Subsection 84(1) - Deemed dividend

See Also

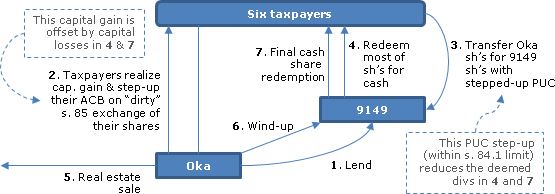

R. v. Golini, 2016 TCC 174

The sole individual shareholder (“Paul Sr.”) of an Ontario corporation (“Holdco”) received a loan from an accommodation party...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | a loan to a shareholder with recourse limited to an asset pledged by the corporation was a shareholder benefit | 589 |

| Tax Topics - General Concepts - Sham | sham doctrine did not apply to a "minor pretence" | 338 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | interest deduction on limited recourse loan | 305 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | use of corporate asset to create PUC was abuse of s. 84(1) | 250 |

Aylward v. R., 97 DTC 1097, [1997] 2 CTC 2748 (TCC)

The issuance to the taxpayer of shares having a paid-up capital of $350,000 did not give rise to a deemed dividend because they were in respect of...

Administrative Policy

2018 Ruling 2018-0780201R3 - Post-mortem pipeline

CRA provided rulings for a pipeline transaction in which the estate with a resident beneficiary sells a company (Opco) with apparently a real...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | hybrid post-mortem 164(6)/pipeline transactions with 10% per quarter redemptions following 12 months | 396 |

2015 Ruling 2015-0584151R3 - Conversion of Contributed Surplus to PUC

Background.

The central management and control of ACo, which was originally incorporated under the Country A Corporate Act, shifted to Canada. In...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Paid-Up Capital | corporate PUC and capital surplus flowed through on a cross-border continuance | 108 |

2014 Ruling 2014-0533601R3 - Spin-off butterfly - subsection 55(2)

A spin-off butterfly reorganization by DC includes a preliminary step for distributing a small portion of DC's retained business from its...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(1) | matching of PUC of cross-shareholdings to match Part IV tax | 152 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | spin-off by CCPC under Plan of Arrangement of two businesses/matching of PUC of cross-shareholdings to match Part IV tax/leased property as business property | 978 |

| Tax Topics - Income Tax Act - Section 86 - Subsection 86(1) | new common shares distinct on basis of right to interim financials | 97 |

S4-F3-C1 - Price Adjustment Clauses

Where the consideration received on the transfer of property to which a price adjustment clause that meets the conditions listed in ¶1.5 is in...

17 February 2003 External T.I. 2002-0176455 - Amount Added to Paid-up Capital of Shares

Aco holds 30 common shares of Opco (30% of the common shares) having an ACB and PUC of $30 and an FMV of $300 (the net fair market value of all...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85.1 - Subsection 85.1(2.1) | 105 |

23 March 2001 Internal T.I. 2000-0056097 F - Roulement interne

On an internal crystallization transaction, the corporation purchases the individual’s common shares, having a nominal stated capital, in...

12 August 1994 External T.I. 9325945 - PAID-UP CAPITAL

Where an individual transfers his 5% shareholding in Opco, having a paid-up capital and ACB of $100,000 and a fair market value of $1 million, to...

23 September 1992 T.I. (Tax Window, No. 24, p. 1, ¶2190)

Where preferred shares having a low paid-up capital are transferred by the shareholder to the corporation in exchange for common shares having a...

92 C.R. - Q.27

Where convertible preference shares having a high stated capital and a low paid-up capital are converted into common shares having both a stated...

1992 June Hong Kong Seminar, Q. B.8 (May 1993 Access Letter, p. 226)

S.84(9) applies for purposes of s. 94(1).

1992 A.P.F.F. Annual Conference, Q. 1 (January - February 1993 Access Letter, p. 49)

Where an individual exchanges all the outstanding common shares of Opco, having a paid-up capital of $500,000 and a fair market value of $600,000,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(2.1) | 75 |

28 August 1991 Memorandum (Tax Window, No. 8, p. 6, ¶1435)

Where preferred shares having a stated capital of $2 million and a paid-up capital of $1 are converted into common shares having a stated capital...

81 C.R. - Q.6

Where consequences of receiving a s. 84(1) dividend as a result of the paid-up capital of shares issued on a s. 85(1) roll exceeding the fair...

Articles

Brussa, "Capital Reorganizations", 1991 Conference Report, c. 16.

Paragraph 84(1)(b)

Administrative Policy

2021 Ruling 2021-0911211R3 - Foreign Takeover

A Canadian corporation contributed its shares of a subsidiary (Merger Sub1) to a Canadian subsidiary as a contribution of capital. It had...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 54 - Adjusted Cost Base | shares issued to a Canadian parent in consideration for it issuing shares on a Delaware merger had a cost equal to such shares’ FMV/ shares transferred on absorptive merger at FMV | 903 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition - Paragraph (k) - Subparagraph (k)(ii) | deposit of shares to voting trust arrangement was not a disposition | 40 |

| Tax Topics - General Concepts - Payment & Receipt | borrowing and payment of funds pursuant to an internal payment direction agreement | 49 |

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(1) - Paragraph 53(1)(c) | full cost to sub of shares contributed to it | 289 |

7 October 2016 APFF Roundtable Q. 21, 2016-0655901C6 F - Section 7 and bonus paid in share

After noting that it considers that where a Canadian-controlled private corporation has agreed in writing “to award a bonus based on the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(3) - Paragraph 7(3)(a) | s. 7 can govern bonuses paid in shares where discretion ceases prior to the issuance | 266 |

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(1.1) | 7(1.1) applicable to non-discretionary bonus payable in shares | 178 |

Paragraph 84(1)(c)

Articles

Doron Barkai, Alexander Demner, "Dealing with New Subsection 55(2): Issues and Strategies", 2016 Conference Report (Canadian Tax Foundation), 6:1–56

PUC-streaming under s. 84(1)(c) (pp. 6:45-46)

…CRA has not made any specific comments regarding the potential application of new section 55 to...

Paragraph 84(1)(c.3)

Administrative Policy

30 October 2002 External T.I. 2002-0146655 - Meaning of Contributed Surplus

Xco, a taxable Canadian corporation and private corporation, reduced its stated capital account and its paid-up capital in respect of a class of...

Subsection 84(2) - Distribution on winding-up, etc.

Cases

Foix v. Canada, 2023 FCA 38

The shareholders of a private Canadian company (“W4N”) exploiting a valuable item of software had agreed in principle to sell W4N to a U.S....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Certainty | there are acceptable uncertainties in the application of an anti-avoidance provision to taxpayers who test its limits | 136 |

Canada v. MacDonald, 2013 DTC 5091 [at at 5982], 2013 FCA 110, rev'g 2012 TCC 123

{kind=link}

In order to make use of available capital losses before emigrating to the United States, the taxpayer sold the shares of his former professional...

Canada v. Vaillancourt-Tremblay, 2010 DTC 5079 [at at 6833], 2010 FCA 119

In order to convert their shares of a private company ("MHT") that held preferred shares of a Canadian public corporation ("Videotron") into...

