Cases

ExxonMobil Canada Resources Company v. The King, 2026 TCC 42

The US parent of the taxpayer (“EM Corp.”), and two other oil and gas companies (“BP Alaska” and “Phillips Alaska”) entered into an...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Onus | non-suit motions should not be entertained after the close of evidence | 178 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4) - Paragraph 152(4)(b) - Subparagraph 152(4)(b)(iii) | the reassessed feasibility costs of the Cdn taxpayer were incurred by it as a result of an assignment of an interest in the related project agreement to it by its NR parent | 341 |

| Tax Topics - General Concepts - Evidence | in the absence of evidence as to the effect of Alaskan law, lex fori was applied | 89 |

| Tax Topics - Income Tax Act - Section 3 - Paragraph 3(a) | the taxpayer’s costs for a pipeline feasibility study were incurred in relation to a source of income (the pipeline or use of the information generated) | 327 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Incurring of Expense | taxpayer incurred costs as a result of a partial assignment to it of an agreement for conducting a feasibility study | 341 |

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) - Paragraph 247(2)(b) | taxpayer was assigned a portion of a pipeline feasibility project as a likely Canadian participant in any pipeline, and the alternative fee-for-services model was not well established | 268 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(9) | pleading of Part XIII tax arising from the conferral of a benefit was sufficient to ground a Crown argument that the benefit arose under s. 56(2) | 314 |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | entering into a bona fide transaction with a shareholder does not entail the conferral of a benefit | 94 |

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | s. 246(1) cannot satisfy the “benefit” requirement of s. 56(2) so as to engage s. 214(3)(a) | 269 |

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) - Paragraph 246(1)(b) | s. 246(1)(b) benefit is not deemed to be a dividend | 265 |

| Tax Topics - Income Tax Act - Section 214 - Subsection 214(3) - Paragraph 214(3)(a) | s. 214(3)(a) does not deem a s. 56(2) or 246(1) benefit to be a dividend | 286 |

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) - Paragraph 247(2)(a) | terms of cross-border agreement for the sharing of the costs of a pipeline feasibility study were commercially appropriate | 366 |

Potash Corporation of Saskatchewan Inc. v. Canada, 2024 FCA 35

The taxpayer (PCS), which produced and sold potash from mines in Saskatchewan, was subject to both a profit tax and to the making of “base...

Paletta International Corporation v. Canada, 2021 FCA 182

Hogan J had found that a tax shelter partnership, which had funded the prints and advertising expenses for films that it had purchased from...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Sham | no requirement for the Crown to explicitly plead “sham” | 255 |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Real Estate | potential to resell under secondary intention doctrine must be an operating motivation to the acquisition | 53 |

Canadian Imperial Bank of Commerce v. Canada, 2013 DTC 5098 [at at 6020], 2013 FCA 122

The taxpayer paid approximately $3 billion in settlements relating to claims that it or its subsidiaries were jointly and severally liable with...

Lyncorp International Ltd. v. Canada, 2012 DTC 5032 [at at 6684], 2011 FCA 352, aff'g 2010 DTC 1351 [at 4335], 2010 TCC 532

The taxpayer, owned and operated by Mr. Mullen, invested in shares and made non-interest bearing loans to a number of corporate ventures to which...

Teck Corp. v. The Queen, 2005 DTC 5338, 2004 BCCA 514

Mining taxes paid by the taxpayer to the provinces of Ontario, Quebec and Newfoundland and Labrador were income taxes the deduction of which was...

McNeill v. The Queen, 2000 DTC 6211 (FCA)

Some years after the taxpayer sold his chartered accountancy practice to another firm, he was ordered to pay damages and costs of $465,908 in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Timing | 102 | |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Damages | deductible damages for breach of non-compete | 112 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Loss v. Loss - Damages | damages incurred to keep clients were deductible | 122 |

65302 British Columbia Ltd. v. Canada, 99 DTC 5799, [1999] 3 S.C.R. 804

The taxpayer, which was a registered egg producer, deliberately produced over quota in order to maintain its major customer, (who was expanding),...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Public Policy | 71 | |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Improvements v. Repairs or Running Expense | avoidance of threat to business not relevant to income treatment | 124 |

| Tax Topics - Statutory Interpretation - Drafting Style | avoid policy conjectures in detailed and complex statute | 126 |

| Tax Topics - Statutory Interpretation - Ease of Administration | avoidance of undue burden on taxpayer | 74 |

| Tax Topics - Statutory Interpretation - Resolving Ambiguity | 125 |

Taylor v. R., 97 DTC 5120, [1997] 2 CTC 201 (FCA)

In a situation where the taxpayer had misappropriated funds from 1986 to 1989, then effected restitution in 1990, Linden J.A. stated that "the...

Amway of Canada. Ltd. v. The Queen, 96 DTC 6135, [1996] 2 CTC 162 (FCA)

Strayer J.A. found that all amounts paid by the taxpayer to Revenue Canada in settlement of an enforcement action brought against it pursuant to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Public Policy | 156 |

Tonn v. The Queen, [1996] 1 CTC 205 (FCA)

Before going on to find that rental losses incurred by the taxpayers were fully deductible by them, Linden J.A. stated (at p. 6005) that s....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Reasonable Expectation of Profit | REOP test should be applied sparingly if no personal element | 154 |

| Tax Topics - Income Tax Act - Section 3 - Paragraph 3(a) - Business Source/Reasonable Expectation of Profit | 154 |

Poetker v. MNR, 95 DTC 5614, [1996] 1 CTC 202 (FCA)

Before affirming the finding of the Tax Court judge that the taxpayer was not able to deduct persistent losses from two condominium units that the...

Symes v. Canada, 94 DTC 6001, [1993] 4 S.C.R. 695, [1994] 1 CTC 40

Before indicating that it was unnecessary to determine whether there should be a change in the traditional position that child care expenses (in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Other Legislation/Constitution - Charter (Constitution Act, 1982) - Subsection 15(1) | 90 | |

| Tax Topics - General Concepts - Evidence | 80 | |

| Tax Topics - General Concepts - Stare Decisis | 69 | |

| Tax Topics - Income Tax Act - Section 63 - Subsection 63(1) | 45 | |

| Tax Topics - Income Tax Act - Section 9 - Accounting Principles | 70 | |

| Tax Topics - Statutory Interpretation - Specific v. General Provisions | deduction to extent limited by a specific provision could not be deducted under a general provision | 74 |

| Tax Topics - General Concepts - Purpose/Intention | purpose to be determined having regard to objective manifestations thereof | 132 |

The Queen v. Shefner Estate, 93 DTC 5482, [1993] 2 CTC 273 (FCTD)

The expropriation committee of the City of Anjou threatened to pursue criminal and civil action against the taxpayer and a corporation owned by...

Parkland Operations Limited v. Her Majesty the Queen, 90 DTC 6676, [1991] 1 CTC 23 (FCTD)

A loss of $563,396 which the taxpayer suffered from defalcations made by minority shareholders was found to have resulted from wrongful draw-downs...

Graves v. The Queen, 90 DTC 6300 (FCTD)

The taxpayers were entitled to deduct a portion of their house expenses based on the square footage of 1/2 of their basement relative to their...

Friedland v. The Queen, 89 DTC 5341, [1989] 2 CTC 79 (FCTD)

The taxpayer was able to deduct the payment by it of expenses incurred by its individual shareholder in connection with driving his BMW and Rolls...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | payment of legals protected corporate business | 149 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Legal and other Professional Fees | 112 |

La Compagnie Idéal Body Inc. v. The Queen, 89 DTC 5344, [1989] 2 CTC 187 (FCTD)

A private corporation which prior to the death of its principal shareholder had regularly declared and paid bonuses to him of under $100,000 was...

