Subsection 251(1) - Arm’s length

Paragraph 251(1)(a)

See Also

Kiperchuk v. The Queen, 2013 DTC 1088 [at at 486], 2013 TCC 60

The taxpayer was the designated beneficiary of her husband's RRSP, and received the RRSP proceeds upon his death, and was assessed for his unpaid...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | 260 | |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(b) | 94 | |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | transfer time was relevant time | 185 |

Hickman v. The Queen, 2000 DTC 2584 (TCC)

The taxpayer disposed of shares of a corporation to another corporation (“CSC”) all of whose shares were held by a family trust whose trustees...

Wright Estate v. The Queen, 96 DTC 1509 (TCC)

The taxpayer was an estate whose executors and trustees were the son (John) and accountant (Gordon) of the deceased. Gordon had married the widow...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | testamentary trust dealt at arm's lenght with three beneficiaries (2 of them, administrators) who did not get along | 97 |

Administrative Policy

S1-F5-C1 - Related Persons and Dealing at Arm's Length

Trust can be related to persons who are related to its trustee

1.47 Subsection 104(1) provides that a reference to a trust is to be read to...

Paragraph 251(1)(b)

See Also

Kiperchuk v. The Queen, 2013 DTC 1088 [at at 486], 2013 TCC 60

The taxpayer was the designated beneficiary of her husband's RRSP, and received the RRSP proceeds upon his death, and was assessed for his unpaid...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | 260 | |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(a) | taxpayer was not related to her deceased husband | 110 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | transfer time was relevant time | 185 |

Administrative Policy

23 January 2001 External T.I. 2000-0045445 F - DETTE D'UN ACTIONNAIRE - FIDUCIE

Opco, makes an advance to a trust formed by it, of which it is the sole beneficiary, to assist it in acquiring a capital property. CCRA indicated...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2) | where Opco makes a loan to a wholly-owned trust, the loan is included in the trust’s income assuming that an Opco shareholder did not deal with it at arm’s length with Opco | 91 |

17 August 1999 APFF Roundtable Q. 20, 9921060 F - SOCIÉTÉ BÉNÉFICIAIRE D'UNE FIDUCIE

CCRA noted that the addition of s. 251(1)(b) could cause a corporate (CCPC) beneficiary of personal trust to be related under ss. 186(2) and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(4) - Paragraph 186(4)(a) | addition of s. 251(1)(b) caused a corporate beneficiary of personal trust to be related under ss. 186(2) and 186(4)(a) to dividend payer respecting dividend designated to it under s. 104(19) | 163 |

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Capital Dividend Account - Paragraph (a) | no CDA addition re dividend designated to CCPC as a taxable capital gain under s. 104(21) | 52 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(c) | s. 104(19) dividend can come out of safe income | 101 |

Articles

Jeffrey T. Love, Kenneth R. Hauser, "How Various Aggregation Rules Apply to Trusts", 2018 Conference Report (Canadian Tax Foundation), 28: 1-79

CRA application of s. 251(1)(b) (p. 28:52)

The CRA considered the application of paragraph 251(1)(b) to a situation in which a person was a...

Paragraph 251(1)(c)

Cases

Carter v. The King, 2024 TCC 71

The appellant, her cousin (“McAllister”) and her father held 40%, 40% and 20% of the common shares of Brown’s Paving Ltd. (“BPL”),...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) | s. 84.1 did not apply to a sale of the taxpayer’s Opco shares to her cousin’s holdco for cash funded by an Opco dividend | 442 |

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(2) | no evidence that controlling shareholder of Opco did not deal at arm’s length with the holding company which was alleged to control Opco under s. 186(2) | 136 |

Canada (The King) v. MICROBJO PROPERTIES INC., 2023 FCA 157

The taxpayers, who were holding companies for partnerships that had recently agreed to sell their farmlands to third parties, were approached by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | a transaction that split, on the purchaser’s terms, a tax savings purportedly generated by it, was a non-arm’s length transaction | 701 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | taxpayers did not intend to avoid (and were oblivious to) s. 160 | 265 |

| Tax Topics - Statutory Interpretation - Interpretation Act - Subsection 45(2) | subsequent amendment confirmed the prior state of the law | 82 |

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(5) | s. 160(5) did not change the prior view that prior facts could be taken into account | 96 |

Keybrand Foods Inc. v. Canada, 2020 FCA 201

The taxpayer (“Keybrand”), its wholly-owning parent (“BWS”), and another Strassburger-family company were guarantors of loans made to a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) - Subparagraph 20(1)(c)(i) | interest was non-deductible on loan made to company that had no reasonable prospects of recovery | 335 |

| Tax Topics - General Concepts - Purpose/Intention | regard can be had to subsequent steps as confirmatory of the intent at the relevant time | 187 |

Louie v. Canada, 2019 FCA 255

From May 15 to October 17, 2009, the taxpayer directed 71 “swaps” under which TSX-listed shares were transferred between her self-directed...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 207.01 - Subsection 207.01(1) - Advantage - Paragraph (b) - Subparagraph (b)(i) | advantages generated in Year 1 from swap transactions continued to produce indirect advantages thereafter | 547 |

| Tax Topics - Income Tax Act - Section 207.06 - Subsection 207.06(2) | concerns about future value increases are intended to be addressed by relief provisions | 384 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | no necessity for predetermined endpoint or advance determination of price | 211 |

Aeronautic Development Corporation v. Canada, 2018 FCA 67

A Canadian corporation (ADC), which had issued voting common shares (representing voting control) for a modest amount to three Canadian employees,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | non-resident exercised de facto control of mooted CCPC under a development agreement | 646 |

Canada v. 9101-2310 Québec Inc., 2013 DTC 5172 [at at 6455], 2013 FCA 241

In order to defeat a claim of a bank, a tax debtor ("Garneau") deposited $305,000 with a corporation ("2310") (whose shareholder, Mr. Pratte, was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | transfer only of legal title may engage s. 160 | 200 |

Sheldon Inwentash and Lynn Factor Charitable Foundation v. Canada, 2012 FCA 136

In the course of finding that a trust, which was a charitable foundation, did not qualify as a public foundation as it had a single trustee (a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 149.1 - Subsection 149.1(1) - Public Foundation | 114 | |

| Tax Topics - Statutory Interpretation - Interpretation Act - Subsection 33(2) | contrary intention evident | 99 |

| Tax Topics - Statutory Interpretation - Ordinary Meaning | clear words dominate | 137 |

Labow v. Canada, 2012 DTC 5001 [at at 6501], 2011 FCA 305

In finding that the taxpayer, who employed his wife in his medical practice, did not deal at arm's length with an employee health trust which he...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 108 - Subsection 108(1) - Trust - Paragraph (a.1) | 213 | |

| Tax Topics - Income Tax Act - Section 75 - Subsection 75(3) | 213 |

Canada v. Remai, 2009 DTC 5188 [at at 6257], 2009 FCA 340

In order to make promissory notes that he had donated to a charitable foundation cease to be non-qualifying securities, the taxpayer arranged for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | no abuse in controlling funds established | 159 |

| Tax Topics - Statutory Interpretation - Redundancy/ reading in words/ speaking in vain | provision not to be interpreted such that it can never apply | 40 |

Canada v. McLarty, 2008 DTC 6354, 2008 SCC 26, [2008] 2 S.C.R. 79

In finding that an acquisition of seismic data by the taxpayer, acting through the vendor ("Compton") as his agent, was an arm's length...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(e) | consideration in form of non-recourse note was not contingent since it required the sale on maturity of pledged collateral if stipulated principal remained unpaid | 312 |

| Tax Topics - Income Tax Act - Section 66.1 - Subsection 66.1(6) - Canadian exploration expense - Paragraph (a) | limited recourse promissory note | 188 |