Gilmour v. The Queen, 81 DTC 5322, [1981] CTC 401 (FCTD)

The taxpayer was the sole individual shareholder of a personal corporation ("LVG") which, in turn, owned approximately 1/3 of the common shares of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | 99 |

Perrault v. The Queen, 78 DTC 6272, [1978] CTC 395 (FCA)

A substantial dividend was not paid on the "winding-up, discontinuance or reorganization" of a company's business because, following the payment...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | dividend satisfied share purchase consideration | 114 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | a single payment can result in income inclusions to 2 taxpayers - the 2nd as a taxable benefit | 91 |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | 48 |

David v. The Queen, 75 DTC 5136, [1975] CTC 197 (FCTD)

Approximately four months after the corporation of which the taxpayers (the "David group") were shareholders sold its principal business assets,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Evidence | 30 | |

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) | 56 |

Smythe et al. v. Minister of National Revenue, 69 DTC 5361, [1969] CTC 558, [1970] S.C.R. 64

The taxpayers were shareholders of a company (the "old company") who effectively converted its assets to cash through a series of transactions:...

Merritt v. MNR (1941), 2 DTC 513 (Ex Ct), rev'd [1942] S.C.R. 269, 2 DTC 561

The Premier Trust Company ("Premier") acquired all the shares of the taxpayer and other shareholders of the Security Loan and Savings Company...

See Also

Succession Georges Robillard v. The Queen, 2022 TCC 13

The taxpayer, an estate which received shares of a portfolio company (“Holdco”) whose adjusted cost base had been stepped-up under s. 70(5),...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(6) | s. 104(6) permitted the deduction of an amount initially treated as a capital distribution | 182 |

Foix v. The Queen, 2021 TCC 52, aff'd 2023 FCA 38

The shareholders of a private Canadian company (“W4N”) exploiting a valuable item of software had agreed in principle to sell W4N to a U.S....

Kvas v. The Queen, 2016 TCC 199

The general contracting company (“CIA”) of two brothers was dissolved in January of 2008 (the “Dissolution Date”) for failure to file...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | involuntary dissolution did not render the corporation a transferor | 195 |

Latham v. The Queen, 2015 DTC 1104 [at 617], 2015 TCC 75

The taxpayers ("John and Diane Latham") owned a corporation ("Farmers"), which rented out buildings to third parties, and to a related company. In...

| Other locations for this summary | |

|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | distribution to shareholder reimbursed him for loss as guarantor |

Descarries v. The Queen, 2014 DTC 1143 [at at 3412], 2014 TCC 75 (Informal Procedure)

{kind=link}

The six taxpayers, who were siblings (or a step-daughter of their deceased father), held all the shares, having an aggregate fair market value...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 171 - Subsection 171(1) | free to raise an interpretation not advanced by either party | 83 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | use of outside basis to step up PUC abused s. 84.1 | 544 |

MacDonald v. The Queen, 2012 TCC 123, rev'd 2013 DTC 5091 [at 5982], 2013 FCA 110

In order to make use of available capital losses before emigrating to the United Statees, the taxpayer sold the shares of his former professional...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(1) - Tax Benefit | 306 | |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | no abuse in surplus stripping if integration | 368 |

McMullen v. The Queen, 2007 DTC 286, 2007 TCC 16

The taxpayer and an unrelated individual ("DeBruyn") accomplished a split-up of the business of a corporation ("DEL") of which they were equal...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | 270 | |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 198 | |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | mutual benefit and same advisors insufficient to establish non-arm's length in structured sale transaction | 257 |

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) | arm's length: negotiation based on self-interest | 257 |

Geransky v. The Queen, 2001 DTC 243 (TCC)

The taxpayer who owned a portion of the shares of a holding company ("GH") which, in turn, owned an operating company ("GBC") which was engaged in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 295 |

James v. The Queen, 2000 DTC 2056 (TCC)

After the taxpayer's company was struck from the B.C. Register of Companies and dissolved for failure to file annual returns, the Minister...

RMM Canadian Enterprises Inc. v. R., 97 DTC 302, [1998] 1 C.T.C. 2300 (TCC)

A non-resident corporation ("EC") approached a business associate who, along with two other individuals, formed a Canadian corporation ("RMM") to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 159 - Subsection 159(3) | 167 | |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | 188 | |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 235 | |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | purchaser of cash-rich company without any signifcant separate role did not deal at arm's length | 177 |

| Tax Topics - Treaties - Income Tax Conventions | 96 | |

| Tax Topics - Treaties - Income Tax Conventions - Article 10 | 116 |

McNichol v. R., 97 DTC 111, [1997] 2 CTC 2088 (TCC)

The taxpayers sold their shares of a corporation ("Bec"), whose assets (following a sale of real estate) consisted largely of cash, to a corporate...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 234 | |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | 3rd-party purchaser, of cash-rich company, that looked to its own interests dealt at arm's length | 117 |

Kennedy v. MNR, 72 DTC 6357, [1972] CTC 429 (FCTD), aff'd 73 DTC 5359 (FCA)

A corporation of which the taxpayer was the sole shareholder purchased a property for use as the new site for its car dealership business, paid...

Administrative Policy

2024 Ruling 2024-1031041R3 F - Hybrid Post-mortem Pipeline

Background

Prior to the death of Mr. X, who wholly-owned Holdco, Holdco had carried on an investments management business concerning bonds,...

13 May 2026 IFA Roundtable Q. 1, 2026-1087881C6 - Subsection 84(2) and Withholding Tax on Payments to Non-Residents

A shareholder dissents to an amalgamation and receives a payment from the amalgamated corporation for the fair value of its shares. Would s. 84(3)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(3) | s. 84(3) does not apply to a payment made by Amalco to a shareholder dissenting to the amalgamation | 51 |

2025 Ruling 2025-1054291R3 - Post-Mortem Hybrid Pipeline

Background

On the death of Mr. X, he held full basis preferred shares and low-basis common shares of Aco. He also held high-basis preferred...

2024 Ruling 2024-1029151R3 F - Hybrid Post-mortem pipeline

Background

A resident individual (A), died holding redeemable voting shares of Opco (which were deemed to have been redeemed immediately before...

2025 Ruling 2025-1052291R3 F - Post-mortem Hybrid Pipeline

Background

The estate of Mr. A owned all the shares of the Corporation, which carried on an investment management business and whose assets...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Paid-Up Capital | transactions contemplated the distribution of all the PUC of common shares | 71 |

2024 Ruling 2024-1027631R3 F - Post-mortem planning - Pipeline

Background

The estate of A holds a portion of the issued and outstanding shares of Opco, which carried on an investments business. Those shares...

2024 Ruling 2023-0998721R3 - Double post-mortem pipeline

Background

Taxpayer A died holding preferred shares of Opco. Opco carried on a business of deriving interest income from a portfolio of loans...

3 December 2024 CTF Roundtable Q. 14, 2024-1037761C6 - Availability of the Small Business Deduction

CRA provided detailed comments on Foix (finding that s. 84(2) applied to a particular hybrid sale transaction) in 10 October 2024 APFF Roundtable,...