Moloney v. The Queen, 89 DTC 5062, [1989] 1 CTC 162 (FCTD), aff'd 92 DTC 6570 (FCA)

The taxpayer and other individuals each paid $20,000 to an off-shore corporation ("Applied Research") purportedly as a pre-paid royalty for a...

Mattabi Mines Ltd. v. Ontario (Minister of Revenue), [1988] 2 CTC 294, [1988] 2 S.C.R. 175

In response to a submission that mining machinery and equipment had not been purchased "for the purpose of earning income" because the profits...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(a) - Revising Claims | CCA claim revisions that would advantage statute-barred years were denied | 77 |

| Tax Topics - Statutory Interpretation - Comparison of Provisions | "income" has same meaning in different sections | 114 |

| Tax Topics - Statutory Interpretation - Interpretation Bulletins, etc. | 34 | |

| Tax Topics - Statutory Interpretation - Resolving Ambiguity | 56 |

Mott v. The Queen, 88 DTC 6359, [1988] 2 CTC 127 (FCTD)

Since travelling expenses incurred for the purpose of commuting between one's place of residence and place of business are not deductible,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 31 - Subsection 31(1) | 65 |

The Queen v. Royal Trust Corp. of Canada, 83 DTC 5172, [1983] CTC 159 (FCA)

In an underwriting agreement, the taxpayer agreed to issue common shares to the underwriter at $8.00 per share and pay an underwriting commission...

The Queen v. Dorchester Drummond Corp. Ltd., 79 DTC 5163, [1979] CTC 219 (FCTD)

The defendant company bought land with the intention of building a highrise office building thereon, but instead operated a parking lot on the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(5) - Paragraph 111(5)(a) | parking lot operator carrying on a real estate development business notwithstanding that parking lot shut down | 74 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Start-Up and Liquidation Costs | 86 | |

| Tax Topics - Income Tax Act - Section 4 - Subsection 4(1) - Paragraph 4(1)(a) | 25 | |

| Tax Topics - Statutory Interpretation - Interpretation Act - Subsection 45(2) | 42 |

Deputy Minister of Revenue (Quebec) v. Lipson, [1979] CTC 247, [1979] 1 S.C.R. 833

The shareholders of a company which was incorporated in 1961 to own and operate an apartment building, in 1962 leased the building from the...

Frappier v. The Queen, 76 DTC 6066, [1976] CTC 85 (FCTD)

The taxpayer, who was a licensed investment dealer, made advances to her clients to cover their losses when the brokerage company for which she...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Timing | advances against future losses | 50 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Loss v. Loss | 63 | |

| Tax Topics - Income Tax Act - Section 5 - Subsection 5(1) | 79 |

Sunshine Mining Co. v. R., 75 DTC 5126, [1975] C.T.C. 223 (FCTD)

Damages paid by the taxpayer as a consequence of its failure to perform exploration work under an agreement to earn one-half interests in mining...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Contract or Option Cancellation | 62 |

The Queen v. Clark, 74 DTC 6242, [1974] CTC 305 (FCTD)

A cash-basis farmer purchased cattle from a cattle company at the end of his taxation year on the understanding that the cattle company would...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Old | 60 |

First Pioneer Petroleums Ltd. v. MNR, 74 DTC 6109, [1974] CTC 108 (FCTD)

Income taxes are not deductible expenses because, "by their very nature the income taxes were incurred because income was gained or produced and...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 256 - Subsection 256(2.1) | 60 |

E.R. Squibb & Sons Ltd. v. MNR, 73 DTC 5139, [1973] CTC 120 (FCTD)

In 1952, the taxpayer purchased 52 acres of land outside Montreal in order to construct its own facilities for use in research, manufacturing and...

Henry v. Minister of National Revenue, 72 DTC 6005, [1972] CTC 33, [1974] S.C.R. 155

The taxpayer was an anaesthetist who supplied his services to a hospital, maintained an office at another location (Douglas Street) in common with...

Olympia Floor & Wall Tile (Quebec) Ltd. v. MNR, 70 DTC 6085, [1970] CTC 99 (FCTD)

Gifts which the taxpayer made to Jewish organizations in the Montreal area in amounts over $100 were accepted to have been made for the purpose of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110.1 - Subsection 110.1(1) - Paragraph 110.1(1)(a) | donations deductible as business expenses rather than as gifts | 94 |

British Columbia Power Corporation, Limited v. Minister of National Revenue, 67 DTC 5258, [1967] CTC 406, [1968] S.C.R. 17

The taxpayer incurred various expenses in connection with communicating with its shareholders respecting B.C. legislation under which its shares...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Legal and other Professional Fees | 216 |

Associated Investors of Canada Ltd. v. MNR, 67 DTC 5096, [1967] CTC 138 (Ex. Ct.)

Before going on to find that the taxpayer was entitled to write off the irrecoverable amount of advances made by it to an employee, Collier J....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Timing | 122 | |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(p) - Subparagraph 20(1)(p)(i) | write-offs deductible on general principles | 165 |

| Tax Topics - Statutory Interpretation - Expressio Unius est Exclusio Alterius | 125 |

Southam Business Publications Ltd. v. MNR, 66 DTC 5215, [1966] CTC 265 (Ex. Ct.), briefly aff'd 67 DTC 5150 (SCC)

Noël J. held that there is no question that an expenditure made by the taxpayer to acquire the Financial Times was made for the purpose of...

Premium Iron Ores Ltd. v. Minister of National Revenue, 66 DTC 5280, [1966] CTC 391, [1966] S.C.R. 685

Before concurring with Martland and Spence JJ. that legal expenses incurred by the taxpayer in connection with challenging potential assessments...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Legal and other Professional Fees | 100 | |

| Tax Topics - Income Tax Act - Section 9 - Nature of Income | prior enforceable agreement to on-pay the receipt | 113 |

Quemont Mining Corp. Ltd. v. MNR, 66 DTC 5376, [1966] CTC 570 (Ex. Ct.), aff'd 70 DTC 6046 (SCC)

"Duties" payable on a graduated scale under the Quebec Mining Act on the difference between the gross value of mining output and specified...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 126 - Subsection 126(7) - Non-Business-Income Tax | 79 | |

| Tax Topics - Statutory Interpretation - Interpretation Act - Subsection 15(2) | 53 |

Seaboard Advertising Co. Ltd. v. MNR, 65 DTC 5188, [1965] CTC 310 (Ex. Ct.)

Unexpired advertising contracts which the taxpayer acquired as part of the purchase of substantially all the business of a competitor were...

MNR v. Eldridge, 64 DTC 5338, [1965] 1 Ex. C.R. 758, [1964] CTC 545

The taxpayer, the operator of an unlawful call girl business, was entitled to deduct the expenses incurred in earning the profits of that business...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Exempt Receipts/Business | profits of call girl operation were taxable | 79 |

MNR v. E.H. Pooler & Co. Ltd., 62 DTC 1321, [1962] CTC 527 (Ex. Ct.)

The taxpayer, which carried on business as a stock broker, was required to pay a fine to the T.S.E. as a result of one of its vice-presidents...

Meteor Homes Ltd. v. MNR, 61 DTC 1001, [1960] CTC 419 (Ex. Ct.)

A payment which one group of shareholders (the "Schoelas") caused the taxpayer to make to another group of shareholders (the "Manasters") was...

Bannerman v. Minister of National Revenue, 59 DTC 1126, [1959] CTC 214, [1959] S.C.R. 562

In discussing the replacement of s. 6(a) in the Income War Tax Act by s. 12(1)(a) of the Income Tax Act, Kerwin C.J. stated (p. 1127):

"In view of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Legal and other Professional Fees | 100 |

British Columbia Electric Railway Company Limited v. The Minister of National Revenue, 58 DTC 1022, [1958] CTC 21, [1958] S.C.R. 133, [1958] CTC 20

Before finding that payments made to municipalities in order to secure their acquiescence to the taxpayer's application for permission to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Contract or Option Cancellation | payments to secure cancellation of obligation to provide passenger rail service were capital expenditures that increased value of taxpayer's franchises | 102 |

Royal Trust Co. v. MNR, 57 DTC 1055, [1957] CTC 28 (Ex. Ct.)