Canada v. Livingston, 2008 DTC 6233, 2008 FCA 89

In order to help her friend (Davies) defeat efforts of CRA to collect unpaid taxes from Davies, the taxpayer opened up a bank account in the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | transfer to an accommodation party was caught | 166 |

Petro-Canada v. Canada, 2004 DTC 6329, 2004 FCA 158

Joint exploration corporations (the "JECs") acquired seismic data from one of the two shareholders of each JEC at a purchase price substantially...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 66.1 - Subsection 66.1(6) - Canadian exploration expense - Paragraph (a) | no plan to use purchased seismic data | 144 |

| Tax Topics - Income Tax Act - Section 67 | paying more than FMV may not engage s. 67 | 109 |

| Tax Topics - General Concepts - Purpose/Intention | purpose test satisfied even if multiple purposes | 77 |

Deptuck v. Canada, 2003 DTC 5273, 2003 FCA 177

S.69(1)(a) applied to reduce the capital cost to a partnership of depreciable property purchased by it to the property's fair market value rather...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(a) | s. 69(1)(a) applies to a purchasing partnership as if it were a person | 156 |

| Tax Topics - Income Tax Act - Section 96 - Subsection 96(1) - Paragraph 96(1)(c) | 115 |

Brown v. Canada, 2003 DTC 5298, 2003 FCA 192 (FCA)

At the time a partnership, of which the taxpayer subsequently became a partner, negotiated an agreement for the acquisition of software, the same...

Dixon v. Deputy Attorney General of Canada, 91 DTC 5584 (Ont HCJ.)

An alleged transaction in which a corporation sold land at a substantial undervalue to another corporation in which its president ("Dixon") had a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Solicitor-Client Privilege | 160 | |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | 58 |

Peter Cundill & Associates Ltd. v. The Queen, 91 DTC 5085, [1991] 1 CTC 197 (FCTD), aff'd 91 DTC 5543 (FCA)

The taxpayer, which was the portfolio manager for the Cundill Value Fund and the Cundill Security Fund was dependent upon Mr. F. Peter Cundill,...

Millward v. The Queen, 86 DTC 6538, [1986] 2 CTC 423 (FCTD)

A company owned by the taxpayer mortgaged land in favour of an RRSP of the taxpayer's partner ("Coates") in his law firm and a company owned by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 4900 - Subsection 4900(4) | 128 |

Beaumont v. The Queen, 86 DTC 6264, [1986] 1 CTC 507 (FCTD), aff'd 88 DTC 6522, [1988] 2 CTC 365 (FCA)

Since the taxpayer was held to be dealing at arm's length with a corporation ("Clarebeau") 1/2 of whose shares were owned by the taxpayer's family...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(1) - Paragraph 7(1)(b) | 136 |

Special Risks Holdings Inc. v. The Queen, 86 DTC 6035, [1986] 1 CTC 201 (FCA)

Before finding that a corporation in which the taxpayer held 50% of the voting shares was subject to de facto control by the taxpayer in light of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(9) | 166 | |

| Tax Topics - Income Tax Act - Section 86 - Subsection 86(1) | 166 |

Windsor Plastic Products Ltd. v. The Queen, 86 DTC 6171, [1986] 1 CTC 331 (FCTD)

The three shareholders of the taxpayer, each of whom was a minority shareholder and one of whom was related to a non-resident corporation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(4) - Paragraph 212(4)(a) | shareholders acting in concert | 139 |

Robson Leather Co. Ltd. v. MNR, 74 DTC 6666, [1974] CTC 872 (FCTD), aff'd 77 DTC 5106, [1977] CTC 132 (FCA)

1/2 the shares of a company ("Appel Process") were held by a second company ("Robson Leather") 75% of whose shares were held by a trust whose...

Oryx Realty Corp. v. MNR, 74 DTC 6352, [1974] CTC 430 (FCA), aff'd in another respect in sub nom. MNR v. Shofar Investment Corp., 79 DTC 5347, [1979] CTC 433, [1980] 1 S.C.R. 350

On April 20, 1959, the taxpayer purchased land inventory, from a company ("Lanber") which was owned in the same proportions as itself, on...

Swiss Bank Corp. et al. v. Minister of National Revenue, 72 DTC 6470, [1972] CTC 614, [1974] S.C.R. 1144

The manager ("SIP") of a Swiss fund incorporated an Ontario company ("City Park") to serve as a vehicle for the investment of monies of the Fund...

Pender Enterprises Ltd. v. MNR, 65 DTC 5202, [1965] CTC 343 (Ex Ct)

The sale by an individual of his business to a corporation owned equally by his brother-in-law and cousin (who also were senior employees of his...

Rolka v. MNR, 62 DTC 1394, [1962] CTC 637 (Ex Ct)

The taxpayer was found to indirectly control, and therefore not to be dealing at arm's length with, a corporation ("Nelmar") for purposes of what...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Solicitor-Client Privilege | 26 | |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | 49 |

Golden Arrow Sprayers Ltd. v. MNR, 61 DTC 1185, [1961] CTC 318 (Ex Ct)

The transfer of patent rights by an individual to a newly-incorporated corporation of which he was to be the controlling shareholder and the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Schedules - Schedule II - Class 14 | patents were Classs 14 property | 51 |

Ancaster Development Co. Ltd. v. MNR, 61 DTC 1047, [1961] CTC 91 (Ex Ct)

The taxpayer, whose three shareholders were Rolka, Young and Atkinson each holding 45%, 45% and 10% of its shares, respectively, sold land at its...

MNR v. Kirby Maurice Co. Ltd., 58 DTC 1033, [1958] CTC 41 (Ex Ct)

A proprietor of a business who wished to incorporate it, directed his solicitors to incorporate a corporation, and instructed them as to the terms...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Schedules - Schedule II - Class 14 | 150 |

MNR v. Granite Bay Timber Co. Ltd., 58 DTC 1066, [1958] CTC 117 (Ex Ct), briefly aff'd 59 DTC 1262 (SCC)

The liquidator of a company, who was one of its three shareholders, distributed all the property of the company to the shareholders subject to the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(1) - Transaction | 112 |

Minister of National Revenue v. Sheldon's Engineering Ltd., 55 DTC 1110, [1955] CTC 174, [1955] S.C.R. 637

When the minority shareholders of a company (the "Old Company") learned that the majority shareholders were going to sell their shares of the Old...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Resolving Ambiguity | 11 |

See Also

Homburg v. The King, 2025 TCC 162

At issue was whether the s. 110(1)(d) deduction was available to the taxpayer in respect of his exercise of options that had been granted to him...