2023 Ruling 2023-0980101R3 - Post-mortem pipeline

Background

At the time of the death of the spouse beneficiary of a testamentary spousal trust, the trust held preferred and common shares of Opco,...

2023 Ruling 2023-0986521R3 F - 104(4) and Pipeline

Background

Trust 1 is a discretionary inter vivos family trust, settled almost 21 years ago, whose principal (resident) beneficiaries are Child 1...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(4) - Paragraph 104(4)(b) - Subparagraph 104(4)(b)(ii) | inter vivos chooses to realize gain on its preferred shares on its 21st anniversary, and transfer those shares for notes in a pipeline trnasaction | 139 |

10 October 2024 APFF Roundtable Q. 18, 2024-1027351C6 F - Arrêt Foix et ventes hybrides

When asked to comment on Foix, which found that s. 84(2) applied to a particular hybrid sale transaction, CRA stated (footnotes...

2024 Ruling 2023-0993651R3 - Post-mortem pipeline

Background

The Deceased held Opco preferred shares, and preferred shares (with no accrued capital gain) and common shares of Holdco, which held...

29 February 2024 Internal T.I. 2023-0987941I7 - Amendments to GAAR and Advance Income Tax Rulings

Regarding the status of post-mortem pipeline transactions following the amended GAAR rule, the Directorate stated:

The Directorate does not...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | CRA will continue to issue post-mortem pipeline rulings following the GAAR amendments, but will not rule on surplus stripping by individuals | 216 |

2023 Ruling 2022-0955451R3 F - Post mortem pipeline

Background

At the time of X’s death, he held the Class A and B shares of Investco, which had a portfolio investment business (holding, e.g.,...

2022 Ruling 2022-0937661R3 F - 104(4) and pipeline transaction

Background

A family inter vivos trust for resident beneficiaries (Trust 1) had distributed its common shares of a CCPC that was an investment...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(5.8) | GAAR applicable to trust holding a corporate beneficiary that was distributed property from an inter vivos trust approaching its 21st anniversary | 116 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(2) | GAAR treated as self-applying | 71 |

2022 Ruling 2022-0933261R3 F - Subsection 104(4) and pipeline transaction

Background

Trust 1, a discretionary inter vivos family trust for A, his Spouse, her child and their children and entitles formed and controlled by...

2021 Ruling 2021-0887301R3 F - Post-mortem pipeline transaction

Background

The Trust was a spousal trust for Mother holding shares of Aco (an investments holding company). Such shares had been bequested to the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2) - Paragraph 84.1(2)(a.1) - Subparagraph 84.1(2)(a.1)(ii) | application of ss. 84.1(1) and (2)(a.1)(ii) to transfer of shares by spousal trust that had received such shares from the testator who had stepped such shares up under s. 110.6(2.1) | 194 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(d.3) | application of s. 88(1)(d.3) to pipeline involving shares that had been stepped up under s. 104(4) | 141 |

2021 Ruling 2021-0877011R3 - Post-mortem Hybrid Pipeline

Background

The will of Mr. X bequeathed his preferred shares (carrying voting control) of Holdco (which had a portfolio which it managed and...

2021 Ruling 2021-0907591R3 F - Post-mortem Pipeline

Background

The deceased (X) held all the shares of Holdco (being Class A voting and participating shares, and Class B voting redeemable preferred...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2) - Paragraph 84.1(2)(a.1) - Subparagraph 84.1(2)(a.1)(ii) | promissory notes issued on pipeline limited by previous s. 110.6(2.1) deduction | 205 |

2022 Ruling 2022-0925601R3 F - Post-mortem Pipeline

Background

On the death of X, X held all the shares of Holdco, which had investments in public company shares and bonds, and mutual fund and...

2021 Ruling 2021-0895631R3 - Post-mortem planning - Hybrid Pipeline

Background

At the time of the death of A, he held the shares (being Class A voting participating shares) of the Corporation (a portfolio...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(3.61) | no stop-loss for s. 164(6) loss realized by estate before pipeline transactions | 156 |

2021 Ruling 2021-0906111R3 - XXXXXXXXXX Post-mortem Pipeline

Background

Before his death, Father transferred his shares (i.e., 50.5% of the common shares) of ACo (which held a diverse portfolio of bonds,...

2021 Ruling 2020-0865901R3 F - Post-mortem Hybrid Pipeline

Background

At the time of the death of X, he held shares of Newco (whose only undertaking was to hold shares of Investments) and a portion of the...

2020 Ruling 2020-0848081R3 F - Subsection 104(4) and pipeline transaction

Two discretionary inter vivos trusts, with an individual (“Father”) and his child (“Child”) as the beneficiaries (both resident in Canada)...

2021 Ruling 2019-0800431R3 - Alter Ego Post-mortem Pipeline and Bump Planning

Background

After he was placed in a long-term care facility, an individual (the “Deceased”) who had owned and been managing the investing...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212.1 - Subsection 212.1(6) - Paragraph 212.1(6)(b) | pipeline ruling for an alter ego trust includes a preliminary deletion of a non-resident beneficiary | 233 |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(d.3) | s. 88(1)(d.3) applied to securities held by investing corportions whose shares were stepped up in hands of alter ego trust and then transferred to and amalgamated under pipeline | 202 |

2021 Ruling 2020-0874931R3 F - Post-mortem Pipeline

Background

At the time of his death, X held all of the shares of Investco (a portfolio holding company) other than non-voting common shares held...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251.2 - Subsection 251.2(2) - Paragraph 251.2(2)(a) | replacement of an executor resulted in an acquisition of control of subsidiaries | 34 |

7 October 2021 APFF Financial Strategies and Instruments Roundtable Q. 8, 2021-0899701C6 F - Post-mortem planning - Pipeline

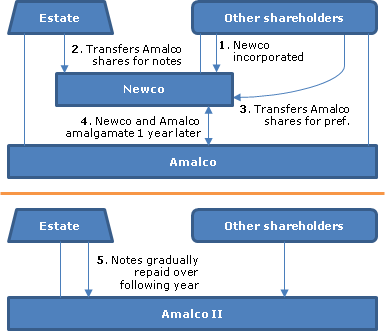

In order to implement pipeline planning, the estate of an individual ("Estate") generally incorporates a new corporation ("Newco") to which it...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) | pipeline transaction can be structured to access hard ACB | 361 |

2021 Ruling 2020-0874851R3 - Post-mortem Hybrid Pipeline

Background

Immediately before her death, A held the common shares (being the only class of shares) of the Corporation, which held marketable...

2020 Ruling 2020-0860231R3 - Post-mortem planning

Background

On the death of the deceased, there was a deemed disposition at FMV of all the Class A common shares of Opco, which is a CCPC with a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(d.3) | bump applied to amalgamation occurring in a pipeline transaction | 161 |

2020 Ruling 2019-0819191R3 F - Post-mortem planning - Pipeline

Background

The Corporation is a portfolio corporation, with ERDTOH and GRIP balances and no CDA, whose Class E and Class K non-voting...

2019 Ruling 2019-0835131R3 F - Post-mortem Pipeline

Background

The will of A provided for his shares of Holdco (which were not qualified small business corporation shares and for which no s....