It was found that the taxpayer's purpose in paying the admission fees and annual dues of social clubs of which its officers were members "was to...

Montship Lines Ltd. v. MNR, 54 DTC 1151, [1954] CTC 295 (Ex. Ct.), briefly aff'd 55 DTC 1060 (SCC)

Repair expenditures which the taxpayer incurred in accordance with the terms of agreements for the sale by it of two vessels were incurred in...

Imperial Oil Ltd. v. MNR, 3 DTC 1090, [1947] CTC 353, [1946-1948] DTC 1090 (Ex. Ct.)

Due to the negligence of its employees a vessel of the taxpayer caused another company's vessel to sink. A substantial sum which the taxpayer paid...

See Also

Bank of Montreal v. The King, 2025 TCC 113

The taxpayer, a Canadian chartered bank, was assessed in 2004 and 2006 for additional U.S. federal income tax and interest, or New York City...

Agences Kyoto ltée v. Agence du revenu du Québec, 2023 QCCQ 2921

The ARQ denied the deduction of the full amount of the management fees paid by the taxpayer (AK) to its wholly-owning parent (GAK) on the basis...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Evidence | no requirement for management fees to be pursuant to a written management agreement | 133 |

Morin v. Agence du revenu du Québec, 2023 QCCQ 2406

Prior to 2002, a pharmacist (“Morin”) carried on directly and through her employees all of the operations of six pharmacies. A services...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4) - Paragraph 152(4)(a) - Subparagraph 152(4)(a)(i) | taxpayer not negligent in relying on the efficacy of a plan originating with her tax advisors | 227 |

Potash Corporation of Saskatchewan Inc. v. The Queen, 2022 TCC 75, aff'd 2024 FCA 35

The taxpayer, which produced and sold potash from mines in Saskatchewan, was subject to a profit tax and to the making of “base payments”...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(m) | sales of potash “related to” potash production | 308 |

DiCaita v. The Queen, 2021 TCC 5 (Informal Procedure)

A condo unit, which the taxpayer had been renting-out for many years, was vacated by the current tenant and ceased to be rentable at a reasonable...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Improvements v. Repairs or Running Expense | reconditioning of rental unit allowed as deductible expense | 242 |

| Tax Topics - Income Tax Act - Section 3 - Paragraph 3(a) - Business Source/Reasonable Expectation of Profit | rental unit was a source of income even when not rentable due to on-going renovations | 77 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(12) | significant time must be spent in home office to justify significant deduction | 166 |

Spiegel Sohmer Inc. v. Agence du revenu du Québec, 2021 QCCQ 69

The individual taxpayer (“Raich”), who was a senior tax partner of a Montreal law firm, sought and received reimbursement from the firm’s...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | reimbursing expenses for the wedding of a law firm partner’s daughter generated a taxable benefit | 164 |

Paletta v. The Queen, 2019 TCC 205, aff'd 2021 FCA 182

A taxpayer used U.S.$82M that had largely been indirectly financed by Twentieth Century Fox to fund, as partner, prints and advertising expenses...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Sham | film marketing partnership loss denied on the basis that an alleged option was a sham | 415 |

| Tax Topics - Income Tax Regulations - Regulation 231 - Subsection 231(6) | expectation of repurchase option being exercised generated a prescribed benefit | 207 |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Real Estate | rental revenues were incidental to secondary intention save for land with 25-year hold | 309 |

| Tax Topics - General Concepts - Evidence | TCC not bound by admission contrary to facts where benefiting party has adduced evidence on point | 50 |

Tournier v. The Queen, 2018 TCC 229 (Informal Procedure)

A retired member of Nova Scotia bar was permitted to deduct $1200 of annual storage fees for client files notwithstanding that her practice had...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Start-Up and Liquidation Costs | file storage fees incurred after business cessation were deductible | 262 |

Béliveau v. The Queen, 2018 TCC 87

The taxpayer, a self-employed dental surgeon, received benefits totalling over $600,000 under three Great-West policies during a two-year period...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Compensation Payments | insurance benefits received by an ill dental surgeon to cover her practice expenses were taxable receipts | 280 |

Fonds de solidarité des travailleurs du Québec (F.T.Q) v. The Queen, 2018 TCC 3, aff'd on s. 18(1)(a) grounds 2019 FCA 36

The corporate taxpayer agreed with the City of Chandler that it would no longer use any loan repayment proceeds received by it from a City-owned...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110.1 - Subsection 110.1(1) - Paragraph 110.1(1)(a) | consideration for "gift" was elimination of obligation to invest the funds | 523 |

| Tax Topics - Income Tax Act - Section 118.1 - Subsection 118.1(1) - Total Charitable Gifts | payment relieving of a correlative contractual obligation was not a gift | 125 |

Emballages Starflex Inc. v. Agence du revenu du Québec, 2016 QCCA 1856

The taxpayer requested, at the trial's opening, to amend its pleadings to claim, in the alternative, that donations made by it to U.S. charities,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 110.1 - Subsection 110.1(1) - Paragraph 110.1(1)(a) | charitable donations not deductible as business expense | 181 |

| Tax Topics - Statutory Interpretation - Specific v. General Provisions | charitable gift rules a complete code | 158 |

Acornwood LLP & Ors v. Revenue and Customs Commissioners, [2016] BTC 517, [2016] UKUT 0361 (Tax and Chancery Chamber)

In the appeal before him by five limited liability partnerships (the “LLPs”) respecting the disallowance of expenditures as trading losses,...

Grenon v. The Queen, 2014 DTC 1207 [at 3805], 2014 TCC 265, aff'd 2016 DTC 5009 [at 6544], 2016 FCA 4

Graham J found that the taxpayer's legal expenses incurred in the course of his separation from his former spouse were not deductible as a...

Emballages Starflex Inc. v. ARC, 2015 QCCQ 7455 (Cour du Québec), see also 2016 QCCA 1856

At the trial's opening, the taxpayer requested an amendment to its pleadings to argue in the alternative that donations made by it to U.S....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 21 | Quebec provision providing Quebec exemption to amounts exempted by Canada did not apply to Art. XXI, para. 7 of the US Convention | 214 |

Bessette v. ARC (Quebec Revenue Agency), 2014 QCCQ 4329

The dental practice of the taxpayer paid fees of approximately 70% of its revenues to a services company (which was wholly-owned by the dentist...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Sham | professional "services" corporation with no employees | 209 |

Michaud v. The Queen, 2014 DTC 1089 [at at 3152], 2014 TCC 83 (Informal Procedure)

Hogan J found that the fact that the taxpayer often took his children along on his prospecting trips did not change that the prospecting...

Garber v. The Queen, 2014 DTC 1045 [at at 2812], 2014 TCC 1

Each taxpayer bought units in a limited partnership, which was to acquire a large yacht to be used for catered vacation charters. However, the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 13 - Subsection 13(21) - Depreciable Property | title not held by GP on behalf of partnership | 122 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | no source required if reasonable expectation of income | 241 |

| Tax Topics - Income Tax Act - Section 3 - Paragraph 3(a) - Business Source/Reasonable Expectation of Profit | fraudulent scheme not a source | 240 |

| Tax Topics - Income Tax Act - Section 96 | GP had fraudulent intention | 241 |

| Tax Topics - Income Tax Regulations - Regulation 1102 - Subsection 1102(1) - Paragraph 1102(1)(c) | asset was mere window-dressing | 146 |

Harvey v. The Queen, 2013 TCC 298

The taxpayer's teenaged daughter and her friends (all without a driving licence) took the taxpayer's Jeep without his permission and got into an...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Evidence | 196 | |

| Tax Topics - Income Tax Act - Section 163 - Subsection 163(2) | guilty plea is prima facie proof of income from tax evasion | 111 |

Lequier v. The Queen, 2013 DTC 1012 [at at 68], 2012 TCC 380

The taxpayer bought a 10-room inn and lived in it. He started a company ("La Zénon) to operate the inn, which had a restaurant and bar.

