Insolvent Corporation50(1)

Summary Under

Tax Topics - Income Tax Act - Section 50 - Subsection 50(1) - Paragraph 50(1)(b) - Subparagraph 50(1)(b)(iii)corporation not insolvent if affiliates intend to pay its creditors, and its shares have value if it has non-capital losses

Parentco elected (in reliance on s. 50(1)(b)(iii)) under s. 50(1) respecting its shares of one of a wholly-owned subsidiary ("Lossco") with...

Words and Phrases

insolvent| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(b) | sale of Lossco with no assets but non-capital losses for nil consideration to another subsidiary generated a gain under s. 69(1)(b) | 125 |

| Tax Topics - General Concepts - Fair Market Value - Shares | shares of corporation that had ceased business and had no assets but had non-capital losses had a significant value | 75 |

5 October 2012 APFF Roundtable, 2012-0454061C6 F - Transfer of a Lossco to a related corporation

lossco with no assets or liabilities cannot be insolvent

Example 1

{kind=link}

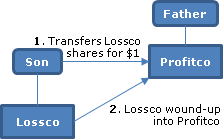

Son claims an ABIL under s. 50(1) with respect to his share investment in a wholly-owned corporation (Lossco), which had ceased active...

Words and Phrases

insolvent| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Shares | non-capital losses of corporation taken into account in valuing its shares | 162 |

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(1) - Paragraph 111(1)(a) | related but not affiliated transfer of Lossco shares to father's or brother's company | 267 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1.1) | lossco losses maintained on father-son or sibling transfers and s. 88(1.1) wind-up | 266 |

15 June 1998 Internal T.I. 9802347 - BUSINESS INVESTMENT LOSSES

A corporation that had made a general conveyance of all its assets to its shareholder in the course of voluntary dissolution proceeding, with the...

Words and Phrases

insolvent