8 July 2020 CALU Roundtable Q. 6, 2020-0842241C6 - Post-mortem pipeline: Gradual repayment of note

After noting that in 2018-0767431R3, the amount of the pipeline note paid in any single quarter in the first post-amalgamation year was not to...

2020 Ruling 2020-0838951R3 F - Post-mortem Pipeline

Background

On the death of X, he and his two resident brothers (Leg1 and Leg2 – who were the legatees under his will of his shares of Holdco)...

2020 Ruling 2019-0832601R3 F - Post-mortem Pipeline

Background

Holdco is a portfolio company that holds cash, public company shares, shares of Opco (which are not liquid) and an interest in a...

2020 Ruling 2019-0824211R3 F - Post-mortem Hybrid Pipeline

Background

On A’s death, A (a Canadian resident) held all the outstanding shares of Opco, being Class A common shares and Class E preferred...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 51 - Subsection 51(1) | s. 51 applicable to exchange of common shares of Opco for common and preferred shares of Opco | 39 |

2019 Ruling 2019-0809581R3 - Leveraged Buyout of Public Company

Background

Pubco, a public corporation with one class of shares (the “Pubco Shares”) and which (directly and through subsidiaries) had been...

2019 Ruling 2018-0789911R3 F - Post-mortem Pipeline

Background

On the death of A, he was deemed to have disposed of his shares of Realco (but with no capital gain resulting), and of his Class A and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) - Subparagraph 20(1)(c)(i) | deductibility of interest on loan used to redeem shares that had distributed accumulated profits | 81 |

2019 Ruling 2019-0822951R3 F - Post-mortem Hybrid Pipeline

Background

On the death of Mr. X, he was deemed to have realized a capital gain on his Class A (common) shares of ACo (a CCPC portfolio company...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(3.61) | s. 164(6) carryback of capital loss coupled with dividend to generate dividend refund | 83 |

2019 Ruling 2019-0793281R3 F - Post-mortem Hybrid Pipeline

Background

On the death of Mr. X, he was deemed to have disposed at a capital gain of his shares of two holding companies (Corporation A and B)...

2018 Ruling 2018-0780201R3 - Post-mortem pipeline

Background

The Deceased held voting redeemable retractable Class A Special Shares of Opco (which the Deceased thereby controlled) and a Family...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(1) | use of CDA and s. 84(1) deemed dividend to generate s. 164(6) loss | 110 |

2018 Ruling 2018-0767431R3 - Post-mortem pipeline

Background

On A’s death, he owned appreciated common and redeemable retractable preference shares and a non-interest-bearing demand promissory...

2018 Ruling 2018-0765411R3 F - Subsection 104(4) and Pipeline Transaction

Background

Trust1, which is a resident inter vivo trust (whose beneficiaries are family members consisting of Indvidual1, who apparently is...

2018 Ruling 2018-0777441R3 F - Post-mortem planning - Pipeline

Background

On the death of X, Class G non-voting preferred shares of Holdco passed on a rollover basis to X’s surviving spouse and on a...

2018 Ruling 2017-0731971R3 - Reorganization and distribution on PUC reduction

Background

The Taxpayer, a listed public corporation, has CCEE, CCDE and no-capital loss pools, has two resource properties used in its first...

2017 Ruling 2016-0646891R3 - Pipeline and subsequent Split-up butterfly

Background

As a result of the death of A, the estate of A acquired A’s Class A common shares of Predecessor1, exchanged such shares for Class B...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Distribution | combined pipeline and split-up butterfly | 144 |

| Tax Topics - Income Tax Act - Section 186 - Subsection 186(1) - Paragraph 186(1)(b) | circularity avoided through 2nd dividend arising on winding-up of DC | 145 |

29 May 2018 STEP Roundtable Q. 10, 2018-0748381C6 - Pipeline Ruling Requests

In the course of confirming that its position on pipeline transactions has not changed as a result of s. 246.1 being proposed, nor of it being...

2017 Ruling 2016-0629511R3 - Post-Mortem Planning and Extraction of "Hard ACB"

Background

A (a Canadian resident like the other persons mentioned), who is the residuary beneficiary of the estate of C (“Trust C”) and also...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(2) - Paragraph 84.1(2)(a.1) | pipeline transfer of inherited shares for their "hard" ACB (excluding CGD and V-Day step-up by deceased) | 117 |

2017 Ruling 2016-0670871R3 - Post-mortem pipeline

Background

On A’s death, he owned appreciated common and preference shares of PCo, which operated a business of dealing and investing in...

4 November 2016 Memorandum 2016-063191

After describing the transactions in what was to become the Foix case, the Directorate stated inter alia (TaxInterpretations translation):

For...

7 October 2016 APFF Roundtable Q. 12, 2016-0655911C6 F - Partial Leveraged Buy-Out and Monetization of ACB

A holds 50 common shares of Opco with a nominal adjusted cost base and paid-up capital and fair market value of $500,000, and B holds the other 50...

27 April 2016 External T.I. 2016-0625001E5 F - Surplus Stripping

An individual (Mr. X), and a corporation (Holdco) wholly owned by him are the beneficiaries of a Quebec discretionary trust (Trust) holding all...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | funnelling deemed dividend to holdco trust beneficiary and resulting PUC to individual beneficiary/shareholder was surplus stripping | 130 |

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(24) | distribution of s. 84(1) dividend effected with note issuance | 231 |

22 January 2016 External T.I. 2015-0617601E5 F - Pipeline followed by butterfly

An estate acquires the shares of Corporation 1 on a stepped-up basis under s. 70(5) and, in August 20X0, transfers the shares to Corporation 2...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(3.1) - Paragraph 55(3.1)(b) | where pipeline transaction followed by split-up butterfly, the opco also is a distributing corporation | 453 |

2015 Ruling 2015-0569891R3 - Ss. 164(6) carry-back and post-mortem pipeline

Background. All of the shares of Mr. A in A Co (which carried on a "business activity" of trading a portfolio) at the time of his death were...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 164 - Subsection 164(6) | redemption of Canco shares bequeathed to U.S. resident (coupled with s. 164(6) carryback) before pipeline strip of Canco | 143 |

2015 Ruling 2014-0548621R3 - Post Mortem Pipeline Planning

{kind=link}

Background

On the death of B (the surviving spouse of A), B was deemed under s. 70(5)(a) to have disposed of the Class C common shares of the...

2014 Ruling 2014-0540861R3 F - Post-Mortem Planning

{kind=link}

Background

At death, X was the sole shareholder of Investments (a CCPC, whose shares did not qualify as QSBCs), which held bank balances, shares...

2015 Ruling 2014-0563081R3 - Post-mortem pipeline

{kind=link}

Current structure

All the shares of A Co (being Class A voting common shares and Class B non-voting common shares) are held by a spousal trust...

2015 Ruling 2014-0559481R3 F - Post Mortem Planning

{kind=link}

Current structure

Since the death of A (who used Investmentco in his professional practice but had Investmentco accumulate investments,...

2015 Ruling 2014-0541261R3 F - Post-Mortem Planning

{kind=link}

Current Holdco structure

Holdco is a portfolio investment company holding bank deposits, certificates of deposit, notes payable and preferred...