Harvard Properties Inc. v. The King, 2024 TCC 139

A Calgary shopping mall was sold by Harvard Properties and the other co-owners to a third party (“Abacus”) in a share sale transaction but at...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | sale of shares, in a structured transaction, at a price that did not reflect a discount for the underlying accrued taxes, was indicative of non-arm's length dealing | 643 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | avoidance on a non-arm’s length relationship so as to avoid the application of s. 160 would be a GAAR abuse | 434 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(2) | GAAR alternative basis was not statute-barred where the primary assessment (under s. 160(2)) was not subject to statute-barring | 197 |

| Tax Topics - General Concepts - Fair Market Value - Shares | shares of company whose only assets were escrowed for an imminently-closing sale transaction did not have any value | 285 |

Godcharles v. Agence du revenu du Québec, 2021 QCCA 1843

A group of unrelated individuals were the co-owners of a seniors’ residence (“SR”), which was leased by them to the corporate operator of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 68 - Paragraph 68(a) | s. 68 reallocated between a retirement home’s business operations sold by one vendor and the home sold by the other vendors | 424 |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(b) - Subparagraph 69(1)(b)(i) | s. 69 cannot reduce inflated proceeds to vendor | 435 |

| Tax Topics - General Concepts - Fair Market Value - Land | goodwill portion of retirement residences business determined as the residual from valuing the residence using the cost method | 272 |

Godcharles v. Agence du revenu du Québec, 2020 QCCQ 2219, aff'd 2021 QCCA 1843

The taxpayers were a corporation (“9118”) and its eight individual shareholders who co-owned a fully-occupied retirement residence whose...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Land | retirement home valued using cost method with residual to goodwill | 127 |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(b) | transaction between parties acting in concert required increased allocation to the real estate sold at shareholder level | 318 |

Keybrand Foods Inc. v. The Queen, 2019 TCC 161, aff'd 2020 FCA 201

The taxpayer (“Keybrand”), its wholly-owning parent (“BWS”), and another Strassburger-family company were guarantors of loans made to a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) - Subparagraph 20(1)(c)(i) | interest was deductible on money borrowed to be lent at interest to company in default cf. money borrowed to acquire its shares when its collapse was imminent | 346 |

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(1) - Paragraph 39(1)(c) - Subparagraph 39(1)(c)(ii) | right of parent of taxpayer to elect majority of board of investee of X through chair’s casting vote entailed de facto control by taxpayer of X | 227 |

HLB Smith Holdings Limited v. The Queen, 2018 TCC 83

A company (“PES,” or the “Operating Company”) providing electricians’ services initially was owned on a 50-50 basis by two individuals...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | s. 160 liability flowed through with dividends paid to 50-50 unrelated shareholders | 154 |

Poulin v. The Queen, 2016 TCC 154, briefly aff’d sub nomine Turgeon v. The Queen, 2017 FCA 103

In the fall of 2007, the two equal individual shareholders (“Poulin” and “Turgeon”) of a Quebec construction corporation (“Amiante”)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) | sale to employee's Holdco with not upside and no risk for employee was non-arm's length | 261 |

Kiperchuk v. The Queen, 2013 DTC 1088 [at at 486], 2013 TCC 60

The taxpayer was the designated beneficiary of her husband's RRSP, and received the RRSP proceeds upon his death, and was assessed for his unpaid...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | 260 | |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(a) | taxpayer was not related to her deceased husband | 110 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(b) | 94 |

Wagner v. The Queen, 2012 DTC 1234 [at at 3645], 2012 TCC 8

An agreement between the taxpayers and an unrelated purchaser of their shares to allocate a portion of the amounts paid by the purchaser to the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 68 | 329 |

Alberta Printed Circuits Ltd. v. The Queen, 2011 DTC 1177 [at at 967], 2011 TCC 232

The taxpayer was a Canadian-controlled private corporation in the business of printing customized circuits, held 75% by a holding company for Mr....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) | internal CUP applied over TNMM | 197 |

| Tax Topics - Treaties - Income Tax Conventions - Article 26 | 96 | |

| Tax Topics - Treaties - Income Tax Conventions - Article 9 | 96 |

The Queen v. Yelle, 2010 DTC 5128 [at at 7083], 2010 ABPC 94

The taxpayer, who was a member of a partnership, was accused of tax evasion under s. 239(1)(a) in connection with capital cost allowance claims...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 13 - Subsection 13(21) - Undepreciated Capital Cost - A | 155 | |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(a) | 126 |

Brownco Inc. v. The Queen, 2008 DTC 2591, 2008 TCC 58

The taxpayer and its 50% shareholder were found not to be dealing with each other at arm's-length in light of the fact that the taxpayer agreed to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | 50% shareholder was entitled to one of two directors with tie-breaking vote | 196 |

McMullen v. The Queen, 2007 DTC 286, 2007 TCC 16

The taxpayer and an unrelated individual ("DeBruyn") accomplished a split-up of the business of a corporation ("DEL") of which they were equal...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | 270 | |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 198 | |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | 229 | |

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) | arm's length: negotiation based on self-interest | 257 |

Baxter v. The Queen, 2006 DTC 2642, 2006 TCC 230

Before going on to find that the taxpayer had purchased a sublicence of software from a person with whom he was dealing at arm's length (and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Other | 124 | |

| Tax Topics - Income Tax Act - Section 9 - Agency - Agency | 94 |

Brouillette v. The Queen, 2005 DTC 1004, 2005 TCC 203

The taxpayer facilitated a leveraged buy-out of him and his co-shareholder of a company ("Brouillette Automobiles") by incorporating a corporation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | 173 |

McLarty v. The Queen, 2005 DTC 217, 2005 TCC 55, rev'd 2006 DTC 6340, 2006 FCA 152, aff'd supra.

The purchase by the taxpayer of an undivided interest in seismic data in a transaction whose terms were set by a promoter nonetheless was an...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 66.1 - Subsection 66.1(6) - Canadian exploration expense - Paragraph (a) | 178 | |

| Tax Topics - Income Tax Act - Section 67 | 105 |

Morley v. The Queen, 2004 DTC 2604, 2004 TCC 280, briefly aff'd 2006 DTC 6351, 2006 FCA 171

An acquisition of software by a tax-shelter partnership was found not be an arm's length transaction in light of the very non-commercial nature of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Other Legislation/Constitution - Charter (Constitution Act, 1982) - Section 8 | 38 | |

| Tax Topics - General Concepts - Evidence | 32 | |

| Tax Topics - General Concepts - Fair Market Value - Other | 98 | |

| Tax Topics - General Concepts - Onus | 100 | |

| Tax Topics - Income Tax Act - Section 13 - Subsection 13(21) - Undepreciated Capital Cost - A | 177 | |

| Tax Topics - Income Tax Act - Section 13 - Subsection 13(27) - Paragraph 13(27)(d) | 88 | |

| Tax Topics - Income Tax Act - Section 96 | start-up activities sufficient to constitute carrying on business in common | 112 |

Siracusa v. The Queen, 2003 DTC 2106, 2003 TCC 941

The taxpayer, who owned one-third of the shares of a corporation that paid a dividend to its shareholders, and was a director and bookkeeper of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | 97 |

Martel v. The Queen, 2003 DTC 1187 (TCC)

The assets of a Canadian-controlled private corporation ("Gestion") consisted of the shares of two companies, the first of which ("2321") was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Corporate/Separate Personality | 65 | |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Small Business Corporation | 134 |

Lanester Sales Ltd. v. The Queen, 2003 DTC 997 (TCC), aff'd 2004 DTC 6461, 2004 FCA 217

After finding that the taxpayer (a franchisee) and the franchisor were dealing with each other at arm's length, Bowman A.C.J. stated (at p....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | no de facto control by franchisor | 130 |

Petro-Canada v. The Queen, 2003 DTC 94 (TCC), aff'd supra.

In order that Canadian exploration expenses of another oil and gas company ("Phillips" could be transferred to the taxpayer for purposes of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Evidence | 80 | |

| Tax Topics - General Concepts - Fair Market Value - Other | 44 |

Joncas v. The Queen, 2002 DTC 1813 (TCC), aff'd 2002 DTC 7060, 2002 FCA 234 (French)

A sale by the taxpayer of his shares of a company (Trans Côte) to a corporation (LBS) whose voting shares were equally owned by the taxpayer and...

Brown v. The Queen, 2001 DTC 1094 (TCC), aff'd supra 2003 DTC 5298 (FCA)

The purchase by a partnership of software from an American company ("ASC") was found to be a transaction between persons not dealing with each...