Paris J...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 8 - Subsection 8(1) - Paragraph 8(1)(f) | 105 |

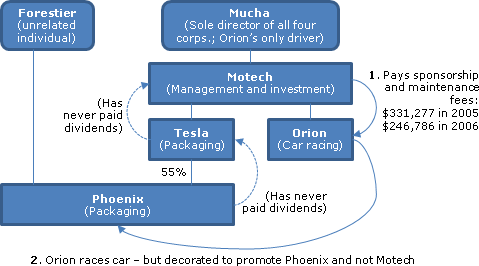

Motech Molding Inc. v. The Queen, 2012 DTC 1293 [at at 3913], 2012 TCC 351

{kind=link}

The taxpayer held two corporations ("Tesla" and "Orion"), and Tesla Packaging held 55% of the shares of another corporation ("Phoenix"). Tesla...

Chow v. The Queen, 2011 DTC 1196 [at at 1088], 2011 TCC 263

V.A. Miller J. found (at para. 27) that the seizure of approximately $110,000 of proceeds of drug trafficking at the taxpayer's apartment did not...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 67.6 | 77 |

Big Bad Voodoo Daddy v. The Queen, 2011 DTC 1173 [at at 955], 2011 TCC 226 (Informal Procedure)

The taxpayer was a U.S. limited liability corporation (LLC) which performed jazz concerts in Canada. A CRA appeals officer stated in his...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 96 | LLC treated as corporation | 140 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Corporation | LLC was corporation | 65 |

4145356 Canada Limited v. The Queen, 2011 DTC 1171 [at at 937], 2011 TCC 220

After finding that the taxpayer was entitled under s. 126(2) to a foreign tax credit in respect of its share of US corporate income tax paid by a ...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 126 - Subsection 126(2) | 350 | |

| Tax Topics - Statutory Interpretation - Consistency | 350 |

Bilous v. The Queen, 2011 DTC 1126 [at at 710], 2011 TCC 154

The individual taxpayer was the principal shareholder of the corporate taxpayer, a canola farm supplier with annual sales in the tens of millions....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 67 | 130 |

Bourget v. The Queen, 2011 DTC 1032 [at at 143], 2010 TCC 642 (Informal Procedure)

The taxpayer could not deduct a payment made to the Receiver General in satisfaction of his director's liability for source deductions under s....

Doiron v. The Queen, 2010 DTC 1348 [at at 4325], 2010 TCC 519, aff'd 2012 DTC 5105 [at 7092], 2012 FCA 126

The taxpayer, a lawyer, received a four-year sentence and was suspended from practising law as a result of his conviction for obstruction of...

Labow v. The Queen, 2010 TCC 408, 2010 DTC 1282 [at at 3956], aff'd 2012 DTC 5001 [at 6501], 2011 FCA 305

The taxpayers disguised a tax deferral scheme as a health plan for their employee wives. Bowie J. found that the plans had not been entered into...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4) - Paragraph 152(4)(a) - Subparagraph 152(4)(a)(i) | taxpayers appreciated the spurious factual underpinnings | 109 |

Les Entreprises Réjean Goyette inc. v. The Queen, 2009 DTC 1880, 2009 TCC 351

Management fees paid by the taxpayer to an affiliated company which had non-capital losses were non-deductible by it given that the only evidence...

Jolly Farmer Products Inc. v. The Queen, 2008 DTC 4396, 2008 TCC 409

In finding that the taxpayer was entitled to deduct capital cost allowance in respect of houses situated close to the taxpayer's greenhouse...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 1102 - Subsection 1102(1) - Paragraph 1102(1)(c) | 119 |

Mensah v. The Queen, 2008 DTC 4358, 2008 TCC 378

Bowman C.J. noted (at para. 35) that amounts that an employee may have stolen from the till of a delicatessen business would have given rise to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4) - Paragraph 152(4)(a) - Subparagraph 152(4)(a)(i) | no copy of return - no evidence | 56 |

Anjaria v. The Queen, 2008 DTC 2306, 2007 TCC 746 (Informal Procedure)

V.A. Miller J. stated (at para. 6):

First of all, the forfeiture of the proceeds of crime was not an expense or outlay incurred by the Appellant. ...

ZR v. The Queen, 2007 DTC 1577, 2007 TCC 598

The taxpayer was permitted to deduct as a business loss amounts paid by her in settlement of claims brought by a franchisor against her bankrupt...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Damages | focus on origin of claim | 147 |

Falkener v. The Queen, 2007 DTC 1470, 2007 TCC 514 (Informal Procedure)

The taxpayer was able to deduct costs of maintaining a dog (who helped protect llamas at his farm from danger) and cats (who were useful for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 31 - Subsection 31(1) | 76 |

Ellis v. The Queen, 2007 DTC 996, 2007 TCC 289, aff'd 2008 DTC 6230, 2008 FCA 92

A fee paid by the taxpayer to Ernst & Young LLP for advice in connection with strategizing as to how to monetize his shares through a forward...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Shares | 68 |

Renaud c. La Reine, 2006 DTC 3104, 2006 TCC 354

The taxpayer, who had made a proposal to creditors, was permitted to deduct trustee's fees incurred by him in making the proposal as the proposal...

Wedge v. The Queen, 2005 DTC 1213, 2005 TCC 480

A compensation payment made by the taxpayer to the taxpayer's shareholder, his wife and children, who were employees of the taxpayer, in respect...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Retiring Allowance | 42 |

Welton v. The Queen, 2005 DTC 869, 2005 TCC 359

A "management fee" paid by the taxpayer, a self-employed real estate agent, to her husband was non-deductible. There was no documentary evidence...

O'Flynn v. The Queen, 2005 DTC 556, 2005 TCC 230 (Informal Procedure)

The taxpayers were able to establish that a dental plan was available to all employees of the corporate taxpayer notwithstanding that only members...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(1) - Paragraph 6(1)(a) | 63 |

Shaver v. The Queen, 2003 DTC 2112, 2004 TCC 10

Expenses incurred by the taxpayer in taking seven people including him, his wife, and some Amway distributors (only two of whom were sponsored by...

Bains v. The Queen, 2003 DTC 376, 2003 TCC 211

The taxpayer had deliberately permitted a business colleague to mislead an investor ("Bhandar") into thinking that the taxpayer and his colleague...

Costigane v. The Queen, 2003 DTC 254, 2003 TCC 67

The taxpayer, who was a dentist, entered into an arrangement with an off-shore company under which that company would pay him 95% of all invoices...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 67 | 72 |

Foresbec Inc. v. The Queen, 2002 DTC 1786 (TCC), aff'd 2003 DTC 5455, 2002 FCA 186

At the time of the sale of a control block of the taxpayer, it and the purchasing shareholder "granted" to the vendor a consulting contract for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Sham | documents did not reflect legal reality | 58 |

| Tax Topics - General Concepts - Tax Avoidance | documents did not reflect legal reality | 58 |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | 97 |

International Colin Energy Corp. v. The Queen, 2002 DTC 2185, 2002 CanLII 47015 (TCC)

The taxpayer paid a fee to a financial advisor, calculated as 0.7% of the market value of its equity and of the amount of its long-term debt net...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Shareholder Assistance | advisor fees incurred to maximize shareholder value did not create a capital structure, and were deductible | 141 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | 183 | |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(e) | 183 |

Chamberlain v. The Queen, 2002 DTC 2050, 2003 TCC 307 (Informal Procedure)

The taxpayer's estranged wife obtained a court order to have the taxpayer jailed and, without authorization, took control of the taxpayer's...