2014 Ruling 2014-0537161R3 - Reduction of stated capital

underline;">: Current structure. The Company is a listed public corporation carrying on the "Business" (comprising resource projects) directly and...

10 October 2014 APFF Roundtable Q. 21, 2014-0538091C6 F - 2014 APFF Roundtable, Q. 21 - Impact of the Descarries Case

What is the CRA position on Descarries? After noting that the case was not appealed because in the result it was favourable and it was only an...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | Descarries failed to recognize scheme against indirect surplus stripping | 750 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | will not impose double taxation under s. 84(2) and (3) | 42 |

2014 Ruling 2011-0415811R3 - Internal reorganization

underline;">: Current structure. Parent, a public corporation which previously had been spun-off by Subco 2 (also a public corporation, but with...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 85 - Subsection 85(1) - Paragraph 85(1)(e.2) | s. 85(1)(e.2) non-application to transfers at ACB to sisters in order to limit ACB shift | 676 |

2014 Ruling 2014-0526361R3 F - Post Mortem Pipeline

{kind=link}

Background

Prior to the death of B (who had been predeceased by her spouse), the Class A common shares of Investmentco, which was a portfolio...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) | step up of PUC of freeze pref shares for purposes of pipeline transaction | 109 |

2014 Ruling 2013-0503611R3 - Post-Mortem Planning

{kind=link}

Overview

A testamentary spousal trust (the "Spousal Trust") whose basis in pref shares of a portfolio investment company ("Holdco") was stepped...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(c) - Subparagraph 88(1)(c)(vi) | bump of marketable securities (no ruling) occurring as part of post-mortem pipeline transactions | 256 |

2013 Ruling 2012-0470281R3 - Reduction of paid-up capital

{kind=link}

Background

Pubco (which is a listed Canadian public corporation engaged in the commercialization of innovative products, and is reorganizing to...

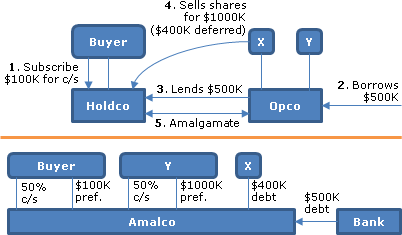

2 April 2013 External T.I. 2013-0479651E5 F - Leveraged buy-out

{kind=link}

X and Y each hold half of the common shares of Opco. X deals at arm's length with Y and Buyer. Buyer incorporates Holdco and subscribes $100,000...

18 June 2013 External T.I. 2012-0433261E5 F - 55(5)(f) and Surplus Stripping

{kind=link}

Two Canadian-resident brothers (Messrs. A and B), who each hold a 50% block of the common shares of a small business corporation (Dividend Payor)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | deliberate engaging of s. 55(2) to convert annual taxable dividends into annual capital gains permitting annual capital dividends would engage s. 245(2) | 149 |

2012 Ruling 2012-0464501R3 - Post-mortem planning

{kind=link}

Background

X's Class A, B and C shares of Amalco (a Canadian private corporation that was not a small business corporation) passed on his death...

29 May 2012 CTF Prairie Tax Roundtable, 2012-0445341C6 - Meaning of business as used in subsection 84(2)

CRA would generally not differentiate between a corporation carrying on an active business and a corporation carrying on a business of earning...

2012 Ruling 2011-0425211R3 - Reduction of capital

Pubco holds foreign affiliates owning non-core foreign exploration properties through two Canadian holding companies (Canco 1 and Canco 2). After...

2012 Ruling 2012-0435291R3 - Public Corporation PUC Reduction

{kind=link}

A CBCA Canadian public company (the "Corporation") transferred Canadian property, which represented substantially all of the assets used by it in...

2012 Ruling 2012-0432431R3 - Reduction of stated capital

Ruling that s. 84(2) will apply to the distribution by a resource public company of a resource subsidiary as a reduction of stated capital, in...

2012 Ruling 2012-0401811R3

At the time of death of Mr X, he held common and preferred shares of (and controlled) Holdco, which carried on an investing business and held a...

21 September 2011 External T.I. 2010-0375361E5 F - Liquidation d'une coopérative agricole

Respecting the treatment of the winding up of an agricultural cooperative within the meaning of s. 135.1(1) pursuant to which the cooperative...

2 June 2011 STEPs Roundtable Q. 5, 2011-0401861C6 - 2011 STEP - Q.5 - Post-Mortem Planning and 84(2)

An estate engages in a "pipeline" strategy in which it disposes of its shares of ACo (having a stepped-up adjusted cost base under s. 70(5)) to a...

8 October 2010 Roundtable, 2010-0373291C6 F - Tuck-Under Transactions - Safe Income Extractions

Given the acceptance of a tuck-under transaction in Vaillancourt-Tremblay, does CRA still consider that s. 84(2) should not apply to such a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | Vaillancourt-Tremblay did not validate all tuck-under transactions | 107 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2.1) - Paragraph 55(2.1)(c) | safe income can be extracted using tuck-under | 63 |

12 August 2010 External T.I. 2010-0370551E5 F - Tuck Under Transaction - Tremblay Decision

A non-resident holds 40% of the common shares of Opco and all of the shares of Holdco (also a Canadian private corporation) which, in turn, holds...

25 February 2010 External T.I. 2009-0352231E5 F - OBNL, profits, perte de statut, gain en capital

CRA , respecting the winding-up of a non-profit organization described in s. 149(1)(l):

If the association is a corporation with capital stock,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 149 - Subsection 149(1) - Paragraph 149(1)(l) | holding of surplus funds permissible only for funding a specific project | 161 |

27 May 2008 External T.I. 2008-0269441E5 F - Withdrawn Ruling Request

In explaining why, in contrast to 2005-0134731R3 F (the "Advance Ruling"), the Directorate could not rule on the proposed transactions, it...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | GAAR applied to use of outside basis, created with the capital gains exemption, for an inter-sibling transfer | 78 |

13 August 2007 External T.I. 2007-0224151E5 F - Surplus Stripping

CRA noted that the taxpayer’s request for rulings had been withdrawn for the reasons noted below in the summary (the text of the letter is...

29 June 2006 External T.I. 2006-0170641E5 F - Distribution of Corporate Property

In two rulings on post-mortem pipeline transactions (2002-0154223 and 2005-0142111R3), CRA required that the subject corporation remain in...

26 April 2006 Ruling 2004-0099201R3 F - GAAR Surplus Stripping

Mr. A is the sole shareholder of Aco, which generates an annual profit from its operations of more than $100,000. His Aco shares have a...

2004 Ruling 2004-0075471R3 - Stated capital reduction by a public corporation

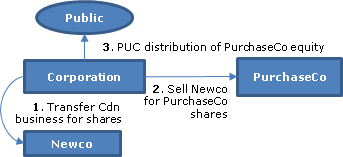

An indirect foreign subsidiary ("Forco 1") of a Canadian public company ("Opco 1" - likely, BCE Emergis Inc.) sold a foreign subsidiary of Forco...