Campbell v. The Queen, 99 DTC 1073 (TCC)

A Bahamian company ("Helvetia") distributed all the shares of its Canadian subsidiary ("Quamco") equally to three trusts each of which owned...

MFC Bancorp Ltd. v. R., 99 DTC 905, [1999] 4 CTC 2468 (TCC)

A transfer by the taxpayer of its interest as lessor in mining concessions and railway rights-of-way to a corporation ("CJC") in which a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(4) | 99 |

Christensen v. The Queen, 98 DTC 1893, [1998] 4 CTC 2198 (TCC)

The transfer to the taxpayer of a property in which she had been living with a married man who controlled the corporate transferor was found to be...

H.T. Hoy Holdings Ltd. v. R., 97 DTC 1180, [1997] 2 CTC 2874 (TCC)

The taxpayer and an unrelated individual (Cloutier) were found to be dealing at arm's length in transactions through which the taxpayer indirectly...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(5) - Paragraph 251(5)(b) | 65 | |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(4) | 50 |

Lixo Investments Ltd. v. R., 97 DTC 1030, [1997] 2 CTC 2772 (TCC)

The corporate taxpayer was found to be dealing in arm's length with a non-resident corporation ("Slupy") which had provided most of the taxpayer's...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Subparagraph 212(1)(b)(vii) | 140 |

Robertson v. The Queen, 97 DTC 449, [1996] 2 CTC 2269 (TCC)

The taxpayer, who was the deputy chairman and a director of a public corporation ("Central Capital"), was found to be dealing at arm's length with...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Loss v. Loss | 36 | |

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(4) | 36 | |

| Tax Topics - Statutory Interpretation - Interpretation Act - Section 32 | s. 32 deals with departures from form rather than content | 43 |

RMM Canadian Enterprises Inc. v. R., 97 DTC 302, [1998] 1 C.T.C. 2300 (TCC)

A non-resident corporation ("EC") approached a business associate who, along with two other individuals, formed a Canadian corporation ("RMM") to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 159 - Subsection 159(3) | 167 | |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | 188 | |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 235 | |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | application of s. 84(2) to sale of cash-rich company to accommodation party who quickly paid cash proceeds therefor | 222 |

| Tax Topics - Treaties - Income Tax Conventions | 96 | |

| Tax Topics - Treaties - Income Tax Conventions - Article 10 | 116 |

McNichol v. R., 97 DTC 111, [1997] 2 CTC 2088 (TCC)

In order to effectively receive the cash held by a corporation ("Bec") owned by them, the taxpayers found a corporate purchaser to purchase their...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 234 | |

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | 191 |

Davidson Estate v. The Queen, 96 DTC 1652, [1996] 3 CTC 2900 (TCC)

The estate of a deceased taxpayer (which was deemed by s.248 to be a person) was found to be dealing at arm's length with the taxpayer's surviving...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Application Rules - Subsection 26(5) | 98 |

Wright Estate v. The Queen, 96 DTC 1509 (TCC)

A testamentary trust was found to be dealing at arm's length with the three shareholders of a family corporation (the son and daughter of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(a) | a trust is a person which is related to no one | 327 |

Freedman Holdings Inc. v. The Queen, 96 DTC 1447 (TCC)

Pursuant to a separation agreement between Mr. and Mrs. Freedman, Mr. Freedman agreed to pay Mrs. Freedman the sum of $950,000 in full...

Whitehouse v. Ellam, [1995] BTC 284 (Ch. D.)

The written assignment by the Netherlands judgment creditor of an insolvent company of debt for a nominal amount to the taxpayer and the other...

Husky Oil Ltd. v. The Queen, 95 DTC 316, [1995] 1 CTC 2184 (TCC), aff'd 95 DTC 5244 (FCA)

The taxpayer purchased the shares of a holding company whose assets consisted of shares of operating companies whose adjusted cost base...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Shares | 82 | |

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) | 128 |

Bowens v. The Queen, 94 DTC 1863 (TCC), aff'd 96 DTC 6128 (FCA)

When a corporation ("Trilogy") made an offer to acquire all the shares of a corporation ("DEB"), including any outstanding stock options, the...

Del Grande v. The Queen, 93 DTC 133 (TCC)

The taxpayer, who was a 25% shareholder in a private company, was found to be dealing at arm's length with the company given that the other...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | not a shareholder benefit if option exercisable only while officer; obligation v. conferral | 197 |

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(5) | 114 | |

| Tax Topics - Statutory Interpretation - Specific v. General Provisions | 81 |

Martin Feed Mills Ltd. v. MNR, 91 DTC 1069, [1991] 2 CTC 2052 (TCC)

A third party ("Grundy") purchased shares of a corporation indirectly controlled by an individual ("Martin") only to accommodate Martin as his...

Francois Fournier v. Minister of National Revenue, 91 DTC 746, [1991] 1 CTC 2699 (TCC)

The taxpayer, who had a 45% shareholding in a private company, agreed with the other principal shareholder and director and on the advice of the...

International Aviation Terminals (Calgary) Ltd. v. MNR, 89 DTC 671, [1990] 1 CTC 2017 (TCC)

A transaction whereby the three indirect individual shareholders of the Appellant "acted in concert to cause the Appellant to distribute $715,000...

Grant v. MNR, 89 DTC 16 (TCC)

Two couples each owned 50% of the voting shares of a private corporation, either directly or through holding companies. A declaration of a...

Roxon Property Management Ltd. v. MNR, 88 DTC 1306, [1988] 1 CTC 2512 (TCC)

In order for the taxpayer to realize an allowable business investment loss with respect to a debt owing to it by its subsidiary (MIL) the two...

May Estate v. MNR, 88 DTC 1189, [1988] 1 CTC 2303 (TCC)

The acquisition of shares by an estate by virtue of the death of the deceased was not an arm's length transaction because "the trust created by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(2) - Paragraph 251(2)(a) | 14 | |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(6) - Paragraph 251(6)(b) | 11 |

Noranda Mines Ltd. v. MNR, 87 DTC 379, [1987] 2 CTC 2089 (TCC)

45.3% of the common shares of Orchan Mines Limited ("Orchan") were owned by Noranda Mines Limited ("Noranda"), and 5.53% of the common shares of...

Re Tremblay (1980), 36 C.B.R. (N.S.) 111 (Q.S.C.)

It was stated, in the context of the Bankruptcy Act, that a transaction is not at arm's length "where one of the co-contracting parties is, by...

MNR v. Merritt Estate, 69 DTC 5159, [1969] CTC 207 (Ex Ct)

The deceased, in one of his sober moments, agreed with his son's professional adviser that in order to protect his investments from further...

Gatineau Westgate Inc. v. MNR, 66 DTC 560 (TCC)

The two principal shareholders and directors of the taxpayer, who also carried on a real estate business in partnership, sold real estate to the...

Sheldons Engineering Ltd. v. MNR, 53 DTC 11 (TAB), aff'd 54 DTC 1106 (Ex Ct) and at 55 DTC 1110, [1955] S.C.R. 637 (supra).

Before going on to find that a transaction was an arm's length one, Mr. Fisher noted (at p. 22) that "the expression 'to deal at arm's length' is...