Fredette v. The Queen, 2001 DTC 621 (TCC)

A partnership that was owned by the taxpayer and trusts for his children owned (through a second partnership that was owned by the first...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Ownership | 99 | |

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(4) | s. 245(4) did not apply to abuse of a Regulation - and not abusive to borrow at partner/shareholder level | 402 |

Matt Harris & Son Ltd. v. The Queen, 2001 DTC 28 (TCC) (Informal Procedure)

The taxpayer, the operator of a wood contracting and construction business, was able to deduct the amount of racing expenses incurred by it (less...

Quantetics Corporation v. The Queen, 2000 DTC 2177 (TCC)

A $1.4 million bonus declared by the company and never paid by it was found to have been made pursuant to a legal obligation, with the result that...

Coté v. The Queen, 99 DTC 5215 (FCTD)

A research program supervised by the taxpayer, who was associated with a Montreal hospital, was found to be a business in itself that was intended...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Legal and other Professional Fees | 71 | |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Legal and other Professional Fees | incurred when grants terminated | 71 |

Gagnon v. R., 99 DTC 845, [1999] 4 CTC 2426 (TCC)

Bowman T.C.J. stated (at p. 848):

It was argued at some length that the income earned and expected to be earned by the appellants was income from...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | 38 | |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(m) | software receipt amortized | 39 |

| Tax Topics - Income Tax Act - Section 67 | 70 |

Splend'or Industries Ltd. v. The Queen, 99 DTC 560 (TCC)

The taxpayer was unable to deduct the cost of replacing the roof of premises that were rented to it because such repair was the responsibility of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Improvements v. Repairs or Running Expense | 32 |

SPG International Ltée v. R., [1998] 3 CTC 2046, 98 DTC 1706 (TCC)

The taxpayer, which was a Canadian manufacturer of tool boxes and metal lockers, established an American marketing subsidiary and decided that,...

Robitaille v. The Queen, 97 DTC 346 (TCC)

Lamarre T.C.J. accepted the evidence of the taxpayer (a criminal lawyer) that he used his automobile 80% for business purposes (namely, visiting...

C.I.R. (Hong Kong) v. Cosmotron Manufacturing Co. Ltd., [1997] B.T.C. 465 (P.C.)

After the taxpayer closed its only factory and ceased its business, it made redundancy payments to laid-off employees pursuant to a statutory...

Vodafone Cellular Ltd. v. Shaw, [1997] BTC 247 (C.A.)

The taxpayer, which provided management services to its two subsidiaries which, in turn, ran a cellular phone system and sold cellular telephones,...

Port Colbourne Poultry Ltd. v. R., 97 DTC 237, [1997] 2 CTC 2480 (TCC)

Rowe D.J. found that a fine that the taxpayer agreed to pay as a result in respect of a decision by one of its unsupervised employees to flush...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Public Policy | 63 |

Sunys Petroleum Inc. v. The Queen, 96 DTC 1759, [1996] 3 CTC 2931 (TCC)

Penalties payable by the taxpayer (which operated gasoline stations) as a result of its failure to remit federal sales and excise taxes on some of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Public Policy | 159 |

Ogden Funeral Homes Ltd. v. The Queen, 94 DTC 1405, [1994] 1 CTC 2564 (TCC)

An indirect shareholder of the taxpayer requested his son, the general manager of the taxpayer, to return from Australia to Canada five days prior...

Grunbaum v. The Queen, 94 DTC 1384, [1994] 1 CTC 2687 (TCC)

Expenses incurred by the corporate taxpayer as a result of inviting business guests to a wedding reception held in honour of the daughter of a...

Barclays Mercantile Industrial Finance Ltd. v. Melluish, [1990] BTC 209 (Ch. D.)

In rejecting a finding of special commissioners that agreements for the licensing or other distribution of a film had not been entered into by a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 245 - Subsection 245(3) | 240 | |

| Tax Topics - Income Tax Act - Section 83 - Subsection 83(2.1) | main purpose was to make a profit, not take deduction | 264 |

| Tax Topics - Income Tax Regulations - Regulation 1100 - Subsection 1100(17) | no "lease" where failure to provide exclusive possession | 75 |

RTZ Oil and Gas Ltd. v. Elliss, [1987] BTC 359 (Ch. D.)

A consortium of oil companies including the taxpayer installed a manifold, loading lines and buoy over an off-shore oil field under a license that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Start-Up and Close-Down Expenditures | 176 |

Harrowston Corporation v. The Queen, 93 DTC 995, [1993] 2 CTC 2247 (TCC), aff'd 96 DTC 6544 (FCA)

A debt to the taxpayer from a non-resident corporation, which arose because of the taxpayer's inadvertent failure to withhold from interest...

Ginn v. MNR, 92 DTC 2233, [1992] 2 CTC 2579 (TCC)

The taxpayer was unsuccessful in his submission that the sum of $159,347 which he was ordered by the Supreme Court of British Columbia to pay as...

United Color and Chemicals Ltd. v. MNR, 92 DTC 1259, [1992] 1 CTC 2321 (TCC)

Kickback payments made by the taxpayer to purchasing agents employed by its customers were made for the purpose of generating sales and therefore...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Evidence | 50 |

ELB Productions Ltd. v. MNR, 91 DTC 1466, [1991] 2 CTC 2661 (TCC)

Before finding that an expenditure by the taxpayer was non-deductible on other grounds, Bowman J. stated (p. 1468):

Risky enterprises sometimes...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Start-Up and Liquidation Costs | 110 |

Cassidy's Ltd. v. MNR, 89 DTC 686 (TCC)

Losses suffered by a corporation, resulting from a senior vice-president fraudulently having cheques issued to him and charged to cost of goods,...

Heather v. P-E Consulting Group Ltd. (1972), 48 T.C. 293 (CA)

A management consulting company provided money on an annual basis to a trust fund which purchased the company's own shares and shares of a holding...

Horton Steel Works Ltd. v. MNR, 72 DTC 1123, [1972] CTC 2147 (T.R.B.)

The taxpayer was reassessed for unpaid federal sales taxes plus a penalty of 8% per annum. In finding that the penalty was non-deductible, Frost...

Harrods (Buenos Aires) Ltd. v. Taylor-Gooby (1964), 41 T.C. 450 (CA)

The taxpayer was resident in the United Kingdom but carried on the business of a large retail store in Buenos Aires. The taxpayer was liable in...

Morgan v. Tate & Lyle Ltd., [1955] A.C. 21 (H.L.)

Before finding that the taxpayer was permitted to deduct expenses which it incurred in opposing a nationalization of its business that would have...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Legal and other Professional Fees | 147 |

Canadian Fruit Distributors Ltd. v. MNR, 54 DTC 1145, [1954] CTC 284 (Ex. Ct.)

The taxpayer, which was the subsidiary of a non-profit fruit growers' non-share corporation, and whose business involved the marketing of fruit...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 111 - Subsection 111(5) - Paragraph 111(5)(a) | sale of fruit and vegetables for third parties and parent was same business | 35 |

| Tax Topics - Income Tax Act - Section 9 - Nature of Income | income reduced to nil by obligation to pay | 151 |

James Snook & Co., Ltd. v. Blasdale (1952), 33 T.C. 244 (CA)

The agreement for the sale of the shares in the capital of the taxpayer provided that the purchaser would cause the taxpayer to pay compensation...