17 December 2003 Internal T.I. 2003-0047367 F - Benefit Conferred on Non-arm's Length Person

The four equal common shareholders of Opco were X (a director and vice president), his wife ("Y"), Y's sister and the sister's husband, and X and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) | s. 246(1) applicable to sale of assets by corporation to employee-shareholder at an undervalue | 189 |

| Tax Topics - Income Tax Act - Section 52 - Subsection 52(1) | application of s. 15(1) or 246(1) to property distributed by corporation to shareholder would be added to the property’s ACB | 65 |

2003 Ruling 2002-018027

U.S.-resident shareholders of a Canadian investment company ("Canco") sell their shares of Canco to an unrelated Canadian purchaser ("Holdco"),...

10 October 2003 Roundtable, 2003-0029955 F - Surplus Stripping Post-Geransky

After negotiations with a purchaser, who is interested in the assets of the business of Opco, it is agreed that the Opco shareholders will sell...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 43 |

26 June 2003 External T.I. 2003-0021595 F - Distribution of Corporate Property

Two brothers (A and B), and their cousins (C and D, who were brothers) each held 50% of the shares of a holding company ("ABco" and ) ("CDco)" for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 107 - Subsection 107(2.1) | illustration of application, by virtue of s. 107(2.001) election, of s. 107(2.1) to distribution of CCPC shares | 157 |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(1) - Safe-Income Determination Time | s. 107(2.1) wind-up of trust holding a Portfolioco would trigger a safe-income determination time if with a view to an inter vivos pipeline transaction with a s. 88(2) wind-up of Portfolioco | 475 |

2000 Ruling 2000-0014443 - PUC Reduction

Ruling that a transfer by a Canadian public company in a taxable transaction of all the assets of a business to a Newco, followed by a...

30 November 1996 Ruling 9701523 - REDUCTION IN PUC OF PUBLIC CORP

Description of reorganization of a public corporation in which the paid-up capital of its issued and outstanding common shares are reduced through...

22 June 1990 T.I. (November 1990 Access Letter, ¶1534)

Where Mr. A effectively wishes to withdraw cash from a corporation of which he is the sole shareholder and accomplishes this by selling the shares...

88 C.R. - Q.34

The "amount or value" of the property distributed is reduced by liabilities assumed by the shareholder of the corporation.

Articles

Balaji (Bal) Katlai, Hugh Neilson, "Challenges and Caution: Using a Pipeline for Shareholder Remuneration", Tax for the Owner-Manager, Vol. 22, No. 4, October 2022, p. 1

Taking back high-PUC shares on pipeline (p. 1)

- In a pipeline transaction, even if there is an issuance of promissory notes by the transferee...

Kenneth Keung, Balaji Katlai, "CRA Essentially Approves Surplus Stripping by Amalgamation", Canadian Tax Focus, Vol. 11, No. 3, August 2021, p. 1

Surplus stripping suggested by CRA position on extracting cash on an amalgamation (p.1)

- 2018-0785921E5 and 2017-0696821E5 indicate that where...

Éric Hamelin, "Post Mortem Pipeline: The CRA Relaxes Its Position", Tax for the Owner-Manager, Vol. 20, No. 3, July 2020, p. 6

Immediate receipt of cash on pipeline to fund s. 70(5) taxes, p. 6

[I]n … 2018-0789911R3 … the CRA relaxed its longstanding position and...

Charles P. Marquette, "Hybrid Sale of Shares and Assets of a Business", Canadian Tax Journal, (2014) 62:3, 857 – 79.

Description of hybrid transaction using external step-up in basis method (pp. 878-9)

[T[he hybrid form of transaction for a corporate business...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 191 - Subsection 191(4) | 146 |

Perry Truster, "Turning Dividends into Capital Gains", Tax for the Owner-Manager, Volume 14, Number 1, January 2014, p. 7.

Sale of stock dividend shares for note which is repaid out of corporate surplus (p. 7)

[I]it is advantageous to convert distributions that would...

Steve Suarez, Firoz Ahmed, "Public Company Non-Butterfly Spinouts", 2003 Conference Report, c. 32.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110 - Subsection 110(1.8) | 0 | |

| Tax Topics - Income Tax Act - Section 55 - Subsection 55(2) | 0 |

Subsection 84(3) - Redemption, etc.

Cases

Macmillan Bloedel Ltd. v. R., 99 DTC 5454, [1999] 3 CTC 652 (FCA)

The taxpayer redeemed U.S.-dollar denominated preferred shares at a time that the U.S. dollar had appreciated relative to the exchange rate at the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(2) | loss on redemption of U.S.-dollar preferred shares | 101 |

See Also

McClarty Family Trust v. The Queen, 2012 DTC 1123 [at at 3122], 2012 TCC 80

A family holding company ("MPSI") paid a stock dividend of preferred shares, having nominal paid-up capital and a redemption amount of $48,000, on...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | 358 |

Gagnon v. The Queen, 2008 DTC 3111, 2006 TCC 194

The taxpayer originally signed an agreement for the sale of his half interest in a business (which was found to be held in a corporation) to his...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | person declared a shareholder retroactively | 149 |

MacMillan Bloedel Ltd. v. R., 97 DTC 1446, [1997] 3 C.T.C. 3012 (TCC), aff'd 99 DTC 5154

The taxpayer was found to have realized a capital loss under s. 39(2) rather than to have paid a deemed dividend under s. 84(3) when it redeemed...

Lalonde v. MNR, 90 DTC 1313, [1990] 1 CTC 2427 (TCC)

The taxpayer established that he purchased the shares of a fellow shareholder as agent for the corporation rather than as principal. Accordingly,...

Belair v. MNR, 89 DTC. 429, [1989] 2 CTC 2186 (TCC)

In the face of inadequate evidence, Morgan J. found that if the corporation had agreed to purchase for cancellation 1/3 of the taxpayer's common...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Legal and other Professional Fees | 60 |

Cabezuelo v. MNR, 83 DTC 769 (TCC)

The taxpayer received $25,000 in cash for shares plus a further balance payable over three years. After finding that these payments should be...

McArdle Estate [No. 2] v. MNR, 62 DTC 402 (TAB)

The president (McArdle) of a private company had been issued “employee redeemable shares,” whose terms provided that they participated on a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Substance | mistaken nomenclature ignored if inconsistent with governing intention | 66 |

Administrative Policy

13 May 2026 IFA Roundtable Q. 1, 2026-1087881C6 - Subsection 84(2) and Withholding Tax on Payments to Non-Residents

After noting its longstanding position that s. 84(3) would not apply to a payment made to a shareholder dissenting to an amalgamation by the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 84 - Subsection 84(2) | s. 84(2) generally does not apply to a payment made by Amalco to a shareholder dissenting to the amalgamation | 121 |

29 November 2022 CTF Roundtable Q. 3, 2022-0949771C6 - Post-closing adjustments and the impact to escrow shares

Under an agreement for the sale of a corporation (Target) solely for shares of the purchaser, which were validly issued on the closing, a portion...