Administrative Policy

2024 Ruling 2024-1008661R3 - Internal reorganization: Half-year rule

2022-0941241R3 concerned the successive wind-ups of two “subsidiary” general partnerships as a result of the parent winding-up under s. 88(1)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 1100 - Subsection 1100(2.2) - Paragraph 1100(2.2)(e) | application of the half-year rule exception on s. 98(5) wind-up: parent was not dealing at arm’s length with the partnership at the moment of its dissolution | 125 |

13 April 2023 External T.I. 2017-0684341E5 F - Perte au titre d’un placement d’entreprise

An individual owned an interest-bearing debt of a wholly-owned corporation operating a restaurant which in 20X1 sued the franchisor at the same...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(1) - Paragraph 39(1)(c) | active business for SBC purposes can continue after regular business operations have ceased/ sale of debt for $1 to unrelated purchasers might be a non-arm’s length transaction | 318 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Small Business Corporation | a corporation may continue to qualify as an SBC well after it has in fact ceased to transact its business | 209 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Income-Producing Purpose | business does not cease until the prior commitments incurred in the course of the business are fulfilled | 136 |

7 October 2021 APFF Roundtable Q. 7, 2021-0900971C6 F - Economic dependence

Is financial dependence of one party on another sufficient in itself to create a non-arm’s length relationship?

CRA stated:

1 June 2021 External T.I. 2020-0865201E5 F - Sale of property for POD less than FMV

Messrs. X and Y (unrelated individuals), who each wholly-owned operating corporations ("ACo" and "BCo"), also equally owned XYZCo, which built 12...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | sale of 2 properties by 50-50 corp at a knowing undervalue to the respective shareholders’ own corporations could engage s. 56(2) | 163 |

23 February 2021 External T.I. 2018-0769891E5 F - 125(7) "revenu de société déterminé"

Opco A (wholly-owned by Mr. A) and Opco B (wholly-owned by Mr. B, who deals at arm’s length with Mr. A) each hold 50% of the shares in Opco D. ...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Specified Corporate Income - Paragraph (a) - Subparagraph (a)(i) - Clause (a)(i)(B) - Subclause (a)(i)(B)(I) | services income from multiple private corporations referenced in s. (a)(i)(A) can be bad income for purposes of the substantially all test | 477 |

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(1) - Paragraph 125(1)(a) - Subparagraph 125(1)(a)(i) - Clause 125(1)(a)(i)(B) | services income from multiple investee private corporations can be bad income for purposes of the specified corporate income - s. (a)(i)(B) safe harbour | 385 |

2021 Ruling 2020-0868661R3 F - Section 84.1 – Leveraged Buyout

The shares of Holdco - which holds real estate that it leases to Opco (carrying on a Canadian active business) – are held by three unrelated...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) | s. 84.1 did not apply to a leveraged buyout financed by the target | 203 |

11 October 2019 APFF Roundtable Q. 12, 2019-0812711C6 - Part IV

The common shares of X Corp. and Y Corp are held equally by two unrelated corporations. Whether Y Corp. was connected to X Corp. - so that a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(2) | two 50% shareholders of two corporations likely acting in concert to produce connectedness | 246 |

7 September 2016 External T.I. 2014-0563781E5 - Articles 10 and 11 of Canada-UK Treaty

An issue arising under the Canada-UK Treaty was whether the 99% share of the limited partners of a UK LP in interest paid by a Canadian subsidiary...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 11 | limited partners of an LP can deal at arm’s length with a Canadian subsidiary of the LP | 452 |

| Tax Topics - Treaties - Income Tax Conventions - Article 10 | limited partners generally do not have control over a company’s voting power/an over-10% limited partner is considered to “indirectly” own over 10% of an LP subsidiary | 471 |

19 January 2017 External T.I. 2015-0576751E5 F - Trust, Disposition of depreciable property, Assumption

CRA agreed that the ½ step-up rule in s. 13(7)(e) does not apply to a deemed disposition under s. 104(5) given that the trust is not related to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 13 - Subsection 13(7) - Paragraph 13(7)(e) | s. 13(7)(e) applicable to s. 107(2.1) distribution but not s. 104(5) deemed disposition | 300 |

| Tax Topics - Income Tax Act - Section 107 - Subsection 107(2) | s. 107(2) generally available where beneficiary assumes trust debt | 168 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Personal Trust | non-commital as to whether assumption of debt could constitute tainting consideration | 183 |

| Tax Topics - Income Tax Act - Section 107 - Subsection 107(2.1) | s. 13(7)(e) applicable to depreciable property distribution | 123 |

29 November 2016 CTF Roundtable Q. 6, 2016-0669661C6 - 84.1 and the Poulin/Turgeon Case

Does the Poulin decision affect CRA’s view of employee buyco arrangements? CRA responded that it could be established that the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(1) - Total Charitable Gifts - Paragraph (c) - Subparagraph (c)(ii) | right of GREs to carry forward donations for five years | 109 |

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) | Poulin is consistent with CRA's previous statements on employee buycos | 148 |

7 October 2016 APFF Roundtable Q. 20, 2016-0655831C6 F - Employee Buycos and the Poulin Case

Following the Poulin decision, does CRA intend to modify its position respecting the potential application of s. 84.1 where a departing employee...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) | Poulin accepted | 134 |

2014 Ruling 2014-0539791R3 - Paragraph 212(1)(b)

CDS trust entered into credit default swaps with a counterparty (a non-resident Bank) desiring credit protection for its bond portfolios and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(b) | creditors' approval of CCAA plan of compromise for the debtor trust did not cause them to not deal at arm's length with trust | 386 |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(3) - Participating debt interest | interest paid on limited recourse debt to the extent of available debtor assets was not participating debt interest | 248 |

S1-F5-C1 - Related Persons and Dealing at Arm's Length

In response to the release in draft form of Folio S1-F5-C1 entitled "Related persons and dealing at arm's length," the Joint Committee made...

S1-F5-C1 - Related Persons and Dealing at Arm's Length

General critiera for non-arm's length

1.38 The following criteria have generally been used by the courts in determining whether parties to a...

25 November 2012 Roundtable, 2013-0479401C6 F - Employés et Achat Ltée commentaires panel ARC

In order to facilitate the disposition of shares of departing employees who had purchased their shares under an employee share ownership plan...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) - Paragraph 84.1(1)(b) | generally a deemed dividend on repurchase of departing employees’ shares by employer-funded Buyco | 141 |

25 November 2012 CTF Roundtable, 2013-0479402C6 - Employee Buycos - comments from CRA Panel

Employees of Opco received Opco shares as incentives under an Opco employee share ownership plan ("ESOP"). Under the terms of the ESOP, on...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) | stock option Buyco not at arm's length | 194 |

19 April 2012 External T.I. 2012-0439781E5 - Specified employee for SRED credits

Corporation A and Corporation B have 60% and 40% interests in a partnership which employs Corporation A's sole shareholder (Mr A) to perform...

10 April 2012 External T.I. 2011-0428701E5 F - Lien de dépendance - commanditaire et SEC

Two corporations (X and Y) each wholly own the two general partners (each with a 1% GP interest) of a limited partnership and also own (on a 50-50...

8 October 2010 APFF Roundtable, 2010-0373181C6 F - Non-arm's length relationship

Respecting a transaction between a non-profit organization and a registered charity where both entities share certain board members, CRA stated...

15 September 2010 Internal T.I. 2010-0371521I7 F - French Version of paragraph 23 in IT-419R

The French version of IT-419R2, para. 23, which rendered "not dealing at arm's length" as "sans lien de dépendance" will be promptly corrected.