Newsom v. Robertson (1952), 33 T.C. 452 (CA)

A barrister had chambers in London where he carried on his practice but resided at Whipsnade where he maintained a library and worked on...

Fairrie v. Hall (1947), 28 T.C. 200 (K.B.D.)

Damages which a sugar broker paid as a result of maliciously libelling a business rival were non-deductible notwithstanding that successully...

Bassett Enterprises, Ltd. v. Petty (1938), 21 T.C. 730 (K.B.D.)

The purchaser of the shares of a corporation undertook as part of the arrangement that the acquired corporation would pay for the cancellation of...

British Sugar Manufacturers, Ltd. v. Harris (1937), 21 TC 528 (C.A.)

The taxpayer agreed to pay 20% of its net profits to other corporations in consideration for their provision of managerial services and advice on...

Tata Hydro-Electric Agencies, Bombay v. Income Tax Commissioner, [1937] A.C. 685 (P.C.)

In acquiring the business of managing hydro-electric companies from a predecessor corporation, the taxpayer assumed the obligation to pay a...

The Herald and Weekly Times Ltd. v. Federal Commissioner of Taxation (1932), 2 A.T.D. 169 (H.C. of A.)

In finding that damages paid by an Australian newspaper for libel actions were deductible by it, the Court stated (p. 171):

None of the libels or...

B.W. Noble, Ltd. v. Mitchell (1927), 11 TC 372 (CA)

Although the taxpayer, which was an insurance and reinsurance broker, had cause to dismiss one of its directors, and to require him to transfer...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Contract or Option Cancellation | lump sum (payable in instalments) to terminate a director did not secure an enduring advantage | 137 |

British Insulated and Halsby Cables, Ltd. v. Atherton, [1926] A.C. 205 (HL)

Before going on to find that a substantial lump sum contribution by the taxpayer to an employee pension plan was a non-deductible expenditure,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Improvements v. Repairs or Running Expense | pension fund settlement was one-time expenditure for enduring benefit | 174 |

C.I.R. v. Alexander Von Glehn & Co. Ltd. (1920), 12 T.C. 233 (CA)

The taxpayer was unable to deduct penalties which it agreed to pay to the Attorney-General as a result of being unable to establish that goods...

Administrative Policy

12 June 2025 External T.I. 2025-1051441E5 - Deductibility of BC Home Flipping Tax

The B.C. Residential Property (Short-Term Holding) Profit Tax Act (“RPPTA”) imposes the “BC Home Flipping Tax” where a residential...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(1) - Paragraph 40(1)(a) - Subparagraph 40(1)(a)(i) | BC Home Flipping Tax did not qualify as a disposition expense | 170 |

21 September 2023 External T.I. 2023-0984251E5 - Ransomware attacks and BEC scams

Regarding whether amounts related to ransomware attacks and business email compromise (“BEC”) scams, including ransom payments, payments to a...

13 April 2023 External T.I. 2017-0684341E5 F - Perte au titre d’un placement d’entreprise

Regarding when a mooted small business corporation, which had ceased its restaurant operations in 20X1, but sued the franchisor at the same time...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(1) - Paragraph 39(1)(c) | active business for SBC purposes can continue after regular business operations have ceased/ sale of debt for $1 to unrelated purchasers might be a non-arm’s length transaction | 318 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Small Business Corporation | a corporation may continue to qualify as an SBC well after it has in fact ceased to transact its business | 209 |

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | sale of debt for $1 in order to trigger a loss might be a NAL transaction | 150 |

13 August 2020 External T.I. 2019-0802891E5 F - Unclaimed RRSP Benefits

The estate of the deceased annuitant of an RRSP was fully settled without the executor (his surviving wife and the sole beneficiary) being aware...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 146 - Subsection 146(1) - Benefit - Paragraph (a) | benefit includible in deceased annuitant’s return was not subject to "benefit"-(a) exclusion because it was not reported | 312 |

| Tax Topics - Income Tax Act - Section 146 - Subsection 146(8) | s. 146(8) benefit paid to the taxpayer’s administrator was not includible in her income until the year she was identified and received the amount | 377 |

| Tax Topics - Income Tax Act - Section 146 - Subsection 146(4) - Paragraph 146(4)(c) | tax imposed on RRSP under s. 146(4)(c) where RRSP issuer unaware of annuitant’s death | 187 |

| Tax Topics - General Concepts - Payment & Receipt | constructive receipt of amount deducted on account of fees that were the recipient’s obligation | 280 |

| Tax Topics - Income Tax Act - Section 9 - Timing | receipt of income by an administrator was not income of the beneficial owner until the year she was identified | 350 |

26 June 2020 External T.I. 2017-0688121E5 F - Déductibilité des intérêts et pénalités imposées sur les taxes foncières

Can interest paid on property taxes be deducted pursuant to s. 9 in computing business income? CRA responded:

[I]nterest charged on an unpaid...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 67.6 | tardiness “penalty” added by municipality to unpaid property taxes came within s. 67.6 | 107 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Financing Expenditures | interest paid on property taxes incurred as a business expense is itself deductible | 36 |

S4-F14-C1 - Artists and Writers

Examples of deductible expenses of an artist such as specialized wardrobe, lessons and PD and filming and recording costs for performance (but not...

1 August 2019 Internal T.I. 2018-0781951I7 - Employee benefit plan and recharge agreement

Employees of a Canadian subsidiary participated in a performance share plan (“PSP”) under which the non-resident public parent (Parentco)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(3) - Paragraph 7(3)(b) | no s. 7(3)(b) prohibition where at employer’s option to settle PSPs in cash or in shares | 250 |

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(1) - Paragraph 7(1)(a) | s. 7 rules do not apply to shares purchased through a trust | 180 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Employee Benefit Plan | custodial PSP arrangement was an EBP | 190 |

| Tax Topics - Income Tax Act - Section 32.1 - Subsection 32.1(1) | payments made by Canco to parent for the value of parent shares distributed by parent-funded EBP to Canco employees were not deductible under s. 32.1 | 269 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(4) | request for deduction not to be allowed if based on case decision rather than error | 281 |

27 June 2018 External T.I. 2018-0742881E5 F - Royalties under Canada Petroleum Resources Act

Respecting whether royalties paid under the Canada Petroleum Resources Act ("CPRA") would be considered a tax on income or profit and, therefore,...

26 March 2015 Internal T.I. 2013-0503031I7 F - Existence d’une source de revenu

After finding that the taxpayer’s expenses were likely non-deductible as his activities likely were a hobby rather than a business, CRA went on...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 3 - Paragraph 3(a) - Business Source/Reasonable Expectation of Profit | individual’s sideline activity not a business so that revenues exempt | 100 |

AD-18-01: "Taxable Benefit for the Personal Use of an Aircraft" 17 March 2018

After noting the distinction between personal use of a corporate aircraft qua employee and qua shareholder, CRA stated:

Where the benefit was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(1) - Paragraph 6(1)(a) | 720 | |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | 428 |

4 March 2015 External T.I. 2014-0562151E5 F - Frais de psychothérapie dépense d'entreprise

In the course of a business of offering psychology services, a psychologist incurs psychotherapy fees in order to reduce such therapist's personal...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(28) | potential choice between claiming therapy expense and credit | 115 |

9 October 2015 APFF Roundtable Q. 10, 2015-0595671C6 F - Question 10 - Table Ronde APFF 2015

When CRA disallows part of the deduction by a corporation of the management fee charged to it by another (presumably affiliated) corporation...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Effective Date | price adjustment clause not required to reduce income for an excessive management fee | 101 |

24 March 2015 External T.I. 2012-0470991E5 F - Mutual fund trust

After noting that in McNeil, 2005 DTC 328, 2005 TCC 124 at para. 6, the Tax Court had indicated that a s. 39(4) election also determined the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 104 - Subsection 104(21) | flow-through to unitholder of capital gain designated by MFT | 183 |

| Tax Topics - Income Tax Act - Section 132 - Subsection 132(6) | day trading included in investment undertaking | 62 |

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(5) - Paragraph 39(5)(a) | election can be made by leveraged day-trading MFT | 183 |

| Tax Topics - Income Tax Act - Section 9 - Capital Gain vs. Profit - Shares | capital v. income character determined at trust level | 94 |

27 June 2014 External T.I. 2013-0500701E5 F - Déductibilité de certaines dépenses

In the course of a general discussion as to deductibility of expenses by a family corporation on redacted facts, CRA stated:

In determining the...