25 November 2021 CTF Roundtable Q. 1, 2021-0911841C6 - Indemnities and subsection 87(4)

There has been a triangular amalgamation under which a subsidiary of Parent amalgamated with Target and the Target shareholders received shares of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(4) | payment of damages, for breach of reps, by the parent following a triangular amalgamation would not preclude satisfaction of s. 87(4) | 242 |

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(1) | damages paid for breach of rep following an amalgamation did not breach s. 87(1)(a) | 144 |

27 November 2018 CTF Roundtable Q. 5, 2018-0780041C6 - GAAR on PUC reduction

Shareholders of DCco transfer shares of DCco having an aggregate PUC of $10,000 and an ACB of $1,000 and a FMV higher than $10,000 to TCco in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) - Paragraph 88(1)(b) | where Parent acquired the net tax equity in Subco at a bargain price (low share ACB), avoiding a s. 88(1)(b) gain on wind-up through reducing PUC is abusive | 548 |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | avoidance of s. 88(1)(b) where insufficient safe income was abusive | 393 |

27 June 2018 External T.I. 2018-0745681E5 F - Wind-up of a partnership

A family farming partnership ("Partnership"), whose three partners equally owned the common shares of Opco, owned preferred shares of Opco, with a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 98 - Subsection 98(5) | s. 98(5) inapplicable on simultaneous dissolving transfer of partnership interests | 167 |

| Tax Topics - Income Tax Act - Section 28 - Subsection 28(1) - Paragraph 28(1)(f) | application of s. 28(1)(f) on partnership wind-up | 203 |

26 May 2016 IFA Roundtable Q. 3, 2016-0642111C6 - PUC of Shares of a FC Reporter

CRA considered that a Canadian corporation which has the U.S. dollar as its elected functional currency nonetheless is required to keep track of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 261 - Subsection 261(1) - Canadian Tax Results | deemed dividend calculation for shareholder not part of Cdn tax results | 323 |

2015 Ruling 2014-0532201R3 - Corporate reorganization

Towards the completion of an intricate internal reorganization for a privately-held Canadian corporate group, a newly-amalgamated corporation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 38 - Paragraph 38(a.1) | donation of pubco shares to foundation and immediate cash sale to affiliate | 521 |

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(1) - Total Charitable Gifts | donation and sale-back of public company shares | 85 |

S4-F7-C1 - Amalgamations of Canadian Corporations

1.5 …[S]ubsection 84(3) will not otherwise apply to deem a shareholder of a predecessor corporation to have received a dividend where the...

29 October 2013 External T.I. 2013-0507881E5 - Price adjustment clause

A price adjustent clause in the share provisions for preferred shares issued by Opco to the taxpayer in Year 1 in consideration for the transfer...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | 330 |

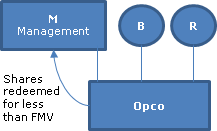

3 July 2012 Internal T.I. 2012-0450821I7 F - Interaction of 84(3) and 69(1)(b)

{kind=link}

A CCPC ("Opco"), whose voting common shares were owned by two individuals (B and R) and by a Canadian-controlled private corporation ("M Holdco")...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(b) | s. 69(1)(b) adjustment generates capital gain even though larger share redemption proceeds in the 1st place would have been exempt | 223 |

29 November 2011 Roundtable, 2011-0426361C6 F - Price adjustment clause and redemption of shares

Subsequent to an estate freeze, the freeze preferred shares were redeemed (in 2006). In 2011, it was determined that the redemption amount was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | deemed dividend through operation of price adjustment clause arises in the adjustment rather than redemption year | 63 |

21 November 2011 External T.I. 2011-0422191E5 F - Price adjustment clause and redemption of shares

if preferred shares with a redemption amount which is subject to a price adjustment clause are redeemed before there is an upward adjustment to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | additional payment, pursuant to price adjustment clause, in year following shares; redemption is recognized then | 54 |

23 July 2007 Internal T.I. 2007-0228601I7 F - Redemption of U.S. Denominated Shares

Parentco owned preferred shares of a subsidiary wholly-owned corporation (Holdco) denominated in U.S. dollars. Holdco purchased the preferred...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(2) | s. 86 exchange of US-dollar denominated prefs does not affect patrimony of issuer | 75 |

15 January 2007 Internal T.I. 2006-0216801I7 - Redemption of US $ Denominated Shares

Confirmation of a previous position that in light of the MacMillan Bloedel decision, CRA intends to assess any redemption of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(2) | s. 39(2) application on USD pref redemption, cf. if USD common shares | 77 |

28 October 2005 External T.I. 2005-0145891E5 F - Redemption of Shares - Balance of Purchase Price

On January 1, 2005, Canco purchases for cancellation 100 common shares, having a fair market value of $100,000, in consideration for paying...

2004 APFF Roundtable Q. 15, 2004-008682

Respecting the situation where a subsidiary purchases for cancellation a portion of the common shares in its capital held by its wholly-owning...

31 December 2004 Internal T.I. 2004-0091781I7 - Redemption for Proceeds Less than FMV

In a situation where preferred shares were redeemed for an amount less than the fair market value, the Directorate stated that "where, in a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(1) - Paragraph 69(1)(b) | s. 69 rather than s. 84(3) applies where FMV excess | 135 |

10 October 2003 Roundtable, 2003-0030005 F - $500,000 Deduction - Application of GAAR

A purchaser is interested in purchasing an operating subsidiary ("Opco") of a management corporation ("Managementco") and not Managementco....

1 November 2002 External T.I. 2002-0146775 - Share Sale by Employees Yields Cap. Gain

Where employees of Opco (who as a group, own 14% of its issued common shares) are terminated, they are required to sell their Opco common shares...

2002 Ruling 2002-0138993 - XXXXXXXXXX . - 95(2)(a)(ii)(D)

A foreign subsidiary ("Holdco") which is making a takeover bid for a public corporation in the same foreign jurisdiction ("Targetco'), acquires...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(a) - Subparagraph 95(2)(a)(ii) - Clause 95(2)(a)(ii)(D) | 110 |

10 August 2000 External T.I. 2000-0016875 - SAR DISPOSITION, SHARES

"Where an employee has income from employment under paragraph 7(1)(a) related to the disposition, by virtue of subsection 7(1.1), of shares and a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | 83 | |

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(3) - Paragraph 7(3)(a) | 36 |

26 October 1998 Internal T.I. 9803947 - REDEMPTION OF SHARES

Where shares held by a financial institution are redeemed, s. 84(3) will be considered to take precedence over s. 142.5(1), and s. 248(28) will...

6 June 1997 Internal T.I. 9631867 - REDEMPTION OF SHARES HELD BY FINANCIAL INSTITUTIONS

S.142.5(1) takes precedence over s. 84(3). To the extent that an amount has been included in computing income under s. 142.5(1), such amount will...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 142.5 - Subsection 142.5(1) | 38 |

6 July 1995 External T.I. 9316465 F - Payment to Dissenting Shareholders on Amalgamation

In response to a proposal that a payment be made to a separated wife of a husband by her dissenting to the amalgamation of a corporation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | 153 |

12 August 1994 External T.I. 9415495 - AMALGAMATION/WIND-UP

Where there is a wind-up of a wholly-owned subsidiary that also owns shares of its parent, s. 84(3) will not apply to the subsidiary because the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(1) | 89 | |

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) | 68 |

30 March 1994 External T.I. 9337225 - SHARES HELD AS INVENTORY

On the redemption of shares held as inventory, a deemed dividend will arise pursuant to s. 84(3) and, to the extent that the paid-up capital of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Computation of Profit | 72 |

93 C.R. - Q. 56

Cash payments received from an amalgamated corporation for shares held by shareholders dissenting from the amalgamation will be proceeds of...