22 May 2009 Internal T.I. 2009-0312791I7 F - Transfert de biens entre un rentier et son REÉR

Before finding that the purchase of RRRSP property (the “Co-op” shares) by the RRSP’s annuitant at cost was to be treated as the payment of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 146 - Subsection 146(1) - Premium | purchase of RRSP property at cost is viewed as premium to the extent of excess over FMV | 166 |

5 October 2007 APFF Roundtable Q. 10, 2007-0243171C6 F - Surplus Stripping

CRA considered that where an individual (Mr. X) holding all the common shares of Opco exchanged all his common shares for retractable preferred...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) | treatment of Employeeco purchase depends on whether it has a separate economic interest | 360 |

IT-419R2

"Meaning of Arm's Length." At para. 29:

The following criteria have generally been used by the courts in determining whether parties to a...

12 September 2005 External T.I. 2005-0134631E5 F - Superficial Loss - Realization of Latent Loss

Four unrelated individuals each holding 25% of the common shares of a small business corporation, transfer their shares to a corporation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Superficial Loss | loss could be realized by 4 unrelated individuals transferring their equal shareholdings of Opco to Newco | 139 |

2005 Ruling 2005-0133041R3 - Investors not dealing non-arm's length

In the context of an issue as to whether shares of a non-resident corporation were taxable Canadian property, CRA ruled that the winding-up of the...

2 July 2003 External T.I. 2002-0180015 F - Usufruit d'un immeuble

Mr. X disposes of his principal residence and the underlying land to a corporation (whose shareholders are his son and an arm’s length person)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(b) - Subparagraph 69(1)(b)(i) | application of s. 69(1)(b)(i) on transfer of individual’s property to a corporation with him having the usufruct | 126 |

| Tax Topics - Income Tax Act - Section 105 - Subsection 105(1) | no benefit re use of personal-use property | 180 |

12 June 2003 External T.I. 2003-0019725 F - Sale of Holding' Shares to OPCO

Three unrelated individuals (X, Y and Z), in addition to holding some of the shares of Opco directly, also held Opco shares through their...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) | s. 84.1 likely applicable re transaction in which 3 unrelated individuals act in concert to step up shares in Opco | 203 |

26 March 2003 External T.I. 2003-0008645 F - Non-Arm's Length Sale of Shares

Regarding whether a transaction between a holding company owned equally by a married couple and a corporation wholly-owned by the nephew of one of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) | no presumption that a transaction between companies owned by couple and nephew, respectively, is not arm’s length | 113 |

28 March 2003 External T.I. 2002-016665

Two shareholders collectively holding 24% of the shares of Opco transfer their shares of Opco to a newly-incorporated holding company ("Xyco") and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) | 84.1 may apply to partial buyout by Holdco for independent employees | 170 |

13 September 2002 External T.I. 2002-0159525 F - Non-Arm's Length Sale of Shares

Regarding whether a sale of shares of a farming corporation by a resident individual to a Canadian purchaser owned by his nephew would be a...

25 February 2002 External T.I. 2000-0046485 F - Majoration et Immobilisation

Planning to equalize assets of two target corporations (Aco and Bco) in connection with their sale to two purchasers (HoldcoA and HoldcoB) - which...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(c) - Subparagraph 88(1)(c)(v) | reciprocal transactions entailed acting in concert, so that the bump was denied under s. 88(1)(c)(v) | 296 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(c) - Subparagraph 88(1)(c)(vi) - Clause 88(1)(c)(vi)(B) - Subclause 88(1)(c)(vi)(B)(I) | reciprocal transactions entailed acting in concert, so that the bump was denied under s. 88(1)(c)(vi)(B)(I) given resulting specified shareholder status | 323 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(d.2) | reciprocal transactions entailed acting in concert, so that the bump was denied under s. 88(1)(c) and (d.2) by virtue of backdating acquisition of acquisition of control by parent | 321 |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Shares | arguable that preferred shares received on s. 85(1) rollover basis for eligible capital property transfer, and immediately sold, were not capital property | 62 |

10 May 2001 External T.I. 2001-0075685 - EMPLOYEE STOCK OPTION IN A RRSP

An employee implicitly was treated as not dealing at arm's length with his RRSP.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(3) - Paragraph 7(3)(a) | 81 |

22 May 2001 External T.I. 2000-0047245 F - Divorce

Prior to their divorce, Mr. A transferred to Ms. A a portion of his shares of Opco and Ms. A exchanged her shares of Opco for freeze preferred...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) | sale of ex-wife’s shares of Opco (acquired in marriage settlement) to new Holdco of her ex-husband for Holdco note would engage s. 84.1 if these were “reciprocal transactions” | 162 |

29 March 2001 External T.I. 2001-0074145 - Affiliated persons & stop loss rules

Where the shares of a corporation are owned equally by four trusts having the same corporate trustee, s. 40(3.6) will apply to deny a capital loss...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(3.6) | 70 |

15 February 2001 External T.I. 1999-0008405 F - Lien de dépendance

Y sold his wholly-owned corporation (Yco) to a corporation (Xco) owned by an unrelated individual (X), in consideration for $100,000 in cash ...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) | secured promissory note potentially could give rise to de facto control | 107 |

20 January 2000 External T.I. 9918035 F - SOCIETE DE PERSONNES RATTACHEE

Five individuals, who were equal members of a partnership (X P/p) through their respective wholly owned corporations, also were equal direct...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(2.1) | partnership between 5 equal individual partners likely would be connected with such individuals qua shareholders of their respective corporations that formed a second partnership | 184 |

14 April 1999 Internal T.I. 9901637 F - CATEGORIE 41 -LIE A SOI MEME

Before finding that the exclusion in (a.1)(iv) of Class 41, for where the property “acquired by the taxpayer [had] been used for any purpose by...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Schedules - Schedule II - Class 41 - Paragraph (a.1)) - Subparagraph (a.1)(iv) | (a.1)(iv) exclusion for NAL acquisition did not apply where the taxpayer acquired the property that it previously had leased | 148 |

May 1998 Conference for Advanced Life Underwriting Round Table, Q. 1, No. 9807000

A donor and donee may be considered to have different interests and, therefore, to deal at arm's length notwithstanding that each party may have...

Income Tax Technical News, No. 9, 10 February 1997

Where two unrelated shareholders each own 50% of the shares of a corporation, the fact that they used their own RRSPs to acquire shares of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Other Legislation/Constitution - Federal - Indian Act - Section 87 | 30 | |

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Subparagraph 212(1)(b)(vii) | events must be beyond borrower's control | 79 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | loss transfer must be to affiliated person - related not enough | 50 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(c.3) - Subparagraph 88(1)(c.3)(ii) | 159 | |

| Tax Topics - Income Tax Regulations - Regulation 4900 - Subsection 4900(12) | 71 | |

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(1) - Paragraph 53(1)(e) - Subparagraph 53(1)(e)(i) | avoidance of double taxation through absence of ACB adjustment | 137 |

6 January 1997 External T.I. 9640845 - TRUST AND ARM'S LENGTH DEALINGS

In response to a query as to whether two trusts are considered to

be dealing at arm's length notwithstanding that they have the same public...

23 May 1996 External T.I. 9604655 - DEEMED REACQUISITION - WHETHER NON-ARM'S LENGTH

Where there is a deemed dispostion and reacquisition of property under s. 149(10), the corporation in question will not be considered to be...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 13 - Subsection 13(7) - Paragraph 13(7)(e) | person potentially may not deal at arm's length with itself | 74 |

11 October 1996 APFF Roundtable, 7M12910 - APFF ROUND TABLE

Because two shareholders who together owned all the shares of a corporation (50% each) used their respective RRSPs to acquire shares in the...

11 October 1996 APFF Roundtable, 7M12910 - APFF ROUND TABLE

Where $500,000 of shares of Opco are sold by its individual shareholder to a corporate purchaser, following which the purchased shares are...