27 May 2014 Internal T.I. 2014-0521631I7 F - Déductibilité d'un alcoomètre

Can an employer deduct expenses related to the installation and monthly recalibration of an alcohol interlock in the vehicle of one of its...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(1) - Paragraph 6(1)(a) | full personal element if the expense would have otherwise been paid by the employee | 100 |

30 October 2013 External T.I. 2013-0500831E5 F - Frais de bureau à domicile

CRA indicated that where a corporation is using an office in its individual shareholder’s home, “for the shareholder to be able to deduct...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 8 - Subsection 8(13) | inapplicable where corporation uses its individual shareholder's office | 71 |

| Tax Topics - Income Tax Act - Section 45 - Subsection 45(1) - Paragraph 45(1)(c) | incidental rental use of home does not result in part disposition | 143 |

2015 Ruling 2013-0513411R3 F - Société de professionnels

Current structure. Mr. A, who carries on a professional practice and employs various individuals directly, holds Class E voting discretionary...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Related Companies | fees paid by professional practice to family management company | 123 |

20 November 2012 External T.I. 2012-0466891E5 F - Non-Cash Gifts and Non-Cash Awards

Are gifts and awards to employees deductible to the employer? CRA responded:

The Agency's policy is to allow an employer to give an unlimited...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(1) - Paragraph 6(1)(a) | $500 tax-free non-cash gift amount calculated including sales tax | 60 |

15 November 2012 Internal T.I. 2012-0459321I7 F - Biens locatifs - frais de déplacement

Can a taxpayer owning two adjacent rental duplexes generating property income deduct the travel expenses incurred to travel from the taxpayer’s...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(h) | notwithstanding the s. 18(1)(h) postamable limitation to business income, there is a circumscribed deduction for travel to and from single rental property | 206 |

18 September 2012 External T.I. 2012-0442581E5 F - Fiducie au profit d'un athlète amateur

A world-class amateur athlete (the “Athlete”) deposits qualifying performance income (as defined in s. 143.1(1)) to an athlete trust (the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 143.1 - Subsection 143.1(2) | amounts distributed from athlete trust were business income | 129 |

| Tax Topics - Income Tax Act - Section 3 - Paragraph 3(a) - Business Source/Reasonable Expectation of Profit | tests for source of business income for amateur athlete | 149 |

S2-F1-C1 - Health and Welfare Trusts

Employer contributions required

1.20 An employer is required to make contributions to a health and welfare trust to fund employee health and...

S4-F2-C1 - Deductibility of Fines and Penalties

1.12 ...[A] fine or penalty incurred in relation to a transaction that is outside the scope of a taxpayer's normal business activities should not...

Provincial income tax

1.24

Paragraph 18(1)(t) does not prohibit the deduction of provincial income tax. However, provincial income tax is not an expense made or...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(t) | 200 |

S3-F9-C1 - Lottery Winnings, Miscellaneous Receipts, and Income (and Losses) from Crime

Repayment of stolen property

1.30 Gains from theft or embezzlement as well as cash or property received as a result of extortion, blackmail,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(a) - Timing | timing of deduction for loss from theft or embezzlement | 132 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(p) - Subparagraph 20(1)(p)(i) | bad debt from fraudulent investment scheme | 85 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Business | 314 | |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Disposition | 170 | |

| Tax Topics - Income Tax Act - Section 3 | non-enumerated sources included/hobby receipts, windfalls and true gifts excluded | 1077 |

| Tax Topics - Income Tax Act - Section 40 - Subsection 40(2) - Paragraph 40(2)(f) | 306 | |

| Tax Topics - Income Tax Act - Section 5 - Subsection 5(1) | 220 | |

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(1) - Paragraph 6(1)(a) | voluntary payments | 88 |

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(3) - Paragraph 6(3)(c) | 142 |

26 February 2014 External T.I. 2013-0510921E5 F - Remboursement de frais médicaux à un employé

In providing a general response to the question as to whether in computing an employer could deduct, in computing its business income, amounts...

8 October 2013 External T.I. 2011-0428931E5 F - Assurance-invalidité

Facts

As a condition to making a loan to finance the purchase by a corporation of a building, a financial institution required that the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Exempt Receipts/Business | proceeds received as a result of business credit card insurance were not income | 336 |

5 June 2012 External T.I. 2012-0437831E5 - Professional Fees

After stating that "any legal or accounting fees...relating to the filing of a voluntary disclosure are not deductible by the taxpayer under...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 60 - Paragraph 60(o) | voluntary disclosure costs not covered | 41 |

5 October 2012 Roundtable, 2012-0451251C6 F - Excess of foreign tax withheld at source

Tax is systematically withheld on income from ADRs at above the maximum rates permitted by the conventions. In addition to finding that such...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 126 - Subsection 126(7) - Non-Business-Income Tax | foreign withholdings on American depositary receipts in excess of Treaty-limited rate does not qualify as an income tax | 113 |

21 March 2011 External T.I. 2011-0395011E5 - Deductibility of Ontario SAT

A particular Ontario tax on life insurance corporations ("SAT") is determined as a fixed percentage of the amount by which the corporation's...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(x) | 177 |

24 June 2010 External T.I. 2010-0358981E5 F - Déductibilité de dépistage de la XXXXXXXXXX

Can customers of a testing business deduct the cost of testing for bacteria in computing their income? CRA responded:

[I]it is not necessary to...

28 April 2010 External T.I. 2009-0347581E5 F - Frais de formation

When asked whether expenses for attending a convention, seminar, luncheon meeting or other meeting incurred by an individual in the course of...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(b) - Capital Expenditure v. Expense - Know-How and Training | distinction between training and convention expenses/ luncheon seminar fees on case law generally are professional deductions | 329 |

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(10) | convention expenses providing an enduring benefit may be deducted within the s. 20(10) limitations | 185 |

8 October 2010 Roundtable, 2010-0378521C6 F - Déduction des primes d'assurance frais généraux

In affirming its policy in IT-233 respecting the deductibility of premiums under an overhead expense insurance policy, CRA stated:

As stated in...

20 August 2009 Internal T.I. 2009-0326941I7 F - Intérêts, Taxe sur le capital, déductibilité

Is provincial capital tax, and interest thereon, deductible in computing income? After observing that “[p]rovincial income tax is not deductible...

10 April 2008 Internal T.I. 2008-0271801I7 F - Frais juridiques liés à amende ou pénalité

Regarding the deductibility of legal fees incurred in defending in court against various fines and penalties, other than those prescribed, the...

16 December 2008 Internal T.I. 2008-0300361I7 F - Déductibilité de l'impôt minimum sur les sociétés

In finding that the Ontario corporate minimum tax ("CMT") provided for in ss. 57.1 to 57.12 of the Corporations Tax Act was not deductible in...

6 November 2007 External T.I. 2007-0227241E5 F - Crédit de taxe sur le capital - moment

After noting that the Quebec capital tax credit was government assistance that reduced the capital cost of the related depreciable property at the...