3 September 1991 T.I. (Tax Window, No. 8, p. 21, ¶1436)

S.84(3) does not apply to deem a dividend to have been paid when shares of a corporation owned by its wholly-owned subsidiary are cancelled on the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 88 - Subsection 88(1) | 32 |

3 July 1991 T.I. (Tax Window, No. 5, p. 13, ¶1334)

S.84(3) does not apply to an amalgamation to which s. 87 applies.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 87 - Subsection 87(2) - Paragraph 87(2)(a) | 23 |

31 May 1990 T.I. (October 1990 Access Letter, ¶1469)

With respect to an argument that where a corporation purchases for cancellation only some of the shares of a given class and pays an amount...

87 C.R. - Q.59

A shareholder dissenting pursuant to s. 184 of the CBCA who receives cash from the amalgamated corporation realizes proceeds of disposition rather...

87 C.R. - Q.69

Where a share having a high stated capital and low paid-up capital is exchanged in a s. 86 reorganization for another share with a high stated...

84 C.R. - Q.45

The calculation of the amount of the dividend arising on a purchase for cancellation will include the value of any type of consideration given for...

Articles

Didier Fréchette, Ryan Rabinovitch, "Current Issues Involving Foreign Exchange", 2015 CTF Annual Conference paper

Whether deemed dividend on redemption of USD preferred shares (pp. 26:35-39)

A Canadian-resident corporation issues preferred shares for US$100...

R. Durand, I.M. Freedman, "Dealing with Paid-Up Capital", 1997 Corporate Management Tax Conference Report, c. 17.

Subsection 84(4)

Articles

Didier Fréchette, Ryan Rabinovitch, "Current Issues Involving Foreign Exchange", 2015 CTF Annual Conference paper

Whether deemed dividend on returns of capital of USD shares (p. 26:39-40)

[A] Canadian corporation issues a preferred share for US$100 per share...

Subsection 84(4.1) - Deemed dividend on reduction of paid-up capital

Articles

Judith Paris, "Paid-Up Capital and Return of Capital Public Corporations", Business Vehicles, Vol. VI, No. 2, 2000, p. 290.

Subsection 84(5) - Amount distributed or paid where a share

Administrative Policy

1 June 2001 External T.I. 2001-0075455 F - Remaniement et capital versé

On a reorganization of capital, Ms. A exchanges her common shares of Aco, having a PUC and ACB of $10 and an FMV of $10,000 (with the balance of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 86 - Subsection 86(2.1) | PUC reduction under s. 86(2.1) of new shares to PUC of old shares | 95 |

18 Aug. 89 T.I. (Jan. 90 Access Letter, ¶1082)

On the transfer by Mr. A of 1/2 of the common shares of Opco to Opco in exchange for preferred shares of Opco having 1/2 the paid-up capital of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110.6 - Subsection 110.6(2.1) | 67 | |

| Tax Topics - Income Tax Act - Section 84.1 - Subsection 84.1(1) | 43 |

Subsection 84(6) - Where s. (2) or (3) does not apply

Administrative Policy

7 January 1998 External T.I. 9712655 - NORMAL COURSE ISSUER BID

A normal course issuer bid would not give rise to deemed dividends.

1997 Ruling 971084

The purchase by the issuer of common shares held by a majority holding company would not taint the application of s. 84(6) with respect to its...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 183.1 - Subsection 183.1(2) | 33 |

90 C.R. - Q50

The reference to the "manner in which shares would normally be purchased by any member of the public in the open market" means that the shares...

Subsection 84(7)

Administrative Policy

4 January 2012 External T.I. 2011-0414731E5 F - Interaction between 84.1 and 83(2) ITA

Before concluding that the “CRA does not intend to adopt a permissive administrative position permitting a s. 83(2) election where there is a s....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 83 - Subsection 83(2) | no s. 83(2) election available for s. 84.1(1)(b) deemed dividend paid to non-shareholder | 48 |

Subsection 84(9) - Shares disposed of on redemptions, etc.

Cases

EYEBALL NETWORKS INC. v. HER MAJESTY THE QUEEN, 2021 FCA 17

Pursuant to a conventional s. 55(3)(a) spin-off transaction, a company (“Oldco”) spun off one of its two businesses to a “Newco,” also...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 160 - Subsection 160(1) | s. 160 did not apply to s. 55(3)(a) where each step involved a value-for-value exchange (including the cross-share redemptions) | 565 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | “series of transactions” requires at least one tax-driven transaction | 284 |

| Tax Topics - General Concepts - Effective Date | price adjustment clause eliminated any possible value discrepancy between the FMV of the transferred property and the consideration therefor | 118 |

| Tax Topics - General Concepts - Fair Market Value - Other | note supported only by pref, then note, of a sister had full FMV | 132 |

See Also

Gaumond v. The Queen, 2014 DTC 1024 [at at 98], 2014 TCC 339 (Informal Procedure)

The taxpayer renounced debt owing to him by his small business corporation pursuant to a bankruptcy proposal. Lamarre J found that, in the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(1) - Paragraph 39(1)(c) | renounced debt is not disposed of to anyone/s. 50 not available where debt settled in year | 277 |

| Tax Topics - Income Tax Act - Section 50 - Subsection 50(1) | s. 50 not available where debt settled in year | 108 |

Special Risks Holdings Inc. v. The Queen, 86 DTC 6035, [1986] 1 CTC 201 (FCA)

The taxpayer, following a modification in the capital structure of a company ("RMC") exchanged its voting shares of that company for non-voting...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | relationship enabling one party to dictate terms | 148 |

| Tax Topics - Income Tax Act - Section 86 - Subsection 86(1) | 166 |

Administrative Policy

20 February 1991 T.I. (Tax Window, No. 2, p. 8, ¶1182)

Where a corporation is wound up and the shares are cancelled as a result of the winding-up, s. 84(9) does not apply.

10 January 1990 T.I. (June 1990 Access Letter, ¶1257)

Under Canadian corporate law, the shares of a corporation which is being wound-up or liquidated are not disposed of "to a person" as a result of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(2) - Paragraph 40(2)(e) | 52 |

IT-484R "Business Investment Losses"

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(1) - Paragraph 39(1)(c) | 0 | |

| Tax Topics - Income Tax Act - Section 164 - Subsection 164(6) | 48 |

Articles

Gregory M. Johnson, Wesley R. Novotny, "An Update on Flow-through Shares in the Energy Sector", 2016 Conference Report (Canadian Tax Foundation),12:1-39

Flow-through shares issued after announcement of long-form amalgamation may be prescribed shares (p. 12:20-21)

...On an amalgamation, it is...

Commentary

Benefit of coming within s. 84(2)

Along with the exception described in draft ss. 84(4.1)(a) and (b), and a reorganization of capital described in...