1995 Ontario Tax Conference Round Table, Q. 5 (No. 952503)

Where $500,000 of shares of Opco are sold by its individual shareholder to a corporate purchaser, following which the purchased shares are...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 124 |

27 October 1994 External T.I. 9424545 - PROFIT SHARING PLAN FOR CORPORATE PARTNER

"Where a partnership owns more than 50% of the issued voting shares of a corporation and where a particular partner is entitled without...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(2) - Paragraph 251(2)(c) - Subparagraph 251(2)(c)(i) | 75 |

12 January 1993 T.I. (Tax Window, No. 28, p. 21, ¶2388)

Where a widow is the sole beneficiary of her husband's estate and all the shares of a corporation previously owned by her husband are held by an...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(5) - Paragraph 251(5)(b) | 67 |

21 August 1992 T.I. (Tax Window, No. 23, p. 1, ¶2141)

Discussion whether a transaction occurring pursuant to a buy-sell agreement entered into between a taxpayer and a company owned by her husband as...

92 C.R. - Q.33

The acquisition of shares of a deceased by his estate is a transaction between persons not dealing at arm's length.

92 CPTJ - Q.14

Under normal circumstances, the general partner in a limited partnership will be considered to control the partnership and, therefore, will not be...

18 December 1991 T.I. (Tax Window, No. 12, p. 23, ¶1572)

The Bank of Canada does not deal at arm's length with any federal department, agency or Crown corporation.

10 July 1991 T.I. 1991-111

Where two limited partnerships have the same general partner and none of the limited partners in either partnership are related to each other, the...

9 May 1991 T.I. 5-7883 [GP control's LP's business]

CRA stated:

[I]n a limited partnership with only one general partner, that general partner will generally have control of the partnership's...

8 March 1991 T.I. (Tax Window, No. 2, p. 23, ¶1190)

Even if the beneficiary of a trust is found not to deal at arm's length with the trust, he will not necessarily be considered not to deal at arm's...

29 December 1989 T.I. (May 1990 Access Letter, ¶1223)

Whether a partnership and a corporation are dealing at arm's length with each other is a question of fact. A series of examples were given. For...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 13 - Subsection 13(7) - Paragraph 13(7)(e) | 62 |

September 1989 Revenue Canada Round Table (December 89 Access Letter, ¶1040.11)

If a person acquires a minority interest in a small private corporation, operating with a deficit, it is likely that this person has expressed...

IT-140R3 "Buy-Sell Agreements"

Where the deceased and the survivor did not deal at arm's length at the time a buy-sell agreement was made, s. 69(1)(b) applies when the estate...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Shares | 0 |

Articles

Matias Milet, Emily Gilmour, "A Discordant Jurisprudence: What does it Mean to be ‘Acting In Concert’?", International Tax (Wolters Kluwer CCH), No. 118, June 2021, pp. 1-7

Swiss Bank (p. 4)

[A]lthough it did not expressly reject the Exchequer Court decision, the SCC [in Swiss Bank] did not refer to the "acting in...

Sandra Mah, Mark Meredith, "Factual Non-Arm's Length Relationships", 2014 Conference Report, (Canadian Tax Foundation), 16:1-24

Kirby-Maurice (16.3)

Kirby-Maurice…formulates in different terms the concept that was expressed by the Supreme Court in Sheldon's Engineering as...

Flannigan, "The Legal Construction of Rights of First Refusal", The Canadian Bar Review, Vol. 76, Nos. 1 & 2, March - June 1997, p. 1.

Owen, "Acting in Concert: Fact or Fiction?", 1992 Canadian Tax Journal, No. 4, p. 829.

Subsection 251(2)

Paragraph 251(2)(a)

See Also

Mathieu v. The Queen, 2014 TCC 207

Through a holding company, the taxpayer held 37.5% of the shares of a corporation which granted him employee stock options ("Forages Garant"). A...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(3) - Paragraph 7(3)(a) | non-arm's length option surrender proceeds were exempted by s. 7(3)(a) | 150 |

| Tax Topics - Statutory Interpretation - Interpretation Act - Subsection 45(2) | may look at subsequent amendment to determine whether it changed the law | 132 |

| Tax Topics - Statutory Interpretation - Specific v. General Provisions | stock option rules more specific than employee benefits | 55 |

May Estate v. MNR, 88 DTC 1189, [1988] 1 CTC 2303 (TCC)

An individual is not related to the relatives of his deceased wife.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | estate did not deal at arm's length with testotor re bequest | 142 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(6) - Paragraph 251(6)(b) | 11 |

Administrative Policy

25 July 2022 External T.I. 2021-0905871E5 - Section 116 Certificate

A non-resident estate holding the Canadian condo of the Canadian deceased and cash, sells the condo for cash and utilizes the principal residence...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 150 - Subsection 150(1.1) - Paragraph 150(1.1)(b) - Subparagraph 150(1.1)(b)(iii) | no obligation of non-resident estate to file a return where its gain on the sale of a condo was exempted under the principal residence exemption and it had no other income | 237 |

| Tax Topics - Income Tax Act - Section 116 - Subsection 116(6.1) | disposition of capital interest arising from estate’s distribution to US beneficiary of cash derived from sale of Canadian real estate was disposition of treaty-protected property | 316 |

12 July 2018 External T.I. 2018-0755471E5 - Half-brothers and related persons

The definition of blood relationship in s. 251(6)(a) includes two persons who are the “brother or sister of the other.” Following inter alia

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(6) - Paragraph 251(6)(a) | half-brothers were connected by blood relationship | 111 |

20 May 2002 External T.I. 2002-0117885 F - Lien de dépendance et application de 120.4

In finding that a trust is related to an individual if its trustee is so related, CCRA stated:

Subsection 104(1) provides in part that, for the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 120.4 - Subsection 120.4(1) - Split Income - Paragraph (c) | split income definition applied on the basis that the business of a partnership is carried on by its partners and that a trust if related based on the relatedness of its trustee | 311 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(1) | s. 104(1) indicates that related party status of trust is tested through its trustee | 97 |

Paragraph 251(2)(b)

Subparagraph 251(2)(b)(i)

See Also

Kruger Wayagamack Inc. v. The Queen, 2015 DTC 1112 [at at 667], 2015 TCC 90, aff'd 2016 FCA 192

Kruger Inc. was the 51% shareholder of the taxpayer and was entitled under the unanimous shareholders agreement between it and the other...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Shares | non-assignable put right ignored | 98 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(1) - Paragraph 256(1)(a) | de jure or de facto control requires strategic control, not merely operational control | 340 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(1.2) - Paragraph 256(1.2)(c) | effect of s. 256(1.2)(g) is as if company were run by 3rd party | 254 |

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(5.1) | de facto control requires strategic control, not merely operational control | 216 |

Ministic Air Ltd. v. The Queen, 2008 TCC 296

The appellant was denied a credit under ETA s. 231(1) in respect of an alleged bad debt, in part, on the basis that 1/3 of the appellant's...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 231 - Subsection 231(1) | debt not written off a recipient not at arm's length | 202 |

Administrative Policy

21 November 2001 Internal T.I. 2001-0094527 F - PERTE REPUTEE NULLE-BRYAN

The discharge pursuant to a bankruptcy proposal of unsecured debt owing by a small business corporation o its shareholder for cents on the dollar...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(2) - Paragraph 40(2)(g) - Subparagraph 40(2)(g)(ii) | Byram now followed re loss on non-interest-bearing shareholder loan to corporation | 57 |

| Tax Topics - Income Tax Act - Section 50 - Subsection 50(1) - Paragraph 50(1)(a) | no partial bad debt recognition under s. 50(1)(a) | 64 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(27) | s. 248(27) does not permit partial debt write-off under s. 50(1)(a) | 75 |