14 June 2007 External T.I. 2006-0209341E5 F - Utilisation d'un bien d'une société de personnes

A partnership in whose farming business the partners are actively involved owns the residence of one of the partners, who does not pay rent, but...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 103 - Subsection 103(1) | personal use of property is a factor going to the reasonableness of the profit-sharing arrangements | 74 |

| Tax Topics - Income Tax Act - Section 96 - Subsection 96(2.2) - Paragraph 96(2.2)(d) | personal use of property could engage s. 96(2.2)(d) | 104 |

| Tax Topics - Income Tax Act - Section 246 - Subsection 246(1) | conferral-of-benefit provisions do not apply to a partner’s personal use of partnership property other than car | 71 |

17 February 2005 External T.I. 2004-0104731E5 - Disability Income Insurance

Premiums paid by a corporation on a policy providing monthly income benefits to a shareholder for loss of his or her self-employment income would...

16 February 2005 Internal T.I. 2004-0105401I7 F - Frais de publicité

A corporation placed advertisements in newspapers in the form of short statements criticizing a redacted matter, and also purchased copies of a...

27 October 2004 External T.I. 2004-0063061E5 F - Provision pour somme payable

Regarding a situation in which a mutual fund trust would covenant to pay a guaranteed rate of return to its beneficiaries, coupled with an...

3 August 2004 Internal T.I. 2004-0078781I7 F - Déduction de l'impôt sur la masse salariale

For a taxpayer referred to in s. 1159.2(e) of the Taxation Act (Quebec), the amount of tax imposed thereunder was 1% of the wages paid in the...

28 April 2004 Internal T.I. 2004-0066991I7 F - Paiement incitatif

In finding that premiums paid by self-employed individuals to acquire exempt life insurance policies on their life (or by a corporation to insure...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 12 - Subsection 12(1) - Paragraph 12(1)(x) | incentive payments received from broker to purchase an exempt life insurance policy were received “in the course of earning income from … property” (the policy) | 166 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Property | property “includes practically any type of economic interest” | 142 |

8 October 2004 APFF Roundtable Q. 11, 2004-0090791C6 F - Maladies graves et soins de longue durée

Regarding the deductibility of premiums paid by corporations for individual critical illness policies and individual long-term care policies...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(1) - Paragraph 6(1)(a) - Subparagraph 6(1)(a)(i) | sickness plan can comprise individual critical illness policies | 128 |

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(1) - Paragraph 6(1)(f) | periodic payments under long-term care insurance are not taxable | 167 |

13 February 2004 External T.I. 2003-0027361E5 F - Déductibilité des intérêts -TPS et TVQ

Is interest incurred as a result of an assessment of uncollected and unremitted GST and QST amounts, or collected but unremitted GST and QST...

30 January 2004 Internal T.I. 2003-0037191I7 F - Fabrication /sous-traitants/frais de gestion

Individuals performed services only for Cco but (for administrative ease) were paid by a sister of Cco (Bco), so that Bco was responsible for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5202 - Cost of Labour - Paragraph (a) | cost of labour included amounts paid to a sister company that paid the employees on behalf of the manufacturer | 205 |

| Tax Topics - Income Tax Act - Section 153 - Subsection 153(1) - Paragraph 153(1)(a) | s. 153(1) applicable to salaries paid as agent | 143 |

| Tax Topics - Income Tax Regulations - Regulation 5202 - Cost of Labour - Paragraph (b) - Subparagraph (b)(iii) | tasks performed by subcontractors were not normally performed by employees | 106 |

19 June 2003 Internal T.I. 2003-0021297 F - LOI SUR L'ACCISE PENALITES INTERETS

Regarding the deductibility of interest and penalties arising under the ITA and ETA, the Directorate indicated:

- Deductibility of the former was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(t) | GST/HST interest and penalties are deductible based on application of ordinary principles | 52 |

28 February 2002 Internal T.I. 2001-0097117 F - TPS/TVH SUR UN AVANTAGE IMPOSABLE

Where a corporation uses its employees to earn income from a business or property, can it deduct the GST/HST that it must pay pursuant to ETA s....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 9 - Timing | accrual-basis taxpayer may deduct GST on employee benefits on a cash basis | 160 |

8 May 2001 Internal T.I. 2001-0079857 - WORKERS' COMPENSATION PREMIUMS

Workers' compensation premiums paid by a self-employed Alberta individual would be deductible in computing his income given that compensation...

25 February 2004 External T.I. 2003-0042461E5 F - Invalidité d'un actionnaire/admin./employé

A corporation, which is the policyholder and beneficiary of an insurance policy protecting it against the disability of its...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 3 - Paragraph 3(a) | disability benefits received by corporation to fund continuing salary-equivalent payments to its chief employee are not income | 116 |

| Tax Topics - Income Tax Act - Section 6 - Subsection 6(1) - Paragraph 6(1)(a) | taxable continued payment of salary-equivalent payments to disabled employee, but no taxable benefit from employer’s previous payment of premiums on funding disability policy | 150 |

20 November 2003 Internal T.I. 2003-0036237 - DEDUCTIBILITY OF HST ASSESSMENT

GST penalties payable by the taxpayer would be deductible by it given that they were incurred in connection with a profit-making scheme and its...

26 January 2005 Internal T.I. 2004-0101351I7 F - Déduction pour frais juridiques - Alinéa 60o)

The shareholder of an insolvent corporation incurred legal fees in defending against an ARQ sales tax assessment made on the basis that he was...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 60 - Paragraph 60(b) | legal fees incurred in disputing sales tax assessments are not included | 60 |

30 November 2004 External T.I. 2004-0090181E5 F - Assurance maladie grave

A corporation purchases a critical illness insurance policy on the life of its sole shareholder and there is also, at an additional cost, a rider...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 39 - Subsection 39(1) - Paragraph 39(1)(a) - Subparagraph 39(1)(a)(iii) | no capital gain on receipt by corporation of benefit under a critical illness insurance policy or of refund of premiums | 174 |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | misallocation shareholder benefit could arise if corporation pays premiums for its critical illness policy and sole shareholder pays for rider entitling him to premium refunds | 285 |

| Tax Topics - Income Tax Act - Section 18 - Subsection 18(1) - Paragraph 18(1)(h) | premiums paid by corporation for critical illness policy of which it is beneficiary are non-deductible pursuant to s. 18(1)(h) | 320 |

2 March 2004 External T.I. 2003-0042631E5 F - Déductibilité de dépenses

Following the death of their father in 2002, three brothers inherited a condominium from their father who, however, had granted his common-law...

10 October 2003 Roundtable, 2003-0035385 F - POLICE D'ASSURANCE CONTRE MALADIE GRAVE

A CCPC is the policyholder of a critical illness policy respecting its sole shareholder where either the shareholder is the beneficiary of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | corporate payment of premiums on critical illness policy for its sole shareholder generated taxable benefit | 87 |

3 October 2003 External T.I. 2003-0004575 F - ASSURANCE-INVALIDITE

Regarding where a corporation is the policyholder and beneficiary of a disability insurance policy for an employee-shareholder, CCRA stated:

We...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 3 - Paragraph 3(a) | disability benefits received by corporation for disability policy on shareholder-employee are not income | 92 |

16 January 2003 Internal T.I. 2002-0177807 - GST PENALTIES&INTEREST DEDUCTIBILITY

Although whether penalties and interest assessed under the Excise Tax Act are deductible is a question of fact, they generally will be deductible....

18 December 2002 Internal T.I. 2002-0164817 F - HONORAIRES POUR SERVICES DE MANDATAIRE

A professional paid his management company for 115% of the costs it purportedly incurred in managing his professional practice. However, the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 67 | CCRA policy on cost-plus-15% management companies of a professional inapplicable where it is providing agency services | 194 |

10 May 2001 Internal T.I. 2001-0065827 F - FINES + PENALTIES - INTÉRETS ET PÉNALITÉS