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(1) - Paragraph 39(1)(c) - Subparagraph 39(1)(c)(ii) | settlement of corporate debt under a bankruptcy proposal did not entail disposition of the debt to the corporation | 89 |

| Tax Topics - Income Tax Act - Section 116 - Subsection 116(5) | settlement under bankruptcy proposal of debt did not entail a disposition of that debt to the corporation | 50 |

11 May 2017 Internal T.I. 2016-0665931I7 - Related to participating employer

Respecting where two unrelated individuals each held exactly 50% of the (voting common) shares of their employer corporation, the Directorate...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 8000 - Subsection 8300(1) - Individual Pension PLan | two unrelated 50% shareholders potentially could both be related to the corporation based on Duha USA rights and s. 251(5)(b) rights | 295 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(5) - Paragraph 251(5)(b) | s. 251(5)(b) deemed control does not undercut actual de jure control | 161 |

8 September 2017 External T.I. 2014-0549771E5 - Article XXIX-A:3

CRA found that in the situation where a U.S. parent was the trustee of a U.S. trust whose beneficiary was a U.S. Opco, that U.S. Opco qualified as...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 29A | a trust is related for purposes of Art. XXIX-A (3) of the Canada-U.S. Treaty to a corporation that is controlled by its corporate trustee | 338 |

| Tax Topics - Treaties - Income Tax Conventions - Article 3 | "person related thereto" defined by ITA meaning of "related person" | 39 |

5 November 2014 External T.I. 2014-0529991E5 F - Avantage pour automobile-personne liée

The board members of a Quebec non-share corporation that is exempt under s. 149(1) ("Entity") are appointed by "Municipality." During a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(2) | standby charge computed based on cost to auto owner which is related to employer | 187 |

10 October 2014 APFF Roundtable Q. 16, 2014-0538031C6 - APFF 2014 Q. 16 - Capital gain

In the course of considering the availability of the exception in s. 55(3)(a) for a spin-off, CRA stated (TaxInterpretations translation):...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3) - Paragraph 55(3)(a) | interposition of holdco to permit related-person spin-off compliant with s. 55(3)(a)(ii) and (v) | 933 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.01) - Paragraph 55(3.01)(g) | interposition of holdco to permit related-person spin-off compliant with s. 55(3)(a)(ii) and (v) | 925 |

S1-F5-C1 - Related Persons and Dealing at Arm's Length

1.46 Where a trust owns a majority of the voting shares of a corporation…the trust and the corporation will be related persons by virtue of...

Example 7

Mr. A is the sole trustee of a particular trust that owns all of the issued shares in the capital of a corporation.

Both the particular trust and...

1 May 2014 External T.I. 2013-0494981E5 F - De Jure Control

The sole beneficiary of a Quebec trust with two trustees who are unrelated to him has the power to dismiss them (Scenario 1), to dismiss and...

2012 Ruling 2011-0402571R3 - De Jure Control - Debt Settlement

Parent owns the Class B common shares of Lossco and Mr. A, who deals at arm's length with Parent (and with Profitco, a subsidiary of Parent) holds...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(7) - Paragraph 256(7)(b) | 259 |

6 October 2000 External T.I. 2000-0038055 F - Contrôle par une société de personnes

Respecting the question whether two corporations are related persons if they are controlled by a limited partnership or a general partnership, the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(2) - Paragraph 251(2)(c) - Subparagraph 251(2)(c)(i) | general partner usually controls | 217 |

29 August 2000 Internal T.I. 2000-0023187 F - Société privée sous contrôle canadien

A corporation (Opco), the voting rights of which were owned as to 1/3 by an individual and as to 2/3 by a limited partnership of which the general...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 125 - Subsection 125(7) - Canadian-Controlled Private Corporation | ultimate control of Opco was held by Pubco through an indirect wholly-owned subsidiary that was the general partner of an LP holding 2/3 of Opco’s voting shares | 112 |

9 August 1994 T.I. 933312 [control by partner with voting rights]

In a situation where a husband and wife each own a holding company (H Holdco and W Holdco), H Holdco has a controlling interest in a partnership...

23 March 1992 T.I. (Tax Window, No. 18, p. 20, ¶1825) [control by trustee]

The sole individual trustee of the family trust controls the corporation whose shares are held by the trust, with the result that that corporation...

90 C.R. - Q28

A partnership is considered to be a person when the computation of income at the partnership level is involved. For example, a partnership that...

87 C.R. - Q.18

Where a subsequent employer purchases all the assets or shares of the former employer, the former employer will qualify as a "person related to...

Subparagraph 251(2)(b)(ii)

Cases

Miron and Frères Ltd. v. Minister of National Revenue, 55 DTC 1109, [1955] CTC 182, [1955] S.C.R. 679

997 out of the outstanding common shares of a corporation were owned as to 400 shares by an individual and his brother (200 shares each) and, as...

See Also

Castro v. The King, 2024 TCC 3

As a condition to receiving a loan to fund the renovation of a property of the Castros, they were required to transfer the property to a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 231 - Subsection 231(1) | unreported GST on sale to corporation controlled de jure by vendors (but with pledge) could not be claimed as credit when unrecoverable from corporation | 329 |

Côté-Létourneau v. The Queen, 2010 DTC 1116 [at at 3092], 2007 TCC 91

A sale by the taxpayers (a husband and wife) of their shares of a controlled corporation to another corporation ("9061") all of whose shares were...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(5) - Paragraph 251(5)(c) | 86 | |

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2) - Paragraph 84.1(2)(a.1) | 44 |

Subparagraph 251(2)(b)(iii)

Administrative Policy

3 June 2025 External T.I. 2025-1064821E5 F - Related persons

CRA explained how a corporation (Opco), owned equally by Father and Uncle, was related to a corporation (Newco), owned equally by five holding...

22 August 2014 External T.I. 2014-0540751E5 F - Acquisition of control

Two brothers (A and B) own 100% of the shares of Holdco A and Holdco B, respectively, which, each in turn, owns 50% of the shares of Opco. A sells...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(7) - Paragraph 256(7)(a) | addition of cousin to control group would taint it/cousins part of related control group while fathers alive | 529 |

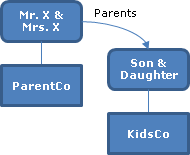

30 January 2013 External T.I. 2012-0470931E5 - Related corporations

{kind=link}

Suppose parents Mr. and Mrs. X hold ParentCo, and their children ("Son and Daughter") hold KidsCo. Then:

Mr. X and Mrs. X are related to...

Paragraph 251(2)(c)

Cases

Electric Power Equipment Ltd. v. MNR, 67 DTC 5322, [1967] CTC 479 (Ex Ct)

Before finding that two corporations were associated pursuant to a predecessor of s. 256(1)(d), Sheppard DJ stated:

Being related to oneself can...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Interpretation Act - Subsection 33(2) | 63 |

Subparagraph 251(2)(c)(i)

Cases

Colmvest Holdings Corporation v. The Queen, 2022 TCC 70

Colmvest, which was the 25% shareholder of a corporation (“443307”), incurred legal fees in an arbitration between it and the 75% shareholder...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Excise Tax Act - Section 186 - Subsection 186(1) | a minority shareholder could not use the ETA s. 186(1) rule to access ITCs | 234 |

Chutka v. Canada, 2001 DTC 5093 (FCA)

A sale of equipment by a corporation to a partnership whose general partner was wholly-owned by the same individual who owned the vendor...

| Locations of other summaries | Wordcount | |

|---|---|---|